Quick Answer

A strong material procurement platform for marketplaces keeps one traceable control line from requisition to PO to approved bill to payment approval to reconciliation-ready evidence. The best options make approval states explicit, support supplier onboarding and compliance controls, expose machine-readable payout states, and produce reconciliation outputs finance can use without manual reconstruction, especially for cross-border supplier payouts.

How material procurement works on platforms#

For platform teams evaluating material procurement platforms marketplaces raw material purchases supplier payments, the real question is whether you can keep control from start to finish. Can your workflow stay intact from internal request to supplier disbursement to ledger-ready evidence? If that chain breaks, finance inherits more manual review, ops inherits supplier friction, and engineering inherits avoidable exception handling.

Raw-material procurement is broader than a checkout flow. It usually spans forecasting or planning, supplier sourcing, contract negotiation, purchase orders, inventory management, and payment processing. In practice, you are connecting procurement decisions, AP controls, and payout execution across entities, countries, or both.

A useful shortlist should be tested against three operating checkpoints, not vendor feature marketing:

- Requisition to PO

A Purchase Requisition is an internal request to buy goods or services. A Purchase Order (PO) is the formal buyer-issued order sent to a supplier. They are different controls, and the request-to-PO handoff is a real approval checkpoint. Once the request is approved, the PO is issued. If a platform blurs this step, you lose an early Source-to-Pay control point.

- Invoice approval to payment release

Capture is not payment approval. In enterprise AP workflows, supplier bills are reviewed and approved after entry or receipt, with matching and workflow used to auto-approve eligible items and escalate exceptions. A key control is three-way match before payment: invoice, PO, and receiving report. Release can also require approver review before final supplier disbursement. Practical rule: if you cannot see exactly which approval state unlocks payment, reject the option.

- Payment evidence to reconciliation

A "paid" status is not enough. You need evidence that supports reconciliation of payables subledger balances to the general ledger. At minimum, that chain should include the approved request, issued PO, approval record, three-way match result where applicable, payment approval record, and reconciliation-ready records. If one owner cannot assemble this quickly at month-end, the stack is likely not under control.

This article compares procurement options by execution risk first, especially for cross-market supplier payouts. Cross-border payments have been a G20 policy priority since 2020, with most global quantitative targets set for end-2027. Official progress reporting still says the work has not yet produced tangible global end-user improvements. Teams still face diverging regulatory frameworks, AML complexity, data restrictions, and interoperability frictions.

Throughout this guide, the standard is simple: preserve traceability from Requisition to PO to approved billing to payment approval to reconciliation. Be explicit about implementation effort and control depth. By the end, you should have a shortlist you can act on, plus checkpoints and failure controls that keep supplier payments from turning into a finance cleanup exercise.

Selection Criteria That Actually Matter for Platform Teams#

For platform teams, the shortlist is really a control test. The right option keeps a clear chain from internal approval to supplier payout to reconciliation evidence.

This section is aimed at marketplace-style procurement across entities or borders, where approval workflow controls, supplier onboarding, and API-linked finance operations have to stay connected. If you issue POs, review supplier bills, pay suppliers across markets, and rely on API or webhook status updates, treat these criteria as non-negotiable.

If you run a single legal entity with mostly domestic AP, a small supplier base, and low payment complexity, you may not need this full operating model. KYC, KYB, and event handling can still matter, but they may not be your first selection gates.

The six gates#

| Gate | Focus | What to verify |

|---|---|---|

| Source-to-Pay depth | Request to PO to approved billing | Confirm approval ties back to PO lines and, where applicable, three-way matching against product receipt lines |

| Supplier Onboarding | Pre-transaction supplier data | Collect tax IDs, banking details, and compliance documents; compliance review may also require beneficial-owner identification and verification procedures |

| Payment execution | Cross-border payout states | Verify machine-readable states such as paid, failed, and canceled, plus programmatic disbursement support at your required scope |

| Reconciliation quality | Settlement to underlying transactions | Prefer payout reconciliation reports that match settlement batches to underlying transactions instead of generic completed statuses |

| Compliance controls | KYB and AML evidence | Check how KYB and AML reviews are triggered, stored, and enforced across onboarding and payout workflows |

| Integration effort | Retry safety and event delivery | Require API idempotency for safe retries and webhook event delivery for payment-state changes |

- Source-to-Pay depth

Start here. Source-to-Pay spans sourcing through payment, so verify the handoff from request to PO to approved billing, not just release automation. Confirm that approval ties back to PO lines and, where applicable, three-way matching against product receipt lines.

- Supplier Onboarding

Onboarding should be complete before commercial transactions begin. At minimum, you should collect tax IDs, banking details, and compliance documents. For legal entities, compliance review may also require beneficial-owner identification and verification procedures, including under US AML rules in [31 CFR 1010.230](https://www.ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1010/subpart-B/section-1010.230). The real test is whether onboarding data becomes usable payment and compliance evidence later.

- Payment execution

For cross-border payouts, verify explicit, machine-readable states such as paid, failed, and canceled, plus programmatic disbursement support at your required scope. One infrastructure path documents payouts to more than 50 countries, which matters if you need more than domestic AP behavior.

- Reconciliation quality

A payout confirmation alone is not enough. You need reconciliation output that matches settlement batches to underlying transactions so finance can tie payable, payment, and bank movement without manual reconstruction. Prefer systems that produce usable payout reconciliation reports over generic "completed" statuses.

- Compliance controls

Cross-border payment operations still face friction on cost, speed, access, and transparency, and AML control expectations are anchored by FATF standards. Check how KYB and AML reviews are triggered, stored, and enforced across onboarding and payout workflows. The key question is evidence retrieval: can you produce the onboarding record, compliance result, and release decision on demand?

- Integration effort

Do not let a polished UI hide weak integration behavior. Require API idempotency for safe retries and webhook event delivery for payment-state changes. If retries can duplicate payouts or missed events can leave approved payables in the wrong state, operational risk is already too high.

Hard rule: if supplier payment status cannot be traced from an approved bill to payout state and reconciliation output, reject the option. Ask for one real transaction walkthrough from approval to payout state to reconciliation output. If the chain is incomplete, the risk is visible now, not later.

We covered this in detail in How Platforms Control Non-Core Spend Through Indirect Procurement.

Comparison Table of the Main Platform Options#

If event-driven supplier payouts are mandatory, eliminate options that cannot show safe API retries and usable webhooks before you compare UI or procurement breadth. That cuts the risk of duplicate payouts and stuck payable states. Implementation complexity here is operator judgment based on scope and integration surface, not a vendor-published timeline or cost.

| Option | Best for | Implementation complexity | Compliance depth (KYC/KYB/AML) | Payout visibility | Reconciliation ownership | Unknowns to confirm | Eliminate first for programmable supplier payouts? |

|---|---|---|---|---|---|---|---|

| Ivalua | Enterprises that want one Source-to-Pay layer from intake through procure-to-pay | Higher, because suite scope spans intake, supplier management, and payments | Strong supplier and spend governance positioning; region-by-region payout compliance depth still needs confirmation | Ivalua says it orchestrates supplier payments across ACH, virtual cards, and global rails | Likely shared between procurement and finance in-suite; still confirm ledger-ready payout exports | Raw-material handling depth, country coverage, webhook model, idempotent retry support | Conditional. Reject only if retry safety and event delivery cannot be documented |

| Euna Marketplace | Public-sector teams optimizing compliant, on-contract buying | Medium for buying adoption; thin evidence for payout execution | Procurement compliance posture is clear; supplier payout KYC/AML depth is not shown in retrieved material | Thin public evidence on supplier-payment rails or payout-state events | Likely outside the marketplace unless a native payment and settlement chain is shown | Public-sector focus, U.S./Canada supplier-network orientation, non-public-sector fit, raw-material depth, payment rails | Yes, unless event-driven payout controls are proven for your use case |

| Tipalti | Teams with upstream purchasing already in place that need supplier onboarding, tax collection, and payout operations | Medium, with substantial finance integration even when procurement stays elsewhere | Documented onboarding-time W-9/W-8 collection, legally mandated KYC, and sanctions/watchlist-style screening | Coverage claims are extensive, but unresolved across official pages: 196 countries / 120 local currencies vs 200+ countries and territories / 120 currencies / 50+ payment methods | Usually finance/AP-owned; confirm batch, attempt, and exception exports | Upstream request controls, final regional coverage, rail-specific behavior, public idempotency/webhook semantics | Conditional. Keep only if API and event model meet retry and status needs |

| Spendesk | Companies prioritizing bill approvals, three-way matching, and international payment reach | Lower to medium if procurement front end already exists | Approval controls are explicit; cross-border supplier-program compliance depth is less clear in retrieved sources | Markets secure payments in 100+ countries, but public API docs say current focus is spend-data use cases | Finance owns most reconciliation; engineering evidence is thin for payout-state automation | Supplier-payment rails, raw-material buying depth, payout event model, idempotency semantics | Yes for marketplace-grade payout orchestration unless vendor proof closes those gaps |

| Rippling | Organizations already centered on Rippling that want procurement and bill pay alongside HR/finance admin | Medium inside Rippling; external integration freedom is constrained | Approval routing is well supported; supplier payout KYC/KYB/AML depth is not established here | Bill pay exists, but public webhook access is limited to App Shop partners | Internal finance likely owns it; external orchestration may be awkward for non-partners | Payout rails, regional scope, non-partner API/event access, raw-material depth | Yes for non-partners needing direct webhook access or payout automation outside App Shop constraints |

| Payments infrastructure stack using Virtual Accounts and Payout Batches | Platform teams that need programmable disbursements, batch control, and event visibility | Highest engineering ownership | Provider-dependent; require documented onboarding and compliance gating | Highest potential: one pattern supports up to 1,000 payouts in one request with async processing, per-item results, and webhooks; another supports up to 15,000 payments per call | You own reconciliation design, including batch IDs, payout attempts, and settlement mapping | Procurement UX, supplier-onboarding UX, region-by-region compliance scope, provider rail coverage | No, but eliminate any provider that cannot show explicit idempotency and duplicate-event handling |

