Quick Answer

Start by treating payment sandbox testing as integration validation, not launch proof. Set architecture and conflict rules first, then run failure-focused cases for delayed, duplicate, and out-of-order events, and only then sign off on reconciliation and compliance gates. Use provider constraints as hard inputs: Stripe can retry undelivered webhooks for up to three days, and PayPal requires HTTP 2xx acknowledgments. Finish with a limited production canary using real instruments where supported before full rollout.

Why payment sandbox testing still fails at go-live#

Passing a sandbox flow does not prove production readiness. For CTOs and engineering leads, the real question is whether payment status, webhooks, retries, and operational controls still hold up when events arrive late or more than once.

This guide is provider-agnostic on purpose. The point is to help you sequence decisions so you launch faster with fewer surprises, not just make one test card succeed.

The happy path is easy; parity is not#

Most teams can make a sandbox checkout pass. Sandboxes are useful isolated test environments, but a green result is still narrow evidence.

| Provider | Sandbox note |

|---|---|

| Stripe | Sandbox payments are not processed by real card networks or payment providers. |

| Square | Some production functionality may be missing or behave differently in sandbox. |

| PayPal | Sandbox has the same API feature set as live. |

The practical takeaway is simple: parity is provider-specific. One reassuring claim does not tell you how much go-live risk remains.

Async event handling is where launches break#

Issues often show up after checkout returns success. Webhooks are HTTPS posts from the provider to your server, and delivery is asynchronous. Stripe also notes that endpoints can receive the same event more than once.

If your test plan only validates synchronous approval, you are testing a demo path. Before you call a lane ready, confirm end-to-end behavior for:

- approved payment with expected webhook arrival

- delayed or undelivered webhook followed by retry

- duplicate event delivery handled idempotently

If handler logic is not idempotent, duplicate updates and status drift become likely outcomes.

Sequence decisions before test cards#

A practical approach is to settle three decisions early: the system of record, how async events are applied and reconciled, and what evidence counts as launch-ready. Test cards should confirm that design, not substitute for it.

Start with failure modes. For example, Stripe retries undelivered webhook events for up to three days. Test endpoint outages, replay handling, and traceable reconciliation across that window before you trust any happy-path result.

Scope limits to accept up front#

Some details are only knowable from each provider's current docs, dashboard settings, and account configuration. Stripe explicitly says sandbox settings and capabilities are not synchronized with live and can diverge over time.

Use this guide as a decision sequence, not a parity guarantee. Provider behavior differs, enabled features differ, and sandbox behavior is not interchangeable across payment stacks.

If you want a deeper dive, read How to Build a Payment Sandbox for Testing Before Going Live.

What payment sandbox testing is and what it is not#

Sandbox testing is integration validation in an isolated, non-production provider environment. It is not validation of live money movement. In practice, you use non-production credentials, test cards, or test accounts in environments like Stripe Sandboxes, Square Sandbox, PayPal Sandbox, and Apple sandbox testing flows.

That isolation is the point. Depending on the provider, sandbox transactions can look successful without real payment processing, and test transactions do not move funds. Square also separates sandbox and production credentials, and PayPal sandbox testing avoids impact to live accounts. Use sandbox to validate integration correctness, such as:

- request and authentication flow correctness

- field mapping and token handling

- webhook parsing and status-transition handling

- expected app behavior for provider test outcomes

Do not use sandbox alone to prove production readiness. A green sandbox run does not prove live behavior with real cards, real acquirers, and live risk controls. After you have sandbox confidence, run controlled production validation to check real authorization and settlement behavior and confirm operational support paths. If your plan only tests happy-path approvals, you are validating a demo, not launch risk.

Choose your integration architecture before you write test cases#

Decide what is authoritative before you write assertions. If payment status can change in both your PSP and your ledger, define the conflict-resolution rule first. Otherwise, QA will end up validating contradictory outcomes.

A system of record is the authoritative source for a process, while a source of truth is a harmonized view across systems. In practice, choose whether provider status is your operational record for charge state, or whether ledger journal events are authoritative and provider updates are inputs to later posting decisions.

