Quick Answer

Prioritize risk controls first when choosing the best business credit cards for airline miles: confirm approval fit, personal guarantee exposure, and live issuer terms before you value rewards. Then map real spend to earning categories and verify eligibility limits, including rules tied to the last 24 months. For redemptions, lock the route and backup dates before any transfer. Finally, connect the card to bookkeeping early so category drift and missing evidence do not erase the card’s practical value.

If you run a solo business across borders, a business credit card is not just another piece of plastic. It shapes your costs, support, protections, rewards, and how much admin you create for yourself. Most advice still misses that. It assumes a domestic business with predictable categories like office supplies and shipping. It is not built for a Business-of-One paying SaaS vendors in euros, taking clients to dinner in Singapore, and booking multi-leg trips across regions.

This guide starts from that operating reality. It shows you how to choose and use a business credit card as a practical tool that reduces risk, fits your real spending pattern, and cuts back-office drag. We will move through four stages, from defense to offense:

- The Foundation: Mitigate risk before you think about rewards.

- The Earning Engine: Match your card to how you actually spend.

- The Redemption Playbook: Turn points into travel without wasting flexibility.

- The Automation Stack: Connect the card to your books so it saves time, not just earns miles.

That sequence matters. Most comparisons start at the wrong end. This one keeps you from optimizing rewards on a weak setup and helps you turn the card into part of how you run the business.

Step 1: The Foundation - Mitigating Risk Before Maximizing Rewards#

Start by screening out cards that create approval risk, personal-liability risk, or stale-value risk. For most solo operators, that matters more than a headline bonus.

For a solo operator or very small team, the first real decision is not points. It is underwriting fit. Before business credit is established, most applicants are choosing among three paths: a traditional business card, a corporate card that may look more at revenue or cash balances, or a secured business card that usually requires a refundable deposit that sets the credit limit. If you have not sorted that baseline yet, start with The Best Business Credit Cards for Freelancers before you optimize for miles.

Use the four-check shortlist#

Use this shortlist to eliminate weak options early, before you spend time comparing transfer partners or lounge perks.

| Check | Keep if | Verify | Reject when |

|---|---|---|---|

| Underwriting fit | The card clearly fits your stage | Whether the issuer is evaluating credit history versus revenue or cash balances | You are only pursuing it because you assumed "no credit" meant no personal credit history |

| Personal guarantee exposure | You are comfortable backing the account personally | The guarantee language before applying | Your whole thesis depends on finding a no-PG, no-credit-check option for a brand-new business |

| Terms freshness | It still matches the issuer page on application day | Any review article against the live offer and current terms | The value case depends on an old fee, bonus, or spend threshold |

| Usable value | The benefits match how you spend and travel | The current benefit guide and terms | The value lives mostly in perks you will admire but rarely use |

- Underwriting fit

Traditional business cards often require a personal guarantee and personal credit check. Keep cards that clearly fit your stage. Verify whether the issuer is evaluating credit history versus revenue or cash balances. Reject any option you are only pursuing because you assumed "no credit" meant no personal credit history. In a startup context, it usually means no business credit history.

- Personal guarantee exposure

If a card needs your personal guarantee, treat that as a real risk decision, not boilerplate. Keep it if you are comfortable backing the account personally. Verify the guarantee language before you apply. Reject the card if your whole thesis depends on finding a no-PG, no-credit-check option for a brand-new business. Those are less common, especially for brand-new businesses.

- Terms freshness

Rewards rates, fees, and offer terms change. Keep only what still matches the issuer page on application day. Verify any review article against the live offer and current terms. Reject any card where the value case depends on an old fee, bonus, or spend threshold. A guide published on October 8, 2025 or even April 2, 2026 is only a checkpoint, not the final source.

- Usable value

Premium travel cards can be worth it, but only if your business will actually use the protections, credits, lounge access, or reporting controls. Keep the card if the benefits match how you spend and travel. Verify the current benefit guide and terms. Reject cards whose value lives mostly in perks you will admire but rarely use.

Enter the application like an audit trail matters#

Treat the application as if you may need to review it later. That mindset helps you avoid common approval mistakes and makes follow-up easier to handle.

| Application point | What to do | Why it matters |

|---|---|---|

| Qualification path | Decide whether you fit a traditional, corporate, or secured route before you apply | Approval odds depend heavily on the issuer's underwriting model |

| Personal guarantee | Confirm whether you are personally backing the account | This is a real liability decision, not a small checkbox |

| Terms and offer | Match the live issuer page to the offer you intend to apply under | Terms and conditions apply, and published comparisons age quickly |

| Support files | Keep records for the figures and business details you enter | Helps you keep your application details consistent |

The usual application errors are not complicated. People treat no business credit history as the same thing as no personal credit history. Or they apply from a review page without checking the live issuer terms first.

For your own audit trail, save:

- the exact offer page you applied under

- the current benefit guide you relied on

- the terms or pricing page visible on application day

If you are down to a few well-known travel options, verify them at this level before you go further:

| Card | What to verify first | Annual fee posture | Best fit by spend pattern |

|---|---|---|---|

| Chase Ink Business Preferred | Current terms, benefit guide, and eligibility language | Verify current annual fee | You want business travel value with a lower-fee posture |

| The American Express Business Platinum Card | Current terms and which premium benefits your business will actually use | Verify current annual fee | You travel often enough that premium protections and credits may offset the cost |

| Capital One Venture X Business | Current terms, protections, and whether the card's controls match your operation | Verify current annual fee | You want a premium-leaning travel setup and will use the benefits repeatedly |

The failure mode here is simple. You chase a travel card that looks strong in a comparison. Then you discover the approval path was wrong, the personal guarantee was a bigger commitment than expected, or the fee only works if you maximize benefits you will barely use. Get this filter right first, and the earning decision in the next step gets much easier.

If you want a deeper dive, read The Best Business Credit Cards for Hotel Points. If you want a quick operational next step, try the free invoice generator.

Step 2: The Earning Engine - Aligning Rewards with Your Global Reality#

Map spend first, check eligibility second, then choose card type. That sequence helps you avoid earning into a program that does not match how you actually travel.

Start from your real business transactions and group spend into practical buckets. If your baseline fit is still unclear, validate that first in The Best Business Credit Cards for Freelancers before optimizing for miles.

Build the spend map#

Use your posted transactions as the source of truth, then verify how each issuer treats those charges.

| Bucket | What belongs here | What to verify before you count on rewards |

|---|---|---|

| Recurring software | SaaS, cloud tools, design apps, phone, internet | Whether merchants post consistently under the same category over time |

| Travel | Flights, hotels, rail, rides, coworking, work meals | Whether value depends on booking through an issuer portal rather than booking direct |

| Ads | Search, social, marketplace ads | Category posting reliability, especially when spend routes through agencies or billing platforms |

| Contractor and vendor payments | Freelancers, agencies, production partners, outsourced ops | Whether large payments are excluded or only earn at base rates |

For edge cases, classify by how the charge is processed, not how it looks at a glance. If spend runs through an intermediary, confirm how a real posted transaction codes before you assume category earnings.

Run the eligibility and cash-flow check#

Before you value a welcome bonus, confirm the restrictions that can block eligibility. A common rule is a same-product bonus restriction if you received that bonus in the last 24 months, and some issuers also apply language tied to opening five or more personal cards in the last 24 months.

Also check time-limited value. If perks were scheduled to end on December 31, 2025, do not treat them as durable value for a 2026 decision; the same applies to benefit language tied to specific flight periods, such as priority boarding for 2026 and beyond.

Cash flow still outranks rewards. If you may carry balances, miles can lose value quickly, and if you use a charge-card structure, you need reliable full statement payoff capacity. Run your own sample math with current terms before you count a bonus as meaningful.

Choose flexibility or loyalty#

After spend fit and eligibility are clear, decide based on route stability and operational reliability, not headline perks.

| Option | Best when | Avoid when | What to verify first |

|---|---|---|---|

| Flexible-points business card | Routes change, you book across multiple carriers, or you want a fallback when availability shifts | You consistently fly one airline and mainly want that airline's specific perks | Transfer options, portal dependence, and category-posting reliability |

| Premium flexible-points card | You will repeatedly use premium travel benefits and finance controls | The fee only works if rarely used perks are fully maximized | Current benefit terms, usable credits, and whether booking path changes value |

| Co-branded airline business card | Most paid travel is concentrated in one airline program and you will use its recurring perks | Route volatility is high or client destinations shift frequently | Bonus restrictions, temporary benefits, and whether the airline fits your repeat routes |

If your routes move often, flexibility is usually safer than lock-in; that same tradeoff shows up in The Best Travel Credit Cards for Digital Nomads. If your routes stay concentrated, a co-branded setup can work well, but confirm the program still matches how your business actually travels.

Step 3: The Redemption Playbook - Turning Points into High-Value Travel#

Redemption works best when you run it as a route-first checklist, not a points-first guess. If you cannot name the exact route, backup dates, and transfer path before you move points, wait.

- Define the route first

Start with the trip you need: segments, date window, cabin, and flexibility requirements. Then identify which airline program, partner program, or alliance family can ticket it based on current program details. If your client travel shifts across regions, document a backup city pair or carrier in advance, as covered in The Best Travel Credit Cards for Digital Nomads.

- Compare real trip cost, not headline points

Check the cash fare for the identical seat on the same dates in incognito mode, then compare it to the points option. Subtract taxes and fees from the cash equivalent before calculating value. With dynamic pricing and shifting award charts, rough estimates can lead to weak redemptions.

- Validate transfer risk before moving points

Confirm live award space first, then verify transfer ratio, timing, and finality on the issuer and partner pages. Transfer bonuses can appear monthly, and valuation benchmarks are refreshed quarterly, but neither helps if the seat disappears or the total trip cost stops making sense.

- Set a fallback before transfer

Save one primary itinerary, one backup route or date, and one cash alternative. Keep screenshots of points pricing, cash pricing, and cancellation or redeposit terms shown at checkout in case availability reprices. If your decision depends on issuer rebate timing, treat it as a cash-flow checkpoint. Verify the current rebate rate, cap, and posting window, then confirm you can carry the gap until posting.

A strong redemption process preserves flexibility. A rushed transfer removes it.

| Redemption path | Use when | Check first | Main friction |

|---|---|---|---|

| Issuer portal | Use portal when you need cash-like inventory and want to avoid transfer wait | Paid-ticket rules, total points cost, and any issuer rebate terms | Booking is simpler, but value may trail strong partner options |

| Direct airline program | Use direct program when it prices your exact route cleanly | Total taxes and fees, cancellation flexibility, and live pricing on your dates | Dynamic pricing and surcharges can erase expected value |

| Partner program | Use partner when alliance inventory beats direct-program pricing | Live award space, transfer finality, and total trip cost after fees | Highest friction: timing, availability, and reversibility risk |

For a step-by-step walkthrough, see The Best Business Bank Accounts for Freelancers.

