Quick Answer

Start by choosing the operating model before UI details: J.P. Morgan Wallet for bank-style virtual sub-ledgers, Moov-style multiple wallets for compartmented balances, or Circle Wallets for USDC/EURC asset flows. Then lock four items in writing: what each wallet can store, when FX is triggered, which policy states block payout, and which records prove settlement. Approve go-live only after one end-to-end test shows creation, movement history, and reconciliation export.

Sub-wallets are an operating choice, not a balance display feature#

Step 1#

Short answer: treat sub-wallets as an operating choice, not just a balance view in your product. The core decision is not about UI. It is about where money lives, what a balance actually represents, and what your team will need to reconcile later.

That is why this guide separates three designs that often get blurred together when teams talk about multi-currency wallets and sub-wallets. At one end, J.P. Morgan Wallet is framed as an accounting-based model for creating sub-ledgers in real time. In the middle, Moov-style multiple wallets let one account hold separate compartments, each with its own balance and transaction history. On the stablecoin side, Circle positions USDC and EURC as the core assets for wallet and payment builds.

Use one checkpoint before you design anything: can your team name the source of truth for balances, the asset being stored, and the event that proves a payout happened? If that answer changes depending on who you ask, you are not choosing a wallet feature yet. You are still choosing an operating model.

Step 2#

Compare the three paths on the same sheet before you commit. The practical question is not which wallet looks cleaner. It is which model fits your payout obligations, reconciliation needs, and asset constraints.

The bank sub-ledger route can be a fit when you need accounting-grade balance control and broad payout operations. J.P. Morgan markets Wallet for high-volume payment operations and cites reach across 170+ countries and 120+ currencies, 24/7/365. Treat that as a useful coverage signal, not proof that your exact corridor, payment type, or program setup is ready out of the box.

The product-segmentation route solves a different problem. Moov's multiple-wallet model gives you clean compartments with independent balances and histories, which is useful for organizing funds across projects or business functions. The tradeoff matters. Multiple wallets do not answer FX, treasury, or ledger design questions on their own. You still need to define whether each wallet is single-currency only, whether conversion exists at all, and how those events are recorded.

Step 3#

Use the stablecoin path only if you are comfortable choosing a different asset model, not just a different API. Circle's support is explicitly bounded to USDC and EURC on supported blockchains, so this is not a generic all-currencies option. EURC is described by Circle as reserve-backed, redeemable 1:1 for EUR, and positioned under MiCA, which matters if euro-denominated balances are in scope.

For most teams, the advice is simple: choose the architecture first, then document the hidden operating assumptions early. Your first evidence pack should at least capture what creates a wallet or balance compartment, what asset sits inside it, and what records finance will use to verify movement later. That small discipline usually reduces rework later.

What to prepare before you design anything#

Before anyone builds wallet objects or payout routes, lock scope, controls, integrations, and evidence handling. If you leave country coverage, currency behavior, or audit traceability for later, you will usually redesign core flows.

| Area | What to define | Grounded details |

|---|---|---|

| Scope note | Contractor countries, payout methods, target currencies, and where multi-currency behavior is required versus optional | Build a country-and-currency support matrix by payment method; "we support EUR" is incomplete unless you specify presentment currency, settlement currency, or both. |

| Control surface | Who can create and close sub-wallets, who can trigger or approve conversions, and which actions must appear in audit logs | Wallet states can include active and closed; default wallets may be non-closable and remain active; some models cap accounts at up to 10 active general wallets. |

| Integration constraints | What stays with the provider and what your internal services must own | J.P. Morgan Wallet is positioned around Real-time Virtual Sub-ledgers, while Circle's Developer-Controlled Wallets Node.js SDK supports wallet creation, transaction execution, and signing through APIs and SDKs. |

| Evidence pack | How you will retain FX quote identifiers, payout status-change events, and reconciliation exports | Keep artifacts in CSV-friendly form where possible; downstream audit exports can have per-export limits such as 50,000 records in a standard export. |

-

Write a short scope note. List contractor countries, payout methods, target currencies, and where multi-currency behavior is required versus optional. Build a country-and-currency support matrix by payment method, because support varies by method and cross-border payout programs often target freelancers and similar counterparties in local currency. Flag ambiguity early: "we support EUR" is incomplete unless you specify presentment currency, settlement currency, or both.

-

Define the control surface. Decide who can create and close sub-wallets, who can trigger or approve conversions, and which actions must appear in audit logs. Lifecycle constraints are real: wallet states can include

activeandclosed, default wallets may be non-closable and remainactive, and some models cap accounts at up to 10 active general wallets. If your UX assumes unlimited, user-deletable compartments, verify that before design review. -

Inventory integration constraints early. Bank-ledger and API-first models place ownership in different places. J.P. Morgan Wallet is positioned around Real-time Virtual Sub-ledgers, while Circle's Developer-Controlled Wallets Node.js SDK supports a model where you control wallet creation, transaction execution, and signing through APIs and SDKs. Document what stays with the provider and what your internal services must own.

-

Choose the evidence pack before you build. Define how you will retain FX quote identifiers when available, payout status-change events, and reconciliation exports. Keep a simple standard: each conversion and payout should be traceable from request to export artifact, in CSV-friendly form where possible, since downstream audit exports can have per-export limits such as 50,000 records in a standard export.

Sub-wallets vs sub-ledgers and what multi-currency really means#

Sub-wallets and sub-ledgers are not the same object, and that distinction should be explicit in your spec from day one. If audit-grade traceability is the first priority, design the sub-ledger model first; if user budgeting buckets are the first priority, design wallet behavior first and map each action back to ledger events.

Step 1. Define the object clearly. A sub-wallet is a product-facing balance compartment. In Moov's multiple-wallet model, each wallet has its own balance and transaction history, which supports fund management and reconciliation. A sub-ledger is an accounting ledger for a detailed subset of transactions, and sub-ledger totals roll up into the general ledger. J.P. Morgan Wallet describes Real-time Virtual Sub-ledgers as an accounting-based capability, so treat that path as ledger infrastructure first, not just UI compartments.

Step 2. Declare where truth lives. Write one unambiguous line in the spec: either "wallet balances are user-facing projections" or "sub-ledger balances are operational truth." Then enforce traceability so wallet movements can be matched to ledger entries and reconciliation outputs.

Step 3. Define "multi-currency" with specific actions. A multicurrency account can hold, manage, and transact in multiple currencies without requiring conversion on every transaction. So state whether your wallet supports per-currency storage only, or also FX conversion between currencies. Avoid loose phrasing like "supports EUR" unless you specify whether funds are stored, settled, converted, or paid out. For a useful contrast, see How Platforms Use Pooled Wallets vs. Individual Wallets for Contractors.

Compare the three architecture paths before committing#

Compare all three paths on the same control surface before building. If you need broad fiat payout operations now, do not default to a stablecoin architecture unless compliance and treasury explicitly approve it.

Step 1 Compare all three paths on the same control surface#

Put J.P. Morgan Wallet, a multiple-wallet product model such as Moov, and a stablecoin route such as Circle Wallets side by side. This avoids treating a bank sub-ledger model, a product wallet model, and a USDC/EURC swap flow as if they are interchangeable.

| Path | Wallet lifecycle controls | Conversion support | Reconciliation depth | Integration burden | Market and compliance caveats |

|---|---|---|---|---|---|

| Bank sub-ledger model with J.P. Morgan Wallet | Treat controls as account and sub-ledger governance, not just UI buckets. Positioned for high-volume real-time operations with one bank account. | Confirm exact FX behavior for your use case. Evidence supports reach in 170+ countries and 120+ currencies, 24/7/365, but does not confirm your conversion path. | Strong fit when accounting-grade compartmentation is the first requirement. J.P. Morgan positions it around managing millions of payments in real time. | Confirm implementation scope, SLA, and reporting artifacts directly with the provider. | Do not assume corridor or product eligibility from headline reach alone. Confirm supported countries, currencies, and onboarding requirements. |

| Platform multiple-wallet model such as Moov | Clear wallet-level create/manage behavior. Each wallet has its own balance and transaction history for function-level separation. | Do not assume FX is included. Confirm whether conversion is supported or must be added separately. | Independent balances and transaction histories support wallet-level reconciliation. | Confirm event model, exports, and wallet limits for your operating flow. | Wallet-level cost may vary by fee plan and agreement. Pricing, SLA, and country coverage must be confirmed directly. |

| Stablecoin model with Circle Wallets using USDC and EURC | Circle's example centers on developer-controlled wallets, so lifecycle design depends on your wallet and key-management choices. | The grounded example is swap behavior between USDC and EURC. That is not the same as full fiat FX operations. | Reconciliation scope must cover wallet activity, swaps, and any offchain payout steps. | Validate the full payout architecture, not only wallet creation and swap flow. | MiCA is relevant for euro-denominated stablecoin context: rules on asset-referenced and e-money tokens applied from 30 June 2024, and the broader framework applies from 30 December 2024. Circle wallet pricing is tiered by monthly active wallets and includes a 0-1000 free tier. |

Verification checkpoint: for each path, require one end-to-end test case showing wallet creation, funding, movement history, close or freeze behavior, and reconciliation export.

Step 2 Choose the path that matches your first hard constraint#

Your first hard constraint should drive architecture selection.

If your first hard constraint is audit-grade compartmentation and high-volume fiat operations, review the bank sub-ledger route first. If your first hard constraint is product-level balance separation in your application, review the multiple-wallet route first. If your first hard constraint is onchain value storage or USDC/EURC swap behavior, review the stablecoin route first.

Step 3 Freeze unknowns before you commit#

Do not proceed on assumed parity across vendors. Mark each of these as confirmed or unknown: pricing schedule, SLA, country coverage, supported currencies, conversion behavior, and reconciliation exports.

Approval evidence should include a pricing document, country/currency matrix, one sample reconciliation export, and written confirmation of lifecycle actions (create, close, freeze). If those artifacts are missing, treat that as decision risk, not a paperwork delay.

Design currency storage and FX execution in the right order#

Define wallet currency states before FX policy. FX only occurs when funds move between different currencies, so if you have not decided what each wallet can hold and pay out, quote and routing logic will stay ambiguous.

Step 1 Define what each wallet can actually store#

Document whether each wallet or sub-ledger is single-currency, multi-balance by currency, or just a presentation layer over one underlying balance. That decision determines whether conversion is required at all.

Some setups can hold and pay out in supported currencies without forced conversion. Stripe Connect documents this for up to 18 supported currencies, so in that model you may keep funds in invoice currency until conversion is actually needed.

Use one concrete test flow: contractor invoices in EUR, your platform is funded in USD, payout goes to GBP. Decide whether your product allows EUR storage, forces immediate conversion, or lets the contractor trigger conversion later from a sub-wallet.

Verification point: for one contractor journey, map funding currency, stored currency, payout currency, and whether conversion occurs.

Step 2 Set quote policy before you wire conversion triggers#

Once storage rules are fixed, lock quote behavior in writing. Separate indicative and firm quotes, define which flows require a tradable quote ID, and specify expiry handling.

This matters operationally: providers can return an indicative quote outside opening hours that is not tradable, while firm quotes include a quote ID and expiry time. Stripe extended FX quotes can be set for 5 minute, 1 hour, or 24 hour windows.

If a retry happens after quote expiry, reject the stale quote and fetch a new one. Use idempotency keys on conversion requests so repeated retries return the same prior result instead of creating duplicate execution.

Verification point: run one expired-quote test and one repeated-request test in sandbox, and confirm you get one rejection path and one single conversion outcome.

Step 3 Choose the conversion moment and map dependencies early#

If invoice currency and payout currency differ, choose the trigger explicitly. There is no universally correct moment, so document the tradeoff you accept:

| Conversion moment | Why choose it | Tradeoff or dependency |

|---|---|---|

| At funding | Earlier balance certainty | Less flexibility later. |

| At payout | More routing flexibility | Rate and expiry exposure closer to execution. |

By user action in sub-wallets | Product control | Stronger requirements for intent logging, quote acceptance, and retry handling. |

If you are evaluating onchain conversion, map dependencies before promising timelines: smart contracts, a Circle Developer Account and API key, the Circle Smart Contract Platform NodeJS SDK, and a developer-controlled wallet for contract deployment and execution. Circle's Contracts SDK setup also requires Node.js v22+.

