Quick Answer

Start by shipping the smallest contractor card scope that keeps traceability intact from approved request to payment to ledger entry. For most teams, that means single-use issuance linked to invoice approval, then expanding only after reconciliation and exception handling are stable. A virtual cards contractors platform feature works well when controls run before authorization and event data supports clean matching in systems like QuickBooks Online, Xero, NetSuite, or Microsoft Dynamics 365 Business Central.

Virtual card control starts with knowing which issuance model you need#

Virtual cards deserve a serious look if you need tighter control over contractor spend without turning payments into a bottleneck. For most teams, a practical place to start is a virtual card tied to an approved invoice or request. They can reduce misuse risk compared with standard corporate cards and speed some supplier payments, but they do not fix weak approval logic, poor accounting links, or fuzzy ownership between AP and product ops.

Start with the simple version. A virtual card is digital-only and can be created quickly for a specific spend context. That matters because you can issue a card for a named contractor, vendor, purchase, or subscription instead of handing out a broad, reusable payment instrument. In invoice-led flows, some AP tools also let teams select approved invoices for card payment and automate card generation at higher volume. At that point, the feature stops being a convenience and starts becoming a controlled product surface.

The real decision is not whether virtual cards are useful. It is which issuance model fits your program. A platform adding a contractor card feature to its wallet experience will care about different tradeoffs than a finance team upgrading back-office AP. One team may care most about merchant restrictions and clean ledger mapping. Another may care more about repeat-merchant continuity, contractor experience, or how card events fit alongside other payout methods.

A good implementation keeps the payment promise narrow and testable. Before you commit roadmap time, verify four things with any provider or issuing partner:

- Where control actually lives: Can you constrain who gets paid and how much gets spent, or are you only getting a card number with better reporting after the fact?

- How invoice linkage works: If your flow starts from approved invoices, confirm that cards can be generated from that approval state rather than from a separate manual step.

- What event data you receive: You need enough authorization and settlement detail to post transactions correctly and investigate exceptions.

- Where acceptance and coverage break down: Do not assume every contractor or supplier will take card payments, or that program rules hold across every market.

The rest of this guide compares the strongest patterns for platform teams building contractor wallets, AP-led issuance, and payout-adjacent spend controls. The goal is practical: which option gives you the cleanest controls, which one creates the most reconciliation overhead, and which launch checks should block rollout if they are still shaky.

If you keep one rule in mind, make it this: ship the smallest card feature that preserves traceability from approval to payment to ledger entry. If you cannot explain that chain clearly, faster issuance usually creates more cleanup than value. For a step-by-step walkthrough, see How Independent Contractors Should Use Deel for International Payments, Records, and Compliance.

Choose the right feature path before you build#

Decide this first: are you optimizing for tighter misuse control or lower repeat-use friction. If misuse risk is your main constraint, start with a Single-use virtual card. If repeat merchant continuity matters more, use a Multi-use virtual card only with tighter policy gates.

This is a product and operations decision for teams adding card spend to contractor wallets with traceable controls, not a generic AP explainer. If your need is narrower, a back-office AP flow that lets you select approved invoices for card payment and trigger virtual card generation can be enough without turning cards into a wallet feature yet.

Use these criteria to rank options:

- Control depth: prioritize controls enforced before approval, not reporting after the fact. Strong programs support spend rules plus merchant, location, channel, and time controls, with per-card limits like spend caps, expiration, and supplier restrictions.

- Reconciliation burden: favor flows that preserve a clean trail from approved request to card use. Single-purpose cards can be scoped to a specific supplier, amount, and timeframe, which usually makes exception handling simpler.

- Contractor experience friction: virtual cards can be created and used immediately, which helps urgent approved spend. Single-use reduces blast radius; multi-use reduces repeat-merchant friction but needs consistent guardrails, for example merchant-category and policy conditions.

Before you commit roadmap time, validate two implementation points in a test environment: how cards are requested with explicit controls and limits, and whether issuance can start directly from an approved invoice/payable state instead of a separate manual step.

Set stakeholder expectations early: coverage and compliance are program- and market-specific, so do not assume one setup will hold across every country or card program.

Compare the best implementation options at a glance#

If you need the most control and the cleanest audit trail, start with Single-use virtual card. Choose Multi-use virtual card when repeat merchant continuity matters, Lodged card only for tightly scoped centralized patterns, and AP automation with card issuance when you want invoice-driven card payments without building wallet UX yet.

| Option | Best for | Core controls | Ops overhead | Failure modes | System dependencies | Reconciliation expectation | Payment-rail boundary | Provider unknowns to confirm |

|---|---|---|---|---|---|---|---|---|

| Single-use virtual card | Invoice-linked or approval-linked spend where you want one card per purchase | Per-transaction card creation, spend limits, expiration, merchant category controls, supplier restrictions where supported | Higher issuance volume, but cleaner exception handling | Declines from merchant-category mismatch, expiration, over-limit attempts, orphaned auth vs later settlement | Issuer/processor support for per-card policy controls plus auth/settlement events tied to approval objects | Cleanest matching path. QBO can surface connected transactions for categorization, Xero can import daily feeds, NetSuite can use CSV import for charges/refunds, and Business Central can reconcile imported transactions | Replaces some card-eligible spend; coexists with ACH transfer and Wire transfer for coverage/finality gaps | Confirm authorization behavior by network/merchant type, settlement timing by country/payment method, and supplier acceptance |

| Multi-use virtual card | Repeat purchases with approved merchants or recurring contractor spend | Reusable card with spend caps, velocity rules, merchant category limits, and time controls where offered | Moderate: fewer issuances, more monitoring for drift | Card-on-file reuse after approval context changes, incremental auth edge cases, repeated misuse | Strong policy engine, lifecycle controls, and reliable webhook/event delivery | Works if approval and merchant metadata stay attached across many lines; QBO/Xero/NetSuite/Business Central patterns above still apply | Usually coexists with ACH transfer; rarely replaces Wire transfer where immediate finality is required | Confirm repeated-authorization behavior, card usability window after updates, and merchant acceptance for stored-card flows |

| Lodged card | Narrow, centrally managed recurring spend with approved intermediaries/merchants | Central account number held by an intermediary or approved merchant | Lower end-user support, higher central oversight | Weak user-level attribution, larger blast radius if controls loosen, merchant dependency | Explicit provider support for lodged-card behavior in your use case | Import paths into QBO/Xero/NetSuite/Business Central may work, but line-level attribution is often the constraint | Typically coexists with ACH transfer and Wire transfer, not a full replacement | Confirm acceptance terms, statement detail granularity, settlement timing, and whether identifiers survive into settlement data |

| AP automation with card issuance | AP-first teams paying approved invoices by card without contractor-facing wallet features | Invoice selection for virtual-card payment generation with payables approvals | Lower product overhead, moderate accounting setup | Supplier card refusal at payment time, weak contractor UX, fragile mapping if export paths are manual | AP tool must support selecting invoices for virtual-card payment and exporting accounting-ready records | Strong when invoice state is the source of truth; QBO/Xero often easier with feeds/connectors, NetSuite often CSV-disciplined, Business Central depends on imported matching | Replaces part of manual AP disbursement choice; commonly coexists with ACH transfer and sometimes Wire transfer | Confirm supplier acceptance, settlement timing against invoice-close rules, and visibility of auth/settlement events outside the AP tool |

Do not optimize this choice for issuance speed alone. Validate month-end survivability with a test export that includes approval ID, invoice ID, merchant, amount, and settlement date, then verify the exact import and match path in your accounting stack.

Cards usually replace a controlled subset of spend, not every payment rail. ACH remains an efficient, low-cost batched rail, and Fedwire remains real-time gross settlement with immediate, final, irrevocable transfer once processed.

Acceptance is a scale constraint, not a side note. Mastercard reports 89% of suppliers struggle to balance their own needs with B2B customer needs, so treat adoption forecasts as provisional until providers show live evidence for authorization behavior, settlement timing, and acceptance coverage in your target markets.

Best for tight control with invoice-linked spend#

Choose a single-use virtual card when the invoice is your approval object and misuse risk matters more than repeat-purchase convenience. In AP, this keeps spend tightly bounded to one supplier, one authorized amount, and one expiration window, with invoice details carried in remittance where supported.

| Launch check | What to confirm |

|---|---|

| Supplier restriction | Works for invoice or PO payment flows. |

| Exact-amount authorization | Behaves as expected with your target merchants. |

| Remittance and export data | Includes invoice reference, approved amount, and settlement date. |

| Supplier acceptance | Validated in practice, not assumed. |

The value here is precision. J.P. Morgan describes one-time cards tied to a specific supplier, amount, and expiration date, and SAP Concur documents one-time, exact-amount vendor use. That sharply limits blast radius if credentials are stolen or reused, because charges are constrained by both amount and supplier context.

This pattern also supports cleaner Automated reconciliation when metadata is consistent. The key fields are practical: authorized amount, expiration date, and invoice references. With those fields preserved through authorization and settlement, finance can map transactions to invoice records without relying on merchant text alone.

A common flow is straightforward: a contractor submits an invoice-backed purchase request, AP approves it, the platform issues a one-time card for the exact amount and approved supplier, the supplier charges once, and settlement is matched back to the invoice. If your issuer supports it, the credential can then be retired after payment is confirmed.

The tradeoff is operational overhead. Single-use means more card issuance events, more expired-card edge cases, and more support when someone tries to reuse a credential for a follow-on purchase. That is usually the signal to evaluate multi-use later, not to loosen controls early.

Before launch, reconfirm the same points with your provider:

- Supplier restriction works for invoice or PO payment flows.

- Exact-amount authorization behaves as expected with your target merchants.

- Remittance and export data includes invoice reference, approved amount, and settlement date.

- Supplier acceptance is validated in practice, not assumed; Oracle ERP's invoice-card flow explicitly treats supplier onboarding as part of the operating model.

Single-use gives you the strongest control starting point, but it is not automatic reconciliation and it does not guarantee universal acceptance.

Best for recurring contractor and supplier relationships#

For approved recurring merchants, a Multi-use virtual card or, in some programs, a Lodged card is usually the right default when continuity and speed matter more than issuing a new card each time.

This model works best for stable recurring spend, including subscriptions, memberships, vendor services, and repeat supplier replenishment. It can reduce repeated issuance and approval handling, especially when your program supports recurring payouts and dedicated virtual cards per vendor.

The tradeoff is policy drift across billing cycles. Keep controls at the issuer layer so they act before authorization, with Merchant category limits plus spending limits and geographic controls where supported, rather than relying only on after-the-fact review.

Before rollout, confirm:

- You can issue a dedicated card per recurring vendor, not one shared credential across unrelated merchants.

- Reporting and notification data support reliable reconciliation by vendor, cycle, and transaction history.

- Controls match the recurring pattern and can be tightened quickly if usage drifts.

A practical use case is a mixed contractor/supplier program where approved SaaS tools renew monthly and suppliers replenish on a repeat schedule. Keep recurring merchants on this path with tight controls, and move outliers back to Single-use virtual card flows when category or cadence drifts.

Best for embedded spend controls inside contractor wallets#

This is the best fit when you already run Contractor wallets: issue Virtual cards from the same balance layer so spend, funding, and policy checks stay in one system. If you do not already own wallet balances and payout status in-product, this path can become operationally heavy.

| Item | Type | Detail |

|---|---|---|

| Cleaner product UX | Benefit | Balance, payout status, and card activity can live in one surface. |

| Tighter control coupling | Benefit | Rule-based authorization controls can enforce your Spend control policy at authorization time. |

| Better lifecycle visibility | Benefit | Authorized spend can be shown as reserved first, then deducted at capture. |

| Duplicate posting risk | Risk | Webhook endpoints can receive the same event more than once, so ingestion and retry paths must be idempotent. |

| Timing assumptions | Risk | Some issuer flows require near-real-time authorization decisions, and uncaptured authorizations can expire. |

| Event-model mismatch | Risk | Verify your provider exposes pending vs. settled states clearly enough for your ledger and UI. |

The key architecture decision is linking each payment instrument to the contractor's balance account. In providers that support this model, card authorizations and captures reconcile against that same account, so you can track funding, reserved amounts, deducted amounts, and remaining balance in one ledger view. Contractors are an explicit supported user type in this balance-platform structure.

In practice, that gives you a cleaner product UX, tighter control coupling, and better lifecycle visibility. It also creates the failure modes in the table above: duplicate posting, timing assumptions, and event-model mismatches.

Before launch, confirm three items:

- Each card is linked to the correct contractor balance account, not a shared program pool.

- Your transaction rules enforce the exact category and policy gates you require at authorization.

- Webhook consumers and retry paths are idempotent, and duplicate-event behavior is covered in QA.

If your use case is funded contractor balances with category restrictions and payout eligibility gates, this is the right pattern. If you mainly need back-office payable controls, stay closer to AP-first issuance and avoid wallet-card coupling until you can support it operationally. Related: Best Business Credit Cards for Airline Miles for Global Freelancers.

Best for AP-first teams modernizing without a full wallet build#

For teams that already run on payable queues, an AP-led virtual card program is usually the most practical way to add controlled card spend without taking on a full wallet build first.

Use it as a multi-rail setup, not an all-or-nothing replacement: keep ACH transfer and Wire transfer where they fit, and add virtual cards for invoices where tighter controls or supplier acceptance make sense. Oracle's supplier-invoice flow reflects this model: set up a bank-backed virtual card program, update supplier profiles, and choose invoices to pay by card instead of only ACH, wire, or check.

The early win is operational clarity, not a new contractor-facing product surface. Tying issuance to approved invoices can improve approval visibility and support cleaner Automated reconciliation workflows. In NetSuite, payment automation includes status tracking across ACH, check, and virtual-card forms. In QuickBooks Online, reconciliation outcomes are connector-specific, so validate actual integration behavior before making broad promises.

Before launch, verify:

- Each issued card is invoice-scoped or otherwise controlled; in Mastercard's AP virtual-card flow, at least one control is required per card or transactions can fail.

- Your accounting evidence chain works end to end: approved invoice ID, supplier or contractor record, payment status updates, and export mapping into NetSuite or QuickBooks Online.

The tradeoff is straightforward: this path can lower initial implementation scope for AP modernization, but it offers less contractor-facing differentiation than wallet-native issuing. If your near-term priority is cleaner approval operations plus accounting or ERP sync, this is the right pattern.

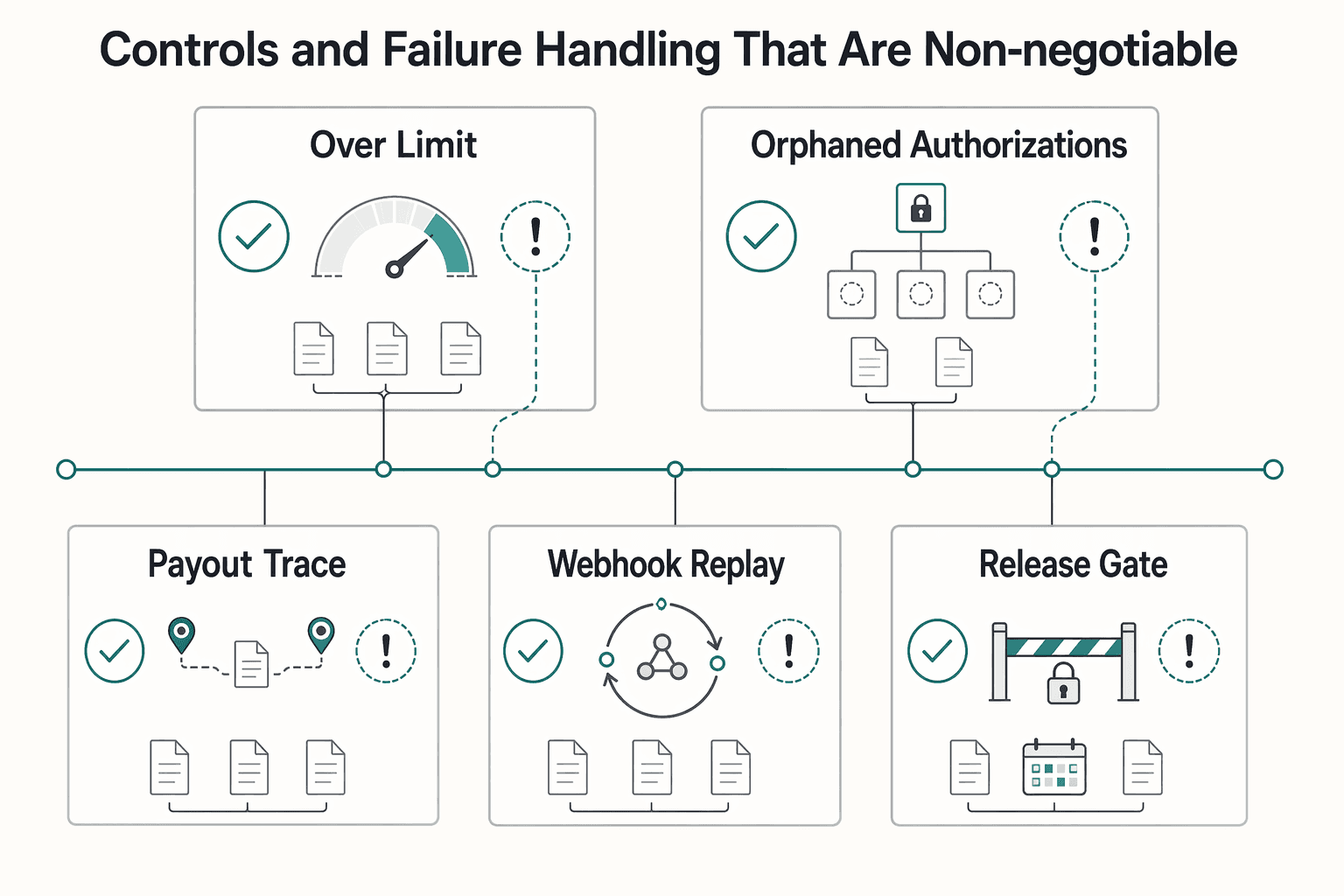

Controls and failure handling that are non-negotiable#

Do not scale card issuance until you can prove the full path from request intake to accounting closeout. The core risks usually show up downstream: duplicate ledger effects, unexplained declines, and exports finance cannot trust.

| Failure scenario | Handling note |

|---|---|

| Over-limit authorization attempts | Tie them to decline reasons such as limit or velocity exceeded. |

| Orphaned authorizations | Build explicit handling for authorizations that never settle. |

| Delayed settlement | Handle settlement after approval-window or accounting-period changes. |

| Duplicate webhook delivery | Use idempotency keys on requests and deduplication in webhook handling so retries do not create duplicate operations. |

| Stale approval context | Keep the operating sequence fixed so cards do not stay active after the original request is no longer valid. |

- Lock the operating sequence before tuning limits.

Keep this order fixed: request intake, policy and approver check, card issuance, authorization and settlement webhooks, ledger posting, then export and closeout. If those steps blur, stale approval context can leave cards active after the original request is no longer valid.

Make traceability mandatory: each card should map to the source request, approver decision, contractor or supplier record, and invoice or purchase reference. For virtual cards, include control payloads at issuance. Mastercard is explicit that at least one control must be set per virtual card or transactions will fail. In practice, teams commonly start with amount and date controls, then add supplier or MCC restrictions where appropriate.

- Design for retries, duplicates, and event timing issues from day one.

Treat webhooks as non-deterministic inputs: events can be out of order, partial, or duplicated. Use idempotency keys on requests and deduplication in webhook handling so retries do not create duplicate operations.

Apply this in two places: issuance calls, to prevent duplicate cards on retry, and ledger ingestion, to prevent duplicate postings from repeated auth or settlement events. Regularly replay the same event payload and verify you get one ledger effect, not two.

Build explicit handling for:

- over-limit authorization attempts tied to decline reasons such as limit or velocity exceeded * orphaned authorizations that never settle * delayed settlement after approval-window or accounting-period changes * duplicate webhook delivery * stale approval context

Do not treat authorization as final cash movement. Authorizations can expire, and validity windows vary by card scheme. Your ledger should separate pending authorization from settled spend.

- Ship only with a release evidence pack finance can use.

Require the same artifacts every release: control matrix, decline taxonomy, reconciliation exception log, and accounting export tests for Xero and Microsoft Dynamics 365 Business Central.

| Artifact | What it must prove | | --- | --- | | Control matrix | Which controls are enforced by card type, merchant class, amount, date, and supplier | | Decline taxonomy | How provider decline codes are grouped into customer action, policy failure, merchant issue, and retryable processing error | | Reconciliation exception log | Which auths, settlements, reversals, and exports did not match, and who owns resolution | | Export tests | That Xero and Microsoft Dynamics 365 Business Central receive expected payment records without field loss or duplication |

Keep export tests concrete. In Xero, test the payment-file route used in bill-payment batches, including expected bill-paid behavior. In Microsoft Dynamics 365 Business Central, test vendor-payment export from Payment Journals. Neither path guarantees zero exceptions, so the exception log is part of launch criteria.

- Use hard stop rules when quality signals degrade.

If authorization failures exceed your internal tolerance, tighten Merchant category limits before expanding card limits, and review decline patterns first. Broad merchant access often creates policy-shape failures that look like limit pressure. For control design details, use this spend control policy guide.

Apply the same discipline to accounting integrity. If Automated reconciliation is unstable, pause new cohorts until it is stable again. Expanding volume on top of unresolved reconciliation breaks usually increases closeout risk.

Conclusion#

After comparing the options, the practical answer is straightforward: treat cards as a controlled product surface, not as a loose payment add-on. If you cannot show how a request becomes an authorization record, then a categorized transaction record, then a ledger entry backed by usable reporting, keep the rollout narrow.

- Build issuance around controls and references

A real card feature is more than card creation. The supported pattern is issuance with spending controls, custom reference data, and payment beneficiaries attached at the start, because that is what gives you enforceable policy and usable context later. The key difference is timing: spending controls run before real-time authorizations and can decline a purchase, so you are stopping bad spend in the decision path rather than trying to clean it up after settlement.

- Expand only after ops prove they can carry the load

Start with the option that matches your risk and operational maturity, then widen scope once the basics are stable. For many teams, that means beginning with a tighter issuance scope, then broadening only after reconciliation is dependable. The checkpoint is not user demand. It is whether your team can consistently reconcile balance activity and categorized transaction history without manual guesswork. As payment capabilities grow, your internal controls need to keep pace rather than trail behind.

- Treat traceability as the scale gate

Before you issue to larger cohorts, test whether you can explain each step in plain English: who requested the spend, which rule allowed it, what happened at authorization, what was recorded in transaction history, and how finance recorded it. Authorization traceability is stronger when you retain the history of every time a pending request authorization was approved or declined, because that gives audit and operations a clean decision record instead of a black box. The red flag is simple: if exceptions live in inboxes, spreadsheets, or tribal knowledge rather than in reporting your team can inspect, you are not ready to scale issuance.

The best verification step is also the least glamorous. Pull a sample of transactions and walk them end to end from request record to authorization history to categorized transaction history to internal ledger posting. If that walkthrough breaks on edge cases, or if your team cannot explain unmatched activity quickly, pause expansion and fix the handling first.

That is the real standard for a contractor card feature. Not how many cards you can issue, but how well you can control, trace, and reconcile them when something goes wrong. Related reading: The Best Travel Credit Cards for Digital Nomads.

Frequently Asked Questions

What is a virtual card feature for contractors on a platform?

A virtual card feature gives a contractor a digital card credential with configurable spending controls, so they can make a card transaction without you issuing a plastic card. The useful distinction is control: you can restrict where and how much it can spend instead of sending a general cash payout and hoping policy is followed.

How do I choose between a single-use virtual card and a multi-use virtual card?

Pick single-use when you need tight invoice- or purchase-level control, because one card per transaction can create a cleaner one-to-one link between approval, spend, and reconciliation. Pick multi-use when you want an ongoing card pattern and are prepared to enforce ongoing controls. If misuse risk is your main concern, start with single-use and expand later. For a deeper build pattern, see Virtual Credit Cards for Platforms: How to Issue Single-Use Cards for Contractor and Vendor Payments.

What controls are required before issuing contractor spend cards?

At minimum, your card program should enforce spending controls such as merchant category, country, merchant ID, and limits per authorization or per month. The practical checkpoint is whether each issued card ties back to an approved request and spend context. If those links are weak, exception handling and closeout become harder to manage.

How do virtual cards improve reconciliation in contractor payment operations?

They help when you attach the card to a specific project, business unit, or invoice context, because that gives finance a clearer path from spend to ledger posting. The win is not automatic. You still need reliable reconciliation processes, and the card itself will not fix accounting noise on its own.

When should virtual cards coexist with ACH transfer and wire transfer?

Most teams should treat cards, ACH, and wires as complementary rails rather than an either-or choice. ACH has operating-window constraints and does not currently settle on weekends and federal holidays, so it is not always the right tool for time-sensitive contractor spend. Fedwire, by contrast, is immediate, final, and irrevocable once processed, which makes it a better fit for urgent, high-certainty funds movement than merchant spend.

What does a virtual card feature not solve without wallet, payout, or compliance modules?

Cards do not replace wallet ledgering, payout orchestration, or compliance operations on their own. If you need balance tracking, payout eligibility, or a contractor-facing money movement view, you still need those product surfaces and ledger rules. You also cannot ignore KYC and AML work. Identity verification is operationally complex and ongoing, even when a provider handles parts of the regulatory and bank relationship stack for you.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- consumerfinance.gov/ask-cfpb/what-is-a-wire-transfer-en-1163trusted

- docs.stripe.com/issuing/controls/spending-controlstrusted

- federalreserve.gov/paymentsystems/fedfunds_about.htmtrusted

- occ.gov/publications-and-resources/publications/comp...trusted

- stripe.com/issuingtrusted

- corpay.com/commercial-cards/virtual-cardsexternal

- coupa.com/products/ap-automation/virtual-cardsexternal

- coupa.com/blog/how-virtual-cards-for-b2b-payments-impr...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Virtual Credit Cards for Platforms: How to Issue Single-Use Cards for Contractor and Vendor Payments

Single-use virtual cards are often positioned as a fit for controlled vendor payments, but not for every contractor payout. This guide helps product, Payments Ops, and AP teams decide whether virtual cards fit their operating model, or whether cards belong alongside ACH, checks, or other payout rails.

Virtual Card Issuance for Platform Contractors With Controlled Vendor Spend

Fast issuance matters only when policy comes first and every card action can be traced afterward. If you cannot tell who requested a card, what it can buy, where it can be used, and how it lands in finance records, you do not have a launch-ready virtual card program.

How to Build a Spend Control Policy for Virtual Cards on Your Platform

Treat virtual-card spend control as a product and infrastructure decision from day one. If you reduce it to a few card settings, you may issue cards quickly. You can also end up with weak ownership, inconsistent approvals, and records that are harder for finance to reconcile later.