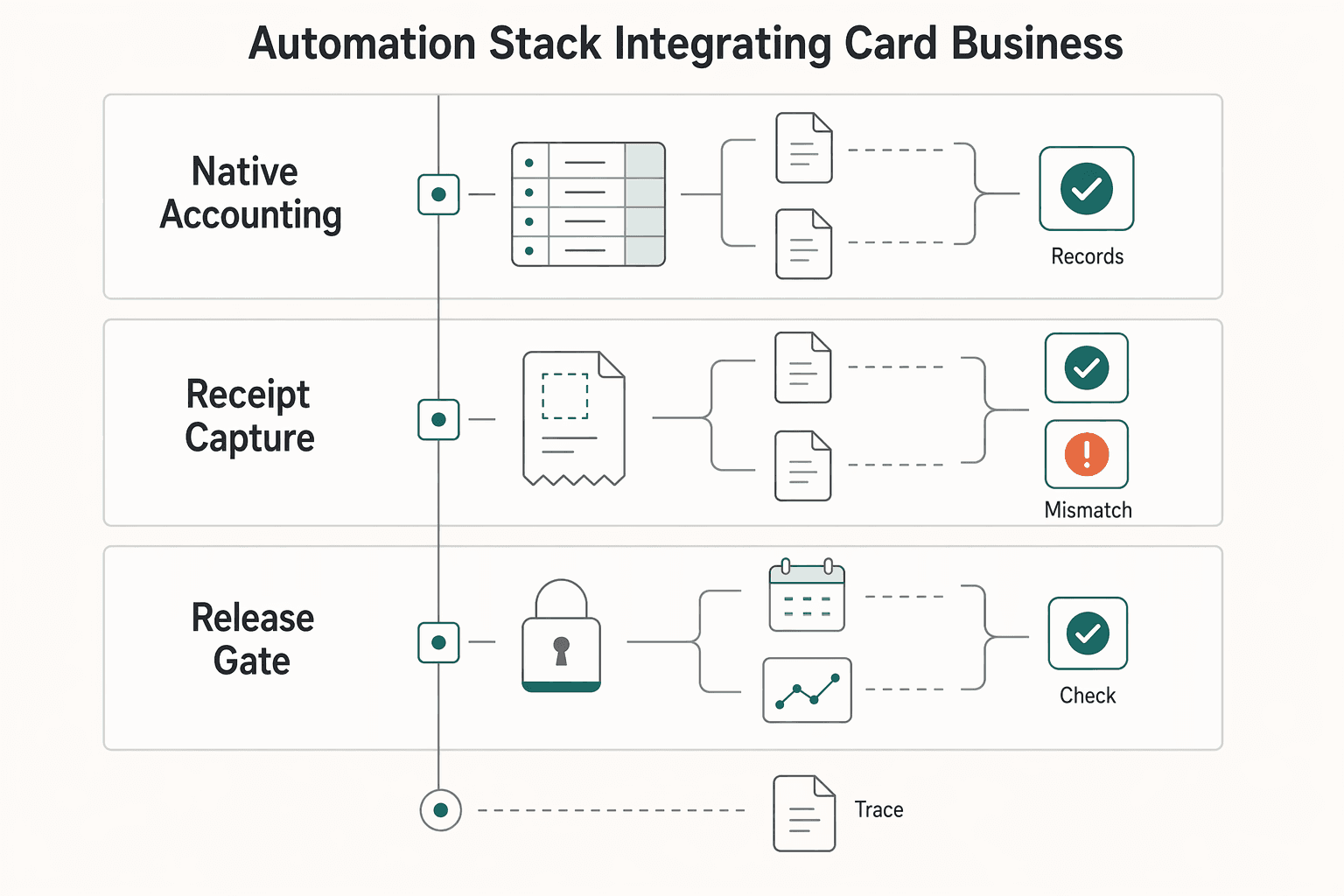

Step 4: The Automation Stack - Integrating Your Card into Your Business OS#

Control comes before convenience in this step. If a card earns well but creates messy records, missing receipts, or month-end confusion, it is weakening your system. If you are still choosing a card, frame that choice inside your full finance workflow, not just miles strategy, as outlined in The Best Business Credit Cards for Freelancers.

1. Connect the feed with one owner. Owner: you or your bookkeeper. Trigger: new card approval, replacement card, or accounting migration. Output: one clean transaction source with a confirmed opening date. Connect this first, then layer on receipts or reimbursements. Verify imported dates and amounts against the latest statement, and watch for duplicate imports after reconnects or replacement cards. For any card or spend tool login, verify you are on the correct provider domain and treat OTP-sharing requests as suspicious.

2. Standardize categories and merchant names. Owner: whoever closes the books. Trigger: first 2 to 4 weeks of live transactions. Output: stable category rules you can trust. Tie rules to your chart of accounts, not merchant marketing labels. Category drift is the main risk, especially when descriptors change and the same vendor lands in different categories. If a rule starts failing, pause it and fix the mapping before more transactions stack up.

3. Isolate risky spend with dedicated cards or tags. Owner: spender plus reviewer. Trigger: recurring vendors, ad platforms, and reimbursable client costs. Output: cleaner reporting and smaller blast radius when something breaks. Use dedicated virtual cards or clear tags where possible for supplier and ad-platform spend. This improves visibility, supports policy enforcement, and makes billing issues easier to trace. Monitor limit exhaustion on cards tied to ads or critical vendors, because failed charges can interrupt operations, not just bookkeeping.

By this point, your card setup should be producing fewer surprises and cleaner records, not just points.

| Automation path | Best use | Verify before rollout | Failure mode to monitor | Main tradeoff |

|---|---|---|---|---|

| Native accounting feed | Fast import into the ledger | Current integration status and opening import date | Feed disconnects or duplicate imports | Fewer moving parts, less receipt context |

| Receipt capture tool | Attach proof to each charge | Current connection status and file-link behavior | Missing receipt links after sync issues | Better evidence, more admin overhead |

| Rebilling or approval layer | Client-tagged or team-approved spend | Current tagging and approval setup | Category drift or untagged billable charges | Cleaner client invoicing, stricter process discipline |

4. Close monthly with an evidence pack. Owner: finance reviewer. Trigger: statement close. Output: reconciled ledger plus support for disputes, writeoffs, and client rebills. For multi-currency exceptions, document four fields each time: source amount, posted amount, variance note, and supporting file location. Keep original-currency detail from the receipt or invoice intact. For client rebilling, require a project or client tag and attach support at transaction level so your evidence pack is ready at invoice time; a simple tracker in your accounting stack or A Guide to Notion for Freelance Business Management is usually enough when reviewed monthly.

You might also find this useful: The Best Tools for Tracking Your Credit Card Points and Miles.

Conclusion: Your Card Is a Strategic Asset, Not Just Plastic#

Once your rules and receipt trail are working, the card stops being a rewards toy and starts acting like an operating tool. That is the standard to keep when you compare cards for airline miles.

- Risk control

Start by verifying the hard terms that can damage cash flow if you ignore them: annual fee, purchase APR, cash-advance APR, foreign transaction fees, eligibility, and offer conditions. One concrete example from an issuer page: the TD Aeroplan Visa Business Card lists a $149 annual fee, 14.99% on purchases, 22.99% on cash advances, and Canadian residency plus age of majority as eligibility gates. The same page also shows the offer as effective March 2, 2026. You are screening for avoidable cost and approval friction before you think about miles.

- Earning fit

Pick a card whose bonus checkpoints match spend you can reach without forcing bad purchases. If an offer says "Conditions Apply," requires the account to remain approved, open, and in Good Standing, and uses milestones like $15,000 within 180 days, treat those as operating requirements, not marketing footnotes. Your earning plan should fit your real billing cycle.

- Redemption discipline

You need simple rules for when to use points and when to preserve cash. That keeps rewards from pushing you into poor booking choices or surprise out-of-pocket costs. A good card should help you travel on purpose, not just accumulate balances.

- Admin discipline

Keep statements, receipts, and approvals in one evidence pack, and run recurring checks for uncategorized or unexpected charges. This keeps exception handling and reviews easier to manage. In practice, rewards matter less than whether the card improves day-to-day operational clarity.

Use this checklist for next steps:

- Choose your primary card profile only after you verify current issuer terms and date stamps.

- Define your earning and redemption rules: bonus checkpoints, spend cap, and when to redeem versus pay cash.

- Set a recurring review cadence, weekly or monthly, to confirm fees, Good Standing, uncategorized charges, and bonus progress.

- Avoid relying on archival pages that may not reflect current policies.

Keep one final filter in place. If a card does not improve control, clarity, and consistency in your business operations, it is a poor fit no matter how strong the rewards marketing looks.

We covered this in detail in Best Corporate Debit Cards for Global Spending in Small Teams.

Frequently Asked Questions

How should you narrow your shortlist first?

Start with the issuer’s current official terms and benefit details. If fees, eligibility wording, or redemption conditions are unclear or outdated, do not shortlist the card yet. | Filter | What to confirm | Drop it if | | --- | --- | --- | | Shortlist filter | Current issuer terms, fees, offer conditions, eligibility wording | Key terms are missing, vague, or only repeated from third-party roundups | | Flexibility check | Whether the rewards setup matches your usual routes and booking habits | The value appears to depend on narrow assumptions you cannot verify | | Workflow-fit check | How statements and records would fit your close process | It looks hard to document consistently |

What should you verify before you trust any roundup?

Use third-party rankings as starting points, not decision documents. Historical information can go stale, and old performance or old offers are not reliable guides to current terms. A practical checkpoint is to save the current issuer terms and benefit details when you apply. If you cannot confirm current official terms, pause and re-check before making a decision.

Should you choose an airline-specific card or a flexible travel card?

Choose based on current official terms and your own travel pattern. If your travel is concentrated, an airline-linked option may fit. If your routes or carriers change often, broader flexibility may reduce risk. If your business spend is still the bigger question, start with The Best Business Credit Cards for Freelancers.

Do rewards rates matter more than workflow fit?

Not always. A higher earn rate on paper may not be worth it if terms are harder to verify or records become harder to reconcile at close. If your travel pattern is the real constraint, compare this article with The Best Travel Credit Cards for Digital Nomads.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- admissions.yale.edu/podcast-transcriptstrusted

- cocoafl.gov/FAQ.aspxtrusted

- das.nebraska.gov/materiel/purchasing/6556/Pinnacle%20Bank.pdftrusted

- gao.gov/assets/gao-21-387.pdftrusted

- muw.edu/images/docs/office_finance_administration/it...trusted

- register.dls.virginia.gov/vol28/iss24/v28i24.pdftrusted

- sec.gov/Archives/edgar/containers/fix030/806636/0000...trusted

- southportland.gov/CivicAlerts.aspxtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Business Credit Cards for Freelancers

Pick for reliability first. For a freelancer, the right business card is usually the one that keeps recurring bills moving, keeps records clean, and avoids extra costs when income swings from month to month. Rewards still matter, but they sit on top of those basics. They do not replace them.

The Best Travel Credit Cards for Digital Nomads

Build a three-part card setup (primary, spend, backup) so one failure is less likely to derail your trip or your work. Forget the myth of "one perfect card." You want a system that still works when a terminal declines your card, a transaction gets flagged, or a merchant won't take your usual option.

A Guide to Notion for Freelance Business Management

If your workspace feels busy but fragile, you do not need more pages. You need one connected system. Treat your freelance business like a business-of-one and use Notion as the control layer that connects client decisions, delivery, and billing in one place.