Pick one status owner#

Pick a single owner for each money-moving status. If the PSP owns status, internal records should project provider transitions. If the ledger owns status, states like paid or reversed should come from journal events, not from whichever webhook or API response arrived first.

The common failure mode is hidden dual authority: checkout marks paid, a webhook updates it again, and finance trusts a third ledger path. Either architecture can work, but only with an explicit tie-break rule. Before you write tests, document for each state:

- which component can create it

- which component can amend it

- what evidence is required

If you use Stripe events, account for freshness explicitly. Snapshot payloads can be stale. Thin events are designed for up-to-date handling. Fetch the latest resource state from the API before you make final decisions.

Define clear boundaries between checkout, Wallet, and payouts#

Define ownership boundaries early. One workable pattern is to use checkout for payment interaction, Wallet for balance-affecting journal events, and payout batches for settlement grouping and export. Unclear boundaries can turn webhook failures into reconciliation drift.

Design tests to catch replay and retry behavior, not just happy paths. A common failure is crediting Wallet from an early success signal, then crediting it again on replay. Stripe also warns against processing the same event multiple times, and retries can span very different windows, live mode up to three days versus sandbox three times over a few hours.

Require an idempotency key and replay policy for every balance-changing action. Then validate that policy with a compact evidence set: an event map, one duplicate-delivery trace, and one payout reconciliation report mapped back to included transactions. This matters even more for instant payouts, where Stripe says you are responsible for mapping payouts to transaction history.

Treat Merchant of Record as part of event design#

Merchant of Record decisions belong in your event model before launch. In Stripe Connect, charge type can change who the merchant of record is. For example, direct charges make the connected account the merchant of record.

At minimum, carry the selling entity, liable entity, and payout beneficiary through your events. If those fields are missing, refunds, disputes, and reporting become harder to untangle later. Keep legal-entity verification in scope during testing where your provider requires it, since verification can gate whether payments and payouts can proceed.

Related: How to Build a Developer Portal for Your Payment Platform: Docs Sandbox and SDKs.

Compare provider sandbox capabilities before you commit a launch date#

Your schedule should be set by the hardest lane to validate, not the easiest one to demo. In practice, parity gaps and setup friction matter more than how quickly a happy path passes.

Capability matrix#

| Provider | Test cards or tokens | Webhook simulation depth | Setup friction and environment constraints | Known unknowns |

|---|---|---|---|---|

| Apple Pay Sandbox | Uses Sandbox Apple accounts in App Store Connect; cited sources here do not show a broad public test-card catalog comparable to Square. | No equivalent public webhook simulator is documented in the cited sources. | App Store Connect access is role-gated (Account Holder, Admin, App Manager, or Developer). Setup includes Merchant ID creation and a Payment Processing certificate, and Apple documents certificate expiry at 25 months. | Public docs here do not expose a broad failure-trigger catalog or webhook simulation surface. |

| Square Sandbox | Square documents test credit card numbers and payment tokens for sandbox payments. | Webhooks are testable; Square also states webhooks can be delivered more than once, so duplicate handling is required. | Free isolated environment with separate credentials and resources. Constraint: card-present testing is currently not supported, and some production functionality may be missing or behave differently in sandbox. | Docs confirm behavior gaps, but not a complete parity map for all production conditions. |

| PayPal Sandbox | Uses sandbox accounts in a virtual environment that simulates production behavior. | PayPal provides a webhook simulator, but simulated events are for demonstration, not tied to any App, and not shown in the dashboard event viewer. PayPal also retries failed deliveries up to 25 times over 3 days. | Setup requirements vary by integration; PayPal notes some features do not apply to sandbox. | The simulator checks listener behavior, but full app-bound, production-equivalent event behavior still needs separate validation. |

| Stripe Sandboxes | Isolated Stripe test environments; cited docs here focus on sandbox environment behavior, and Stripe supports up to five environments. | Stripe CLI supports direct webhook event triggering in a sandbox. | Setup requirements vary by integration. Documented limitation: IC+ pricing cannot be tested in a sandbox. | Direct event triggering helps validate listeners, but sandbox tests still exclude some live conditions (for example, IC+ pricing). |

Use the weakest lane as your estimate#

Once you understand the capability spread, estimate from the weakest critical lane. Before you commit a date, require each provider lane to pass three checks:

- confirm environment and credential access is working end to end

- confirm webhook testing matches that provider's documented simulation limits

- record at least one unsupported or unclear area as an explicit launch risk

That is the practical output of sandbox testing: a realistic readiness estimate based on the hardest lane, not a single green dashboard.

