Quick Answer

Start with settled purchase transactions and calculate retained earnings, not headline interchange. Split activity into debit and credit, then break debit into business and consumer where your data supports it, plus CNP versus card-present. Trace the payment path from merchant acquirer to issuing bank, apply only contract-backed deductions and period adjustments, and reconcile one closed month to ledger records before using the model for pricing or launch decisions.

How to Estimate Platform Interchange Revenue#

The number that matters is net interchange revenue, not the headline interchange fee. If you only track gross interchange, a platform card program can look like it is scaling while the earnings you actually keep are getting thinner.

This guide is built for that problem. It shows you how to move from transaction activity to retained economics so you can make better calls on pricing, card design, and growth targets. That matters if you sit in product, finance, or revenue and need to decide whether your card program is a margin driver, a rewards subsidy, or both.

Start with the money you actually keep#

Interchange fees are incurred on debit and credit transactions and are set by the card network. In simple terms, interchange moves from the merchant side to the issuing side. The acquiring bank pays it to the issuing bank when a cardholder makes a purchase. Your platform does not automatically keep all of that revenue, which can create modeling errors early on.

One practical rule is to keep interchange income, gross interchange revenue, and retained platform earnings as separate line items. They are not interchangeable in a forecast or a board deck. If your growth model assumes every extra dollar of gross interchange drops through as margin, you can underprice the product, overfund rewards, or approve acquisition spend that does not pay back as expected.

Use this guide for decisions, not averages#

You will see plenty of generic interchange ranges in the market. Those can help with orientation, but they are not enough to price a real program. Rates vary by factors including card type, sponsor-bank size, and merchant category, and your retained economics also depend on how your program is set up.

That is the operating tension behind this article. Spend volume can rise while margin falls if the mix shifts, rewards get richer, or your share of the economics is smaller than the headline suggests. The right question is not "what is the interchange rate?" It is "after the issuing side is paid and program economics are applied, what do we keep?"

Set the caveats before you model#

Assume from the start that outcomes vary by card network and program setup. The same transaction volume can produce different results across a debit versus credit mix, across merchant categories, or across two programs with different issuing-bank and program agreements.

One checkpoint is worth adopting early. Before you forecast forward, reconcile a recent reporting period using actual transaction records and the interchange income your finance team sees in statements or ledger outputs. If those do not tie closely enough to explain the gross-to-net story, stop there and fix the data before making pricing or launch decisions. That check helps you avoid building a polished model on the wrong base.

What to Gather Before You Calculate Anything#

Before you forecast, build a minimum data pack and confirm what your platform actually retains.

| Input or check | What to include | Note |

|---|---|---|

| Recent transaction file | Transaction count and purchase volume, split by debit and credit; where available, Business debit card and Consumer debit card | Interchange revenue comes from debit and credit purchase activity, so those splits should be in the first working file |

| Context fields | Merchant category, geography, and Card-not-present (CNP) vs card-present at the transaction level or segment rollup level | A single blended spend total can hide meaningful mix changes |

| Signed agreements and terms | Current signed agreements and fee/revenue-share terms | Model what the issuing bank, sponsor/program partners, and your platform actually receive |

| Reconciliation checkpoint | Use a recent closed period and tie reported interchange income to ledger-level transaction records | If the difference is not explainable with evidence, fix the data baseline before you trust any forward model |

- Pull one recent transaction file with core splits.

Start with transaction count and purchase volume, then split by debit and credit. Where available, split debit into Business debit card and Consumer debit card. Interchange revenue comes from debit and credit purchase activity, so those splits should be in your first working file, not added later.

- Add context fields that affect mix visibility.

Include Merchant category, geography, and Card-not-present (CNP) vs card-present at the transaction level or segment rollup level. A single blended spend total can hide meaningful mix changes.

- Confirm contract reality before modeling retained earnings.

Interchange fees are set by the card network, and the payment flow involves the acquiring bank and issuing bank. Pull the current signed agreements and fee/revenue-share terms so you are modeling what the issuing bank, sponsor/program partners, and your platform actually receive.

- Run one reconciliation checkpoint before projecting forward.

Use a recent closed period and tie reported interchange income to ledger-level transaction records. If the difference is not explainable with evidence, fix the data baseline before you trust any forward model.

Map the Money Flow From Swipe to Platform Earnings#

Model retained earnings from the actual fund flow, not from a Visa or Mastercard headline. Interchange is remitted to the issuer, and your platform keeps only the share defined in its program agreements.

Step 1: Trace the transaction in order. A cardholder makes a purchase. The merchant acquirer (the merchant's bank) handles the merchant-side funds flow, and the card network provides the rail between acquirer and issuer. Interchange is part of the merchant discount rate and is remitted to the issuer, not directly to your platform.

Step 2: Separate network structure from platform economics. Visa and Mastercard run card systems and set network structures, but that does not define your retained economics. Your retained share is determined by your signed program documents, including fee schedules, revenue-sharing terms, and any amendments.

Step 3: Flag where monthly earnings can look wrong. Refunds, reversals, disputed transactions, and delayed postings can distort a monthly view when finance books only top-line inflows. Reconcile one closed period by tying recorded inflows back to transaction records and the agreement that governs your share. If offsets or timing cannot be explained, treat the period as unreconciled before forecasting.

Build the Calculation From Gross Interchange to Net Interchange#

Build this as a gross-to-net bridge by segment, then roll it up. Keep branded debit and branded credit separate until the end so you can see what actually moved.

Step 1. Estimate gross interchange revenue by segment. Interchange is generated when customers make purchases with debit and credit cards, and businesses pay an interchange fee after each transaction. Model each cohort separately: Gross interchange revenue(segment) = settled purchase volume(segment) × assumed interchange yield(segment).

Start with branded debit and branded credit. If you operate across countries, split those cohorts by country before applying a yield, since interchange can vary across countries.

Step 2. Subtract contract-defined direct costs to reach segment net. For each segment, subtract only pass-through amounts and program costs defined in your signed agreement, fee schedule, and amendments for that period. Treat this as a gross-profit style bridge: revenue minus direct costs, before overhead and indirect spend.

Use: Net interchange revenue(segment) = gross interchange revenue(segment) - contracted deductions(segment) ± period adjustments(segment). If a deduction is not contract-backed for that period, do not include it in retained interchange.

Step 3. Build a monthly bridge with owners. Keep one view that finance and product can both audit quickly.

| Bridge line | What belongs here | Owner |

|---|---|---|

| Gross interchange revenue | Sum of segment gross for branded debit and branded credit | Finance |

| Contracted deductions | Pass-through amounts and program costs defined in agreements | Finance and payments ops |

| Period adjustments | Month-specific adjustments needed to reconcile period results | Finance and risk or ops |

| Net interchange revenue | Ending retained interchange after deductions and adjustments | Finance |

Step 4. Verify before using for pricing or planning. At close, tie total gross and net to the same month's transaction records and ledger, then compare segment actuals against forecast. Keep an assumption log for major inputs (owner, source, update date, rationale) so changes are reviewable.

If legal or regulatory references inform your assumptions, confirm you are using official editions before you rely on Federal Register prototype/XML pages as final legal authority.

Segment Transactions So Your Forecast Is Not Fiction#

If your segments do not match how interchange economics are set, your forecast will look clean and still miss the real drivers. Start by separating credit vs debit, then business debit vs consumer debit where your data supports it, and then card-not-present (CNP) vs card-present inside each card type.

Build segments on economics, not reporting convenience. Card networks set interchange fees that compensate issuers, and credit interchange fees make up much of merchant interchange fee spend, so blending everything into one bucket hides mix risk. A segment is only useful if you can trace it from settled transactions to the closed-month bridge and explain why changes in that mix affect retained economics.

Add merchant category as a second-layer split only where behavior is materially different. Do not split every merchant category by default. Isolate categories that clearly drive different transaction patterns, refund behavior, or channel mix. Keep the rest rolled up until added detail improves forecast accuracy.

Use a simple cohort check before you expand model complexity:

| Cohort | Volume share | Yield sensitivity | Volatility risk | Confidence level of assumptions |

|---|---|---|---|---|

| Business debit card | Measure from last closed-month settled volume | Score from your own history and mix movement | Score from month-to-month variance | High only if business/consumer tagging is consistent in settled data |

| Consumer debit card | Measure from last closed-month settled volume | Score from your own history and mix movement | Score from month-to-month variance | High only if debit classification reconciles to ledger |

| Credit card | Measure from last closed-month settled volume | Score from your own history and mix movement | Score from month-to-month variance | High only if contract-backed deductions are mapped by cohort |

| CNP transactions | Measure as share within debit and credit | Score from your own history and mix movement | Score from month-to-month variance | Medium unless settlement-level channel flags are complete |

| Card-present transactions | Measure as share within debit and credit | Score from your own history and mix movement | Score from month-to-month variance | Medium to high if channel source data is stable |

Decision rule: if one segment explains most of forecast variance, improve instrumentation there before adding more cohorts elsewhere. In practice, that usually means fixing field quality and weekly mix visibility on the biggest moving segment first.

Keep debit isolated so later routing or policy assumptions can be applied cleanly instead of being smeared across the portfolio.

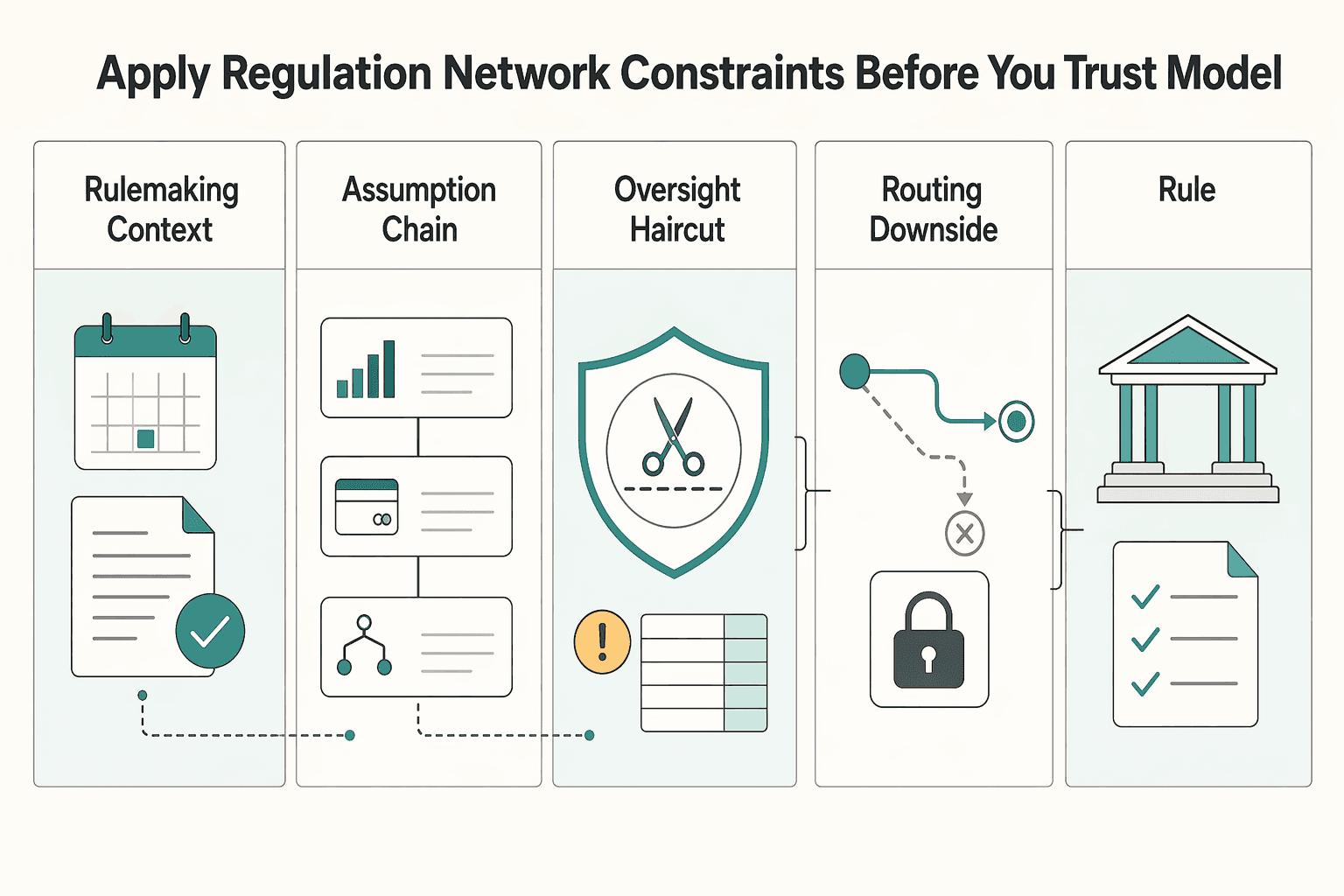

Apply Regulation and Network Constraints Before You Trust the Model#

Debit assumptions are not durable by default, so put regulation and routing downside into the model before you trust retained margin.

| Constraint | What to document or test | Model response |

|---|---|---|

| Rulemaking context | Monitor Regulation II; a May 10, 2024 stakeholder comment responded to proposed Federal Reserve amendments under Docket No. R-1818; RIN: 7100-AG67 | Use scenario-based assumptions instead of a single-point forecast |

| Assumption chain | Keep written support for the assumption chain: issuer or program agreement, pricing schedule, and whether economics depend on Durbin-exempt treatment or a specific routing outcome | If that chain is not documented, classify the cohort as higher risk and use a lower assumption |

| Oversight haircut | Apply an oversight haircut instead of assuming yield stability | Use stakeholder claims as stress-test inputs, not forecast facts |

| Routing downside | Model routing as a downside case and confirm settled transactions can be segmented by debit network and by card-present versus card-not-present where available | If you cannot isolate exposure, your downside case is too generic to rely on |

| Go/no-go rule | Pause launch if economics only hold under unchanged debit assumptions and best-case routing | Rework pricing, reduce dependence on weaker debit cohorts, or rebalance card mix before scaling |

Step 1. Map each debit assumption to a specific policy exposure. Treat the Durbin Amendment and broader Dodd-Frank-era debit constraints as active model inputs, not history notes. In current rulemaking context, monitor Regulation II: a May 10, 2024 stakeholder comment responded to proposed Federal Reserve amendments under Docket No. R-1818; RIN: 7100-AG67. That is enough to justify scenario-based assumptions instead of a single-point forecast.

For each debit cohort, keep written support for the assumption chain: issuer or program agreement, pricing schedule, and whether economics depend on Durbin-exempt treatment or a specific routing outcome. If that chain is not documented, classify the cohort as higher risk and use a lower assumption.

Step 2. Apply an oversight haircut instead of assuming yield stability. Federal oversight has been persistent, including a Senate hearing record on June 16, 2010 and a dedicated "Payment System and Reserve Bank Oversight" section in the Federal Reserve's 2022 annual report. That context does not predict a final rule outcome, but it does argue against treating current debit yield as fixed.

Use stakeholder claims as stress-test inputs, not forecast facts. In the May 10, 2024 letter, the commenter said the Durbin exemption for smaller institutions has been "largely illusory" and cited Board data indicating nearly a 31 percent inflation-adjusted decline for exempt single-message interchange fees.

Step 3. Put routing downside in the retained-margin math before launch. Model routing as a downside case, not a footnote. If your forecast only works when routing stays best-case, the model is fragile.

Operationally, confirm settled transactions can be segmented by debit network and by card-present versus card-not-present where available. If you cannot isolate exposure, your downside case is too generic to rely on.

Step 4. Use a clear go/no-go rule. If economics only hold under unchanged debit assumptions and best-case routing, pause launch. Rework pricing, reduce dependence on weaker debit cohorts, or rebalance card mix before scaling.

Compare Monetization Choices With Clear If Then Rules#

Choose the model that is least fragile for your current mix, not the one with the highest headline yield.

| If this is true | Then prioritize | Why this is usually safer for margin stability |

|---|---|---|

| Your transaction mix is heavily Card-not-present (CNP) and volatile | Fee-led or hybrid, with conservative assumptions and a stronger downside buffer | You reduce dependence on interchange outcomes that can move against you |

| Business debit card share is growing and retention is stable | Interchange-led optimization before adding user-facing fees | You can improve net economics through card strategy and rewards discipline before increasing price friction |

| Your mix is still changing quarter to quarter | Hybrid | You keep interchange upside while adding protection if card economics soften |

Use two-sided market logic when making the call. Card economics link merchant-side fees and consumer-side rewards, and consumer adoption can be more price-sensitive than merchant acceptance, so adding user-facing fees too early can hurt uptake.

Before approving growth targets, run one check: do card type choices, rewards posture, and onboarding decisions improve Net interchange revenue, not just top-line volume?

For a deeper breakdown of how interchange affects your pricing, read How Interchange Fees Change the Price You Need to Charge.

Common Forecast Mistakes and How to Recover Fast#

Forecast misses usually come from four controllable errors: blended assumptions, gross-versus-net confusion, untracked mix shifts, and stale regulatory inputs.

| Forecast issue | Recovery action | Check |

|---|---|---|

| Blended network assumptions | Split Visa and Mastercard before you forecast, then rebuild by network and by debit versus credit, business versus consumer, and CNP versus card-present | For a recent settled month, tie each segment's reported interchange income to transaction-level records and the correct network bucket |

| Gross-versus-net confusion | Force a gross-to-net bridge every month | Show deductions such as reversals, disputes, rewards, partner shares, and other contract-level pass-throughs |

| Untracked mix shifts | Monitor merchant category and CNP mix weekly | Set threshold-based reforecast triggers for meaningful CNP-share changes or sharp category shifts |

| Stale regulatory inputs | Treat regulation as a live assumption, not a constant | Keep a dated quarterly assumption review for Durbin and routing-related inputs, assign owners, and run a downside case before approving the next forecast cycle |

Step 1. Split Visa and Mastercard before you forecast. Do not use one blended rate across both networks. Rebuild by network, then by the segments that move economics: debit versus credit, business versus consumer, and CNP versus card-present. Recovery check: for a recent settled month, tie each segment's reported interchange income to transaction-level records and the correct network bucket.

Step 2. Force a gross-to-net bridge every month. Gross interchange is not retained earnings. Interchange fee is a transfer paid by the acquiring bank to the issuing bank, and the transaction fee stack can also include assessment fees and processor markup. Recovery path: in every monthly review, bridge from gross to net by showing deductions such as reversals, disputes, rewards, partner shares, and other contract-level pass-throughs.

Step 3. Monitor merchant category and CNP mix weekly. Mix shifts can break a forecast faster than monthly reporting can catch them. Set threshold-based reforecast triggers for meaningful CNP-share changes or sharp category shifts, then prioritize instrumentation on the cohort driving most variance.

Step 4. Treat regulation as a live assumption, not a constant. Do not treat regulatory context as fixed once the model is built. Keep a dated quarterly assumption review for Durbin and routing-related inputs, assign owners, and run a downside case before approving the next forecast cycle.

Final Decision Checklist for Finance and Product Teams#

Your final decision is trustworthy only when finance, product, and partner teams are approving the same assumptions, responsibilities, and criteria.

- Lock decision parameters before partner conversations.

Define clear approval parameters tied to your company goals, and keep them in one artifact your approvers will actually read.

- Complete a self-assessment before demos and technical calls.

Confirm your team's involvement and responsibilities up front so partner discussions stay aligned and comparable.

- Make the provider responsibility split explicit.

State whether you need a full package or a-la-carte services, and document which responsibilities sit with your team versus the provider. Similar outcomes are possible across models, but path, cost, and time can differ materially.

- Assign named owners for assumptions and updates.

Avoid shared accountability by naming who owns each core assumption and who updates it when partner scope or operating conditions change.

- Set go/no-go criteria in writing before the decision meeting.

Record approval criteria and exception rules in advance so decisions are based on documented standards, not live debate.

A practical way to keep this disciplined is to place the checklist inside your formal evaluation section, for example an evaluation overview, so evidence, ownership, and criteria stay in one place.

Frequently Asked Questions

How do I calculate platform interchange revenue from card transactions in a way finance can trust?

Start from settled debit and credit purchase transactions that actually generate interchange. In the basic card flow, interchange is paid from the acquirer to the issuer, and it is the portion of MDR remitted to the issuer. Keep those definitions consistent in your model so finance can reconcile results.

What percentage should we assume for interchange revenue if our card mix is still changing?

Do not force a single benchmark percentage into the model. Use scenario ranges with a base case and downside case, and refresh them as your transaction mix becomes clearer.

Which input usually changes results the most: card type, merchant category, or transaction channel?

The provided excerpts do not rank card type, merchant category, and transaction channel by impact. Treat this as an empirical question: test each driver in your own data and keep the one that explains the variance.

How should we model Business debit card versus Consumer debit card without overfitting?

The provided excerpts do not define a required method for Business debit versus Consumer debit modeling. If you split them, keep cohorts separate only when observed interchange outcomes show the split improves forecast accuracy.

Why can interchange revenue miss forecast even when payment volume is growing?

Payment volume growth alone does not determine interchange forecast accuracy. Interchange is tied to debit and credit purchases and follows the acquirer-to-issuer flow as part of MDR, so misses often come from modeling assumptions that do not match recorded outcomes.

When should we optimize interchange economics versus change pricing or product design?

Make this decision only after your model reflects the supported mechanics: interchange is part of MDR and is remitted to the issuer. Use your own performance data for that call.

How do regulation and routing constraints change what we can realistically keep?

Treat regulation and routing as scenario constraints, not certainties. Card networks set interchange fees, but the provided excerpts do not include specific regulatory or routing thresholds, so avoid assuming favorable conditions in your base case.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/work1295.pdftrusted

- cms.gov/regulations-and-guidance/guidance/transmitta...trusted

- economics.princeton.edu/wp-content/uploads/2023/01/Wang_jmp.pdftrusted

- federalregister.gov/documents/2011/07/20/2011-16861/debit-card-i...trusted

- federalreserve.gov/publications/2022-ar-payment-system-and-rese...trusted

- federalreserve.gov/SECRS/2024/July/20240719/R-1818/R-1818-A_051...trusted

- files.consumerfinance.gov/f/documents/cfpb_wang-regulating-competing-p...trusted

- govinfo.gov/content/pkg/CHRG-111shrg57097/html/CHRG-111s...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Calculate NRR for a Subscription Platform Without Reconciliation Gaps

The formula is the easy part. In practice, the hard part is producing a single Net Revenue Retention number that finance, ops, and product can all trace to the same recurring revenue base and the same set of in-period movements.

Revenue Leakage from Payment Failures: How Much Are Failed Transactions Really Costing Your Platform?

Payment failures can be recoverable and still drain platform margin. Teams can track yesterday's declines and still miss the full cost when failures combine with under-billing, delayed recovery, reconciliation drag, and payout timing. The practical goal is simple: quantify the real cost, then map each failure point to a weekly checkpoint finance, ops, and product can actually run.

Prepaid Cards as a Payout Method: When They Work for Platforms and When They Don't

Prepaid cards are a real payout option, but they are not a shortcut to sound payout design. If you run payouts for a marketplace platform or embedded payments product, the question is not just whether a rail moves money fast. It is whether the rail fits your use case and operating model.