Quick Answer

Default to ACH direct deposit for owed payouts, and keep gift cards for discretionary incentives. Classify each payment as incentive or earned compensation before release, then block any automatic fallback from owed funds into merchant cards. Use prepaid cards only when broader spend acceptance is required and the product type is verified up front. For operations, require approval records, delivery and claim states, provider references, and replacement reason codes so finance can reconcile unresolved value without guesswork.

When Gift Cards Make Sense for Platform Payouts#

For payout decisions, keep the rule simple: use gift cards for discretionary incentives. Default to direct deposit (ACH) when money is owed for work. If a payment settles an obligation rather than rewards behavior, start with a cash rail and make any exception earn extra review.

That distinction matters because these methods solve different jobs. Gift cards can work well when you want a memorable reward or simpler campaign fulfillment. Cash works better when recipients need flexibility or the amount is material. In U.S. contexts, ACH is the network behind direct deposit and direct payments, with reach to U.S. bank and credit union accounts. That is why it remains a practical default for many recurring U.S. payouts.

The first policy red flag is simple: do not let your product present gift cards as just another equivalent payout method for earned funds. Federal wage guidance uses "paid finally and unconditionally" and "free and clear" language, and IRS guidance groups gift cards with cash-equivalent items in tax discussions. That does not answer every contractor scenario, but it is enough to justify a stricter internal rule. Incentives can use card-based options. Owed earnings should go through a cash rail unless counsel approves something narrower.

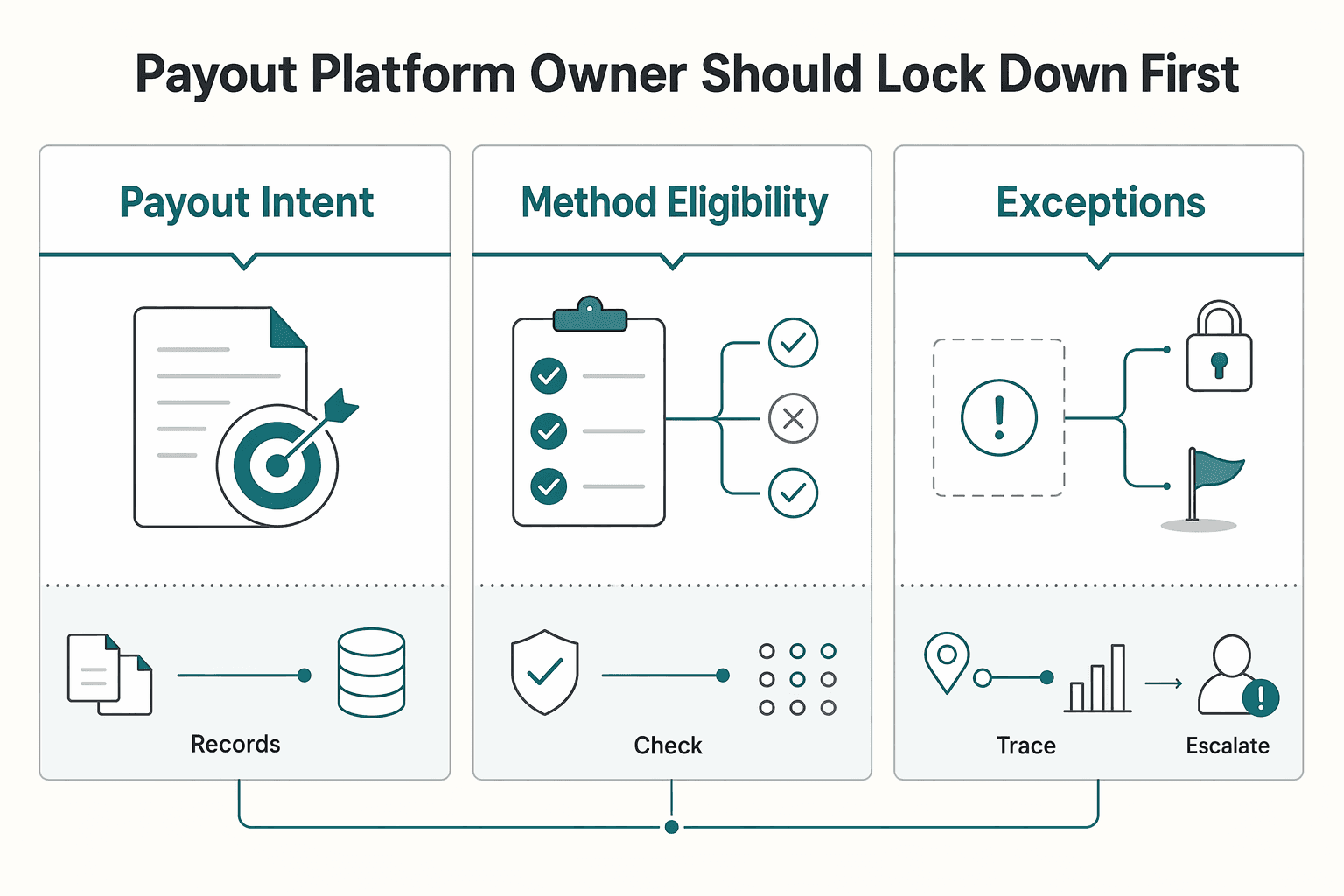

What a payout platform owner should lock down first#

Before engineering enables any method, you want three decisions documented across product, finance ops, and engineering:

| Decision | What to define | Control note |

|---|---|---|

| Payout intent label | Mark each use case as incentive, bonus alternative, refund-like credit, or owed earnings | If you cannot classify it cleanly, pause rollout |

| Method eligibility rule | Tie each intent label to approved rails | A referral reward may allow a merchant gift card; invoice settlement should not silently fall back to one |

| Exception owner and evidence | Define who reviews edge cases, what approval is needed, and what record proves why a method was used | Store the request reason, selected rail, approver, and provider response from day one |

Those three decisions sound basic, but this is where teams get into trouble. Your platform should store the request reason, selected rail, approver, and provider response from day one. If finance later asks why a creator payment went out as a prepaid digital gift card instead of ACH, "the user picked it" is not a strong control.

This article is written for teams making that operating choice at scale, not for one-off employee perks. The practical question is less about preference and more about intent, recoverability, and auditability. If your program is discretionary and campaign-driven, gift cards may reduce friction. If users are relying on the funds, keep them on cash rails and build the rest of your payout platform around that rule.

Want a quick next step on "gift card payouts platforms when to use gift cards vs cash"? Try the free invoice generator.

At-a-glance comparison for gift cards, prepaid cards, and cash rails#

Choose the rail by payout intent first: merchant gift cards for discretionary rewards, prepaid digital cards when you need broader spend flexibility, and ACH/wire for owed, recurring, or operationally critical payouts.

| Criteria | Merchant gift card | Prepaid digital card | ACH/Wire transfer |

|---|---|---|---|

| Recommendation | Best for rewards program | Best for broad spend flexibility | Best for contractual or recurring payouts |

| Payout intent | Discretionary incentives, referrals, campaign rewards | Discretionary payouts where brand restriction is a problem | Earned payouts, invoice settlement, repeat creator or contractor payments |

| Recipient acceptance | Limited to a specific merchant or brand family | Broader than a merchant card, but not universal by default | High practical flexibility because funds land in an account |

| Failure recovery | Usually resend or reissue, but merchant-specific redemption issues can create edge cases | Reissue may be possible, but replacement rules and user confusion matter | Return and retry flows are usually clearer than redemption disputes |

| Support burden | Higher when users cannot find the email, redeem at the wrong merchant, or expect cash-like use | Medium to high if card rules are unclear or the card is mistaken for a normal bank card | Lower variance for repeat payouts, though bank detail errors still create tickets |

| Reconciliation effort | Needs issued, delivered, redeemed, expired, and reissued views | Needs the same card lifecycle views, plus replacement tracking | Cleaner settlement tracking for owed payouts, especially on repeat runs |

| Compliance sensitivity | High if anyone tries to use it for owed earnings | Medium to high, depending on product structure and payout use case | Lower for owed-payment use cases, but still requires normal payout controls |

| Redemption breakage handling | Track outstanding unused balances and expired value | Unused balances and unclaimed value still need visibility | Not a redemption concept in the same way |

| Manual support tickets | Common for delivery, resend, merchant restriction, and "where can I use this?" questions | Common for activation, acceptance, and replacement questions | More concentrated around bank account errors and payout status questions |

| Exception-case reissues in the payout platform | Needs approval rules, reason codes, and duplicate-send controls | Same need, plus clear distinction between replacement and second payout | Needs retry and return handling; do not auto-downgrade owed funds into cards |

Verify the product type before rollout. CFPB is explicit that gift cards and prepaid cards are different, and it notes gift cards typically do not have protections under the CFPB's 2019 prepaid rule. If a vendor sells a "prepaid digital gift card," confirm whether it is an open-loop prepaid card with a network logo or a closed merchant product, because that changes acceptance, recipient expectations, and compliance review scope.

On cash rails, keep labels precise. Nacha describes ACH as the network that drives direct deposits and direct payments, so for U.S. repeat payouts this is the default rail, not just a generic "bank transfer."

The hidden cost is usually post-issuance cleanup, not face value. Vendor materials point to this directly: Tango highlights order history, delivery tracking, resend capability, and redemption history, while gift-card automation messaging calls out spreadsheets, manual sends, approvals, and tracking pain. If a provider cannot expose delivery status, redemption status, provider reference IDs, and reissue history in exports or webhooks, expect support load to rise.

Treat published claims from Blackhawk Network, Tango, and Giftbit as directional, not neutral proof. Use them to shortlist options, then validate against your own metrics: delivery failure rate, resend rate, reissue rate, unredeemed balance aging, and ticket volume per 1,000 payouts.

If you need one operating rule: when payout obligation and recipient flexibility matter more than campaign experience, use ACH or wire; keep cards for rewards.

Classify payout intent before choosing any rail#

Start by labeling payout intent, then choose the rail. Use cards for discretionary incentives, and route earned or recurring payouts to cash rails, with ACH/direct deposit as the default for repeat payments.

| Intent label | Default method | Red flag |

|---|---|---|

| Discretionary incentive | Merchant gift card | Recipient may assume it works like cash |

| Broad-spend incentive | General-use prepaid card | Product may be mistaken for a gift card, or vice versa |

| Earned or repeat payout | ACH / direct deposit | Do not downgrade owed funds into cards |

Be precise about product type before launch. Under CFPB definitions, a gift certificate is redeemable at a single merchant or affiliated merchant group, while a general-use prepaid card is usable across multiple unaffiliated merchants or ATMs. If a vendor offers a "prepaid digital gift card," confirm which product it actually is before enabling it in your payout platform.

Require product and finance sign-off on the intent label before engineering enables any method. Keep the policy packet specific: allowed use cases, blocked use cases, recipient-facing payout language, and the exact product type being purchased. This governance step helps prevent intent drift between policy and implementation.

Add one tax checkpoint to the policy. IRS guidance says gift certificates redeemable for general merchandise, or with cash-equivalent value, are not de minimis benefits and are taxable. Practical rule: document intent, keep direct deposit as the default for recurring payouts, and require exception review before any card option goes live.

Related: How to Pay Research Participants: Survey Incentives Gift Cards vs. Direct Deposits for UX Teams.

Where gift cards fit and where they create risk#

Use gift cards for narrow, optional incentives. If the payout is money the recipient is likely to treat as owed, default to ACH.

| Scenario | Gift card fit | Why | Better default if not a fit |

|---|---|---|---|

| Referral reward or one-off campaign incentive | Strong | Discretionary, time-bounded, and tied to engagement rather than owed compensation | Merchant gift card can work |

| Short-term engagement boost inside a Rewards program | Strong, with controls | Works when framed as promotional and the merchant choice matches recipient expectations | Merchant gift card or prepaid option, depending acceptance needs |

| Contractor invoice settlement | Weak | A store gift card is redeemable at a single merchant or affiliated merchant group, so acceptance limits create delivery risk | ACH |

| Guaranteed minimum or make-whole payout | Weak | Recipient expectation is usable funds, not merchant-restricted value | ACH |

| Any payout where spend flexibility matters | Weak | Merchant limits become support friction when recipients try to redeem outside that scope | ACH, or consider prepaid cards later if card delivery still matters |

The operational question is not whether you can send a card. It is whether the recipient can use the value in the way they need. Under CFPB definitions, store gift cards are merchant-limited. That can fit a known retailer reward, but it is risky for contractor or creator payouts. Before go-live, confirm the exact product type, including whether a "prepaid digital gift card" is actually merchant-limited.

Treat redemption friction as a real risk category, not an edge case. Public complaint threads show a repeat pattern: redemption failure followed by unclear support resolution. Two failure modes matter early: activation issues that shift ownership to retailer or issuer support, and minimum-balance redemption rules that create partial-balance exceptions your team must handle.

Recommendation: keep gift cards for optional rewards where merchant fit is part of the offer. For owed or business-critical payouts, use the ACH cash rail, especially when you cannot tolerate redemption exceptions and manual support.

This pairs well with our guide on Cash Pickup Payouts for Unbanked Contractors in Cash-Preferred Markets.

When prepaid cards outperform merchant gift cards#

Use a general-use prepaid card when you need card-style delivery and broader spend flexibility than a merchant gift card. If payouts are recurring or likely to be treated as owed earnings, move to ACH/direct deposit instead.

| Method | Acceptance scope | Replacement handling | User confusion risk | Best fit |

|---|---|---|---|---|

| Merchant gift card | Single merchant or affiliated merchant group under Regulation E | Depends on merchant or issuer policy | High when users expect broad card acceptance | One-off rewards tied to a specific retailer |

| Prepaid digital gift card | May still be merchant-limited if it is a gift card in digital form | Varies by issuer or bank | High if product naming is unclear | Digital reward delivery where scope is verified up front |

| General-use prepaid card | Multiple unaffiliated merchants, and sometimes ATMs, when network-branded | Issuer-specific policies still apply | Lower than merchant cards, but not the same as cash rails | Discretionary payouts where broad merchant choice matters |

The operational check is product classification, not packaging. Regulation E separates store gift cards from general-use prepaid cards, so verify the exact product type, network logo, and issuer policy before launch.

Naming is a common failure point. A gift card can look like a prepaid card, but it is different; if your UI or help copy uses terms loosely, recipients may expect network-card acceptance and open support tickets when redemption fails.

Prepaid cards can reduce merchant-restriction friction, but they are still not the default for repeat or high-importance payouts. ACH is built for scheduled recurring payment flows, so escalate from prepaid to direct deposit when payout frequency or payout criticality increases.

If you want a deeper dive, read Prepaid Cards as a Payout Method: When They Work for Platforms and When They Don't.

Cash rails for owed earnings and repeat payouts#

For owed earnings and repeat payouts, use cash rails by default: ACH where eligible, with an approved Wire transfer exception path, and no automatic downgrade to Gift card.

ACH is a bank-to-bank batched network, and direct deposit of payroll is a standard ACH credit use case. A wire transfer is electronic movement between bank accounts, and the Fedwire Funds Service is used for large-value, time-critical payments that are immediate, final, and irrevocable once processed. For owed funds, those rail properties should drive your method choice.

| Rail | Use it for | Timing profile | Policy guardrail |

|---|---|---|---|

| ACH | Routine earned payouts and repeat disbursements | Batched (not real-time) | Default where recipient/program eligibility is confirmed |

| Wire transfer | Time-critical or approved exception cases | Can be immediate and final once processed on Fedwire | Use as an approved fallback path, not an ad hoc substitute |

| Gift card | Discretionary incentives | Delivery/redemption-dependent | Do not use as fallback for owed earnings |

Set fallback logic explicitly in product and ops policy:

- Attempt ACH when the recipient, market, and program support it.

- Route to approved wire when ACH is unavailable or timing is critical.

- Block any automatic conversion of owed earnings to gift cards.

For cross-border payouts, validate eligibility before release. Coverage and transfer options vary by country, currency, and transfer type, and delivery time is route-dependent. Avoid promising one global SLA: additional compliance or security checks can take 2 to 10 working days, and sometimes longer.

If funds are owed, keep them on cash rails and treat card programs as incentive tools, not liability settlement. For a step-by-step walkthrough, see When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts.

Redemption operations and failure handling#

If you use gift cards, the operational risk is post-issue: proving what happened, assigning ownership, and separating normal recovery from fraud risk. Run redemption as an event-driven workflow with webhook updates and explicit states, not a single "sent" flag.

Use this order of operations: issue event, recipient delivery, claim status, redemption confirmation, then exception escalation. That sequence prevents false closure because delivered is not claimed, and claimed is not fully redeemed. Some voucher lifecycles explicitly separate DELIVERED, FAILED_DELIVERY, CLAIMED, and REDEEMED, and partial use can remain in CLAIMED until fully redeemed. Do not treat the liability as resolved until the provider confirms final redemption.

| Stage | What to record | Typical owner | Escalate when |

|---|---|---|---|

| Issue event | Internal payout ID, recipient ID, idempotency key, provider order request | Engineering and payout ops | Write call times out or is retried without dedupe controls |

| Recipient delivery | Delivery status, delivery channel, provider order status, timestamp | Provider and support ops | Status moves to failed delivery, or pending exceeds expected window |

| Claim status | Claimed or partially claimed state, remaining value if provider exposes it | Support ops | Recipient reports partial use but internal records show final redemption |

| Redemption confirmation | Final redeemed state, terminal timestamp, provider reference IDs | Finance ops | Internal ledger closes before terminal provider state arrives |

| Exception escalation | Internal case ID linked to provider referenceOrderID or externalRefID | Support and finance ops | Manual review starts without both IDs |

Failure modes and owner map#

Non-delivery is often the first real support event. Providers may send asynchronous status updates for successful, retrying, failed, or partially failed processing, so your intake should process non-terminal updates instead of waiting only for a final status. Review items still pending after one business day.

| Failure mode | What it means | Handling note |

|---|---|---|

| Non-delivery | Often the first real support event | Process non-terminal updates and review items still pending after one business day |

| Partial redemption | Not a failed redemption, but not complete | Confirm provider state, remaining value if available, and the internal case before any replacement decision |

| Expired links | Some programs issue specialized links with specific expiration dates | Model as a possible exception path |

| Merchant rejection | Not assumed as a universal status | Handle as a program-specific exception reason |

| Duplicate attempts | Duplicate deliveries can occur | Use idempotent retries for issue and replacement writes, and deduplicate webhook consumers |

Partial redemption needs a separate path. It is not a failed redemption, but it is not complete, and that affects support handling and finance closure. Before any replacement decision, support should confirm provider state, remaining value if available, and the internal case tied to the original issue.

Expired links should be modeled as a possible exception path, since some programs issue specialized links with specific expiration dates. Merchant rejection should also be handled as a program-specific exception reason, not assumed as a universal status.

Duplicate attempts are preventable. Use idempotent retries for issue and replacement write operations so retries do not create duplicate outcomes. Webhook consumers must also deduplicate because duplicate deliveries can occur.

Replacement protocol and traceability#

Replacement should follow policy, not queue discretion. Define approval thresholds and require a reason code on every replacement so finance can distinguish user error from delivery/provider issues and higher-risk cases.

The verification checkpoint is mandatory: every redemption exception should map to an internal case ID plus provider reference (referenceOrderID or externalRefID). If support cannot jump from ticket to provider event trail quickly, resolution slows and ownership blurs. For teams comparing gift cards with cash, this is often the operational deciding factor.

Finance controls and reconciliation artifacts teams need on day one#

Set the day-one control standard early: every payout must be traceable from request to provider response to ledger posting, whether you use gift cards or ACH.

| Control area | Gift card path | ACH path | Finance requirement |

|---|---|---|---|

| Audit trail | Payout request, issue response, delivery/claim events, redemption status, ledger posting | Payout request, transfer response, payout/deposit status, ledger posting | One internal payout ID tied to provider reference IDs with immutable timestamps |

| Reconciliation artifact | Issued vs. redeemed view, plus outstanding unredeemed value | Payout reconciliation report plus bank reconciliation view | Summary totals that drill down to itemized transaction detail |

| Exception review | Failed delivery, partial redemption, replacement, duplicate issue attempts | Return, reject, pending deposit, duplicate payout attempt | Aging report with owner, reason code, and current status |

| Support signal | Method-level ticket volume and repeat failure reasons | Method-level ticket volume and return reasons | Track by payout platform and method to expose operating cost, not just volume |

The key checkpoint is drill-down, not summary totals. Provider reporting should let finance reconcile each payout to the underlying transaction batch and inspect itemized records. For monthly close, pair payout reconciliation with bank reconciliation so finance can track payout/deposit status and outstanding balances.

For gift card programs, keep an internal monthly pack that covers issued value, redeemed value when redemption events provide it, outstanding liability, exception aging, and method-level support volume. That support metric is an internal operating control, not a universal external reporting requirement.

Policy gates that stop category mistakes#

Set approval gates before sending any payout. Separate incentive campaigns from owed earnings, define method eligibility by payout type, and require reason codes plus review when reissues cross your internal risk threshold. If a user is owed compensation, a failed ACH should not auto-fall through to a gift card replacement.

Engineering checks that make the books defensible#

Use idempotency keys on write operations so retries do not create duplicate payouts or active codes; Stripe notes keys can be removed after they are at least 24 hours old. Make webhook consumers replay-safe by logging processed event IDs and skipping duplicates. Keep immutable, tamper-evident event logs so you can detect post-delivery modification or deletion during reconciliation and audit review.

| Check | Why it matters | Article detail |

|---|---|---|

| Idempotency keys on write operations | Retries do not create duplicate payouts or active codes | Stripe notes keys can be removed after they are at least 24 hours old |

| Replay-safe webhook consumers | Duplicate events do not create duplicate processing | Log processed event IDs and skip duplicates |

| Immutable event logs | Reconciliation and audit review can detect post-delivery modification or deletion | Keep logs tamper-evident |

Conclusion#

Keep the policy simple: incentives can use a gift card, but owed earnings should default to a cash rail such as ACH. That rule will save you more cleanup than any vendor feature comparison, because the hard problems here are not cosmetic delivery choices. They are reporting exposure, redemption tracking, support burden, and whether finance can defend the ledger later.

For recurring creator or contractor payouts, ACH is the practical default because ACH credit transfers sit behind common direct-deposit use cases. If a payment is urgent enough that same-day certainty matters, wire can be the approved exception, not the everyday path. Fedwire is built for mission-critical same-day transfers and emphasizes payment finality. If you keep a wire fallback, document your bank cutoff handling against the Fedwire business-day window rather than assuming ACH and wire behave the same way.

A clean rollout is easier if you phase it instead of turning on every method at once:

- Classify payout intent first.

Start with the payout types you already have and label each one as either discretionary incentive or owed compensation. This is the checkpoint that matters most. Finance should verify whether any contractor or service payment can trigger Form 1099-NEC reporting, and product should confirm the user promise matches that label.

- Turn policy into method rules.

Once the intent labels are approved, map them to allowed rails. Incentive campaigns may use gift cards where program rules allow. Contractual, recurring, or SLA-sensitive payments should route to ACH, with wire reserved for documented exception cases. Use tax and program-policy guidance as the reason to keep that line firm rather than treating cards and cash as interchangeable.

- Add controls before scale.

Gift-card programs need written controls because weak tracking creates fraud, waste, and abuse risk. Your minimum pack should cover issuance approval, reissue rules, and monthly reconciliation of issued value, redeemed value where available, and outstanding balances. If you hold prepaid customer value, keep the accounting treatment disciplined as a liability until the underlying obligation is satisfied rather than treating everything as immediate revenue at issuance.

The payoff is simple: if you separate incentives from obligations early, you will avoid most of the ugly edge cases later. Your next step can be low friction. Take your current payout catalog, validate each method rule with finance and engineering, then enable only those approved paths in your payout platform.

Related reading: Mass Payouts for Gig Platforms That Teams Can Actually Operate.

Frequently Asked Questions

Are gift cards legal for contractor payouts, or should we treat them as incentives only?

Treat them as incentives unless you have a very specific reason and legal review to do otherwise. If the payment is for services, IRS reporting can still apply, including potential Form 1099-NEC obligations once reportable payments meet the threshold amount, so a gift card does not make the compensation reporting issue disappear. A useful rule is simple: promotional rewards can fit a gift card model, while owed earnings are generally better handled on a cash rail.

When should a platform choose a prepaid card instead of ACH or wire transfer?

Choose ACH first for normal earned payouts because the ACH system is the standard network behind direct deposits. Use wire when the payment is urgent and same day matters, since the Fedwire Funds Service is built for mission-critical transfers. Consider a prepaid card only if you intentionally want card-based delivery and have documented the product terms up front, because gift and prepaid card terms are not uniform.

What are the most common gift card redemption failure modes at scale?

Failure modes can include redemption issues and unauthorized use after the code is exposed. One especially ugly failure mode is theft or unauthorized use, because there is often little or no recourse once value is drained. Every exception should tie back to an internal case ID plus the provider reference so support and finance are looking at the same event.

How should finance teams reconcile issued, redeemed, and expired gift card balances?

Keep three core balances every month: issued value, redeemed value when redemption events are available, and outstanding unredeemed value. Track expirations and fee events separately, and verify card terms before you book anything because terms can vary and broad assumptions will create cleanup later. For accounting, do not treat breakage as instant revenue at issuance. Guidance supports recognizing expected breakage in proportion to the pattern of rights exercised.

What fallback path should we use when a gift card cannot be redeemed?

Base fallback on payout intent, not on whatever method is easiest to click in the platform. If the original payout was an incentive, reissue only after reason-code review and duplicate-check validation. If it was owed compensation, move to the approved cash method and preserve the audit trail. Do not let owed earnings fall into a gift-card retry loop.

Which payout method should we default to for recurring creator or contractor earnings?

Default to ACH for recurring earnings, creator payouts, and contractor payments that are part of normal operations. Use wire for exception cases where urgency justifies same-day handling. For the core decision here, recurring earned payouts are typically better suited to direct deposit than merchant gift cards.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumerfinance.gov/consumer-tools/prepaid-cards/choose-the-righ...trusted

- consumerfinance.gov/ask-cfpb/where-can-i-use-my-prepaid-card-en-383trusted

- ecfr.gov/current/title-29/subtitle-B/chapter-V/subcha...trusted

- ecfr.gov/current/title-12/chapter-X/part-1005/subpart...trusted

- fdic.gov/consumer-resource-center/2024-12/what-you-sh...trusted

- fdic.gov/consumers/consumer/news/december2019.pdftrusted

- federalreserve.gov/paymentsystems/fedach_about.htmtrusted

- federalreserve.gov/paymentsystems/fedfunds_about.htmtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Prepaid Cards as a Payout Method: When They Work for Platforms and When They Don't

Prepaid cards are a real payout option, but they are not a shortcut to sound payout design. If you run payouts for a marketplace platform or embedded payments product, the question is not just whether a rail moves money fast. It is whether the rail fits your use case and operating model.

How UX Teams Should Pay Research Participants with Gift Cards or Direct Deposit

Research incentives are not just a budget line you approve after recruitment. They can shape who responds and how smoothly your study operations run. If you want to pay participants with gift cards or direct deposit without rollout surprises, you need to set the amount and the payout method together.

Virtual Credit Cards for Platforms: How to Issue Single-Use Cards for Contractor and Vendor Payments

Single-use virtual cards are often positioned as a fit for controlled vendor payments, but not for every contractor payout. This guide helps product, Payments Ops, and AP teams decide whether virtual cards fit their operating model, or whether cards belong alongside ACH, checks, or other payout rails.