Quick Answer

Start with a weighted vendor scorecard, then require proof before contract. For bulk payment processing platforms thousands payouts, prioritize idempotency, webhook duplicate handling, and reconciliation artifacts over headline coverage. Validate one real corridor matrix, inspect the event catalog, and demand a failed-then-retried demo. If a provider cannot map request IDs to payout-item outcomes and close-ready reporting, keep that option in pilot status.

What to Evaluate Before Your First Large Batch#

If your team runs recurring payouts at real volume, the real decision is operational. Can you execute a batch and still handle delays, bad recipient data, and month-end close without chaos? This guide is for founders, product leads, finance ops, and engineering owners evaluating bulk payment processing platforms for high-volume payouts.

A bulk payout means sending many recipient payments together in one batch instead of one by one. The focus here is recurring contractor, creator, marketplace, or commission runs where status updates can arrive asynchronously and the accounting trail matters as much as payment execution. It is not about occasional one-off transfers handled manually.

The right way to evaluate these platforms is simple: check platform fit first, then pressure-test the controls that keep production runs stable.

- API: the software interface your systems call programmatically

- Webhooks: HTTP endpoints that receive provider events, including asynchronous payout updates

- Idempotency: retry safety that reduces duplicate effects when requests are repeated

- Month-end close: the accounting process that finalizes activity and reconciles transactions

In practice, unclear behavior creates rollout risk. You need to know how payout creation, status updates, retries, and reconciliation outputs connect. Verify idempotency in detail, including key-retention limits, since some APIs note keys may be removed after 24 hours.

Keep finance involved from the start. A payout run is not done when money is sent; it is done when you can match payouts to the underlying transactions, export accounting-ready files such as CSV reports, and review an audit trail of system and user activity.

Success here should look boring: a predictable run with traceable statuses, controlled exceptions, and audit-ready evidence. Basic operator questions should be easy to answer. Which request created the payout? Which webhook changed state? Was a retry safe? Is a Trace ID available for delayed funds, including escalation after 10 business days where applicable? Do differing ACH batch-header attributes require separate batches?

We covered this in detail in How Payment Platforms Really Price FX Markup and Exchange Rate Spread.

Who This List Is For and Not For#

This list is for teams whose payout operations are frequent enough that batch execution, recipient-method mix, and reconciliation output affect daily work. If your volume is still low enough to review each payment one by one, these tradeoffs may matter less.

- Marketplace and contractor platforms

Best fit if you pay sellers, service providers, freelancers, or suppliers at high volume. Batch workflows are built for that pattern, with published limits such as 1,000 payments in one Wise upload and 15,000 payments per call in the PayPal Payouts API.

- Programs with mixed recipient methods

Strong fit if your program needs a mix of payout methods, including bank-account destinations and wallet options like PayPal or Venmo. One payouts API supports multiple PayPal or Venmo recipients, and Tremendous positions ACH, Venmo, and PayPal in one bulk payout product.

- Global affiliate, vendor, and referral payout teams

Prioritize this list if you run cross-border contractor, vendor, or affiliate payouts and need programmatic disbursement coverage. Stripe Global Payouts cites support for more than 50 countries and explicitly includes contractor, vendor, and affiliate use cases, but country and method coverage still needs provider-by-provider validation.

- Finance-ops-heavy teams with reconciliation pain

If close and controls are the main problem, prioritize reconciliation depth over headline coverage claims. Stripe notes that when you create payouts manually, you're responsible for reconciling payouts against transaction history, and PayPal offers a Payouts Reconciliation Report to help reconcile end-to-end money flow and transactions.

For a step-by-step walkthrough, see Mass Payouts for Gig Platforms That Teams Can Actually Operate.

The Selection Criteria That Actually Predicts Success#

Failure handling should come before coverage. A provider that looks fast in a demo but gives you weak retry controls, thin status detail, or vague support terms usually creates more pain than one with slightly slower payout completion.

The five buckets that matter most#

| Bucket | What to verify | Grounded example |

|---|---|---|

| Payout method coverage | Validate the country-and-method matrix your recipients actually need before signing | Programs may depend on ACH in the US, wallet payouts, or local bank rails in specific countries |

| Geography | Check coverage as country plus payout method | Thunes states reach across 140 countries and mentions payouts to mobile wallets, bank accounts, and cards |

| Integration depth | Confirm webhooks, duplicate handling, and idempotent request handling | One provider retries failed webhook deliveries up to 25 times over 3 days and offers event-level tooling |

| Control model | Decide whether you need file-based execution, API orchestration, or both | Wise says you can make up to 1,000 payouts in one go; Dwolla documents up to 5,000 payments in one API request processed asynchronously |

| Support SLA | Match severity definitions, response channels, and escalation paths to payout windows | Stripe publishes 6-hour, 4-hour, and 15-minute response SLAs depending on plan |

- Payout method coverage

Start with the methods your recipients actually need, then validate by corridor. "Bank payouts" is too broad if your program depends on ACH in the US, wallet payouts, or local bank rails in specific countries. What matters is the country-and-method matrix you can test before signing.

