Quick Answer

Lock the payable event and revenue base first, then keep compensation in three separate rules: base split, tier trigger, and bonus scoring. Use the same system-of-record data so finance, ops, and legal can reproduce one payout line without debate. Before live cash, run a shadow cycle that traces source event, ledger record, payout state, provider outcome, and exception note. Pause release when KYC, KYB, AML, or W-8/W-9 documentation is incomplete.

What a stable revenue-share model needs#

A workable platform revenue-sharing model starts with payout logic you can explain and report on clearly. The sequence matters: define the parties, covered revenue streams, and payment and reporting rules first, then choose a simple split method (fixed, performance-based, or tiered) and put dispute and exit terms in writing before cash moves.

Pick the revenue model that matches your platform economics#

Pick the model whose payout result can be independently reproduced from source records, then add complexity only after that base rule works consistently. There is no universally best allocation rule, so your job is to choose one your team can explain, calculate, and defend under review.

Step 1 Test whether your contribution signal is actually auditable#

Before you lock in ad, commission, or subscription sharing, test the signal behind the payout. If finance and ops cannot recreate the payable amount from trusted records, the model is too complex for this stage.

Start with a simple check: can someone outside product calculate the same result from the underlying records? If not, tighten the base rule before you add tiers, bonuses, or variable weighting.

Step 2 Match the allocation rule to your economics and review burden#

Three baseline rules are practical starting points: equal division, pro-rata, and user-centric. Compare each against fairness, stability, and failure modes before you scale it.

| Allocation rule | What it emphasizes | Where it can strain operations |

|---|---|---|

| Equal division | Simplicity and predictable interpretation | Can ignore real differences in contribution |

| Pro-rata | Share proportional to measured contribution | Depends heavily on input quality and measurement design |

| User-centric | Allocation tied more directly to user-level behavior | Can be harder to operate when data structures are fragmented |

Stress-test the rule with realistic edge cases, including changes in input measurement units, subscription-sharing behavior, and group decomposition. If the rule breaks under those tests, simplify it before launch.

Step 3 If you use tiers, keep them sequential and pre-defined#

Tiered logic should be explicit and sequential: the next tier activates only after the previous tier is satisfied. Keep that ordering clear in your governing agreement before execution so payout interpretation does not drift during live operations.

Complexity is a tradeoff: too much layering can reduce goal clarity, while overly simple structures can miss meaningful differences. If you add performance-linked bonuses, keep goals SMART so participants can understand what drives outcomes.

Step 4 Keep the payout base definition explicit#

Keep the agreement focused on revenue logic: what is included, what is excluded, when amounts become payable, and how adjustments or disputes are handled. Use a pre-launch checkpoint: ask legal, finance, and partner ops to define the payout base in one sentence. If those definitions differ, rewrite it.

Related: How to structure a 'joint venture' agreement for a software product.

For expansion dynamics, see What Is Negative Churn? How Platform Operators Achieve Revenue Expansion Without New Customers.

Prepare the inputs before you draft splits#

Before you negotiate percentages, lock the inputs. If a payable line does not map to one owner, one system of record, and one verification artifact, your split design is not ready.

| Input | Owner | System of record | Verification artifact |

|---|---|---|---|

| Economic baseline by segment | Finance | Pricing, billing, and revenue data by segment | Segment view that lists in-scope revenue streams and agreed deductions before split |

| Measurement ownership | Named product or data owner for each payable event | Event store or billing platform that records the payable event | Versioned event definition, attribution window control note, and replay check for late, duplicate, or corrected events |

| Legal and tax scope | Legal plus finance | Draft revenue-sharing agreement and onboarding records | Responsibility matrix for tax handling, required documents, and any unresolved requirements that must be verified against the contract, finance policy, provider reports, and tax records before use. |

| Shared evidence pack | Partner ops | Reporting workspace tied to the payment schedule | Current pack with revenue sources, contribution metrics, performance targets, statement template, dispute path, and exit terms |

- List parties, revenue streams, and deductions by segment.

Identify everyone involved, list current and expected future revenue streams, and quantify contributions (money, time, skills, or intellectual property). Define which costs are deducted before revenue is split. Pass: finance can show pre-share contribution by segment from agreed inputs. Fail: one party assumes add-ons, upgrades, fees, or future monetization are included while another assumes they are excluded.

- Assign measurement ownership before you call anything payable.

Name an owner for each payable event, then document the event definition version, attribution window control, and handling for late, duplicated, or corrected events. Keep the method simple but reproducible from source records. Pass: a team outside product can recreate payable amounts from the system of record using the current definition version. Fail: event names change without version notes, or no one can explain replay and correction handling.

- Set legal and tax dependencies during drafting, not after.

State who collects documents, who handles tax responsibilities, what must be complete before first payout, and where jurisdiction-specific checks still apply. Where the exact requirement is unresolved, verify it against the contract, finance policy, provider reports, tax records, or other approved source records before use. If the setup is closer to a shared product venture than a standard partner payout, draft in parallel with How to structure a 'joint venture' agreement for a software product. Pass: missing documentation can block payout, and the agreement assigns each responsibility clearly. Fail: tax scope lives in side threads or unresolved comments.

- Assemble one shared evidence pack and tie it to reporting.

Include revenue sources, contribution metrics, performance targets tied to measurable outcomes, payment schedules, dispute handling, and exit terms. This is the same pack ops should use for statements and legal should use for review. Pass: payout statements and supporting evidence come from one shared pack. Fail: disputes require reconstructing line items from scattered spreadsheets, chat logs, and memory.

For a step-by-step walkthrough, see How to Set Up a Multi-Entity Payment Structure for Global Platform Operations.

Design split tiers and bonus rules that do not backfire#

Use a layered design so payouts stay understandable and auditable: base split first, tier uplift second, bonus pool last. Trying to force all incentives into one percentage usually creates disputes and margin drift.

Step 1 Build the payout math in layers#

Start with a base split for eligible payable events. Add tier uplift for scale, then add a separate bonus layer for performance.

Keep each layer separate in reporting. For each partner and period, you should be able to show the payable base, base rate, tier status, and bonus result from source records.

Be explicit about the payable base. Do not blur revenue-share and profit-share logic, and if downside sharing applies, state it clearly in the same rule set.

Step 2 Gate tier uplifts with consistency rules#

Volume alone should not unlock richer tiers. Add a written consistency gate so uplift can be paused when performance quality falls below your defined standard.

Use rules that can be reproduced from records, not judgment calls. In one platform case, consistency controls included a cap where a single day could not exceed 50% of total profits and a minimum profitable-day rule (for example, 3 days at 1%).

If your sales cycle is long, separate tier-qualification windows from payout cadence. You can still pay monthly while qualifying tiers on a longer trailing window to reduce reversals.

| Tier design | Likely behavior effect | Margin impact | Operational complexity |

|---|---|---|---|

| Flat base split only | Easy to understand, weaker incentive to improve | Predictable but may underreward strong contributors | Low |

| Volume tiers only | Encourages growth, can invite threshold gaming | Can drift if low-quality volume qualifies for higher rates | Medium |

| Volume tiers with consistency gate | Rewards scale with quality control | Better protection when uplift can be frozen | Medium to high |

| Base split plus bonus pool | Targets specific outcomes without rewriting the core split | More controllable if pool size and eligibility are bounded | High |

Step 3 Constrain bonuses so they stay useful#

Treat bonuses as a bounded layer, not a replacement for the core commercial deal. Define the pool size, eligibility, scoring period, and exception handling in writing.

Keep bonus metrics short and auditable, and make sure finance can reproduce results after close. Track trend checkpoints each month so rule changes can be reviewed against real outcomes.

Plan for concentration risk. In one case, over 71.4% of payout outflows occurred on first withdrawal, which is why consistency-focused safeguards were introduced.

For packaging strategy, see How to Build Plan Tiers and Add-Ons That Maximize Revenue Per Platform User.

For a lean-team implementation, see IndieHacker Platform Guide: How to Add Revenue Share Payments Without a Finance Team.

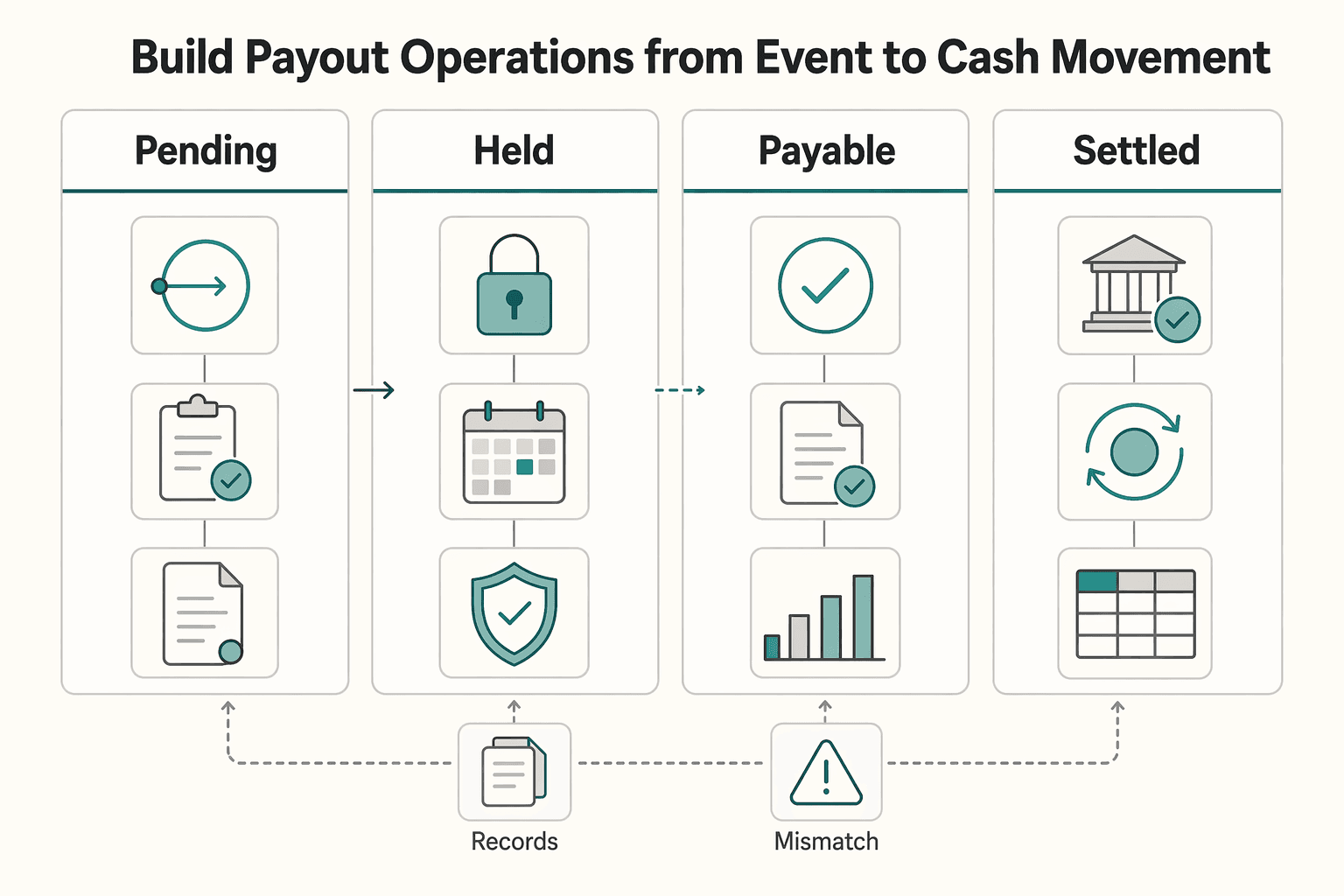

Build payout operations from event to cash movement#

Treat payout operations as a state flow, not a percentage batch: every line should move through clear states so you can explain each cash movement without interpretation.

| State | When it applies |

|---|---|

| Pending | until [program criteria verified] |

| Held | if [risk or dispute condition applies] |

| Payable | when [release criteria met] |

| Settled | only after provider confirmation |

Step 1 Map a single event-to-cash flow. Move each source event through eligibility review, hold (if needed), payable, payout batch, provider outcome, and final settlement. Keep adjustments separate from the original event so reversals, chargebacks, or deduction-based net-share items do not rewrite history.

Your checkpoint: for any payout line, you can trace the originating event, the rule that made it payable, and the later state change that moved or reduced cash.

Step 2 Keep the ledger first, then reconcile outward. Your internal ledger record should include event ID, partner ID, amount basis, status, and calculation rule. Reconcile with a fixed loop: internal ledger record, provider outcome, exception queue, and a named resolution owner for each mismatch.

Do not treat provider status as source truth before your own ledger is complete, or dispute resolution gets harder later.

Step 3 Define pending and payable eligibility in your own operating model. Use reproducible states such as pending until [program criteria verified], held if [risk or dispute condition applies], payable when [release criteria met], and settled only after provider confirmation. Require a resolution note and evidence pack before any manual promotion from pending or held states.

Step 4 Set payout cadence by cohort risk. Monthly can work, but your review depth should follow data reliability and dispute exposure. Low-variance cohorts can run on standard review, while new partners, volatile ad-sharing inputs, or high-adjustment cohorts should trigger pre-release sampling or full review before cash moves.

For a concrete execution example, see Podcast and Audio Platform Payouts: Ad Revenue Sharing and Per-Stream Models. For a payments-adjacent revenue stream, see Calculate Platform Interchange Revenue From Card Transactions and What You Keep.

Put contract terms and compliance gates in writing#

Write payout logic into the contract so every payout decision is explainable from the signed terms, not team-by-team interpretation. If a reviewer cannot map a payout line to a clause, margin drift and disputes become likely.

| Contract area | What to state | Why it matters |

|---|---|---|

| Payable revenue | What creates a payable amount, what is excluded, and what can reduce it later | A reviewer can trace each inclusion, exclusion, or adjustment to a clause |

| Compliance gates | When payouts are paused and when they can proceed for KYC, KYB, or AML checks | The same status gets the same treatment across teams |

| Document dependencies | What happens when W-8 or W-9 documentation is missing or incomplete | Teams know what is held and what partner communication is sent |

| Change control | Who approves changes, how notice is given, when updates take effect, and how previously earned amounts are handled | Updates stay controlled after signature |

Step 1. Define payable revenue so legal terms match calculation logic. State what creates a payable amount, what is excluded, and what can reduce it later. Name the revenue base, exclusions, reversals, credits, refunds, chargebacks, and dispute handling in plain language. Your check: for any payout line, a reviewer can point to the exact clause that explains it.

Step 2. Write compliance gates as operating conditions. If your program uses KYC, KYB, or AML checks before release, define when payouts pause and when they can proceed. Keep the rule operational rather than improvised so teams apply it consistently.

Step 3. Make document dependencies explicit up front. If your workflow requires W-8 or W-9 forms, state what happens when required documentation is missing or incomplete. Clarify what is held and what communication is sent to the partner.

Step 4. Add change-control terms for tiers and KPI updates. Define who can approve changes, how notice is given, when updates take effect, and how previously earned amounts are handled. Ongoing contract management helps protect outcomes and reduce third-party risk. Maintain the terms, review them regularly, and monitor compliance after signature.

Related: Podcast and Audio Platform Payouts: Ad Revenue Sharing and Per-Stream Models.

For the full breakdown, see How to Structure Platform Fees Without Violating Money Transmission Laws.

Launch with a shadow period and hard go live criteria#

Do not release live cash until shadow runs show that finance, support, and engineering reach the same payout answer from the same evidence. This is where split, tier, and bonus design either proves reliable or starts creating partner disputes.

Step 1. Run a production-equivalent shadow cycle#

Simulate production without moving funds, using the same inputs, timing, and reconciliation path you plan to run live. Treat line-level traceability as the pass condition, not cohort averages.

For each payout line, verify one full evidence chain: source event, ledger record, payout decision state, provider outcome, and exception disposition.

If any payout still needs spreadsheet fixes or side-channel judgment, extend shadow. That usually means your process depends on tribal knowledge instead of reproducible evidence. For a model-specific implementation example, see Podcast and Audio Platform Payouts: Ad Revenue Sharing and Per-Stream Models.

Step 2. Lock go-live gates before reviewing shadow results#

Define pass or fail gates before anyone reviews outcomes, then apply them by partner cohort so healthy averages do not hide broken segments. At minimum, document:

- variance between ledger output and provider reports: verify the exact variance limit from finance policy, provider reports, and approved source records before go-live

- unresolved exceptions still open: verify the exact exception tolerance from the contract, finance policy, and approved source records before go-live

- reconciliation completeness across the full evidence chain

If variance clusters around one source field or partner group, pause go-live and fix instrumentation first. Weak payout logic tends to surface later as churn, missed goals, and avoidable disputes.

Step 3. Validate replay and release controls#

Prove retry safety before go-live. The same job with the same approved input set should produce one recognized batch identity or a clean no-op.

Document the idempotency control, batch identity rules, and release sign-off owner before the first live run. Launch only when duplicate payouts are prevented by design and the sign-off packet is reviewable without explanation calls. For broader model framing, see Choosing Between Subscription and Transaction Fees for Your Revenue Model.

This section pairs with Revenue Leakage from Payment Failures: How Much Are Failed Transactions Really Costing Your Platform?.

Handle common failure modes before they become partner disputes#

Most disputes are preventable if you remove ambiguity before money moves. In practice, the biggest risks are unclear split terms, incomplete revenue definitions, and unclear payment and reporting rules.

| Failure mode | Preventive action | Checkpoint |

|---|---|---|

| Ambiguous split terms | Define parties, split logic, and model scope in writing at the outset | Each stakeholder can explain how income is split without interpretation gaps |

| Missed revenue streams | List all current revenue sources and how future streams will be handled | No material revenue stream is left undefined in the agreement |

| Opaque payout operations | Set payment timing, calculation method, and reporting format before execution | Finance, ops, and partners can trace how each payout amount was calculated |

Step 1 Lock down split terms early#

Set the framework at the start, not after performance pressure builds. Clear written terms reduce dispute risk because they remove room for case-by-case interpretation.

If the model changes later, update the written terms before you apply new logic to payouts.

Step 2 Define revenue scope completely#

Conflicts often start when one side assumes a revenue stream is included and the other does not. Name all revenue sources up front, including how future streams will be treated.

If you cannot point to where a stream is defined, treat that as an open risk before go-live.

Step 3 Make payment and dispute handling explicit#

Document when payments happen, how they are calculated, and what reporting partners will receive. Then predefine how disagreements are resolved and what exit terms apply so escalation paths are clear before a dispute.

For performance-linked sharing, keep targets measurable and reviewable so payout changes tie to outcomes instead of interpretation. Related reading: How to Use Performance-Based Pricing for Your Freelance Services. You may also want How to Structure Your Platform for Investor Due Diligence: Financial Compliance and Tech Stack.

Use this checklist before you finalize your model#

Use this as your launch-readiness filter: if any item lacks a named owner, a written rule, and one report or document, pause go-live.

- Lock the payable event and revenue base. Define included revenue, exclusions, and whether expenses are allocated before sharing.

What to verify: The agreement is clear enough that two people can calculate the same result from the same record.

- Test candidate split ranges against margin guardrails before approval. Scenario-test contribution, support load, marketing cost, reversals, and delivery costs before setting percentages.

What to verify: You have best-case, base-case, and stress-case outputs with assumptions another operator can inspect.

- Write the base split as a standalone rule. Keep the base formula separate so the core share is reproducible.

What to verify: The rule names the calculation base, pre-share deductions, reporting source, and sign-off owner.

- Write tier logic as a separate rule. If tiers are used, define trigger, review timing, and measurement source in plain language.

What to verify: The terms prevent inconsistent crediting and unclear targets across teams.

- Write bonus logic as a separate rule. Treat bonuses as an add-on layer, not a blended percentage inside the split.

What to verify: Each KPI has one source of truth, one dated snapshot, and a clear adjustment approver for late data changes.

- Fix payment terms and reporting before launch. State payout schedule, method, reporting template, and how holds or corrections appear on statements.

What to verify: Terms are explicit, including any due window (for example, within 30 days after reports are submitted), and both sides read the same standardized report.

- Assign responsibilities and compliance review in writing. Name all parties, responsibilities, and owners for legal, finance, support, and payout questions.

What to verify: Dispute-resolution steps are documented, and any pending compliance treatment is verified against approved legal, tax, contract, or provider records before use.

- Run one shadow cycle and stop if exceptions are still manual. Recreate one full payout run without moving cash, then reconcile line by line to source records.

What to verify: Every payable line is traceable from source event to statement, and exception handling is documented.

If your split design depends on packaging strategy, read How to Build Plan Tiers and Add-Ons That Maximize Revenue Per Platform User. If your payout logic is tied to media-style monetization, see Podcast and Audio Platform Payouts: Ad Revenue Sharing and Per-Stream Models. If the partnership structure itself is still unclear, use How to structure a 'joint venture' agreement for a software product.

When every checklist item is green, move to execution with Gruv tools. If one or two items still depend on your country, entity setup, or partner structure, talk to Gruv.

Frequently Asked Questions

What is a platform revenue-sharing structure in practical terms?

It is the written rule set for what counts as payable revenue, who qualifies for a payout, how the split is calculated, and when cash is released. In practice, the percentage is only part of it. You also need transparent reporting and records detailed enough to explain each payout line.

How do you set split tiers without damaging gross margin?

Start with the simplest split method you can measure cleanly: fixed, tiered, or performance-based. If you add tiers, define the exact trigger, review timing, and revenue base in writing, including any deductions taken before the share is calculated. A common failure mode is ambiguous terms or overlooked revenue streams, so define triggers, metrics, and exclusions clearly.

How is revenue sharing different from a commission model operationally?

A commission model usually pays a percentage on a defined sale or service sold. Revenue sharing is broader and can include fixed splits, tiers, or performance-linked payouts, which means you need clear rules for eligibility, exclusions, and reporting. If you combine methods, clearly separate commission, shared revenue, and bonuses in reporting.

Which KPIs are safest for performance bonuses?

Use KPIs tied to measurable outcomes such as sales or growth, and pair them with transparent reporting so both sides can verify results. Keep the metric set small and clearly defined. If measurement is unclear, keep bonus terms simple until reporting is reliable.

How often should payouts run when reconciliation is still maturing?

Choose a cadence your team can execute and explain consistently. There is no universal required weekly/monthly/quarterly cadence in this context, so define payment timing and reporting clearly in the agreement. If reconciliation is still fragile, use a cadence you can reproduce consistently from the same records.

What must be included in the agreement before launch?

At minimum, list every party involved with full legal names, addresses, and contact details, then define all covered revenue streams and any exclusions. Spell out the split method, any deductions before sharing, payment timing, reporting duties, dispute handling, and exit terms. Red flags are vague wording or overlooked revenue streams.

Do you need to review the agreement after launch?

Yes. Revenue-sharing terms should be revisited periodically so the agreement still matches how the business actually earns and reports revenue. If your statements keep needing manual exceptions, revisit both contract language and operations.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- irs.gov/pub/irs-pdf/p5653.pdftrusted

- oregonlegislature.gov/bills_laws/ors/ors646a.htmltrusted

- sec.gov/Archives/edgar/data/1830043/0001193125210419...trusted

- som.yale.edu/sites/default/files/2025-05/SCOTT-MORTON_Dig...trusted

- transit.dot.gov/sites/fta.dot.gov/files/docs/ntd/56681/unifo...trusted

- web-archive-storage.oecd.org/aemint-web-archive-prod/web-archive/45/45e8f...trusted

- wordpress.nccommunitycolleges.edu/wp-content/uploads/2026/03/Ex-Libris-ILS-50-...trusted

- affnook.com/revenue-shareexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Build Plan Tiers and Add-Ons That Raise Revenue Per Platform User

Treat plans and add-ons as one packaging decision. If you split them apart, execution can get messy across billing, sales, and renewals. The goal is not just to raise prices or create more ways to buy. It is to improve revenue in a way your product, finance, ops, and revenue teams can actually support.

How to Structure a Joint Venture Agreement for a Software Product

Before you draft terms for a **joint venture for software product**, make a clear go or no-go call on the people, rights, and authority involved. If either side cannot prove who can sign, what code they can legally contribute, or how deadlocks get resolved, pause and fix that first.

Podcast Platform Payouts and the Net Economics Behind Ad Revenue and Streams

Teams can overestimate podcast payouts when they compare bundled products as if they were one decision. They are not. Hosting, distribution, ad access, and payment handling may sit inside the same product, but you should still treat them as separate layers until the payout mechanics are clear.