Configure environments and credentials in the right order#

Setup order matters more than most teams expect. Late failures in sandbox often come from environment and transport issues, not only payment-logic bugs.

Start with Apple Pay prerequisites, and split web from app#

For Apple Pay, complete identity and certificate setup first. Apple's sequence is straightforward. Confirm Apple Developer account access. Confirm Team Agent or Admin for web setup. Create the Merchant ID. Then create the required certificates, with CSR generation and upload in the certificate flow.

Use each certificate type for its actual role. The payment processing certificate is tied to the Merchant ID and encrypts payment data. The merchant identity certificate is for Apple Pay on the web session authentication and is not required for app-only flows. Track certificate lifecycle early, since Apple states the payment processing certificate expires every 25 months.

Prove transport and domain setup before any UI test#

For Apple Pay on the web, validate HTTPS, valid SSL, and TLS 1.2 or later before you test checkout UI. Also register and verify every top-level domain and subdomain where the Apple Pay button appears.

If transport or domain verification is incomplete, stop there and fix it first. Otherwise, you can easily misread environment failures as checkout-code defects.

Confirm device and account state for sandbox Wallet testing#

Before you call the integration ready, verify device and tester state. Apple documents Sandbox Apple accounts in App Store Connect for development-signed device testing, and Developer Mode must be enabled on each test device.

For iCloud sandbox sign-in, follow your processor guidance. Here, that explicit requirement is documented in Braintree's Apple Pay sandbox guidance.

Run a preflight checklist before functional tests#

Before you run any functional case, collect proof that setup is actually clean:

| Preflight area | What to verify |

|---|---|

| Access and ID setup | Developer access and role confirmed; Merchant ID exists; correct certificate type mapped to web versus app path. |

| Certificate handling | CSR handled where required; payment processing certificate validity tracked; merchant identity certificate present for web path. |

| Web transport and domains | Apple Pay web HTTPS and TLS 1.2+ verified; all Apple Pay domains and subdomains verified. |

| Callback endpoints | Callback endpoints validated in the target environment; Stripe public webhook endpoints use HTTPS; PayPal simulator target is HTTPS on port 443. |

If preflight fails, pause functional testing until the environment is clean.

Design test data that forces both success and failure behavior#

Once preflight passes, each test case should answer the basics clearly: what should happen, how should it recover, and what must never happen twice.

Build the matrix around provider-documented triggers#

Start with what each sandbox can actually simulate, then map each case to your Wallet and payout-batch outcomes.

- Square Sandbox: use sandbox test values and token or card test paths, since it does not accept valid credit cards.

- Stripe testing lanes: include approvals, declines, disputes, authentication-related failures, and delayed-notification methods where

PaymentIntentcan stay inprocessingbefore final success or failure.

| Scenario | Provider lane | Input style | Expected internal outcome |

|---|---|---|---|

| Approval | Square Sandbox, Stripe | Documented success trigger | Wallet and payout eligibility move only at your defined confirmation point |

| Decline or authentication failure | Stripe | Documented decline or auth path | No duplicate balance movement; no unintended payout candidate |

| Duplicate submission | Stripe and Square | Same logical purchase retried; same idempotency key where supported | One financial effect only; duplicate safely ignored or mapped to prior result |

| Delayed confirmation | Stripe delayed-notification method | Method that can remain processing | Wallet remains pending until terminal outcome; payout stays gated |

| Token or card edge case | Square Sandbox | Sandbox token or test value, not real card data | Failure path is handled without orphaned internal state |

If you use Stripe idempotency keys, test the key lifecycle as part of the matrix. Stripe supports keys up to 255 characters and notes keys can be removed after 24 hours, so include both normal retry behavior and behavior when a key is reused after your retention window.

Define state transitions before execution#

Do not start execution until the before and after states are explicit for Wallet and downstream payout batches. Provider docs do not define your internal state contract, so your team has to.

For delayed Stripe methods, that usually means a required processing checkpoint before terminal status. For duplicate and retry paths, prove that financial and fulfillment effects remain exactly once even if processing is retried.

Include operator-reality failure paths#

This is where test plans usually thin out, and where real launches break. Add intermittent endpoint failures and partial workflow completion that must resume safely. Stripe documents that webhook endpoints can receive duplicate events and that undelivered events are retried for up to three days, so recovery tests should include reprocessing protection.

When your required scenarios are not explicitly documented by providers, add internal synthetic scenarios and label them clearly as simulation assumptions. Keep them separate from provider-documented triggers, such as Square's sandbox dispute test amount 8803 (DUPLICATE). Keep the results caveat just as clear: sandbox behavior is useful for validation, but it is not full production parity.

Validate webhooks and retry safety under asynchronous load#

Webhook testing is a critical lane for launch safety. Asynchronous delivery can arrive late, out of order, duplicated, or overlap with manual recovery work. Treat it as a first-class part of the plan, and verify that async behavior cannot create a second Wallet credit, a second fulfillment action, or an invalid payout-batch entry.

Make event handling resilient before you test volume#

Assume disorder by default. Stripe states event order is not guaranteed, duplicate deliveries can happen, and undelivered events are retried for up to three days. PayPal similarly requires an HTTP 2xx acknowledgment for each webhook and retries failed deliveries up to 25 times over 3 days.

Design handlers for that reality, not for ideal sequencing. Avoid assumptions like "success always arrives after processing" or "replay is always safe because the first run finished." For each event family, define one rule: check whether the event is new, stale, or already consumed, then allow only one internal transition.

Separate request idempotency from event deduplication#

Do not collapse these into one control. You need both.

For outbound API retries, define a canonical idempotency key per logical operation. Stripe idempotency keys can be up to 255 characters and can be removed once they are at least 24 hours old. For PayPal REST POST retries, use PayPal-Request-Id.

For inbound webhooks, deduplicate on provider event ID and log processing status. Stripe explicitly recommends logging processed event IDs to guard against duplicate deliveries. Do not treat outbound idempotency keys as a substitute for inbound event deduplication.

For one logical payment, keep an auditable chain that ties together provider object ID, provider event ID, outbound idempotency key or PayPal-Request-Id, resulting ledger journal event ID, and payout-batch decision. Replays should resolve to a no-op or a pointer to existing journal state, not a second financial effect.

Race conditions worth forcing on purpose#

You will learn more from a few deliberate race conditions than from another round of happy-path tests. Force these cases in executable tests:

| Scenario | What to force | Expected result | Red flag |

|---|---|---|---|

| Event arrives before API poll | Webhook updates status before poller reads provider state | One converged final state; poll path does not write a second ledger journal event | Wallet or fulfillment changes twice |

| Poll before event | Poll marks pending or terminal before webhook lands | Late event is accepted or ignored by conflict rule, with no duplicate side effect | Event reopens or reverses state without allowed rule |

| Duplicate event after success | Replay same webhook after terminal success | Duplicate provider event ID is logged; handler returns success with no new money movement | Second Wallet credit, second email, second payout candidate |

| Out-of-order updates during payout batches | Send older status after newer status while item is evaluated for payout | Payout uses defined finalization gate; stale event cannot incorrectly change eligibility | Batch export diverges from ledger truth or eligibility flips repeatedly |

Also test overlap between manual recovery and automatic retries. Stripe documents that manual undelivered-event processing can run at the same time as automatic resend traffic, and manual retrieval is limited to events from the last 30 days.

Define one pass condition that ops can audit#

A passing async test ends with one traceable final state plus an auditable event trail. If the trail is unclear, the case is not passing even if the UI looks correct.

For Stripe testing, prove which event ID was accepted, which duplicate was ignored, and which ledger journal event recorded movement. For PayPal testing, verify your listener returns HTTP 2xx and use the simulator against an HTTPS port 443 listener when validating receiver behavior before go-live. Include at least one operator replay case using event inspection or resend controls.