- Geography

Check coverage as a pair: country plus payout method. Thunes publicly states reach across 140 countries and mentions payouts to mobile wallets, bank accounts, and cards, but you still need corridor-level confirmation for your payout mix. The useful differentiator is supported countries by method, recipient type, and currency, not the headline footprint.

- Integration depth

For recurring payout operations, API support alone is not enough. You also need webhooks for asynchronous lifecycle updates, and at least one major provider explicitly notes webhook consumers must handle duplicate deliveries. One provider retries failed webhook deliveries up to 25 times over 3 days when your endpoint does not return 2xx, and offers event-level tooling to review and resend notifications. The real test is whether you get both idempotent request handling and an event model your team can operate under retry conditions.

- Control model

Choose whether your team needs file-based execution, API orchestration, or both. Wise supports batch payouts and API automation, and says you can make up to 1,000 payouts in one go with Batch Payments. Dwolla documents mass payments of up to 5,000 payments in one API request and notes those requests process asynchronously after submission. The practical question is where approvals, onboarding/KYC checks, exceptions, and resubmissions live: in your product, an ops console, or a file process your team has to push through month end.

- Support SLA

Support terms matter most on payout day. Stripe publishes response targets on paid support plans, including 6-hour, 4-hour, and 15-minute response SLAs depending on plan. What matters is whether the vendor commits to severity definitions, response channels, and escalation paths that match your payout windows.

A practical weighted scorecard for finance and engineering#

There is no universal formula, so use this as a starting point. If finance owns close risk and engineering owns execution risk, score each vendor from 1 to 5 in the four areas below, then apply weights that match your actual pain.

| Criterion | Why it predicts success | Finance weight | Engineering weight |

|---|---|---|---|

| Execution reliability | Duplicate protection, async status accuracy, retry safety | 30 | 35 |

| Exception tooling | Ability to isolate, resend, cancel, or investigate failed items | 20 | 25 |

| Compliance gating | KYC or onboarding checks, release controls, approval points | 20 | 15 |

| Reconciliation outputs | Batch-level reports, payout references, close-ready exports | 30 | 25 |

Decision rule: if failures are expensive for your business model, weight execution reliability first. Stripe documents idempotency for safely retrying requests without accidentally performing the same operation twice. That usually matters more than speed claims when you are trying to control payout risk.

Apply the same logic to status tooling. A provider can accept a request immediately while the final outcome arrives later through events, returns, or provider-side processing. If your team cannot trace a payout from request ID to provider event to final reconciliation artifact, you are carrying hidden risk even when submission looks smooth.

The pre-signing evidence pack to require#

Do not rely on verbal confirmation in sales calls. Ask every finalist for the same evidence pack and compare what they can actually produce:

- Country and method matrix with supported countries, payout methods, recipient types, and known exclusions for your target corridors

- Webhook event catalog with sample payloads, delivery behavior, retry semantics, and whether duplicate event delivery is expected

- Incident and escalation terms covering severity levels, support hours, escalation channels, and committed response targets

- Reconciliation artifact samples such as payout reports, field definitions, delivery cadence, and how payouts map back to underlying transaction batches

This checkpoint exposes gaps early. If a provider cannot show its event catalog, cannot explain duplicate webhook handling, or cannot produce a sample reconciliation file, expect more manual work later. One major provider's reconciliation report documentation shows the level of specificity to request. It frames the report as an end-to-end money-flow artifact and states the report is placed on SFTP by 9:00 AM daily.

For teams evaluating high-volume payout operations, this evidence pack matters more than polished product language. It tells you whether the provider can support finance close, engineering retry logic, and incident response when a batch does not go as planned.

If you want a deeper dive, read FedNow vs. RTP: What Real-Time Payment Rails Mean for Gig Platforms and Contractor Payouts.

Use your weighted scorecard to map required payout methods, webhook visibility, and exception handling before vendor selection, then compare that operating model with Gruv Payouts.

Quick Comparison of Leading Options in This SERP Set#

If you need to narrow the field fast, Wise and Dots appear the most operationally legible in current public excerpts. Treat Thunes, PayQuicker, and Tremendous as viable candidates that still need more pre-signing proof for high-stakes payout runs. This is not a product verdict. It is a visibility verdict based on what is verifiable now.

For bulk payout operations, coverage headlines are not enough. In this excerpt set, the safer shortlist is usually the vendor that explains post-submission status, retries, and reconciliation with the least ambiguity.

| Provider | Best for | Known strengths from current excerpts | Unknowns to validate | Integration confidence* |

|---|---|---|---|---|

| Thunes | Teams prioritizing broad international bank payout reach | Markets a single API for real-time, traceable bank transfers; one page claims 8 billion bank accounts in over 140 countries, including 60 real-time systems | Coverage figures vary across pages (130+ vs over 140); pricing model, failure rates, API/webhook depth, support structure, reconciliation outputs, and corridor-level method coverage are unverified here | Medium |

| Dots | Platforms wanting one API story from onboarding/compliance through payout and tax reporting | Positions an end-to-end Payouts API; claims real-time webhooks; says it handles failures, retries, and returned payments automatically across 150+ currencies and 190+ countries | Need proof of retry/return behavior in production, exact payout methods by corridor, pricing model, API limits/depth, support terms, and reconciliation artifacts | Medium-High |

| PayQuicker | Teams needing both file-based execution and API connectivity | Explicitly supports batch file upload and full API integration | Pricing model, market coverage, payout methods, failure handling, webhook/status model, API depth, support structure, and reconciliation exports are unclear from current excerpts | Medium-Low |

| Wise | Teams wanting documented batch mechanics and explicit status caveats | Supports batch automation via open API; docs state Batch Groups enable up to 1,000 transfers; docs also state COMPLETED does not imply payouts were successfully completed; public material highlights payout visibility as key to reconciliation cost | Pricing model, support structure, exact country-method fit for your corridors, webhook depth in this excerpt set, and audited failure rates remain unverified | High |

| Tremendous | Teams wanting API, integrations, or uploads for mass payout sending | Offers API, 5k+ integrations, and bulk uploads; API docs claim 2000+ payout methods; product page cites 24,000 companies | Cross-border depth, finance controls, approval model, failure recovery, pricing model, API depth, support escalation, and exact country-by-method availability need validation | Medium |

*Integration confidence reflects how much usable implementation detail is visible in current public excerpts, not a final product score.

How to read this table without over-trusting it#

Wise and Dots stand out because the excerpts expose more operating detail. Dots makes stronger visible claims on retries, returns, and webhook-driven sync. Wise gives a clear warning that batch-level completion is not the same as recipient-level success, which is a useful lens for both finance and engineering.

Thunes can still be attractive on reach, but its public country count is inconsistent across pages and should be verified before internal approval. PayQuicker is clearer on integration modes than on exception behavior. Tremendous is clear on sending options and breadth signals, but exception handling and close-ready finance detail still need proof.

What to validate before contract#

Before contract, request the same evidence pack from every finalist and compare it side by side:

- A country and payout-method matrix for your exact corridors and recipient types

- A webhook/event catalog with sample payloads, retry behavior, and duplicate-delivery expectations

- A reconciliation sample showing linkage between batch ID, item-level payout, and provider reference

- Support and escalation terms with severity definitions and response targets

Use one realistic test scenario and make each vendor map it end to end. If they cannot show the IDs, events, and reports your team will receive at each stage, lower their integration confidence regardless of how smooth the demo looks. For a deeper breakdown, read Webhook Payment Automation for Platforms: Production-Safe Vendor Criteria.

Thunes for Broad Global Payout Reach#

If your priority is cross-border coverage across mobile wallets and bank accounts, Thunes is a credible option to evaluate. Its public positioning emphasizes global payout reach.

Why Thunes stands out#

Thunes describes itself as built for global mass payouts, including claims of connectivity to over 120 mobile wallet providers and reach to four billion bank accounts. Other public materials present broader figures, including 4B mobile and stablecoin wallets, 8B bank accounts, and 15B cards across 140 countries, and a March 30, 2026 announcement frames the offer for paying remote overseas teams, freelancers, and gig workers.

That matters when your problem is method mix by market. If some recipient groups need wallet payout while others need bank deposit, Thunes presents a multi-rail model worth testing.

Its integration posture is also worth noting. Thunes presents a single API model, and Money Transfer API v2 is positioned as the gateway to initiate and retrieve transfer transactions.

Where the fit is strongest#

The clearest fit is scaling contractor and workforce payouts across regions where payout preferences vary by country. Thunes also cites adjacent use cases such as overseas payroll, international gig-working platforms, e-commerce refunds, and insurance claims, which suggests broader applicability than one payout pattern.

For this use case, the key diligence question is corridor-level fit. Can your exact recipient cohorts be paid on the right rail in the right country without splitting operations across multiple providers?

What should make you cautious#

The public materials in this set do not provide verified detail on retries, webhook guarantees, or reconciliation exports. You should treat that as a diligence gap, not proof that those capabilities will meet your operating requirements.

There is also a visibility limit before contract: Thunes states that specific endpoint details are provided upon account creation. The same docs note that non-breaking API changes may be introduced without prior warning, so integration resilience should be planned explicitly. Public docs list 2 environments: production and pre-production.

Reach figures also vary across materials, including 4B, 8B, and 12 billion in different contexts. Read these as context-specific claims, not one normalized metric.

What to ask for before you sign#

Ask for an evidence pack tied to your real corridors:

- A country-by-method matrix for your recipient types, split by bank account and mobile wallet

- A Money Transfer API v2 lifecycle example from request to final status in pre-production

- Written guidance on handling API changes where non-breaking updates can ship without prior warning

- A finance-facing example of how failed, returned, or unresolved payouts are surfaced for review

If Thunes can prove corridor fit and operational visibility, it is a strong expansion candidate. If not, broad reach claims may still leave your finance and engineering teams with avoidable post-launch uncertainty. For the US banking rail angle, see ACH Payment Processing for Platforms: How to Move Money via the US Banking Network.

Dots for Affiliate and Commission-Heavy Programs#

Dots is a shortlist candidate when your core problem is recurring affiliate commissions at monthly volume. Its clearest fit is programs that need to pay large, changing recipient groups in a single run.

This is more than generic payout sending. Dots frames its affiliate offering around scaling referral-program payouts, with global rails, tax automation, and white-labeling in one API. That focus is relevant when creator, influencer, and partner cohorts change month to month.

Why the fit is strongest#

Batch execution is the main reason to evaluate it. Dots says you can send thousands of payouts with one API call or CSV upload, and launch via CSV, API, or webhook-triggered automation. That gives finance a manual fallback while engineering builds deeper integration.

Its affiliate content also matches the real operating pattern: programs that may owe commissions to 5,000 affiliates every month. Evaluate it for dynamic cohorts and payout-method shifts, not for one stable payroll-style list.

Method coverage claims line up with common affiliate needs as well: local bank transfers, ACH, PayPal, Venmo, wires, and more, plus a separate claim of 150+ currencies and 190+ countries. If you run both US and international cohorts, test those claims against your actual recipient mix.

What makes it attractive for operators#

Dots defines a payout as a transfer from a user's Dots wallet to an external account, such as a bank account. That signals a wallet-based money movement model you should map to your treasury, funding timing, and ledger workflows before launch.

Dots also says real-time dashboards surface exceptions, retries, and approvals in one place. For commission cycles, that is exactly the area to validate, because post-batch exception handling can be harder than initiating the batch.

What you still need to prove#

Public pages do not show enough depth on compliance controls, API behavior, duplicate prevention, or payout exception recovery. They also do not document a webhook delivery SLA or exact partial-batch failure handling.

Treat scale metrics as directional, not normalized benchmarks. Dots pages cite 1M+ payees and 190+ countries, but annual volume figures differ across pages: $1bn+, $1.3B, and $1.5bn.

Before signing, ask for an evidence pack from one real monthly commission cycle:

- A sample CSV and matching API request for the same payout run

- Status trails for successful, failed, and retried payouts

- Finance-facing reconciliation outputs for approvals, exceptions, and completed disbursements

- Written handling for stale recipient details, returned payouts, and unresolved items

Wise also lists affiliate commissions as a standard bulk-payment use case, so this is a common category pattern. Prefer Dots only if it proves the affiliate-specific fit and CSV/API flexibility in your workflow. If retries, duplicates, and recovery remain unclear, keep it in pilot mode. Related reading: Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

PayQuicker for Automated Global Bulk Disbursement Flows#

PayQuicker can be a shortlist option when you want a more unified global bulk disbursement flow instead of stitching together separate local payout processes. Its clearest fit appears to be teams that need to run hundreds or thousands of payments in one coordinated run, with both file-based and API-based execution paths.

Where the fit is strongest#

PayQuicker explicitly frames global mass payouts as automated bulk disbursements for high-volume worldwide runs. It also defines batch payments as grouped transactions submitted by file or API instruction, which is useful when finance needs batch operations and engineering wants API integration.

Its public product positioning describes a mixed operating model: bulk uploads, single payments, or API integration. The developer materials also state support for batch file upload and full API integration to back-office or wallet-linked workflows.

PayQuicker's homepage claims broad reach and maturity, including 210+ countries and territories, 80+ currencies, and 18+ years in business. Treat these as vendor claims to validate against your actual recipient and method mix.

What to verify before committing#

PayQuicker's public messaging emphasizes instant and compliant outcomes, and its trust-center content states security, compliance, and privacy controls plus a compliance program aligned with legal and regulatory obligations. That helps, but it does not de-risk live operations on its own.

Before you commit, ask for evidence from one real payout run:

- Matching batch file and API payload for the same payout set

- Status outputs showing completed, rejected, and in-review items

- Reconciliation outputs finance can map to source instructions

- Written handling for returned funds, stale recipient details, and duplicate submissions

- Incident escalation terms and any applicable support SLA language

The reviewed public excerpts do not document partial-batch failure behavior, return handling, retry semantics, or verified SLA terms. If exception recovery speed is critical to your close process, treat those as open risks until documented.

Wise and WePay Signals for Platform Payout Reliability#

Use Wise and WePay as benchmark signals, not standalone proof of payout reliability. They show what platform-oriented vendors should be able to demonstrate on API posture, support framing, and platform context, but verify failure handling and recovery performance independently before committing to a platform.

Wise#

Wise provides an integration-readiness signal. Its platform API is documented as REST-based payment infrastructure access, and its docs also reference ongoing enterprise-grade technical support. For vendor evaluation, that sets a practical baseline. Your engineering team should be able to run payout operations programmatically, not only through manual dashboard steps.

Wise also claims coverage for 160+ countries and receiving in 40+ currencies, which is useful for global-fit scoping. But those claims do not confirm exception handling, duplicate controls, or recovery behavior. In diligence, ask for the exact payout status model, webhook or event coverage if used, and reconciliation output tied to one submitted payout set.

WePay#

WePay is mainly a platform-context signal. Chase media describes WePay as infrastructure that helps software platforms provide integrated payments processing, WePay support states it is part of J.P. Morgan Payments, and J.P. Morgan describes WePay integration into its payments platform as ongoing. That can matter if your shortlist prioritizes embedded-payments alignment and long-term platform backing.

The scale references are meaningful but historical. A Mar 06, 2018 Chase release cites more than 1,000 platforms, including GoFundMe and Meetup, and the October 17, 2017 acquisition release frames WePay around software-platform integration. Treat that as platform narrative, not current operational proof.

When a vendor leans on these kinds of signals, ask for the missing evidence directly:

- Payment and payout state definitions

- Rejected-item and returned-fund handling

- Escalation path and support terms

- Reconciliation outputs for stuck or failed items

That is the difference between a strong platform story and a provider you can run at close.

Tremendous for Fast Setup on Common US-Friendly Methods#

Tremendous is a strong fit when speed and recipient familiarity matter more than broader payout complexity. For incentive, rebate, and reward programs that need quick rollout on ACH, PayPal, or Venmo, it is a practical shortlist option. For cross-border operations, exception handling, and finance-close depth, the public material still leaves gaps you should validate directly.

The setup posture is clear. Tremendous positions bulk payouts as easy to start and offers three delivery paths for scale: API, bulk uploads, and 5k+ integrations. It also supports multi-option rewards, so recipients can choose from a configured payout set instead of being hard-routed to one method.

| Method | Delivery window | Scope shown |

|---|---|---|

ACH bank transfer | 2-4 days | US + Puerto Rico |

Venmo | 1-3 days | US-based users, US + limited territories |

PayPal | 1-3 days | 114 countries supported |

That method detail is enough to scope a first US-friendly launch, but not enough to treat as full cross-border readiness. Tremendous also says it can send monetary payouts worldwide, so confirm a live method-by-country map for your recipient mix before committing.

For finance and ops diligence, ask for exact monetary fee treatment and a real audit-trail example covering W-9 collection, approvals, and order review. Pricing language states Venmo, PayPal, Cash App, and bank transfers may incur a 4-6% fee, which can materially change unit economics at volume.

Plan for reversals upfront. Tremendous says payouts successfully sent to PayPal, Venmo, Cash App, or bank accounts cannot be recalled. If recipient details or approvals often change late, tighten review gates before release. Also verify current option counts directly, since public pages show both 2,000+ and 2,500+ figures.

When Gruv Is the Better Fit for Control and Traceability#

Gruv is the better fit when payout risk is less about speed and more about control, visibility, and audit readiness across each run. If your team needs clear lifecycle evidence from request through status updates and reconciliation, prioritize that operating model over fastest setup.

A practical decision rule helps here. If duplicate payouts, unclear approvals, or month-end reconciliation pain are costly, favor idempotent API behavior to reduce duplicate-request risk, plus webhooks for asynchronous status visibility. That is usually the safer choice for recurring contractor, creator, or marketplace payout cycles where retries and exceptions are routine.

Gruv positions this model around real-time updates, webhook notifications, detailed audit trails, configurable approval routing, automated compliance checks, and ERP-compatible reconciliation exports. For cross-border contractor payouts, this is typically where finance and engineering both benefit from a more unified operating view instead of fragmented status tracking.

Before go-live, align payout execution to your internal gates:

- Confirm how idempotent retries are handled in your integration path

- Map approval rules to policy owners before release

- Validate compliance checks and tax-document steps for your program

- Test reconciliation exports in your finance close workflow

Implementation Sequence for Your First Production Batch#

Your first production batch should optimize for traceability, not volume. If failure rates exceed what your team can absorb, pause expansion and fix data quality and retry handling before the next run.

| Stage | Main focus | Grounded checks |

|---|---|---|

| Prepare recipient data | Keep an auditable payload | Include internal recipient ID, amount, currency, payout rail, and exact destination detail used at execution; ACH failures can include R03 |

| Validate payout method first, then batch behavior | Separate rails early | Bank-account payouts can fail on routing accuracy or account status, while wallet payouts can fail on recipient identifier quality |

| Dry-run in sandbox and prove traceability | Link client batch identifier, idempotency key, and provider response reference | One payouts API rejects reused sender_batch_id values from the last 30 days; on HTTP 5xx it allows retry with the same batch ID |

| Execute live with webhook logging and an exception ledger | Assume asynchronous updates | Webhooks can be retried for up to three days; PAYOUTSBATCH webhooks do not include item-level details |

| Close reconciliation before scaling | Do not mark the run complete at accepted | Minimum evidence pack: batch request IDs, webhook event logs, an item-level exception ledger, and a close report |

- Prepare recipient data

Start with a recipient payload you can audit later: internal recipient ID, amount, currency, payout rail, and the exact destination detail used at execution. This matters because some payout APIs do not immediately validate all payout item values at batch creation, so bad data can be accepted and fail later.

For bank-account payouts, check for stale or mistyped routing and account details. ACH failures can include R03 when an account is closed or cannot be located. For wallet rails, validate required destination details, such as phone number format, before go-live.

- Validate payout method first, then batch behavior

Method choice changes failure modes. Bank-account payouts can fail on routing accuracy or account status, while wallet payouts can fail on recipient identifier quality even when batch submission succeeds.

If you support multiple rails, run them separately in early production so you can isolate whether issues are rail-specific, data-specific, or provider-specific.

- Dry-run in sandbox and prove traceability

Use sandbox to test request formation, webhook ingestion, and exception handling before funds move. The goal is not only "request succeeded," but a complete trace linking your client batch identifier, idempotency key, and provider response reference.

Test exact retry behavior before production incidents. For example, one payouts API rejects reused sender_batch_id values from the last 30 days. On HTTP 5xx responses, it allows retry with the same batch ID.

- Execute live with webhook logging and an exception ledger

Assume asynchronous updates in production. Webhooks can be retried for up to three days, so handlers must be replay-safe and avoid duplicate processing.

Log all webhook events, but do not treat batch-level webhooks as item-level truth. In that same API, PAYOUTSBATCH webhooks do not include item-level details, so use follow-up item lookups to maintain an exception ledger by payout item.

- Close reconciliation before scaling

Do not mark the run complete at "accepted." Mark it complete when bank payouts, provider statuses, failed items, and your internal ledger align.

Your minimum evidence pack for batch one is simple: batch request IDs, webhook event logs, an item-level exception ledger, and a close report. If reconciliation drift appears early, pause, fix data checks and retry policy, then scale volume. This pairs well with our guide on SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For.

Red Flags and Contract Terms to Set Before You Sign#

Do not sign until coverage constraints, duplicate controls, webhook behavior, and reconciliation outputs are written into the contract or an attached schedule. If those terms stay vague, production risk shifts to your team.

| Term | Require | Grounded example |

|---|---|---|

| Coverage matrix | Written country, currency, and method matrix for your actual payout mix | One provider documents Venmo as US-only and notes separate API calls per currency type |

| Support escalation | Named severity levels, support entry points, escalation ownership, and incident update expectations | Do not treat technical docs as incident commitments unless those terms also appear in the commercial agreement |

| Retry and webhook rules | Idempotency, duplicate batch handling, acknowledgment rules, retry windows, and duplicate-event handling | One payouts API rejects reused sender_batch_id values from the last 30 days; Wise retries can back off from 1 minute to 24 hours; Stripe may resend undelivered events for up to three days |

| Reconciliation artifacts | Item-level batch detail access, downloadable reports, and audit-friendly exports | Stripe notes payout reconciliation reports are available only with automatic payouts enabled |

- Coverage matrix, not brochure copy

Require a written country, currency, and method matrix for your actual payout mix, not a generic "global payouts" claim. Exclusions and restriction rules can block payouts, some methods are country-specific, and some APIs require separate calls by currency. For example, one provider documents Venmo as US-only and notes separate API calls per currency type. Practical checkpoint: send your top corridors and methods and require each one to be marked supported, restricted, or unsupported before signature.

- Defined support escalation and incident-response terms

"Support included" is not enough for payout operations. Require named severity levels, support entry points, escalation ownership, incident update expectations, and what evidence the vendor must provide when a batch fails or stalls. Do not treat technical docs as incident commitments unless those terms also appear in your commercial agreement.

- Retry, duplicate prevention, and webhook rules in writing

Make retry safety explicit in both contract language and implementation requirements: idempotency, duplicate batch handling, webhook acknowledgment rules, retry windows, and duplicate-event handling. Key controls to verify: one payouts API rejects reused sender_batch_id values from the last 30 days; Wise treats webhook delivery as successful only after HTTP 200 and retries can back off from 1 minute to 24 hours; Stripe warns events can be delivered more than once and may resend undelivered events for up to three days. Verification step: require a sandbox or live demo that retries the same request after a timeout and shows the exact fields proving no duplicate execution.

- Reconciliation artifacts and production references

Do not accept dashboard visibility as reconciliation evidence. Require item-level batch detail access, downloadable reports, and audit-friendly exports up front. Ask to see the exact artifact set: item-level payout details tied to a batch reference such as payout_batch_id, payout reconciliation reports where available, and audit report exports. Confirm eligibility limits in advance, for example Stripe notes payout reconciliation reports are available only with automatic payouts enabled. Also request production references that match your payout pattern, whether marketplace, creator, or affiliate disbursements, and treat this as ongoing risk management, not a one-time onboarding checklist.

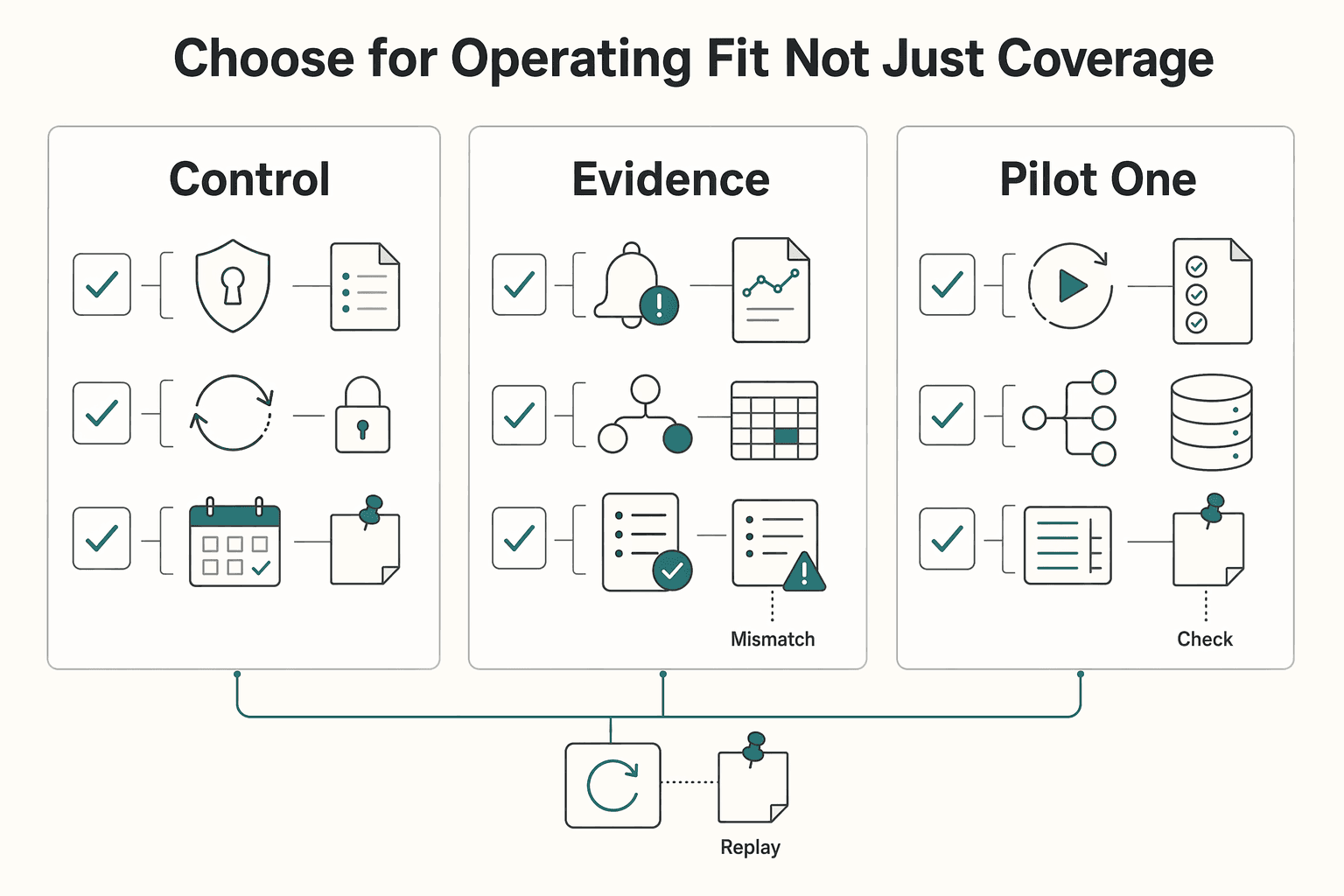

Choose for Operating Fit Not Just Coverage#

Choose the provider your team can run and recover under pressure, not the one with the broadest coverage slide. If several options look similar, break ties on operating fit: retry safety, asynchronous failure handling, and reconciliation your finance team can actually use.

- Score recovery controls above headline reach.

One major payouts API documents up to 15,000 payments per call, but capacity alone does not show whether your team can recover from partial failures without duplicates. Weight idempotency, async event handling, and payout reconciliation outputs more heavily than corridor count or batch-size claims when payout errors are costly.

- Require evidence before signing.

Use a weighted comparison with a short proof checklist for each score: country and method fit, duplicate prevention, async event visibility, reconciliation artifacts, and escalation clarity. Ask every vendor for the same evidence set: corridor and method matrix, webhook event catalog, sample payout reconciliation export, retry behavior, and a failed-then-retried sandbox batch demo. A critical checkpoint is rerunning the same request after a forced timeout and confirming idempotent behavior with no duplicate payout. Stripe also notes most webhook events are asynchronous, so treating the initial API response as final can leave failures unresolved in your system.

- Pilot one flow, then expand canary-style.

Start with one production payout path, move a small percentage first, and instrument it end to end: request ID, provider batch ID, item statuses, webhook receipts, failed or returned items, and the reconciliation export used at close. Expand only when you can trace each item to final state and tie batch totals back to reconciliation output. This aligns with lifecycle third-party risk management, with controls sized to your risk and complexity.

The decision is not "who covers the most." It is "who can we operate reliably." Run the weighted comparison, verify the evidence pack before signature, pilot one flow in sandbox and controlled production, and scale only when exception handling and reconciliation are stable.

Before scaling beyond a pilot batch, align engineering and finance on idempotent retries, compliance gates, and reconciliation artifacts using the implementation details in Gruv Docs.

Frequently Asked Questions

What is a bulk payout platform for thousands of payments?

A bulk payout platform sends high-volume outbound payments to many payees at once instead of one-by-one transfers. In practice, strong implementations include batch references, item-level statuses, failure notifications, and finance-reconciliation outputs. Without those artifacts, you may have send capacity but limited operating control.

How do platforms send thousands of payouts in a single run without creating duplicates?

The core control is retry safety, so a retried request does not create a second payout. Stripe documents idempotent requests, one payouts API rejects a sender_batch_id reused within the last 30 days, and Dots rejects transfers that reuse an idempotency key. Before go-live, rerun the same batch after a forced timeout and confirm the provider reuses or rejects by the original reference rather than executing a second payment.

What should we compare first between `Thunes`, `Dots`, `PayQuicker`, `Wise`, and `Tremendous`?

Start with your real country-and-method mix, then compare each vendor’s documented fit for that mix. Thunes markets payout reach across 140 countries, Dots markets bank-account payouts over ACH and RTP with idempotency controls, PayQuicker positions automated global bulk disbursements, Wise documents batch groups of up to 1000 transfers, and Tremendous advertises ACH, Venmo, and PayPal. If coverage looks similar, prioritize the vendor that can show clear failure events, duplicate controls, and reconciliation outputs.

Which payout methods should we support first across `ACH`, `PayPal`, `Venmo`, `mobile wallets`, and `bank accounts`?

There is no universal method order for every platform. Start with the methods your recipients can actually complete in your highest-volume corridors, then expand. Grounded examples include Tremendous support for ACH, Venmo, and PayPal, one payouts product supporting PayPal and Venmo recipients, and Dots support for ACH and RTP bank transfers.

What usually breaks at scale during batch payouts, and how do we contain it?

Recipient account-data errors and return handling can become failure points when volume increases. Nacha flags administrative and overall return-rate levels at 3.0% and 15.0%, and return codes like R02, R03, and R04 are relevant operational signals. Contain risk by validating recipient data before release, monitoring asynchronous failures through events such as PAYMENT.PAYOUTS-ITEM.RETURNED and Wise transfers#payout-failure, and pausing expansion when return patterns worsen.

What vendor details are still unknown from marketing pages, and what should we demand before signing?

Marketing pages usually do not answer your exact country-by-method coverage, pricing, partial-failure handling, support escalation terms, or finance-ready report outputs. Require a written coverage matrix for your top corridors, webhook event catalogs, duplicate and retry rules, sample item-level exports, and a live failed-and-retried batch demo. Also confirm the exact product path you are buying, because one payouts product documents up to 15,000 payments per API call, 5,000 payments per CSV file, and Standard Payouts to 96 countries.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/12.206trusted

- developer.paypal.com/docs/api/payments.payouts-batch/v1trusted

- developer.paypal.com/docs/payouts/standard/payouts-webtrusted

- docs.stripe.com/api/idempotent_requeststrusted

- docs.stripe.com/webhookstrusted

- fdic.gov/sites/default/files/2024-03/pr23047a.pdftrusted

- occ.gov/news-issuances/news-releases/2023/nr-ia-2023...trusted

- occ.gov/news-issuances/news-releases/2023/nr-ia-2023...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: