Quick Answer

Choose an operating model first, then tune rails and speed. In this mass payouts gig platforms guide, the practical recommendation is to run one model your product, engineering, finance, and compliance teams can all execute and reconcile end to end. Use API-first when you can own status logic and exception handling, keep CSV uploads for narrow correction paths, and pick Same Day ACH, RTP, FedNow, or Push-to-card by scenario after confirming provider and program support.

How to run mass payouts on gig platforms by choosing the right model before tuning rails and speed#

- Why mass payouts moved upstream

Mass payouts are no longer just a finance back-office concern. If your platform pays contractors, creators, or marketplace sellers, the payout experience affects recipient trust and your operational workload. In practical terms, mass payments mean paying many recipients in one flow instead of sending transfers one by one. That makes payout design a product and operations decision, not just an accounting task.

- Why the decision gets harder as you grow

A simple setup usually works only at low volume. Once you add more recipients, more exception cases, or cross-border flows, manual uploads, spreadsheet checks, and disconnected tools increase the odds of delays, failed transactions, and reporting gaps. At that point, bulk payments stop being just a speed problem and become an orchestration problem across onboarding, payout release, status tracking, and reconciliation.

- What this guide is built to help you decide

This guide is for founders, product leaders, engineering owners, and finance ops teams that need to choose an operating model without creating avoidable rework. The focus is decision value: how to compare options, what to implement first, and where failure points usually show up when API integration and finance controls are designed in isolation. A good rule of thumb is to choose the model your team can actually operate and reconcile, then optimize speed and coverage after that.

- What to verify before you commit to a provider or rollout plan

Coverage, onboarding, and compliance details vary by provider and program, so you should validate specifics before launch instead of assuming any vendor claim is universal. One payout provider, for example, states support for 70+ currencies and 238 countries and markets. That is a provider-specific claim, not a market-wide baseline. The same caution applies to KYC or KYB onboarding, and to cross-border complexity, which usually increases as currencies and regulations expand.

That is the lens for the rest of this guide. You will get concrete comparison points, implementation order, and failure-mode checks so your payout stack does not split into separate truths across product, engineering, and finance. Use this early checkpoint: can you trace a payout request from recipient readiness through execution status and into reconciliation evidence without relying on spreadsheet cleanup after the fact? If not, tighten orchestration before you scale volume.

Related: Guide to Bulk Payment Processing: How Platforms Send Thousands of Payouts in a Single Run.

Who this list is for and how to pick your path#

This list is for teams making platform payout decisions, not workers comparing gig apps. If you are paying large recipient groups across regions, treat this as an operating architecture choice, not consumer app selection.

Use these filters to pick your path:

- Decision context fit

Use guidance built for business mass payouts, especially if your model resembles paying large gig-work populations across multiple regions.

- Audience fit of your inputs

Separate worker-focused gig-app content from the inputs you use for payout decisions. Worker-side advice can be useful background, but it is not a technical or operating blueprint for payout architecture.

- Evidence quality

Treat working-paper material as directional, not final authority, and avoid overcommitting based on non-final evidence alone.

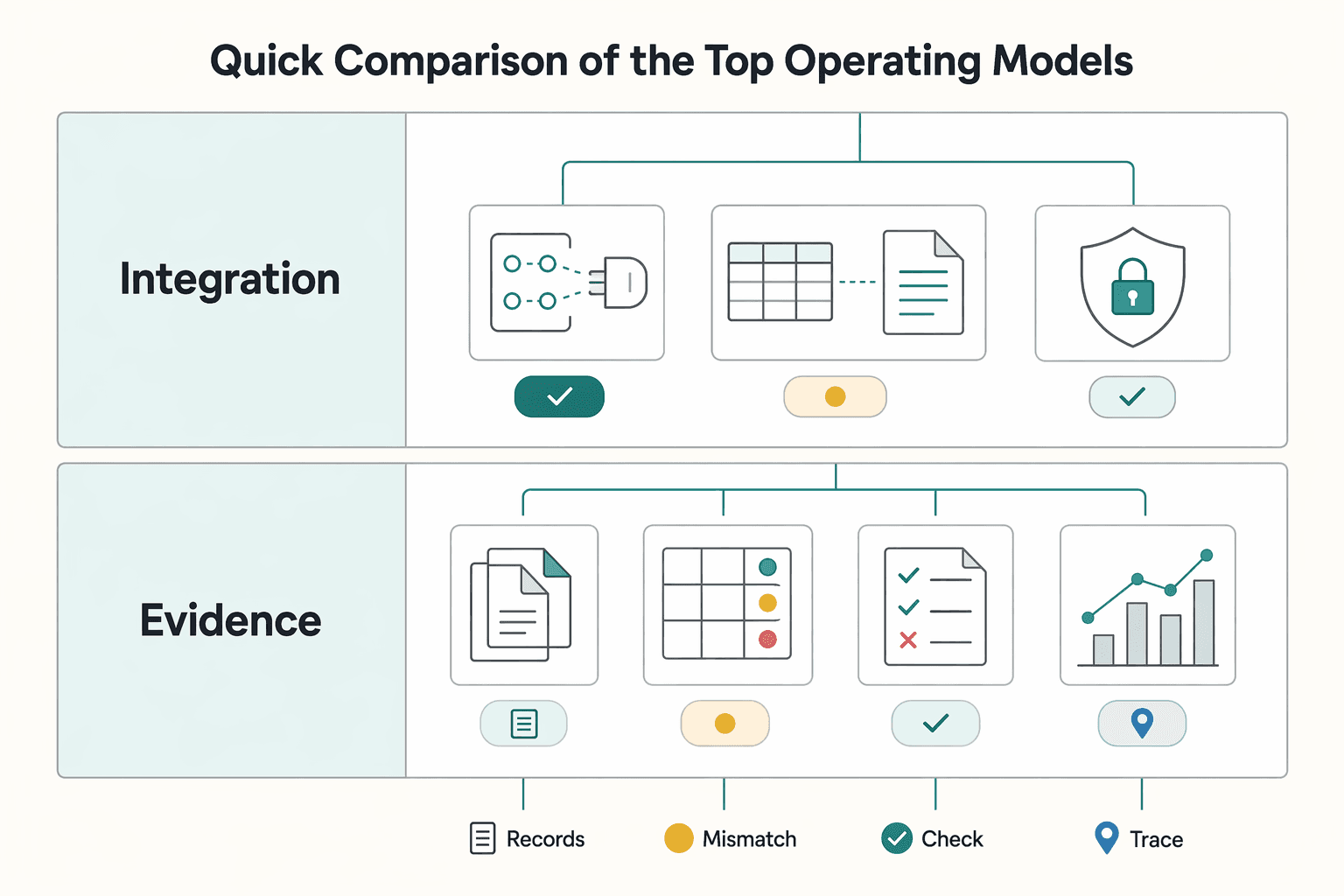

Quick comparison of the top operating models#

Choose the model your team can run end to end, not the one with the strongest marketing. For most teams, the practical split is API-first for higher-maturity recurring operations, hybrid API + CSV uploads for phased change, and Merchant of Record (MoR)-led operations when compliance ownership is the main constraint.

| Model | Team maturity | Best for | Key pros | Key cons | First use-case to launch | KYC/AML checkpoint | Expected ERP steps | Ledger journal reconciliation |

|---|---|---|---|---|---|---|---|---|

| API-first orchestration | Higher maturity across product, engineering, and finance | Recurring high-volume payouts with strict operational controls | Strong automation, clearer status handling, consistent payout IDs | Higher implementation and exception-handling load | One standard domestic batch flow | KYC/AML controls are enforced before release; AML is handled as ongoing monitoring, not a one-time check | Approved payee records, payout status exports, and journal posting rules with clear ownership | One payout ID traces from request to status event to journal entry without spreadsheet repair |

Hybrid API + CSV uploads | Mid-maturity teams modernizing in phases | Teams that need API scale but still rely on file-based finance ops for exceptions | Faster rollout, preserves familiar finance workflows during transition | Dual-system drift risk, duplicate-send risk, uneven audit trails | API for standard payouts; CSV uploads only for defined exceptions (for example, corrections or reversals) | Same KYC/AML gate as API path, with explicit review ownership for file-based exceptions | API-driven records plus controlled file intake mapped into the same finance flow | CSV rows map back to the same payout ID and journal structure used by API payouts |

Merchant of Record (MoR)-led operations | Earlier-stage or compliance-constrained teams, especially in cross-border expansion | Teams prioritizing speed to launch over deep payout-stack customization | Can reduce direct compliance operations your team must run | Less direct control and potentially thinner operational detail for finance | One new country or seller segment where compliance work is blocking launch | Define which KYC/AML responsibilities are handled by MoR vs your internal team before go-live | Confirm what reconciliation and status outputs finance receives and how often | Validate journal-ready output quality early; if exports are thin, month-end effort shifts to manual cleanup |

Treat ranking content as input, not proof. One vendor-authored 2025 comparison says it evaluates seven platforms and cites criteria such as API integration speed, rail options, tax compliance, and payee experience; another comparison source is explicitly marked [Promoted]. Corridor-level pricing, failure-rate benchmarks, and independently audited ranking methodology are often not provided, so validate those gaps directly before committing.

Option 1 API-first orchestration for control and scale#

API-first orchestration is usually the best fit when you need reliable payout visibility, safer retries, and cleaner reconciliation at recurring volume. It works when your team can own both the engineering workflow and the finance mapping, so payouts run as a product system instead of a manual file process.

Where this model fits#

API-first payout platforms turn payouts, onboarding, and compliance into programmable components, with payouts pushed from your app through REST APIs. In practice, your application becomes the source of truth for release, status, and exceptions rather than email or shared-file handoffs.

This model is strongest for recurring high-volume payout operations with strict status visibility requirements, including teams that need event-level tracking across the payout lifecycle.

What you gain and what you must build#

You gain strong automation through programmatic payout triggering, webhooks, and idempotency. Webhooks support near-real-time status handling, and idempotency keys make retries safer when responses are delayed or ambiguous.

You also take on heavier implementation work:

- Payout state design and webhook-to-record update rules

- Exception routing for failed, delayed, or duplicate requests

- Reliable mapping from payout outcomes into ERP and Ledger journals

A consistent ledger is a core scaling requirement. If ledger mapping is unclear, API integration alone will not solve month-end risk.

Use this readiness test before expanding scope: can you trace one payout ID from request, through webhook events, into final Ledger journals and ERP records?

Common failure mode#

The usual failure is incomplete exception design, not the send endpoint itself. Teams often launch payout creation first, then discover gaps in duplicate handling, delayed webhook logic, reissue rules, or finance-status mismatches.

Start narrow: move one manual batch payments flow into an event-driven run, post status updates via webhooks, and write only final outcomes to Ledger journals. Keep CSV uploads out of the normal path so you do not reintroduce a second source of truth.

One caution: vendor comparisons can be useful directional input, but not proof across providers. For example, one comparison dated 9th Feb 2026 reports "under 3 developer days" and "14 webhook events" for a single product; treat those as product-specific inputs, not category-wide expectations.

If you want a deeper dive, read Payee Verification at Scale: How Platforms Validate Bank Accounts Before Sending Mass Payouts.

Option 2 Hybrid API and CSV operations for mixed team maturity#

Hybrid works when you need phased modernization: run routine payouts through APIs, and keep CSV uploads as a tightly controlled exception path. The operating rule is simple: CSV should support exceptions, not compete with your primary flow.

Where this model fits#

Use this model when product and finance are moving at different speeds. You can keep manual handling for reversals, one-off adjustments, or records that fail standard validation while API-based payout flows mature.

CSV control matters more than most teams expect. A CSV export is a comma-separated tabular file with fixed headers, so header drift or manual edits can break consistency quickly. If CSV stays in scope, lock and version the header schema.

What you gain and what you must lock down#

The gain is phased delivery without forcing every edge case into automation on day one. The tradeoff is tighter cross-channel controls.

