Quick Answer

Use prepaid cards when recipient access and immediate usability matter more than batch predictability. For the query "prepaid cards payout method platforms when to use," the article’s rule is clear: choose card rails for underbanked or urgency-driven segments, and use ACH or direct deposit when recipients are mostly banked and scheduled payout cadence is the priority. Do not launch any rail until failed-status handling, retry behavior, and payout-batch reconciliation are explicitly defined across product, ops, finance, and engineering.

When Prepaid Cards Make Sense for Platform Payouts#

Prepaid cards are a real payout option, but they are not a shortcut to sound payout design. If you run payouts for a marketplace platform or embedded payments product, the question is not just whether a rail moves money fast. It is whether the rail fits your use case and operating model.

-

Speed is a weak decision rule. In practice, platform payouts usually go to one of two places: a payee's bank account or a debit or prepaid payment card. That makes card payouts a real option, not a niche edge case, but speed alone still tells you very little. A speed-only decision can miss critical design needs around failed payouts, compliance, and reconciliation. The first checkpoint is simple: if your team cannot describe what happens after a failed payout, you are not ready to launch that rail.

-

The real decision is use case fit. A prepaid card is a stored-value payment tool funded in advance, and a card payout sends funds to a recipient's debit or prepaid card instead of a bank account. Some embedded-payment implementations combine prepaid cards with other rails, like ACH, Real-Time Payments, or push-to-card, so customers can choose the best tool for the job. The tradeoff is that prepaid programs do not behave the same way. Coverage, limits, fees, and operational constraints can vary by program, so you should verify actual program terms before product or support teams promise an experience you cannot deliver consistently.

-

This guide is about rail architecture, not consumer card advice. Consumer guidance on prepaid cards usually focuses on choosing the right card. That is useful for individuals, but it is a different problem from deciding how your platform should move funds. Here, the comparison is across rails such as prepaid cards, ACH/direct deposit, and card-based payouts. One concrete anchor matters: Nacha governs the ACH Network, the payment system that drives Direct Deposits and Direct Payments. That is the level of operator detail that matters when you compare recipient access, failure handling, compliance load, and reconciliation quality.

This guide separates four decisions that often get bundled together. First, whether prepaid cards belong in your rail mix at all. Second, when card or bank rails are the better choice. Third, what engineering and finance need to validate before launch. Fourth, which failure modes need a fallback path from day one. Some platforms should start with prepaid cards. Others should treat them as a secondary option beside ACH or direct deposit. The right answer depends on your recipient base, your urgency promise, and how much operational ambiguity your team can absorb.

For the full breakdown, read Accounting Automation for Platforms That Removes Manual Journals and Speeds Close.

If you just need a quick next step, try the free invoice generator.

Start with selection criteria and who this is for#

Use this section if you own payout outcomes across product, finance, ops, or engineering for contractor, creator, or gig economy flows. Skip it if you need consumer cardholder guidance.

- Confirm owner and scope

This is about payout rail design, not budgeting tips. Rail choice changes support burden, compliance handling (KYC/AML), and how reliably payout batches reconcile.

- Rank rails on five criteria before launch

Compare prepaid cards, ACH, direct deposit, and other card-based options on recipient access, payout speed, failure handling, compliance load, and reconciliation quality. Before launch, verify what your provider returns on failed payouts and whether finance can map that status back to a payout batch, not only a single transaction.

- Pick the first test rail from recipient profile

If your recipients skew underbanked and fast access is part of your promise, test prepaid cards or push-to-card first. FDIC reports that in 2023, 4.2% of U.S. households were unbanked and 14.2% were underbanked. If recipients are mostly banked and operational predictability matters more, benchmark ACH and direct deposit first; Nacha states ACH can reach all U.S. bank and credit union accounts.

Compare payout options before picking prepaid cards#

Choose a payout rail only after you compare how it behaves in failure, returns, and reconciliation, not just how fast it looks in a demo.

| Rail | Best for | Major pros | Major cons | Concrete use case | Return or failure visibility | Webhook or event support | Reconciliation effort | Failed payout batch handling |

|---|---|---|---|---|---|---|---|---|

| Prepaid cards | Program-based payouts when card access is important | Fast recipient access and a controlled program experience | Program constraints and card-support overhead can increase ops load | Program-linked disbursements where recipients rely on card access | Varies by issuer and provider, so confirm failed, returned, and reversed states up front | Provider-specific, not universal | Usually needs tie-out across loads, reversals, and fees | Define separate paths for unclaimed funds, failed loads, and reissues |

| Push-to-card payments | Faster disbursements to eligible cards | Uses Original Credit Transaction (OCT) to push funds to eligible card accounts; one implementation targets arrival within 30 minutes | Coverage depends on network and card eligibility | Earned wage access or insurance claims | Can be strong when lifecycle states are explicit (for example: processing, posted, failed, returned, canceled) | Available in some implementations through status webhooks | Easier when transfer IDs and state changes are returned consistently | Route failed cards to retry and fallback rails such as ACH or direct deposit |

| ACH | Routine domestic payouts to banked recipients | Broad bank reach and familiar finance operations | Batch-based, not instant; returns can appear after submission | Weekly contractor settlement | Often file- and report-driven; one production payout system reports returns typically within 2-3 business days | Varies by provider | Best when files, return entries, and ledger postings map cleanly | Requeue returns, suppress duplicates, and route return-reason handling to ops |

| Wire transfer | High-value or time-sensitive bank payouts, including some cross-border flows | Fedwire funds transfer is immediate, final, and irrevocable once processed | Errors are expensive and exception handling is often manual | Cross-border payouts | Visibility is often tied to bank confirmations rather than rich return codes | Usually bank-specific and limited | Investigation records matter as much as ledger tie-out | Escalate exceptions before release; post-send recovery is limited |

| Checks | Paper fallback and low-enrollment recipient segments | Still a valid rail; most checks are collected and settled within one business day after deposit | Printing, mailing, stale checks, address errors, and stop-pay operations add friction | Insurance claims | States are fragmented (mailed, delivered, deposited, stale, uncashed) | Usually none unless layered by a vendor | Typically high manual effort across issue, positive pay, stop-pay, and escheat | Failed batches become reissue, address-fix, and stop-pay queues |

| Direct deposit | Recurring payroll-like payouts to known bank accounts | Common ACH credit use case with familiar recipient experience | Requires bank data and inherits ACH timing/return behavior | Scheduled workforce payouts | Similar to ACH, often cleaner with standardized payee setup | Varies by provider | Strong when setup data, payroll export, and bank file stay aligned | Failed items usually route to account-update, ACH retry, and support paths |

The operator columns are usually where rail choices succeed or fail. Before you approve a rail, confirm the exact status vocabulary and source of truth across API responses, webhooks, portal timelines, bank reports, and batch exports.

The core rail mechanics are different enough to matter in design. ACH is batch-based, and direct deposit is a common ACH credit pattern. Push-to-card is typically an OCT with eligibility constraints. Fedwire is immediate, final, and irrevocable once processed, so pre-send controls matter more than retry logic.

Before broad rollout, use a one-page post-failure playbook for each shortlisted rail: status names, source of truth, expected return timing, retry owner, fallback rail, and ledger treatment for failed versus returned payouts. If that flow is still unclear across product, ops, finance, and engineering, keep the rail in pilot.

Related: Real-Time Payment Use Cases for Gig Platforms: When Instant Actually Matters.

Prepaid cards as a payout method when they work best#

Prepaid cards work best when a bank-account-only payout design would block access and fast, usable funds are part of the product promise.

- Bank account capture is the blocker

Prepaid cards can be used for spending and bill payment without accessing a bank account or line of credit. That matters because a meaningful segment still needs non-bank payout options: the FDIC reports that 4.2% of U.S. households (5.6 million) lacked a bank or credit union account, and 33.8% of unbanked households relied on a combination of prepaid cards or nonbank online payment services. In practice, this means you can pay recipients who would otherwise stall in a bank-account-only flow.

- Waiting for funds breaks the experience

Cards are a strong fit for contractor, creator, and short-term workforce payouts on marketplace platforms when recipients need funds they can use quickly. Card-based disbursement is often positioned as faster than traditional direct deposit, and one payout-to-card implementation says funds typically become available within 30 minutes. In high-frequency payout patterns, immediate spend access can be a real product advantage.

- You can validate program constraints before launch

Prepaid performance depends on program details, not just headline speed. Coverage can vary by supported location, currency, and setup, and processing time can vary by issuer. Cards work when your team verifies the operating constraints up front.

Before go-live, require three artifacts: a supported locations/currencies matrix, the exact fee schedule, and the cardholder disclosure. Prepaid cards can include fees for holding or using the card, and covered prepaid accounts must provide clear, upfront fee information, so get those documents early.

The cleanest use case is high-frequency creator or task payouts where fast access matters and bank capture is weak. If you choose cards, keep a fallback rail for recipients who fail eligibility or sit outside the supported program footprint.

If you want a deeper dive, read Gift Card Payouts for Platforms: When to Use Gift Cards vs. Cash and How to Manage Redemption.

Push to card rails when instant card funding is the priority#

If instant, card-usable funds are your core promise, use push-to-card rails and validate eligibility before launch. Push to Card is a 24/7 disbursement method to eligible debit or reloadable prepaid Visa or Mastercard cards, and on Visa this is commonly sent as an Original Credit Transaction (OCT).

For urgency-driven payouts, the recipient experience is the advantage: funds are typically available in about 30 seconds, with a documented network maximum of 30 minutes. That is why the rail is a strong fit for cases like insurance claims and selected wage-related disbursements.

Coverage is the real go/no-go check. Availability can differ by region, client profile, receiving institution, and program requirements, and supported endpoints can vary by setup. Confirm your provider's market matrix, endpoint eligibility, limits, and failure scenarios in writing before you promise instant funding. Published limits can be up to $125,000 per transaction, while some money-transfer use cases may be capped at $50,000 per transaction.

If your priority is minutes-level access, push to card where eligibility is confirmed. If broader fallback coverage matters more, launch with card push plus ACH or wire transfer.

This pairs well with our guide on When Platforms Are Responsible for Contractor Tax Fraud or Money Laundering.

Bank rails when predictability and broad acceptance matter more#

If instant card usability is not the core promise, bank rails are usually the better default for routine payouts because they support scheduled operations and familiar finance controls. Start with ACH/direct deposit for planned runs, and use wires for time-critical exceptions.

- ACH for planned domestic payout batches

ACH is built for batches of electronic credits and debits between depository institutions, so it fits scheduled payout runs where payee, amount, and due date are known in advance. It is explicitly used for large volumes of scheduled, recurring payments between known counterparties on known due dates.

The main operational advantage is reach plus predictable cadence: the ACH Network reaches all U.S. bank and credit union accounts, and 93% of American workers are paid through ACH. For non-urgent contractor or marketplace settlements, this is typically the first rail to benchmark.

- Direct deposit when familiarity matters more than speed

Direct deposit is an ACH credit, and recipients generally recognize it as a standard bank payout experience. That makes it a practical fit for low-urgency disbursements where consistency matters more than immediate card funding.

The tradeoff is timing: ACH is not a 24/7 instant rail. It processes 23 1/4 hours every banking day, settles four times every banking day, and does not currently settle on weekends or federal holidays. Your product messaging and payout-status expectations should match that banking-day behavior.

- Wire transfer for high-value, time-critical exceptions

Wire is the bank rail for cases where immediate finality matters once processed. The Fedwire Funds Service is real-time gross settlement, and transfers are immediate, final, and irrevocable once processed; the Federal Reserve describes it as generally used for large-value, time-critical payments.

Use wire as an exception path, not your default scheduled payout rail. Fedwire operates Monday through Friday within its published window (9:00 p.m. ET to 7:00 p.m. ET). If your next decision is cross-border wire design, read International Wire Transfer for Platforms: When to Use Wires vs. Local Rails for Cross-Border Payouts.

Before launch, confirm three items in writing: payout interval settings, cutoff/holiday behavior, and how transfer events flow back into your ledger or ops queue. Providers support scheduled payout logic (including daily intervals and sweeps), and some emit webhooks when sweep-driven transfer requests are created. Bank rails are often the right answer for low-urgency payouts, but only if your product copy, cash planning, and status reporting match real processing windows.

Cross border design choices that reduce payout failures#

For cross-border payouts, design by corridor and failure recovery first, then pick rails. Treat wire transfer, prepaid cards, and Virtual Accounts as different operating models with different recipient eligibility, return handling, and investigation burden, not interchangeable options.

| Option | Where it fits | What to validate before launch |

|---|---|---|

wire transfer | Urgent cross-border exceptions | Beneficiary instruction quality must be exact; missing required information can cause delays or returns, and recovery options narrow quickly once sent. |

prepaid cards | Programs where recipients are eligible for supported card payout options | Coverage and recipient fit can vary by location, currency, program rules, limits, and fees, so confirm corridor-level eligibility and fallback paths in writing. |

Virtual Accounts | Reconciliation and control across cross-border flows | Use as a cash-concentration and reporting layer for daily reconciliation; pair with payout endpoints (including prepaid-card programs) based on corridor and recipient constraints. |

Use this order of operations: define target corridor, set compliance gates (KYC, KYB, AML), test payout and return-message flows, then scale through monitored payout batches.

Before scaling, run a failure-mode checklist: unmatched deposits, held or returned statuses, stale routing data, and delayed status propagation into ops dashboards.

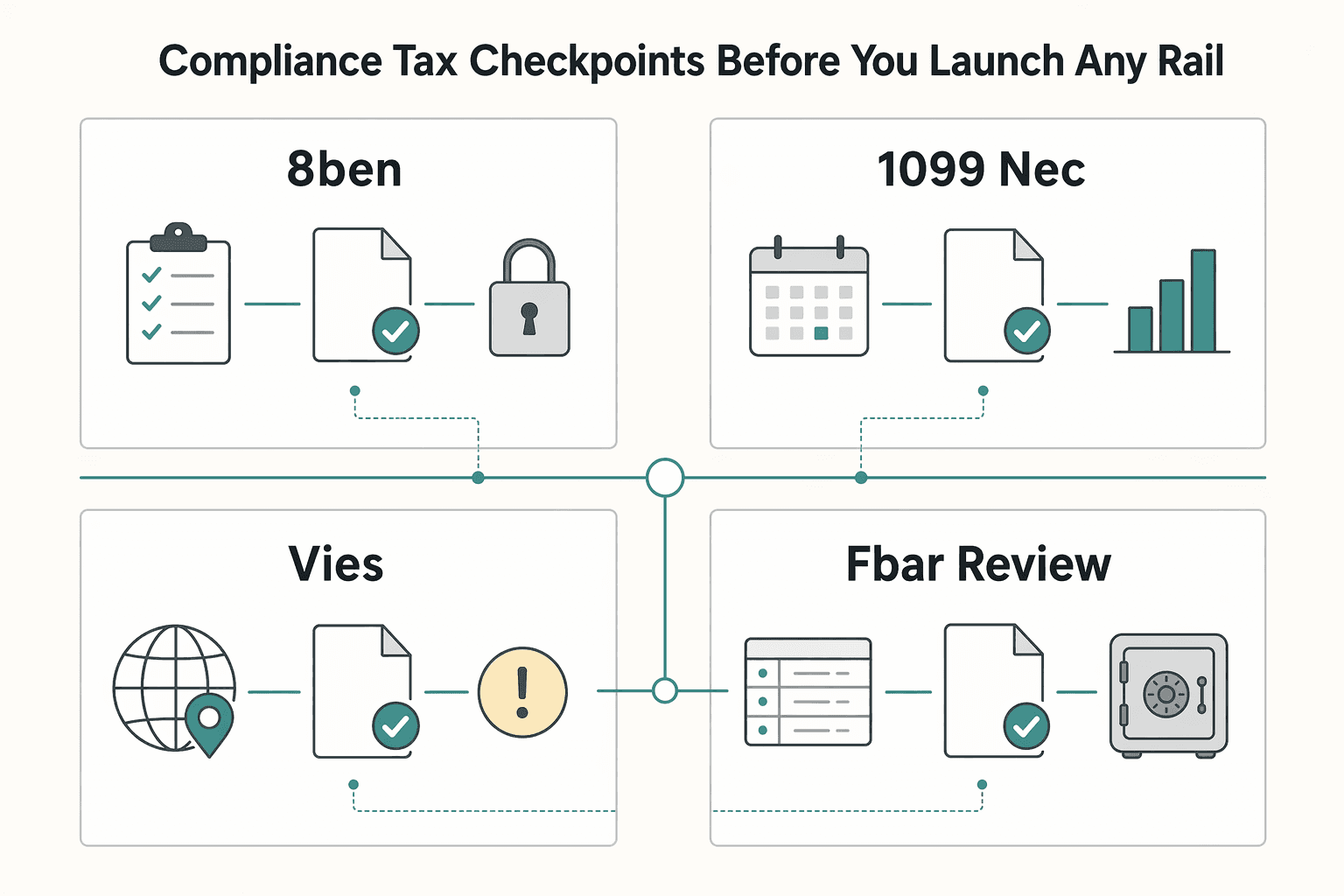

Compliance and tax checkpoints before you launch any rail#

Set these controls before go-live: your team should be able to prove why a payout was allowed, which documents supported it, and what a retry does.

| Item | Use when | Detail |

|---|---|---|

| W-9 | Payer information-return contexts | Use by recipient type rather than one form path for all payees |

| W-8BEN | Foreign persons when requested by the payer or withholding agent | Route tax documents by recipient type |

| 1099-NEC review | Eligible nonemployee compensation | Add an explicit review step |

| VIES | EU VAT checks | Store the validation result used at decision time |

| FBAR review | Aggregate foreign-account value exceeds $10,000 at any point in the year | Track cases that may require review |

- Build a pre-launch evidence pack

Tie policy gates, approvals, and reconciliation to payout batches. Keep payout-eligibility rules, required audit-trail states, and reconciliation exports finance can use to match and compare transaction records. A practical check is whether one batch ID is traceable from recipient approval through payout outcome without manual stitching.

- Route tax and documentation by recipient type

Do not use one form path for all payees. Use W-9 for payer information-return contexts and W-8BEN for foreign persons when requested by the payer or withholding agent. Add an explicit 1099-NEC review step for eligible nonemployee compensation. For EU VAT checks, validate numbers through VIES and store the validation result used at decision time. For foreign-account monitoring, track cases that may require FBAR review when aggregate foreign-account value exceeds $10,000 at any point in the year.

- Define AML/KYB holds and make retries idempotent

Document what triggers an AML hold, who can approve exceptions, and what evidence is required to release funds, with controls designed to detect and report suspicious activity. Include CIP-style identity verification and beneficial-owner identification for legal entities at account opening. Make payout retries idempotent so repeated requests with the same key return the same result, and log that key against the payout and batch record.

For a step-by-step walkthrough, see When Platforms File 1099-K and 1099-NEC.

Conclusion#

-

Choose the rail that fits the payout promise. Prepaid cards can earn their place when access and timing are real product requirements. That does not make them the default winner. Even strong instant-funding claims are conditional: Visa Direct says funds to U.S. bank accounts linked to eligible debit cards can be available within 1 minute or less starting in April 2025. The real decision is eligibility and operational clarity, not the fastest headline.

-

Keep bank-rail fallbacks ready from day one. ACH is still valuable because it is a batch, store-and-forward process, which makes it a different tool from prepaid cards or push-to-card options. If your finance team needs predictable scheduled runs, ACH may still carry most of the volume. Use card-based options where urgency matters, but do not force every recipient segment or market into one method if coverage, limits, or return handling are still uncertain.

-

Do not ship until failure handling is boring and traceable. The winning decision is not "fastest rail wins." It is the rail mix you can operate with clear exception paths, compliance gates, and reconciliation discipline. In practice, you should be able to trace one payout from approval to settlement or return without spreadsheet stitching, and you should know what happens on a retry, hold, or duplicate request before you scale.

-

Treat launch like a certification event, not a feature toggle. That approach matches documented instant-payment readiness models. The Federal Reserve said early adopters of FedNow would complete a customer testing and certification program, with formal certification beginning in the first week of April before launch, and onboarding guidance requires participants to certify and attest to operational readiness before production. Your pilot should follow the same discipline even if your rail is not FedNow. Named owners, approval gates, and readiness attestations reduce avoidable go-live risk.

-

Run a controlled pilot with explicit stop rules. Set success metrics that match your business, not generic benchmarks, because there is no universal threshold that fits every platform. Include at least three operator checks in the owner-approved go or no-go checklist: recipient eligibility validation, settlement and return traceability, and clean reconciliation outputs for payout batches. If any one of those breaks under pilot volume, expand your fallback rails first and fix the gap before broad rollout.

If you take one thing forward, make it this: use prepaid cards where speed and access gaps are real. Then keep ACH and other bank-rail fallbacks available when predictability and broader acceptance matter more.

Related reading: Accounts Payable Software Comparison for Platforms That Need Operational Proof.

Frequently Asked Questions

When should a platform choose prepaid cards over ACH or direct deposit?

Choose prepaid cards when recipient access matters more than bank-rail familiarity, especially if some payees do not have a bank or credit union account. ACH is a batch process, so it is generally better for scheduled disbursements than urgent access promises. If your promise is "funds available fast," cards are worth testing first, but only after you verify return handling and reconciliation.

Who are payout cards best for in contractor and creator ecosystems?

They fit recipients who need access to spendable funds and may not want, or may not have, a traditional deposit account. This can be relevant in payout populations where access to traditional bank accounts is limited. The key differentiator is access: a prepaid card is funded in advance and is not linked to a bank account.

When should a platform avoid prepaid cards even if recipients want fast access?

Avoid them if your recipients are already fully banked and your finance team cares more about predictable batch settlement than instant access. Also pause if your provider cannot document program constraints, exception handling, and how failed payouts surface back to ops. Fast funding is not enough if you cannot explain what happens on a return, hold, or duplicate request.

How do push-to-card payments and Original Credit Transaction (OCT) differ from standard card usage?

Standard card usage is the recipient spending from a card, while push-to-card is your platform sending funds directly to the recipient's card account. The card-rail mechanism for that disbursement is the Original Credit Transaction, or OCT. In one documented implementation, OCT credit timing is typically within a maximum of 30 minutes, which is very different from ACH batch timing.

What is the practical difference between wire transfer and prepaid cards for cross-border payouts?

A wire transfer electronically moves money from one bank account to another, so it assumes the recipient can receive funds through a bank account. A prepaid card does not depend on the recipient holding a traditional bank account, which can widen eligibility in some payout populations. The tradeoff is operational: for either option, you still need corridor and program validation before scaling cross-border payouts.

Which compliance checks are mandatory before enabling prepaid card payouts across markets?

At minimum, confirm AML coverage, customer due diligence, and tax document collection paths before launch. For legal entities, covered institutions must identify and verify beneficial owners; for U.S. information reporting, collect Form W-9; for foreign beneficial owners, use Form W-8BEN when requested by the payer or withholding agent. If your provider cannot show the exact document and approval path, do not enable the rail yet.

What should teams verify in a pilot before expanding to full payout batches?

Make one batch ID traceable from payout creation to settlement or return status without spreadsheet stitching. Verify retry behavior is consistent and that reconciliation identifiers stay attached to the payout record. If those checks fail in pilot, larger payout batches can create reconciliation disputes instead of speed.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/FinCENFBARHelp.pdftrusted

- consumerfinance.gov/consumer-tools/prepaid-cardstrusted

- consumerfinance.gov/ask-cfpb/what-types-of-fees-do-prepaid-cards...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- fdic.gov/news/press-releases/2024/fdic-survey-finds-9...trusted

- fdic.gov/household-surveytrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Gift Card Payouts for Platforms When to Use Gift Cards vs Cash

For payout decisions, keep the rule simple: use gift cards for discretionary incentives. Default to direct deposit (ACH) when money is owed for work. If a payment settles an obligation rather than rewards behavior, start with a cash rail and make any exception earn extra review.

When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts

Treat rail choice as product logic, not team habit. No rail wins everywhere. SWIFT and local payment rails solve different payout risks, so your job is to route each payout by destination, currency, speed, and cost, not by whichever option sounds more global or more modern.

When Instant Payout Matters for Gig Platform Payments

Instant payout is a tool, not the goal. The real operating decision is where instant timing creates measurable value, where batch timing is enough, and where both should run side by side.