Quick Answer

Choose payout-focused infrastructure when contractor payment risk starts after approval, and keep procurement-led tools when the main issue is off-policy buying. Evaluate each path on policy gates, audit trail depth, integration effort, cross-border compliance support, and exception handling. Then run one live trace that proves settlement status, return reasons, and reconciliation exports are connected. If retries can still create duplicates or status events are missing, use API-first payout rails or a hybrid stack.

What to Look For in a Tail-End Spend Management Platform#

Tail-end spend management can start to break down when long-tail contractor payouts begin to scale. Tools built for low-value, low-visibility procurement can tighten approvals and policy. They are not automatically built for payout-state tracking, retry safety, payout failures, or reconciliation evidence. That gap is the real decision here.

The distinction starts with scope. Tail spend solutions are framed around noncritical goods and services from vendors procurement does not actively manage, and tail spend management focuses on low-value purchases outside strategic spend. That framing is useful, including the common 80/20 heuristic, but it does not cover the full contractor payment lifecycle. In practice, the split looks like this:

- Spend control

Procurement workflows focus on approvals, policy compliance, purchase requests, invoicing, and visibility into unmanaged or off-contract activity. Procure-to-pay systems are built for that requisition-to-payment chain.

- Payout execution

Contractor payouts move through lifecycle statuses before funds are credited, and failure is a real state. Execution-focused infrastructure exposes status activity, for example through webhooks, so teams can see credited versus failed outcomes and recover with control.

- Reconciliation readiness

"Payment sent" is not enough if the records do not match. Reconciliation means matching transaction records to accounting records, with clear traceability for what was approved, attempted, settled, or failed.

Treat this as an operating-model choice, not a generic software shortlist. If your main issue is off-policy buying, a spend tool may be enough. If your issue is high-volume contractor payouts where duplicates, failed disbursements, or settlement delays create real risk, payout infrastructure should come first.

Two checks help prevent expensive mistakes. First, confirm the product exposes payout-state events your team can actually consume. Second, confirm retry behavior, including idempotent request support, so retries do not execute the same payment twice.

The document layer matters too. For U.S. independent contractors, onboarding starts with Form W-9. Reporting can require Form 1099-NEC once reportable thresholds are met. If TIN requirements are not met, backup withholding can be 24%. Cross-border operations add more friction because differences in laws, regulations, and practices increase both cost and risk.

The ranking that follows is about fit. Which path gives your team the right mix of policy control, audit-ready records, and payout reliability before small failures turn into month-end problems?

For a step-by-step walkthrough, see How MoR Platforms Split Payments Between Platform and Contractor.

Selection criteria and who this list is actually for#

Use this shortlist when the bottleneck is payout execution, not general low-value buying. If failure recovery, contractor onboarding, and month-end tie-out are business-critical, tools built for contractor payouts may fit better than generic tail spend management software. It is for teams that own one or more of these across a contractor base:

| Criterion | What to check | Article detail |

|---|---|---|

| Policy gates | Stop a payment at the right control points before release and during review | The real test is whether controls continue through payout release. |

| Audit trail depth | Approval history, payout references, failed-payout reporting, and transaction-level reconciliation exports | Finance should be able to trace approved, attempted, settled, and failed states. |

| Integration effort | What engineering is required for identity checks and tax-data capture | Do not assume provider verification covers your independent legal obligations. |

| Cross-border compliance support | Checks for required originator and beneficiary information | Confirm whether cross-border controls are first-class or an afterthought. |

| Exception-handling clarity | Failed-payout outputs and return-reason classification | ACH return codes require scenario-specific handling; some return windows can be as short as 2 days after settlement. |

- Contractor onboarding where Form W-9 collection, tax identity checks, or cross-border data requirements may gate payout.

- Payout orchestration where retries, failed disbursements, and duplicate prevention matter more than basic invoice approval.

- Month-end reconciliation where finance needs transaction-level evidence, not just a paid or unpaid flag.

This list is not for teams whose main issue is petty cash, e-marketplace purchases, or office tactical buys with no meaningful payout-state complexity. Tail spend scope varies by category, and the classic 80% / 20% pattern describes transaction mix, not whether contractor payment risk is covered. Judge each option on five practical criteria:

- Policy gates

Can you stop a payment at the right control points before release and during review? In P2P flows, requisitions should follow procurement policy approvals. The real test is whether controls continue through payout release.

- Audit trail depth

"Payment sent" is not enough. Look for approval history, payout references, failed-payout reporting, and transaction-level reconciliation exports so finance can trace approved, attempted, settled, and failed states.

- Integration effort

Compliance-heavy onboarding is often the hidden cost. Verify what engineering is required for identity checks and tax-data capture, and do not assume provider verification covers your independent legal obligations.

- Cross-border contractor compliance support

Confirm checks for required originator and beneficiary information. The question is whether cross-border controls are first-class or an afterthought.

- Exception-handling clarity

Ask to see failed-payout outputs and return-reason classification. ACH return codes require scenario-specific handling. Some return windows can be as short as 2 days after settlement.

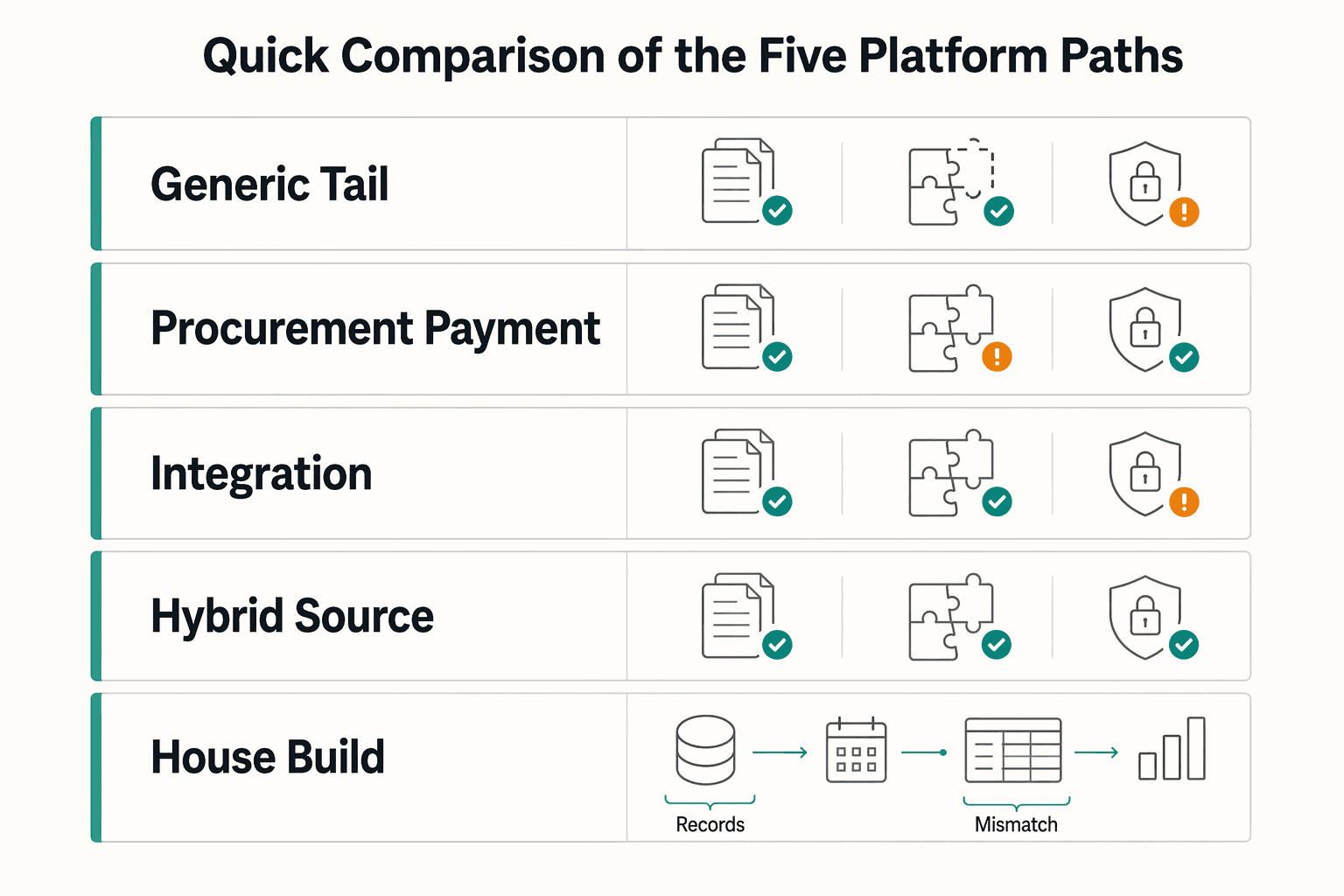

Quick comparison of the five platform paths#

If your pain starts after approval, prioritize payout operations over procurement coverage. In payout-heavy environments, the decision often narrows to API-first payout infrastructure or a hybrid stack. The other paths can fit, but usually within tighter constraints.

| Platform path | Best for | Control depth | Speed to launch | Engineering lift | Operational risk | Unknowns to validate | Finance handoff burden |

|---|---|---|---|---|---|---|---|

| Generic tail spend management software | Teams improving control over unmanaged purchasing across noncritical goods and services | Procurement-focused spend control, with limited proof of contractor payout-lifecycle depth | Can be faster when procurement workflows already exist | Low to moderate | Higher if you need native contractor payout-state handling | Request evidence of contractor onboarding checks, failed payout reporting, retry handling, and beneficiary-level status. Category positioning is procurement-centric, not payout-specific. | Can be heavy. Approval records may exist, but finance can still chase settlement status and exceptions outside the tool. |

| Procurement-to-payment platform suites | Enterprises standardizing procurement and invoicing controls in one platform | Strong upstream governance across procurement and invoicing | Moderate | Moderate | Can rise when payout exceptions drive risk | Verify whether contractor payouts are first-class workflow objects or just payment outputs. Public positioning for Order.co and Coupa emphasizes procure-to-pay and purchasing or payment workflows in the reviewed excerpts. | Medium to heavy unless transaction-level payout evidence, return reasons, and close-ready exports are available. |

| API-first payout infrastructure | Product, engineering, and payments ops teams managing high-volume contractor or marketplace disbursements | High payout-state control with documented event and retry mechanisms | Moderate | Moderate to high | Lower for payout reliability when event or retry controls are in place, with separate risk for procurement-reporting gaps | Confirm webhook or event coverage, idempotent request support, non-domestic payout support, and reconciliation report availability. Also confirm what onboarding and compliance data you still own. | Lighter when payout reconciliation reports and status events are usable; heavier if finance must manually stitch API data into ERP reporting. |

| Hybrid source-to-pay software plus payout stack | Organizations needing procurement policy control and payout-state depth without a full custom build | High if ownership boundaries are explicit | Moderate to slower | High | Moderate, mainly at integration seams | Lock source-of-truth rules early: approval owner, payout-state owner, and final audit-export owner. Ivalua's S2P positioning is broad, but that alone does not prove contractor payout exception depth. | Medium when reconciliation artifacts and exception ownership are designed up front; heavy when handoffs are unclear. |

| In-house build with selected vendor primitives | Mature teams with differentiated payout logic and strong engineering ownership | Potentially highest | Often slower | High | High if maintenance and compliance ownership are weak | Validate whether you truly need custom policy logic, corridor-specific behavior, or internal risk scoring. Otherwise you may rebuild webhook handling, retries, and reconciliation already available from providers. | Potentially strongest long term, but heavy at launch since finance depends on your export layer, case handling, and audit lineage. |

What this comparison is really saying#

The real dividing line is scope. Tail spend definitions are procurement-led, so they do not automatically prove depth in payout retries, returned payments, or contractor-level status history. If month-end pain shows up after approval, a procurement-first category may be the wrong anchor. That is why Mekari Expense, Order.co, Coupa, and Ivalua need explicit validation for contractor payout operations. In the reviewed public excerpts, their messaging focuses on expense, procurement, invoicing, or broad S2P coverage, not detailed contractor payout-state handling.

The path that usually wins when payouts are product-critical#

API-first payout infrastructure is often the strongest fit when payout execution is part of your product promise. Idempotent requests and payout webhooks support retry safety, duplicate prevention, and status-driven exception handling.

The tradeoff is straightforward. You can get stronger payout control, but procurement policy and internal spend reporting may live elsewhere. Before you commit, confirm the finance evidence pack supports close across approved, attempted, settled, and failed states.

When hybrid beats pure payout infrastructure#

Hybrid wins when procurement governance is non-negotiable but payout complexity goes beyond suite-native depth. It works best when you assign three owners before integration starts: approvals, payout state, and reconciliation exports.

Use a simple rule. If your biggest risk is off-policy spend, start from S2P or P2P and add payout depth. If your biggest risk is failed or opaque disbursements, start from payout infrastructure and layer procurement reporting around it.

You might also find this useful: What Is Spend Management? A Platform Operator's Guide to Controlling Contractor Costs.

Option 1 generic tail spend tool with contractor workaround#

Use this as an interim path, not a long-term payout architecture. It fits when procurement already runs tail spend analysis, your contractor cohort is still small, and the immediate goal is tighter approvals and spend visibility.

- Best for: teams already using tail spend controls that need a fast interim lane for contractor payouts.

- Pros: faster visibility, more consistent approval policy, and pressure to consolidate vendors.

- Cons: limited depth for contractor onboarding, payout-state tracking, and cross-border contractor compliance.

- Concrete use case: off-policy spot purchases plus a small domestic contractor cohort while you scope a dedicated payout layer.

Where it helps first#

This helps most when consistency is the real problem. Procure-to-pay is built around requisition through payment and policy compliance, so it can help centralize ad hoc requests, enforce approvers, and improve supplier discipline.

If your immediate pain is off-policy requests and scattered contractor invoices, a generic spend tool can pull that activity into one approval lane quickly. That is a real operational gain, even if payout operations remain shallow.

What the workaround usually misses#

The weakness shows up after approval. Contractor onboarding is more than a supplier record. For U.S. independent contractors, the first step is Form W-9, which the IRS says to retain for four years. Foreign payees may require Form W-8 BEN when requested by the payer or withholding agent. Attaching files is not the same as a purpose-built onboarding flow that collects and verifies recipient identity or business details.

Payout-state handling is the second gap. Payout platforms use status events and webhooks to show transfer progress and changes. A procurement-first tool may show approved or exported payments, but that does not by itself confirm payout outcomes such as settled, returned, or failed.

The operator checkpoint that matters#

Before you treat this as workable, run a single-contractor trace test through approval and settlement. You should be able to produce, in one place:

- approved request or invoice record

- contractor tax form, for example a W-9

- payee destination details confirmation

- payout attempt date

- final settlement status, or return or failure reason

If finance has to stitch that together from email, ERP exports, and bank notices, you do not have a durable payout process. You have an approval front end.

When to stop stretching it#

The failure mode is predictable: visibility improves, but payout exceptions stay opaque. Returned payouts are often caused by incorrect destination information, and those cases are harder to resolve without event-driven status handling. Cross-border payees can add additional documentation, withholding requirements, and ongoing compliance maintenance burden.

Use this path for a small domestic cohort while you design a dedicated payout layer. If payout returns or failures are recurring, stop treating this as a long-term architecture.

Related: Maverick Spend in Platforms: How to Stop Off-Contract Contractor Payments Before They Drain Margin.

Option 2 procurement-to-payment suite as the system anchor#

This can be the right anchor when enterprise governance matters most, but only if contractor payout lifecycle records are treated as first-class in the suite.

- Best for: organizations standardizing procurement controls where a Procure-to-pay or Source-to-pay operating model is the top priority.

- Pros: strong control over requisition-to-payment workflow, policy compliance, and linked procurement records.

- Cons: can break down for contractor payouts if failures, returns, and beneficiary-level status live outside the core record model.

- Concrete use case: a central procurement transformation that extends existing tail-end spend governance into contractor spend while separately validating payout lifecycle operations.

P2P and S2P suites are built to govern how spend enters and moves through the business. That makes them strong when the immediate risk is inconsistent intake, weak approvals, and fragmented record lineage.

The main risk shows up after approval. Contractor payout operations can be asynchronous, include executed and failed states, and surface returns days later. A suite that stops at approved or exported payments may improve procurement discipline without giving you reliable payout operations.

The validation test before you commit#

Run one live contractor trace end to end and confirm the suite can show final settlement or failure handling without relying on disconnected exports. Before signing, validate that you can see:

- contractor or beneficiary details as a native record, not only attachments

- payout-state changes captured in-platform as first-class events

- failed or returned payouts visible with enough detail for operations and reconciliation

- one evidence chain tying approval, payable record, payout reference, and final status

If the demo ends at approval or file export, treat it as procurement control, not full payout lifecycle ownership.

Option 3 API-first payout infrastructure for contractor-heavy platforms#

Choose API-first payout infrastructure when payout execution is customer-facing and failures such as duplicate payouts, delayed status visibility, or cross-border payout issues are unacceptable. If your trace breaks after approval or file export, this is usually the better anchor.

This path fits product and engineering teams that treat contractor payments as an operational surface, not just a finance workflow. Procurement-to-payment or source-to-pay tools can still handle approvals, but the center of gravity shifts to payout orchestration, event handling, and contractor-level status tracking.

Why this path fits contractor-heavy platforms#

API-first providers are built for platforms moving money between multiple parties. Stripe Connect is explicitly positioned for that model, and its cross-border payouts documentation covers paying sellers, freelancers, content creators, and service providers in local currencies.

The practical difference is state handling. Webhook-driven asynchronous events let your system track what happens after initiation instead of treating submission as completion. In practice, outcomes can change after initiation, and some platform webhooks expose outcome fields such as data.status.

What you gain, and what it costs#

You gain tighter execution control, but you pay for it with real integration work. If procurement visibility is the real goal, that effort may be unnecessary.

- Execution controls: idempotent request patterns reduce duplicate payout risk on retries. Stripe supports idempotency keys up to 255 characters and notes keys can be pruned after at least 24 hours, so key lifecycle design has to be explicit in your records.

- Operator levers: PayPal Payouts supports up to 15,000 payments per call, rejects reused

sender_batch_idvalues within 30 days, and supports status lookup viapayout_batch_id. - Tradeoff: Stripe's onboarding guidance shows the API onboarding path as the highest-effort option and one that can delay go-live. Expect additional build work across onboarding, webhook ingestion, retries, exception handling, and internal reconciliation or reporting flows.

What to verify before you commit#

Do not choose this path off a brand demo. Validate it with a live or sandbox trace, and confirm that:

- retry protection is implemented in payout creation logic, not only documented

- asynchronous status events are stored and tied to contractor and payout references

- cross-border onboarding includes compliance and verification handling, since verification is explicitly complex and regulatory requirements evolve

Your evidence chain should connect contractor identity, onboarding status, payout request, provider reference, event or batch outcome, and reconciliation export. If those records live in disconnected logs or CSVs, month-end operations will absorb the gap.

API-first infrastructure is typically stronger at payout execution than procurement reporting, so approvals and spend categorization may need separate modeling. If payout reliability is the bigger business risk, this is the right option. If not, a hybrid model is usually the better next step.

If you want a deeper dive, read Vendor Data Management: How Platforms Keep Contractor Payment Details Accurate and Compliant.

Option 4 hybrid stack with source-to-pay control plus payout rails#

Use a hybrid stack when you need procurement control and payout operations depth at the same time.

- Best for: teams that need S2P policy governance and contractor payout execution.

- Pros: S2P handles approvals, policy, and spend controls; payout rails handle post-initiation state, reversals, reporting, and contractor-level outcomes.

- Cons: integration seams can create ownership ambiguity unless finance, ops, and engineering define record authority up front.

- Concrete use case: procurement owns tail spend controls, while payments ops runs contractor payouts with status visibility and exception handling.

This split works because the systems are built for different jobs. S2P is designed to carry procurement from sourcing through payment with policy discipline. Payout infrastructure handles execution after initiation, where states such as processing, posted, failed, returned, and canceled need to be tracked reliably.

The four decisions that make or break it#

- Approval authority

Let S2P own approvals, spend policy, and release conditions. Keep the approval trail in one authoritative place.

- Payout-state authority

Let payout rails own execution status after initiation. If systems disagree on payment state, the payout rail should be the execution system of record.

- Reconciliation authority

Define which export finance uses to reconcile transactional and accounting records before and after general-ledger posting. Reconciliation is not just proof of approval.

- Data harmonization rule

Write down system-of-record and source-of-truth roles explicitly: which tool owns approvals, which owns payout state, and which produces the reconciliation view when records conflict.

The main risk and the practical control#

The core failure mode is not just integration effort. It is ownership ambiguity. When teams assume different systems are authoritative, conflicting or outdated records spread and reporting errors follow.

Prevent that with a short pre-launch RACI: one accountable owner for approval records, one for payout-state ingestion, and one for reconciliation exports. Then run a full payment trace, including an exception path. Confirm the payment was approved in S2P, the payout was created once, idempotency retry controls worked, payout events were captured, and the reconciliation output ties transactional and accounting records together.

If procurement governance and payout execution detail both matter, hybrid is a strong fit. Decide record authority first, not after integration. Related reading: How to Write a Payments and Compliance Policy for Your Gig Platform.

Option 5 in-house orchestration with selected vendor primitives#

Choose this option only when custom payout logic is part of your product differentiation. If the main issue is slow vendor evaluation, this is often the wrong tradeoff because in-house orchestration brings high delivery effort and ongoing maintenance ownership.

Best for#

This fits mature teams that need onboarding, internal risk scoring, approval policy, and payout release rules in one controlled layer. It is most defensible when contractor payouts depend on conditions generic tools do not model well, such as corridor-specific eligibility, work-type restrictions, or country-specific document checks.

Pros#

- Full control over policy logic, exception routing, and payout decisioning.

- Ability to keep onboarding requirements, fraud vetting, payout holds, and exception handling in one orchestration layer.

- Flexibility to use vendor primitives for rails or identity while keeping internal control over release logic.

Cons#

- High ongoing ownership burden across security updates, integration maintenance, and compliance operations.

- API-led onboarding flows must be updated when provider requirements change.

- Cross-border scope expands quickly because international flows add currency, regulatory, and compliance complexity.

- Depending on configuration, platform-controlled account models can require you to handle requirements collection and carry loss-liability exposure.

Concrete use case#

A platform with complex eligibility rules and market-specific cross-border contractor compliance constraints that generic off-the-shelf flows may not cover well.

Operator checks before you commit#

- Verification checkpoint: Run one end-to-end corridor test from contractor onboarding to payout creation and reconciliation. Retry the same payout request with the same idempotency key and confirm only one payout is created.

- Control evidence: Keep a record set with onboarding requirements snapshot, approval reference, payout reference, exception reason code, if any, and final settlement status.

- Failure mode to plan for: If country-specific onboarding requirements change and your API flow is not updated, onboarding and payout readiness can be disrupted and exception volume can rise before finance sees the close impact.

Decision rule: Build only when custom payout logic is product-critical, not just because vendor evaluation is slow. If your platform wins on specialized eligibility and compliance handling, this route can be worth it, but only with explicit ownership for requirements updates, fraud controls, and reconciliation evidence.

Non-negotiable controls before you scale payouts#

Scale exposes control gaps before it rewards speed. For contractor payouts, five controls are worth prioritizing: onboarding eligibility, idempotent initiation, release checks, exception coding, and end-to-end reconciliation lineage.

| Control | Required check | Practical proof |

|---|---|---|

| Onboarding eligibility | Verification must be complete before payments or payouts are enabled | Leave one requirement incomplete and confirm the contractor remains blocked until status changes. |

| Idempotent initiation | One idempotency key per payout intent stored with the internal approval reference | Simulate a timeout and resend the same request; you should still get one payout object. |

| Release checks and exception reasons | Before release, confirm the contractor is still eligible, verification is still satisfied, and no new block was added | If a payout is blocked, record a reason code, timestamp, and owner. |

| Evidence pack | Connect the approval trail, payout request, provider payout reference, exception reason code, if any, and final settlement evidence | Use a canonical lineage: approval ID -> payout request ID -> provider reference -> settlement batch or file identifier -> bank statement line. |

| Vendor validation | Ask for concrete artifacts before signing | Request a reconciliation export sample, a payout exception reason-code list, and evidence of how verification status affects payout eligibility. |

- Gate contractor onboarding before funds can move.

Treat onboarding as a hard policy gate, not a form step. In some platform payment stacks, verification must be complete before payments or payouts are enabled, and added checks can temporarily disallow payouts. Your release logic should check live verification status, not rely on an old approval snapshot. A practical test is to leave one requirement incomplete and confirm the contractor remains blocked until status changes.

- Make payout initiation idempotent and block duplicate paths.

Retry safety becomes more important as volume rises. Idempotent requests let you repeat the same request without creating a second object, so require one idempotency key per payout intent and store it with the internal approval reference. Then simulate a timeout and resend the same request. You should still get one payout object. If different callers can create the same payout with different keys, add a second duplicate check on the approval reference before release.

- Run a release check and write machine-readable exception reasons.

Approval is not the last control. Before release, confirm the contractor is still eligible, verification is still satisfied, and no new block was added after initiation. If a payout is blocked, record a reason code, timestamp, and owner instead of leaving a generic failed or pending state. This helps keep finance and ops from mixing data-fix issues with risk holds or provider-side returns.

- Define one evidence pack that survives audit and close.

Your evidence chain should connect the approval trail, payout request, provider payout reference, exception reason code, if any, and final settlement evidence. Reconciliation should tie bank payouts back to payment batches, with transaction-level traceability and metadata where available. Use a canonical lineage before rollout: approval ID -> payout request ID -> provider reference -> settlement batch or file identifier -> bank statement line. If any link is manual, close can be slower and less reliable.

- Treat vague vendor claims as validation tasks, not buying criteria.

Procurement-centric tail-spend framing does not prove contractor payout depth. If Gartner Peer Insights or vendor pages do not show operational detail, log that as an open validation item. Ask for concrete artifacts before signing: a reconciliation export sample, a payout exception reason-code list, and evidence of how verification status affects payout eligibility.

If you only tighten one discipline first, make it reference lineage tied to idempotent creation and settlement proof. That is what makes each payout auditable, safely retryable, and reconcilable.

This pairs well with our guide on How to Embed Payments Into Your Gig Platform Without Rebuilding Your Stack.

If this checklist is becoming your implementation spec, use Gruv's Payouts docs to map policy gates, status events, and reconciliation handoffs before rollout.

Implementation sequence and ownership by function#

Once the controls are defined, start with a narrow slice and expand as status handling and reconciliation stabilize.

| Stage | Primary focus | Before moving on |

|---|---|---|

| Map the real money path | Trace approval, release, provider reference, settlement batch or file, and bank statement line | Document one operating flow that includes approvals, status tracking, failures, and reconciliation. |

| Classify failures | Separate internal policy blocks from provider-side or bank-side failures | Route each class to a defined response path instead of a generic payment failed bucket. |

| Set policy gates and ownership | Assign one owner per stage for release controls, evidence requirements, exception follow-up, retry safety, and event reliability | One named owner per stage reduces the risk of stalled payouts with no accountable team. |

| Integrate event and status handling | Use webhook events, or equivalent asynchronous status delivery, so internal state tracks real payout changes | Test delayed returns after an apparent success. |

| Automate reconciliation and expand in phases | Start with one corridor or one contractor segment | Before expanding, verify reconciliation outputs and payout-ledger exports agree on counts, amounts, and final statuses. |

- Map the real money path first.

Trace one contractor payment end to end: approval, release, provider reference, settlement batch or file, and bank statement line. Payment operations covers the full lifecycle of money movement, so document one operating flow that includes approvals, status tracking, failures, and reconciliation, not just initiation.

- Classify failures before you automate responses.

Separate internal policy blocks from provider-side or bank-side failures. For ACH, treat error-claim returns and no-authorization claims as different cases. Nacha's phased differentiation is a useful reminder that exception categories need to be specific. Route each class to a defined response path instead of dumping everything into a generic "payment failed" bucket.

- Set policy gates and assign one owner per stage.

Assign clear ownership for release controls and evidence requirements, exception follow-up, retry safety (idempotency) and event reliability, and service-level expectations for states such as pending, returned, and paid. The exact split will vary, but role clarity is a control requirement. One named owner per stage reduces the risk of stalled payouts with no accountable team.

- Integrate event and status handling before broad launch.

Use webhook events, or equivalent asynchronous status delivery, so internal state tracks real payout changes. Test asynchronous status handling, including delayed returns after an apparent success. Your ledger and exception queue should update when status changes, not only during later finance review.

- Automate reconciliation, then expand in phases.

Start with one corridor or one contractor segment. Use payout-batch reconciliation where available, and use lifecycle-status reporting when invoice reconciliation depends on status-level detail. If you phase rollout, a pattern like advisory, testing, then closed-loop production is one example. Before expanding, verify reconciliation outputs and payout-ledger exports agree on counts, amounts, and final statuses.

If exceptions in the first corridor grow faster than payout volume, pause expansion and fix ownership, classification, or record lineage first.

Failure modes that quietly destroy margin#

Once ownership is clear, margin often leaks through poor status visibility. If approvals look clean but payout states are unclear, you may not be controlling contractor payouts yet.

- Approval looks healthy, money movement does not

Procurement-centric tail-spend coverage is not the same as payout control. Market definitions focus on noncritical goods and services and vendors not actively managed by procurement, which helps policy and buying discipline but does not, by itself, confirm payout-lifecycle depth.

Run one practical test: can you trace an approved contractor invoice to a provider reference, settlement batch, and bank statement line? If not, approvals are working as a front-end filter, not as a complete operating record for payouts. A practical differentiator is beneficiary-level status visibility: pending, paid, returned, rejected, or under review.

- Unmatched payout states turn close into investigation work

Reconciliation drag can rise when systems disagree on status and teams cannot connect exceptions back to the original contractor record. Payment flows explicitly route transactions into type-specific exception queues when exceptions occur, so backlog growth is a practical operational risk.

The differentiator is whether you reconcile from lifecycle-status and payout-batch outputs, not just invoice approval status. If manual matching work keeps rising, treat it as a control gap.

- Weak contractor onboarding creates payout holds at release time

Compliance failures can surface late, at payout. A payee can clear commercial approval and still be blocked because verification requirements are incomplete. Some platform models explicitly include timelines for pausing payouts and payments when requirements are not met.

The hard edges are concrete. If a required taxpayer identification number is missing, backup withholding must begin immediately on reportable non-payroll payments. If a sanctions-related transaction is rejected, a report must be submitted to OFAC, and related records must be kept for 10 years. In cross-border payment flows, inconsistent data usage and misaligned message flows add downstream friction.

- Fragmented records erase consolidation gains

Consolidation gains can erode when identity, approval history, and payout records live in separate systems. Fragmented data creates consolidation and accessibility problems, and manual reconciliation on top of that delays financial insight.

Set clear record authority: which system owns contractor identity, which owns payout state, and which IDs must match across systems. If legal name, tax profile, contractor ID, and payout reference do not align across exports, duplicate investigations and payment errors become easier to introduce.

If exception queues grow faster than payout volume, treat it as a warning to tighten state visibility first: typed exceptions, traceable references, and one connected record from contractor identity to payout outcome.

Conclusion#

The right choice is not the broadest tool category. It is the architecture that matches your payout complexity and control requirements.

- If you mainly need procurement visibility, stay procurement-led.

Use a tail-spend or procurement-to-payment approach when the core problem is off-policy buying and unmanaged low-value activity. Tail spend is procurement-centric by definition: high-volume, low-value, noncritical purchases from vendors procurement does not actively manage. Decision test: if finance can already trace an approved contractor invoice to payout and accounting records without cross-team chasing, this path can still fit.

- If you need payout traceability, choose payout depth first.

When retries, returns, and contractor-level status handling drive daily operations, approval visibility alone is often not enough. You need transaction-level outcomes that support reconciliation, not just batch-level success. A practical check is status structure: ISO 20022 pacs.002 reports whether a payment was accepted or rejected, and ISO 20022 message formats are designed to support automated end-to-end processing. If that level of visibility is missing, you still have only partial control.

- Make ownership explicit before scale makes it expensive.

Architecture risk rises when responsibilities are blurred. Assign clear ownership for approval, payout execution, and reconciliation review, and keep one evidence chain from approval to payout outcome. That aligns with internal-control guidance to separate posting, reconciliation, and review duties. It also fits the broader direction of payment-rule expectations around message responsibility, transparency, and fraud monitoring.

If you are deciding between paths, use this rule of thumb. When payout failures are visible to contractors or reconciliation depends on manual investigation, prioritize the path with first-class payout traceability, explicit control ownership, and routine reconciliation.

When you are deciding between generic spend tooling and payout-first infrastructure, use a short scoping call to confirm market coverage and control ownership with Gruv.

Frequently Asked Questions

What is tail-end spend management for contractor payments?

Tail spend management usually means controlling high-volume, low-value purchases outside core strategic categories. For contractor payouts, that definition is often incomplete on its own. You still need policy control, payout-state visibility, reconciliation records, and contractor data checks that hold up after approval.

When do long-tail contractor payouts become an operational risk instead of a finance nuisance?

There is no universal transaction-count breakpoint. It becomes an operational risk when your team cannot trace an approved invoice to payout and accounting records without manual investigation. If exception queues grow faster than payout volume, or asynchronous status updates arrive but are not captured cleanly, you have a control gap.

What capabilities are table stakes in a platform handling long-tail contractor payments?

At minimum, look for contractor onboarding records, beneficiary-level payout states, typed exception handling, reconciliation exports, and duplicate-prevention behavior. Idempotency matters because retries should not create a second payout, and webhook handling matters because outcomes often arrive asynchronously. If a vendor cannot show clear contractor-level payout outcomes and exception paths, treat that as a red flag.

How should approvals and policy gates work when payout volume spikes?

Use stage-based controls: onboarding, payout initiation, release, and post-payout reconciliation. In the U.S., the first contractor tax step is Form W-9 collection for domestic payees, and Form W-8 BEN may be required for foreign beneficial owners when requested by the payer. If required taxpayer information is missing for a U.S. payee, backup withholding at 24% may apply, so do not leave tax checks until release day.

How do we choose between generic tail spend tools and payout-focused infrastructure?

Choose generic tools when the main issue is approval discipline across many low-value transactions and contractor complexity is still low. Choose payout-focused infrastructure when beneficiary-level status, retries, webhook events, and reconciliation timing are business-critical. If payout failures are felt directly by users or contractors, procurement-first tooling may be too shallow for the operating core.

What records do we need for audit and reconciliation readiness?

Keep one evidence chain from contractor identity to payout outcome: approval trail, contractor ID, tax form, payout reference, exception reason, settlement export, and bank-statement tie-out. For U.S. contractor files, keep Form W-9 for 4 years, and remember Forms 1099-NEC must be e-filed if you file 10 or more information returns in a calendar year. If vendor controls matter for financial reporting, request a SOC 1 report and confirm which controls are relevant to your reconciliation process.

What unknowns should we validate before signing a vendor?

Ask for product proof, not category language. Require a live walkthrough of retry behavior, idempotency-key handling, exception exports, webhook payloads, and how batch-level versus transaction-level statuses are represented. Validate any tax-threshold claims against current IRS pages directly, especially where public claims conflict with long-used 1099-NEC reporting guidance.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/bppdf/bispap167.pdftrusted

- dol.gov/agencies/whd/flsa/misclassification/rulemakingtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-V/part-501trusted

- federalregister.gov/documents/2024/05/10/2024-10033/reporting-pr...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-3-establish-structu...trusted

- irs.gov/businesses/small-businesses-self-employed/fo...trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

- law.cornell.edu/cfr/text/31/501.604trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Keep Contractor Payment Details Accurate and Compliant

Reliable contractor payouts start with controlled vendor data, not the payout click. What looks like a payout failure is often an upstream record problem, and ACH return codes like `R03` and `R04` only make that visible once a payment is processed.

Maverick Spend in Platforms: How to Stop Off-Contract Contractor Payments Before They Drain Margin

Off-contract contractor payments become dangerous when they repeat. Small off-policy spend adds up, fragments data, and weakens compliance. Teams usually discover it later during invoice review, audit, or reconciliation.

Contractor Spend Management: Total Cost and Payout Controls

For platform operators, contractor spend is not a simple software seat decision. The real cost shows up in money movement, verification gates, failed or delayed payouts, and the finance time required to reconcile what actually happened against what should have happened. That mismatch often starts with the accounting boundary between [accrued expenses and accounts payable for contractor liabilities](/blog/accrued-expenses-vs-accounts-payable-contractor-liabilities-platform).