Quick Answer

Choose this model only when the firm ties price to your specific outcomes, responsibilities, review cadence, and written change control. A flat fee alone is not enough. The proposal and engagement letter should match line by line, define acceptance criteria and KPIs, and state how out-of-scope work is approved before it starts.

As the CEO of a business of one, you do not make purchases. You make investments. You analyze, you vet, and you expect a return on every dollar. Yet when it comes to the function that protects your wealth most directly, your accounting, many otherwise sharp operators slip back into an old employee habit and pay for hours worked.

That is not just a tactical mistake. It is a real liability, because the billable hour model works against your interests by rewarding reaction instead of prevention. It adds friction at exactly the wrong time. You hesitate to ask a quick question because you know the meter is running. For a global professional, the consequences are not minor bookkeeping issues. They can be multi-jurisdictional tax complexity, foreign bank account reporting oversights, or a tax domicile mistake that invites an audit. At bottom, the model puts your goals and the provider's incentives at odds.

| Your Goal (The CEO) | The Hourly Provider's Incentive |

|---|---|

| Efficiency & Speed: Resolve issues and complete filings as quickly as possible. | More Time: The longer a task takes, the higher the revenue. |

| Early Prevention: Identify and mitigate risks before they become problems. | Reactive Problem-Solving: Fixing problems generates more billable hours than preventing them. |

| Strategic Partnership: Gain a partner who understands your business and offers foresight. | Task Execution: Focus on completing discrete, billable tasks as they are assigned. |

The value here is not what appears on a timesheet. It is what never goes wrong. You are not buying bookkeeping alone. You are buying risk reduction. The real return is the penalty you never pay and the audit you never have to manage.

This guide shows you how to buy accounting services through that lens, so the relationship gives you stronger compliance, better control, and clearer decisions.

