Quick Answer

Start with one intake route for non-core requests, enforce a fixed approval workflow, and require an approved PO before supplier commitment. For indirect procurement platforms manage non-core spend, early control comes from guided buying, budget enforcement, and contract-linked invoice checks. Track PO coverage, invoice-to-request match rate, and maverick spend each sprint. If teams keep buying through side channels, simplify required fields before layering more controls.

Why indirect procurement matters for platform operators#

Step 1. Catch this earlier than most teams do. Indirect procurement can sound like back-office spend, but in a platform business it shapes how quickly teams buy tools, onboard vendors, and keep records clean as spend spreads across the company. Speed matters because buying delays slow delivery, and weak controls create cost and compliance problems.

Step 2. Treat decentralized buying as an operating risk, not a side issue. This spend is often decentralized and reactive, which matches how platform teams work when product, engineering, finance, and ops raise requests from different angles. The problem starts when that behavior stays informal: requests begin in chat or email, budgets are assumed rather than checked, and invoices arrive before an approved request or contract reference is clearly documented.

That is where maverick spend and off-contract purchasing become a visibility problem. A consistent approval path breaks down, supplier data fragments, and audit readiness weakens because purchases are harder to trace. If your team cannot answer three basic questions quickly, you likely have a control gap: who approved this, what contract or policy covered it, and where the invoice should be matched.

Step 3. Put in controls that protect speed instead of fighting it. You do not need every low-risk request to go through a heavy approval chain. A practical starting point is a short sequence: standardize request intake, route approvals consistently, then require commitment controls before spend is locked in. In practice, early controls like guided buying, budget enforcement, and integrated supplier data are the core levers for reducing maverick behavior.

Use one simple checkpoint: can you trace a request from intake to approver to supplier to invoice without pulling data from five places? If not, the issue often reflects a loose request path, unclear required fields, or too many ways to buy outside the approved route with no visible exception owner.

This guide is built for that reality. It gives you a decision-oriented sequence for tightening indirect spend in stages. Use it to check what is actually improving: approval speed, visibility into off-contract purchases, and whether the records behind each purchase are strong enough to stand up when finance or audit asks for proof.

Indirect procurement in platform operations#

Set the boundary first: if you manage direct and indirect spend the same way, forecasting, approvals, and visibility usually get weaker.

Step 1. Separate core delivery from operating support. Use direct procurement for materials and labor that directly contribute to what you sell. Treat indirect procurement as SaaS, marketing services, travel, and similar purchases that support operations without becoming part of the final product.

Step 2. Treat maverick spend and off-contract purchases as control failures, not budgeting noise. They usually indicate buying happened outside the agreed path, with inconsistent approval and weak visibility. A practical check is whether recent indirect purchases clearly show an approver, a supplier record, and a contract reference or documented exception.

Step 3. Standardize language before scaling. Define purchase requisition, approval workflow, and supplier contracts once, then use those exact terms in request forms, Slack guidance, finance reviews, and onboarding so routing stays consistent across teams.

Related: Procurement Data Management for Platforms: How to Centralize Vendor Contracts and Payment Terms.

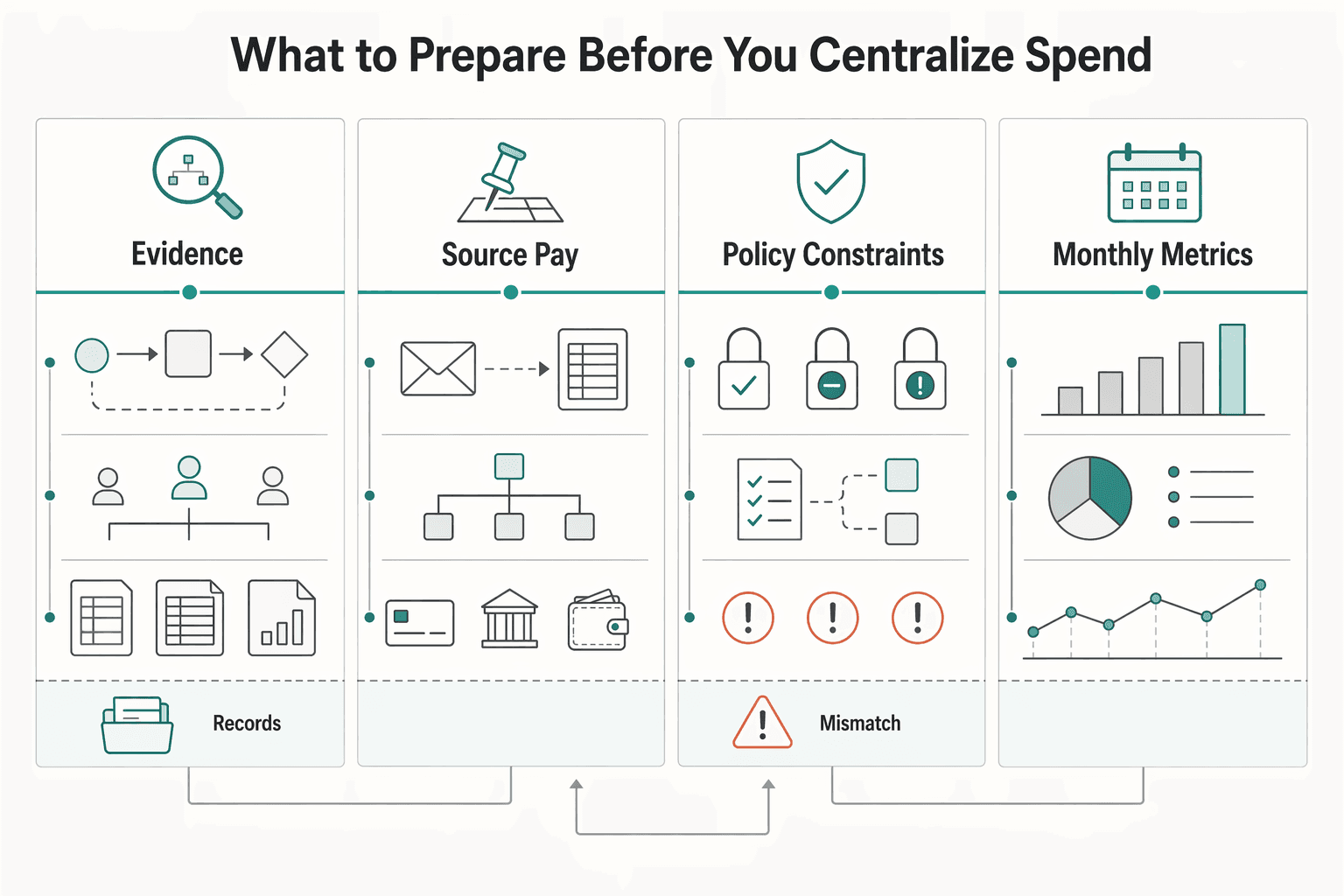

What to prepare before you centralize spend#

Prepare a defensible baseline before you centralize spend, or you will only centralize visible requests while hidden decisions stay in email and spreadsheets.

| Preparation step | What to document | Check |

|---|---|---|

| Baseline evidence pack | Current PO flow, invoice processing path, approval owners, and top non-core spend categories by department; show where requests start, where vendors are approved, when a PO is issued, and how invoices reach payment | Trace five recent purchases from request to invoice and confirm the approver, supplier record, and whether a PO existed before commitment |

| Source-to-pay chain | Every tool and handoff in the source-to-pay chain, including unofficial steps in email and spreadsheets | Flag duplicate data entry, approvals outside the platform, or invoices arriving before requests are visible to finance |

| Policy constraints | Where budget enforcement is mandatory, where exceptions are allowed, who can accept risk, and which categories or departments need hard controls versus documented exceptions | If exception authority is vague, maverick and off-contract spend will keep being treated as urgency instead of policy breaches |

| Monthly metrics | Approval cycle time, off-contract rate, late invoice count, and exception volume tied to audit risk | If two people calculate the same metric from the same evidence pack and get different answers, fix definitions first |

Keep this as a short evidence exercise, not a redesign project. You need a clear record of how requests move today, who approves them, where non-core spend sits by department, and which exceptions already create audit risk.

Step 1. Build a baseline evidence pack. Document the current purchase order (PO) flow, invoice processing path, approval owners, and top non-core spend categories by department. Show where requests start, where vendors are approved, when a PO is issued (if one exists), and how invoices reach payment.

Use a simple check: trace five recent purchases from request to invoice. If you cannot show the approver, supplier record, and whether a PO existed before commitment, the baseline is incomplete.

Step 2. Inventory the full source-to-pay chain. Map every tool and handoff in your source-to-pay chain, including unofficial steps. Manual activity often stays hidden in email and spreadsheets until late in the process, so treat those as real operating steps.

Flag gaps like duplicate data entry, approvals outside the platform, or invoices arriving before requests are visible to finance.

Step 3. Document policy constraints before rollout. Write down where budget enforcement is mandatory, where exceptions are allowed, and who can accept risk when policy is bypassed. Be explicit about which categories or departments need hard controls versus documented exceptions.

Indirect procurement still covers business-critical operating spend, even when it is not sold to customers. If exception authority is vague, maverick and off-contract spend will keep being treated as urgency instead of policy breaches.

Step 4. Set monthly metrics you can verify. Start with approval cycle time, off-contract rate, late invoice count, and exception volume tied to audit risk. Use definitions your team can reproduce from the same records every month.

Consistency is the test. If two people calculate the same metric from the same evidence pack and get different answers, fix definitions first. Then, when you pilot PO automation and expand centralization, you will have a credible before-and-after view.

For more on long-tail spend, see Tail-End Spend Management: How Platforms Can Automate Long-Tail Contractor Payments.

Pick an ownership model before you buy more software#

Set ownership first, then buy software. If approvals, contracts, and exceptions are unclear, a new tool usually gives you cleaner intake with the same control gaps.

Indirect spend is distributed across departments and suppliers, so it should not run on a one-size-fits-all model. Use this rule: if spend is fragmented across many teams and contracts, use hybrid governance (central policy, local request owners). If control failures are severe, start centralized and relax later.

Step 1. Score the model against your failure pattern#

Use a simple comparison tied to your source-to-pay reality, not a "universal best" model.

| Ownership model | Approval workflow speed | Budget enforcement strength | Audit risk exposure | Where it fits |

|---|---|---|---|---|

| Centralized finance-led | Low to medium | High | Low | When control failures are visible and you need a single gate quickly |

| Federated team-led | High | Low | High | When teams already manage spend consistently and contract paths are clean |

| Hybrid governance | Medium to high | Medium to high | Medium to low | When spend is fragmented across teams, categories, and supplier contracts |

Use the same five recent purchases from the previous section and test each one: who approved the request, who owned the supplier contract, and who approved any exception. If any item has shared or unclear ownership, your model is still too vague.

Step 2. Assign hard ownership where requests drift#

Most breakdowns happen when many people touch a request but no one owns the decision. Name one accountable owner for each control point.

- Supplier contracts: keep ownership central (finance, procurement, or legal policy owners) for consistent standards.

- Purchase requisition approvals: assign to the role closest to budget accountability; in hybrid models, this is usually a department or cost-center owner, with finance setting routing and required controls.

- Exception approvals: keep ownership central and explicit; one named risk owner approves and logs exceptions that bypass normal policy.

If "business owner," "finance," and "ops" all share exception authority, risky spend usually gets reviewed too late.

Step 3. Treat vendor claims as inputs, not proof of fit#

Evaluate tools against your ownership design, not brand narrative. A ProcureDesk demo, an Ivalua page, or a sales deck can be useful input, but not evidence of fit.

Apply the same caution to analyst badges, including a 2026 Gartner Magic Quadrant for Source-to-Pay Suites mention. That is market context, not proof your approval flow, budget controls, and exception handling will work in your environment.

Require a written mapping to your ownership model: approval routing, exception authority, supplier contract linkage, and the records that prove requests followed the approved path. If a vendor cannot map that clearly, stop there.

Implement the minimum control stack in the first 60 days#

Use the first 60 days as a proof phase: lock the core controls in place and show measurable risk reduction before expanding scope. Keep the rollout in purchase sequence: requisition intake, approval routing, then PO before vendor commitment. This aligns with the broader first-100-days guidance to focus on proof over reinvention.

| Control area | Rule or fields | Evidence |

|---|---|---|

| Purchase requisition intake | Use one intake path; keep fields decision-critical: business purpose, supplier, expected amount, cost center, contract reference if available, and approver | If adoption is weak, simplify immediately and keep contract reference and approver |

| Approval workflow routing | Route by budget or cost-center owner, keep exception approval centralized, and do not allow requesters to pick approvers | Record request date, approver identity, approval timestamp, and exception notes in one place |

| PO before vendor commitment | No supplier commitment, kickoff, renewal, or invoice submission without an approved PO | If the PO is created after work starts, treat it as backfill, not control |

| Additional controls | Add guided buying, then links to supplier contracts, then automated invoice match checks once request and PO data are reliable | Where documents specify invoice submission instructions and Net 30 terms, carry those requirements into intake and invoice rules |

- Standardize purchase requisition intake first.