Use a hard release gate: if any async case ends with two plausible truths, such as "ledger succeeded" but "payout still pending," block release until state resolution is deterministic.

Reconcile ledger truth before polishing dashboards#

Do not let dashboard polish outrun money movement. Release should stay blocked unless finance can replay one trail from request to ledger journal event to payout export.

A reconciliation test should pass only when ledger journal events and Wallet projections stay aligned through retries, late provider updates, and reversals. Treat Wallet as a projection of ledger truth, not a second source of truth. For each logical payment, keep one traceable chain: request identifier, provider object or transaction reference, provider event evidence, ledger journal event, Wallet effect, and payout-batch decision.

Use transaction-level evidence, not payout totals#

Totals are not enough. Stripe is explicit that payout objects alone do not include the individual transactions behind the total. Reconcile at the transaction level with BalanceTransaction records, and for payout checks, filter BalanceTransaction by payout ID so your internal payout batch can be rebuilt from those rows, not just matched to a total.

PayPal positions its payouts reconciliation report for end-to-end money-flow reconciliation and states the report is placed on SFTP by 9:00 AM daily. If your team cannot match internal export records to that report without guesswork, the settlement path is still fragile.

| Lane | Verify | Release red flag |

|---|---|---|

| Stripe payouts | Filter BalanceTransaction by payout ID; tie each row to a ledger journal event and Wallet movement | Total matches, but one included transaction cannot be explained |

| Square webhook-driven eligibility | Store webhook event IDs and acknowledgment outcomes before marking payout eligibility | UI shows paid, but a late or duplicate event changes eligibility after export |

| PayPal payouts | Match internal batch records to the payouts reconciliation report delivered by 9:00 AM daily on SFTP | Finance cannot reproduce end-to-end money movement from internal and report evidence |

Validate payout batches against webhook evidence#

Do not sign off from status screens alone. Square warns duplicates can be sent when acknowledgments are delayed, and your app has 10 seconds to respond. Square also does not guarantee delivery order. Include a test where a transaction appears complete in the UI, then send an older or duplicate webhook. Exported batch correctness should still hold because eligibility is tied to stored event evidence and acknowledgment history.

Stripe also provides payout.reconciliation_completed as a reconciliation workflow signal. Use it as operational input. A practical check is to start from payout ID and inspect related BalanceTransaction rows. Then find the webhook or report artifact that closed reconciliation, and land on the exact ledger journal events that produced or withheld Wallet movement.

Add exception paths before go-live#

Exception paths are often where launches fail: unmatched funds, returned payouts, and delayed corrections. Stripe reporting includes a failed payouts section, so test at least one case where funds do not settle and the item is held for investigation instead of marked complete.

Document the investigation workflow in operator terms: where unmatched items queue, which report or webhook is checked first, which identifiers must match, and who can approve a correcting ledger journal event. If finance cannot reproduce request-to-ledger-to-export movement, release is not ready.

Add compliance and tax gates to end-to-end tests#

Once money movement is traceable, hold compliance and tax to the same standard. A payment flow is not ready if payment or payout can bypass the compliance or tax state your program requires.

| Form or filing | Purpose | Threshold or note |

|---|---|---|

| Form W-9 | Provide a correct TIN | To a requester filing an information return. |

| Form W-8BEN | For a foreign beneficial owner | When requested by a withholding agent or payer. |

| Form 1099-NEC | Nonemployee compensation | Keep output paths distinct from Form 1099-K. |

| Form 1099-K | Reportable payment transactions | Keep output paths distinct from Form 1099-NEC. |

| FinCEN Form 114 (FBAR) | Filed when FBAR applies | Trigger: aggregate foreign account value exceeded $10,000 at any time during the calendar year reported; due April 15 with an automatic extension to October 15. |

| Form 8938 | FATCA-related asset reporting | For specified foreign financial assets. |

If KYC, KYB, AML, or VAT validation is enabled, test those controls as stateful gates, not static profile fields. Cover pass, pending, and fail branches, and verify each branch changes payment acceptance, payout eligibility, or manual review at the expected step. Your audit trail should show who was screened, which status was returned, when it changed, and which downstream decision consumed it.

Apply the same branching to tax profiles. Form W-9 is used to provide a correct TIN to a requester filing an information return. Form W-8BEN is for a foreign beneficial owner when requested by a withholding agent or payer. If your program collects either form, test form selection, stored form type, and downstream reporting hooks. Then confirm output paths stay distinct for Form 1099-NEC (nonemployee compensation) and Form 1099-K filing duties for reportable payment transactions.

For U.S.-linked foreign-account scenarios, represent FBAR and FATCA controls only where relevant, but do not leave them implicit. When FBAR applies, it is filed on FinCEN Form 114, with a trigger when aggregate foreign account value exceeded $10,000 at any time during the calendar year reported. The annual due date is April 15, with an automatic extension to October 15. FATCA-related asset reporting uses Form 8938 for specified foreign financial assets.

Publish variance by country and program. Stripe notes sandbox and live settings can diverge, and Stripe Tax calculates only in jurisdictions where you added a registration. Square also states seller location affects available payment methods, features, and regional tax or security requirements. Maintain an enabled-versus-planned matrix so "covered" does not hide real gaps.

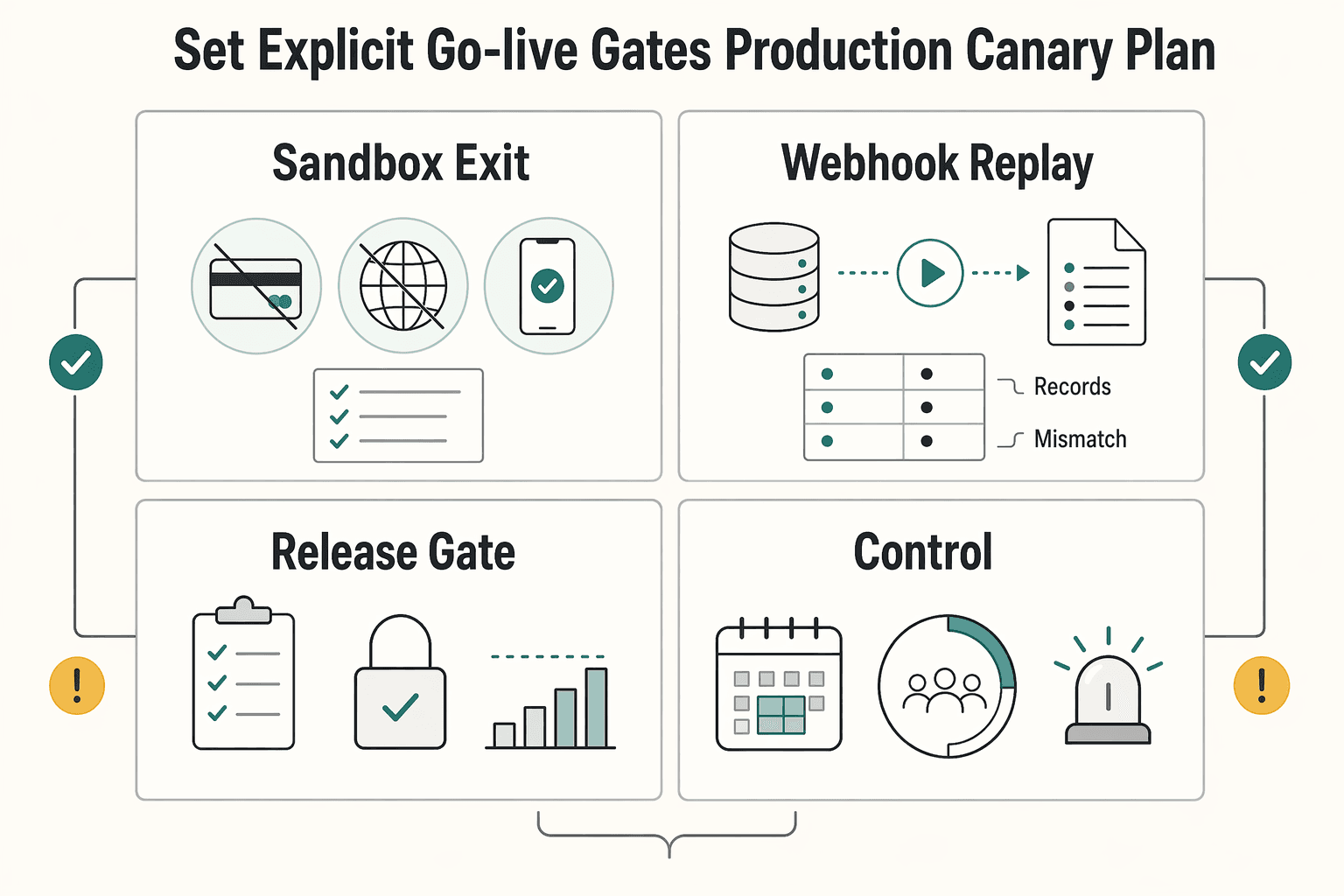

Set explicit go-live gates and a production canary plan#

Sandbox success is a starting point, not a launch decision. Before full launch, require gate evidence from live-path behavior and a bounded production canary. Stripe Sandbox payments do not run through real card networks or processors, PayPal sandbox test values do not work in production, and Apple sandbox results can appear successful without real payment processing.

| Gate | Minimum evidence before launch | Hold or rollback trigger |

|---|---|---|

| Sandbox exit | Critical approval, decline, retry, duplicate, and delayed-event cases passed with saved traces | Any unresolved gap in a critical payment, payout, or compliance path |

| Webhook reliability | Live endpoint verified separately from test; listener returns HTTP 2xx; duplicate and replay handling proven | Non-2xx responses, missing events, or inconsistent end state after retries |

| Reconciliation sign-off | Request, provider event, and internal records align for canary transactions | Any unexplained mismatch, orphaned event, or required manual correction |

| Compliance controls | Required compliance and PCI controls are confirmed on the live path your program uses | A live transaction bypasses a required control, or audit evidence is incomplete |

Run the canary as a partial, time-limited rollout on a tightly scoped slice using real production traffic or real payment instruments where supported. Define rollback alarms before the first live transaction.

Treat webhook behavior as a hard go-live signal. Stripe's go-live checklist calls for confirming live endpoint behavior separately from test behavior. PayPal treats receipt as successful only on HTTP 2xx and can retry up to 25 times over 3 days. Stripe can resend undelivered events for up to three days, and Square notes webhooks can be delivered more than once.

If Apple Pay is in scope, require explicit production verification beyond sandbox. Apple Pay Sandbox completion is not sufficient, and sandbox cards are rejected in live processing.

For a step-by-step walkthrough, see How to Set Up an IRS Payment Plan and Keep It Active.

Map each go-live gate to concrete webhook, idempotency, and reconciliation checks in the Gruv docs before rollout.

Build confidence with evidence not just green test runs#

Green sandbox runs are useful, but they are not a release argument. Build confidence by moving through clear gates in order and keeping evidence at each gate so engineering, payments ops, and finance can review the same facts.

Sequence the work in the order risk appears#

A practical sequence keeps the work honest: architecture, setup, async and failure behavior, then reconciliation and compliance. It is a practical pattern, not a universal provider mandate.

Start by defining state ownership and conflict rules before QA. If one path marks success from an API response and another updates state from later events, lock that rule first so retries and delayed events do not create ambiguous outcomes.

Then confirm setup before functional runs. Validate credentials, confirm the webhook endpoint is reachable over HTTPS, and verify test events are accepted and logged before spending cycles on happy-path flows. Include unhappy-path inputs too: incomplete, invalid, and duplicate data.

Treat async behavior as release evidence#

This is where launch risk often appears. Stripe says live and sandbox are designed to be similar, but also states sandbox payments are not processed by real card networks or payment providers. Square documents that some production functionality may be missing or behave differently in sandbox. PayPal retries webhook delivery on non-2xx responses, up to 25 times over 3 days.

Your checkpoint should be simple: every async case reaches one traceable final state with an auditable event trail. For Square, respond quickly. Its docs call out a 10-second response window tied to duplicate resend behavior. Record response codes and event IDs used for duplicate suppression. For PayPal, deliberately test non-2xx handling and confirm retries do not cause duplicate state mutations.

Keep one evidence pack per gate#

There is no single provider-required format, but you still need review-ready evidence:

- Architecture pack: state ownership, conflict rules, and expected final states for success, invalid-input failure, retry, and duplicate-event cases.

- Setup pack: credential validation, webhook reachability over HTTPS, and proof that test events are accepted and logged.

- Async and failure pack: request IDs, event IDs, duplicate-suppression proof, retry outcomes, and delayed or out-of-order event logs.

- Reconciliation and compliance pack: payout reconciliation evidence tying payouts to underlying transactions, plus any production-access or compliance steps with lead time; some programs document at least one week for production-access processing.

Turn this into release criteria with owners#

The last step is operational discipline. Convert these gates into a launch checklist with an owner, due date, and release-blocking rule for each one. A phased model is practical: integration testing, finance testing, then dogfood. If reconciliation cannot tie payouts back to source transactions, or webhook retries still create state drift, keep launch blocked until it is resolved.

If you want a starting structure, use Testing Payment Flows in Sandbox: A Developer's Checklist. Adapt it to your providers, ledger rules, and sign-off process.

Related reading: How to Build a Contractor Payment System for a Nursing or Allied Health Staffing Agency.

If you want a second set of eyes on your launch gating model and market-specific constraints, contact Gruv. ---

Frequently Asked Questions

What is payment sandbox testing?

Payment sandbox testing validates your integration in an isolated, non-production environment with test credentials and provider-defined test card values. It helps you verify request handling, event flow, and user-path behavior before real money is involved. Use it as integration evidence, not proof of live payment processing.

Does passing sandbox tests mean we are go-live ready?

No. Sandbox payments do not prove behavior on real card networks or live payment rails. Plan a limited production check with real instruments where supported, and monitor webhook delivery and retry behavior closely.

What do we need before starting sandbox tests?

Start with provider accounts and API credentials. For webhook testing, use endpoints that are publicly reachable over HTTPS. If Apple Pay is in scope, set up the Merchant ID and Payment Processing certificate first, and ensure Apple Pay web traffic runs on TLS 1.2 or above. Before functional runs, confirm credentials, certificate and domain setup where required, and that test events are accepted and logged.

What should we test besides successful payments?

Test failure paths as first-class cases, not just approvals. Include declines, fraud and invalid-input cases, retry behavior with idempotency keys, duplicate webhook deliveries, and out-of-order or partial webhook payloads. Define the expected final state for each case across customer status, internal records, and operations handling.

Why do teams still fail at launch after green sandbox tests?

Launch issues usually come from async behavior and environment gaps that were not exercised in test. Teams often assume webhook timing and ordering that does not hold in production, or discover late that sandbox parity is incomplete for a critical path.

How do we handle provider differences safely?

Assume sandbox parity is uneven and document it explicitly in a capability matrix. Mark supported paths, unsupported paths, and unknowns for each provider, then fill critical gaps with targeted production checks. For a practical coverage structure, use Testing Payment Flows in Sandbox: A Developer's Checklist and gate launch on the weakest critical provider path, not the easiest one to test.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- developer.paypal.com/tools/sandboxtrusted

- developer.paypal.com/api/rest/webhookstrusted

- docs.stripe.com/sandboxestrusted

- docs.stripe.com/webhooks/process-undelivered-eventstrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/businesses/corporations/foreign-account-tax-...trusted

- taxation-customs.ec.europa.eu/taxation/vat_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Build a Payment Sandbox for Testing Before Going Live

Platform teams need a sandbox before go-live because it lets you validate payment behavior without touching live merchants or your production account. More importantly, it keeps launch decisions from resting on a clean demo of the happy path.

Testing Payment Flows in Sandbox: A Developer's Checklist

This is a release-grade **payment sandbox testing checklist** for engineering leads, not a generic QA list. It keeps sandbox validation focused on your PSP connection and related payment flows before controlled live validation.

How to Build a Developer Portal for Your Payment Platform: Docs Sandbox and SDKs

Build your portal so teams can move from the first sandbox call to production approval without guessing what comes next. The goal is speed without hidden integration debt: clear auth setup, explicit test expectations, and a defined go-live path.