Quick Answer

The best travel credit cards for nomads are not one card but a system: a primary rewards card, a daily spend/FX card, and a separate backup. Pick cards by role, then filter by your region eligibility and acceptance realities. Use a risk-first check for declines, ATM/FX costs, and billing-cycle timing so your setup protects cashflow, not just points.

Stop guessing: build a 3-card nomad money stack that protects cashflow (not just points)#

Build a three-part card setup (primary, spend, backup) so one failure is less likely to derail your trip or your work. Forget the myth of "one perfect card." You want a system that still works when a terminal declines your card, a transaction gets flagged, or a merchant won't take your usual option.

The mindset shift is simple: you are not picking "the best" cards in a popularity contest. You are designing reliability under stress. Points matter, but continuity matters more.

A lot of freelancer pain comes from timing and friction: late client payments, a surprise hold, or a charge that fails at the exact moment you need it to go through.

The 3 roles in your stack (and why each exists)#

Use roles, not vibes. Here are the three roles that help you stay operational.

| Stack role | Job to be done | Common failure it covers | What "good" looks like |

|---|---|---|---|

| Primary credit (rewards) | Put predictable, high-value spend on a rewards rail | You over-optimize categories and the card stops fitting real spend | Simple earn structure that matches your actual expenses and workflow |

| Spend card (day-to-day + cash access) | Handle everyday purchases and local-currency needs | You hit avoidable conversion friction or you need cash fast | Low-friction spending abroad (where supported), clear controls, and easy replenishment |

| Backup credit (ideally independent if possible) | Save the day when the primary fails | Lock, refusal, damaged card | Lives in a different bag, stays funded, and you test it periodically |

You can build this with mainstream options people already consider. Treat every perk and fee as "unverified" until you read the current benefit guide and pricing for your country and eligibility.

A risk-first selector you can run fast (no spreadsheets required)#

Run these checks before you chase travel rewards or credit card points. You're trying to reduce declines, not win a points debate.

| Check | What to verify | Grounded note |

|---|---|---|

| Region reality check | What you can actually qualify for | Rules, pricing, and eligibility vary by issuer and jurisdiction, and they change. |

| Acceptance plan | Keep a fallback that does not share the same single point of failure | Do not rely on a single way to pay. |

| Cashflow timing check | Map your invoicing cadence to your billing cycle | If payments land late, you need headroom and a plan that does not force panic spending. |

| Failure drill | Decide what you do if the primary declines at checkout | Store the backup separately and keep issuer contact info accessible. |

Because this happens in real life: you arrive, try to pay, and the terminal declines your primary card. If your backup sits in the same wallet, you may still be stuck. If your backup lives elsewhere and you've already tested it, you're more likely to keep moving.

If you also run business spend, pair this with a dedicated business setup: The Best Business Credit Cards for Freelancers.

Who this list is for (and not for) + the selection criteria we actually use#

This list is for operators with variable income who want fewer declines and less FX fee leakage, not hobbyist points collecting.

If you're searching for travel cards as a nomad, first decide whether this category actually fits your situation and what should matter in the ranking.

This is for (and not for)#

This is for freelancers, creators, and small teams who run real monthly burn across SaaS, ads, lodging, and flights. You want to keep that spend on a predictable rewards rail (think a mainstream travel card). You also want a debit fallback for day-to-day operations.

It's not for two groups:

- Anyone carrying a revolving balance. Interest costs usually erase travel rewards and credit card points fast, and it turns your "stack" into debt management.

- Anyone optimizing one airline at all costs. If you only care about a specific airline network, you want a program-specific deep dive, not a generalist nomad stack (for example, a premium travel card plus a debit backup for acceptance gaps).

Hypothetical: you run client work from abroad, your ad platform bills overnight, and your lodging deposit hits the same week. You do not win by squeezing an extra category multiplier. You win by preventing a decline, avoiding unnecessary FX fees, and keeping your spend auditable.