Ivalua is a strong suite candidate on breadth, but confirm machine-readable payout states, retry behavior, and reconciliation exports before you commit. Euna is clearly positioned for compliant public-sector buying, but public evidence is thin on payout rails and event handling for supplier disbursements.

Tipalti and Spendesk solve different problems. Tipalti is better documented for supplier onboarding, compliance, and payout operations. Spendesk is stronger on approvals and bill workflow, with less public proof for programmable payout orchestration. Rippling can work in a Rippling-first estate, but webhook access constraints matter if you are not an App Shop partner.

For elimination testing, require one live payout retry with an idempotency key and one webhook duplicate-handling walkthrough. A practical benchmark from published API guidance is unique keys up to 255 characters, retention for at least 24 hours, and explicit duplicate-event handling guidance. If a vendor cannot show that, remove it from the shortlist for marketplace-scale supplier payouts.

For a step-by-step walkthrough, see Virtual Credit Cards for Platforms: How to Issue Single-Use Cards for Contractor and Vendor Payments.

Option 1 All-in-One Source-to-Pay Suites#

Choose an all-in-one suite when your priority is end-to-end procurement governance, not just paying suppliers at the end. This option is strongest when you need traceable control from internal request to Purchase Order (PO) to approval before payment release.

Where this option fits#

An all-in-one suite can centralize Source-to-Pay (S2P) into one operating layer that connects sourcing and purchasing activity to procurement controls and financial settlement. It is a practical fit when procurement, finance, and IT all need aligned controls, including multi-ERP environments where federated process orchestration matters.

A concrete fit is a setup with formal approvals and finance sign-off before supplier payment release. SAP Ariba positions procure-to-pay around visibility, cost control, and compliance, and SAP also highlights federated processes across multiple ERPs.

Why suites are strong#

The core advantage is policy continuity across the full chain. Ivalua positions this as consistent policy enforcement from contract through payment on one data foundation, including deep approval-layer control.

For demos, ask vendors to show a simple sequence:

- Purchase request approval before PO creation

- Bill approval before payment initiation

The MuleSoft Coupa+SAP reference flow shows that sequence. Treat it as reference architecture, not universal product behavior. Ask vendors to show each state transition, approver record, and downstream handoff.

This is also where suites can support audit and reporting needs. KPMG links S2P programs to finance pressure around audit reviews and timely reporting.

Where they slow you down#

The tradeoff is implementation burden across both systems and people. Ivalua's S2P guidance ties success to integration and change management, and KPMG describes S2P as cross-functional across procurement, finance, and IT. If ownership and handoffs are unclear, rollout risk rises even when the software is capable.

What to verify before you commit#

Before shortlisting suites such as Ivalua or SAP Ariba, confirm:

- A live workflow from request approval to PO, bill approval, and payment release as linked states

- Approval logs and records finance can use for audit support and reporting

- Multi-ERP behavior and where process orchestration lives

- What happens after bill approval and before payment executes downstream

One risk to test is strong upstream procurement controls with unclear payment-state visibility after approval. If that chain is not clear, governance may look complete in process while still be incomplete in execution.

Related reading: How Marketplaces Build Vendor Trust Through Supplier Relationship Management.

Option 2 Procurement Marketplace Platforms#

Choose a procurement marketplace when your priority is compliant, on-contract buying behavior, not full supplier payout orchestration. It gives buyers a controlled procurement front door, but it is not the same thing as deep payment infrastructure.

Where this option fits#

This option is strongest in public procurement settings, where policy compliance and purchasing integrity are core requirements. Euna Marketplace is positioned as a public-sector procurement front door that connects staff to approved contracts and approved suppliers.

It is a practical fit when buyer adoption is the bottleneck. The value is making compliant, on-contract shopping simple enough that teams actually use it in day-to-day purchasing.

Why teams choose it#

The main advantage is contract-aligned purchasing at the point of demand. Euna describes continuous compliance checks against contracts, expiration dates, and non-compliant pricing, and supports cooperative contracts to expand approved shopping options.

Teams also choose this model for implementation flexibility. Euna states marketplace deployments can run standalone or integrate with ERP systems, and its Workday integration messaging describes catalogs, compliance checks, approvals, purchase orders, and reporting in one procurement workflow.

Where the boundary shows#

The boundary is payment depth. Euna's payments positioning centers on revenue collection, and the cited marketplace material does not establish cross-border supplier payout rails, FX execution, or settlement controls.

If cross-border supplier payments are a requirement, validate that capability separately. Payment automation vendors such as Tipalti and Spendesk explicitly market international payment execution coverage, which makes the boundary clear between compliant procurement marketplaces and payout orchestration layers.

Before you commit, ask for a live walkthrough of four points:

- Contract compliance checks for expirations and non-compliant pricing

- Approval-to-PO handoff with reporting outputs for finance

- ERP-versus-marketplace ownership of catalog, supplier, and PO status data

- Post-approval handling when supplier payment must run outside the marketplace

A common failure mode is assuming compliant shopping equals complete procure-to-pay control. If supplier payout execution or payment exceptions matter, you may need an additional AP or payments layer.

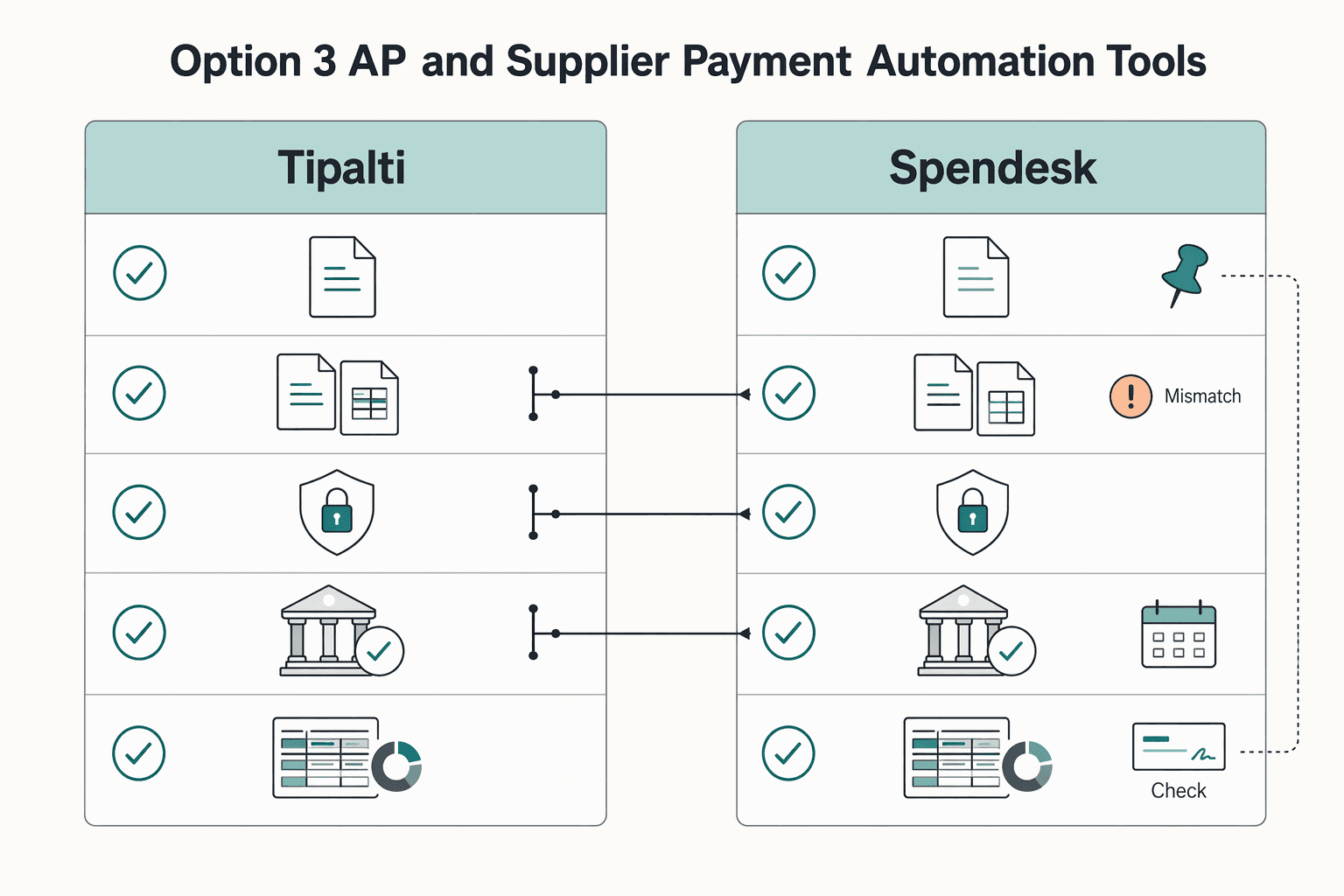

Option 3 AP and Supplier Payment Automation Tools#

Choose this option when procurement intake is already in place and the bottleneck is payable execution: moving an approved bill through approvals, matching, payment, and reconciliation with clear controls. It is strong for bill-to-payment operations, but it is not automatically full upstream raw-material procurement control.

That boundary is the key decision point. Source-to-Pay runs from supplier finding and contracting to final payment, while AP applications are centered on bill processing, payment facilitation, and supplier master data, often integrated with broader source-to-pay stacks.

Two examples show the split:

- Tipalti

Tipalti fits when you want one payable layer from supplier onboarding to reconciliation. Its AP workflow includes bill-stage controls such as approval routing and Purchase Order (PO) matching, and it positions payment execution across 200+ countries and territories, 120 currencies, and 50+ payment methods. Tipalti also publishes procurement capabilities, including intake and rules-based approval routing, so the practical check is scope depth. Confirm whether its procurement layer is enough for your request process or whether you still need a separate upstream tool.

- Spendesk

Spendesk fits when you need tighter bill approvals, matching, and payment scheduling to standardize supplier payouts. It markets AI extraction, approval flows, three-way matching, and payments in 100+ countries. Spendesk also publishes procure-to-pay capabilities, including PO creation after request approval, so the real question is not procurement versus no procurement. It is whether the upstream controls are deep enough for your buying model and receipt workflow.

If your pain is approvals, disbursement control, and payout standardization, this category is usually the right next layer. If the pain starts earlier, such as planning, sourcing, contracting, purchase-order workflows, or inventory management, pair AP automation with a stronger procurement system.

One risk is assuming bill automation covers the whole chain. In raw-material purchasing contexts, AP automation may still need to be paired with stronger upstream procurement controls.

Option 4 Payments Infrastructure Plus Procurement Orchestration#

Choose this path when supplier payouts are part of your product and you need programmable control, not just AP workflow screens. If your main pain is bill approvals and scheduled payments, this is usually more than you need.

You are trading extra product and engineering ownership for tighter control of payout states, retries, reconciliation evidence, and policy gates such as AML and related verification controls. Which gates apply depends on your provider model, legal role, and jurisdiction.

Core building blocks#

| Building block | Role | Cited detail |

|---|---|---|

| Virtual Accounts | Tracking and attribution | Unique account numbers mapped within a physical settlement account; identifiers, not standalone stores of funds |

| Payout Batches | Release many supplier payouts in one action | Wise supports batches of up to 1,000 payments |

| API with idempotency keys | Safe retries on write operations | Providers can require idempotency keys on create or update calls |

| Webhooks and event destinations | Asynchronous payment events | Can route events to webhook endpoints, Amazon EventBridge, or Azure Event Grid |

- Virtual Accounts

Unique account numbers mapped within a physical settlement account for tracking and attribution. They improve money-movement visibility, but they are identifiers, not standalone stores of funds.

- Payout Batches

Useful when you need to release many supplier payouts in one operational action. Wise supports batches of up to 1,000 payments.

- API with idempotency keys

For write operations, providers can require idempotency keys on create or update calls. This is what makes retries safe without creating duplicate outcomes.

- Webhooks and event destinations

Webhooks are HTTP endpoints for asynchronous payment events. Event destinations can route those events to systems like webhook endpoints, Amazon EventBridge, or Azure Event Grid.

What improves in practice#

The biggest gain is control over payout states. Instead of treating payouts as paid or unpaid, you can track states like paid, pending, in_transit, canceled, and failed. That matters because a payout can still move to failed or canceled within 5 business days after submission.

You also get stronger reconciliation traceability by tying provider payout IDs, internal PO and bill references, batch IDs, and supplier IDs into one auditable record.

What you must own#

This model works only if you keep request, PO, approval, and payout records aligned when events are delayed, duplicated, or out of order. Stripe's guidance explicitly warns that undelivered webhooks can be retried for up to three days. Retries can continue even after manual processing, so deduplication and processing-state tracking are mandatory.

A practical reliability test is simple:

- Replay the same payout-creation request with the same idempotency key and confirm one business outcome

- Replay the same webhook event and confirm your handler no-ops after first successful processing

Compliance and evidence#

This model lets you gate payout release on policy checks instead of manual review alone. Keep scope precise: compliance obligations are not identical for every marketplace. In US money services business scope, 31 CFR 1022.210 requires an AML program.

Your evidence pack should be complete without manual stitching: onboarding record, verification result, approval log, payout request payload, provider response ID, payout-status history, and batch artifact when applicable.

When to choose it#

Choose this route when you need marketplace-grade payout reliability, retry safety, and event-level visibility for supplier disbursements. Avoid it when you only need AP throughput and do not want to own orchestration, ledger mapping, webhook handling, and exception queues.

Option 5 ERP-Led Build with Custom Integrations#

Choose this path when your ERP is already the finance center of gravity and you can own a custom integration stack over a multi-month delivery. It gives you a high degree of control over Purchase Order (PO) logic and approval workflow design, but it is usually too heavy if you need fast rollout or low ongoing engineering ownership.

What makes it attractive#

This route is attractive when you want procurement and payment controls anchored in the same finance system rather than spread across several tools.

- ERP-first control surface

You can shape how requests move from Draft to Approved and when a Purchase Order (PO) is created. It fits teams that want procurement and payment controls anchored in the same finance system.

- Custom approval workflow logic

ERP workflows can support condition-based, one-step, and multi-step PO approvals. That makes this option practical when routing must reflect organization-specific policy instead of fixed approval tiers.

- Tailored reconciliation outputs

If close depends on specific exports, mappings, and reference fields, an ERP-led build can align procurement and payment reference data to your accounting model. These outputs require configuration and integration work. They are not guaranteed by default.

What makes it expensive#

The cost is not just the initial project. ERP implementation is typically complex and often runs for a few months, with process mapping, data migration, and third-party integrations in scope. Maintenance continues after go-live through bug fixes, updates, and feature changes.

Where custom integrations usually break#

Webhooks are a key integration risk to design for. They are HTTP endpoints for asynchronous events, and undelivered events can be resent for up to three days. Some operational changes can also produce duplicate deliveries. Your handlers need idempotent processing and clear state tracking to avoid duplicate business effects.

Cross-border supplier payments add another layer of reconciliation risk. When bill entry and payment happen at different exchange rates, realized gain or loss can be recorded. Your design needs invoice currency, payment currency, payment-time exchange rate, and resulting accounting entries tied together.

What to verify before you commit#

Before you commit, prove the custom path can survive both normal approvals and broken event delivery:

- Run requests through each major approval path and confirm routing from Draft to Approved and into

Purchase Order (PO)creation. - Simulate a missed webhook delivery, recover relevant events, and confirm replay does not change the business outcome twice.

Your audit trail should be complete without manual stitching: request history, PO approval log, bill reference, payment event IDs, payment-status changes, FX details where relevant, and final ledger posting.

Related: How to Create a Pitch Deck in Canva.

Option 6 Hybrid Stack for Cross-Border Raw Material Procurement#

A hybrid stack belongs on the shortlist when procurement controls are strong but payment execution visibility is weak. It works for cross-border raw-material buying only if you keep one traceable chain from request to approved billing to payout status, with clear ownership at each handoff.

Why this option earns a place on the shortlist#

This option matters when you need modular tools without losing auditability. In Source-to-Pay, supplier onboarding, purchasing, bill validation, and supplier payment should stay connected. In Procure-to-Pay, traceability should run from request and sourcing through Purchase Order (PO), receiving, billing, and payment.

Use this model when procurement needs structured controls and payments operations needs payout visibility, retries, and compliance checkpoints, with procurement, finance, and accounts payable systems integrated rather than isolated. A Purchase Requisition remains the internal authorization to buy, and a Purchase Order (PO) remains the external vendor document. The hybrid goal is to keep payment execution visible after approval.

What matters most in cross-border use#

For cross-border payments, transparency is a core requirement, not a nice-to-have. Baseline frictions are well known: high costs, low speed, limited access, and insufficient transparency.

The practical rule is simple: if you buy in one region and pay in another, prioritize stacks that expose FX details and payment status clearly. Those fields should stay tied to the approved bill and supplier record, not sit in a disconnected payments console.

A second checkpoint is supplier compliance evidence. Where cross-border onboarding is in scope, you need adequate, accurate, and up-to-date beneficial ownership information for the supplier entity.

Where hybrids usually break#

Governance and oversight can become the failure mode, not just tooling. Cross-border and cross-currency operating models are harder to govern because oversight spans functions and jurisdictions.

Define ownership explicitly:

- Procurement: request approval, PO issuance, bill-policy exceptions

- Payments ops: supplier onboarding checks, payout release, payment-status exceptions

- Finance and engineering: event mapping, ledger fields, retry handling, reconciliation outputs

When these lines blur, reconciliation can fail quietly. Suppliers can be approved in procurement but held in payments, or payables can be marked ready while payouts remain under review.

What to verify before rollout#

Run one end-to-end cross-currency test before committing. Confirm that supplier ID, PO ID, bill reference, payout reference, payment status, and FX detail stay linked from Purchase Requisition through Purchase Order (PO), approval, and payout.

Then test failure handling. Event-driven integrations can power near-real-time finance actions, but webhook delivery can fail and replay. Undelivered events can be resent for up to three days, and recovery tooling may only return the last 30 days of events. Use idempotency keys on payout requests so retries map to the original request instead of creating duplicate payment effects.

Keep an evidence pack from day one: approval logs, supplier onboarding records, beneficial ownership documents where collected, bill reference or image, payout attempt history, exception notes, and final ledger posting.

Implementation Checkpoints for the First 90 Days#

In the first 90 days, focus on one traceable line from request to approved billing to payment evidence. That keeps a hybrid rollout controllable and makes reconciliation easier than treating procurement and payouts as disconnected tracks.

| Checkpoint | Primary focus | Grounded details |

|---|---|---|

| Map the line of record first | Link request through payment | Use stable line-level keys: supplier ID, requisition ID, PO line, receiving reference, invoice reference, and payment request ID |

Define the Approval Workflow around evidence | Keep required documents with approvals | Collect Form W-9 when applicable and keep it for 4 years, and collect Form W-8BEN for foreign payees when requested by the payer or withholding agent |

| Connect bill states to payout triggers only after controls are proven | Test duplicate requests and webhook replays | Require matching to PO and receipt where those records exist; confirm idempotency keys prevent duplicate payment effects and deduplicate by processed event IDs |

| Build tax and reporting steps into onboarding | Store validation and reporting triggers | Validate VAT numbers with VIES where relevant, track the January 31 filing deadline for Form 1099-NEC, and note the FBAR trigger above $10,000 at any time during the calendar year |

-

Map the line of record first. Start with request and

Supplier Onboarding, then map throughPurchase Order (PO), receipt or shipment evidence, billing, and payment. Use stable line-level keys, not just document headers: supplier ID, requisition ID, PO line, receiving reference, invoice reference, and payment request ID. Run at least one live test where payment authorization cannot proceed without documentary support tied to the payable document. -

Define the

Approval Workflowaround evidence. Lock approval states and required documents at each stage, including taxpayer forms andKYC,KYB, orAMLrecords where your provider or regulatory setup requires them. If beneficial-owner verification is in scope, keep those records with the supplier profile. Retain onboarding documents, approval logs, payout attempt history, and exception-resolution notes based on your policy and regulatory requirements. CollectForm W-9when applicable and keep it for 4 years, and collect[Form W-8BEN](https://www.irs.gov/forms-pubs/about-form-w-8-ben)for foreign payees when requested by the payer or withholding agent. -

Connect bill states to payout triggers only after controls are proven. Do not release payouts from approval alone. Require matching to PO and receipt where those records exist. Before launch, test duplicate payment requests and confirm idempotency keys prevent duplicate payment effects. Replay duplicate

Webhooksand confirm your consumer deduplicates by processed event IDs. If useful for your control design, run a reconciliation dry run so approved payables, released payments, failed payouts, and ledger outputs tie to the same references. -

Build tax and reporting steps into onboarding. For EU supplier flows where relevant, validate VAT numbers with VIES and store the result in the onboarding record. For U.S. reporting, reference current IRS rules for

Form 1099-NECin workflow logic rather than hardcoding assumptions, and track the January 31 filing deadline. SupportFBARtracking where enabled. The trigger is aggregate foreign financial account value above $10,000 at any time during the calendar year, and applicability depends on actual account ownership and structure.

The rollout sequence is lifecycle mapping, evidence-backed approvals, payout-event reliability, then tax and reporting steps. Reversing that order can leave payout flows looking finished but harder to defend operationally. Before rollout, align your webhook replay tests and reconciliation checkpoints to a concrete integration pattern in the developer docs.

Red Flags That Break Procurement and Supplier Payments at Scale#

At scale, the control chain usually breaks in a small number of predictable places. These are the four to watch first.

- Split

Purchase Order (PO)approval from payout release

If settled payable records cannot be tied back to the approved buy, control breaks quickly at higher volume. Where receipt or service evidence exists, use three-way matching so payment does not move on PO and bill alone. If matching puts a bill on hold, release it only after the missing receipt or service evidence is tied to the same reference chain.

- Incomplete

Supplier Onboarding

This can show up as payout capability not enabled or missed payouts. Before live transactions, confirm that required verification data is complete for your provider setup, including applicable identity or business-verification requirements. Where beneficial-owner identification is in scope for covered institutions, collect it at account opening instead of waiting for an exception.

- Non-idempotent

APIrequests and weakWebhookshandling

Retries are normal. Duplicate payment effects are a control failure. Use idempotent payment requests and deduplicate webhook processing by event ID, since providers may deliver the same event more than once. As a practical test, resend the same payout request with the same idempotency key and confirm one payment outcome.

- No written owner for exceptions

If procurement, finance, and engineering all "help," exceptions stall and accountability blurs. Assign responsibility and authority in writing for bill holds, onboarding remediation, and event-processing failures. Require payout-attempt history and exception-resolution notes in the same evidence pack so decisions are traceable.

Need the full breakdown? Read What Is Procurement as a Service? How Platforms Can Outsource Vendor Sourcing and Contracting.

Conclusion#

Choose the option that keeps one clean control line from internal request to payout evidence. In practice, the winning decision is not always the tool with the longest feature list. It is the one that keeps procure-to-pay intact across procurement, finance, and accounts payable while still giving you retry-safe payment execution and documentation you can use.

If you are making the final call, use these three rules:

- Pick for traceability, not feature breadth

Procure-to-pay spans request, sourcing, Purchase Order (PO), receiving, billing, and payment. A break anywhere in that chain can lead to the same result: approvals that look complete but cannot be tied to a settled supplier payment. If one option has strong policy control but weak payout status, and another has strong payout tooling but weak upstream proof, neither is complete on its own.

Run one end-to-end trace test. You should be able to follow the approved request, PO, bill, payable state, and final payout reference without guesswork. Where receiving evidence matters, confirm three-way match support rather than only PO-to-bill comparison, since adding goods receipt or service entry evidence improves accuracy and financial control.

- Treat retry behavior as a control decision

Procurement controls are not enough if the payout layer can duplicate requests during timeouts or retries. Safe retries depend on idempotency: with the same idempotency key, a request can be retried without creating a second object or running the operation twice.

Test this directly. Replay the same payout request with the same idempotency key after a forced timeout, and confirm the retry maps to the same operation instead of creating a second payment. Stripe documents idempotency keys up to 255 characters, Adyen documents a maximum of 64 characters, and PayPal warns that omitting its request ID header can duplicate a request. You want that failure mode exposed before rollout, not during month-end close.

- Assign owners and require an evidence pack from day one

Control can weaken quickly when procurement, payments, and reconciliation run as separate projects with no named accountability. A practical management standard is to assign responsibility, delegate authority, and hold people accountable for control responsibilities. In rollout terms, name who owns approval policy, who owns payout execution, and who owns reconciliation and exception closure.

Do not rely on verbal assurance. Require evidence at each stage: onboarding records, approval logs, receiving or service evidence where relevant, bill approval history, payout attempt history, and exception notes. If the team cannot produce that pack for one test transaction, you are not ready to scale.

A practical path is the least complex one that still keeps procure-to-pay discipline, programmable payment execution, and documented reconciliation in one accountable model. Make the choice, name the owners, run the trace test, and move from vendor evaluation to controlled rollout quickly.

If your decision leans toward programmable supplier disbursements, evaluate whether Payouts fits your control, status visibility, and batch-operations requirements.

Frequently Asked Questions

What is a material procurement platform for marketplaces in practical terms?

It is more than a buying screen. It should cover the full procure-to-pay chain: identifying need, routing requests, selecting suppliers, issuing POs, approving supplier bills, and releasing supplier payments. The key test is whether those stages stay connected in one traceable evidence trail.

How should supplier payments connect to procurement approvals and invoice status?

Supplier payment should start from a payable bill state, not from PO approval alone. Release payments only when bills meet explicit criteria such as due date, discount timing, approval status, and, where used, two-way or three-way matching. If you cannot trace the approved request to a matched bill and then to payment status, treat that as a control gap.

Which controls are non-negotiable before scaling cross-border supplier payouts?

Baseline controls are customer due diligence, record keeping, retry safety, and event tracking. In U.S. contexts, missing or clearly invalid TIN data can require immediate backup withholding, and foreign persons may need to provide Form W-8BEN to the payer or withholding agent. If beneficial ownership reporting applies to your entity, track FinCEN timing, including updates within 30 calendar days when previously reported information changes.

When should a team choose an all-in-one suite versus a hybrid procurement plus payments stack?

Choose an all-in-one Source-to-Pay suite when your main need is one connected workflow across intake, supplier management, PO, and bill-to-payment steps. Choose a hybrid stack when procurement intake is acceptable but payout execution, cross-border rails, webhook visibility, or reconciliation detail is the bottleneck. Suites are better for centralized workflow control, while hybrid stacks are better for flexible payout integrations and event-driven handling.

What are the most common failure points in requisition-to-payment flows?

Common failure points are payment released without bill proof, incomplete supplier onboarding, duplicate effects from non-idempotent API retries, and weak webhook handling. Reconciliation can also break when the payout model does not preserve transaction-to-payout linkage. Test early by tracing one bill to one payout and one reconciliation record, then replaying the same request with the same idempotency key to confirm a single outcome.

How should teams phase MVP versus scale architecture without re-platforming too early?

At low volume, manual handling can work for MVP, but keep stable reference IDs and approval records from day one. Preserve consistent IDs across supplier, request, PO, bill, and payout records so automation can be added without breaking traceability. Move to event-driven processing before volume climbs, and deduplicate by event ID because some providers can retry webhook delivery for up to 3 days.

What operator detail matters most during vendor evaluation?

Ask for live proof, not slides. Have the vendor show how an approved bill becomes payable, how exceptions are held, and what evidence remains after settlement. For cross-border payouts, require exact coverage and rail details for your supplier footprint instead of generic global claims.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/32.905trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- gao.gov/greenbooktrusted

- gao.gov/products/gao-25-107721trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-3-establish-structu...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-5-enforce-accountab...trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: