Quick Answer

Yes. You can offer instant vendor spend only after the card clears spend-ready gates, not when it is merely issued. Keep `issued` and `spend-ready` separate, bind each card to the vendor or payable, and enforce limits or merchant restrictions before first authorization. A launch claim is credible only if one approved payment and one blocked attempt both map cleanly to the internal finance record without spreadsheet cleanup.

How Virtual Card Issuance Helps Control Contractor Spend#

Fast issuance matters only when policy comes first and every card action can be traced afterward. If you cannot tell who requested a card, what it can buy, where it can be used, and how it lands in finance records, you do not have a launch-ready virtual card program.

A virtual card is simply a digitally generated card number used for defined business payments instead of sharing a physical card. That simplicity is exactly why teams move too fast. A card can be issued quickly, but that does not make it spend-ready.

Step 1. Set the business promise#

Start with a narrow promise to the business, not a broad promise to the market. The promise should be straightforward: cards can be created quickly where your program supports it, controls are applied before first spend, and every lifecycle event stays tied to an internal payment record.

Teams get into trouble when they collapse speed and access into one claim. They promise "instant spending power" even though the product still depends on manual review, weak vendor matching, or after-the-fact cleanup. Use a simpler standard. You are not ready to market immediate spend access unless you can apply a spending limit, make an authorization decision in real time, block merchant categories, or confirm a transaction through the controls your provider supports.

This is also where the operating model matters. Stripe, for example, presents two issuing setup paths: complete program management and modular issuer processing. If your team has not decided which model you are actually running, you should not promise the same speed, control depth, or operational ownership across every use case. The card experience may look similar to the user, but the responsibility load behind it is not.

In practice, virtual cards may be single or multi-use and scoped by limit, timeframe, and where or how they are used.

Step 2. Draw the scope boundary#

The cleanest launches start narrow. This article is about contractor and vendor payments inside a platform, not a broad employee card program, travel spend, or general reimbursement.

Write down an "in scope / out of scope" line. In scope might include vendor-specific online purchases, single-payment supplier charges, or tightly limited recurring service spend. Out of scope might include open-ended discretionary buying, card-on-file expansion across every merchant, or any use case where vendor identity is optional. If the vendor or payment object is unknown at issuance time, that is a red flag because your controls and reconciliation will weaken later.

This is where the issued versus spend-ready distinction saves you work. You can create a card record early. It should not become usable until it is linked to the right vendor or payable, assigned the right control set, and tied to the finance record that will carry the transaction. If you want a deeper look at those policy decisions, read How to Build a Spend Control Policy for Virtual Cards on Your Platform.

Step 3. Define the success criteria#

Success is not "a card appeared in the provider dashboard." Success means the card works where intended, is blocked outside that boundary, and maps back to your own records without manual detective work. It also means you can reverse course quickly. Virtual cards can be created, frozen, or cancelled quickly, which matters when a vendor changes, a request was wrong, or a supplier system is compromised.

Before widening access, run one short pre-launch test. With a single test card, confirm you can answer all four of these without checking chat or email:

- who the request owner is

- which vendor or payment object the card is linked to

- what control set is attached, such as limit, merchant restriction, or usage pattern

- which internal finance record should reflect issuance, authorization activity, and closure

If any one of those answers lives only in a spreadsheet, you already have reconciliation drift. A constrained virtual card number exposed at a supplier does less damage than broad shared credentials, but only if your controls were real in the first place. That is the thread for the rest of this guide: fast creation is useful, but controlled spend and clean evidence are what make the program durable.

Related: How to Pitch Instant Payouts to Gig Contractors Without Overpromising.

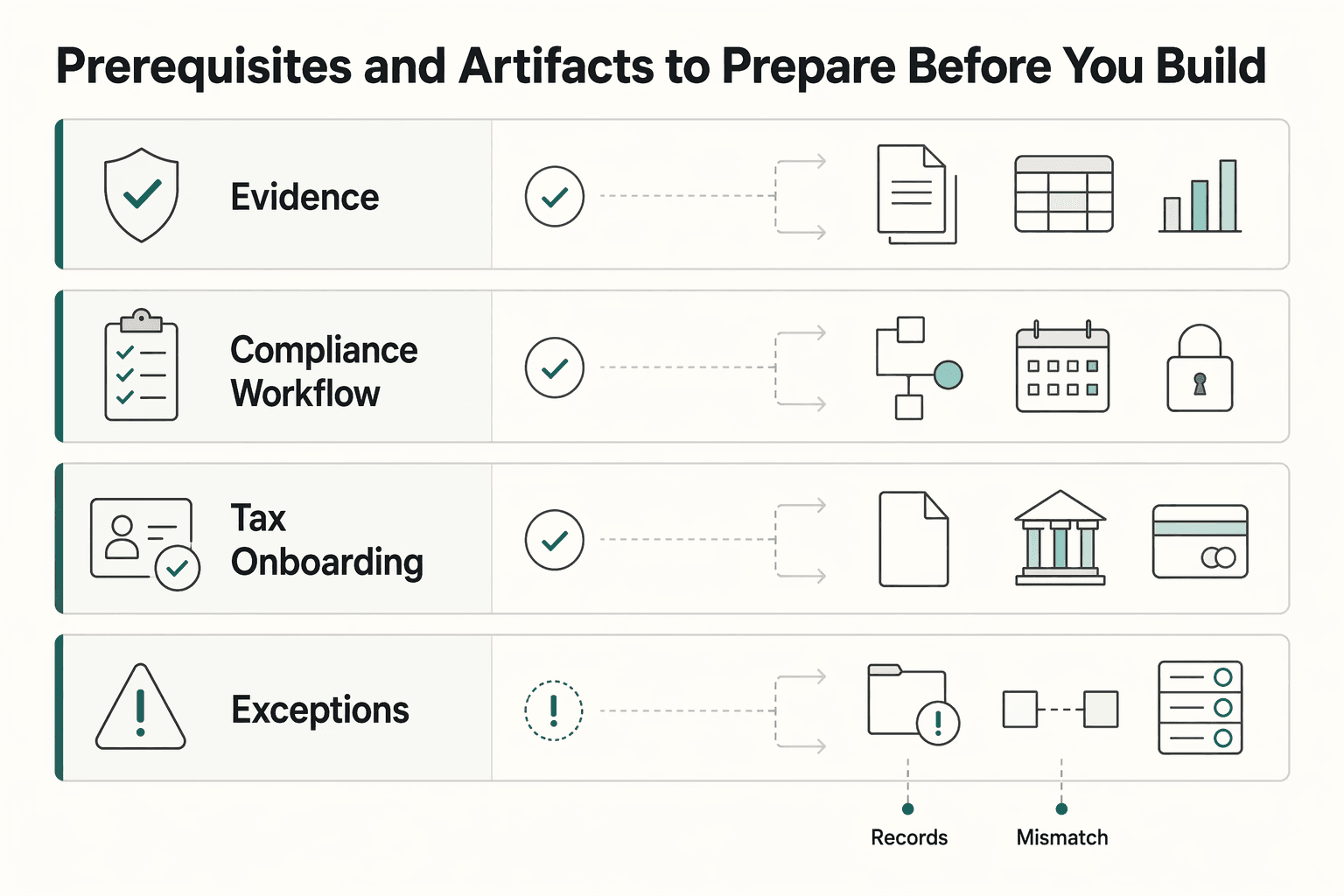

Prerequisites and artifacts to prepare before you build#

Do not build the launch path until your evidence pack is complete and each artifact has a release gate. A card can be issued earlier, but it is not spend-ready until ownership, status source, and blocking rules are explicit.

| Artifact | Owner | System of record | Release gate |

|---|---|---|---|

| Launch scope and acceptance evidence | Product + operations | Scope memo or launch spec linked to ticketing | In-scope contractor/vendor flows are named, target jurisdictions are listed, acceptance is confirmed for the intended payment path, and any coverage detail still awaiting verification is recorded as unresolved before launch approval |

| Compliance workflow map | Compliance + onboarding ops | Onboarding tool or case-management queue | KYC/KYB/AML steps, states, blockers, and override rules are documented; unresolved review can allow issued status only, with spend blocked |

| Tax onboarding pack | Tax ops + vendor onboarding | Tax document repository or vendor profile | Required tax records for your program are collected, statused, and retrievable; missing or mismatched records block spend-ready status |

| RACI and exception matrix | Finance + platform ops | Policy doc with named approvers and audit trail | Policy owner, exception approver, and reconciliation sign-off path are named; spreadsheet-only exceptions are not allowed in production |

Before launch, make sure all of this is true:

- Scope is locked in writing: who the contractor and vendor flow is for, what is out of scope, and which payment rail each path assumes.

- Acceptance is verified for your real payment path; supplier acceptance is still a common AP failure point.

- Compliance ownership is unambiguous: who collects onboarding data, who clears review, where status lives, and who can place or remove holds.

Issuedandspend-readyare separate states in your system of record; if readiness requires chat or email confirmation, the gate is too weak.- Tax document operations are defined up front: collection, validation, storage, correction, and retrieval. Gaps should trigger visible holds.

- RACI and exception handling are review-ready: scope and findings are explicit, least privilege and separation of duties are enforced, and audit-failure alerting is defined. CMMC Level 2 is guidance, not a universal legal mandate, but this control pattern is still practical for release gates.

For how these prerequisites map into card product shape, read Virtual Cards for Contractors: How Platforms Can Issue Spend Cards as a Feature. For rail design alongside card programs, read Virtual IBANs for Platforms: How to Give Every Seller Their Own Dedicated Bank Account Number. For operational follow-through after launch, read Expired Card Management for Platform Teams Scaling Card-on-File Payments.

Choose the issuance model that matches your contractor and vendor flow#

Choose the model from the payment pattern first, then add the tightest controls that still let the payment succeed.

Step 1. Pick the card model first#

| Model | Best fit | Default controls to set at launch | Main tradeoff |

|---|---|---|---|

| One-off card for a single planned payment | One payment with low tolerance for misuse | Tight spend limit, short expiration window (including disposable use when supported), fast freeze/cancel path | Lowest flexibility if amount or timing changes |

| Reusable card for repeat payments | Recurring spend in the same payment flow | Spend limits, clear usage boundaries, bounded expiration window, freeze/cancel ownership | Better continuity, but more ongoing control work |

| Broader spend card with merchant-type boundaries | Spend across a narrow merchant set when the exact payee is not known upfront | Merchant-type restriction, spend limits, short review cycle, explicit freeze/cancel ownership | More flexibility, with more exposure if controls are mis-set |

Use a simple rule: if spend is narrow and risk-sensitive, start with the narrowest model and short expiry. Expand only after the pattern is stable.

Step 2. Choose the funding path with explicit failure handling#

After you set the card type, pick the funding path and define failure handling before launch:

- Pre-funded from stored balance: fund before spend, and define how balances are monitored and replenished.

- Just-in-time from treasury workflow: fund near authorization, and define what happens when timing, approval, or posting does not complete as expected.

Do not launch either path until latency expectations, authorization-failure handling, and owner handoffs are documented and tested.

Step 3. Set a hard launch checkpoint#

Before go-live, product, ops, and finance should approve:

- Abuse scenarios for that model: vendor mismatch, retry loops, overspend attempts, or out-of-scope use

- Rollback behavior: freeze/cancel, expiration handling, and reissue ownership

- A measurable reconciliation path from issuance through authorization and finance posting

If you cannot trace one normal payment, one blocked authorization, and one rollback case in your ledger flow, the model is not launch-ready.

Related: How to Find Vendors for Your Platform and Vet Third-Party Providers at Scale.

Also useful: Platform Status Page Best Practices: How to Communicate Payment Outages to Contractors.

Set policy gates before you promise instant spending power#

Treat "instant" as an authorization outcome, not a label. A card should only be considered spend-ready when it can be authorized against its connected wallet balance and active spend controls.

1. Keep issued separate from spend-ready#

Issued means the card exists. Spend-ready means authorization can actually pass with the wallet balance and control rules attached to that card.

If those states are merged, teams and users cannot tell whether a card is merely created or truly usable.

2. Define the gate in policy, then enforce it in product#

Set the exact conditions that must be true before spend is enabled, and make sure the same rule is applied every time. At minimum, you need a usable activity trail built from programmatic issuance records and transaction history so operations can review what happened.

Use card type as part of the gate: single-use cards for fixed invoice-style payments, and card-on-file style cards for recurring charges.

3. Match your "instant" promise to what your program can prove today#

If your flow still depends on setup steps before authorization, say that clearly and avoid promising immediate spend before those gates are met. "Minutes vs. months" can describe go-to-market posture, but your launch claim should still match real authorization readiness in your own program.

Related: Virtual IBANs for Platforms: How to Give Every Seller Their Own Dedicated Bank Account Number.

For more detail, see How to Build a Risk-Based KYC Framework for Your Platform: Tiering Contractors by Risk Level.

Design the control stack as product defaults, not optional toggles#

Make controls part of the default card template, not optional settings applied later. Start each card with least-privilege defaults, then expand only after spend behavior and reconciliation are consistently clean.

Step 1. Build the matrix by use case#

Define one default control set per real use case, then map issuance to that template. Virtual cards make this practical because you can issue separate card details per vendor flow instead of reusing one shared card.

| Use case | Spending limit | Usage cap | Expiration rule | Merchant restriction |

|---|---|---|---|---|

| One-off vendor payment | Fixed to approved amount | Single use | Short auto-expire | Vendor-locked card |

| Recurring vendor spend | Approved recurring amount | Multi-use with cap | Review-based renewal (not open-ended) | Restricted to the named vendor |

| Broader contractor spend card | Low initial limit | Tight cap at launch | Short initial expiry | Restricted to approved merchants supported by your setup |

Merchant restriction is one of the highest-leverage defaults. Locking a card to a specific merchant, then pairing that with auto-expiry, reduces the chance that copied details can be reused elsewhere.

Step 2. Default to least privilege, then expand on evidence#

Set defaults to the smallest limit, lowest cap, shortest expiry, and narrowest merchant scope that still fits the request. Expand only when the spend pattern is stable and your records reconcile cleanly.

If either signal is weak, keep controls tight. Early lock, unlock, or reissue work is usually cheaper than cleaning up broadly usable cards with weak guardrails. Keep a lightweight evidence pack for each template version: use case, rationale, control settings, and mapped provider capability.

Step 3. Assign lifecycle ownership and verify authorization-time enforcement#

Templates alone are not enough. Before launch, assign clear owners for issue, lock, unlock, reissue, and terminate so support, risk, payments ops, and finance are not improvising during incidents.

Then verify controls at authorization time, not only in UI settings:

- Spending limit: attempt a charge above the limit.

- Usage cap: attempt one more authorization after the cap is reached.

- Expiration rule: test a payment after expiry.

- Merchant restriction: try an unauthorized merchant.

If enforcement is unclear at authorization time, treat that control as unproven and keep tighter defaults until validated.

For a step-by-step walkthrough, see How to Build a Spend Control Policy for Virtual Cards on Your Platform.

Related: Building a Virtual Assistant Platform Around Payments Compliance and Payout Design.

Implement API, webhook, and idempotency paths that survive retries#

Retry-safe issuance is mostly an operating model problem: keep one intent record, one accountable owner, and one traceable reporting trail before you scale.

| Step | What to do | Why it matters |

|---|---|---|

| Persist a single intent and retry identity first | Record issuance intent before any provider-side action, require one stable retry identity, and store request identity, retry identity, control template/version, provider reference, and status timestamps | Keeps one authoritative record when requests are retried or delayed |

| Make status processing replay-safe and finance posting single-path | Treat provider status updates as replay-safe inputs, make repeated delivery produce no repeated finance impact, and use one path for final ledger/finance posting | Lowers double-post risk when synchronous responses and async updates arrive out of order |

| Build reporting and ownership for scale | Assign ownership for breaks in the chain and make each issuance traceable end to end: request record, provider reference, ledger outcome, and finance export | Lets your team explain one card request quickly and consistently |

Step 1. Persist a single intent and retry identity first#

Record the issuance intent in your own system before any provider-side action, and require one stable retry identity for that intent. This gives your team one authoritative record when requests are retried or delayed, instead of competing versions of the same action.

Keep the intent record complete enough for review and handoff:

- request identity

- retry identity

- chosen control template/version

- provider reference, when assigned

- status timestamps from accepted to final posted state

Step 2. Make status processing replay-safe and finance posting single-path#

Treat provider status updates as replay-safe inputs, especially when updates are delayed or duplicated. The practical rule is simple: repeated delivery should not create repeated finance impact.

Use one path to create the final ledger or finance posting for issuance state, and keep other paths read-only for that step. This reduces double-posting risk when synchronous responses and asynchronous updates arrive out of order.

Step 3. Build reporting and ownership for scale, not just happy-path flow#

At scale, reporting and ownership are control surfaces, not admin overhead.

Define who owns breaks in the chain and make every issuance traceable end to end: request record, provider reference, ledger outcome, and finance export. If your team cannot answer what happened to one card request quickly from that trail, your retry path is not ready for larger volume.

Related: How to Scale a Gig Platform From 100 to 10000 Contractors: The Payments Infrastructure Checklist.

Also useful: How Platform Operators Pay Contractors in Indonesia With GoPay, OVO, DANA, or BI Fast.

Run treasury and reconciliation without manual cleanup drift#

Treasury and reconciliation stay stable when you run them as one control loop: define ownership before issuance, work exceptions in a reporting system every day, and reconcile from source artifacts instead of dashboard totals alone.

Step 1. Set funding and ownership before you mark spend as ready#

Choose the funding posture and account ownership model before cards go live, then keep that decision visible in your operating records. If you cannot quickly confirm how a card is funded and who owns the next action, drift starts early.

Program operations are easier to manage when account setup, account management, and issue resolution are explicitly assigned, not handled ad hoc.

Step 2. Treat daily exception handling as core operations#

A clean dashboard is not enough; unresolved exceptions are where control breaks compound. Keep a daily queue in your reporting workflow, and require each item to have a named owner, current status, and next action.

This keeps your process aligned with a formal review lane rather than waiting for month-end cleanup.

Step 3. Reconcile against records, not snapshots#

Reconcile using source artifacts from your card program reporting system, provider settlement records, and your internal ledger journal. Tie those records together with shared identifiers so one transaction can be traced end to end.

Use dashboard views for visibility, but do not treat them as final proof that postings and settlements agree.

Step 4. Run a recurring review process to contain risk drift#

Use a recurring review process and data analytics to monitor compliance and inform management decisions, not just to produce reports. Focus reviews on patterns that signal growing exposure, including repeated exceptions and unresolved account issues.

The goal is practical: improve efficiency while maintaining internal controls that reduce fraud, misuse, and delinquency risk over time.

Related: Offer Spending Accounts to Contractors with Embedded Debit Controls.

Common mistakes and how to recover quickly#

Most launch damage comes from promising speed before proving control. The quickest recovery is to tighten card use rules first, then scale access after controls and tracking are stable.

| Mistake | Recovery |

|---|---|

Treating issued and ready to use as the same thing | Make the user-facing status explicit in your own workflow, and only mark cards as usable after core controls are in place. |

| Launching broad permissions too early | Move back to least-privilege defaults: vendor-locked, one-time, or limited-purpose cards with clear limits. |

| Retrying payments without clean tracking | Before resending, verify the payment trail for that invoice in your tracking flow. If records are unclear, pause new retries until the prior attempt is reconciled. |

| Letting reconciliation stay manual for too long | Treat invoice reconciliation and payment tracking as an operating control, not cleanup work for later. Tighten controls and reduce exception handling before adding volume. |

Use the table for the quick scan. The playbooks below add the operator steps that matter when you need to recover fast.

- Mistake: treating "issued" and "ready to use" as the same thing.

Recovery: Make the user-facing status explicit in your own workflow, and only mark cards as usable after core controls are in place. Before you share card details, confirm the spend scope: single-use or multi-use, limits, and merchant restrictions.

- Mistake: launching broad permissions too early.

Recovery: Move back to least-privilege defaults: vendor-locked, one-time, or limited-purpose cards with clear limits. Virtual cards are designed to support this tradeoff, and narrower scope helps contain exposure if a supplier system is compromised or a convincing fake invoice gets through. Supplier acceptance is a real constraint, but it is not a reason to make every card broadly reusable. If you need help tightening defaults, see How to Build a Spend Control Policy for Virtual Cards on Your Platform.

- Mistake: retrying payments without clean tracking.

Recovery: Before you resend, verify the payment trail for that invoice in your tracking flow so one obligation does not become multiple payment attempts. If records are unclear, pause new retries until the prior attempt is reconciled.

- Mistake: letting reconciliation stay manual for too long.

Recovery: Treat invoice reconciliation and payment tracking as an operating control, not cleanup work for later. If your team is already spending heavy manual time each month, for example ~20 hours, tighten controls and reduce exception handling before adding volume.

Early warning signals: rising manual reconciliation hours, repeated resends tied to the same invoice, frequent "exception" handling, and growing supplier acceptance friction.

Related: How Platform Operators Pay Contractors in Colombia with PSE Nequi and DIAN Controls. Also useful: Virtual Cards for Contractors: How Platforms Can Issue Spend Cards as a Feature.

Conclusion and copy-paste launch checklist#

Treat launch as earned, not declared. If card creation works but controls, retries, and reconciliation are still shaky, you are not ready to expand. A practical go-live rule is simple: do not broaden rollout until blocked and approved authorizations behave as expected, duplicate events do not create duplicate outcomes, and finance can trace a transaction from card record to ledger entry without guesswork.

Use the checklist below in your launch review, and require evidence for every row. If a provider or internal team claims a capability you have not verified yet, mark that capability as unresolved instead of treating it as production truth.

| Launch step | Verification | Watch-out |

|---|---|---|

| Step 1. Choose the narrowest issuance model per use case | From one record, confirm the vendor, approver, intended use, and stop condition are all visible. | "General vendor spend" on a reusable card can create permission sprawl early. |

| Step 2. Set default controls before exceptions | Run one approved authorization and one intentionally blocked authorization, then confirm both outcomes appear in the same operator view. | A control shown in a template or UI is not proven until the authorization result matches it. |

| Step 3. Prove retry-safe card-state handling | Replay a duplicate create or update event in staging and confirm you still end with one card, one approval, and one spend path. | Happy-path issuance can look fine while delayed or duplicate updates still create double processing. |

| Step 4. Confirm finance traceability before wider rollout | Trace one real or test transaction from card record to transaction export to posted ledger line without manual screenshot stitching. | If ops or finance needs inbox searches and ad hoc CSV joins to explain a charge, expansion will multiply cleanup. |

| Step 5. Publish promise caveats by market and program | Review product copy, sales language, and support macros for "where supported" or equivalent caveats tied to actual tested coverage. | "Instant" is not universal. Visa public rules also note some operational and security details are omitted, and some rules apply only within the relevant region or country. |

| Step 6. Run the final readiness pass on state integrity and ownership | Sample active cards and confirm issued is distinct from spend-ready, funding and controls are live, and every exception queue has a named owner. | If exceptions belong to "ops" in general, they usually belong to no one when a disputed or stuck payment appears. |

A few judgment calls matter more than the rest. First, model choice can drive risk more than launch copy. Start with purpose-bound or disposable behavior where you can, then move into reusable access only after the owner, vendor, and stop condition stay clean in live operations. Second, do not confuse a technical event with an operating state: issued should mean the card record exists, while spend-ready should mean the funding path, controls, and monitoring are actually live.

This is also where teams tend to get sloppy with messaging. The useful standard is not "the provider says this is instant." It is "we tested this use case in this market and saw the expected authorization and monitoring outcome." Publicly available Visa Core Rules and Visa Product and Service Rules are not a full operational spec, and region- or country-specific rules are not universally applicable. In supplier programs with contractual requirement sets, non-compliance may be treated as a material breach and can lead to termination, and conflicting requirements may default to the more restrictive obligation. Your launch language should follow tested coverage and applicable contracts, not your broadest assumption.

If your launch review gets stuck on control design, use this deeper guide on how to build a spend control policy for virtual cards on your platform.

Paste this checklist into the launch review doc, assign an owner and evidence artifact to every row, and do not approve production expansion until all six gates are proved.

Frequently Asked Questions

What is instant virtual card issuance for contractors, and what is still not instant in practice?

A virtual card is a payment card that exists only in digital form, and it is commonly used for online purchases or subscription payments. “Instant” usually refers to how quickly a card-issuing platform can create the card details, not to universal vendor acceptance or every downstream step moving at the same speed. Your checkpoint is simple: create a test card and confirm the authorization and monitoring events appear in the same admin view your support team actually uses.

Does issued mean the card is spend-ready?

No. In operational terms, “issued” should mean the card record exists, while “spend-ready” should mean the funding path is live, the controls are attached, and ops can see the card event if something goes wrong. If your team still has to ask finance whether funds are available or whether the card is restricted correctly, treat it as issued only.

Which controls should be mandatory at launch for contractor and vendor card programs?

Make spend limits, merchant restrictions, expiry or disposable-card behavior, and freeze or cancel actions non-optional at launch. Those controls help reduce misuse, abuse, and fraud risk without blocking legitimate spend. Before any live card is sent out, open the live record and verify the settings there, not just in a template or product spec.

How can a platform give vendors instant spending power without weakening control?

Start narrow. A card with a defined limit, clear usage restriction, and disposable behavior for one-off payments gives you speed without handing out broad reusable access. As an operator check, run one approved test authorization and one intentionally blocked authorization so you know the controls work in practice, not just on paper.

Does instant issuance mean funds are immediately usable in every market?

No. Fast card creation does not mean every supplier or merchant will accept virtual card payments in every country or use case, and supplier acceptance is a known implementation challenge in AP-style programs. In each target market, test with real vendors before you promise “instant” externally, and use “where supported” language in rollout copy.

What should product teams evaluate first when comparing providers?

Start with the control surface and monitoring, not the demo polish. You want API-based virtual card issuance, real-time monitoring, and card-level controls such as limits, merchant-type restrictions, and immediate freeze or cancel actions. Ask the provider to show one successful authorization, one blocked authorization, and the resulting audit trail in the admin console or equivalent account-management view.

What usually breaks first when issuance volume grows?

Ownership and oversight are common early failure points. If reusable cards stay active without a named owner responsible for purchases and account management, misuse risk increases. Review active cards regularly. Make sure each one still has a current purpose, a current limit, and a clearly assigned owner. If supplier payment acceptance is the issue rather than control design, this short guide on ePayables and virtual card payments is the more relevant comparison.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/sites/default/files/page_file_uploads/far-co...trusted

- apps.sceis.sc.gov/SCSolicitationWeb/attachmentDisplay.dotrusted

- charlestoncounty.gov/departments/procurementtrusted

- csudh.edu/procurement-contracts/csubuytrusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2.pdftrusted

- ecfr.gov/current/title-15/subtitle-B/chapter-VII/subc...trusted

- gsa.gov/buy-through-us/purchasing-programstrusted

- hks.harvard.edu/sites/default/files/centers/mrcbg/Final_AWP_...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Virtual Cards for Contractors and the Real Cost of Getting Issuance Wrong

Virtual cards deserve a serious look if you need tighter control over contractor spend without turning payments into a bottleneck. For most teams, a practical place to start is a virtual card tied to an approved invoice or request. They can reduce misuse risk compared with standard corporate cards and speed some supplier payments, but they do not fix weak approval logic, poor accounting links, or fuzzy ownership between AP and product ops.

Virtual IBANs for Platforms: How to Give Every Seller Their Own Dedicated Bank Account Number

If you want to give each seller their own receiving bank details without opening a separate traditional account per seller, start by treating this as an account-mapping and controls decision, not just a UI feature. In common setups, a virtual IBAN looks like a standard IBAN but points to an underlying master payment account rather than a standalone account.

What Are ePay/ePayables? How Platforms Replace Paper Checks with Virtual Card Payments

If you are replacing checks in a high-volume environment, treat this as a controls-and-scale decision first. The goal is to choose the right ePayables model, introduce virtual cards without creating avoidable new exceptions, and keep reconciliation and audit trail intact from the AP source record through payout.