Our weighted scoring rubric (repeatable, not vibes)#

We use a weighted rubric so you can sanity-check every recommendation and rerun the process when issuers change terms.

| Criterion (weight) | What we check in practice | Safe baseline comparator |

|---|---|---|

| FX friction and fee leakage (30%) | Foreign transaction fees, conversion behavior, ATM behavior. We treat "mid-market" as the benchmark for fairness in conversion. | Wise: "We only use the mid-market rate, the one you can check on Google." |

| Acceptance and continuity (25%) | Network coverage realities, terminal quirks, and your backup plan (separate card and a debit rail). | Wise card or a local debit (availability varies). |

| Rewards fit (20%) | Does the earn match your actual spend (flights vs coworking vs software) without constant category admin. | A simple, flat-rate travel card (as a reference point). |

| Travel protections (15%) | Trip interruption concepts, rental coverage concepts, purchase protections. You confirm in the current benefit guide. | Premium cards often compete here, but terms vary by issuer and region. |

| Eligibility and operational admin (10%) | Region reality, onboarding friction, and long-term "no spreadsheet pain" maintainability. | The simplest stack you can keep for years. |

Here's one concrete anchor for "leakage": Wise Canada lists 2 free ATM withdrawals each month as long as you do not withdraw over 350 CAD, then it charges 1.75% on any amount over that threshold, plus 1.5 CAD per withdrawal after the free withdrawals. That kind of clarity becomes our yardstick when we evaluate anything that touches FX and cash.

Related: A Guide to Notion for Freelance Business Management.

What's the best travel credit card for a digital nomad in 2026? Use this 10-minute selector (not opinions)#

The best travel credit card for a digital nomad is the one that fits a single "primary" job in your 3-card stack, clears your region and acceptance constraints, and survives a simple risk check for declines, cash, and timing.

Use the rubric above (FX leakage, acceptance, rewards fit, protections, admin) and stop debating vibes. This is how you pick from the universe of travel cards without buying into rewards you cannot reliably use.

Step 1 (3 minutes): Choose your stack role (pick one primary)#

Pick the job first, then shortlist cards that typically play that job well in your market.

| Your primary job-to-be-done | Start your shortlist at | Key differentiator to verify in the current guide |

|---|---|---|

| Premium travel perks and protections | Premium travel credit cards you can actually apply for in your country | Protections and eligibility change. Confirm what triggers coverage and where you can use the card. |

| Simple, consistent travel rewards | A low-admin travel rewards card from a major issuer in your market | Low-admin earning matters more than theoretical optimization when you run a business-of-one. |

| Everyday spend abroad with lower FX friction | A "no/low FX" everyday card that fits your residency and banking setup | Decide your "daily driver" once, then reduce switching costs with a stable habit. |

Pick the job first, then keep it simple. Decision rule: if you cannot describe the card's primary job in one sentence, it will become shelfware.

Step 2 (3 minutes): Apply two hard constraints (before you read a single points blog)#

Region constraint: build your list from cards you can actually apply for based on where you live and bank. Big brands can run different products in different countries, so confirm the exact product and terms from issuer docs.

Acceptance constraint: assume nothing. If your itinerary includes smaller merchants or infrastructure friction, bias your stack toward whatever payment networks are most reliably accepted where you are going, and treat any "maybe accepted" option as conditional, not the foundation.

Step 3 (4 minutes): Run the "Nomad Risk Check" so travel rewards do not break your ops#

- Decline plan: carry a second credit card and keep it physically separate. Add a debit option (for example, a multi-currency account with a debit card) so you can still pay when an issuer freezes spend.

- Cash plan: validate the ATM rules on your debit rail. Example: Wise's Canada pricing shows 2 or less withdrawals as free up to 350 CAD per month per account, then it lists 1.75% plus 1.50 CAD per withdrawal beyond that. Wise also positions conversion around the "mid-market rate": "We only use the mid-market rate, the one you can check on Google."

- Timing plan: map invoice timing to your billing cycle and choose limits you can repay in full. You want flexibility, not a new dependency.

Hypothetical: your lodging deposit fails on your primary at check-in. You pull out your backup credit card, then use your debit option for local spending until the issuer clears the lock. No scrambling, no reputation damage.

If you want a parallel framework for business spend, pair this selector with The Best Business Credit Cards for Freelancers.

Should you use credit cards, debit cards, or both? The safe-default stack (with failure modes)#

Use both: a credit card for credit-based spending and a debit/spend card for controlled day-to-day spending (especially across currencies).

The goal is not to win on paper. The goal is to keep your money ops simple and predictable.

The 2-rail stack I want you to operate (not debate)#

-

Credit card (your primary "statement-based" spend rail): Use a credit card for consolidated spend where you want one monthly statement and clean merchant reporting. Keep it boring: fewer accounts to reconcile, fewer moving parts.

-

Debit/spend card (your FX-control and multi-currency rail): Use a card like the Wise card for controlled spending in multiple currencies. On Wise's Canada pricing pages, Wise says you can "Spend at home or abroad in 40+ currencies" and that there are "No charges just for using your card abroad, with low conversion fees." For conversion expectations, Wise anchors to the benchmark: "We only use the mid-market rate, the one you can check on Google."

If you use Wise, the Canada card-fees page also lists ATM-related details: 2 free withdrawals each month "as long as you don't withdraw over 350 CAD," then fees apply (including 1.75% of any amount over 350 CAD, and 1.5 CAD per withdrawal after the 2 free withdrawals).

Quick operator notes (Wise Canada pricing)#

| Topic | What Wise's Canada pricing pages say |

|---|---|

| Exchange rate | Wise says it uses the mid-market rate (no markups or margins). |

| Card use abroad | Wise says no charges just for using your card abroad, with low conversion fees. |

| Currencies | Wise says you can spend in 40+ currencies. |

| ATM withdrawals | 2 free withdrawals/month if you don't withdraw over 350 CAD; after that, fees apply (including 1.75% over 350 CAD and 1.5 CAD per withdrawal after the 2 free withdrawals). |

| Account pricing model | Wise says you only pay for what you use, with no subscriptions or plans (and account registration is listed as Free on the Canada pricing page). |

If you add redundancy beyond this, keep it simple: avoid putting all your access (cards + app logins) in one place.

The best travel credit cards for digital nomads (by job-to-be-done) + a fast comparison table#

The right travel card setup depends on the job in your stack (primary, daily spend, fallback), not hype.

That is how you get through declines, FX friction, and admin fatigue. Below is a job-to-be-done shortlist you can plug into the 3-rail stack, with specifics only where terms are published.

Quick comparison table (scan first, then choose)#

| Card | Best role in stack | Biggest win | Biggest watch-out | Best for |

|---|---|---|---|---|

| Chase Sapphire Reserve | Primary | Pick one "primary" and run it consistently | Terms, eligibility, and ongoing cost structure vary by product and country | Insurance-and-simplicity operators |

| Chase Sapphire (family) | Primary | Simple "one card" workflow if it fits your spend | Benefits differ by product, check your exact version | Generalist earners |

| American Express Platinum Card | Primary | Makes the most sense if your life actually runs through airports | Keep a backup on a different payment network | Airport-heavy weeks |

| American Express Gold Card | Primary | Can work if your spend clusters in a few categories | Category fit adds admin | Food-heavy spend patterns |

| Capital One Venture X | Primary | A set-and-forget setup if you like fewer knobs | Portal and benefit terms require reading | Low-admin optimizers |

| Capital One Venture Rewards Credit Card | Backup or starter primary | A straightforward backup rail for continuity | Lighter premium benefit set | Backup-first pragmatists |

| Halifax Clarity | Daily spend | Can be a steady daily rail if it fits your profile | Not a perks-first setup | Fee-minimizers |

| Barclaycard Rewards | Daily spend | Another daily-driver option if it matches your needs | Not a premium protection play | Simplicity seekers |

| British Airways American Express credit card | Secondary | Add it only if you will redeem intentionally | Do not make one network your only rail | Points-focused flyers |

| Wise card | Daily spend + ATM | 40+ currencies spending with Wise's mid-market rate | Not a credit line, and pricing varies by country | FX control across currencies |

| Starling | ATM + local spend | Extra redundancy if you want another spending rail | Rewards not the point | Cash access operators |

| Chase UK | Backup | Extra continuity layer | Not a travel rewards credit card | Redundancy-first setups |

Picks by job-to-be-done (use-cases + where each fits)#

Primary credit card (any issuer): Make one your default, keep a backup on a different payment network, and do not "rotate" constantly unless you actually enjoy admin.

