Quick Answer

Marketplaces build vendor trust by treating Supplier Relationship Management as a product and operating control, not just a partner-relations task. Trust grows when suppliers are tiered by risk and revenue impact, onboarding and payout checks require verifiable evidence, event and ledger records reconcile cleanly, and supplier updates include clear status, ownership, timestamps, and next actions.

Why Supplier Relationship Management Builds Vendor Trust#

Vendor trust in a marketplace belongs in your revenue model, not in a vague partner-relations bucket. If suppliers do not trust how your platform onboards them, governs issues, or communicates status, growth can get more expensive. Activation can slow, and teams may spend more time handling exceptions and manual fixes that should have been designed into the product and operating policy much earlier.

That is why Supplier Relationship Management, or SRM, matters well beyond procurement. Gartner defines SRM as the buyer-supplier partnership used to sustain and improve supplier value. For marketplace operators, that lens fits. Trust controls should protect supplier participation and the commercial value tied to it. Research on cross-border e-commerce platforms reaches a similar conclusion from the seller side. Seller trust is essential to platform success, and platform governance plays a direct role in shaping it.

The practical question is not whether trust matters. It is where to put the controls so trust supports monetization instead of dragging on it. If you own product, revenue, finance, or operations, you need clear rules for when to deepen due diligence and when a basic Service Level Agreement is enough. You also need to know what evidence must be verifiable in your records, and when a supplier should stay out of a revenue-critical flow until key checks are complete. A common failure mode is pushing for fast activation without those gates, then dealing later with escalations and avoidable cleanup.

The goal here is to make those decisions easier. You will leave with a workable way to tier suppliers by risk and revenue impact, the checkpoints that should exist from onboarding through ongoing performance, and a short list of trust KPIs worth tracking. The emphasis is on evidence, not sentiment. That means due diligence artifacts, SLA attainment, payout exception rates, communication timestamps, and audit trail completeness. If you cannot verify those basics, you are probably asking people to compensate for missing controls.

A useful reality check: Gartner notes that supplier segmentation is foundational to effective SRM, yet only 35% of chief procurement officers have a working model to differentiate critical suppliers by value. At the same time, supplier collaboration rose in priority for 88% of procurement leaders over the prior 24 months. In plain terms, trust is strategically important, but many teams still do not have the tiering logic to manage it consistently.

Keep one constraint in view: an e-marketplace may not have identical requirements everywhere. Coverage, obligations, and control depth may vary by market or program. So the goal is not more process across the board. It is matching the right controls to the supplier exposure you actually have, then checking how those controls affect activation quality, operating cost, and retention.

If you want a deeper dive, read What Is Vendor Management? A Platform Operator's Guide to Supplier Lifecycle Control.

Why vendor trust changes marketplace economics#

If a supplier touches a revenue-critical flow, treat trust controls as pricing and margin infrastructure, not procurement overhead. In an e-marketplace, weak controls show up in dispute handling, payout exceptions, slower reconciliation, and manual proof work across teams.

| Signal | What it covers | Why it matters |

|---|---|---|

| SLA attainment | Expected performance, how performance is measured, and what happens if levels are missed | Makes supplier performance comparable |

| Payout failure and exception rates | Failed or delayed payments, especially when resolution needs manual intervention | Create direct handling cost and erode confidence |

| Reconciliation speed from ledger journals | Matching journal and ledger records to external statements, including reconciliation references on related journal lines where clearing accounts are used | Shows whether finance can trace supplier events to payout status and ledger evidence without cross-team reconstruction |

Supplier Relationship Management (SRM) is the ongoing evaluation of vendors that supply goods, materials, or services. Vendor Relationship Management (VRM) is often used similarly, including in procurement guidance that treats it as another name for SRM. In practice, the label matters less than the operating job: select suppliers, govern performance, and improve outcomes while reducing risk and overhead across the relationship lifecycle.

The economics shift when obligations and evidence are unclear. Support absorbs avoidable disputes, finance spends time on failed or delayed payment follow-up, and operations fills gaps with manual investigation. Those costs are usually distributed across teams, but they still compress margin.

Strong SRM does the opposite: it reduces avoidable exception work, makes supplier performance comparable, and supports supplier retention in the parts of the marketplace that drive revenue. You may not be able to tie trust controls to a single fixed take-rate uplift, but you can see whether they protect monetization by reducing friction in revenue and settlement flows.

Trust becomes measurable when you tie it to operating evidence:

- SLA attainment: a Service Level Agreement should define expected performance, how performance is measured, and what happens if levels are missed.

- Payout failure and exception rates: failed or delayed payments create direct handling cost and erode confidence, especially when resolution needs manual intervention.

- Reconciliation speed from ledger journals: teams should be able to match journal and ledger records to external statements; where clearing accounts are used, reconciliation references on related journal lines are a practical control point.

A practical rule: if finance cannot trace a supplier event to payout status and ledger evidence without cross-team reconstruction, trust is still dependent on human memory rather than system controls.

SRM in marketplaces is a product design decision#

In a marketplace, SRM needs to be built into the product, not handled mainly through ad hoc escalation. Once trust depends on transaction states, payouts, and exceptions, your controls need to live in API flows, status visibility, and webhook handling so teams are not reconstructing outcomes from inbox threads.

This matters especially for B2B SMEs. A 2025 study found that communication consistency and credibility influence how SME buyers form trust in e-marketplaces, so your UX and your operating policy both act as trust controls. Clear, event-linked updates usually protect credibility better than vague updates with no verifiable state behind them.

The test is simple: can the platform prove what happened without relying on human memory? Webhooks are used to notify applications when events happen, including asynchronous events, and your audit trail should let finance and ops reconstruct the sequence and connect it to ledger journals.

Use this checkpoint:

- Each supplier-facing event has an event ID, timestamp, delivery record, and resulting status change.

- Each money movement is traceable from the event trail into subledger activity and the general ledger, including journal reporting links.

- Retries are idempotent so altered or duplicate requests do not create mismatched states.

If those links are not machine-verifiable, finance and ops usually absorb the cost later.

Tier suppliers and match control depth to risk and revenue impact#

Use one rule: control depth should be proportionate to supplier risk and revenue impact. Do not run every supplier through the same onboarding, monitoring, and escalation path.

Build your tiers from due diligence and risk assessment inputs: supplier value, criticality, revenue at risk, payout volume, and compliance exposure. The tier should be explainable from evidence, not internal preference. If someone outside the deal can review the file and see why a supplier is Tier 1 rather than Tier 3, the model is doing its job.

A practical evidence pack includes due diligence records, expected revenue concentration, service criticality, payout patterns, compliance constraints, and incident history. This keeps tiering tied to both upside and downside: where failure would be hardest to absorb, unwind, or remediate. The gap is real in practice: Gartner reports only 35% of chief procurement officers have a working model to differentiate critical suppliers by value.

Set controls across the full supplier lifecycle, not only at onboarding. A lifecycle view covers planning, due diligence and selection, contracting, ongoing monitoring, and termination. For each tier, define SLA metrics, escalation windows, review cadence, and exit triggers in advance.

| Supplier tier | Required controls | Approval owner | Review cadence | Exit trigger conditions |

|---|---|---|---|---|

| Tier 3 standard | Baseline due diligence, signed SLA, metric monitoring, named ops contact, issue logging | Marketplace ops or category owner | Monthly metric review, formal review every 6 months | Repeated SLA misses, unresolved payout exceptions, newly discovered compliance gap |

| Tier 2 material | Full risk assessment, baseline compliance management, defined escalation windows, document refresh, incident review | Business owner plus finance or risk review | Monthly ops review, quarterly risk review | Repeated misses against agreed metrics, rising revenue concentration, missed remediation commitments |

| Tier 1 strategic or high-risk | Enhanced due diligence, enhanced compliance management, tighter escalation windows, audit pack, executive visibility, exit plan prepared in advance | Named business owner plus compliance and finance sign-off | Weekly exception monitoring, monthly formal review | Material compliance breach, sustained critical SLA failure, inability to evidence controls or complete remediation |

If a supplier is high-revenue and high-risk, complete stricter onboarding before activation. Confirm the due diligence file, approved SLA metrics, named escalation contacts, and retrievable audit pack first.

If a supplier is low-revenue and low-risk, optimize for faster activation with guardrails. Keep standard due diligence, standard SLA terms, automated monitoring, and a clear rule that unresolved compliance issues pause go-live.

Build trust across the full money lifecycle#

Trust in a marketplace is built by making the money path traceable from onboarding through final payout or exit. Each supplier should move through a clear sequence: KYC/KYB, contract and SLA, transaction statusing, payout batch closure, exception handling, and renewal or termination. Each checkpoint needs a named owner and retrievable evidence.

Onboarding alone is not the trust event; handoffs are where trust usually breaks. For legal-entity suppliers, if your program requires beneficial owner procedures, the key control is being able to show beneficial owners were identified and verified where applicable before first live payout.

Contract and SLA controls should be complete before activation. Define obligations, service thresholds, escalation paths, and payout timing terms in a system of record, not scattered across email. If your provider has an initial payout delay, set expectations early. Stripe, for example, says an initial payout is typically scheduled 7-14 days after the first successful payment.

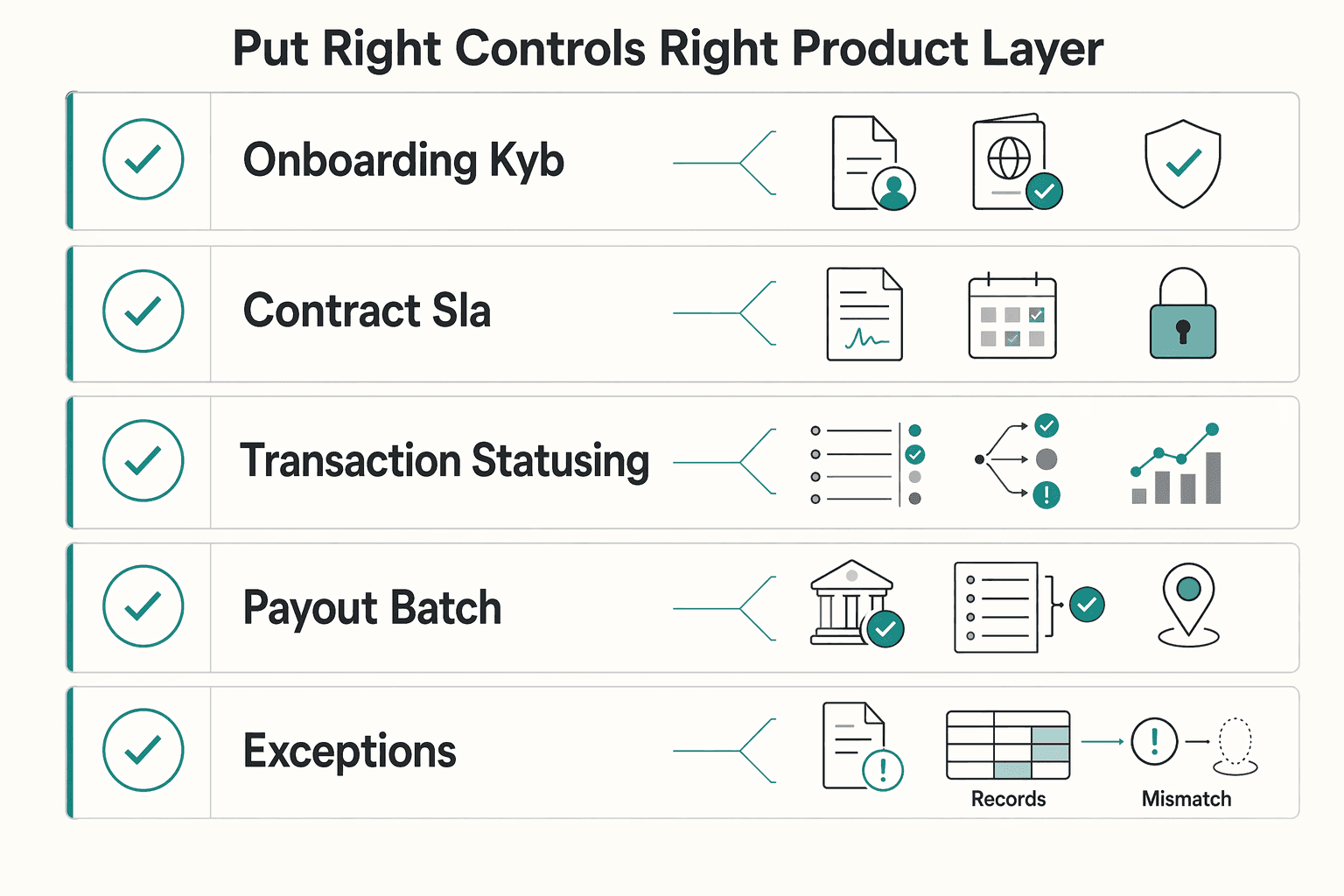

Put the right controls in the right product layer#

Use product modules to enforce trust controls where they work best. Virtual Accounts support inbound attribution by assigning unique account numbers inside a physical settlement account, which helps reduce manual reconciliation work. Merchant of Record is a liability decision: if you use MoR, that entity is legally responsible for processing customer payments and carries the financial, legal, and compliance responsibility for those transactions.

The payout layer should reliably convert approved balances into batches and prove what was included at batch close. Reconciliation should show transaction-level contents, including payments, refunds, and chargebacks, not just a net total.

| Lifecycle checkpoint | Required artifact | Owner | System of record | Verification evidence |

|---|---|---|---|---|

| Onboarding and KYB | Entity details, beneficial owner verification where required, approval decision | Compliance or risk owner | Compliance tool or onboarding system | Verification result with timestamp and reviewer |

| Contract and SLA | Signed contract, SLA terms, payout timing terms, escalation contacts | Business owner plus legal or ops | Contract repository | Executed agreement version and approval record |

| Transaction statusing | Order-to-payment status mapping, event-handling rules | Product plus payments ops | Payment platform and event log | Webhook receipt matched to internal transaction state |

| Payout batch close | Batch file or report, approved payout contents, reconciliation output | Finance or payouts ops | Payout console and reconciliation reports | Reconciliation export showing included payments, refunds, and chargebacks |

| Exception and exit | Incident record, remediation decision, renewal or termination approval | Named incident owner plus business owner | Incident tracker and contract system | Hold or release decision, payout note, termination or renewal record |

Design for asynchronous returns#

Asynchronous provider events are normal, so replay-safe processing is mandatory. Without strong idempotency and replay-safe webhook handling, retries and delayed events can create duplicate actions or mismatched states.

Require idempotency on create and update requests so the same operation is not executed twice. For inbound events, store event IDs, ignore duplicates, and only advance state when the event matches an expected transition. Before you go live, test replay and delay scenarios to confirm records stay consistent.

If records still drift, pause payout release and rebuild the truth from batch and event evidence before issuing a final supplier answer. Exit planning belongs in the same control path: define renewal or termination flow, open-exception handling, and final payout sign-off in advance.

Communication signals that move supplier behavior#

Supplier communication should optimize for credibility, not volume. In an e-marketplace, trust rises when updates are consistent, precise, and tied to verifiable details such as the event, owner, timestamp, and next update point.

Research in B2B e-marketplaces links communication consistency and credibility to trust and engagement, and shows they can partially substitute for each other. The practical implication is simple: if you cannot update constantly, make each update dependable and specific.

Turn trust into visible operating signals#

Use signals suppliers can verify without opening a ticket. Define response and acknowledgment expectations in your SLA, then reflect them consistently across your portal, API status surfaces, and incident messages.

For incidents, use a repeatable pattern: acknowledge early, summarize the known impact, and state when the next update will arrive. A 30-minute cadence is one example during active incidents, but the key is predictable cadence for the incident type and consistent messaging across channels.

Frequent but vague updates usually reduce trust. Fewer updates can work better when each update includes a concrete status change, a timestamp, and a clear owner.

A useful checkpoint is to sample recent incidents and compare your status page, supplier emails, and incident records. If impact statements, timestamps, or next-step commitments do not match, the trust issue is operational.

Use an escalation ladder suppliers can believe#

Define escalation before the next issue, especially for payment, onboarding, and account access. Keep one shared artifact with clear ownership and communication paths.

| Trigger event | Owner | Communication channel | Expected resolution window |

|---|---|---|---|

| First-response SLA missed | Support or supplier operations owner | Case update plus email | Per SLA or incident policy |

| Payout or settlement incident affecting supplier funds | Payments operations or finance owner | Early status notice plus direct supplier message | Acknowledge early; continue at stated cadence |

| Compliance review blocks activation or payout | Compliance owner | Portal notice plus case message | Based on required review step |

| Repeated cross-channel mismatch or unresolved issue | Senior operations owner | Direct outreach with written action plan | Next decision point communicated clearly |

Avoid promising fix dates before facts are verified. Commit to the next decision point and keep portal, API, and human communication aligned so suppliers can trust what they see.

Related reading: Form 3520 Playbook: A 3-Step Framework for Foreign Trust Transactions and Foreign Gift Reporting.

Compliance and tax controls that protect trust at scale#

When money is about to move, trust depends on one rule: if required AML, KYC, KYB, VAT, or tax artifacts are incomplete for the relevant market or program, pause payout or withdrawal release. Tell the supplier exactly what is missing and what happens next. Do not bypass controls for speed or account size.

Put hard gates before payout-sensitive actions#

Use payout gates that match the supplier's market, business type, and program setup, because requirements are not uniform. KYC requirements can change by country, business type, and requested capabilities, so an account can pass onboarding but still be blocked for payouts. For legal entities, KYB should include entity details and, where applicable, beneficial owner verification. For relevant EU cross-border cases, VAT validation through VIES is a clean gate because the result is explicit: valid or invalid.

| Gate | What to verify | Payout rule |

|---|---|---|

| KYC | Required identity fields for the supplier's country, business type, and requested capabilities | Hold payout if required verification information is missing |

| KYB / AML | Legal entity details and beneficial owner information where applicable | Hold payout until entity review is complete |

| VAT validation | VAT registration status through EU VIES for relevant cross-border cases | Do not release tax-sensitive payouts on an invalid result |

The main failure mode is releasing funds while compliance still shows incomplete verification. That split state breaks trust fast because compliance, finance, and supplier-facing status no longer match.

Track tax readiness without oversharing#

For global suppliers, keep a tax-readiness view where your program supports it: W-9 status (correct TIN collection), W-8/W-8BEN status for foreign beneficial owners, and tracking flags for FEIE, FBAR, and Form 1099 handling where relevant.

| Status item | What to track | Scope note |

|---|---|---|

| W-9 status | Correct TIN collection | For global suppliers where your program supports a tax-readiness view |

| W-8/W-8BEN status | Status for foreign beneficial owners | For global suppliers where your program supports a tax-readiness view |

| FEIE flag | Tracking flag | Applies only when IRS qualification requirements are met |

| FBAR flag | Tracking flag | Concerns certain foreign financial accounts and uses a $10,000 threshold at any time during the reported calendar year |

| Form 1099 handling | Tracking flag | Follows the IRS General Instructions for Certain Information Returns |

Keep scope tight. FEIE applies only when IRS qualification requirements are met. FBAR reporting concerns certain foreign financial accounts and uses a $10,000 threshold at any time during the reported calendar year. Form 1099 handling follows the IRS General Instructions for Certain Information Returns. These are not default obligations for every supplier.

In portal or case views, expose only masked status fields: form type, request date, received date, review state, and next action.

Reconcile compliance status with payout state#

Before finalizing payouts, verify three checkpoints:

- Policy decision log exists for each hold or release (reason code, owner, timestamp, evidence reference).

- Audit trail is complete from document request to review outcome to payout decision.

- Compliance status and payout state reconcile for each supplier.

If compliance says "verification incomplete" while payout says "released," stop and resolve that mismatch first. Trust at scale comes from one consistent story across policy records, audit trails, and money movement.

Related: Retail and eCommerce Accounts Payable Automation: How Marketplaces Pay Suppliers at Volume.

Red flags that create trust debt and how to recover#

Trust debt builds when your onboarding promises, platform states, and incident response stop matching each other. The recovery pattern is straightforward: make eligibility qualifiers explicit, reconcile state from ledger evidence, and run incidents with clear ownership.

| Red flag | What it looks like | Recovery step |

|---|---|---|

| Promises that ignore compliance reality | Suppliers are told they can activate, sell, or withdraw funds before the relevant market or program checks are actually available | Publish supported markets or programs, eligible entity types, required documents, payout prerequisites, and hold conditions up front |

| States that do not reconcile | Transaction status says one thing and payout status says another | Rebuild truth from ledger journals as the audit trail, then replay webhooks with idempotency controls |

| Incidents with no clear owner | Ownership is unclear during a trust incident | Assign one accountable owner, keep a written incident timeline, and give suppliers a remediation plan with current impact, timestamps, next update, and the exact condition for resolution |

Promises that ignore compliance reality#

If suppliers are told they can activate, sell, or withdraw funds before the relevant market or program checks are actually available, trust starts breaking before money moves. Recovery starts by clearly publishing qualifiers up front: supported markets or programs, eligible entity types, required documents, payout prerequisites, and hold conditions. If a supplier cannot clear required checks for that route, say so before signup completes.

Use one quick alignment check: compare sales copy, onboarding UI, and your policy decision log. If they describe different eligibility rules, disputes are predictable.

States that do not reconcile#

When transaction status says one thing and payout status says another, treat it as a data-integrity issue first. Rebuild truth from ledger journals as the audit trail, then replay webhooks with idempotency controls. Webhook delivery can duplicate events, so retries and replay must prevent duplicate side effects.

Avoid manual exception patches that fix one screen while finance, support, and supplier views remain out of sync.

Incidents with no clear owner#

Trust incidents degrade faster when ownership is unclear. Assign one accountable owner, keep a written incident timeline so teams stay aligned, and give suppliers a remediation plan with current impact, timestamps, next update, and the exact condition for resolution. Without that structure, coordination slips and supplier confidence drops.

For a step-by-step walkthrough, see How to Build a Trust-First Project Roadmap for Client Work.

Conclusion#

Treat vendor trust as a monetization control. In a marketplace, SRM is not just relationship upkeep. It is a strategic choice that can be judged by three things: how well it protects revenue, what it does to margin, and whether it makes operations more resilient when something goes wrong.

That is the useful shift in mindset. Strong SRM takes a full-lifecycle view, from onboarding to offboarding, and aims at long-term value while reducing risk. If a control does not improve reliability, reduce avoidable exceptions, or make supplier performance easier to verify, it may still feel helpful, but it is probably not doing enough commercial work for the cost.

Your next move should be practical, not abstract. Start by segmenting suppliers by business impact, then apply a risk-based approach so the deepest checks sit where the exposure is highest. That means high-impact, higher-risk suppliers get more due diligence, tighter review, and clearer escalation ownership. Lower-impact suppliers can move faster, but not without basic guardrails. A common operational mistake is applying the same depth everywhere. That can slow growth on the low-risk end and leave you under-protected where failure is expensive.

To get this moving, use a short checklist:

- Define supplier tiers by business impact and risk. Use factors like service criticality, revenue dependence, and compliance exposure so your team knows which relationships need the most attention.

- Assign control depth by tier. Set the minimum evidence required before activation, payout, or expanded access, and make approval ownership explicit.

- Instrument trust KPIs against business objectives. Start with supplier measures that are easy to explain and verify, such as on-time delivery, lead time, defect rates, and cost variances, then add the marketplace signals that matter to your model.

- Audit event-to-ledger traceability. Pick real transactions and confirm the supplier-facing event, internal status, and ledger record tell the same story. An audit trail is there to prove accuracy, completeness, and timeliness, not just to satisfy a control checklist.

If you only do one verification step this quarter, do that last one. Trust can break where status messaging, finance records, and operational handling drift apart. A common failure mode is misalignment: a portal says one thing, the ledger implies another, and your team burns time reconstructing what happened after a complaint lands.

If you want to pressure-test your marketplace design, Gruv can help you confirm market and program coverage, map the control depth your model needs, and assess whether the implementation fits how you actually onboard, monitor, and pay suppliers.

Frequently Asked Questions

What builds vendor trust fastest in an e-marketplace?

The fastest gains usually come from aligning promises with actual supplier experience. Precise status, timestamps, and clear next actions build more trust than frequent but vague reassurance. A useful check is whether onboarding copy, policy rules, and recorded status outputs all match.

How is marketplace SRM different from traditional vendor management?

Traditional vendor management focuses more on contracts, orders, and performance monitoring. Marketplace SRM is broader because it aims to improve long-term value, reduce risk, and support stronger partnerships. In a marketplace, trust has to show up in daily operations, not just account-manager communication.

Which trust dimensions matter most in supplier relationships?

A useful framework is competence, benevolence, integrity, and reliability. Competence is about execution, integrity is about honest and consistent rules, reliability is about repeatable outcomes, and benevolence appears when actions are not purely self-protective during issues. For operators, reliability and integrity are often the best place to start because they are easier to observe in outcomes.

What are the biggest trust failure points for marketplace operators?

Measurement is a major failure point. Many teams talk about trust but struggle to quantify it or spot decline early. When supplier-facing updates and internal operating records do not align, trust problems become harder to detect and resolve.

How should we balance fast supplier onboarding against compliance risk?

Use a risk-based approach instead of one uniform process for every supplier. Higher-risk suppliers should face deeper due diligence before key approvals, while lower-risk suppliers can move faster with guardrails. If compliance artifacts are incomplete, hold the process and clearly explain what verification is still required.

What should we measure if we want trust programs to improve margin, not just satisfaction?

Start with metrics that already connect to cost and supplier performance, such as on-time delivery, lead time, defect rates, and cost variances. In a marketplace, pair those with exception and reconciliation indicators. If the program does not reduce disputes or improve predictability, it may lift sentiment without improving margin.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/01trusted

- comptroller.war.gov/Portals/45/documents/fmr/Volume_06a.pdftrusted

- csrc.nist.gov/glossary/term/audit_trailtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- hbsp.harvard.edu/product/H07C20-PDF-ENGtrusted

- irs.gov/forms-pubs/about-form-w-9trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Vendor Relationship Management for Platforms That Finance and Ops Can Run

Start with the operating model before the product demo. If finance, operations, and product do not agree on who owns vendor intake, approval, activation, and review, a vendor relationship management platform becomes one more place where incomplete records pile up.

What Is Vendor Management? A Platform Operator's Guide to Supplier Lifecycle Control

Vendor management in a platform business is not back-office admin. It is a core control point in the business. It determines which third parties can influence core operations, service quality, and customer experience, and under what conditions they can do it.

How Retail and eCommerce Marketplaces Pay Suppliers at Volume

For many retail and ecommerce finance teams, AP automation is the starting point because the first pain is usually obvious: too many invoices, too much manual approval chasing, and not enough visibility into what is owed. Accounts payable is the money you owe suppliers and vendors for goods or services bought on credit, and automation reduces the manual work that slows processing and creates human error.