Before approval, show one end-to-end path from stored currency to quote to conversion trigger to payout route, with the artifacts you will reconcile later.

For a step-by-step walkthrough, see How to Evaluate Multi-Currency Personal Finance Software for Tax Residency, FBAR, and Invoicing.

Build reconciliation and audit controls as first-class features#

Make the ledger the authority and treat wallet balances as derived views. This is the control that keeps late events, retries, and returns from turning into finance disputes.

Step 1 Set the ledger as the system of record, and document projection lag on purpose. Your event store or ledger journal should be the place you can always reconstruct truth from, while wallet balances and ops screens remain derived projections. Document eventual consistency in plain language for support and finance: derived read models can lag writes, so a visible wallet balance can update after the ledger entry exists. Checkpoint: take one contractor payout and rebuild current wallet state from historical events without reading the wallet balance table.

Step 2 Define one posting chain for every money movement. For each conversion, payout, credit, return, and reversal, define one repeatable chain before launch:

- Client or internal request ID

- Idempotency key on the write call

- Provider event or transaction reference

- Processor-level reconciliation reference (when available)

- Ledger journal entries created from the event

- Wallet projection update derived from the journal

- Export artifact for close or settlement review

Stripe event objects include an event ID and the API request ID that caused the event, and processor references such as reconciliation IDs are used to track requests through processing. For close, keep exportable artifacts so finance can tie settlements back to ledger totals, for example payout reconciliation views that support CSV export.

Step 3 Verify traceability and replay safety before launch. Every conversion and payout should resolve to one event chain from initiation to ledger to provider result. You should be able to search by internal request ID, idempotency key, provider reference, event ID, or payout batch identifier and land on the same movement.

Run two preproduction checks:

- Retry the same conversion or payout after a client timeout with the same idempotency key and confirm one economic outcome.

- Inject a delayed provider event and confirm duplicate posting is rejected while the audit trail is still updated.

Step 4 Create explicit exception queues for unmatched and late items. Keep unmatched work visible; do not hide it behind a generic processing state. At minimum, expose queues for unmatched credits/returns, provider events with no known local request, and local requests with no provider confirmation yet.

For reversal-clearing operations, add a hard validation where relevant: if the operation is meant to net offsetting items, require selected transactions to total 0 before clearing. Final checkpoint: give support and finance messy cases, including a late webhook and an unmatched return, and confirm they can find the item, understand why it is stuck, and export evidence for close without engineering help.