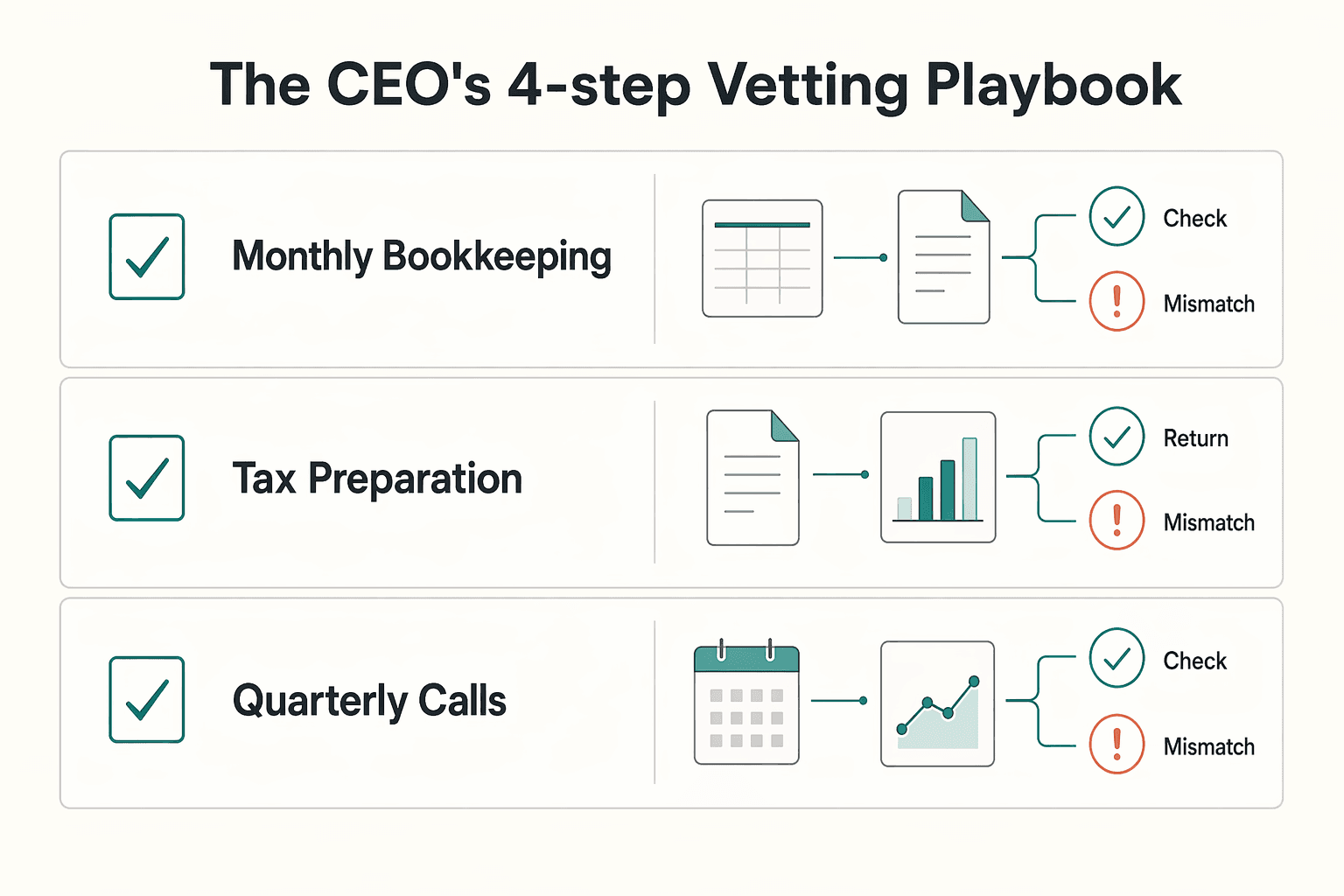

The CEO's 4-Step Vetting Playbook#

Start with the incentive problem, because it gives you a clean filter. If a firm cannot turn discovery into a written scope, measurable outcomes, named KPIs, and a written change process, that is a no-go.

| Step | Focus | Key detail | Red flag |

|---|---|---|---|

| 1 | Discovery before pricing | Questions define scope, responsibilities, deliverables, timing, and billing | Quoted after a brief call and moved into a standard menu |

| 2 | Outcomes instead of tasks | Each deliverable has acceptance criteria, owner, and review cadence | A third party still cannot tell when the work is done |

| 3 | Scorecard accountability | Objective, KPI, owner, review cadence, current status, and next action | A KPI has no owner or no review cadence |

| 4 | Written change control | Scope changes, approval authority, repricing, and timing are defined before extra work starts | "We'll sort it out later" |

Use the terms carefully. In value pricing for accounting, value pricing means services are packaged and priced around what you value, not around hours or internal cost. A fixed fee is different. It is often one preset price for the same service across clients. Scope is the boundary of work, responsibilities, deliverables, and timing in the engagement letter. An outcome is a measurable financial result. A KPI is the metric you use to judge progress against that result.

Step 1: Qualify the firm through discovery, not sales talk. A serious firm should ask enough questions to understand your needs and what you value before it prices anything. At minimum, that means questions that let them define scope, responsibilities, deliverables, timing, and billing, not just your revenue or monthly transaction count. Look for these discovery inputs:

- what you need done and what matters most to you

- who on each side is responsible for records, approvals, and responses

- what deliverables you expect and when you need them

- the start and end dates, billing terms, and any known limits or exclusions

One reliable warning sign is shallow intake. If they quote after a brief call and then move you into a standard menu, you may be looking at a standardized fixed-fee model rather than client-specific value pricing.

After discovery, you should receive a written proposal and a draft engagement letter that state clearly what will and will not be done. Use this checkpoint. Compare the proposal to the engagement letter line by line. If the proposal promises strategic support but the engagement letter lists only compliance tasks, stop there.

That document discipline matters. AICPA/CNA risk material notes that only around half of claim files asserted against CPA firms had an engagement letter tied to the underlying engagement.

Step 2: Rewrite the scope into outcomes you can accept or reject. If the proposal reads like a task list, you are still buying effort. Ask the firm to restate each deliverable in outcome language, with acceptance criteria, owner, and review cadence attached.

| Task-based wording | Outcome-based wording | Acceptance criteria | Owner | Review cadence |

|---|---|---|---|---|

| Monthly bookkeeping | Monthly close completed by the agreed date, with financial statements delivered for review | Required accounts reconciled, statements delivered, open items documented | Firm prepares; you provide records and approvals | Monthly |

| Tax preparation | Return prepared and filed by the applicable deadline, with support package retained | Draft reviewed, filing completed where authorized, confirmation saved | Firm prepares; you review and sign where required | Each filing cycle |

| Quarterly calls | Decision review held with cashflow, compliance calendar, and action items documented | Agenda sent in advance, notes issued, next actions assigned | Shared | Quarterly |

A good test is whether a third party could read the row and tell when the work is done. If not, the scope is still too loose.

Step 3: Put the relationship on a scorecard. If you want accountability, you need a short scorecard that ties objectives to ownership. Keep it simple: objective, KPI, owner, review cadence, current status, next action.

Use three KPI groups:

- Cashflow protection: the financial visibility you need to manage cash, with your own verified target date or reporting window inserted

- Compliance confidence: due dates met, required filings completed, and open issues tracked

- Decision visibility: delivery of the financial pack, unresolved questions, and decisions waiting on you

Do not let the firm fill this with vague promises. If a KPI has no owner or no review cadence, it is not a control.

Set the communication rhythm up front as well. Use one recurring operating review, plus a deeper quarterly review if your business changes often. The agenda should always cover scorecard status, upcoming deadlines, decisions needed from you, and business changes that may affect scope.

Step 4: Require written change control before extra work starts. This is where many otherwise workable engagements break down. Private accounting engagements are not governed by federal procurement rules, but the discipline is still useful. Changes should be written down, approval authority should be explicit, and price adjustments should be handled quickly.

Your engagement letter should define how scope changes are triggered and approved, including how repricing and timing will be handled.

The practical rule is simple. Discuss additional work before it starts, state the price and delivery time, and treat written approval from both sides as the gate before out-of-scope work begins.

The common failure mode is, "We'll sort it out later." That usually ends in surprise invoices, rushed work, or both. Review the engagement letter periodically, not just at renewal, so the paper still matches the real engagement. Related: How to Price a Bookkeeping Service for Small Businesses.

Red Flags: How to Spot a "Fixed Fee" in Disguise#

A flat quote alone does not prove you are getting value pricing. Use this rule: if the price is not tied to your specific outcomes, responsibilities, and change terms, you are likely buying a fixed fee or a time-based model in a fixed-fee wrapper.

| Model | How the article defines it | What to verify |

|---|---|---|

| Fixed fee | Preset price for a defined service, often standardized across similar clients | Whether scope changes are defined in writing |

| Value pricing for accounting | Client-specific and based on what you value | Whether price is tied to specific outcomes, responsibilities, and change terms |

| Time-based price in a fixed-fee wrapper | Built from labor, software, overhead, and markup, then presented as one bundled number | Whether estimated labor and markup are still driving the bundled price |

A fixed fee is a preset price for a defined service, often standardized across similar clients. Value pricing is client-specific and based on what you value. A time-based price in a fixed-fee wrapper is usually built from labor, software, overhead, and markup, then presented as one bundled number.

Run these tests before you sign#

Discovery test (how they set price): If discovery keeps centering on what you paid before, what your current provider charges, or competitor ranges, treat that as context, not proof of value pricing. If your priorities, risks, deadlines, and decision needs are secondary, the pricing logic is likely backward-looking.

| Test | What to examine | Risk signal |

|---|---|---|

| Discovery test | Whether priorities, risks, deadlines, and decision needs are central in discovery | Backward-looking anchoring if discovery centers on past fees, current provider charges, or competitor ranges |

| Proposal test | Whether acceptance criteria, owner, timing, and exclusions are named | Packaging, not outcome-based pricing, if the proposal sounds strategic but the engagement letter only commits to task delivery |

| KPI test | What results define success, what will be delivered, by when, and what counts as done | Delivery risk if answers stay abstract or drift back to effort |

Proposal test (what is actually promised): Flag broad phrases like "ongoing support," "advisory as needed," or "full service bookkeeping" when they are missing acceptance criteria, owner, timing, or exclusions. Then compare the proposal and engagement letter line by line. If the proposal sounds strategic but the engagement letter only commits to task delivery, you are looking at packaging, not outcome-based pricing.

KPI test (how success is measured): Ask what results define success, what will be delivered, by when, and what counts as done. If answers stay abstract or drift back to effort ("hours," "responsiveness," "access to our team"), the offer is likely not value-based. Missing KPIs alone do not prove non-compliance, but evasive answers increase delivery risk because there is no shared finish line.

| What you hear | What it usually means | What to ask next |

|---|---|---|

| "Our monthly package starts at one flat rate for everyone in your size band." | Standardized fixed-fee menu pricing | "Which parts are client-specific, and which outcomes change the price?" |

| "We looked at your old fee and kept you in the same range." | Backward-looking anchoring | "Which forward-looking outcomes or risks set this price beyond prior spend?" |

| "It is fixed fee, so you never need to worry about hours." | Hours may still be the internal pricing driver | "Was this built from estimated labor and markup, or from defined client outcomes?" |

| "We can handle extra requests as they come up." | Out-of-scope work is not clearly controlled | "Show the written change process, approval path, and repricing method in the engagement letter." |

If the provider is close but unclear, ask for a revised proposal with named outcomes, review cadence, and written out-of-scope terms. If they can define compliance work but not strategic outcomes, narrow scope to what they can define clearly. Walk away if they cannot put responsibilities and change-control terms in writing before extra work starts.

If you want a deeper dive, read How to Calculate Your Billable Rate as a Freelancer. For a quick next step, try the free invoice generator.

Conclusion: You Are a CEO - It's Time to Invest Like One#

Treat this as a buying decision, not a trust exercise. The accounting model is under multiple pressures at once, and a familiar setup is not always the right one to renew. Your goal is to choose a partner you can evaluate clearly as conditions change.

The practical shift is straightforward: stop comparing providers by effort alone and start comparing them by how clearly they define commitments, how they show progress, and how they handle change. If those basics are vague, you do not have enough clarity to judge the price or the fit.

A final check is whether the service fits the stage your business is in. A six-stage corporate life-cycle lens is a useful reminder: businesses create decision problems when they refuse to act their age. If your needs are still narrow and repeatable, avoid buying unnecessary complexity. If your complexity, reporting needs, or risk exposure have grown, do not renew a stripped-down package just because it is familiar. A real red flag is passivity when your business has clearly changed.

Use this short checklist before you choose or renew. That is how you improve decision quality: not by buying the cheapest option, but by buying decision clarity.

- Confirm before signing: scope, responsibilities, review points, and how changes are handled are written in plain language.

- Track during delivery: whether commitments are met on time and whether updates produce usable decisions.

- Reassess providers if: your business needs have changed and the service model has not, or the firm stays passive under new pressures.

You might also find this useful: Value-Based Pricing for Strategic Consultants Under Real Payment Risk. Want to confirm what's supported for your specific setup? Talk to Gruv.

Frequently Asked Questions

How do you tell if a price is fair?

A fair price is a value-and-risk question, not just hourly math. The written terms should clearly cover scope, responsibilities, deliverables, timelines, billing, and out-of-scope work. A market benchmark can help, but it should not outweigh a weak engagement letter.

Is a fixed fee the same as value pricing?

No. A fixed fee is a preset price for the same service, while value pricing is tied to the value delivered to your specific business. Ask what client-specific outcomes changed the price and where those outcomes appear in the proposal.

What should you ask before you sign?

Ask to see the engagement letter before work begins and compare it line by line with the proposal. It should spell out scope, responsibilities, deliverables, timelines, billing, and what counts as out of scope. Also confirm communication access and, if IRS representation is involved, who is authorized and what documents are needed.

Which pricing model fits what kind of work?

It depends on the shape of the work, how often scope changes, and how much communication you need. Compare each model by pricing basis, change handling, communication access, and accountability for outcomes. Subscription and hybrid models work best when recurring scope and extra-work rules are clearly defined.

Are tiered, subscription, or hybrid retainers always a good fit?

No. Subscription models can be useful for ongoing recurring services, but they are not automatically the right fit for every engagement. Tiered or hybrid options work only when scope, change triggers, and billing terms are explicit.

Is this just a way for accountants to charge more?

Sometimes the label is used loosely, so ask what actually changed. If a higher fee comes with better written scope, change handling, communication expectations, and accountability, it may reflect real value. If those terms did not improve, it may just be fixed-fee packaging.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- acquisition.gov/far/subpart-43.2trusted

- acquisition.gov/far/52.243-1trusted

- comptroller.war.gov/Portals/45/documents/fmr/Volume_05.pdftrusted

- irs.gov/forms-pubs/about-publication-947trusted

- accaglobal.com/gb/en/technical-activities/technical-resourc...external

- accountingtoday.com/news/its-time-to-rethink-the-accounting-modelexternal

- aicpa-cima.com/resources/download/example-format-and-contentsexternal

- apqc.org/sites/default/files/files/Measurement%20Fram...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Calculate a Freelance Rate You Can Actually Get Paid On

A workable rate is not the neat number a calculator produces. It is the number that still works after you account for real billable capacity, non-client time, scope drift, and the gap between sending an invoice and receiving cleared cash. Start with hourly math even if you do not plan to bill hourly, then turn that number into a quote with clear `payment terms`.

How to Price a Bookkeeping Service for Small Businesses

**Step 1. Reset what a bookkeeping price is supposed to do.** A usable price is not just a number that sounds competitive. It should reflect the work required and how the engagement will actually run. Market comparisons help with context, but they do not replace a pricing strategy built around the real workload.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.