Quick Answer

Start with a mixed-rail operating model: run virtual-card ePayables for card-ready suppliers, keep ACH for bank-ready vendors, and reserve checks for controlled exceptions. Then clear three launch gates before scaling: enrollment data that routes payments correctly, approval controls for issuance and release, and reconciliation that links the AP record to provider references without spreadsheet reconstruction. This sequence reduces manual payment handling while keeping audit evidence intact during staged check reduction.

Start Here if You Need to Replace Checks Without Breaking Ops#

If you are replacing checks in a high-volume environment, treat this as a controls-and-scale decision first. The goal is to choose the right ePayables model, introduce virtual cards without creating avoidable new exceptions, and keep reconciliation and audit trail intact from the AP source record through payout.

- Use this guide when volume and risk are already operational problems

This guide is for platform, finance, payments ops, and engineering teams handling recurring B2B payments where manual checks, exception handling, and approval gaps are already creating operational friction. It is not a basic AP explainer for low-volume, one-off invoices. At this scale, rail choice becomes an operating decision. The ACH Network reported 35.2 billion payments in 2025 worth $93 trillion, and reporting also cited close to 8.1 billion B2B payments with B2B volume growth near 10% in 2025. At that level, rail choice changes controls, supplier handling, and finance review, not just delivery speed.

- Use a three-part decision path, not a single-rail stance

The immediate question is usually not whether to digitize. It is which rail mix gives you the best balance of supplier coverage, approval control, and reconciliation workload. ePayables is commonly defined as digital vendor payments using virtual cards assigned per supplier, and virtual card programs support controls such as date, amount, and merchant limits. Some programs also describe 45+ payment controls. Start with traceability. Each payment should map cleanly from the AP record to the issuer or bank reference and then into reconciliation output. If you still need spreadsheet repair to do that, the operating model is not ready. Plan for mixed rails from day one where needed, with explicit approval rules and fallback handling.

- Keep scope narrow and evidence standards high

This guide focuses on operator decisions that often get skipped: rail selection, supplier enrollment, approval controls, reconciliation mapping, and audit evidence. It does not assume uniform pricing, universal card acceptance, or a fast full shutdown of checks. The adoption picture still points both ways. AFP survey reporting says 65% of respondents reported check-fraud exposure, while 70% of organizations currently using checks said they did not plan to discontinue checks within two years. Mixed-rail operations remain common. Approve this work only when you can verify three things up front: supplier enrollment data can route payments reliably, your control model can approve and release cleanly, and reconciliation outputs produce a defensible audit trail without manual reconstruction.

How to Choose the Right ePayables Path for Your Team#

Choose your ePayables path as an operating-model decision, not a generic AP software purchase. If payment volume is growing, supplier readiness, rail coverage, controls, and reconciliation quality matter more than any promise to remove checks in one step.

- Choose this path when payments are cross-functional, not AP-only

Use this section when AP, payments ops, product, and engineering each own part of payment execution and reliability. AP automation is often a stronger fit once operations become higher volume and more complex. One provider flags businesses processing more than 150 payments and/or 200 invoices per month as a common fit signal, not a universal cutoff. What matters is whether the model will hold up across approvals, file delivery, and reconciliation.

- Do not force a full rollout if checks are occasional and operations are stable

If you issue only occasional checks and do not need additional automation or controls, a full ePayables rollout may add more overhead than value. Supplier enablement and integration work can be meaningful. The trigger is operational strain, not a preference for digital tools.

- Set selection criteria before comparing providers

Use the same five checks every time: supplier acceptance, rails coverage, reconciliation burden, integration effort, and control requirements. Supplier acceptance comes first. Even if a provider cites a network of 600,000 suppliers accepting electronic payments, validate your own supplier readiness and payment preferences before assuming coverage. Next, test reconciliation and integration. Checks and ACH can require more manual invoice matching, and providers may route payments by supplier preference across virtual card, ACH, and check, so review remittance outputs and reconciliation workflows early. For controls, confirm that virtual payments can run only when approved and only for the authorized amount. If you cannot test payment file input, provider or bank output, and reconciliation together, you are not ready to choose.

- Apply a simple decision rule

If volume is rising, move first on an ePayables model that includes virtual cards. If supplier acceptance is low, launch with fallback rails from day one, typically ACH and, where needed, check, instead of delaying the program. That is usually the practical path because check usage is still material. One bank notes nearly 40% of commercial payments are still made by check. The strongest path supports operations now and phased check reduction over time.

