Quick Answer

Yes, discounted cash flow dcf valuation can work for solo professionals when you model owner-available cash, apply a rate that fits that cash-flow type, and pressure-test likely and downside outcomes before committing. In this framework, key anchors are Net Professional Income, a Personal Autonomy Rate rubric, and a walk-away floor for employment offers. The model is used to choose a clear next move based on risk-adjusted value rather than headline price alone.

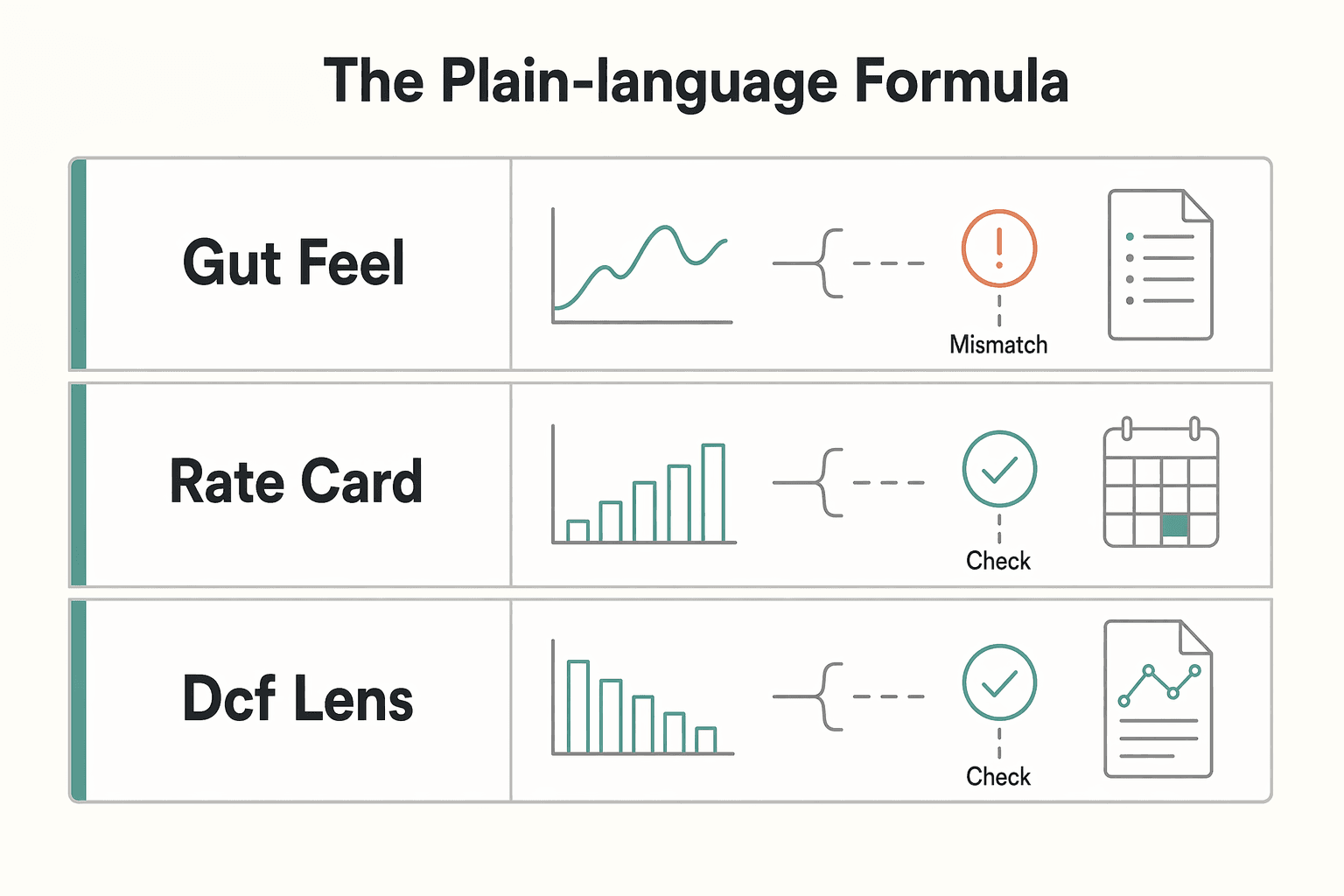

First, Forget Corporate Finance: What DCF Really Means for a Solo Professional#

When you compare client options, do not start with the headline fee. Start with which option gets you more cash sooner, with less risk. That is what discounted cash flow (DCF) means in practice.

Two offers can look similar on price but deliver very different value once you account for payment timing and uncertainty. Cash you receive now is worth more than the same amount later. Riskier future payments should be discounted at a higher rate than safer ones.

The plain-language formula#

DCF = sum(CF_t / (1 + r)^t)

Use it like this:

- CF: the cash flow you expect in each period

- r: the discount rate that reflects risk and time value of money

- t: the time period

- sum: add all discounted cash flows into one present-value estimate

This gives you an intrinsic-value view based on cash-generation ability, not surface pricing.

| Decision lens | What it helps you do | What it tends to miss |

|---|---|---|

| Gut-feel pricing | Make quick calls on fit | Timing effects, risk differences, and hidden downside |

| Rate-card math | Keep pricing structure consistent | Payment schedule risk and uneven cash-flow timing |

| DCF lens | Compare different timing and risk on one present-value basis | Output quality drops fast if assumptions are weak |

Use DCF as a decision tool, not a standalone truth. It can sharpen judgment, but it is highly sensitive to assumptions. Pair it with other checks, including your pricing and operating reality. The next step is to define what you mean by cash flow before you choose a discount-rate method.

If you want a deeper dive, read Hiring Your First Subcontractor: Legal and Financial Steps.

How to Define "Cash Flow" When You Are the Business#

Pick one cash-flow definition before you run any DCF math, then keep it unchanged across scenarios. DCF estimates present value from projected future cash flows. If your inputs mix different meanings of "cash," the output can look precise while still point you in the wrong direction.

A workable structure is to define your DCF input cash flow with explicit lines for expected operating inflows, recurring operating outflows, and tax treatment.

Treat this as a model rule, not a universal accounting standard. Keep each line explicit:

Inflows: cash you reasonably expect from real work, not unverified upsideOutflows: recurring costs required to win and deliver that workTax treatment: a separate line, checked against your recent reality

Set one owner-pay rule and apply it consistently so you do not double count or omit it across scenarios.

Use one working metric#

"Net Professional Income" can be your label for DCF inputs, as long as you define it once and reuse it consistently.

| Metric | What it captures | Best use in your model |

|---|---|---|

| Accounting profit | Your accounting-basis result for the period | Trend check, not your primary DCF input when timing matters |

| Cash received | Cash that hit your account in the period | Helps you see collection timing risk |

| Net Professional Income | Your documented internal model definition (not a standard term) | Primary DCF input if kept consistent |

Run a quick verification pass before you forecast. Reconcile one recent month or quarter to actual bank activity and tax payments. If model "available cash" and your lived cash reality diverge, fix the definition first.

Build the forecast in passes#

Build the forecast in layers so you can see exactly what changes value:

| Pass | What to include | Note |

|---|---|---|

| Base case | Current work pattern, recurring costs, and tax treatment assumptions | Start with a base case |

| Major assumption groups | Add one at a time | For example, renewals; add a short support note for each |

| Pricing changes | Layer in pricing changes as a separate pass | When relevant |

| Utilization or capacity gaps | Show explicitly | When relevant |

| Payment-timing assumptions | Show explicitly | Later cash has lower present value than earlier cash |

Work through those passes in order so you can see which assumption actually moves value, and by how much.

This future-focused method is useful even when history is thin, but it is sensitive to assumptions. Keep the same cash-flow definition, tax treatment, and timing logic in your base, upside, and downside cases so the comparison stays valid.

Related: How to Perform a Business Valuation for a Small Agency.

The "Personal Autonomy Rate": A Discount Rate That Values Your Freedom#

Use a discount rate that matches the cash flow you are discounting. If your model discounts owner-available cash after recurring costs and tax provision, you are usually in an equity-style view. In that case, a cost-of-equity style required return is usually a better fit than defaulting to WACC.

WACC is not automatically wrong. It is a blended financing cost for firm cash flows. But if your projections are cash flows to equity, pairing them with a firm-level rate creates a mismatch that can materially distort value. Fix that alignment before you settle on a percentage.

Why this is not just WACC with a new label#

The rule is simple: discount equity cash flows with a cost-of-equity style rate, and firm cash flows with a cost-of-capital style rate. Your "Personal Autonomy Rate" is a practical label for the return you require on your own equity-like cash flows.

Use WACC when you are truly modeling firm cash flows before debt claims. If debt is meaningful or likely to change, note that in your model and consider a firm-value approach or separate financing treatment such as APV.

Score the three inputs the same way every time#

A repeatable rubric matters more than false precision. Use Low / Medium / High for each input, plus a one-line note explaining why. Start with a current benchmark from Federal Reserve H.15, then layer in your personal adjustments.

| Input | Low | Medium | High |

|---|---|---|---|

| Risk premium | Diversified clients, stable renewals, cleaner collections | Some concentration or periodic timing risk | Heavy concentration, weak payment terms, repeated delays |

| Opportunity cost | Employed alternative is clearly weaker after full compensation mapping | Alternatives are comparable after benefits and self-funded replacements | Employed alternative is materially stronger once total compensation is mapped |

| Growth uncertainty | Renewals and demand are already visible | Some growth depends on assumptions still in progress | Forecast depends on unproven pricing, new niche traction, or one major win landing on time |

- Risk premium

Score cash-flow reliability, not optimism. Low: diversified clients, stable renewals, cleaner collections. Medium: some concentration or periodic timing risk. High: heavy concentration, weak payment terms, repeated delays. Calibration note: if one missed project breaks the plan, this should not be low.

- Opportunity cost

Score the quality of the realistic employed alternative in full, not salary alone. Low: employed alternative is clearly weaker after full compensation mapping. Medium: alternatives are comparable after benefits and self-funded replacements. High: employed alternative is materially stronger once total compensation is mapped.

- Growth uncertainty

Score how much of forecast value depends on assumptions not yet visible in your pipeline. Low: renewals and demand are already visible. Medium: some growth depends on assumptions still in progress. High: forecast depends on unproven pricing, new niche traction, or one major win landing on time.

| Component | Employed baseline, what to capture | Independent baseline, what to map | Evidence to use |

|---|---|---|---|

| Cash compensation | Salary, bonus, commission | Owner pay target the business must support | Actual offers or market comps you would realistically accept |

| Employer-funded benefits | Health coverage, retirement contributions, paid leave, other benefits | Self-funded replacements or explicit out-of-pocket gaps | BLS December 2025 private-industry split: wages/salaries $32.36/hour and benefits $13.79/hour |

| Self-funded replacement costs | Often missed in salary-only comparisons | Health insurance, retirement funding, unpaid leave, and other out-of-pocket replacements | Your invoices and plan records, including health insurance amounts you actually pay |

This split keeps you from understating opportunity cost. It also separates cash pay from benefit value instead of blending both into one vague number.

Calibrate before you use it in your model#

Before you apply the rate in your DCF, run a short sanity check:

- Pull a fresh H.15 snapshot and record the release date in your model.

- Check your final rate against recent revenue and collection volatility; avoid scoring all three inputs high unless your data supports it.

- Check your rate against forecast confidence. Signed or near-signed work can support a lighter uncertainty adjustment than an assumption-heavy pipeline.

- Re-run valuation one band lower and one band higher. If value swings are extreme, tighten your forecast and payment-risk assumptions before treating the midpoint as final.

The goal is a rate you can defend and reuse. Match cash-flow and rate logic, use a dated benchmark anchor, and keep documented scoring notes.

We covered this in detail in How to Build a Freelance Financial Model That Protects Cash Flow.

The "Acquisition" Model: How to Calculate Your Walk-Away Number#

Treat a full-time offer as a potential buyout of your future owner cash flows, not just a salary choice. In this framework, your walk-away number can be the present value of what you would give up, plus a separate autonomy premium for the control you would lose.

In DCF terms, you are comparing two values: keeping future owner cash flows or exchanging them for an employment package.

Run the offer through the same lens every time#

Map each offer component to the value it has to replace, then flag missing terms before you assign value to it.

| Offer component | Your valuation component | Verify before you count it | Gap if missing |

|---|---|---|---|

| Cash compensation | Owner pay target and current cash compensation from independent work | Base salary, pay frequency, review timing, probation terms | Treat as partial value only |

| Variable compensation | Variable portion of your forecast cash flows | Formula, triggers, caps, payout timing, discretion | Treat as uncertain value |

| Benefits replacement | Self-funded items you currently cover | Health coverage, retirement match, paid leave, out-of-pocket gaps | Add replacement cost to your floor |

| Equity terms | Future upside offered instead of cash | Vesting, purchase/strike terms if relevant, dilution risk, liquidity path | Do not price as guaranteed value |

| Autonomy premium | Non-cash value of independence you give up | Schedule expectations, remote policy, approval rights, IP assignment, moonlighting limits | Keep this premium explicit |

Use this checklist each time you evaluate an offer#

Start by freezing the comparison so you are not moving assumptions around to fit the offer.

- Freeze one forecast version.

Use a single set of revenue, income statement, and cash flow projections so your comparison stays consistent. If a key renewal or pipeline item is unresolved, mark that assumption risk.

- Calculate your present-value floor.

Discount your owner-available future cash flows to present value using one consistent discount-rate approach. Treat this output as a decision aid, not a precise number, because DCF is assumption-sensitive.

- Score autonomy separately.

Do not hide this inside the discount rate.

| Autonomy factor | Your score | Pre-set importance | Evidence note |

|---|---|---|---|

| Schedule control | Set before comparing offers | Set before comparing offers | Written expectations only |

| Location flexibility | Set before comparing offers | Set before comparing offers | Written policy only |

| Project selection | Set before comparing offers | Set before comparing offers | Approval/assignment terms |

| IP ownership | Set before comparing offers | Set before comparing offers | Offer/IP language |

- Build your negotiation evidence pack.

Use the written offer, benefits summary, equity summary if any, remote or attendance policy, and IP or invention language. Do not rely on verbal assurances for high-impact terms.

Set decision outputs before the next call#

Set your decision outputs before you negotiate, not during the conversation.

| Output | Meaning | Constraint |

|---|---|---|

| Walk-away floor | Present-value floor plus autonomy premium | Adjusted only for verified offer terms |

| Target package | The package you would accept with confidence | Not just the minimum |

| Non-negotiable terms | Terms that can fail the deal | Even if headline pay looks strong |

Rule of thumb: move forward only if the verified package appears to clear your walk-away floor and meets your non-negotiables. Walk away if it does not.

You might also find this useful: How to Build a 3-Statement Financial Model.

Turning "Guesswork" into Strategy: Your What-If Scenario Planner#

Use this before you accept, price, or renegotiate an engagement. Test whether the cash flow still works once payment timing and risk show up.

That is the real job of DCF in independent work: not predicting one perfect outcome, but checking whether present value still holds when risk changes the timing or reliability of cash and may require a higher discount rate. Money received sooner is worth more than money received later.

Keep the standard high. Scenario quality depends on input quality. The math usually is not the weak point. Unsupported assumptions are. If an assumption is not backed by verifiable evidence or clear written terms, treat it as uncertain, not guaranteed cash.

| Assumption to test | What changes in cash flow | Early warning signal | Negotiation response |

|---|---|---|---|

| Payment timing | Cash arrives later, so present value can drop | Vague invoice cycle, unclear approver, long procurement steps | Shorter payment terms, upfront deposit, milestone billing |

| Scope control | Extra work can raise delivery cost without matching revenue | No change-order language, broad revision promises, undefined deliverables | Tight SOW, revision limits, paid change requests |

| Dispute risk | Cash receipts can be delayed, reduced, or held | Subjective acceptance terms, no sign-off process, verbal approvals only | Written acceptance criteria, named approver, defined dispute window |

| Termination risk | Expected future cash can stop earlier | Convenience termination with no fee or notice | Notice period and payment terms for completed work |

| Collection friction | Recovery can take more time and cost | Cross-team billing confusion, inconsistent billing contact, missing payment details | Confirm billing contact, invoice method, and late-fee language before start |

Run it in four passes:

- Build the base case. Start with revenue minus fixed and variable expenses using the contract as written.

- Stress the downside. Delay receipts, add unpaid effort where scope is weak, and reduce future cash where termination risk is real.

- Set your acceptance threshold. If the downside case misses your minimum acceptable value, do not rely on optimistic assumptions.

- Prepare fallback terms. Go into the next call with two or three contract changes tied directly to the risks you found, and make sure each assumption is defensible line by line.

This pairs well with our guide on How to Read a Cash Flow Statement.

Before you finalize your likely and downside scenarios, run the numbers through the payment fee comparison tool so your DCF inputs reflect real collection costs.

Your Business, Your Value, Your Terms#

Use your model to make the decision, not just to defend your rate. With a 12-month cash-flow forecast, discount-rate logic matched to that cash-flow risk, and a best, likely, and worst scenario range, you can place each opportunity into one of three outcomes: accept, renegotiate, or decline.

That is the practical job of DCF in a solo business. You are testing whether the work creates enough present value after timing risk and downside risk, not arguing from instinct. If the likely case shows a positive present-value spread and the downside still works on terms you can accept, proceed. If the deal only works in the best case, treat it as a negotiation warning.

Use your numbers to change the conversation#

You do not need to show a client your full model, but you should bring a short evidence pack built from your own analysis:

- your 12-month cash-flow projection for the engagement

- your discount-rate logic, including why that rate fits the cash-flow risk

- your scenario range, especially what breaks in the downside case

- the contract terms that move the deal from weak to acceptable

That shifts the conversation from "why is your rate this high?" to "what terms make this engagement viable?" It also prevents a common mistake. You can use valuation language and still ignore payment risk. A positive NPV can support an accept decision, but it does not prove payment reliability or scope control. Those outcomes still need clear contract terms and process discipline.

| Approach | Positioning | Evidence you bring | Contract terms you ask for |

|---|---|---|---|

| Before: defending your rate | "My fee is based on experience and market pricing." | Portfolio, past work, rough estimate | Standard scope and price discussion |

| After: pricing the likely case | "At this fee and timeline, the work clears my required return in the likely case." | 12-month cash-flow forecast, discount-rate note, likely-case present value | Milestone-linked payments, written scope, change-approval rules |

| After: protecting the downside | "If payment slows or revision load rises, the economics change. These terms keep the project viable." | Worst-case scenario with delayed cash, added unpaid time, or early-stop risk | Upfront payment, shorter billing intervals, tighter acceptance criteria, pause rights on aged invoices |

Keep one checkpoint in front of you#

Before negotiating, verify that cash-flow type and discount-rate logic still match. If you are discounting cash flows to yourself as the equity owner, keep that consistent and do not switch into firm-level logic such as WACC.

Your pre-call action sequence#

Before any client call, do this in order:

- Prepare the model outputs you will use: likely case, downside case, and payment-timing assumptions.

- Define your acceptable downside: the lower bound that still protects your cash flow and time.

- Set a walk-away condition: if the downside goes negative unless terms improve, the decision is renegotiate or decline.

- Map terms to risk level: lower risk can support simpler terms; higher risk should trigger stronger payment timing, scope control, and approval language.

Use the model with discipline. Accept work that clears your required return, renegotiate work that can be fixed with terms, and decline work that only works under optimistic assumptions. Keep your final lens on risk-adjusted value and cash-flow protection.

For a step-by-step walkthrough, see A Guide to 'Comparables Analysis' for Business Valuation.

When you are ready to turn this valuation into a repeatable get-paid workflow, review Gruv's freelancer tools.

Frequently Asked Questions

Can you really use discounted cash flow dcf valuation if you work solo?

Yes, if you base the model on the cash flows your work is expected to generate. Match the discount rate to the cash-flow type you are discounting. If you are discounting cash flows to equity, use cost of equity as the checkpoint.

How should you choose your discount rate?

Choose a required return you can defend based on the risk in your expected cash flows. Treat any custom label as a judgment framework, not a fixed formula. If you use a market anchor, state why your chosen rate should differ.

How is this different from just looking at annual income?

DCF focuses on expected future cash flows and the discount rate used to value them, not just a single-period income figure. It is more decision-useful when timing and risk assumptions can change the result.

How should you handle terminal value in a business-of-one?

Treat terminal value as an assumption you must justify, not a default plug. Stress-test how sensitive your valuation is to that assumption, and treat results as uncertain if most of the value comes from that single input.

What is the biggest modeling mistake?

A major failure mode is mismatching cash flows and discount rates. Keep currency consistent between projected cash flows and the discount rate. Also keep nominal with nominal. If your cash flows include expected inflation, your discount rate should too.

How do you sanity-check assumptions before using the output in pricing or negotiation decisions?

Document each major input and why it matches the cash-flow type and risk you are modeling. Then run a downside case; if the decision only works under optimistic assumptions, treat that as a warning, not a green light.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bls.gov/news.release/archives/ecec_03202026.PDFtrusted

- bls.gov/ecectrusted

- federalreserve.gov/releases/h15trusted

- iese.edu/media/research/pdfs/DI-0449-E.pdftrusted

- irs.gov/instructions/i7206trusted

- online.hbs.edu/blog/post/discounted-cash-flowtrusted

- online.hbs.edu/blog/post/time-value-of-moneytrusted

- pages.stern.nyu.edu/~adamodar/pdfiles/dcfinput.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

How to Perform a Business Valuation for a Small Agency

---

How to Build a 3-Statement Financial Model

Use this model as an operating tool for getting paid and staying liquid, not only as a valuation exercise. If you invoice clients, your real questions are practical: when cash will arrive, what you already owe, and what happens if a client pays late, disputes a payment, or pushes unclear payment terms.