Quick Answer

Build W-9 collection at scale as a control system, not a reminder process. Route payees into the correct tax lane first, collect a signed electronic Form W-9, run TIN and status checks, and then decide payout state with documented ownership. Keep exception categories explicit and require approval artifacts for any conditional release. The standard is simple: you should be able to reconstruct one payee record from onboarding through Form 1099 treatment without stitching data across disconnected tools.

Why W-9 Collection Gets Hard at Scale#

High-volume contractor payout programs can break on control gaps, not because they lack another tool. W-9 collection is easier to defend when you can show three things clearly: who was routed into the U.S. onboarding path, what tax data they submitted, and why payment was allowed or held.

The goal is not to build a heavy process for its own sake. It is to reduce downstream tax reporting risk, avoid preventable tax-handling problems, and keep onboarding fast enough that growth does not turn into a year-end cleanup project. In practice, that means treating tax-form collection as an operational control, not a document you chase after the first payout.

A useful checkpoint is simple. Before payout enablement, confirm the payee is in the right tax lane and that the submission record is complete enough to support follow-up if something later fails.

Scope matters as much as speed. This article covers U.S. contractor onboarding, where a payee is being handled as a U.S. person and routed into a U.S. tax-form path. Once that assumption becomes shaky, your process should stop treating it as a domestic case. If the facts point toward a non-U.S. lane, you are usually into adjacent handling such as FATCA context and local compliance review, not a forced U.S.-person form-collection step.

That boundary is worth calling out early because cross-border reporting has its own rules and evidence needs. The IRS says certain U.S. taxpayers holding financial assets outside the United States must report those assets to the IRS, generally using Form 8938 under FATCA. It also says Form 8938 must be attached to the taxpayer's annual tax return. The IRS says the aggregate value of those assets must exceed $50,000 to be reportable in general, while noting that some thresholds may be higher. It also provides a comparison resource to help determine whether Form 8938, FBAR, or both are required.

For operators, the recommendation is straightforward. Draw the line between your U.S. Form W-9 path and your non-U.S. review path early, and keep evidence of that decision. A common failure mode is letting onboarding, tax classification, and payout release sit in one queue with no clear checkpoint or owner. That may feel efficient for a week, but it can create missing records, late exception handling, and filing-season surprises that are hard to defend later.

Related: Payee Verification at Scale: How Platforms Validate Bank Accounts Before Sending Mass Payouts covers the bank-account verification side of contractor onboarding.

Define the minimum control system and scope#

Before you automate anything, lock down the minimum controls as internal policy. For W-9 collection at scale, treat tax-data intake, review, and payout release as connected controls rather than cleanup after first payout.

| Control domain | What it covers |

|---|---|

| Intake | who collects required tax data and certifications |

| Validation | who reviews data consistency and exceptions |

| Storage | where records are retained and which version is authoritative |

| Access | who can view or update tax data |

| Reporting and escalation | who decides whether exceptions affect payout or downstream Form 1099 handling |

Define routing boundaries early. Keep one documented path for payees your program treats as U.S.-person cases and a separate review path for cases your program routes to Form W-8 handling. The IRS excerpts in this section do not provide specific W-9/W-8 routing criteria or TIN-validation rules, so your policy should state who decides, what evidence is required, and when payout is held.

From there, define five control domains and assign a named owner for each:

- Intake: who collects required tax data and certifications

- Validation: who reviews data consistency and exceptions

- Storage: where records are retained and which version is authoritative

- Access: who can view or update tax data

- Reporting and escalation: who decides whether exceptions affect payout or downstream Form 1099 handling

The biggest scope mistake is applying U.S. logic to non-U.S. cohorts. Publication 515 (for use in 2026) covers withholding for nonresident aliens and foreign entities and includes a topic entry for Form 1099 reporting and backup withholding. The IRS also states IRIS is available beginning January 1, 2026, while some submissions must continue through FIRE until FIRE is retired (tax year 2026 / filing season 2027).

Set ownership and escalation before you automate#

Set named ownership first, then automate. For W-9 collection at scale, you need clear accountability for three decisions: onboarding completion, tax exception clearance for Form 1099 reporting, and payout release.

IRM 2.5.13 includes sections titled Roles and Responsibilities and Program Controls. Use that as a practical governance model: if no one is explicitly accountable for a decision, you do not have a reliable control.

| Decision area | Primary owner | Consulted | Payment effect |

|---|---|---|---|

| Vendor onboarding completion | Payments Ops | Compliance | Do not move to payable status when tax intake is incomplete |

| Tax information reporting exception review | Finance or Tax lead | Compliance, Legal (edge cases) | Keep open exceptions visible through reporting season |

| Payout approval for exceptions | Finance or designated approver | Payments Ops, Compliance | Release only after documented approval, or hold |

Define escalation triggers before launch so operators do not improvise. Common triggers are missing electronic signature, conflicting TIN data, and unresolved U.S.-status signals that may require a Form W-8 path. Treat these as internal stop conditions for tax/legal review before payment release, not as assumptions to clean up later.

Make escalation evidence mandatory: case notes, decision timestamp, approver identity, and a linked audit-trail artifact. Add a RACI-style handoff checkpoint between onboarding completion and Form 1099 prep so unresolved exceptions are explicitly accepted, owned, and traceable.

For a broader finance operations view, Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount covers how teams scale payment workflows without adding the same amount of manual work.

Decide when to block payouts and when to allow conditional pay#

Use one payout decision standard for U.S. payees: default to block when a Form W-9 is missing, unsigned, or materially inconsistent, and do not rely on reminders or manual follow-up alone.

Your three-state model is an internal control choice, not a universal legal rule. Publication 225 says its explanations reflect IRS interpretation and are not intended to replace the law or change its meaning, so treat this table as policy under tax and legal oversight.

| Payout state | Form W-9 status | TIN status | Risk classification | Required action |

|---|---|---|---|---|

block | Missing, unsigned, or materially inconsistent | Failed, conflicting, or not yet verified where policy requires | Elevated or unresolved | Stop payout, open exception, assign owner, collect corrected record before release |

conditional | Substantially complete with a defined open issue | Pending review or limited mismatch allowed by policy | Known, bounded, approved exception | Time-box release, handle backup withholding if policy requires it, obtain executive sign-off |

clear | Complete and accepted | Passed or otherwise resolved per policy | Standard | Enable payout and retain validation evidence with the payee record |

Keep the conditional lane narrow#

Treat conditional as an exception lane, not a pressure-release valve. Limit it to written policy cases, require a named approver and expiration, and define the next action to cure the record or reroute the case.

If a submitted record conflicts with what you already hold, route to review instead of one-off approval. Where conditional release is allowed, make sure backup withholding handling is in place before payout, and keep a complete evidence pack (submitted W-9 version, validation result, approver, timestamp, and exception rationale).

Align payout controls across existing gates#

Avoid split decisions across separate queues. If your platform already uses payout gates for other controls, align statuses so one owner-facing decision determines whether funds can move.

At final pre-release review, confirm accepted W-9 status, TIN validation status, and payout risk state together. If those fields sit in different tools, require a single approval artifact or status snapshot so a hold in one lane cannot be missed in another.

Design the intake and validation sequence for Form W-9#

Use a strict intake order if you want fewer downstream tax exceptions: collect the electronic Form W-9, capture the electronic signature on that version, then run TIN and U.S.-status checks before payout enablement. The IRS does not prescribe one exact onboarding sequence, so this order is an internal control choice designed to keep evidence and decisions defensible.

You are not only collecting a form. You are deciding whether a submitted record is complete enough to support payout release and later tax information reporting.

Put the signed record before validation#

Validate only after you have a signed submission artifact. Publication 1099 (2026) includes "Electronic submission of Forms W-9," which supports digital intake, but it does not define your internal step order.

In practice, prevent payees from reaching payout-ready status from typed profile fields alone. Capture the electronic Form W-9, bind the electronic signature to that version, store the timestamp, and then run validation and routing checks. If your record cannot reproduce the exact signed version later, your audit trail is weak.

Keep logs thin and the source record controlled#

Treat masking, role-based access, and encrypted retention as control design choices, not IRS-prescribed architecture in this context. IRS materials here support electronic submission and recipient-statement workflows, not a specific storage model.

Keep logs limited to what operators need to resolve cases. Show masked values and status fields broadly, and restrict unmasked records to the smaller group handling tax exceptions. Maintain one controlled source record so teams are not resolving conflicts across multiple exports.

Make retries idempotent and status checkpoints explicit#

Make retries idempotent so dropped sessions, duplicate calls, or timeouts do not create duplicate tax profiles or conflicting statuses. Reuse the same submission key unless a new signed W-9 version is intentionally created.

| Checkpoint | Required record |

|---|---|

| Submission received | signed electronic Form W-9 artifact stored, timestamped, and linked to the payee |

| Validation passed or failed | results attached to that specific submission version |

| Exception opened or closed | owner, reason, and resolution timestamp recorded against that same record |

| Handoff ready for tax information reporting | accepted record marked usable for Form 1099 preparation, with validation evidence retrievable for your filing channel, including IRIS if you use it |

Track explicit checkpoints:

- Submission received: signed electronic Form W-9 artifact stored, timestamped, and linked to the payee.

- Validation passed or failed: results attached to that specific submission version.

- Exception opened or closed: owner, reason, and resolution timestamp recorded against that same record.

- Handoff ready for tax information reporting: accepted record marked usable for Form 1099 preparation, with validation evidence retrievable for your filing channel, including IRIS if you use it.

The tradeoff is straightforward: tighter sequencing adds onboarding friction, but loose sequencing creates year-end ambiguity about which W-9, which validation result, and which payout decision actually governed the payee.

Related: Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

Handle the exception cases competitors usually skip#

Define exception states up front and tie each case to the exact signed Form W-9 version reviewed, or your queue becomes inconsistent and hard to trust.

| Exception state | Definition |

|---|---|

| Missing W-9 | No signed Form W-9 artifact is on file for a payee in your U.S.-person path. |

| Invalid TIN | The submitted TIN did not pass your validation step; keep that result attached to that submission version. |

| Conflicting legal name | The name on the tax submission conflicts with prior identity, contract, or existing payee data. |

| Stale certification | The certification no longer matches the currently payable profile or entity and should be re-collected under your policy. |

| U.S.-status mismatch (W-8 review needed) | Intake started as W-9, but the profile should be routed to Form W-8 review; freeze the W-9 path and reroute. |

- Missing W-9

No signed Form W-9 artifact is on file for a payee in your U.S.-person path.

- Invalid TIN

The submitted TIN did not pass your validation step; keep that result attached to that submission version.

- Conflicting legal name

The name on the tax submission conflicts with prior identity, contract, or existing payee data.

- Stale certification

The certification no longer matches the currently payable profile or entity and should be re-collected under your policy.

- U.S.-status mismatch (W-8 review needed)

Intake started as W-9, but the profile should be routed to Form W-8 review; freeze the W-9 path and reroute.

When profile data conflicts with prior identity records, escalate for enhanced review: use KYB for entity context and KYC for individual context as your internal risk control.

Set internal SLA and aging rules for open exceptions so unresolved cases automatically change queue priority and payout permissions instead of relying on manual follow-up.

Also validate your document authority before closure: draft IRS materials are marked DRAFT, NOT FOR FILING, can change before final release, and are subject to OMB approval before official release. Record which final document version was used, plus review date, reviewer, and the signed submission artifact.

Track repeat exception patterns by onboarding source. Faster closure helps operations, but recurrence by source is what shows whether your intake controls are actually improving.

Keep evidence audit-ready from onboarding through filing#

Your process is only audit-ready if you can trace one payee record from onboarding to payout to Form 1099 output without gaps. Treat evidence capture as part of each control, not as year-end cleanup.

Electronic Form W-9 collection has been presented as permissible since 2014, but permissibility is not the same as defensibility. In practice, you should be able to show what was submitted, what was reviewed, what decisions were made, and how that record flowed into payout and reporting.

| Control point | Evidence to retain | Audit check |

|---|---|---|

| W-9 submission | Signed submission artifact for the reviewed version, with timestamp and payee link | The accepted artifact is the one tied to the active payee record |

| TIN validation | Validation outcome linked to that same submission version | The status history is preserved across retries and updates |

| Role-based access | Access history for viewing or changing tax data | Access behavior aligns with your internal role model |

| Exception resolution | Decision log, change history, and approval record | Closure rationale and approver trail are clear and retrievable |

A common failure is broken linkage between systems: intake evidence in one tool, validation in another, approvals somewhere else. When that linkage breaks, teams struggle to prove that the approved tax record is the one that drove payout and Form 1099 treatment.

Use Publication 1075 as a security reference point for tax information handling, especially when reviewing storage, access, and evidence controls. Keep it as a pressure test for your design, not a checklist for controls you have not implemented.

Test evidence retrieval quarterly as an internal operating discipline so failures surface before filing season. For a practical cross-functional workflow lens, see Collection Agencies for Small Businesses: Use a Payment Assurance System First.

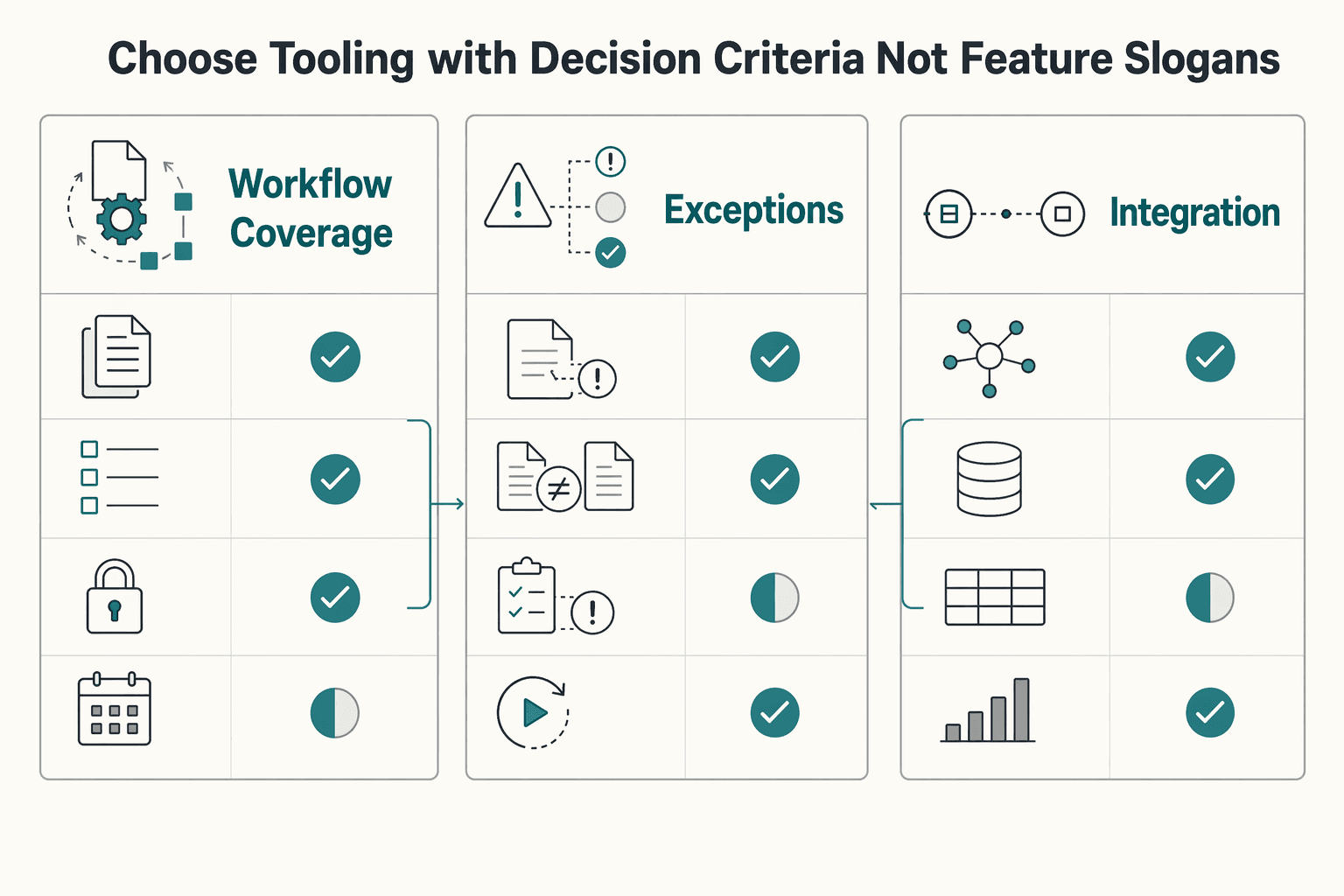

Choose tooling with decision criteria not feature slogans#

Choose the tool that supports your full Form W-9 control workflow, not just Form 1099 output. Businesses use W-9 data to complete Forms 1099-NEC and 1099-MISC, so a strong filing screen does not reduce risk if intake, validation, exceptions, and payout gating are disconnected.

Use a criteria matrix (for example, a Pugh-style scorecard) so options are judged against explicit requirements, not demo polish.

| Evaluation area | What to verify in the demo or sandbox | Red flag |

|---|---|---|

| W-9 workflow coverage | Can one payee record stay linked from W-9 submission through validation, approval, and 1099 reporting? | The flow starts at 1099 output and cannot show upstream control history |

| Audit trail and exception handling | Can you retrieve reviewer actions, timestamps, case status, and closure rationale for a single payee record? | Evidence is split across screens or cannot be exported as one record |

| Integrations and policy gating | Do API/webhook status changes feed payout controls and exception queues in your operating flow? | Tax status changes do not drive payout or exception decisions |

Ask vendors to walk through awkward scenarios, not just happy paths: mixed Form W-8/Form W-9 operations, resubmissions, and multi-entity reporting. Also treat unknowns as selection signals, especially implementation effort, edge-case handling, and reporting limits after go-live.

Related reading: Discounted Cash Flow DCF Valuation for Solo Professionals.

Conclusion#

The durable win here is not faster chasers or prettier intake screens. It is a control set you can defend when someone asks what you collected, what you checked, what you decided, and why money was or was not allowed to move.

That standard is stricter than operational convenience. The IRS 2025 General Instructions for Certain Information Returns are a useful reminder because the contents do not stop at filing mechanics. They explicitly call out Recipient Names and Taxpayer Identification Numbers (TINs), Backup Withholding, and penalties alongside the Form 1099 family. In plain terms, the risk surface starts before year-end filing, so your process should too.

The practical test is evidence. These excerpts do not prescribe a specific W-9 decision table or audit-trail design, but they do show that recipient/TIN handling, backup withholding, and penalties sit in the same compliance scope. If a control cannot clearly show what was submitted, what was checked, what exceptions were raised, and the resulting Form 1099 handling, treat that control as incomplete. A fast operation that cannot reconstruct one payee record without stitching together inboxes, screenshots, and memory is fragile, even if it feels efficient in normal weeks.

Your next move should be sequence, not shopping. First define your decision states for your program. Then define exception categories so materially different issues do not all collapse into a generic "needs review" bucket. After that, build the evidence checklist that proves each decision. Tooling matters, but it should conform to those choices rather than quietly making them for you.

One red flag is copying thresholds or assumptions from the wrong reporting context. The same 2025 IRS instructions note transition relief for Form 1099-K TPSO reporting at more than $2,500 in 2025 and more than $600 in calendar year 2026 and after. That is a good example of why your team should tie rules to the exact form and year in scope, not borrow a number and apply it across all onboarding or payout cases.

If you want a simple operator rule to leave with, use this one: when a payee file cannot show complete intake, a supportable check on tax data, and a documented resolution of any exception, do not call the process finished. Build the decision logic, evidence retrieval, and review path first. Then tune integrations, reminders, and filing tools around that foundation.

Frequently Asked Questions

What are the minimum controls required for W-9 collection at scale?

At minimum, you need a reliable way to collect Form W-9 (officially, the Request for Taxpayer Identification Number and Certification), retain the submitted record, and validate key tax data. You also need to track exceptions and connect finalized records to Form 1099 reporting when required.

When should we block payouts for missing or invalid Form W-9 data?

Treat payout blocking as a policy decision tied to risk, not as a one-size-fits-all legal rule. A common approach is to hold payouts when a U.S. payee has not submitted a complete Form W-9 or has unresolved material data issues, then document any limited exceptions.

What records should we retain to be audit-ready for IRS review?

Keep the submitted W-9 record, when it was received, and any validation or correction history tied to downstream Form 1099 reporting. A practical checkpoint is whether you can produce one clear payee record from collection through reporting status. Also remember that the completed W-9 is provided to the requester and is not filed with the IRS by the person completing it.

How is workflow automation different from basic e-file tooling?

Basic e-file tooling mainly helps with Form 1099 output. Automation covers earlier control points too: routing U.S. persons to W-9, routing other payees to Form W-8, collecting Form W-9 electronically, and handling validation or correction workflows before filing season.

How do we avoid year-end Form 1099 scrambles?

Collect W-series forms during onboarding, long before filing season arrives. Use real-time TIN matching so correction requests go back to the vendor while the relationship is still new, not in January when finance is already closing the year.

How should we handle contractors who may belong on Form W-8 instead of Form W-9?

Use the routing rule supported here: requesters collect W-9 forms from U.S. persons and W-8 forms from other payees. If the profile shows mixed signals, pause automated routing and send it to tax or legal review before enabling payouts.

What should we verify before selecting a W-9 automation vendor?

First, confirm the product supports electronic Form W-9 collection (described here as permitted since 2014). Then verify it can handle Form W-8 and Form W-9 routing and provide records you can use for Form 1099 preparation. A red flag is heavy reliance on handwritten submissions and manual re-entry, which can increase delays and errors.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

Airline Delay Compensation Payments for Customer Experience and Control

If you are evaluating an `airline compensation payments customer experience delays platform`, split the work into three lanes first: legally owed refunds, discretionary compensation, and outsourced claims recovery. Vendor pages often blur these together, but they lead to different policy choices, ledger treatment, and customer outcomes.

How Platforms Validate Bank Accounts Before Mass Payouts

For mass payouts, the real question is not whether to verify payees. It is how much verification you require before release, who can override it, and what evidence you can produce later. If you cannot show that evidence on demand, your release rule is weaker than it looks.