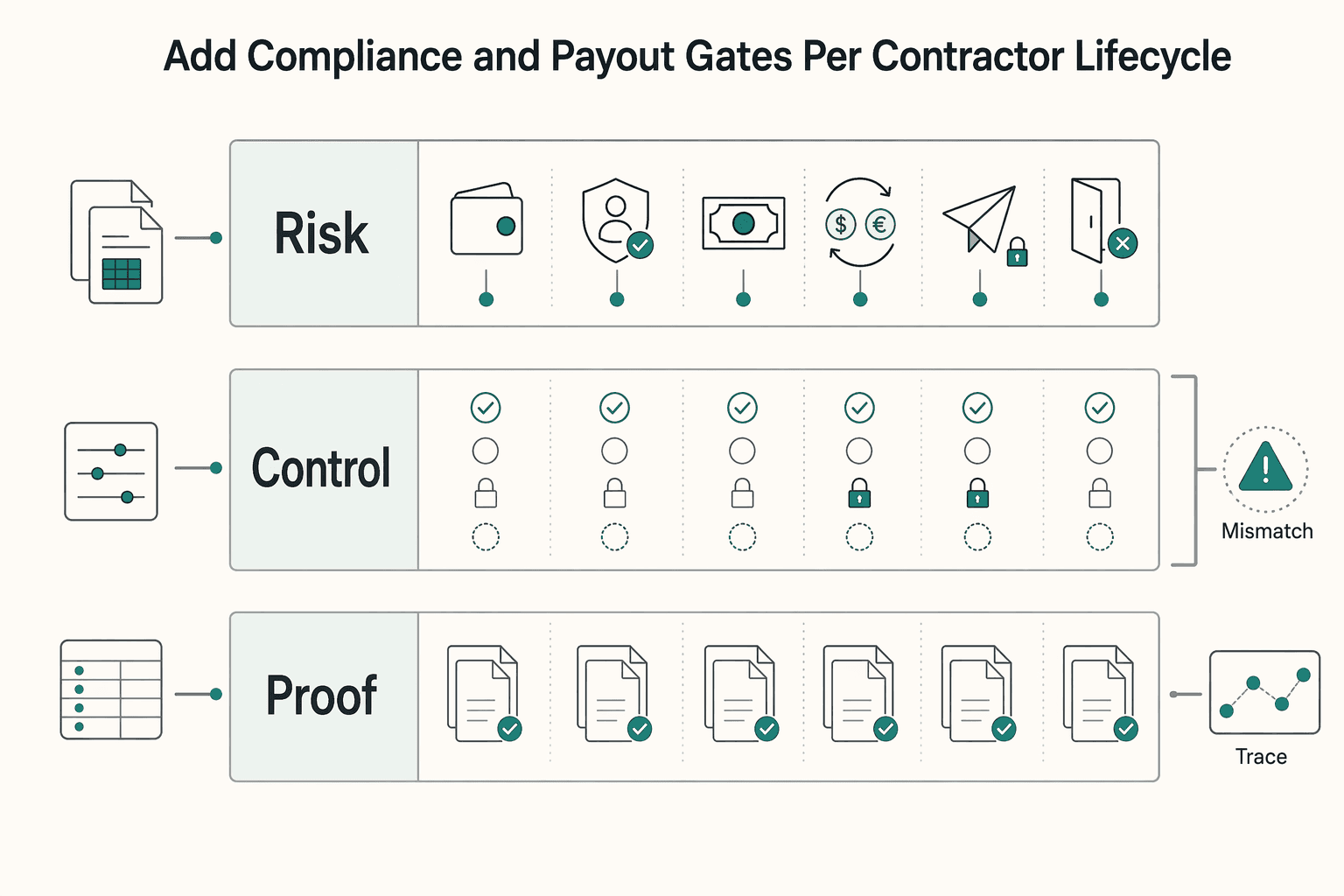

Add compliance and payout gates per contractor lifecycle#

Tie payout eligibility to compliance state, not just balance or payout status. A contractor sub-wallet can be created and funded before payout is allowed, but only where your market and program rules permit that split.

Step 1 Define lifecycle checkpoints as policy checkpoints. Use the same lifecycle every time: wallet creation, activation, funding, conversion, payout, and closure. For each stage, record the policy fields that control the action: KYC status, KYB status for business contractors, AML or review hold state, withdrawal eligibility, and missing-information flags. If these checks are split across tools, teams will approve payouts on partial information.

A practical verification test is simple: from one screen or API response, can you tell whether this wallet can be created, activated, funded, converted, paid out, and closed right now, and why? If any blocked stage has no clear reason code, the gate is too loose.

Step 2 Gate risky actions by policy, not by operator judgment. KYC requirements apply before connected accounts can accept payments and send payouts, and KYB applies when the counterparty is a business. In higher-risk or virtual-asset programs, controls such as customer due diligence, record keeping, and suspicious transaction reporting belong in the design, even when triggers vary by market.

Use an explicit rule: when policy status is incomplete, funding may be allowed while payout release is blocked where required by market or program. Keep "funding allowed" and "payout blocked" as separate states so product, ops, and compliance are not guessing.

Step 3 Make payout release read live verification state. Run the payout gate against current verification state at execution time, not only at activation. Platforms can have payouts disabled when required verification information is not provided by deadline, so eligibility can change after the wallet is active.

A clear red flag is a queue that shows payouts as "ready" based on balance while compliance holds sit elsewhere. Test this directly: submit a payout with incomplete verification, confirm the payout is blocked, confirm the hold reason is visible to ops, and confirm the balance remains traceable in the ledger.

Step 4 Minimize and protect sensitive data from the start. Collect and retain only the personal data needed for the stated purpose. Keep sensitive fields out of broad event payloads, support notes, and general logs unless truly required. If logs include PII, protect log privacy, and encrypt sensitive stored verification data to reduce exposure risk.

In ops tools, default to masked views. If card data appears, show no more than the first six and last four digits. At closure, keep operational records such as closure reason, final compliance state, and approver, and avoid retaining extra sensitive artifacts without a clear need.

Common implementation mistakes and how to recover#

Most failures here come from vague semantics, demo-first planning, and unclear ownership, not missing rails. Fix those first.

Mistake 1: Shipping "multiple wallets" without explicit currency semantics. Recovery: Define each wallet's stored currency, whether conversion is allowed, when conversion happens, and which currency payouts leave in. Charge and settlement currencies can differ, so conversion logic must be explicit instead of implied. For migration, map every existing wallet or balance bucket to a currency-aware target and keep a simple trail: old wallet ID, new wallet ID, currency code, opening balance, and conversion reference when a balance is re-denominated. Validate with historical balances before launch so any residual amount is explainable.

Mistake 2: Treating USDC/EURC swap demos as full payout architecture. Recovery: Keep proof-of-concept and production readiness in separate checklists. A USDC/EURC swap demo on testnet, for example Sepolia with Ethereum Sepolia Faucet and Circle Testnet Faucet, proves swap flow, not production payout readiness. Testnet success is meant to avoid risking real-world assets; it does not prove live payout routing, reconciliation, or country-specific compliance readiness. Production criteria should explicitly cover live payout routes, supported stored currencies, reconciliation evidence, and verified country/program constraints.

Mistake 3: Weak reconciliation ownership. Recovery: Assign one named owner for ledger correctness and one named owner for payout operations, then make them share an incident playbook. Reconciliation is a core control for financial accuracy, completeness, and validity, so ownership cannot stay ambiguous. Test one failure mode on purpose: create a mismatch between provider payout status and internal balance, then confirm who pauses payouts, who investigates journals, and what artifact closes the incident.

Mistake 4: Hiding unknown vendor constraints. Recovery: Keep a live assumptions log for SLA terms, compliance coverage, and routing limits, with source link, owner, last-checked date, and decision impact. Payout behavior and verification requirements vary by industry and country, so treat any claim that is not tied to a source or contract as unverified.

Conclusion#

Choose your architecture by operating constraints, not by the cleanest demo. If you compare a bank virtual sub-ledger model, a multiple-wallet product model, and a stablecoin path against the same control, payout, and reconciliation tests, the right answer usually becomes clear.

Step 1: Approve the wallet model and ledger model definitions. Write down what a wallet is in your product, what the ledger is in finance terms, and which one is the source of truth. The models solve different problems. A bank virtual sub-ledger path is built around centralized cash structure and scale from one bank account. A multiple-wallet path gives you separate balances and transaction history that change how support and reconciliation work. Verify: finance, product, and engineering can each explain the same flow without redefining "wallet" mid-conversation. Red flag: if your demo shows balances but nobody can point to the journal entry chain, you are still designing UI, not operations.

Step 2: Specify currency storage and conversion moments. Decide whether you are only storing balances by currency or also converting between them, and say exactly when conversion happens: at funding, at payout, or by user action. Do not confuse broad presentment options with payout readiness. A provider may support charging in over 135 currencies, while payout minimums and fees still vary by settlement setup. Verify: every payout currency has a documented funding source, conversion trigger, and minimum payout blocker rule. Failure mode: a payout request is accepted, but the post-conversion balance still does not meet the minimum payout amount.

Step 3: Implement policy gates and payout blockers before release. Tie payout execution to explicit policy status, not just balance availability. If policy is incomplete, you may allow funding but block release where your program requires it. This is especially important if you are considering Circle, USDC, or EURC in the EEA: MiCA context matters, but it does not answer global compliance scope by itself. Verify: blocked payouts produce a named reason code that ops can see and support can explain. Evidence pack: keep policy status, wallet state, payout request ID, and release decision in the same audit trail.

Step 4: Test reconciliation artifacts and replay-safe retries. Your check is not "the API returned 2xx." Async payment flows can accept the request and still fail later. Retries must be idempotent so making the same request multiple times produces the same result. Verify: for one conversion and one payout, you can trace request ID, provider reference, ledger journal, wallet balance update, status event, and close export. Red flag: duplicate retries create different downstream outcomes.

Step 5: Document the unknowns before go-live. Keep an assumptions log for country coverage, fee conditions, supported currencies, wallet-count limits, and compliance scope. For example, a product limit such as 10 general wallets per account may matter a lot if your design assumes wider segmentation. If any of those unknowns can change routing, support load, or close timing, treat them as launch blockers, not future cleanup.

Related reading: How to Choose a Presentation Currency for Financial Reports.

Frequently Asked Questions

What is the practical difference between a sub-wallet and a sub-ledger for a contractor platform?

A sub-wallet is a product-facing balance compartment, often at the customer level. Circle describes sub-wallets as typically being the wallets of your customers, while a sub-ledger is the accounting layer that generates journal entries for those transactions. If audit traceability is a primary requirement, define the sub-ledger behavior first and then map wallet balances to it.

Does enabling multiple wallets automatically give me a true multi-currency wallet?

No. Multiple wallets can simply mean you hold separate balances by currency, with no conversion at all. A provider can support holding and paying out in up to 18 supported currencies without implying FX, so you need to state explicitly whether conversion is allowed, when it happens, and which currency the payout leaves in.

When should I create one sub-wallet per contractor instead of pooled balances?

Create one per contractor when you need independent balance and transaction history for reconciliation. That separation is operationally useful because each wallet can maintain its own balance and history for reconciliation. If you do not need per-contractor balance and history separation, pooled balances can be simpler.

What changes operationally when I add FX and conversion to existing payout flows?

FX is not just a payout feature. It can appear in payments, transfers, payouts, application fees, and other transaction types, so your event model and reconciliation scope gets wider. Track each conversion as a distinct event with journal entries and clear links to the related payout flow. A common failure mode is a payout getting stuck because the post-conversion balance still does not meet the minimum payout amount.

Is a stablecoin route with `Circle Wallets` a shortcut or a different operating model?

Treat it as a different operating model, not a shortcut. The wallet structure may still use a main wallet balance plus customer sub-wallet balances, but you still need explicit rules for whether conversion is allowed, when it happens, and which currency payouts leave in. Multiple wallets alone do not prove FX behavior or payout readiness.

Which table-stakes controls should exist before launch for reconciliation and audits?

At minimum, your ledger should be the source of truth. Funding events, conversions, and payouts should be traceable as linked records, and per-wallet balance and transaction history should remain reconcilable where separation is required. Include payout-readiness checks for minimum payout amounts before execution, especially when conversions are involved.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- commission.europa.eu/law/law-topic/data-protection/rules-business...trusted

- docs.stripe.com/currenciestrusted

- docs.stripe.com/connect/multicurrency-settlementtrusted

- eur-lex.europa.eu/EN/legal-content/summary/european-crypto-ass...trusted

- finance.cornell.edu/sites/default/files/account-reconciliation-n...trusted

- govinfo.gov/content/pkg/GOVPUB-C13-PURL-LPS69969/pdf/GOV...trusted

- nvlpubs.nist.gov/nistpubs/SpecialPublications/NIST.SP.1800-28...trusted

- ojp.gov/ovc_fmrc_guide_sheet_internal_control_separa...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Expand Your Subscription Platform to APAC: Payment Methods Currency and Regulatory Landscape

Asia-Pacific (APAC) expansion requires country-by-country launches, not one regional motion. This guide helps you decide with payment, currency, and regulatory evidence so you do not mistake a strong regional headline for real launch readiness in your subscription platform.

How Platforms Use Pooled Wallets vs. Individual Wallets for Contractors

Choose pooled wallets when your platform needs centralized control over funds and operations. Choose individual wallets when users must control private keys and accept the recovery boundary that comes with that choice.

Intacct vs. NetSuite for Payment Platforms: Which ERP Handles Multi-Currency and High-Volume AP Better

Treat this as an integration-debt decision first, and an ERP comparison second. For payment platforms, multi-currency accounting and higher-volume AP risk usually shows up at the seams between product behavior, finance controls, and integrations, not in top-level feature lists.