Use one intake path for new non-core requests in the category creating the most risk now. Keep the fields decision-critical: business purpose, supplier, expected amount, cost center, contract reference (if available), and approver. If adoption is weak, simplify immediately and keep only two non-negotiables: contract reference and approver.

- Enforce approval workflow routing second.

Route by budget or cost-center owner, and keep exception approval centralized. Do not allow requesters to pick approvers. Your record should show request date, approver identity, approval timestamp, and exception notes in one place.

- Require approved PO issuance before vendor commitment third.

Turn this on only after approval routing is stable. Make the rule explicit: no supplier commitment, kickoff, renewal, or invoice submission without an approved PO. If the PO is created after work starts, treat it as backfill, not control.

- Then add guided buying, contract links, and invoice checks in that order.

Start with guided buying rules, then require links to supplier contracts, then enable automated invoice match checks once request and PO data are reliable. Where your documents specify invoice destination and payment terms (for example, explicit invoice submission instructions and Net 30 terms), carry those requirements into intake and invoice rules so they are operational, not buried in documents.

Review these three metrics every sprint:

- Percentage of spend with PO coverage

- Percentage of invoices matched to approved requests

- Maverick spend trendline

Use the metrics as a decision rule. If teams bypass the tool, simplify fields before adding controls. If PO coverage rises but invoice matches lag, fix invoice processing and supplier compliance. If invoice matches improve but maverick spend stays flat, focus on off-path buying behavior before tightening more rules. One benchmark still reports a major indirect-spend visibility gap (65%), so cleaner intake alone is not enough evidence of control.

Tie procurement controls to payment and ledger evidence#

Procurement controls only work when each paid invoice can be traced through your own records, not just approved in intake. For each payment, keep one connected path from request and approval to purchase order (PO), invoice, payment record, and ledger entry.

| Control | Required records | Checkpoint |

|---|---|---|

| Link procurement and payment records | Keep request ID, PO number, supplier name, invoice number, payment reference, and journal reference intact; use durable references, ideally PO number plus invoice number | Pull 10 paid invoices from the last close and verify each one shows request, PO, invoice, payment reference, and journal entry |

| Reconciliation pack | Keep the approved PO list, paid invoice list, exceptions log, and unresolved mismatch report together each payment cycle | This gives you a clear view of what should have been paid, what was paid, what was allowed outside policy, and what still does not reconcile |

| Payout policy gates | Show KYC/KYB/AML or country/payee rule status in the procurement flow; keep payout status and retry handling visible in ops tooling | Requesters and approvers can see holds and ownership before invoices reach AP |

Before tightening controls, confirm which fields survive from procurement to accounts payable to finance. At minimum, keep these join points intact: request ID, PO number, supplier name, invoice number, payment reference, and journal reference. If any of these break between systems, you are recording intent, not producing audit-ready payment outcomes.

- Link procurement and payment records with stable shared references.

Do not match primarily on supplier name and amount. Use durable references, ideally PO number plus invoice number, while keeping the original request and approver visible in the same record.

Use a paid sample as the checkpoint, not a dashboard. Pull 10 paid invoices from the last close and verify each one shows request, PO, invoice, payment reference, and journal entry without manually rebuilding the story across teams.

- Require a reconciliation pack every payment cycle.

Keep four artifacts together each cycle: approved PO list, paid invoice list, exceptions log, and unresolved mismatch report. This gives you a clear view of what should have been paid, what was paid, what was allowed outside policy, and what still does not reconcile.

PO, receipt, and invoice linkage is the core control here. Vendor claims about linked records and pre-payment budget matching are useful benchmarks, but you still need to confirm your own process captures those links and exception reasons every cycle.

- Surface payout policy gates before money moves.

If your cross-border process already uses checks like KYC/KYB/AML or country/payee rules, show their status in the procurement flow so requesters and approvers can see holds and ownership before invoices reach AP.

Also keep payout status and retry handling visible in ops tooling to reduce manual re-entry risk. When these records stay connected, spend analysis becomes operational: a way to understand where money goes and support better budgeting, forecasting, and exception cleanup.

For more on ownership decisions, see Merchant of Record for Platforms and the Ownership Decisions That Matter.

Decide where to optimize for speed and where to enforce control#

Use one rule: speed for predictable, low-risk spend that is already controlled, and tighter gates for categories with higher operational or compliance exposure.

Classify spend before routing#

Build one routing table so each request is classified before approvals start. This keeps low-risk recurring spend out of the same path as higher-exposure requests.

| Spend class | Default control posture | Approval workflow depth |

|---|---|---|

| Low-risk recurring tools | Optimize for speed only when an active supplier contract exists and budget is visible | Light route, typically the business owner plus the relevant budget owner |

| Medium-risk service vendors | Balance speed with control | Standard route with business approval and budget enforcement before PO issuance |

| High-risk compliance-sensitive categories | Optimize for control first | Deeper pre-approval route with business owner, budget owner, and the relevant risk or finance reviewer before vendor commitment |

Sanity-check the table with recent requests from each class. If a request marked low risk still needs exception handling or creates invoice confusion, tighten that classification.

Speed up only the categories that are already controlled#

Loosen routing only when the basics are in place: an active supplier contract, contract reference on the request, and visible budget enforcement. If any of those are missing, keep the gate in place instead of accelerating by default.

A typical miss is treating a renewal as routine after pricing, scope, or payment terms changed. In that case, require a fresh review before PO issuance.

Set delay thresholds and review them monthly#

Define acceptable delay by spend class before rollout, then review performance monthly using failure data, not anecdotes. The tradeoff is straightforward: tighter controls can reduce off-contract purchases, but they can also increase cycle time.

Use the same operating evidence each cycle: approved PO list, paid invoice list, exceptions log, and unresolved mismatch report. Add class-level cycle time and bypass counts. If low-risk spend is clean but still slow, simplify the route. If medium- or high-risk spend keeps producing exceptions or mismatches, tighten controls.

Common failure modes and how to recover fast#

When controls slip, recover by tightening the exact handoff that failed: intake, approvals, or payment blocking. Keep the fix specific before adding more process.

Step 1. Simplify intake when teams bypass the procurement platform. If requests still come through email, chat, or card spend, your intake path is not clear enough. Keep only routing-critical fields (supplier, category, budget owner, and contract reference when it exists), then enforce PO-before-purchase for categories you already marked as controlled.

Use a weekly PO-to-invoice check: compare paid invoices against approved POs. If invoices keep landing without a matching PO, enforcement is failing in practice. Keep an exceptions log with a named owner and aging so bypasses stay visible.

Step 2. Redesign approval workflow tiers when bottlenecks are the problem. Do not route low-risk recurring requests through the same path as new service vendors. Pre-approve recurring categories only when an active supplier contract exists and capped budget enforcement is already in place; keep fuller review for the rest.

The March 2019 LA County purchasing manual is a useful structure reference because it separates Allowable Purchases, Prohibited Purchases, and Procurement Card Dollar Thresholds and Limitations. Do not treat its SAP range (5,001 up to 24,999) as a private-sector default. The practical takeaway is to define categories, caps, and prohibited cases explicitly, then review route aging by approver each month.

Step 3. Tighten invoice processing before mismatches become payment errors. For controlled categories, block payment unless the invoice includes both a PO reference and the relevant contract reference. That gives finance a hard stop instead of relying on vendor familiarity.

Keep a verification pack with the paid invoice list, unresolved mismatch report, and PO/contract references tied to each exception. A familiar vendor is not proof of a clean match when scope, pricing, or terms changed.

Step 4. Treat vendor claims as hypotheses, then run a 30-day pilot. Labels like "end-to-end procurement solution" or "source-to-pay" do not prove fit for your approval rules, exception ownership, or payment controls. Test the workflow against your actual policy logic, including prohibited purchases, capped recurring approvals, and payment blocks without PO coverage.

Track only what your own records can verify: approval cycle time, PO coverage, invoice-to-request match rate, and exception volume. If those do not improve, the demo narrative is not the operating reality.

This pairs well with our guide on How to Manage a Global Freelance Team Without Compliance Gaps.

What to do next without slowing the business#

Use the same evidence standard on your own process first: tighten control by reducing variation, not by adding more policy.

1) Map the current flow and mark where off-contract purchases enter#

Map how a non-core request actually starts today, then trace it through approval, PO creation, and invoice processing. Follow real channels (email, spreadsheets, chat, cards, renewals), not the policy diagram.

Keep the output to one page per priority category: requester, approver, contract location, whether a purchase requisition exists, and whether finance can see the request before invoice arrival. Then compare recent paid invoices against approved requests and supplier contracts to find your first off-contract failure points.

2) Standardize one purchase requisition path and one approval workflow#

Set one purchase requisition path and one approval workflow for all new non-core requests. Keep intake short so teams will use it; at minimum, require a vendor or contract reference and a named approver.

Your check is adoption: if requests still arrive through side channels ("just pay this one" emails, forwarded screenshots, ad hoc messages), the standard route is not yet operational.

3) Enforce PO-before-commitment for priority categories#

Require PO-before-commitment and contract-linked invoice processing in the categories with the most risk or volume. Do this first where unmanaged buying is already causing overspending, delays, or weak visibility.

Match every invoice to an approved request and current contract terms. Watch familiar vendors closely: renewals, scope changes, and seat increases are common ways off-contract spend re-enters.

4) Review monthly and adjust where data shows friction#

Review monthly and tune controls based on maverick spend, cycle time, and exception volume. Assign one owner to compare approved requests, POs, and paid invoices and explain gaps.

If cycle time rises without fewer exceptions, approvals may be too heavy. If maverick spend stays high, the issue is usually process bypass, not policy wording.

For a step-by-step walkthrough, see How to Manage Multiple Freelance Projects Without Losing Your Mind.

Frequently Asked Questions

What is indirect procurement for platform businesses?

Indirect procurement is the buying of goods and services that support daily operations rather than core production or delivery. For a platform team, that usually means operating purchases across functions that keep teams moving but are not the product itself.

How is non-core spend different from direct procurement in practice?

Direct procurement is tied directly to core delivery work such as client services, billable project work, or other spend attached to what you sell. Non-core spend is harder to track because it is not tied to a specific client, product, or project, so requests often arrive through many teams with separate vendors, contracts, and approvals.

Which controls reduce maverick spend the fastest?

Start with guided buying and budget enforcement, then support those controls with integrated supplier data so approved options are visible. If those controls are weak or inconsistent, maverick spend usually stays operational instead of policy-only.

Which workflows should be centralized first in a growing platform team?

There is no single operating model that fits every team. A practical starting point is to centralize intake and approval routing so cross-functional requests are visible, then tighten vendor and contract controls where buying is still reactive.

How do we balance approval speed with audit risk?

Do not send every request through the same approval path. Lower-risk recurring spend can move faster when budget enforcement is active, while new or unclear requests should keep fuller review to protect transparency and reduce audit exposure.

Do we need a full source-to-pay suite, or can we start with a narrower procurement software stack?

You can start narrower if the basics are still weak, especially when the focus is better visibility and tighter control of indirect spend. Move to a broader suite when your current setup cannot provide the data and analytics needed to prove your procurement strategy is working.

What proof should we ask for when a vendor claims better compliance and visibility?

Ask for proof in your own operating context and verify it using internal data and analytics. Analyst mentions such as the 2026 Gartner Magic Quadrant for Source-to-Pay Suites can be useful context, but they do not prove fit for your controls or outcomes.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- armedservices.house.gov/uploadedfiles/h.r._3838_fy26_ndaa_as_reporte...trusted

- congress.gov/committee-report/119th-congress/house-report...trusted

- dcps.dc.gov/sites/default/files/dc/sites/dcps/page_conte...trusted

- docs.legis.wisconsin.gov/document/statutes/16.pdftrusted

- lacounty.gov/wp-content/uploads/2022/03/Purchasing-Policy...trusted

- michigan.gov/-/media/Project/Websites/dtmb/Procurement/Co...trusted

- nvlpubs.nist.gov/nistpubs/specialpublications/nist.sp.800-161...trusted

- surface.syr.edu/cgi/viewcontent.cgitrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Choosing a Tail-End Spend Management Platform for Long-Tail Contractor Payments

Tail-end spend management can start to break down when long-tail contractor payouts begin to scale. Tools built for low-value, low-visibility procurement can tighten approvals and policy. They are not automatically built for payout-state tracking, retry safety, payout failures, or reconciliation evidence. That gap is the real decision here.

Procurement Data Management for Platforms: How to Centralize Vendor Contracts and Payment Terms

Treat every vendor contract and supplier agreement as a payment control, not a filing task. If a term can change approval, payout timing, or a payment hold, it needs to work inside your payment process, not sit in a PDF or get split across systems.

Material Procurement for Platforms: How Marketplaces Manage Raw Material Purchases and Supplier Payments

For platform teams evaluating **material procurement platforms marketplaces raw material purchases supplier payments**, the real question is whether you can keep control from start to finish. Can your workflow stay intact from internal request to supplier disbursement to ledger-ready evidence? If that chain breaks, finance inherits more manual review, ops inherits supplier friction, and engineering inherits avoidable exception handling.