What ePayables Means in Real Platform Operations#

In platform operations, ePayables means replacing check-heavy AP payments with electronic supplier payments, often virtual cards, with approvals, routing, and reconciliation built into execution. Once you choose a path, this is the operating model you are actually implementing.

- Electronic supplier payments, not generic "digital payments"

In AP workflows, ePayables means paying suppliers electronically instead of mailing paper checks. It is not a consumer-style checkout flow. The payment sits inside your payables process, with operational controls wrapped around it.

- A file-driven execution model

After approval, AP or your ERP submits an electronic payment file, and that file can route payments across rails such as virtual card, ACH, and check. The real checkpoint is end-to-end behavior. File input, bank response, and reconciliation output should all be testable together before you scale.

- Virtual card credentials are control primitives

A common payment unit is a bank-provisioned virtual card credential set: a 16-digit number, expiration date, and security code, with some programs explicitly using a 3-digit CVV2. Programs can also bind a virtual account to a specific supplier, amount, and validity window. Implementation varies, so confirm how credentials and remittance are delivered in your workflow.

- Approval and traceability make the model reliable

In real operations, payment execution is approval-gated and constrained to authorized amounts, with each virtual card number able to act as a unique reconciliation identifier. If exceptions cannot be traced from payment file to card reference to reconciliation export, you have electronic payments, but not a reliable ePayables operating model.

For a step-by-step walkthrough, see What is a Virtual IBAN and How Do Platforms Use It to Collect Payments Globally?.

Checks, ACH Payments, and ePayables Compared for Platform Use Cases#

Many platforms run a mixed-rail model. Use ePayables where card acceptance is real and control depth matters, keep ACH primary for bank-ready suppliers, and keep paper checks as a tightly managed fallback.

At a glance#

| Rail | Typical setup pattern | Supplier acceptance risk | Control depth | Reconciliation complexity |

|---|---|---|---|---|

| Paper checks | Commonly retained as a secondary option in business payments | Lower near-term acceptance risk where suppliers still accept checks | Limited once issued; checks are frequently reported as fraud-susceptible | Typically more manual than digital rails |

| ACH payments | Bank-to-bank ACH flow that is batch and file or schedule driven | Often workable for bank-ready suppliers | Moderate; generally less granular than virtual-card controls | Moderate; timing is tied to ACH processing windows |

| ePayables with virtual cards | Provider implementation plus supplier enablement for vendor-assigned or single-use cards | Can be highest of the three because not every supplier accepts card payments | Deepest where supported; controls can include spending amounts, payment periods, and additional transaction controls | Varies by provider program and supplier acceptance |

ACH can be simpler for suppliers already set up for bank transfers. ePayables can improve control depth. Vendor-assigned or single-use virtual cards can be tied to a specific supplier and, in some programs, a specific amount or validity window.

Decision checkpoints#

- Prefer ePayables first when control depth is the primary goal and supplier card acceptance is proven.

- Keep ACH primary when supplier readiness is the constraint and your timing can operate inside ACH batch windows. Same Day ACH remains window-based. Submission runs until 4:45 p.m. ET, and third-window interbank settlement is at 6:00 pm ET.

- Keep checks only as a temporary fallback for suppliers you cannot move yet. Checks still persist, but fraud risk remains material. AFP reports 65% of respondents cite checks as most fraud-susceptible, and 70% of organizations using checks report no immediate plans to discontinue them.

If your biggest problem is control depth, start with ePayables for card-accepting suppliers. If your biggest problem is supplier readiness, keep ACH as the primary electronic rail and add virtual cards where the control benefit justifies the enablement effort.

Before scaling, validate supplier acceptance and reconciliation outputs rail by rail in your own AP or ERP flow. Fee outcomes and speed gains vary by provider and operating model, so confirm both in your own cost model instead of assuming a universal advantage.

The 5 ePayables Setup Options and Where Each Fits Best#

If supplier readiness is mixed, choose a setup pattern before you optimize rails. A practical starting point is often hybrid routing (card plus ACH) or ePayables-first with a defined fallback. Narrower card patterns make more sense once acceptance and controls are proven.

| Option | Best fit | Key consideration |

|---|---|---|

| Per-supplier card assignment | Supplier payments are stable and recurring | Supplier enablement work, including enrollment and self-service support |

| Single-use virtual cards per payment | You want tighter per-payment control and a clear payment-level trail | Higher issuance and coordination volume across suppliers, remittance delivery, and reconciliation |

| Hybrid ePayables plus ACH payments | Card acceptance varies by supplier | Routing logic, remittance standards, and reporting must work across both rails |

| ePayables first with explicit fallback payment rail | You need to reduce manual handling quickly but know card acceptance will not be universal | Document fallback triggers, override authority, and required evidence for each routed payment |

| AP-led file-based launch before deeper API automation | You need near-term modernization without waiting for full API integration | Verify that the payment file, issuer acknowledgment, and reconciliation output all map back to the original invoice or payable ID |

1. Per-supplier card assignment#

Use this when supplier payments are stable and recurring. Some virtual-payables programs can restrict payments to a single supplier and allow multiple charges, which supports a repeatable payment identity for that vendor.

This pattern can help keep AP mapping consistent across the supplier record, remittance, and payment event. The tradeoff is supplier enablement work, including enrollment and self-service support. If enablement is weak, exception volume can increase, including remittance mismatches and fallback use. Confirm the supplier can process the assigned virtual card and that your ERP or AP output maps supplier ID to the correct payment identifier every time.

2. Single-use virtual cards per payment#

Use this when you want tighter per-payment control and a clear payment-level trail. A virtual card is a temporary number linked to a funding account, and some programs can limit each card to a single use.

This fits variable invoice amounts, one-off payouts, or categories where reuse exposure is a concern. Each payment can be tied to a unique virtual card account. The tradeoff can be higher issuance and coordination volume across suppliers, remittance delivery, and reconciliation. Pilot card issuance, supplier acceptance, and AP reconciliation export together before scaling.

3. Hybrid ePayables plus ACH payments#

Use this when card acceptance varies by supplier. Keep ePayables for card-accepting suppliers and route bank-ready suppliers to ACH, an electronic transfer over the ACH network.

The benefit can be broader coverage without forcing full card adoption on day one. The tradeoff is dual-rail operations. Routing logic, remittance standards, and reporting must work across both rails. Some provider models also support direct bank transfer in virtual-payables flows, but routing and reconciliation behavior is provider-specific. Verify exactly how routing is set, what references return per rail, and whether card and ACH outcomes reconcile in one export.

4. ePayables first with explicit fallback payment rail#

Use this when you need to reduce manual handling quickly but know card acceptance will not be universal. Set a clear policy: attempt card-first for enabled suppliers, then route to a defined fallback rail, commonly ACH, with checks reserved for true edge cases.

The strength is policy consistency across approvals and release behavior. The risk is exception churn when fallback rules are unclear. If triggers and override rules are vague, teams end up adjudicating payments one by one. Document fallback triggers, override authority, and required evidence for each routed payment.

5. AP-led file-based launch before deeper API automation#

Use this when you need near-term modernization without waiting for full API integration. ePayables can launch as an AP-managed, post-invoice, file-based flow and still replace part of check volume.

This fits teams that can already produce an electronic payment file and want a controlled rollout. Some implementations offer a website, batch-file processing, and real-time XML API, which supports phased migration instead of a hard cutover. Verify that the payment file, issuer acknowledgment, and reconciliation output all map back to the original invoice or payable ID. For a related architecture example, see How MoR Platforms Split Payments Between Platform and Contractor.

Supplier Enrollment Choices That Decide Success or Failure#

Supplier enrollment is often the go/no-go gate after you pick card-first, hybrid, or fallback routing. Do not scale ePayables until enrollment quality supports reliable reconciliation and manageable exceptions. Weak supplier data can create more manual work, not less.

| Enrollment area | What to confirm | Checkpoint |

|---|---|---|

| Legal payee record first | Legal name, person or corporation code, tax identification number, and 1099 information where relevant | ERP payee data matches the entity receiving remittance and appearing in the payment file |

| Explicit rail acceptance and preference | Whether the supplier accepts virtual cards and which rail to use when they do not | Store acceptance and preferred method in the supplier profile and drive routing from that data |

| Remittance format and matching evidence | Supplier can consume the remittance format, unique payment identifier, and your invoice reference | Run a test payment or remittance sample and confirm supplier-side matching |

| Finance signoff needs evidence and named owners | Enrollment progress, tracked rejection causes or objections, and fallback-rail usage patterns by supplier segment | Define triage by failure origin before launch so issues route to one owner on first review |

- Legal payee record first

Start with the legal payee you will actually pay, not just an outreach contact. Capture legal name, person or corporation code, tax identification number, and 1099 information where relevant. If your process uses two supplier states, prospective and spend authorized, only spend-authorized suppliers should move into financial transactions. Checkpoint: confirm your ERP payee data matches the entity receiving remittance and appearing in the payment file.

- Explicit rail acceptance and preference

Do not assume virtual-card acceptance. Enrollment should record both whether the supplier accepts virtual cards and which rail to use when they do not. Program rules differ, so fallback behavior should be documented per supplier. Checkpoint: store acceptance and preferred method in the supplier profile and drive routing from that data to reduce avoidable reissues.

- Remittance format and matching evidence

Acceptance alone is not enough if posting fails. Virtual payments can include detailed remittance data, and each virtual card number can act as a unique payment identifier, but only if the supplier can consume that format. Success is not just payment completion; it is clean matching to the invoice or payable. Checkpoint: run a test payment or remittance sample and confirm supplier-side matching with the unique payment identifier and your invoice reference.

- Finance signoff needs evidence and named owners

Before you expand volume, require signoff evidence: enrollment progress, tracked rejection causes or objections, and fallback-rail usage patterns by supplier segment. Campaign tracking and reporting should show whether enrollment objectives are being met. Set ownership boundaries clearly: AP owns payment feeds and payable source data; ops, or a dedicated enablement team, can own enrollment support and first-line triage; engineering should own issuer or API integration points needed for virtual-card issuance. Checkpoint: define triage by failure origin before launch so issues route to one owner on first review.

Use one operating rule: scale only when enrollment data is complete enough that fallback behavior is intentional, remittance is matchable, and vendor payment failures can be routed quickly to the correct owner.

Controls You Need Before You Increase Payment Volume#

Before you scale ePayables volume, your controls need to prove approvals, execution, overrides, and reconciliation in one traceable chain. If you cannot show who approved issuance, who released payment, what was overridden, and how it reconciled, higher volume can turn into more unresolved exceptions and weaker auditability.

- Approval gates tied to real payment actions

Separate approvals for card issuance, payment release, and exception overrides instead of relying on one generic "payment approved" status. Use role-based access control so permissions follow job function, and keep virtual-card controls tight: payments processed only after approval, only for the amount authorized, with single-use accounts constrained to supplier, amount, and expiration date. Checkpoint: for one payment, confirm approver identity, timestamp, supplier, authorized amount, and expiration setting in the same evidence chain.

- Traceability from payment file to bank reference to reconciliation output

Your control model is harder to defend if the electronic payment file cannot be traced through bank-side records and back into reconciliation output. ePayables workflows can support payment-file transmission and reconciliation-file delivery, and virtual-card identifiers can help anchor the payable, payment instruction, and reconciliation record. Checkpoint: replay one settled payment end to end from source file to bank reference or virtual-card identifier to reconciliation output. If you need spreadsheet stitching between systems, the audit trail is weaker than it looks.

- Risk-based policy gates and exception logging

Apply compliance gates where they actually belong, and be explicit about scope. OFAC review is framed as risk-based. AML programs for covered financial institutions require internal controls, and beneficial-ownership expectations under 31 CFR 1010.230 should be interpreted with reported FinCEN relief dated February 13, 2026 for covered institutions. Do not copy blanket KYC, KYB, or AML rules from other programs without checking your own regulatory posture and provider obligations. Checkpoint: every exception record should include trigger event, user or role, reason code, before and after state, and linked payment identifier, with log handling that supports generation, storage, access, and disposal. Free-text-only exception notes are a scaling risk.

Build the Cost Model Before You Commit to One Rail#

Do not choose a payment rail on sticker price alone. Use a scenario-based total operating cost model. Do not approve expansion until the provider validates the assumptions behind it. Once the controls are defined, this is where you test whether the model holds financially.

1. Start with total AP cost, not just rail fees#

Begin with direct rail cost, then add the full AP operating cost. For card-based payments, merchant discount rate is often cited in the 1% to 3% range. That is only a starting assumption until you validate it against your actual card mix and supplier profile.

Then add the indirect cost buckets teams often skip: AP handling time, reconciliation effort, supplier enablement, and exception handling. APQC's cost-per-invoice framing is useful here because AP cost includes outsourced, overhead, personnel, system, and other costs, not just payment fees.

2. Price supplier enablement and exception handling as real work#

Supplier enablement is not automatic and should be modeled as real effort. In practice, teams usually need to confirm supplier acceptance, remittance format, routing preference, fallback method, and ownership across AP and operations. Integration and training requirements also vary by provider.

Exception and loss exposure belongs in the model too. Checks create documented cost, delay, and fraud/loss exposure, so your paper-check baseline should include those risks and the manual follow-up work they create. AFP's 2024 survey release reports 80% of respondents experienced attempted or actual payments fraud activity in 2023, and 65% reported check-related fraud attacks.

3. Compare scenarios, not averages#

Averages hide decision risk, so compare full scenarios side by side.

| Scenario | Include | Common miss |

|---|---|---|

| Current paper checks baseline | Print and mailing steps, AP handling time, check exceptions, fraud and loss follow-up | Reconciliation delays and exception follow-up effort |

| ACH payments-heavy baseline | ACH processing steps and exception handling across AP workflows | Manual work when remittance mapping is weak |

| ePayables-heavy target state | Card-related costs, supplier enrollment, payment-file processing, reconciliation output, fallback rail use | Training, provider-specific integration effort, card acceptance variance |

For each scenario, replay one payment from source payable to settlement to reconciliation output and count the human touches. If a "low-cost" rail still depends on spreadsheet stitching, manual remittance matching, or repeated supplier outreach, the model is understating real cost.

4. Use a go/no-go rule before expansion#

Make the decision rule explicit. If tighter controls, payment-level identifiers, and potentially lower manual work outweigh added card-related costs in your supplier mix, expand ePayables in phases. If not, keep ACH or mixed rail as primary and use cards where they clearly improve operations.

Reconciliation quality is one practical upside to include. Virtual payments can carry detailed remittance information and unique payment identifiers, and single-use virtual accounts can be constrained to supplier, amount, and expiration date.

5. Separate knowns from unknowns before final signoff#

Keep two columns in the model: knowns and provider-validated assumptions. Knowns include your invoice volume, exception counts, AP staffing effort, and fallback rail usage. Assumptions include effective card pricing, supplier acceptance, implementation effort, reconciliation export quality, and training scope.

If the business case depends on one unverified blended card-cost assumption or vague automation savings, stop and validate before signoff. Final approval should require clear provider confirmation on pricing mechanics, integration scope, enablement ownership, and reconciliation evidence outputs.

Failure Modes That Break ePayables Rollouts and How to Prevent Them#

Once the cost model supports a test, rollout risk is usually operational. The failure points are typically supplier acceptance, reconciliation data quality, control discipline, and ownership when exceptions happen.

- Low supplier acceptance of virtual cards

Supplier acceptance is a known adoption risk, and resistance can come from fee concerns, integration complexity, or a preference for checks and ACH. Prevent this by defining a fallback rail design before launch, with a clear menu of payment options by supplier segment: card, ACH, or temporary check exception. Then track fallback volume by segment on a regular cadence so you can see where "card-ready" suppliers are still routing to legacy rails.

- Weak reconciliation from poor payment references

A rollout is harder to stabilize if finance still has to match payments manually. Require consistent remittance references and clear mapping between the AP record, payment event, and reconciliation output. Virtual payments can carry detailed remittance information and unique payment identifiers, and single-use virtual accounts can be restricted by supplier, amount, and expiration date. If ACH is part of fallback, enforce addenda format compliance so payments can be correctly identified and applied.

- Control gaps under time pressure

Control drift during a volume ramp can break rollout quality. Lock approval gates so payments run only when approved and only for authorized amounts, and implement control activities through clear policies and procedures. Keep segregation of duties intact: do not allow one person to request, approve, and reroute the same payment when deadlines tighten.

- Mismatched ownership when vendor payments fail

Mixed-rail operations are harder to manage when AP, ops, and engineering ownership is unclear. Define escalation paths with named responsibilities for enrollment issues, payment-file errors, remittance mismatches, issuer or bank coordination, and reconciliation closure. If ACH exceptions are in scope, include timeline handling in your playbook. For FedACH Request for Return workflows, RDFI responses are expected within 10 banking days (effective April 1, 2025), so internal handoffs should be explicit.

If you want one simple operating check, review fallback volume, reconciliation exceptions, and approval overrides together. That combined view can surface instability earlier than high-level launch metrics.

If you want a deeper dive, read What Is an e-Payable? How Virtual Cards and Digital Payments Replace Paper Checks in B2B.

A Phased Migration Plan Off Paper Checks#

A durable migration off checks is usually a four-phase operating change, not a rail switch. The goal is to reduce manual work and keep reconciliation and controls intact as you move supplier by supplier.

1. Baseline the current check and ACH reality#

Start with what AP is actually doing now. Baseline paper-check volume, ACH volume, exception volume, and the reconciliation effort required after payment is sent.

Market data supports the direction, but it does not replace your internal baseline. Checks declined 7.2% per year since 2018, to 11.2 billion by number. ACH reached 34.2 billion transfers in 2021, and in 2021 business payers made most commercial ACH credits by number and value.

Your Phase 1 evidence pack should include:

- Monthly counts and dollar volume by rail

- Exception rate by rail and supplier segment

- Reconciliation aging or manual touch count

- Return, rejection, or reissue reasons

- Approval override count for vendor payments

Before scaling, sample recent check and ACH payments and verify the full trail from the AP record to the payment event to reconciliation output. If reference data is weak, fix that first.

2. Launch a controlled cohort where card fit is highest#

Start with suppliers that have recurring payments, stable payee data, and realistic virtual-card acceptance. Use clear per-supplier routing rules to keep exception handling clear.

Enrollment quality makes or breaks this phase. Track completion rate, rejection reasons, supplier response lag, and whether enrolled suppliers actually transact on the intended rail.

Do not assume smooth acceptance. Supplier-side virtual-card acceptance can be manual, time-consuming, and costly, so keep ACH as a planned fallback when remittance or processing is not stable.

3. Expand by segment, not by enthusiasm#

Scale by supplier segment, not by broad volume pushes. Segment by recurrence, invoice variability, card acceptance, and reconciliation complexity. Track these every cycle:

- Fallback rail usage by segment

- Reconciliation quality, including unmatched or late-applied items

- Audit-trail completeness from the AP record to payment execution to closeout

If payment success rises but remittance matching is weak in supplier ERP workflows, expansion is premature. Keeping ACH primary for poor card-fit segments is also a valid operating choice. Recent ACH data shows continued growth, including 8.5 billion payments in Q1 2025, with B2B up 9% to 1.9 billion.

4. Retire paper checks by policy, with explicit exceptions#

Retire checks through policy, not informal behavior change. Set checks as non-standard by default, then define explicit exception handling. Use a clear policy structure:

- Named approvers for check exceptions

- Valid reason codes

- Required documentation

- Exception validity window and review cadence

The federal model shows the pattern: set a cutover rule and allow defined exceptions. For private platforms, copy that structure, not the federal deadline. Once a supplier is successfully live on a non-check rail, require explicit reapproval for any future check request to prevent check creep.

ePayables replace paper checks with electronic execution, but the migration only holds when policy, enrollment tracking, reconciliation quality, and exception governance move together.

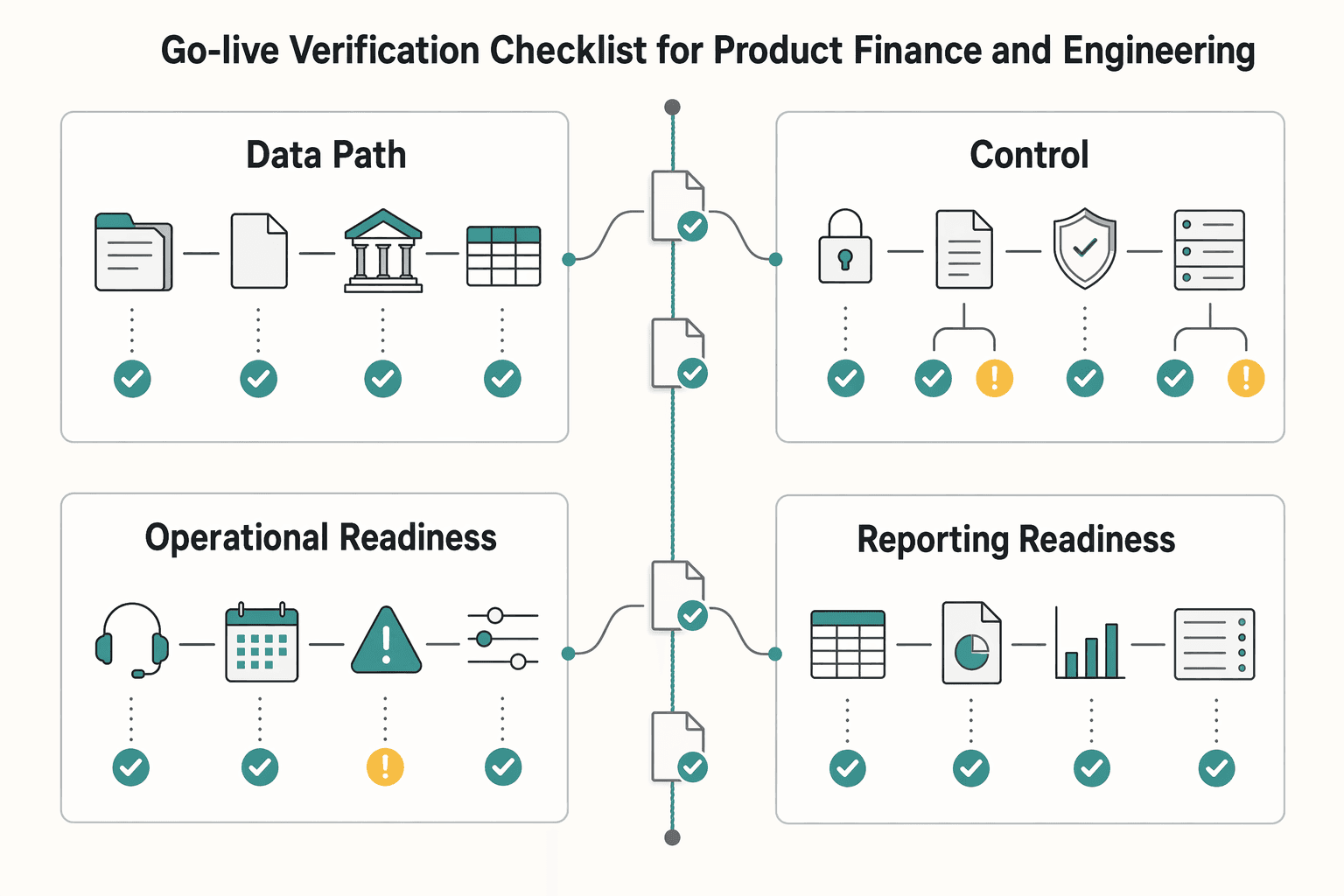

Go-Live Verification Checklist for Product, Finance, and Engineering#

Go-live is not a config milestone. In ePayables, it is a no-go until product, finance, and engineering can prove the payment path, controls, and reporting hold under retries, exceptions, and supplier support load.

| Area | Go-live check | Key point |

|---|---|---|

| Data path integrity | Trace one source transaction from AP record to electronic payment file, bank/payment-system acknowledgment, and reconciliation export | Payment events tie back to source data without manual guesswork |

| Control integrity under replay and retry | Re-run a payment request with the same idempotency key and confirm no duplicate effect; replay webhook or event delivery | Validate duplicate prevention and auditability together |

| Operational readiness for mixed-rail reality | Document supplier support ownership, fallback rail execution, and after-hours accountability through a RACI | Ownership and fallback execution, not just supplier status |

| Reporting readiness for finance review | Finance can open one audit-trail view and see approval, execution, remittance, and reconciliation status without rebuilding the record in spreadsheets | Reporting is go-live critical only when it supports direct audit review |

- Data path integrity

Go live only when you can trace one source transaction end to end: AP record, electronic payment file, bank/payment-system acknowledgment, and reconciliation export. If you use ACH files, validate matching header and control records and confirm each entry's unique trace number can be tied into downstream records. If your bank sends ISO 20022 status messages such as pain.002.001.03, verify you can map both batch-level and transaction-level outcomes back to the original payment intent. This is not "file sent successfully"; it is proof that payment events tie back to source data without manual guesswork.

- Control integrity under replay and retry

Go live only when controls still work off the happy path. Re-run a payment request with the same idempotency key and confirm no duplicate effect, then replay webhook or event delivery because providers may resend undelivered events for up to three days. Confirm permissions, approval overrides, and exception handling all land in a reviewable security log. Here you are validating duplicate prevention and auditability together.

- Operational readiness for mixed-rail reality

Go live only when supplier support ownership and fallback rail execution are documented. Verify who owns supplier questions, who can switch a failed payment to another approved rail, and who is accountable after hours through a documented RACI. If card-accepting suppliers are still being onboarded ad hoc, keep volume constrained. This check is about ownership and fallback execution, not just supplier status.

- Reporting readiness for finance review

Go live only when finance can open one audit-trail view and see approval, execution, remittance, and reconciliation status without rebuilding the record in spreadsheets. Virtual-card programs can support this with detailed remittance data and a unique payment identifier per card number. If reconciliation still depends on offline file stitching, you are early, not ready. Reporting is go-live critical only when it supports direct audit review, not after-the-fact cleanup.

Use this checklist as your implementation handoff. Then map each approval gate, retry path, and reconciliation export in Gruv Docs.

The Practical Next Step for Most Platforms#

For most platforms, a practical next step is a constrained ePayables rollout with explicit go or no-go gates, followed by staged check retirement with documented exceptions.

1. Pilot a narrow cohort#

Start with a supplier cohort you can observe end to end, not the largest spend segment. The goal is to prove reconciliation and audit-trail integrity under real volume before you chase migration totals.

Your first checkpoint is traceability from the AP record to the payment credential to the reconciliation result. With virtual cards, each payment can have a unique card number, expiration date, and CVC. Scale only when your team can map that chain cleanly without spreadsheet reconstruction.

2. Set hard go or no-go gates#

Do not expand on elapsed time alone. Promote cohorts only when enrollment, controls, and exceptions meet explicit thresholds you define up front.

Treat enrollment tracking as a launch control, not a reporting afterthought. For each gate, keep an evidence pack with:

- supplier enrollment completion and rejection reasons

- confirmation that approval routing follows existing approval processes

- exception counts by rail, plus cause and owner

- audit-trail samples linking source record, payment event, and reconciliation output

If exception volume rises faster than stable enrollment, pause expansion and fix the operating handoff first.

3. Expand only when mixed rail is stable#

Mixed-rail operation is normal during transition. Federal Reserve business research, covering 2,000 U.S. businesses, shows checks and cash still appear as secondary methods. ACH also remains at scale, with 8.5 billion payments and $22.1 trillion in Q1 2025, so keeping ACH alongside cards is practical while supplier readiness catches up.

Retire checks in stages, with written exceptions and periodic review. That mirrors Treasury's paper-check phaseout becoming effective on September 30, 2025, with Section 4 exceptions.

Keep fallback capability where supplier profiles require it. Atlanta Fed reporting notes nearly 80 percent of very small firms, under $1 million revenue, use checks, so a forced card-only policy can create avoidable exceptions for those suppliers.

Related: Virtual Credit Cards for Platforms: How to Issue Single-Use Cards for Contractor and Vendor Payments. Before full cutover, validate your target rail mix, fallback design, and coverage assumptions with Gruv's team.

Frequently Asked Questions

What are ePayables in plain terms for a platform team?

ePayables refers to handling payables electronically rather than through paper-check workflows. The term is not standardized, so some providers use it for electronic payables in general while others use it specifically for virtual-card vendor payments. In practice, confirm which definition your provider uses before you scope implementation.

How are ePayables different from ACH payments in day-to-day operations?

ACH is a batch-based rail for electronic credit and debit transfers between depository institutions, so operations typically center on batch submission and reconciliation. Virtual-card ePayables focuses on issuing digital payment credentials per supplier or payment and applying transaction-level controls. ACH is also a very large rail, with 35.2 billion ACH payments in 2025.

Can ePayables fully replace paper checks for all vendor payments?

Not immediately for every supplier and use case. Checks are still in active use, and Federal Reserve materials note that about 11 billion checks were written in 2021 even as usage declined. Treat check removal as a phased transition and keep a fallback rail until supplier acceptance is proven.

How do virtual cards reduce payment risk compared with paper checks?

Paper checks are vulnerable to theft, alteration, and forgery. Virtual cards can be configured with controls such as date, amount, and merchant parameters, which narrows where a payment credential can be used. That can reduce exposure, but it does not eliminate fraud.

What should we evaluate first before switching from checks to ePayables?

Start with supplier enrollment and acceptance, because that is the practical gate for scaling virtual-card disbursements. Then verify that reconciliation is reliable across the rails you plan to run. If those two pieces are weak, you may just shift exceptions instead of reducing them.

When should we keep a fallback payment rail instead of forcing full card adoption?

Keep a fallback when supplier enrollment is incomplete or supplier card acceptance is inconsistent. Mixed-rail operations are normal, and AP offerings commonly support virtual card, ACH, and check together. Consider delaying card-only behavior until enrollment and exception handling are stable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01trusted

- csrc.nist.gov/pubs/sp/800/92/r1/ipdtrusted

- csrc.nist.gov/glossary/term/role_based_access_controltrusted

- doa.virginia.gov/reference/virtualPayables/SupplierFAQ.pdftrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fbi.gov/investigate/cyber/alerts/2025/mail-theft-rel...trusted

- federalregister.gov/documents/2025/03/28/2025-05522/modernizing-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is an e-Payable? How Virtual Cards and Digital Payments Replace Paper Checks in B2B

Platform teams usually replace paper checks once payment speed, status visibility, and clean matching become operating requirements, not nice-to-haves. Checks still work in many workflows, but they can become a bottleneck as volume rises and control expectations tighten. If your team is still chasing check status by email, you are already paying the cost of that bottleneck.

Virtual Credit Cards for Platforms: How to Issue Single-Use Cards for Contractor and Vendor Payments

Single-use virtual cards are often positioned as a fit for controlled vendor payments, but not for every contractor payout. This guide helps product, Payments Ops, and AP teams decide whether virtual cards fit their operating model, or whether cards belong alongside ACH, checks, or other payout rails.

Open Banking for Platforms: How to Use Account-to-Account Payments to Bypass Card Fees

Account-to-account (A2A) payments can reduce card-fee exposure, but only in the right lanes and markets. The real decision is not whether to replace cards. It is which transactions should move off card rails first, and what that change adds in product, support, finance, and control work.