Quick Answer

Yes. Responsibility can increase when your team controls onboarding, tax-profile checks, fund release, or exception decisions and still moves money after obvious warning signs. Use a market-by-market readiness gate rather than a single global rule, and pause entry where controls are thinner than local demands. Validate one end-to-end escalation path with your banking partner, confirm decision ownership, and ensure the case record can be rebuilt later if a payout is questioned.

Why Platforms Can Be Held Responsible#

If you are deciding where to launch contractor payouts, the real question is whether your current controls are strong enough for each market you want to enter. The liability issue is not just an abstract policy debate. It comes down to whether onboarding, tax-data handling, payments, and exception handling leave preventable gaps for tax crime or money laundering.

Many teams hit a similar tradeoff early. Growth wants faster onboarding and broader coverage, while risk and compliance need stronger checks, monitoring, and escalation. Those controls can directly shape market reach, payout speed, and partner support. They are part of go-to-market capacity, not a separate legal layer.

That tradeoff gets more concrete once funds start moving. In the U.S. banking context, the Bank Secrecy Act framework dates to 1970, and banks are required to maintain BSA/AML compliance programs. That does not mean every platform has the same direct reporting duties. It does mean banking and payments partners may examine how your model collects and reviews information, handles anomalies, and preserves evidence when decisions are questioned.

Why one market decision does not transfer cleanly to the next#

A control design that works in one country can fail in another. FATF Recommendations provide a global baseline, but each country applies them in its own legal and operational context. In practice, identity checks, tax workflows, and partner requirements can vary enough that default reuse creates risk.

A risk-based approach also means control depth should match exposure. Higher-risk areas need enhanced mitigation, while lower-risk areas may justify simplified measures. So the decision is not maximum controls everywhere versus move fast and fix later. It is whether your team, tooling, and escalation process can support the scrutiny each target market requires.

What this guide is and is not#

This is an operational decision guide for founders and operators. It is not legal advice, and it does not give jurisdiction-specific legal conclusions. Liability outcomes vary by country, program design, and who controls onboarding, fund flows, and exception handling.

Before you commit product or go-to-market resources, map who verifies identity, who collects tax data, who approves payouts, and who can override holds in each market. One recurring operational risk is fragmented records across onboarding, support, and payout systems. When that happens, detection can weaken, and so can your evidence if payout decisions are reviewed later.

What you will leave with#

The rest of this article is built for launch decisions, not policy statements. You will get a country-by-country liability-readiness scorecard, a control checklist for onboarding, tax data, payouts, and monitoring, an escalation design for suspicious cases and partner coordination, and clear go or no-go rules when required controls exceed current operating capacity.

- a country-by-country liability-readiness scorecard

- a control checklist for onboarding, tax data, payouts, and monitoring

- an escalation design for suspicious cases and partner coordination

- clear go or no-go rules when required controls exceed current operating capacity

Define platform liability in practical terms#

Platform liability, in practice, is the risk created by what your team can see, control, approve, or ignore. You do not need to be the employer to face facilitation exposure. If your product controls onboarding, payout flow, or exceptions, your decisions can become part of a tax-fraud or money-laundering pattern.

Start with the legal core#

In U.S. criminal framing, payroll tax evasion is not just unpaid payroll tax. It centers on willful failure to collect, account for, and pay over required taxes. Employers are also expected to deposit and report federal employment taxes, and DOJ payroll cases describe wages paid without remitting employee and employer payroll-tax portions.

Money laundering, in the concealment sense, is moving funds in ways designed to hide criminal source, ownership, or control. “Platform liability” is an operating label for the risk that your controls, or your inaction, help that conduct happen, even though there is no single universal definition across payout models or jurisdictions.

Direct abuse versus facilitation#

The practical line is direct misconduct versus facilitation. Your platform may not create a shell company or run off-the-books payroll, but it can still enable the flow. Under federal aiding-and-abetting law, a party that aids or induces an offense can be treated as a principal.

That is why shell-company patterns matter operationally. DOJ cases describe shell entities with no real labor force receiving and cashing large payroll-related amounts, including one case with more than $147 million. A useful control check is whether stated business activity, ownership information, and payout behavior line up. Repeated overrides despite obvious mismatches can indicate elevated risk.

Why charges stack#

DOJ outcomes show wire fraud, mail fraud, and money laundering can appear together, and payroll-tax schemes have also been paired with wire-fraud allegations. A practical rule is that more control over onboarding, payout release, and exception handling usually increases facilitation risk, but legal exposure still depends on your role, jurisdiction, and applicable statutes.

What enforcement patterns actually signal for platform teams#

Treat enforcement material as a control-pattern library. It shows what suspicious behavior looks like in real payment flows and what your banking partners need documented when they escalate.

Read FIN-2023-NTC1 like an operator#

FIN-2023-NTC1 (August 15, 2023) flags recurring payroll-tax-evasion and workers’ compensation fraud patterns, so your monitoring should focus on behavior after onboarding, not just KYB at entry. In platform terms, the repeat signals are:

- Networks of individuals using shell entities and fraudulent documents to route labor-related funds.

- Off-the-books payroll behavior that avoids normal payroll reporting and required payroll-tax payments.

- Transaction volume, amount, or frequency that is uncharacteristic for the claimed workforce.

- Minimal to no tax- or payroll-related remittance behavior where that visibility exists.

Use the first material payout batch as a hard verification point. If the onboarding profile and live money movement no longer align, pause and re-review before additional releases.

Do not hardcode these patterns to construction#

IRS-CI construction cases are pattern evidence, not an industry boundary. One cited case combined $146,077,535 in payroll checks and a stated $36,957,616 payroll-tax loss with wire-fraud and tax-fraud conspiracy counts.

The same stacked-charge pattern appears outside construction. A staffing-company indictment announced November 20, 2025 combined wire-fraud conspiracy, money-laundering conspiracy, and failure-to-account-and-pay-over employment-tax counts. For platform teams, the operational takeaway is to detect behavior patterns, not industry labels.

Why BSA and SAR quality change your product requirements#

FDIC's suspicious-activity FAQs summarize the same point: financial institutions report suspicious activity through SARs. The base trigger is $5,000, with other conditions. There is usually a 30-day filing window from initial detection, and a 60-day outer limit when suspect identification is delayed. Your platform may not file SARs directly, but your partners work inside those timelines.

That makes evidence quality a product requirement, not a compliance afterthought. FFIEC guidance treats the SAR narrative as critical because weak descriptions reduce investigative usefulness. Alerts and case notes should let an analyst quickly explain who is connected, what changed, why activity conflicts with the stated business, and which accounts, dates, and records support the suspicion.

For related detail, see A Guide to Stripe Radar for Fraud Protection.

Where your control surface increases legal exposure#

Legal exposure rises at the points where your team can admit, classify, hold, or release counterparties and funds. The closer you are to onboarding and payout decisions, the harder it is to treat warning signs as someone else’s problem.

The highest-impact control points are:

- Onboarding and business verification: Identity and business-verification checks help confirm the person or entity is real and that ownership information is coherent. For legal entities, beneficial owner identification and verification can be a key checkpoint where required.

- Tax profile collection: Form W-9 supports U.S. TIN collection for information reporting, and Form W-8BEN supports foreign-status certification for U.S. withholding and reporting. If tax identity details appear inconsistent, treat that as a risk signal, not just filing cleanup.

- Payout approvals: Approving release after reviewing account behavior is an active risk decision, not a passive software action.

- Manual overrides: Override decisions should include a reason, reviewer identity, and linked evidence. Without that, you create a high-risk decision with weak defensibility.

Money movement changes the posture#

A listing or network-only platform and a payout-orchestrating marketplace do not carry the same exposure profile. Under U.S. AML rules, a party that only provides delivery, communication, or network access services is carved out of the money transmitter definition. Accepting and transmitting funds or other value can fall within money transmission services.

This does not mean every platform that touches funds is automatically a money services business in every setup. It does mean full payout orchestration should be treated as a higher-responsibility operating model from day one. If your team can see high-risk signals and still releases funds, treat that as an elevated liability posture. For entities operating as MSBs, SAR considerations include transactions that involve or aggregate at least $2,000.

The hidden multipliers that make cases harder to defend#

Three gaps repeatedly amplify exposure in practice:

- Weak TIN matching: IRS TIN Matching validates name/TIN combinations before information return filing. If mismatches are left unresolved, payee records degrade and withholding consequences can follow. Fix this before scale and store validation outcomes in the account record. TIN Matching for Platforms: How to Validate Contractor Tax IDs Before Filing Season

- Poor audit logs: BSA recordkeeping has a five-year retention baseline. You should be able to reconstruct a payout decision end to end: submitted tax form, verification result, alert, reviewer notes, override reason, approval timestamp, and released funds.

- Fragmented evidence across tools: Disorganized case narratives make analysis materially harder. If onboarding, tax forms, and payout exceptions live in disconnected systems, it becomes difficult to show who knew what, when, and why funds still moved.

For a fuller breakdown, read Are You an Employee or a Contractor? A Self-Assessment Checklist.

Build a country-by-country liability readiness scorecard#

Use this scorecard as a launch gate. Score each jurisdiction by the controls you must actually run, and do not launch where those controls exceed your current operating capacity.

This turns your exposure map into a market decision. It helps you separate manageable administrative load from requirements your team cannot reliably operate yet.

| Market or program | Required onboarding depth | Tax form or reporting obligation | AML escalation expectation | Documentation retention need |

|---|---|---|---|---|

| United States contractor payouts | Collect contractor tax identity early; IRS guidance says the first step for independent contractors is Form W-9. | Form 1099-NEC applies once the reportable threshold is met. If you file 10 or more information returns in a calendar year, e-filing is required. If your model implicates third-party settlement reporting, current IRS newsroom guidance references Form 1099-K at more than $20,000 and more than 200 transactions. | Through the regulated financial institution, suspicious activity handling runs on hard timelines: SAR filing is due within 30 calendar days of initial detection, or up to 60 calendar days if no suspect is identified. CTR reporting applies to cash transactions above $10,000 daily aggregate. | Five years for BSA records. |

| EU market with DAC7 exposure | Collect seller data up front for in-scope activity, including personal services and sale of goods. | DAC7 places reporting obligations on platform operators, including qualifying non-EU operators. It has applied since 1 January 2023, and eligible operators can report in one EU country if they meet simplification criteria. | DAC7 is tax transparency, not AML escalation. Keep a clear escalation route through your payments partner. Treat FATF high-risk and FATF increased-monitoring jurisdictions differently when setting diligence expectations. | Confirm country implementation and partner requirements before launch. If retention rules are unclear, score as unresolved risk. |

| United Kingdom market with MLR recordkeeping exposure | Onboarding must support partner AML checks and later reconstruction of account decisions. | This pack does not establish a UK tax-form equivalent to U.S. Form 1099 or EU DAC7. Validate UK tax-reporting obligations separately. | Escalation usually depends on the regulated institution in your stack. Operationally, your team must be able to package a complete case quickly for partner review. | Five years under Regulation 40 baseline captured here. |

Score the drivers of operational drag#

Use a 1-5 scale per criterion: 1 means you can run it now with current staff and tools, while 5 means you need new legal interpretation, new data collection, or a new review queue.

- Legal complexity: overlap across regimes, local implementation uncertainty, and partner-term dependency

- Verification burden: identity, business, and tax evidence required before payout

- Monitoring cost: expected alert volume, manual review load, and need for structured escalation for SAR and CTR handling

- Incident response maturity: ability to preserve records, write a coherent case file, and act within timelines such as the U.S. 30-day SAR baseline

- Launch timeline impact: engineering, policy, training, and partner enablement required before first payout

Score each jurisdiction twice: once for the regime as written, and once for your delivery model. A U.S. listing product and a U.S. payout-orchestrating product should not get the same readiness score.

Make the tradeoff explicit#

Thin controls can speed launch, but they raise failure risk once alerts arrive and your team cannot reconstruct who approved payout, what tax profile was on file, or when escalation timelines began.

A slower setup is usually more defensible. Collect tax identity at onboarding, store verification outcomes on the account, preserve reviewer notes, and define escalation paths your partner can use for SAR decisions when needed. Evidence on platform liability also points to a cost tradeoff: stricter liability regimes can increase auditing and operating costs.

For jurisdiction calibration, raise legal complexity and verification burden when a corridor touches a FATF high-risk jurisdiction. Do not automatically assign the same score to FATF increased-monitoring status.

Set a hard internal launch gate#

Do not launch if required controls exceed operating capacity. In practice, treat it as a no-go when a single market would absorb capacity needed to monitor the rest of your book, or when any critical category is a 5, especially verification burden or incident response maturity, without a staffed owner and tested evidence workflow.

Before the first live payout, consider an internal checkpoint such as legal review sign-off plus a mock case walkthrough with product, ops, and your payments partner. If the team cannot clearly answer what triggered the case, who can block release, when partner escalation occurs, and whether the full file can be produced five years later, pause launch.

Design onboarding controls before first payout#

Treat onboarding as a sequence gate: verify identity and business details first, verify tax identity second, then enable payouts.

Tax forms alone are not identity proof. Form W-9 collects a payee name and TIN for IRS reporting, and Form W-8BEN is submitted when requested by a payer or withholding agent for foreign beneficial owners. Use them after identity and business verification, not as a substitute.

Start with identity and business reality#

Collect core identity data before account opening. For individuals, a practical benchmark is the CIP-style data set used by covered financial institutions: name, date of birth, address, and identification number. For legal entities, include beneficial-ownership verification in your KYB flow so payout does not go live while ownership is still unclear.

If a payments or banking partner runs formal checks, keep your product and ops sequence aligned with that process. The failure pattern to avoid is payout activation triggered by completed tax fields while account identity confidence is still low.

Use tax checks as a second gate, not the first one#

After identity and KYB checks are in place, run tax-identity checks before payout enablement. In U.S. contractor workflows, that typically means collecting Form W-9 and validating name/TIN combinations through IRS TIN Matching before filing issues compound. A mismatch response such as code “3” means the name/TIN combination does not match IRS records.

When a name/TIN mismatch appears alongside weak KYB signals, treat that as a stop-and-review condition rather than a clerical cleanup task. If backup withholding applies, the IRS rate is 24 percent. For workflow detail, see TIN Matching for Platforms: How to Validate Contractor Tax IDs Before Filing Season.

Define failure modes before they show up#

Set explicit failure rules before they appear in production:

- Mismatched entity names across incorporation records, bank details, and tax forms

- Recycled directors or nominee-style patterns that can indicate concealed control risk

- Inconsistent tax details, especially failed payee name/TIN matching

- Unverifiable beneficial ownership for legal entities requesting payouts

These signals do not prove misconduct on their own, but they justify escalation. FinCEN’s August 15, 2023 notice links shell-company use and fraudulent documents to payroll tax evasion schemes, which supports doing this screening before funds move.

Set a clear low-confidence path#

When identity confidence is low, apply pre-defined controls such as temporary transaction limits, payout holds, and enhanced review until unresolved points are addressed. Payout enablement should be an output of verification, not a parallel track.

Keep records so decisions are reconstructable. At minimum, preserve the onboarding decision log, verification results, and tax forms collected. For approved exceptions, recording reviewer identity and rationale is a strong internal control choice. For covered financial institutions, CIP procedures require maintaining onboarding records, with certain records retained for five years after account closure.

Set transaction monitoring and escalation triggers#

Once payouts are live, the next control is a monitoring and escalation layer that decides when to slow, stop, or escalate funds before weak signals become reportable cases or avoidable losses.

A strong posture optimizes for usable escalation, not perfect detection or maximum alert volume. Under the U.S. Bank Secrecy Act framework, monitoring is risk-based, and SAR content quality is a core outcome. If you see shell-like movement, repeated reversals, or clustering with no business logic, you need a defined action path before the next payout cycle.

Build triggers that map to real suspicious patterns#

Use a short trigger table, and require each trigger to have a severity tier and a clear owner. FinCEN Notice FIN-2023-NTC1 (August 15, 2023) is construction-sector scoped, but its shell-company and fraudulent-document patterns can still inform contractor payout monitoring design.

| Trigger pattern | Severity tier | First action | Escalate when |

|---|---|---|---|

| Shell-like payment loops between related accounts, especially circular flows with no clear service history | High | Temporary hold on outbound payout and analyst review | Related parties cannot be explained by KYB, invoice trail, or beneficial ownership data |

| Rapid cash-like outflows after receipt of funds, with little balance retention or business activity context | High | Temporary hold or limit reduction | Movement could be intended to hide or disguise funds, or repeats across linked entities |

| Repeated reversals, failed payouts, and re-routing to new beneficiaries | Medium | Soft alert and enhanced review of beneficiary changes | Pattern persists across cycles or coincides with mismatched identity or tax data |

| Anomalous contractor clustering, such as many contractors tied to one address, bank account, device, or controller | Medium to high | Enhanced due diligence on linked accounts | Clustering may indicate concealed control, nominee behavior, or fabricated contractor populations |

Keep the set small enough that analysts can explain why each alert fired and what the next step is.

Tie each tier to one action, not five#

Each severity tier should answer one operational question: what happens to funds now? Use soft alerts for review without stopping normal flow, temporary holds when movement must pause, enhanced due diligence when more evidence is required, and partner escalation for Suspicious Activity Report (SAR) consideration.

Keep the filing boundary explicit: SAR and CTR duties attach to covered financial institutions and MSBs, not automatically to every platform. For banks, SAR obligations often involve suspicious activity that involves or aggregates at least $5,000. For MSBs, the floor is $2,000. Your role is to send a clear, decision-ready case package to your bank or payments partner.

If activity may involve illegal-source funds, attempts to hide or disguise funds, or conduct designed to evade BSA requirements, route it to partner escalation with evidence attached.

Set internal timing standards before the first urgent case#

Set internal triage and escalation timelines up front. Regulations define SAR and CTR filing deadlines, but they do not set a universal product-team SLA like 24 or 48 hours.

Use documented internal targets such as same-day triage for high-severity holds, fixed partner-escalation deadlines, and scheduled review points for unresolved medium-severity alerts. This protects downstream filing windows. SARs are due within 30 calendar days of initial detection, and no later than 60 calendar days when no suspect is identified.

Define unblock criteria as clearly as hold criteria. Release funds only after missing facts are resolved, such as verified account relationships, confirmed beneficiaries, refreshed KYB or beneficial ownership data, and analyst notes that reconcile activity with a legitimate business purpose.

Add BSA and CTR paths through financial partners#

If payouts run through a bank or MSB partner, include a BSA handling lane for CTR-related events and urgent law-enforcement scenarios. For banks, currency transactions totaling more than $10,000 in one business day are treated as a single transaction for CTR purposes (subject to applicable exemptions), and CTR filing is due within 15 days after the reportable transaction date.

If your platform does not handle currency directly, state that clearly and keep CTR handling as a partner-notification path rather than a platform filing path. If cash-touching activity exists through a partner, monitor for same-day aggregation instead of isolated events.

Include an urgent-case branch. When activity appears ongoing and severe, the bank may need immediate telephone notification to law enforcement in addition to SAR filing. Your escalation template should capture urgency, transaction status, linked accounts, and whether funds are still moving.

Case quality is the final control point. Preserve alert logic, transaction timeline, linked-account analysis, hold and release decisions, analyst notes, and partner escalation references so the file is usable and defensible.

Decide payout rail restrictions by risk signal#

Do not treat payout rails as interchangeable. When risk signals rise, narrow rail access: keep the most controlled option available, slow higher-velocity methods, and require refreshed due diligence before restoring speed.

This is the risk-based approach in practice. Higher-risk cases require enhanced measures, and rail restrictions are a practical control product and ops can apply quickly.

| Rail type | Lower-risk use case | What changes when risk is elevated | Why it matters |

|---|---|---|---|

| Bank transfer or wire-style payout | Established entity, stable payout history, complete ownership and account data | Keep enabled only when required originator and beneficiary information is complete; escalate missing data before release | Funds transfers of $3,000 or more can trigger specific recordkeeping and transmittal requirements |

| ACH-style or local bank payout flows | Routine domestic payouts with strong account ownership confidence | Prefer when you need controlled release, but do not assume wire-style information rules apply the same way | FFIEC materials note some transfer types, including ACH, are excluded from the specific funds-transfer definition used for certain requirements |

| Virtual account flows or other faster/local rails where supported | Operationally useful for routing or local collection and payout where partner controls are clear | Approve by country and program; if data pass-through, ownership, or partner controls are unclear, keep the rail off for higher-risk segments | Cross-border regulation is not uniform, and some payment relationships require enhanced due diligence |

The practical rule is simple: if risk signals remain unresolved, restrict the rail that moves funds fastest or with the least review friction. Use a more controlled payout path and require additional due diligence evidence before re-enabling broader options. For legal entities, keep beneficial ownership identification as a required checkpoint at account opening.

Make verification rail-specific, not only account-specific. Before activating a rail in any country or program, confirm what originator and beneficiary data your partner captures, retains, and transmits, and whether missing-information logic can execute, reject, or suspend a payment. If the provider cannot answer that clearly, treat it as a blocker for higher-risk corridors.

Virtual account setups need extra caution because obligations can vary by jurisdiction and payment relationship.

Use explicit if-then restrictions#

Write these rules into policy so ops does not have to improvise under pressure:

- If ownership or beneficiary data is incomplete, allow only the most controlled rail or hold the payout.

- If risk indicators increase across customer, product, channel, or geography, require refreshed due diligence and beneficial ownership review before restoring faster rails.

- If a payments partner raises an AML control concern, pause rail expansion until the partner provides a documented path forward.

Audit every override like it may be reviewed later#

Exception handling should be documented and auditable so controls can be reviewed after release.

Build the evidence pack investigators and auditors will ask for#

Your evidence pack should let someone reconstruct a case from onboarding to payout without chasing screenshots across teams. Once you restrict rails or approve exceptions, you should be able to show what you knew, what you reviewed, and who approved release.

Start with a minimum pack, not an open-ended file#

Define a fixed artifact set for every closed case so completeness stays consistent under audit.

| Evidence item | What should be in the file | Why it matters |

|---|---|---|

| Onboarding artifacts | KYC/KYB results, beneficial ownership review, business profile, bank account verification, onboarding decision log | Shows what you relied on before enabling payouts |

| Tax forms | Form W-9 for U.S. payees, Form W-8BEN for foreign individuals, Form W-8BEN-E for foreign entities, and filing outputs such as Form 1099-NEC where applicable | Supports withholding and information-reporting logic |

| Payout records | Payment request, approval record, ledger entries, payout ID, destination account snapshot, release timestamp, and any hold or rail-restriction history | Creates the request-to-ledger-to-payout chain |

| Case notes | Alert summary, reviewer actions, override approvals, partner communications, escalation dates, closure rationale | Explains judgment, not just raw data |

Be precise about form handling. Form W-9 is given to the requester, not sent to the IRS as part of routine collection. Form W-8BEN is given to the withholding agent or payer, not filed with the IRS. Keep the exact version collected, the date received, and the linked person or entity.

Preserve the chain end to end#

Traceability is the core control: request to ledger movement to final payout, with system timestamps and named reviewer actions. If you cannot show who changed payout state, when, and on what basis, the decision is harder to defend.

Test this with a single payout ID. You should be able to retrieve the request, approval, holds, overrides, ledger posting, and disbursement record from system records, not chat history. If a case is escalated to a BSA-covered partner for SAR consideration, record the initial detection date clearly. That partner may be working under a 30-day timeline, or up to 60 days if no suspect is identified. Where BSA recordkeeping rules apply, required records are retained for 5 years.

Add cross-border tax context only when it actually matters#

Only add cross-border tax context when the case facts support it. Typical triggers are a U.S. person with foreign financial accounts or a foreign entity documenting status through Form W-8BEN-E.

Keep FBAR and Form 8938 separate in your workflow. FBAR (FinCEN Form 114) applies when aggregate foreign financial accounts exceed $10,000 at any point in the year for a U.S. person. Form 8938 is a separate FATCA-related obligation with a general $50,000 baseline, with higher thresholds in some cases. One does not replace the other. In the evidence pack, this usually means preserving the triggering facts and review trail, not collecting those filings from every contractor.

Run a periodic completeness check#

A periodic sample review is an operating control that can catch evidence gaps before an external review does. Sample routine payouts, restricted-rail cases, and overrides. Then confirm end-to-end completeness: onboarding evidence, tax forms, payout chain, reviewer notes, and payee-facing artifacts such as recipient statements when Form 1099-NEC was filed.

Two recurring errors are avoidable. First, misclassification: payments reportable on Form 1099-K by a payment settlement entity are generally not reported again on Form 1099-NEC or 1099-MISC. Second, missing decision context: teams keep forms but lose the reasoning behind fund release. In this risk area, missing rationale can be a bigger liability than a missing document.

Related: How to Build a Contractor Onboarding Checklist: KYC Tax and Bank Verification Steps.

Assign ownership across product, compliance, ops, and legal#

Clear named ownership helps keep case handling timely and consistent when a matter needs to be reconstructed.

A practical RACI works here, but the exact split is your design choice, not a universal legal rule:

- Product: Own control design in the product, including payout blocks, override paths, required fields, and audit-trail capture.

- Compliance: Own policy, escalation standards, and intake for cases that may need SAR escalation through a BSA-covered partner.

- Ops: Own day-to-day execution, including alert review, record collection, and hold application.

- Legal: Own jurisdictional interpretation where classification, tax handling, or reporting duties may vary by market.

Before launch, require named people, not just teams. You should be able to identify one policy owner, one escalation owner, one ops lead, and one legal contact. If a banking or payments partner requires defined BSA escalation, your policy should also specify who makes intake decisions, what evidence must be attached, and how decisions not to escalate are documented. That point matters because interagency SAR FAQs explicitly address documenting decisions not to file a SAR.

If you are a bank, FFIEC guidance is explicit that the board is ultimately responsible for BSA/AML compliance and must designate a qualified BSA compliance officer to oversee day-to-day program execution.

Assign explicit ownership for AML/CFT National Priorities updates. Treasury published the priorities in 2021, and agencies stated that publication itself did not immediately change BSA requirements. FinCEN's 2024 proposed AML/CFT program rule also describes requiring financial institutions to review and incorporate government-wide priorities. Treating this as an owned policy workflow is more defensible than leaving it informal.

For incident command, keep roles minimal and explicit:

- One clearly accountable lead for decision timing.

- A designated evidence recorder for case file integrity and chronology.

- One external counsel contact path, reviewed with counsel in advance.

If these roles are unnamed, delays and inconsistent decisions can become part of the record.

If you want a deeper dive, read Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

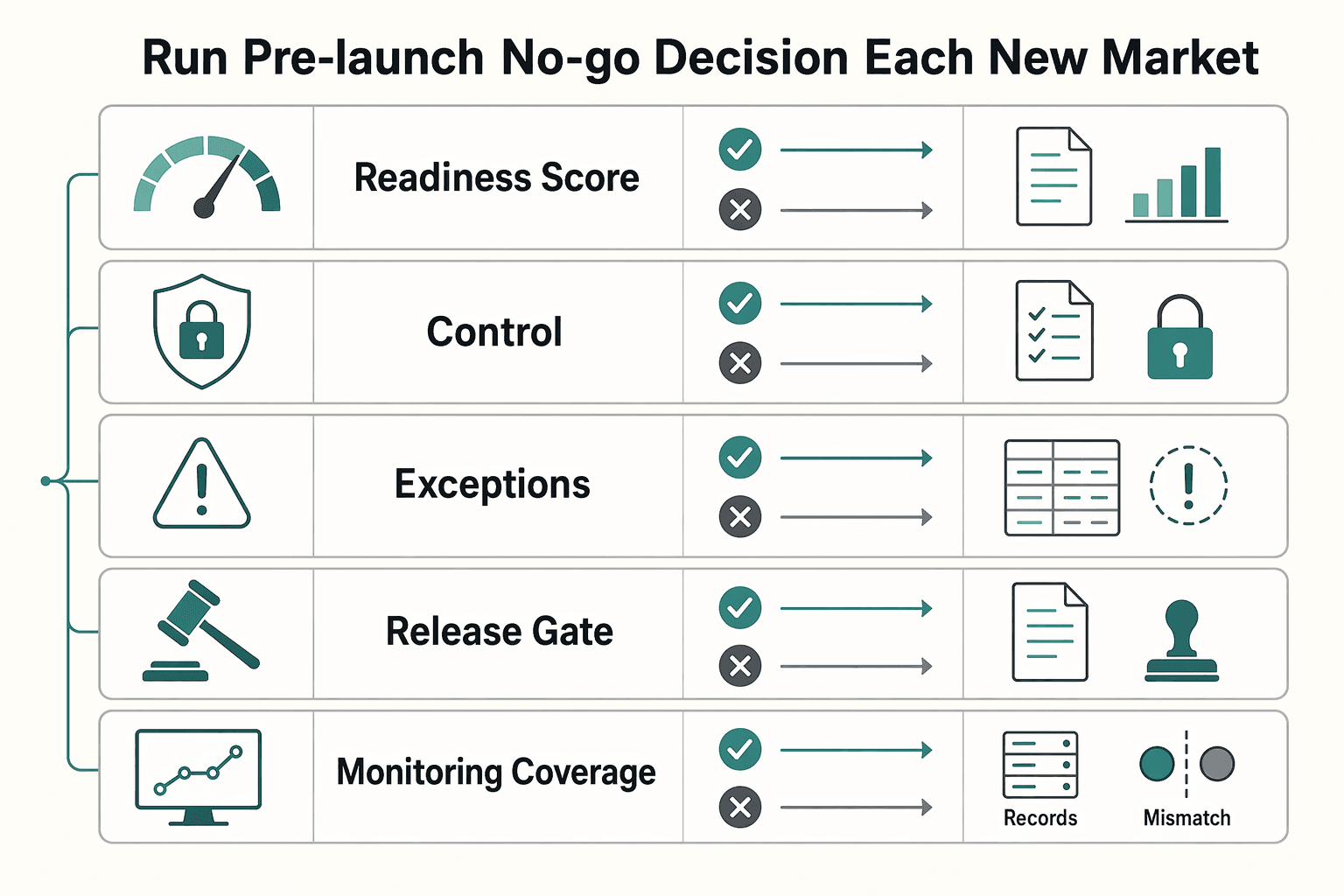

Run a pre-launch go or no-go decision for each new market#

Make a binary launch call for each market: if market-specific risk assessment, controls, staffing, legal review, and monitoring are not ready, it is a no-go.

Use a short final checklist and require evidence for each item:

- readiness score for that specific market

- control test pass for onboarding, payout holds, and case logging

- escalation staffing for time zones, weekends, and partner handoffs

- legal sign-off on the local operating model and key liabilities

- monitoring coverage for suspicious patterns from first payout onward

Apply a hard gate: if current controls cannot detect shell-company and off-the-books payroll patterns, return no-go. Recent IRS-CI cases describe shell companies used to move funds in payroll-tax fraud schemes, and weak risk identification can cascade into downstream control failure.

Before launch, run one realistic mock escalation case end to end through your Bank Secrecy Act partner path: alert creation, analyst review, evidence attachment, hold decision, and partner handoff. If your partner may need to work within the 30-calendar-day SAR timeline after initial detection, your internal queue cannot rely on ad hoc staffing.

Set an internal 30-day post-launch review checkpoint as a standing launch condition for each market. Treat this as an operating policy choice, not a universal legal requirement. Review effectiveness, not volume alone: alerts, false positives, payout delays, unresolved cases, and how continuing-activity decisions were documented. If unresolved cases rise or overrides bypass detection, pause expansion and fix monitoring first.

If you are a covered firm under FINRA Rule 3310, confirm written senior-management AML program approval and current independent testing before go-live.

If your checklist passes only with stricter approval paths and escalation SLAs, use Gruv Docs to map the controls into implementation-ready workflows.

Conclusion#

Use a strict launch rule: enter a market only when your controls, evidence discipline, and escalation capacity are already working in daily operations. If they exist only on paper, you are not launch-ready.

In this risk area, exposure often comes from the execution gap, not the policy library itself. The real issue is what happens when controls are incomplete and a payout still gets released.

The practical standard is operational enforcement. Written policies and procedures alone are not enough. Implementation has to match them. In platform terms, that means your team can consistently apply control paths, record exceptions, and explain approval decisions with usable evidence.

Escalation capability is part of that same standard. Suspicious activity reporting is treated as foundational in the BSA reporting system, and reporting quality matters. Even when your platform is not the direct filer, you still need to escalate quickly to your bank or payment partner with a clear narrative and supporting records.

Before launch, run one realistic high-risk scenario end to end and test whether your team can stop payout, reconstruct decisions, and escalate without improvising ownership. If that fails, treat it as a no-go. After launch, keep risk assessment and controls updated as products, payment rails, and AML/CFT priorities change, including FinCEN priority updates made at least every four years.

Next step: run the readiness scorecard for your next target market, then approve launch only if the go or no-go checklist passes without exceptions. If controls are not yet commensurate with that market’s risk profile, wait, narrow scope, or limit payout functionality until they are.

Before you commit GTM resources to a new market, validate payout coverage and compliance gating assumptions with Gruv.

Frequently Asked Questions

Can a platform be liable if contractors commit tax fraud?

Not automatically. Risk can rise when your team controls onboarding, tax data collection, payout release, or exceptions and still allows funds to move despite suspicious signals. Public charging language shows payroll-tax conduct can be charged alongside wire-fraud and money-laundering conspiracy counts, so ignored red flags may increase exposure.

Which red flags most strongly indicate shell-company abuse or off-the-books payroll risk?

FinCEN states that many payroll-tax evasion schemes involve networks of individuals, shell companies, and fraudulent documents. In practice, treat combined inconsistencies as high risk, especially when entity and tax details conflict, ownership cannot be verified, or payment flows do not match the stated business purpose. When those signals cluster, review the full onboarding-to-payout chain before release.

What are the minimum controls to launch safely in a new market?

Set verification before payout: risk-based Customer Due Diligence, required tax form collection, suspicious-pattern alerting, case logging, and a clear hold-and-escalate path. For tax forms, that typically means Form W-9 when a payer requests taxpayer identification information and Form W-8BEN for foreign beneficial owners when requested by the withholding agent or payer. Launch readiness should include auditable evidence for each control, including exception handling and market-specific legal review.

When should a platform file or escalate a SAR-related case through its financial partners?

Do not assume your platform files SARs directly, because SAR obligations apply to financial institutions covered by SAR rules. If facts create knowledge, suspicion, or reason to suspect suspicious activity, escalate to your bank or payment partner with a clear narrative and evidence. For banks, SAR timing is generally no later than 30 calendar days after initial detection, up to 60 days when no suspect is identified, and near-threshold transaction size alone does not require a SAR.

How do we choose between faster onboarding and stronger KYB/KYC controls?

Use a simple rule: if faster onboarding weakens your ability to verify the entity, tax profile, or payout purpose, slow down before the first payout. A practical compromise is staged access, such as allowing signup while capping activity or holding payouts until required checks clear. If core verification is incomplete, speed increases exposure more than it increases durable growth.

What is still unknown from public enforcement summaries about country-specific liability thresholds?

Public summaries are useful for pattern recognition, not for setting country-specific liability thresholds. FATF standards are implemented differently across jurisdictions, so one notice is not a universal liability rulebook. You still need jurisdiction-specific legal analysis for local AML/CFT duties, platform reporting, and tax-reporting obligations, including DAC7 annual seller reporting in the EU.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: