Quick Answer

Yes. accounting automation platforms eliminate manual journal entries close faster when they replace spreadsheet prep, email approvals, and rekeying into the GL with controlled posting flows. Start with repeatable accrual and auto-reversal work, keep disputed or incomplete items in an exception queue, and require records for source transaction IDs, approval history, posting logs, and final disposition in the ERP.

Why Platform Finance Teams Automate Accounting#

Treat manual journal work as a chain, not a single task#

If you are asking whether reducing manual journal entries helps you close faster, the short answer is that it can, especially when automation removes the handoffs around journals, not just the typing. Manual journal work is rarely just someone typing into the General Ledger. It is often a chain of accruals, spreadsheet handoffs, approval waits, reconciliation checks, and final ERP posting that turns month-end close into one of the most time-sensitive and resource-intensive jobs in finance.

That chain matters because partial automation can look impressive while leaving the real bottleneck untouched. You can auto-create journal entries and still lose time if finance is waiting on offline files, missing source data, or late approvals. Many companies still rely on manual accounting processes that consume time and increase error risk. That drag does more than slow accounting. It also limits timely financial insight, which can slow decision-making across the business.

Scope the problem to platform payment operations#

This guide is for teams running contractor, creator, marketplace, or embedded-payments flows, where finance depends on product events, payout statuses, provider updates, and ERP imports lining up cleanly. In that environment, journal automation is not just an accounting feature. It sits between your source transaction data and your close process, so upstream assumptions often show up as noisy exceptions at month end.

Start with a simple checkpoint. Trace one journal from source event to posted entry without using a spreadsheet that lives on someone's desktop. If you cannot do that today, your close pain is probably coming from handoffs and missing evidence as much as from manual entry itself. A common failure mode is thinking the problem is finance rekeying when the real issue is inconsistent source data, unclear ownership, or reconciliation breaks that surface only near close.

Decide what should automate first and what should stay reviewed#

The goal is not a hands-off close. It is to move repetitive accounting work out of manual queues so your team can spend time on policy judgments, material exceptions, and investigation. Repetitive tasks like data entry, transaction coding, and reconciliation are the right place to start. Entries that depend on unusual business context, disputed transactions, or unclear timing usually still need human review.

By the end of this guide, you should have three decisions made. First, which journal family is repetitive enough to automate first, often accruals or other high-volume entries. Second, which exceptions must stay in an approval path because they carry real accounting risk. Third, how you will verify that improvement is real: fewer manual touchpoints, fewer reconciliation breaks, fewer late adjustments, and a cleaner month-end close, not just more entries posted automatically.

That discipline matters because better tooling does not automatically produce better decisions. Workday has reported that 50% of finance leaders still make gut-based decisions because data is siloed or not readily available. The test is not whether the software posts faster. It is whether your team can close with less manual effort and more trust in the numbers. Related: What Is an Accounting Cycle? How Payment Platforms Should Structure Month-End and Quarter-End Close.

What eliminating manual journal entries actually means in practice#

Eliminating manual journal entries means removing rekeying and handoff work, not removing finance judgment. In practice, approved source events generate entries, those entries post to the General Ledger (GL) without manual re-entry, and people focus on policy decisions and material exceptions.

Define the target state#

Use a testable standard for each in-scope flow: you can trace an entry from source event to GL post, confirm its approval history, and match it in reconciliation without pulling an offline spreadsheet.

If your team still copies values into Excel templates, attaches support files, and emails approvals before posting, the manual process is still in place. Redwood's point is that some "automated" setups hide that upstream labor behind a cleaner interface.

Separate typing from judgment#

"No typing" is not the same as "no judgment." Repeatable entries, including accruals and auto-reversal journal entries, are often good automation candidates once triggers, account mapping, and reversal timing are agreed.

Keep material exceptions in approval workflows, especially when entries involve disputed transactions, missing source data, or unclear cut-off. A common failure mode is automating the standard path while exceptions pile up offline near close.

Measure close speed as an outcome#

Treat "faster close" as an operational result you verify, not a vendor promise. The checks are straightforward: less GL rekeying, fewer spreadsheet-based reconciliations, and tighter reconciliation flow.

That standard matters because Redwood-sponsored findings published March 17, 2026 reported that 97% of organizations still rely on people to complete close, only 2% report a fully automated end-to-end process, and 86% still reconcile in spreadsheets. The win is fewer manual handoffs surviving into month-end, not just a higher count of auto-posted entries. Related reading: Choosing Value Pricing for Accounting and Bookkeeping Services.

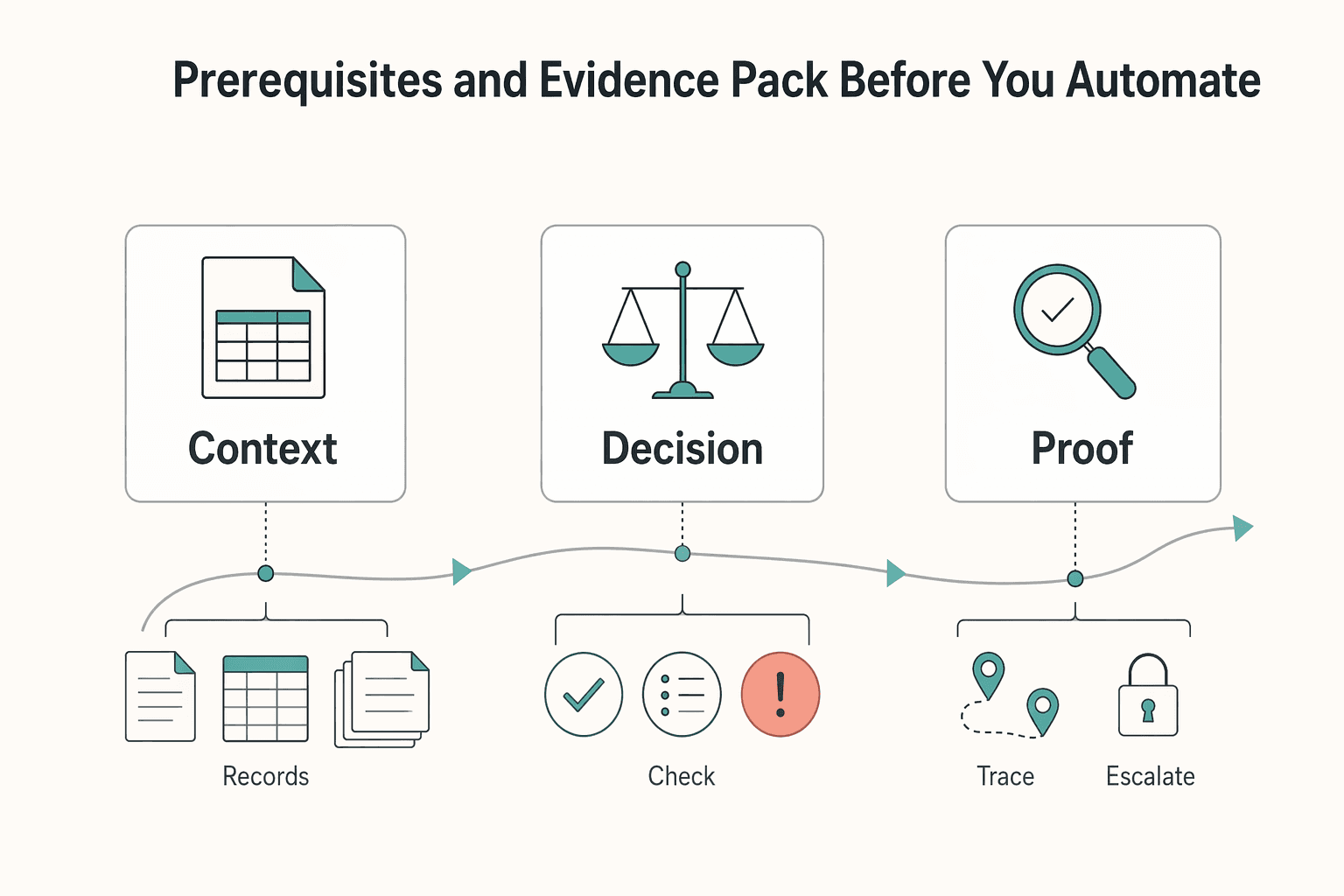

Prerequisites and evidence pack before you automate#

Before you change tooling, build an evidence pack for the current close. The goal is simple: make automation reduce manual work you can verify, not just move it around.

Step 1: Build a baseline pack for the current close. Document each in-scope journal path end to end. Capture manual touchpoints, late adjustments, reopen reasons, and reconciliation breaks by journal type. Keep it specific: which spreadsheet is used, who rekeys into the General Ledger (GL), what support is attached, and what usually triggers post-entry corrections.

Use this baseline as your control sample when you run a close stress test and parallel reporting before full rollout.

Step 2: Confirm system boundaries and owners. Map where the source event starts, where posting decisions are made, and where the final entry lands in the Enterprise Resource Planning (ERP) system. Assign clear owners at each layer: ERP admins (posting access and import behavior), product/engineering owners (event creation and data quality), and finance owners (posting policy, approval tiers, and period rules).

If ownership overlaps or exception decisions have no owner, fix that before automation design.

Step 3: Inventory audit artifacts up front. For each in-scope entry, confirm you can retain source transaction IDs, approval history, posting logs, and exception disposition records. You should be able to answer four questions from records, not memory: what triggered the entry, who approved it, when it posted, and how exceptions were resolved.

Software can handle reconciliations and journal-entry tasks, but it cannot reconstruct missing evidence later.

Step 4: Set non-negotiables in writing. Define a single source of truth for postings. If entries can be edited from multiple channels at once (spreadsheet upload, side tool, and ERP), you do not have control. Define controlled exception queues too, with visible ownership for every failed or out-of-policy item.

Document approval thresholds and approval tiers before build starts. In practice, platform design is an operating-model decision: who does what, when, with which approvals, and under which audit trail. This matters because disconnected systems are a known source of finance-team drag.

Choose your architecture based on volume risk and ERP maturity#

Choose the architecture based on where manual risk begins, not where posting ends. If most close pain sits in one journal family (for example, accruals), start with point automation in the Accounting Journal. If pain spans approvals, intercompany, reversals, and reconciliation before ERP posting, start with end-to-end orchestration from source event to ERP post.

Decision rule: point-first vs end-to-end#

Point-first automation is the faster, narrower path: automate one journal stream with tighter posting rules and lighter integration effort.

End-to-end orchestration is the broader control path. Redwood describes orchestration from data acquisition through posting, and Trintech describes a close lifecycle where reconciliations, journals, approvals, and tasks are connected and traceable. If your failures start upstream in approvals, spreadsheets, source quality, or exception handling, this is usually the better fit.

Use this rule:

- Go point-first when one journal family drives most of the manual workload.

- Go end-to-end when delays and reopen work cross teams and control points.

Sanity-check "automated" claims before you commit#

Treat Brex, Redwood, and other vendor demos as hypotheses to test against your current process. Redwood's own framing is that many tools automate only the last 20-30%, while the first 70-80% can remain in spreadsheets and email.

Validate four items from your evidence pack:

- Where source data is prepared: if teams still export, reshape, or merge files, core risk is still manual.

- How exceptions are handled: out-of-policy items should pause, route, and log in a controlled queue.

- Whether traceability is complete: each posted line should map to a source event and approval record.

- Who owns reversals and replay: unclear ownership here causes drift and duplicate corrections.

Your pass/fail check is not "did it post?" It is whether source transaction ID, approval history, posting logs, and exception disposition all survive into ERP records.

Go or no-go table#

| Criteria | Point automation in Accounting Journal | End-to-end orchestration to ERP | Go or no-go signal |

|---|---|---|---|

| Integration effort | Lower initial effort for a narrow journal scope | Higher effort across source events, approvals, and ERP behavior | Go point-first if upstream data is not ready but ERP posting rules are stable |

| Exception handling depth | Usually limited to posting/journal validation | Can cover pre-post exceptions, approval pauses, and replay | No-go point-first if delays mostly come from upstream exceptions |

| Audit traceability | Strong at post level, weaker if upstream prep stays manual | Stronger when source event through reconciliation is connected | Go end-to-end if evidence breaks before the GL |

| Close-cycle impact confidence | Higher when one journal family dominates close effort | Higher when close drag spans multiple handoffs/teams | No-go point-first if reopen reasons are mostly approvals/reconciliation |

Do not pick architecture on feature density alone. Pick the option that preserves a single source of financial truth and removes manual work before posting, not only at posting.

For a step-by-step walkthrough, see Merchant of Record for Platforms and the Ownership Decisions That Matter.

Map payout and money-movement events to clean journal logic#

A shared event-to-journal map is the control point that removes manual close work. Without it, manual effort usually reappears in reconciliation, spreadsheet fixes, and late adjustments.

Define the accounting moment for each operational event#

Start with lifecycle events, then map journals. Finance data often sits across multiple systems and inconsistent formats, which is exactly what slows journal entry and reconciliation, so each event needs a clear accounting role: informational, obligation-creating, or settlement-confirming.

In Gruv-style flows, this usually means mapping invoice confirmation, payout status changes, asynchronous provider updates, and deposit matching to distinct posting outcomes. Finance defines where accrual starts and clears; engineering confirms the authoritative event and idempotent replay behavior so retries do not duplicate entries.

If an event can arrive late or be corrected, do not let that first signal post final cash by itself. Use it to open an accrual or payable state, then complete, reverse, or reclassify when the confirming event arrives.

Translate lifecycle states into journal behavior and reversal rules#

Use one sign-off table that finance and engineering both approve before production posting:

| Lifecycle event | Finance outcome to decide | Journal behavior | Verification before post |

|---|---|---|---|

| Invoice confirmed | Obligation recognized or not yet recognized | Create accrual or payable if policy requires it | Source transaction ID and approval history are present |

| Payout marked sent | Cash movement initiated, not final | Move to pending/in-transit state if policy requires it | Provider reference is captured and idempotency check passes |

| Provider confirms paid | Obligation settled | Finalize settlement and clear prior balance | Status is final, not only submitted/queued |

| Return or failure update | Prior settlement no longer valid | Reverse or reclassify prior entry per policy | Link to original journal is preserved |

| Bank deposit matched | Cash confirmed | Clear unmatched/in-transit balance | Amount, date, and reference align with source records |

Keep auto-reversal logic explicit. Reversal drift is a common failure mode when accruals post automatically but clearing triggers are inconsistent.

Lock required dimensions before ERP import#

Define dimensions in the mapping, not during import. If ERP posting requires department, class, location, entity, or similar reporting segments, each in-scope event needs a deterministic source rule and a missing-data rule.

This is especially important in multi-entity ERP setups across subsidiaries, divisions, or geographies. If event context cannot reliably identify the right reporting slice, fix the source design before posting. Otherwise, spreadsheet-based reconciliations grow, close takes longer, and accuracy drops.

Put edge cases in scope before go-live#

Include exception paths in v1 of the map: unmatched deposits, returned payouts, and delayed confirmations. For each case, define whether posting pauses, whether reversal/reclassification can run automatically, and who owns the exception queue.

This is where governed workflows matter: integrating ERP, payroll, and subledger data while automating validation, approvals, and posting with traceability intact.

Before production, require one signed mapping artifact approved by both finance and engineering. If both teams cannot sign, the posting logic is not ready.

Build controls that speed close instead of slowing it down#

Once your event-to-journal map is approved, controls should stop risky entries, not every entry. If every batch needs the same review, you have not removed manual work in data entry, transaction coding, and reconciliation; you have delayed it into close.

Tier approvals by risk#

Approve by risk, not by journal volume. Low-risk entries from approved source events with complete dimensions and clean validation should flow through with minimal review. Higher-risk entries, such as missing attributes, unexpected reversals, or source-to-settlement mismatches, should pause for decision.

A control is only real if you can verify it from logs. For each posted entry, you should be able to trace source transaction ID, assigned risk tier, approval requirement, approver (if required), and ERP posting result.

Narrow exception queues to true anomalies#

Exception queues should contain only items that can cause wrong posting or require policy judgment. Route issues like missing source IDs, duplicates, failed idempotency checks, amount mismatches, or failed document validation; keep expected lifecycle timing changes out of the queue.

If finance is treating the queue like a daily inbox, the rules are too noisy. Each exception should carry an owner, reason code, and clear disposition: corrected, approved, reversed, or rejected.

Use IDP for intake, then validate before ERP posting#

Use Intelligent Document Processing (IDP) to extract and organize document data where invoices or receipts are part of the flow. That helps when accruals are recorded before all supporting documentation is available, but extraction is not a posting decision.

Treat IDP as intake, then run deterministic checks before ERP posting. OCR/ICR-era tooling could digitize text, but could not categorize, analyze, or validate data reliably enough on its own. Your evidence chain should still show source event ID, document ID, extracted fields, validation result, approval history (if any), and final ERP journal ID.

If billing complexity is part of the issue, see Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning. It covers the upstream billing workflows that often create downstream accounting work.

Roll out in phases with hard verification gates#

Do not scale all journal families at once. Roll out in phases, and expand only after two stable close cycles with clean, traceable audit trails.

| Step | Action | Verification gate |

|---|---|---|

| Step 1 | Pilot one high-friction journal family | Confirm a clear before/after delta in close effort and error correction, with evidence your team can review quickly |

| Step 2 | Connect posting and reversal into NetSuite or your current ERP | Verify pairing across source event IDs, ERP journal IDs, planned reversal timing, and executed reversal records |

| Step 3 | Harden controls before adding harder cases | Watch for three signals across consecutive closes: exceptions stay focused on true anomalies, approvals stay within your close window, and reopen reasons trend down |

| Step 4 | Scale out only after two stable close cycles | Expand only after two consecutive closes hold up under review, and require real-time audit trails that connect source event, automated journal entry generation, approvals where needed, ERP result, and reconciliation outcome |

Step 1. Pilot one high-friction journal family. Start with one repeat-heavy family (often accruals) and keep scope tight enough to measure. Your gate is not just successful posting. Confirm a clear before/after delta in close effort and error correction, with evidence your team can review quickly.

Step 2. Connect posting and reversal into NetSuite or your current ERP. Move from file handoffs to direct posting and reversal flows. For each cycle, verify pairing across source event IDs, ERP journal IDs, planned reversal timing, and executed reversal records. If reconciliation still depends on offline edits, the manual risk has only moved.

If you are implementing NetSuite, use this deeper checklist: How to Integrate Your Payout Platform with NetSuite: Sync Journal Entries and Close Books Faster.

Step 3. Harden controls before adding harder cases. Before expanding scope, tighten exception queues, approval timing expectations, and reopen-rate thresholds so they are explicit and reviewable. Watch for three signals across consecutive closes: exceptions stay focused on true anomalies, approvals stay within your close window, and reopen reasons trend down because rules are improving.

Step 4. Scale out only after two stable close cycles. Expand to more entities or volume only after two consecutive closes hold up under review. Require real-time audit trails that connect source event, automated journal entry generation, approvals where needed, ERP result, and reconciliation outcome. That phased gate is what turns automation into continuous compliance and audit support, not just faster posting.

Common failure modes and how to recover fast#

When a rollout stalls, recover by fixing the break at the source instead of layering on more manual journal entries. More than half of a typical month-end close depends on journal entries, so upstream process gaps quickly affect the whole close.

Failure mode 1: "Automated" posting still depends on offline spreadsheets. Recovery: remove pre-post manual handoffs, not just the final upload. If entries still start in Excel templates, email approvals, or side-file cleanup, move preparation, approvals, and support into one controlled flow. The practical test is simple: trace posted entries to source records and approval history without opening a separate inbox or spreadsheet.

Failure mode 2: Broken mappings drive wrong GL coding. Recovery: pause that journal family, correct mapping logic, and then resume with controlled reprocessing. Do not treat hand edits in the ERP as a fix, because the same mapping error will recur. Keep a clear record of impacted entries, what was wrong, what changed, and final disposition so the audit trail stays usable.

Failure mode 3: Reversal timing drift creates close noise. Recovery: treat reversal handling as a primary control, not cleanup. Track original and reversal entries as a pair each close cycle so finance can separate timing issues from real business activity.

Failure mode 4: Exceptions accumulate near close. Recovery: triage early with clear reason codes, explicit ownership, and escalation inside approval workflows. Manual processes do not scale well and backlogs are a common outcome, so the queue should hold true anomalies, not routine unresolved work.

For a broader operations view, read Business Process Automation for Platforms: How to Identify and Eliminate the 5 Most Expensive Manual Tasks. It complements the finance-specific workflow changes covered here.

Want a quick next step? Try the free invoice generator.

Final checklist to shorten close without losing control#

Use a proof-first checklist before you scale: shorten close only when speed and control both hold.

Step 1#

Define the target state clearly and align finance and engineering on it. In practice, that means in-scope journal work posts from approved source events, while exceptions that need judgment still get explicit human review.

Be strict about what "automated" means: it should be traceable and reviewable, not just rekeyed through a different interface. That standard matters because close teams can still carry manual work even with modern tooling.

Step 2#

Approve your control and evidence requirements before live posting. You should be able to trace posted results back to source records and show approvals and reconciliation support without relying on side spreadsheets or inbox threads.

If that evidence path is fragmented, fix it before rollout. Faster posting without clean evidence usually shifts risk into audit and post-close cleanup.

Step 3#

Run one scoped pilot, then verify results against your baseline before expanding. Check both speed and control outcomes, including whether exceptions are actually going down instead of stacking up late in close.

Treat one smooth demo as signal, not proof. Scale by journal family only after outcomes are repeatable.

Step 4#

Keep claims narrow and documented. A headline like 6 to 4 days can be a useful case-study reference, but it is not a universal forecast.

Treat zero-day close as a target state: books that are accurate, complete, and ready for review at any moment. Where coverage varies by market or program, document constraints and confirm fit with finance and engineering before wider rollout.

Frequently Asked Questions

What close tasks can be fully automated, and which still need human judgment?

Routine, repeatable work is the best automation target: data entry, transaction coding, and reconciliation prep. Depending on your controls, teams may also automate repeatable journal workflows such as accrual and reversal posting. Human judgment should stay on accounting policy, material exceptions, unusual intercompany flows, and anything where source data is incomplete or contradictory. If a journal cannot be clearly traced to source records and approvals, do not treat it as fully automatable yet.

How do automated accruals and auto-reversals actually reduce month-end close time?

They can reduce waiting and rekeying around journal entries, which matters because more than half of the typical month-end close depends on journals. In practice, time savings come from standardizing recurring journal steps and reducing manual handoffs. Do not promise a universal number for reversal savings. Verify impact with your own close-cycle results.

What controls are mandatory so accounting automation does not increase risk?

You need traceability from source event to ERP post, controlled approvals for higher-risk items, duplicate protection, and an exception queue with owners and resolution history. A practical checkpoint is whether you can pull one posted entry and see the source ID, GL mapping used, approval status, posting log, and final disposition without opening email or Excel. If the evidence only exists in side files, the control is weak even if the post was automated.

How should a platform team evaluate vendors when benchmark data is limited?

Do not rely on case studies as proof of your outcome. Redwood cites one example where a company automated over 80% of monthly journal entries across more than 40 countries, but that is a single case, not a benchmark for your platform. Ask each vendor to run a sample on one journal family and show where manual work still exists behind the interface, especially spreadsheet prep and approval handoffs.

What are the most common implementation failures in ERP journal automation?

The most common failure is pseudo-automation: manual work hidden behind a polished interface. Another common miss is automating the final ERP import while leaving cleanup and support gathering manual upstream. Data gaps across systems can also leave teams relying on gut decisions instead of consistent evidence. If your team is still entering numbers into Excel templates, attaching support, and emailing approvals, you have changed the interface, not the process.

How do we prove “faster close” came from process improvement instead of delayed controls?

Start with a baseline for the same journal family: manual touches, reopen reasons, and exception patterns before rollout. Then compare two stable close cycles after automation and confirm that approvals, support, and reconciliations happened on time rather than being pushed out of the close window. If close is shorter but exception backlog or post-close corrections rise, you did not really improve the process.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- leg.colorado.gov/initiative_files/3308/downloadtrusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12796320trusted

- alteryx.com/resources/use-case/automated-journal-entryexternal

- blog.workday.com/en-us/how-aI-in-accounting-helps-close-your-...external

- brex.com/journal/articles/close-your-books-faster-wit...external

- concourse.co/insights/concourse-ai-agents-accounting-auto...external

- equilityhq.com/blog/exploring-features-quickbooks-enterpris...external

- houseblend.io/articles/netsuite-multi-entity-financial-man...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Integrate Your Payout Platform with NetSuite for Cleaner Journal Syncs

---

Business Process Automation for Platforms: How to Identify and Eliminate the 5 Most Expensive Manual Tasks

Start with the manual work that repeats across people and applications. That is where business process automation usually earns its keep. It is also where teams get into trouble if they automate messy ownership or bad data instead of fixing it first.

Accounting Cycle for Payment Platforms: How to Structure Month-End and Quarter-End Close

Month-end close on payment platforms usually breaks in three places: timing mismatch, explanation debt, and unclear ownership. The fix is to choose a close structure you can actually run, assign clear ownership for each tie-out, and set verification checkpoints for month-end and quarter-end. That keeps financial statements accurate without pushing cleanup into the next period.