- Keep one shared payout reference across API and CSV paths.

- Use the same approval, status, and reconciliation fields in both channels.

- Make retries and resubmissions traceable in both paths.

- Store a complete record for each manual upload: input file, approver, upload time, and outcome/error output.

Use this checkpoint before scaling volume: can you trace a payout from an API request or a CSV row to the final finance record without ambiguity?

When this model should shrink, not expand#

Hybrid fails when dual operations become the default instead of a transition state. If exceptions grow beyond plan, narrow CSV to reversals and adjustments, and keep standard bulk payouts on APIs.

Also keep evidence quality in check. A cited gig-work study covers a 7-day field study with 16 active workers across three distinct platforms; useful context, but limited for architecture decisions at scale. Vendor performance claims (for example, 75% response rates and 2.5-minute response times) are product-specific and should not be treated as payout-model proof.

Option 3 Merchant of Record route when tax and compliance complexity dominates#

Use a Merchant of Record (MoR) route when cross-border tax and compliance complexity is the main constraint, not payout execution itself. The core tradeoff stays the same: you may reduce entity-level tax operations your team handles directly, but you also give up some control over payout operations. Decide only after responsibilities are documented in writing.

Best fit#

This route fits platforms entering multiple jurisdictions where tax treatment, documentation, and recordkeeping create more operational risk than sending funds. The signal is complexity across markets and participant types, not just payout volume.

Cross-border digital trade can trigger obligations even when a business or platform has no physical presence in a customer jurisdiction. The 2023 OECD/WBG/ATAF VAT Digital Toolkit for Africa is useful here because it covers foreign businesses and digital platforms serving consumers across jurisdictions and focuses on policy and implementation guidance.

What you gain and what you trade away#

You gain a simpler operating model if tax and compliance ownership is clearly centralized and your finance team still gets usable records. You trade away some flexibility compared with fully owned payout orchestration, especially for timing, exception handling, and custom status logic.

A practical example is a creator marketplace trying to reduce entity-level tax ops burden while keeping payout transparency for finance. That only works if reconciliation for payouts, adjustments, and reversals is clean in your own records.

What to verify before you commit#

Do not rely on broad compliance marketing. Ask for a written responsibility map, sample exports, field definitions, and retention details before signing.

Use authoritative sources when legal interpretation matters. IRS Internal Revenue Bulletin 2024-19 (May 6, 2024) states its synopses "may not be relied upon as authoritative interpretations." FederalRegister.gov also states its Web 2.0 display is not the official legal edition. If a decision depends on legal interpretation, verify against official text and counsel.

If Option 2 created audit drag through dual operations, this route can simplify ownership. Confirm that simplification shows up in contracts, exports, and month-end close workflows, not just in a sales deck.

You might also find this useful: Merchant of Record for Platforms and the Ownership Decisions That Matter.

Pick payout rails by scenario not by hype#

Choose rails based on the payout promise you make, not on whichever rail has the strongest marketing. If you promise immediate access, prioritize RTP, FedNow, or Push-to-card where your provider confirms support and enablement. If your core need is predictable routine runs, start with Same Day ACH and reserve faster rails for truly urgent cases.

| Rail | Use it first when... | Operational requirement | Coverage and program caveat |

|---|---|---|---|

| Same Day ACH | Routine payouts and predictable earnings runs are the priority. | Keep disciplined release timing and clear exception handling. | Confirm geography, recipient eligibility, and account/program enablement before launch. |

| RTP | Immediate availability is part of the user promise. | Run real-time monitoring and exception handling, not batch-only ops. | Verify recipient-side and provider-side support before promising broad availability. |

| FedNow | You need an instant-availability path for time-sensitive payouts. | Implement active routing plus timeout/error handling. | Validate support and limits for your specific provider program and recipient endpoints. |

| Push-to-card | You need a fast path tied to eligible cards. | Validate recipient card details and program rules up front. | Confirm supported cards, geographies, and account-level limits; do not treat coverage as universal without proof. |

A practical split is to route standard scheduled payouts through Same Day ACH, then use RTP, FedNow, or Push-to-card for urgent cash-out and exception scenarios. This keeps the instant experience where it matters while avoiding an all-urgent operating model. For a deeper bank-rail comparison, see FedNow vs. RTP: What Real-Time Payment Rails Mean for Gig Platforms and Contractor Payouts.

Before locking routing logic, require three artifacts from your provider: a rail-by-rail coverage resource, a written enablement checklist, and a public API/service status page. In practice, this may appear as resources labeled "Global Payouts Coverage" and "Real-time system status." Use these to verify where each rail works, when it is live for your program, and what to monitor on payout day.

One evidence caution: treat broad thought leadership as background, not launch proof. The Harvard M-RCBG paper No. 239 (April 2024) explicitly says papers in that series "have not undergone formal review and approval." Make launch decisions from official rail rules, provider coverage details, and your own reconciliation and exception testing.

Launch controls and failure handling before scaling volume#

Before you scale payout volume, make tax readiness and traceability non-negotiable: you should be able to explain what was reported, why, and from which record without rebuilding history later. If FEIE is in scope for any payee, keep the supporting facts attached to the payout record from the start.

| Control point | Grounded fact | Record use |

|---|---|---|

| FEIE filing reality | Qualifying individuals still file a U.S. return reporting the income. | Treat FEIE as a reporting workflow, not a reporting exemption. |

| Eligibility facts | Eligibility depends on having a tax home in a foreign country and meeting a qualifying test. | Capture the eligibility facts you will need at review time. |

| Physical presence test | 330 full days in foreign country/countries during a 12-consecutive-month period; those days do not need to be consecutive. | Store those underlying facts in your payout records. |

| Year-specific limits | FEIE maximums are $130,000 (2025) and $132,900 (2026) per person; the housing-expense limitation is generally 30% of the FEIE maximum, with IRS-listed housing amount limitations of $39,000 (2025) and $39,870 (2026). | Keep year-specific limits attached to the same record. |

- Treat FEIE as a reporting workflow, not a reporting exemption.

If FEIE is in scope for a payee, anchor your controls to IRS eligibility facts and filing reality: qualifying individuals still file a U.S. return reporting the income, and eligibility depends on details such as having a tax home in a foreign country and meeting a qualifying test.

- Capture the eligibility facts you will need at review time.

For the physical presence test, the IRS standard is 330 full days in foreign country/countries during a 12-consecutive-month period, and those days do not need to be consecutive. Store those underlying facts in your payout records so tax follow-up does not turn into manual reconstruction.

- Keep year-specific limits attached to the same record.

IRS FEIE maximums are $130,000 (2025) and $132,900 (2026) per person. The housing-expense limitation is generally 30% of the FEIE maximum, with IRS-listed housing amount limitations of $39,000 (2025) and $39,870 (2026).

- Run a pre-scale audit-readiness check on tax data integrity.

Before you increase volume, confirm each relevant payout can be traced to the supporting tax facts, applicable year limits, and filing context.

Conclusion#

The right choice is the operating model your team can run cleanly under pressure, not the option with the fastest headline. If finance cannot reconcile it, compliance cannot explain it, or ops cannot recover from a timeout without guessing, it is not ready to scale.

- Choose controllability before speed

Start with the model that gives your team clear ownership of approvals, exceptions, and payout state changes. What matters is not how modern the setup looks, but whether product, engineering, finance, and compliance can all work from the same record of truth. A useful red flag is any design that tries to satisfy rules on paper while sidestepping their intent. Case evidence on platform regulation ties that kind of "creative compliance" to stakeholder backlash and intensified regulatory scrutiny, which is a bad trade when your payout operations already have complexity.

- Prove traceability with one model and one reconciliation standard

Do not launch multiple payout paths and sort out the accounting later. The better sequence is narrower: pick one operating model, keep early complexity limited, and define one reconciliation standard that carries from payout request through provider result into your internal finance records. The checkpoint that matters most is easy to test: for any completed or failed payout, you should be able to retrieve the request ID, provider reference, status history, retry behavior, webhook outcome, and final finance posting without rebuilding history from emails or CSV uploads. If your team cannot do that on exception cases as well as happy paths, gaps usually surface faster as volume grows.

- Validate market and compliance assumptions before architecture hardens

When coverage or compliance requirements are unclear, confirm market or program availability early and keep the proof. The difference here is evidence, not optimism: written confirmation of supported markets, required payee data, compliance dependencies, and reporting outputs your finance team will actually use. One risk is designing around assumed availability, then discovering later that your target configuration or compliance path does not hold where you need it. At that point, changing the payout architecture can become more expensive because volume, worker expectations, and downstream mappings are already in motion.

That is the practical takeaway from this guide. Build the version you can audit, explain, and repeat first. Once end-to-end traceability is stable across both normal and broken cases, then expand scope.

Frequently Asked Questions

What are mass payouts for gig platforms, and how are they different from regular bank transfers?

Mass payouts are bulk disbursements sent to many recipients at the same time, rather than one payment handled one by one. For a platform, the difference is operational scale: you need a consistent process that can track and reconcile many payouts reliably.

When should a platform move from manual `CSV uploads` to API-driven payout automation?

Move once rising volume makes manual uploads time-consuming and error-prone. If you need the same process to work for 100 or 10,000 payees, an API is usually the better fit. Before switching, align developers, finance, and compliance on the integration plan and control model.

How should we decide between `Same Day ACH`, `RTP`, `FedNow`, and `Push-to-card` for different payout types?

Decide based on your payout promise and operational constraints, then verify actual availability, limits, and exception behavior by market and provider. For a deeper rail split, see FedNow vs. RTP: What Real-Time Payment Rails Mean for Gig Platforms and Contractor Payouts.

Are mass payouts a replacement for `Payroll` and `Accounts Payable (AP)`, or a separate system?

Treat mass payouts as a payout capability, not an automatic replacement for payroll or AP. A marketplace payout API can automate and scale disbursement operations, while payroll/AP-related finance and compliance controls still need clear ownership.

What minimum controls should be in place before scaling cross-border `Bulk payouts`?

At minimum, make sure validation and reconciliation controls are defined, and that developers, finance, and compliance agree on responsibilities. Specific KYC/AML or W-8/W-9 thresholds and required fields should be set with your compliance and tax owners.

How do `Webhooks` and `Idempotency keys` reduce payout failures and duplicate sends?

Use your payout-provider documentation to define retry handling, duplicate-prevention behavior, and status-state operations before scaling.

What should we verify before launch if we need `KYC`/`AML` plus tax flows like `W-8`/`W-9`?

Before launch, confirm developers, finance, and compliance are aligned on the integration plan and controls, and that validation and reconciliation are ready for ongoing processing and reporting. Define the execution order for KYC/AML plus W-8/W-9 flows with your compliance and tax teams.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- comptroller.war.gov/Portals/45/Documents/defbudget/FY2026/budget...trusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- federalregister.gov/documents/2026/02/11/2026-02769/patient-prot...trusted

- govinfo.gov/content/pkg/FR-2013-02-22/xml/FR-2013-02-22.xmltrusted

- hbs.edu/ris/Publication%20Files/StantonThomas_Submis...trusted

- hks.harvard.edu/sites/default/files/centers/mrcbg/Final_AWP_...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Validate Bank Accounts Before Mass Payouts

For mass payouts, the real question is not whether to verify payees. It is how much verification you require before release, who can override it, and what evidence you can produce later. If you cannot show that evidence on demand, your release rule is weaker than it looks.

FedNow vs RTP for Gig Platform Contractor Payouts

You are not choosing a payments theory memo. You are choosing the institution-backed rail path your bank and provider can actually run for contractor payouts now: FedNow, RTP, or one first and the other after validation.

Bulk Payment Processing Platforms for Thousands of Payouts

If your team runs recurring payouts at real volume, the real decision is operational. Can you execute a batch and still handle delays, bad recipient data, and month-end close without chaos? This guide is for founders, product leads, finance ops, and engineering owners evaluating **bulk payment processing platforms for high-volume payouts**.