Quick Answer

Start by treating interchange fees as one component inside your full deduction stack, then set pricing from net deposit rather than billed amount. You cannot set Visa or Mastercard schedules, but you can control payment routing, reporting quality, and contract visibility with your provider. Use ACH in the U.S. or SEPA Credit Transfer for stable repeat clients, and keep cards as fallback when completion speed is critical. For international transactions, isolate country and currency effects before changing your fee assumptions.

What's Really Happening When Your Client Clicks "Pay"?#

When your client clicks Pay, the transaction moves through three stages. Interchange is only one part of your total card-acceptance cost. Interchange fees are transaction fees charged between banks when credit and debit card payments are processed, and they sit inside that broader cost.

In practice, four parties shape the flow. The issuer is your client's bank, and it approves or declines the charge. Your acquirer/processor accepts the payment for you. The card network such as Visa or Mastercard routes the transaction and sets interchange programs. You pay your financial institution a merchant discount, which is separate from the interchange reimbursement that moves between acquiring and issuing banks.

The payment flow in your workflow#

The flow is straightforward:

| Stage | What happens | Key note |

|---|---|---|

| Authorization | Your checkout, payment link, or invoice tool sends the request to your acquirer, then through the network to the issuer for approval or decline | Approval or decline happens here |

| Clearing | The approved transaction is validated and financially assessed | Comes after authorization |

| Settlement | The network facilitates the exchange of funds between issuer and acquirer | An approved payment is not the same as settled funds in your account |

The practical point is that approval is not the same as cleared or settled funds in your account.

When one client payment costs more than another, start with transaction-level reporting. At minimum, check card brand, card type or product tier, card-present versus card-not-present status, and MCC. Without those fields, it is difficult to separate network-driven cost from other fees.

What changes your cost of acceptance#

Networks price transactions by program and context, not with one universal rate. That is why the same invoice amount can produce different underlying costs.

| Driver | Why networks price it differently | What you can do |

|---|---|---|

| Card type and product tier | Published tables vary by card tier (for example, Core through World Elite). | You cannot choose the client's card, but you can make card-tier mix visible in reporting instead of relying on one blended view. |

| Card-not-present context | Remote payments are priced under different programs, and recent U.S. data shows card-not-present fraud rates have continued upward. | If you bill online, confirm transactions are correctly labeled and avoid comparing your costs to card-present examples. |

| MCC | MCC classifies your business type, and some published programs are MCC-specific. | Confirm your MCC matches your primary business so transactions are categorized as intended. |

One concrete example: Mastercard's U.S. bulletin shows separate small-ticket rows for card present and card-not-present, with example rates of 1.65% + 0.02 versus 1.95% + 0.02 in that program. That shows context can change cost. It does not mean card-not-present is always higher in every scenario.

What you control and what you do not#

You do not control network-set interchange schedules, the issuer, or the card product your client uses. Also, the U.S. Regulation II debit cap formula ($0.21 + 0.05% + $0.01) applies to covered U.S. debit issuers, not credit cards.

| Item | Control | Article note |

|---|---|---|

| Network-set interchange schedules | Do not control | Card networks set interchange programs |

| Issuer | Do not control | The issuer is your client's bank |

| Card product your client uses | Do not control | Card type or product tier can change underlying cost |

| Accurate MCC | Control | Confirm your MCC matches your primary business |

| Transaction-level reporting | Control | Reporting should show card brand, card type or product tier, card-present versus card-not-present status, and MCC |

| Transaction-context labeling | Control | Confirm transactions are correctly labeled |

You do control setup and visibility: accurate MCC, clear transaction-level reporting, and correct transaction-context labeling. If your reporting cannot show those basics, fix that first before you try to reduce fees.

Related: How to Reduce Stripe Processing Fees.

Beyond Interchange: Deconstructing the "Fee Stack" Eroding Your Revenue#

Your payout can be reduced by more than interchange. The useful question is simpler: which fee layers took money between your invoice total and your final bank deposit?

A useful frame comes from the U.S. Congressional Research Service report R48216 (10/08/2024), which separates swipe-fee structure into Merchant Discount Rate (MDR), Interchange, Network Fees, and Processing Fees. If your account shows one blended charge, those layers may still exist, but you may not be able to see them clearly.

Reading the stack from invoice to deposit#

Start with the paid invoice amount, then map what was withheld before payout. Keep this distinction clear: the CRS report names MDR, interchange, network fees, and processing fees as distinct fee layers, even when your reporting bundles them.

| Fee layer | Who sets or controls it | Where it appears on statements | Can you influence it? | Common confusion point |

|---|---|---|---|---|

| Merchant Discount Rate (MDR) | Not specified in this grounding excerpt; treated as a distinct fee layer | May appear as a summary or bundled charge, depending on reporting | Depends on contract and provider setup | Treated like one standalone fee instead of a bundle |

| Interchange | Named separately in CRS; control details are not specified in this source | Sometimes itemized, sometimes folded into broader reporting | Not publicly documented | Blended together with processor-related charges |

| Network Fees | Named separately in CRS; control details are not specified in this source | May be separate or bundled in reporting | Not publicly documented | Grouped mentally into "processing" |

| Processing Fees | Named separately in CRS; control details are not specified in this source | Often tied to contract terms and reporting format | Depends on contract and provider setup | Hard to isolate when reporting is blended |

If your reporting does not separate the main layers, attribution gets harder. CRS flags this as asymmetric information between merchants and acquirers.

Where pricing models can hide or reveal margin#

Your pricing model affects what you can see, but the label alone does not guarantee clarity.

| Pricing model (listed in CRS) | What you can infer from the label alone | What still needs statement-level verification |

|---|---|---|

| Blended | It is a recognized merchant fee structure | How MDR, interchange, network fees, and processing fees are actually shown |

| Flat-rate | It is a recognized merchant fee structure | How fee layers are bundled or separated in reporting |

| Tiered | It is a recognized merchant fee structure | How fee layers map within each reported tier |

| Subscription | It is a recognized merchant fee structure | How total charges map across fee layers in reporting |

| Interchange +/++ | It is a recognized merchant fee structure | How markup and other fee layers are separated in practice |

The point is simple: the model matters less than the visibility you get with it. You need enough detail to separate fee layers clearly.

The international layer: mark unknowns before you diagnose#

International or conversion-related deductions can be hard to classify when reporting is bundled. This grounding source does not provide specific cross-border or FX formulas, so treat exact mechanics as unknown until your provider maps them clearly.

- Keep international or conversion-related lines separate from core swipe-fee layers during reconciliation.

- Ask for a written mapping from invoice amount to final bank deposit for bundled deductions.

- Do not assume an unlabeled amount is interchange, network fees, or processing fees.

If you look at only one blended deduction, different mechanisms can look identical, and that usually leads to the wrong fix.

Diagnose your stack#

Before you change pricing assumptions, pull the documents that let you map the stack cleanly:

- Recent monthly statements, your pricing agreement, and one transaction-level export with available card, channel, currency, and geography fields

- A direct support mapping of which charges are reported as MDR, interchange, network fees, processing fees, and any international or conversion-related items

- One line-by-line reconciliation from invoice amount to final bank deposit

- Red flags such as blended-only reporting, unclear layer labels, or support replies that do not map charges clearly

If you cannot map the stack clearly, do not treat a headline rate as your true cost of acceptance.

If you want a deeper dive, read The Future of Work is Freelance: Trends to Watch in 2026.

Regaining Control: What You Can (and Cannot) Influence#

Once you can see the stack, decide which parts are fixed and which parts are operating choices. In practice, you usually cannot directly set network-level wholesale logic, including core debit interchange treatment. You can control your provider setup, payment-method mix, pricing policy, and dispute workflow.

Why this matters: changing the wrong layer rarely fixes your margin. U.S. debit evidence around the Durbin Amendment (Section 1075 of Dodd-Frank) shows that even with a cap shift described from about 2 percent to $0.22, the cited study found little across-the-board consumer savings and reported offsetting fee changes through higher bank fees. Use that as a planning guardrail, not a universal rule. Wholesale changes alone may not improve your take-home results.

Accept, optimize, escalate#

Treat wholesale layers as constraints unless your contract clearly says otherwise. Optimize what sits above them: payment mix, processor visibility, and how you price for total acceptance cost.

Escalate to your provider when:

- Reporting is too blended to separate network versus processor charges

- International handling is unclear

- Support cannot map one paid invoice to one final bank deposit

Before you escalate, gather the same four items every time: your merchant agreement, fee schedule, one recent payout statement, and one transaction export with card, currency, and geography fields.

Choose your operating model with a contract-first lens#

A common structural choice is a standard processor or a Merchant of Record (MoR). There is no universal winner here. The better fit depends on your cross-border exposure, buyer profile, and internal ops capacity.

| Decision area | Standard processor (verify in contract) | MoR model (verify in contract) |

|---|---|---|

| Legal seller role | Whether you are the named merchant or seller in the transaction flow | Whether the provider is the named seller for the end transaction |

| Tax/compliance ownership | Which registration, calculation, filing, and remittance tasks remain with you | Which obligations the provider contractually assumes |

| Dispute/fraud liability | Who carries evidence burden and direct loss exposure | What dispute handling or risk the provider takes on |

| Reporting clarity | Whether fee layers are truly itemized versus blended | What is summarized versus itemized in payout or report exports |

If your model is mostly domestic and your team can handle compliance and admin reliably, a transparent standard processor setup may fit. If you have heavier cross-border exposure or limited ops bandwidth, a contractually clear MoR setup may improve predictability.

Your checkpoint list#

Before you commit to a model, use these checks:

- Confirm who the contract names as merchant or seller of record

- Map which fee layers you absorb versus which the provider absorbs

- Verify ownership of tax, compliance, and dispute handling in writing

- Flag unclear terms such as chargebacks, international treatment, and reporting visibility before scaling

You might also find this useful: A Deep Dive into Deel's Pricing and Fees for Contractors.

Building a Resilient Payment Strategy to Maximize Your Take-Home Pay#

The goal is not to shave a few basis points in isolation. It is to reduce fee drag, improve the speed to usable cash, avoid compliance surprises, and make net revenue more predictable.

Lower fee drag by segmenting clients and payment rails#

Payment rail choice is a margin decision, not just a convenience choice. GAO notes that merchants do not receive the full credit-card sale amount because processing deductions apply, and it also reports that total card-acceptance costs rose over time as card use increased.

Use bank-based payment where relationship trust and process stability are strong, and keep cards for cases where buyer convenience matters more. The Federal Reserve (July 07, 2025) describes Pay-by-Bank as an emerging direct account-to-account option and a potentially cost-efficient, secure alternative to cash and cards, so test it by client segment instead of assuming it is always better.

| Client type | Payment rail | Risk level | Operational tradeoff |

|---|---|---|---|

| Repeat client with stable invoice pattern | Bank transfer (including Pay-by-Bank where available) | Lower | Can offer better fee control, but execution depends on client payment process discipline |

| New or first-project client | Card | Medium | Can support buyer completion, with higher fee drag and dispute exposure risk |

| Time-sensitive start or urgent payment need | Card | Medium | Can support quick buyer action, but less control over acceptance-cost drag |

| Cross-border client with variable payment behavior | Bank transfer or card (based on contract and workflow fit) | Medium to high | Can improve client flexibility, but more operational checks are needed before you can predict net revenue |

Operator default: when the client is known and urgency is low, start with bank transfer and keep card as fallback.

Build cost of acceptance into pricing#

If you do not build acceptance cost into pricing, margins can drift. Include every deduction that affects what you actually keep, including card acceptance costs and other provider deductions shown in your statements.

Use a repeatable process:

- Estimate blended acceptance cost by segment using recent statement data.

- Set a margin guardrail for each engagement type, such as a minimum post-acceptance gross margin target.

- Price retainers and projects to protect that guardrail.

- Recheck at renewal, or when payment mix changes.

- If you use an external benchmark, treat it as a placeholder until date and scope are verified.

For a pricing approach that pairs well with this, see Value-Based Pricing: A Freelancer's Guide.

Get from payment to usable cash with one checkpoint list#

Track the path from paid invoice to usable funds, not just headline rates. Use the same checklist each time so cashflow surprises show up early:

| Checkpoint | What to verify |

|---|---|

| Settlement and payout timing | What is expected and where variability can occur |

| Withdrawal mechanics | Any steps or constraints before funds are usable |

| FX handling | Where conversion occurs and how it appears in reporting |

| Reserve or hold risk | What conditions can delay access and how releases are communicated |

| Statement transparency | Whether one invoice and transaction record can be matched to one payout and one bank deposit |

If that last mapping is unclear, reconciliation and forecasting can stay noisy.

Make compliance ownership explicit before scale#

Write down ownership before volume increases. For each provider setup, assign responsibility in writing for tax handling, dispute liability, and recordkeeping across three parties: you, the processor, and any MoR in the flow.

Treat dispute operations as a live risk control, not back-office admin. A 2022 Federal Reserve submission argues that split routing across networks can obscure patterns and increase chargeback burden. That is not a final rule finding, but it is still a practical warning to verify evidence requirements, retention expectations, and loss allocation in advance.

Finally, test continuity posture directly. Ask whether the provider can clearly explain a multilayer resiliency model that covers core redundancy, external redundancy, and stand-in processing so payment operations can continue through disruptions.

For a step-by-step walkthrough, see A Deep Dive into Remote's Pricing and Fees for Contractors.

Before you finalize pricing, run your common client payment mixes through the payment fee comparison tool so your margins reflect real fee paths.

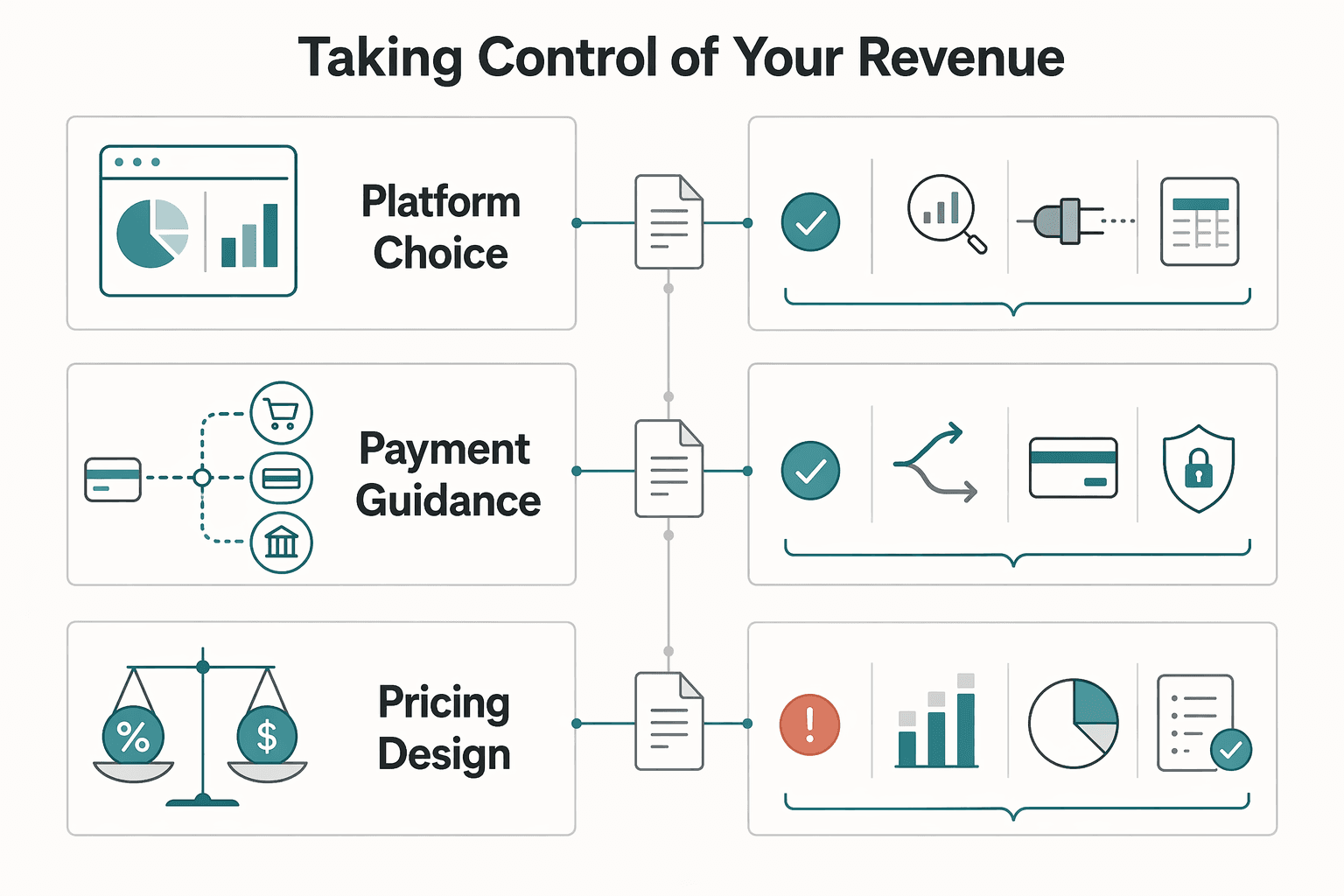

From Fee-Payer to Empowered CEO: Taking Control of Your Revenue#

This is an operating decision, not just a fee problem. Focus on the three levers you own, and stop spending time on the parts you do not. You cannot set network interchange tables or regulatory outcomes such as Regulation II changes. You can control your payment setup, client payment paths, and pricing assumptions so margin swings are less random.

| Control lever | What you control | Main tradeoff | Best use case |

|---|---|---|---|

| Platform choice | Whether you run on transparent processor pricing or a bundled model | Visibility and flexibility versus bundled convenience | You want clear fee diagnostics, or you want one bundled operating model |

| Payment guidance | Which payment route clients see first, and when card stays as fallback | Potential fee relief versus possible checkout friction and extra ops work | Repeat clients, larger invoices, stable billing relationships |

| Pricing design | How cost of acceptance is built into offers, retainers, and renewals | Higher upfront price discussion versus fewer margin leaks later | Services with repeatable delivery and predictable payment behavior |

Start with platform choice, because weak visibility weakens every other lever. If charges are heavily bundled, you may lose bargaining leverage and get less clarity on where margin is leaking. If you use a Merchant of Record, verify exactly who owns tax handling, refunds, chargeback losses, and transaction evidence. Also check your failure path: relying on one PSP can create a single point of failure if checkout goes down, so confirm your failover options.

Then set payment guidance by client profile, not habit. Use the lower-friction route when speed is critical, and test alternative routes where payment behavior is stable and your own data supports the tradeoff. Keep card as a fallback instead of a default when that fits your client mix and operations.

Finally, lock pricing to reality. Build cost of acceptance into proposals and retainers up front instead of absorbing it later. When payment behavior changes, update commercial terms early so your margin stays intentional.

- Audit your current fee stack and mark which costs are bundled versus itemized

- Set default payment routes by client segment, with card as fallback where speed matters

- Update pricing assumptions in proposals, retainers, and renewals

- Add a recurring review point after you verify a workable cadence in your own data

We covered this in detail in How to Invoice for 'Billable Hours' vs. 'Project Fees' in QuickBooks.

If cross-border collections and payout operations are creating overhead, review Merchant of Record for freelancers to evaluate a bundled setup where supported.

Frequently Asked Questions

How can you reduce the impact of interchange fees?

You usually cannot change card-network interchange tables, so a practical lever is deciding when to use cards versus bank transfer. For repeat clients and larger invoices, consider ACH in the U.S. or SEPA Credit Transfer for euro accounts when payment behavior is stable, and keep cards as a fallback when checkout completion speed matters more. Next action: set payment-method defaults by client segment so known clients see bank transfer first and card second.

What is the difference between interchange and Stripe or PayPal fees?

Interchange is a transfer fee inside card rails between acquiring and issuing banks, while your provider price is typically a merchant discount or bundled rate that can include interchange, assessments, and processor markup. Visa states that merchants do not pay interchange reimbursement fees directly; merchants negotiate and pay a merchant discount to their financial institution, which may include multiple processing services. Next action: review your last 90 days of statements and confirm whether fees are shown as pass-through line items or as a single all-in rate.

Are international card payments more expensive?

They can be, but treat international cost as multiple drivers, not one line item. Extra cost can come from country mismatch, currency conversion, and provider surcharges. For example, Mastercard documents a cross-border assessment when merchant and cardholder country codes differ, and Visa Canada documents an additional international acquiring assessment for cards issued outside Canada. Next action: tag each payment by merchant country, cardholder country, settlement currency, and payout currency so you can see where margin is actually leaking.

Can you negotiate these charges as a freelancer or small business?

Assume network tables are mostly not negotiable by you directly, but your processor pricing, contract terms, and payment-method mix may be negotiable depending on your provider and contract. Also separate regulation from contract pricing: U.S. Regulation II includes a covered debit cap formula (21 cents + 5 basis points) and exempts small issuers under $10 billion, while the EU IFR summary caps consumer-card interchange at 0.2% for debit and 0.3% for credit. Next action: ask your provider for a clearer fee breakout or interchange-plus pricing, then move stable client segments to bank transfer by default.

How does a Merchant of Record change what you pay and what you own?

A Merchant of Record is the legal selling entity and may take on payment-related liabilities such as tax collection, PCI compliance, refunds, and chargebacks. That can simplify operations and make costs more predictable, but it does not remove all business risk, so you still need to verify exactly what the contract assigns. Next action: confirm who is named as MoR and who owns tax handling, refund policy, chargeback losses, and transaction-level evidence.

Can you pass card costs directly to clients with a surcharge?

Treat surcharging as a compliance process, not a quick pricing toggle. Visa says surcharging may be allowed in most U.S. states and territories with limits, both Visa and Mastercard disallow surcharges on debit and prepaid cards, both require advance notice to your acquirer, and Mastercard also requires notice to Mastercard. Visa caps surcharge amount at your applicable merchant discount rate or 3%, whichever is lower. Next action: keep current regional surcharging rules pending for each market until they are verified against network, acquirer, and legal source records; then collect legal review, acquirer confirmation, notice records, and disclosure screenshots before enabling surcharging.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bclawreview.bc.edu/articles/3174/files/679bab45ebeb2.pdftrusted

- congress.gov/crs-product/R48216trusted

- congress.gov/crs-product/IF12548trusted

- ecfr.gov/current/title-12/chapter-II/subchapter-A/par...trusted

- eur-lex.europa.eu/EN/legal-content/summary/fees-for-card-based...trusted

- federalregister.gov/documents/2023/11/14/2023-24034/debit-card-i...trusted

- federalregister.gov/documents/2011/07/20/2011-16861/debit-card-i...trusted

- federalreserve.gov/paymentsystems/regii-average-interchange-fee...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

Future of Freelance Work in 2026 for Cross-Border Hiring Decisions

Before you scale cross-border freelance hiring, make one decision first: are you working from evidence you can actually use, or from broad trend claims that sound bigger than they are? That matters more than the headline. If your records are weak, fast sourcing can turn into compliance gaps or classification risk long before it becomes useful capacity.

How to Reduce Stripe Processing Fees

**You can protect margin by treating fees, payout timing, and dispute exposure as one risk system.** It is easy to fixate on headline Stripe fees. In practice, margin usually leaks from three places at once: