Quick Answer

For most small businesses, you should not start with a collection agency. Build a payment assurance system with clear contracts, A/P-ready invoices, pre-work payment setup, and a fixed internal escalation path. Bring in outside recovery only after internal follow-up is exhausted and the file, expected net recovery, and relationship risk justify outsourcing.

Don't Hire a Collection Agency. Deploy a Payment Assurance System.#

If you're searching for the best collection agencies for small business, the short answer is this: a collection agency is a later-stage tool, not your default operating model. Start with a payment assurance system that protects cash flow, keeps client relationships workable, and gives you a clear escalation path when invoices go past due.

Late payments do more than irritate you. They distort cash flow, hiring plans, and growth decisions. A system-first approach starts earlier, with a written collections policy that spells out what happens when an account becomes overdue, who contacts the client, and when the matter moves from client management to formal recovery.

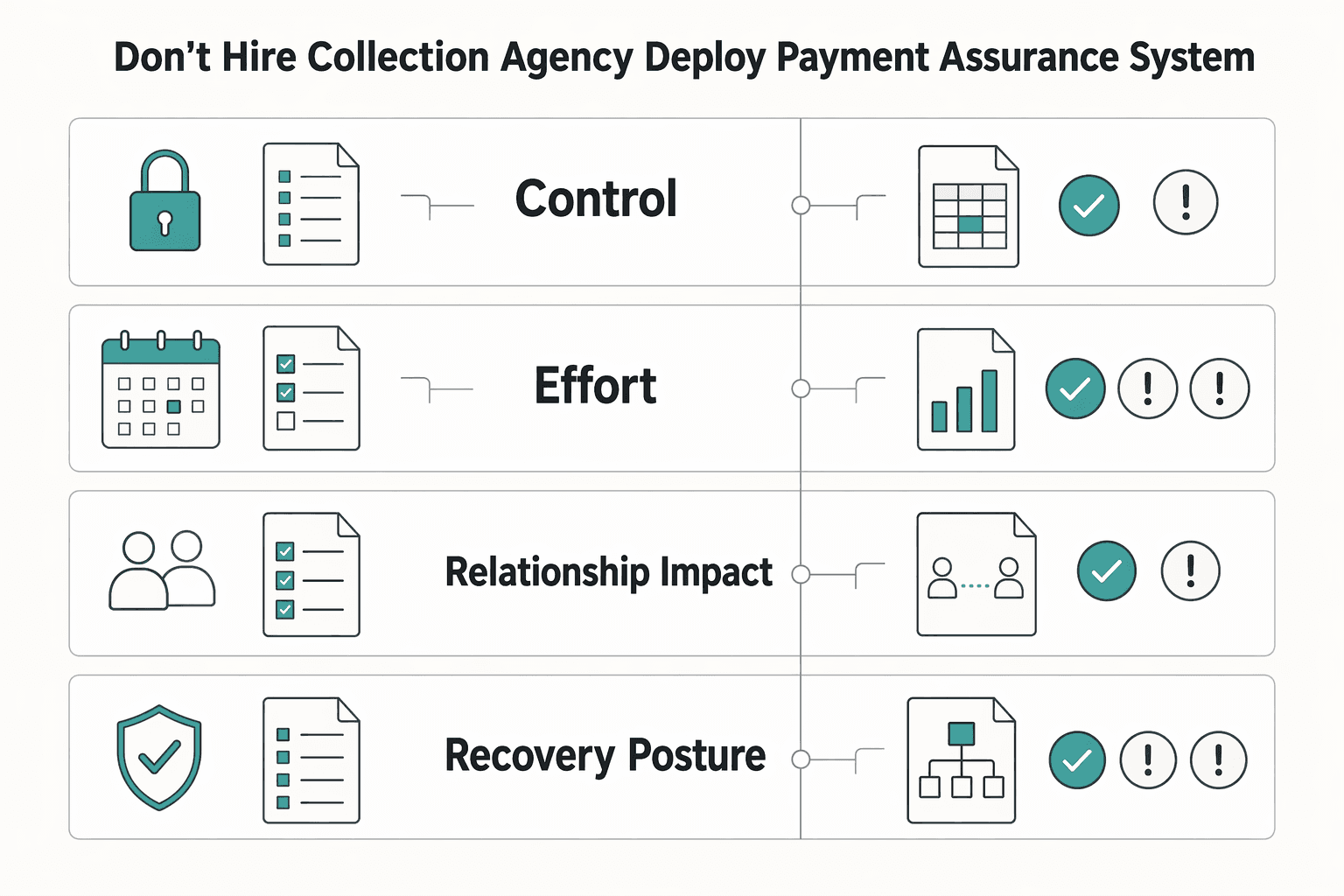

| Decision lens | Collections-first behavior | System-first behavior |

|---|---|---|

| Control | You react after receivables are already in arrears | You set policy, follow-up, and escalation rules before accounts become overdue |

| Effort | Time goes into chasing and vendor handoff after arrears | Time goes into consistent follow-up and documented checkpoints before external handoff |

| Relationship impact | Higher risk of aggressive contact damaging an existing customer relationship | More room for a firm but softer approach that can preserve or repair the relationship |

| Recovery posture | Third party enters when receivables are already in arrears | You escalate internally first and outsource only if needed |

The sequence is simple. Tighten prevention first, use internal escalation second, and consider outside help only after that. By the time you reach that third tier, the question is usually litigation readiness and whether external recovery support is warranted, not whether to send one more reminder.

One checkpoint to keep in mind: if you do hire a receivable management service later, ask for evidence of compliance controls, including contact-time controls. A good vendor should be able to show auditable communications and explain how it avoids inconvenient contact windows such as before 8 a.m. or after 9 p.m. That helps you verify you're buying disciplined debt collection, not avoidable risk. If you want a side-by-side on where small claims fits, see Collection Agency vs Small Claims for Freelancers.

Tier 1: Prevention - The System That Solves 90% of Your Payment Problems#

If you want fewer payment disputes later, tighten prevention now. Your contract, invoice, and submission process should line up exactly so there is less room for delay, confusion, or selective memory when payment is due.

1. Contract control#

Your contract should make two things clear: what was sold and how payment works if a dispute appears. In cross-border work, clarity on dispute handling and forum details becomes even more important.

A practical drafting discipline is the GSAM Part 552 sequence (effective 01/15/2026): identify clauses (552.103), incorporate them (552.102), then modify or complete them (552.104). It does not govern private client contracts, but it is a useful quality check before you sign.

Use that sequence for four clause areas:

| Clause area | Business risk reduced | Documentation to keep | Common failure mode |

|---|---|---|---|

| Scope control | Scope creep becomes a payment dispute | Statement of work, exclusions, revision limits, signed change approvals | Invoice references work the contract never described |

| Payment terms and late-fee policy | Ambiguity around due dates or consequences | Signed agreement, invoice issue date, delivery proof, reviewed fee language if used | Fee language copied from another jurisdiction without review |

| Dispute and fee-recovery language | Disputes become open-ended stalling | Notice method, response window, records of objections and resolutions | Informal complaint appears only after the invoice is overdue |

| Governing law and jurisdiction | Cross-border disputes start with forum conflict | Correct entity names, addresses, country/state, forum details | Template is silent, inconsistent, or names the wrong entity |

The biggest red flag is mismatch: if invoice line items, milestone names, or dates do not mirror the signed agreement, you create your own evidence problem.

2. A/P-ready invoices#

Build invoices for the team that processes payment, not just the person who hired you. Payment operations can involve business teams, finance, banks, vendors, and regulatory steps, so your invoice should leave less room for interpretation.

| Checkpoint | What to match/include | Context |

|---|---|---|

| Client identifiers | Legal entity name, billing address, vendor ID, project code, or PO number | If the client's finance process requires it |

| Line items | Mirror contract language so charges map to approved deliverables, milestones, or billing periods | Before sending the first live invoice |

| Your business details | Legal business name, address, contact email, and any tax or registration details the client requested | Before sending the first live invoice |

| Remittance fields | Invoice number, issue date, due date, currency, payment instructions, and billing contact | Make these fields obvious |

| Payment routes | Primary payment route and a fallback route | For international clients |

Use this checklist before sending the first live invoice:

- Match the client's legal entity name, billing address, vendor ID, project code, or PO number if their finance process requires it.

- Mirror contract language in line items so charges map to approved deliverables, milestones, or billing periods.

- Include your legal business name, address, contact email, and any tax or registration details the client requested.

- Make remittance fields obvious: invoice number, issue date, due date, currency, payment instructions, and billing contact.

- For international clients, set a primary payment route and a fallback route to avoid delays if one method fails.

A practical checkpoint is to send a sample invoice to A/P before the first bill and confirm it can enter their process as-is. A correct invoice sent through the wrong channel can still become a late payment.

3. Pre-work payment setup#

Before the first deliverable, run a brief payment setup check. Confirm who receives invoices, who approves them, where disputes go, and whether submission must happen by email, portal, or both.

Get four answers before work starts: payer contact, approval path, dispute route, and required submission channel. If you hear "just send it to me," verify whether finance also needs A/P routing or portal submission.

This makes everything that follows easier. When contract terms, invoice structure, and submission path align, Tier 2 stays focused on follow-up instead of reconstruction. You might also find this useful: The Best Project Management Tools for Small Agencies.

Tier 2: Internal Escalation - The Professional's Playbook#

When an invoice goes late, use a fixed escalation workflow instead of improvising. Run the same five parts every time: trigger, owner, channel, documentation, and outcome. That consistency helps you resolve real process issues faster and exposes avoidance early, before slippage from net-30 toward net-90 creates avoidable cash-flow pressure.

Stage sequence you can run every time#

Use this sequence on every overdue account.

| Stage | Trigger | Owner | Channel | Documentation | Outcome |

|---|---|---|---|---|---|

| Reminder stage | Due date passes without payment confirmation, or a promised pay date is missed | One receivables owner on your side | Email to finance or Accounts Payable | Sent invoice, proof of submission, payment clause, portal status screenshot (if relevant) | Confirmed payment date or a named blocker |

| Issue resolution stage | No response after your first interval, or finance reports a processing issue | Same receivables owner (not your project lead) | Email first, then phone if finance workflow requires it | Exact blocker such as missing PO, approval hold, disputed line item, or wrong entity name | Corrected paperwork, written payment date, or handoff to the correct owner |

| Formal notice stage | Silence, repeated broken promises, or partial payment without a written plan | Business owner or senior operator | Formal email, ideally with a PDF account summary | Aging summary, contact log, prior notices, contract reference, current balance, response deadline | Full payment, signed payment plan, or Tier 3 review for external recovery |

- Reminder stage

Trigger: due date passes without payment confirmation, or a promised pay date is missed. Owner: one receivables owner on your side. Channel: email to finance or Accounts Payable. Documentation: sent invoice, proof of submission, payment clause, portal status screenshot (if relevant). Outcome: confirmed payment date or a named blocker. Example wording: Subject: Invoice status Hi A/P team, this invoice still shows open on my side. Please confirm payment status or let me know if you need any item re-sent. Attached: invoice and payment details.

- Issue resolution stage

Trigger: no response after your first interval, or finance reports a processing issue. Owner: same receivables owner, not your project lead. Channel: email first, then phone if finance workflow requires it. Documentation: exact blocker such as missing PO, approval hold, disputed line item, or wrong entity name. Outcome: corrected paperwork, written payment date, or handoff to the correct owner. Example wording: Subject: Action needed on open invoice Hi A/P team, I want to resolve any blocker on this invoice under the agreement or SOW. If the hold relates to delivery approval, please point me to the approver. If it is an A/P issue, please confirm the missing item and the revised payment date.

- Formal notice stage

Trigger: silence, repeated broken promises, or partial payment without a written plan. Owner: business owner or senior operator. Channel: formal email, ideally with a PDF account summary. Documentation: aging summary, contact log, prior notices, contract reference, current balance, response deadline. Outcome: full payment, signed payment plan, or Tier 3 review for external recovery. Example wording: Subject: Formal notice for open invoice This is formal notice that the invoice remains unpaid. Please remit payment by the stated response deadline or reply with a signed payment plan. If we do not receive either, we will review external recovery options based on amount, fees, legal complexity, and relationship risk.

| Practice | Weak behavior | Strong behavior | Likely impact |

|---|---|---|---|

| Follow-up | Ad hoc check-ins | Stage-based sequence with owner and logged outcomes | Faster resolution, fewer dropped threads |

| Contact routing | Project contact handles payment chase | Receivables with A/P, delivery with project contact | Lower relationship risk, less confusion |

| Records | Inbox-only history | Central file with invoice, contract, submission proof, replies, promised dates | Better readiness for agency or legal escalation |

Keep delivery and receivables communication separate. Your project contact should own delivery questions; finance should own payment processing. If ownership is unclear, ask directly: Is this a delivery approval issue or an A/P processing issue, and who owns the next step?

Offer a payment plan only when the client acknowledges the balance and the issue appears temporary. Put the balance, installment dates, payment method, treatment of ongoing work, and signer names in writing, then add enforceability checks after legal verification. If the first installment is missed, communication stops, or terms are repeatedly reopened without payment, end the plan and move to Tier 3.

If you want a deeper dive, read The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Tier 3: Strategic Outsourcing - Making the CEO's Decision#

Use outsourcing only when the recovery case is strong enough to justify the added cost and risk. If expected net recovery is thin, your file is weak, or relationship downside is still material, third-party collection can make the outcome worse.

By this point, you have already run internal escalation. Now use a decision gate before agency outreach. Check four items: expected net recovery, documentation strength, jurisdiction complexity, and relationship or reputation downside. Current fee ranges and handoff thresholds must be verified from policy, contract, legal, source, or adviser records before use. A 15/30/60-day cadence is a solid internal checkpoint, but not a universal handoff rule.

| Path | When it fits | Why this is the right call | Evidence you should have first |

|---|---|---|---|

| Proceed now | The balance remains meaningful after verified fees, internal escalation is exhausted, and the relationship is already broken or nonessential | There is enough value and enough proof for efficient external recovery | Signed contract or SOW, invoice trail, proof of invoice submission, proof of delivery, contact log, formal notice record |

| Attempt one more internal step | The debtor is still responding, a process blocker may be fixable, or a payment plan is plausible because they acknowledge the balance | One controlled internal step may recover faster and preserve the account | Written acknowledgment of debt, named blocker (PO or approval hold), proposed payment date or draft payment plan |

| Do not pursue | Expected net recovery is poor, records are incomplete, or legal/reputation cost likely outweighs recovery | External escalation may consume time and still fail | Gap analysis showing missing terms, weak delivery proof, uncertain entity identity, or high downside if the dispute turns public |

If an agency would need to rebuild the story from your inbox, pause. Tighten the record first or stop. A common failure mode is outsourcing a file that still reads like a service dispute instead of a clean overdue receivable.

Vet the agency before they contact your client#

Treat rankings as lead sources, not answers. One review publisher explicitly discloses compensation from some listed companies, and a page labeled for 2026 shows a visible update date of Oct 17, 2024. Take that as a prompt to verify recency and fit yourself.

| Checkpoint | What to verify |

|---|---|

| B2B specialization | What share of their caseload is commercial accounts |

| Dispute intake process | How they handle delivery disputes, approval holds, or contract mismatch claims at intake |

| Cross-border fit | Coverage for the debtor's actual country and legal entity, not generic "international" language |

| Licensing and baseline qualifiers | "Licensed in 50 states" or "low minimum collection balance" as starting points to confirm directly and log with the verification date |

| Reporting visibility | Update frequency, format, and what they treat as a meaningful status change |

| Escalation authority | Who can approve settlement, legal referral, or closure |

- B2B specialization

Ask what share of their caseload is commercial accounts. A label like "Best for B2B Collections" is a signal, not proof.

- Dispute intake process

Ask how they handle delivery disputes, approval holds, or contract mismatch claims at intake.

- Cross-border fit

Verify coverage for the debtor's actual country and legal entity, not generic "international" language. If a legal point matters, do not rely only on FederalRegister.gov XML text; verify against an official edition or counsel.

- Licensing and baseline qualifiers

Listing signals like "licensed in 50 states" or "low minimum collection balance" are useful starting points; confirm directly and log the verification date.

- Reporting visibility

Confirm update frequency, format, and what they treat as a meaningful status change.

- Escalation authority

Confirm who can approve settlement, legal referral, or closure so those decisions are not made by default.

Match by claim profile, then prepare a clean handoff#

Shortlist by claim profile, not brand prestige. Complex commercial claims need strong document intake. Relationship-sensitive recovery needs a contact style you have reviewed. Cross-border files need claim-by-claim verification of jurisdiction coverage, debtor entity, and practical recovery path before you rank any provider.

Before handoff, prepare one clean packet:

- Contract set with signed agreement, SOW, amendments, and payment terms

- Invoice trail with invoice copies, due dates, and proof of submission

- Communication log with reminders, replies, promised dates, and misses

- Proof of delivery such as approvals, portal screenshots, accepted deliverables, or completion emails

- Internal escalation record showing the 15/30/60 cadence, formal notice, and any payment-plan attempt

If the debtor disputes the work, include that record directly. Omitting it usually weakens recovery.

If you like step-by-step vendor comparisons, see The Best HRIS Software for Small Businesses.

The Final Word: You Are the Asset. Protect Your Focus.#

The point of this framework is simple: build control before the invoice goes late, run the same internal escalation every time, and outsource only when the file is clean and the economics still work. You are most valuable when you are delivering work, not reconstructing receivables from a scattered inbox. Protect your focus by making payment assurance part of operations. ---

Frequently Asked Questions

When should you hand an account to a collection agency?

Use an agency only after your own escalation sequence is done and expected net recovery still makes sense. Confirm the current timing window from policy, contract, legal, source, or adviser records before using it, because no single day count is a verified standard for every claim.

What should be complete before you contact an agency?

Treat this as your final checklist: signed contract or SOW, invoice copies, proof the invoices were sent, proof the work was accepted or delivered, and a contact log showing reminders, replies, and any formal notice. If the debtor disputes quality, scope, or approvals, include that record up front so the agency can assess the file accurately.

How do you protect the client relationship while still pursuing payment?

Keep service conversations separate from money conversations for as long as you can, and offer a payment plan if the debtor acknowledges the balance. If you do outsource, ask how the agency handles first contact and disputed accounts. Agencies described as using respectful treatment and clear communication are a better fit when reputation still matters.

How do you tell a commercial collector from a consumer-focused one?

If you're comparing agencies for a small business, look past rankings and ask whether the firm actually handles B2B claims. Consumer-side signals like FDCPA compliance, BBB ratings, and manageable CFPB complaint levels are useful trust indicators, but for commercial files you should also confirm how the agency handles disputes and how transparent its status reporting is.

What should you verify before selecting an agency?

Re-verify current status yourself because listings go stale. One review publisher explicitly discloses compensation from some listed companies, and a page labeled for 2026 shows a visible update date of Oct 17, 2024. Treat rankings as lead sources, not answers, and confirm B2B fit, dispute intake, cross-border coverage, reporting visibility, and escalation authority directly.

What should you expect after placement?

Expect structured status updates, not silence. Before placement, confirm update frequency, format, what the agency treats as a meaningful status change, and who can approve settlement, legal referral, or closure. That keeps visibility in your hands and reduces surprise decisions later.

Can you report an unpaid invoice to credit bureaus?

Treat this as a verification item, not a default tactic. Verify the actual reporting path for the debtor's actual entity and keep your documentation clean before you rely on it in any recovery plan. If a legal point matters, verify against an official source or counsel.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

A Freelancer's Guide to Collecting on a Judgment

Winning the case is only part of the job. Getting paid is a separate enforcement process, and [the court does not collect for you](https://selfhelp.courts.ca.gov/civil-lawsuit/judgment/how-collect). At this point, you are the judgment creditor and the other side is the judgment debtor. Your next decisions are about cash flow, time, and risk.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.