Wise card (Daily spend + ATM): Wise says you "only pay for what you use" (no subscriptions or plans), uses the "mid-market rate," and lets you "spend at home or abroad in 40+ currencies" with "no charges just for using your card abroad" (conversion fees may still apply). On Wise's Canada pricing, you get 2 free ATM withdrawals each month as long as total withdrawals don't go over 350 CAD. After that, Wise charges 1.5 CAD per withdrawal, and you'll be charged 1.75% of any amount over 350 CAD. On the same Canada page, optional express delivery starts from 15.41 CAD (listed as 1-2 days), and replacing your card costs 5 CAD.

Hypothetical: you land in Singapore, your primary credit card works for the hotel, but a smaller vendor needs a debit payment. You run Wise card for the purchase, then keep your backup credit card untouched unless something breaks.

If you want a parallel "work spend" setup, pair this with The Best Business Credit Cards for Freelancers.

Which cards work best if you're UK-based vs US-based? Use these two decision paths#

In practice, US-based nomads often build around a primary rewards credit card, while UK-based nomads often prioritize FX, acceptance, and admin simplicity, with a debit rail for redundancy.

| Decision area | US-based | UK-based |

|---|---|---|

| Primary rail | A premium travel rewards credit card; choose an insurance-first option or a simpler earn option. | An FX-friendly credit card you can use consistently. |

| Add-on / backup | A second rewards credit card stored separately so a lost wallet does not wipe your credit rail. | An optional rewards card that matches how you'll actually redeem; keep a second non-identical card in the stack. |

| Debit redundancy | Wise card for currency control and spending guardrails; Wise says you can spend at home or abroad in 40+ currencies. | Two debit options: one for local payments + ATM continuity and one as pure backup. |

Use your home base to pick one primary credit rail, one daily-spend FX rail, and one backup. Approvals, benefits, and day-to-day usability can diverge between the US and the United Kingdom, so you want a clean path you can implement without second-guessing.

Path A (US-based): optimize travel rewards + protections, then add redundancy#

Treat this as your 3-rail stack for travel rewards and credit card points, with a failure plan you can actually run on a bad day.

- Primary (pick one): a premium travel rewards credit card

Choose an insurance-first option when you want stronger travel protections and you prefer to run one card for most travel purchases. Choose a simpler earn option when you want fewer moving parts to reconcile each month.

- Secondary/back-up: a second rewards credit card

Give it one job: "works when the primary fails." Store it separately so a lost wallet does not wipe your credit rail.

- Daily spend/FX: Wise card

Use it for currency control and spending guardrails. Wise says you "only pay for what you use" with "no subscriptions or plans." Wise also uses the "mid-market rate" (the one you can check on Google). Wise says you can "spend at home or abroad in 40+ currencies."

Path B (UK-based): optimize FX + acceptance + admin simplicity#

Run this path when you care more about predictable day-to-day spending abroad than squeezing every last point.

- Daily driver (pick one): an FX-friendly credit card you can use consistently

Choose one and stop rotating. Consistency makes declines, reconciliations, and merchant testing easier to manage.

- Rewards add-on (optional): a rewards card that matches how you'll actually redeem

Add it only if you actually plan to redeem the rewards. Keep a second non-identical card in the stack so you do not depend on a single rail.

- Debit redundancy: two debit options

Use one as your "local payments + ATM continuity" rail, and keep the other as pure backup.

| Decision you're making | Safer default | Why it stays operational |

|---|---|---|

| "Which primary card do I run?" | US: one primary travel rewards credit card. UK: one consistent day-to-day credit card | One primary reduces admin and makes spend patterns predictable. |

| "What if a merchant declines my usual rail?" | Carry a second card on a different rail (when possible) | Single-rail stacks fail at the worst times. |

| "What if I need FX control fast?" | Wise card | Wise advertises transparent pricing, mid-market rate, and 40+ currencies support. |

Operational admin tip: Put photos of the front/back of each card plus issuer contact numbers inside an encrypted vault. When an issuer flags travel activity or you need an urgent replacement, you move faster with one place to look instead of improvising mid-trip.

Are premium annual fees actually worth it for nomads? A break-even model you can run in 5 minutes#

Premium annual fees are worth it only when you can regularly use two concrete value drivers that beat your simplest low-fee stack.

Otherwise, "premium" becomes extra cost plus extra admin. Use this section to decide whether premium belongs in your system.

Step 1: Start with what you can guarantee you'll use (not aspirational perks)#

Run this like an operator. If you can't confidently use a perk most months, value it at zero.

- Lounge access reality check: If your itinerary rarely includes long airport sits, the American Express Platinum Card value collapses fast. You pay for "airport lifestyle" whether you use it or not, and American Express acceptance gaps can force you onto a backup anyway.

- Protection-first logic: If you currently buy separate travel insurance because missed connections, delays, or cancellations would hurt, then a protections-heavy card like Chase Sapphire Reserve can justify its fee even before you think about credit card points. Do not guess. Read the benefit guide for trigger rules and exclusions.

Step 2: Fill a one-page break-even worksheet (use conservative inputs)#

Use a low estimate for points. Treat credits as "realized" only after you actually redeem them.

| Line item (annual) | Your estimate | How to keep it honest |

|---|---|---|

| Annual fee (premium card) | Use the posted fee, not a promo. | |

| Credits you'll truly use | If you would not pay cash for it, count it as 0. | |

| Points earned on real spend | Apply a conservative value per point, not best-case redemptions. | |

| FX leakage avoided | Compare against your baseline behavior, often easiest vs Wise card pricing. | |

| "Protection value" | Count it only for purchases you actually put on the card (flights, rentals, hotels). |

For an FX baseline, anchor to something tangible. Wise says "We only use the mid-market rate (the one you can check on Google)" and "You only pay for what you use, no subscriptions or plans."

On Wise's Canada pricing page, sending money fees vary by currency "from 0.48%," and Wise also says there are "no charges just for using your card abroad, with low conversion fees."

Hypothetical reality check: If you mainly book cheap regional flights last-minute and pay month-to-month lodging, protections may not trigger often. If you prepay big trips and one disruption would force multiple nights of extra lodging, protections can dominate the points math even when your travel rewards look average.

Decision rule: If you cannot articulate your top 2 value drivers for a premium card in one sentence, default to Capital One Venture Rewards Credit Card (simple travel rewards) plus Wise card (FX control). Then revisit premium after one quarter of real spend data. For business-focused alternatives, see The Best Business Credit Cards for Freelancers.

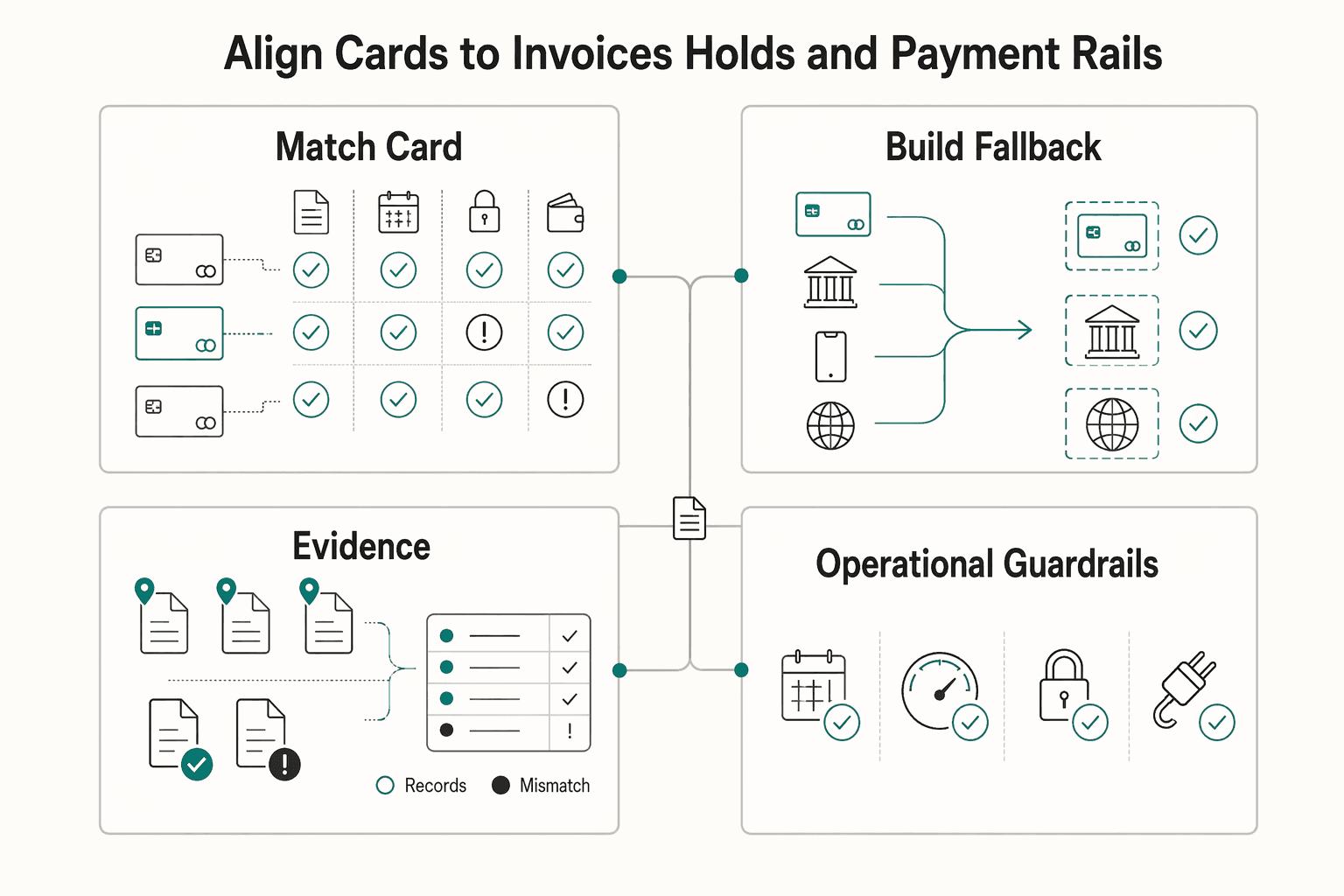

The freelancer cashflow layer competitors ignore: align cards to invoices, holds, and payment rails#

Treat your card stack as a cashflow system first, then layer travel rewards on top.

| Layer | What the article recommends | Concrete anchor |

|---|---|---|

| Match card choice to your billing cycle | Keep your baseline stack boring and survivable; add high-fee cards only when you already use the benefits monthly. | Wise says sending fees vary by currency, from 0.48%. |

| Build a fallback path for getting paid | Have a ready inbound option and a predictable outbound workflow; do not improvise with last-minute cash advances. | Wise says you get a discount when you send over 35,000 CAD (or equivalent), and the discount resets on the first of the month. |

| Reduce payment risk exposure with separation and documentation | Split spend by job-to-be-done and keep receipts and booking confirmations in one place. | Wise describes the card as usable in 40+ currencies, with low conversion fees and the mid-market rate. |

| Operational guardrails that prevent ugly surprises | Use travel notices if your issuer supports them, carry a backup card in a different bag, and run a small test transaction before a large booking. | Wise lists ATM withdrawals as free up to 350 CAD per month per account with 2 or less withdrawals; over that, 1.75% plus 1.50 CAD per withdrawal. |

This is the part that keeps your setup from collapsing when a client pays late, a terminal fails, or you need a non-card rail fast.

-

Match card choice to your billing cycle (the "get paid system" angle) Run a simple rule: variable income hates fixed commitments. If your revenue arrives unevenly, keep your baseline stack boring and survivable (think: a simple primary like Capital One Venture X or Capital One Venture Rewards Credit Card, plus a controlled-spend layer). Add high-fee cards like the American Express Platinum Card only when you already use the benefits monthly. Concrete anchor: if you need a non-card way to move money, Wise says sending fees vary by currency, from 0.48%.

-

Build a fallback path for getting paid (so the card isn't your only lifeline) If a card payment link fails or a client can only pay by bank transfer, you want a ready inbound option (for example, Gruv Virtual Accounts, where enabled) and a predictable outbound workflow (for example, Gruv Payouts, where enabled). Do not improvise with last-minute cash advances. Concrete anchor: Wise says you get a discount when you send over 35,000 CAD (or equivalent), and the discount resets on the first of the month. That kind of rule makes bank-transfer rails easier to plan around when you move larger amounts.

-

Reduce payment risk exposure with separation and documentation Split spend by job-to-be-done so you can prove, reimburse, and unwind cleanly: Chase Sapphire for client-funded travel, Halifax Clarity or Barclaycard Rewards for UK daily living, and the Wise debit card for FX budgeting. Keep receipts and booking confirmations in one place, tied to the card you used, so disputes do not turn into archaeology. Concrete anchor: Wise describes the card as usable in 40+ currencies, with low conversion fees and the mid-market rate.

-

Operational guardrails that prevent ugly surprises Use travel notices if your issuer supports them. Carry a backup card stored in a different bag. When you land in places like Singapore or Brazil, run a small test transaction before you commit to a large booking. Concrete anchor: Wise lists ATM withdrawals as free up to 350 CAD per month per account with 2 or less withdrawals. Over that, Wise lists 1.75% plus 1.50 CAD per withdrawal. Put those thresholds into your cash plan so convenience does not silently tax you.

Hypothetical operator move: you book a client trip on Chase Sapphire, route meals and transit through the Wise debit card to stay on-budget, and keep a backup Capital One card sealed in your laptop sleeve for the one moment your primary gets declined.

The playbook: pick one primary card, one spend card, and one fallback - and make it auditably repeatable#

Use a 3-layer stack - primary credit, daily spend/FX, and a backup credit card - and write down your rules so you can run it anywhere.

The goal is not novelty or "the perfect card." It's a system that still works when you're tired, the Wi-Fi is bad, and a payment gets weird. Assign each card a job, decide where you will and won't use it, and keep the setup simple enough that you'll follow it.

Your 3-card stack (the only structure you need)#

-

Primary rewards card (your "big purchase" card) Description: Put high-stakes purchases here - things you'd rather not troubleshoot mid-trip, like flights, lodging, and work gear. Choose based on how much admin you're willing to do and what benefits you realistically use (for example, a Chase Sapphire option, Capital One Venture X, or Amex Platinum). Key differentiator: You're optimizing reliability and clear rules, not perfect points.

-

Daily spend and FX layer (debit rail) Description: Use a spend card for everyday taps, local currency spending, and controlled conversions. Wise card often fits this role. Wise says, "We only use the mid-market rate - the one you can check on Google." Wise also positions pricing as upfront: "You only pay for what you use: no subscriptions or plans." Key differentiator (with real numbers): On Wise's Canada pricing page, sending money fees vary by currency and start from 0.48%. ATM withdrawals show 350 CAD per month per account free (2 or less withdrawals), then + 1.50 CAD per withdrawal plus 1.75% over that threshold (jurisdiction terms vary). If you use a different spend card (like Starling), verify fees and limits directly with the provider.

-

Backup credit card (your continuity layer) Description: Store a second credit card separately and treat it as your "keep the trip alive" option. The point is not optimizing rewards - it's having a clean fallback when your primary won't go through. Key differentiator: You can keep moving if your primary card gets declined or flagged.

| Stack role | Example | What you optimize | Non-negotiable rule |

|---|---|---|---|

| Primary | Chase Sapphire (or Chase Sapphire Reserve) | Clear rules for big purchases | Put major, high-stakes purchases here |

| Spend/FX | Wise card (or Starling) | Day-to-day spending + FX control | Confirm the currency and total cost before you tap |

| Fallback | Capital One Venture Rewards Credit Card | Continuity | Store separately and keep it ready to use |

Make it repeatable: break-even + review cadence#

Run a basic break-even before you commit to any card with an annual fee (especially American Express Platinum Card and Chase Sapphire Reserve). Write down the 2 benefits you will actually use, subtract the annual fee, and compare it to a lower-overhead setup. Then set a simple switch/keep/cancel rule and revisit it every 6-12 months.

If you want tighter cashflow control beyond cards, consider consolidating inbound and outbound payment rails with Gruv Virtual Accounts and Payouts (where enabled) so card spend becomes one traceable layer in a broader workflow. For a deeper card strategy on the business side, use The Best Business Credit Cards for Freelancers.

Frequently Asked Questions

What’s the best credit card for a digital nomad?

No single card wins for everyone. Treat “best travel credit cards for nomads” as a system choice: pick a primary rewards card that matches your real spend and your tolerance for admin, then add redundancy so one decline does not end your day. Your “best” card is the one you can keep funded, keep compliant, and get accepted often enough to matter.

Should digital nomads use credit cards, debit cards, or both?

Use both, on purpose. Credit cards can help you earn travel rewards (points and miles) from everyday spending, while debit can help with day-to-day payments and cash access when credit isn’t an option. A safe default stack: one primary rewards credit card, one debit card for spending and cash, and one backup credit card stored separately.

Which travel cards are best for UK-based nomads vs US-based nomads?

Start with eligibility. Different countries issue different products and approvals vary, so build from what you can actually get approved for where you live. Treat any shortlist as starting points, then validate fees (including foreign transaction fees), acceptance, and benefit terms directly with the issuer.

How do I know if an annual fee is worth it for my travel schedule?

An annual fee is worth it when you can name the two benefits you will use reliably, not aspirationally. As Nomadic Matt puts it, “most of the best travel credit cards have annual fees (sometimes huge ones),” and those fees “are usually worth it for frequent travelers.” If you travel infrequently, start with no-annual-fee or lower-overhead cards and upgrade only after you prove usage for a full cycle.

What should freelancers prioritize: points, FX savings, or cashflow reliability?

Prioritize cashflow reliability first, then costs like foreign transaction fees, then points. Points and miles can turn everyday spending into travel rewards, but only if you pay on time and avoid interest drag. When your income arrives on invoices, avoiding payment outages beats theoretical rewards.

What are the biggest risks to avoid when choosing nomad cards (declines, ATM fees, FX conversion traps)?

Avoid single points of failure. Where In The World Is Nina calls out the real-world pain: “until you try to pay your bill and your credit card gets declined.” The practical fix is redundancy: more than one way to pay, and at least one true backup you can access quickly.

What’s a simple “backup plan” if my card gets frozen abroad?

Carry two credit cards plus one debit option, stored in different places. Keep issuer contact details accessible (and your account logins working), and run a small test purchase after each border hop so you catch freezes early. If one card gets flagged, switch to your backup and use debit for day-to-day spend until the issuer clears the lock.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Business Credit Cards for Freelancers

Pick for reliability first. For a freelancer, the right business card is usually the one that keeps recurring bills moving, keeps records clean, and avoids extra costs when income swings from month to month. Rewards still matter, but they sit on top of those basics. They do not replace them.

The Best Digital Nomad Cities for LGBTQ+ Travelers

Pick a city only if the country behind it fits your stay, your work, and your risk tolerance. If you are comparing the **best lgbtq nomad cities**, treat each option as one commitment decision: city plus country, not city alone.

A Guide to Notion for Freelance Business Management

If your workspace feels busy but fragile, you do not need more pages. You need one connected system. Treat your freelance business like a business-of-one and use Notion as the control layer that connects client decisions, delivery, and billing in one place.