Quick Answer

Build the dashboard around 20 metrics across six control areas: authorization, payment success, refunds and disputes, settlement and reconciliation, balances and reserves, and payout execution. Publish each card with a formula, source system, owner, refresh timestamp, and first-response action so finance can trust the number before acting on it.

Build dashboards around decisions, not chart volume#

A useful payments dashboard is a decision tool, not a wall of charts. For a marketplace CFO, payment operations dashboard metrics should answer four questions fast: what changed, who owns it, what gets checked next, and what action starts now instead of waiting for month end.

According to the Federal Reserve Payments Study, US payment mix keeps shifting across card and ACH rails. That is why a marketplace CFO needs rail-aware metrics instead of one blended payment-health chart.

Clarity usually breaks first when metrics and KPIs are treated as the same thing. They are not. A metric measures activity or performance. A KPI is the smaller set you use to judge whether day-to-day execution is meeting an objective. That is how you separate operator reporting from vanity reporting and tell the difference between noise and something that needs intervention.

Rail timing belongs in the dashboard too. The FedNow Service overview describes near real-time clearing and settlement with 24x7x365 processing, while Nacha says Same Day ACH can move eligible payments of up to $1 million in a few hours. If payout aging ignores rail, a healthy queue can look broken or a broken queue can look healthy.

Data from Nacha's 2025 ACH Network Volume and Value Statistics shows the ACH Network handled $93 trillion in 2025, including $3.9 trillion of Same Day ACH. In other words, payout timing and liquidity visibility are finance controls, not secondary support metrics.

So this article stays operator-first. We will define terms, map key operating handoffs, enumerate the 20 metrics that belong on the CFO view, and close with practical verification checkpoints so teams can align on one reproducible source of truth.

Before finance signs off on any recurring dashboard, confirm that each figure can be traced back to its source event set and compared to the objective it is meant to support. If product, ops, and finance cannot reproduce the same number from the same underlying events, it is not ready for executive decisions.

Related: Accounts Payable KPIs: The 15 Metrics Every Payment Platform Finance Team Should Track.

Define the four rates before you build anything#

Start with definitions, not charts. If teams do not agree on how a rate is calculated, treat it as draft instead of dashboard-ready. Labels like approval rate, payment success rate, and failure rate can look aligned while product, ops, and finance are each using different status maps.

Adyen's reports-and-payments-lifecycle guidance is a useful reminder that one provider can expose different reports for authorization, settlement, chargebacks, accounting, and payouts. If your team collapses those stages into one label, the CFO dashboard becomes ambiguous before it goes live.

Freeze the formula, not just the label#

For each rate you track, publish the arithmetic with the metric name. Show the numerator, denominator, counting unit, time window, and retry treatment so teams can compute the same value the same way.

Write the formula in the card itself. For example: authorization rate = approved authorizations / authorization attempts * 100%, payment success rate = successful payment intents / unique payment attempts * 100%, refund rate = refunded amount / settled amount * 100%, and dispute rate = disputes / settled card payments * 100%.

Add formula, source, and owner to key cards#

Use a consistent card standard for this payment operations dashboard. Every rate card should say exactly what it measures and what it does not.

| Rate card | Formula to publish | Common ambiguity to lock down | Diagnostic slice to keep |

|---|---|---|---|

| Authorization rate | approved authorizations / authorization attempts * 100% | Retry treatment, partial approvals, and excluded tests | issuer, BIN, market, payment method |

| Payment success rate | successful payment intents / unique payment attempts * 100% | Async completions, duplicate attempts, and canceled flows | checkout step, processor, payment method |

| Refund rate | refunded amount / settled amount * 100% or refunded payments / settled payments * 100% | Amount-based versus count-based view | seller cohort, market, reason |

| Dispute rate | disputes / settled card payments * 100% | Network windows and monitored-program scope | card brand, market, seller cohort |

- formula

- data source

- owner

- refresh timestamp

- first-response action

That small discipline keeps each metric usable. The formula removes naming ambiguity, a linked data source supports drill-down to underlying records, the refresh timestamp shows whether the number is operational or reconciled, and clear ownership makes follow-up explicit instead of waiting for month-end reporting.

Before a rate goes to executive review, run a reproducibility check from the same underlying records to catch definition drift early. If finance, ops, and product cannot rebuild the same number from the same slice, keep the card in draft.

We covered this in detail in How to Build a Compliance Operations Team for a Scaling Payment Platform.

Map the money lifecycle so each metric has a home#

Once formulas are locked, every metric needs a home in the money flow. Map each one to a money-movement stage, a primary view, and a first responder. If a KPI has no clear stage home, teams can end up debating symptoms instead of isolating the break.

A practical stage spine for a marketplace CFO is authorization, payment completion, settlement, reconciliation, balances, and payout execution. Treat that as an operating model, not a universal law. Stage-level tracking matters because payment platforms coordinate activity across buyers, sellers, processors, banks, and payout providers, and each handoff can fail differently.

Use one stage spine across your tools#

Keep one stage map across operations and reporting tools so point-in-time checks and trend checks stay aligned.

| Stage | Core metric family | Primary system of record | First responder |

|---|---|---|---|

| Authorization | approval rate, decline mix, authorization latency | transaction and processor detail | payments ops |

| Payment completion | payment success rate, payment failure rate | normalized transaction table | payments ops or product |

| Settlement | net settled volume, settlement lag | settlement report | finance ops |

| Reconciliation | unmatched items, fee variance, posting breaks | accounting and reconciliation workspace | finance or rev ops |

| Balances | available, pending, reserve-held funds | balance ledger or treasury view | finance or treasury |

| Payout execution | queued payouts, failed payouts, retry aging | payout report and webhooks | payout ops |

Use live operational views for fast diagnosis, and durable records for cross-stage trend analysis. If a chart cannot be traced to underlying records, treat it as a signal to investigate, not a final answer.

Name the failure surface at each stage#

Each stage should include a short note on what can break and what gets checked first. Keep it practical. Early warning signs can include approval drift, settlement lag, unmatched transactions, reserve pressure, or payout backlog.

A simple verification drill works well here. Trace a small sample from stage event to trend record to dashboard metric to exception handling. If any link is missing, the metric does not yet have a reliable home.

Assign the first mover before a metric turns red#

Do not wait for a red metric to decide who acts first. One primary owner per stage can act as the control point, even if secondary owners support the work.

As a working draft, define which function responds first at each stage, then document secondary support. Revisit that split regularly so ownership is clear before KPI damage shows up in revenue, costs, or seller experience.

You might also find this useful: The Payment Operations Maturity Model: How to Benchmark Your Platform Finance Team.

Choose the 20 metrics that actually run operations#

A card should earn its place by telling the team what to check next. If it does not lead to a next action, cut it. A 20-metric set is a practical breadth benchmark for payment operations dashboard metrics, not a universal rule for every marketplace.

The most useful set mixes outcome KPIs with diagnostic and process metrics. That balance reduces the risk of reacting only after lagging KPIs fall and gives operators earlier signals to investigate.

Use a balanced set, not a wall of success rates#

Start with authorization rate, decline mix, and authorization latency. Stripe's card declines guide shows why issuer and decline-code context matters, and its dispute monitoring programs are a reminder that dispute activity needs its own control surface.

Then build out the rest of the set across payment success, post-sale risk, reconciliation, balances, and payouts. The goal is not a beautiful wall of charts. The goal is a complete operating view that tells finance what changed, where cash is stuck, and who acts first.

| Metric | Example formula or view | Stage | Primary source | Why CFOs care |

|---|---|---|---|---|

| Gross processed volume | sum authorized or captured amount | authorization and completion | transaction detail | current payment flow size |

| Authorization approval rate | approved authorizations / authorization attempts * 100% | authorization | processor events | checkout conversion health |

| Hard decline rate | hard declines / authorization attempts * 100% | authorization | decline-code detail | structural acceptance issues |

| Soft decline rate | soft declines / authorization attempts * 100% | authorization | decline-code detail | retry and routing opportunity |

| Authorization latency | p95 auth response time | authorization | gateway or API logs | friction before conversion loss |

| Payment success rate | successful payment intents / unique payment attempts * 100% | payment completion | normalized transaction table | top-line completion |

| Payment failure rate | failed payment intents / unique payment attempts * 100% | payment completion | normalized transaction table | break visibility before settlement |

| Refund rate | refunded amount / settled amount * 100% | post-sale | refund workflow and settlement data | margin leakage |

| Refund aging | median days from request to completion | post-sale | refund workflow logs | customer cash-back lag |

| Dispute rate | disputes / settled card payments * 100% | post-sale | disputes report | network risk exposure |

| Dispute amount | sum open dispute amount | post-sale | disputes report | revenue at risk |

| Net settled volume | settled gross minus fees and reversals | settlement | settlement report | cash actually arriving |

| Settlement lag | median time from capture to settlement | settlement | settlement report | cash timing |

| Unmatched settlement items | count or amount of unmatched transactions | reconciliation | reconciliation workspace | close risk |

| Fee variance | expected fees minus reported fees | reconciliation | payment accounting report | margin surprise |

| Ledger posting exceptions | count of unposted or failed ledger entries | reconciliation | ledger exception queue | close integrity |

| Available versus pending balance | current available, pending, and reserve-held funds | balances | balance ledger | payout capacity today |

| Payout queue age | oldest queued payout age | payout execution | payout report | backlog detection |

| Payout failure rate | failed payouts / submitted payouts * 100% | payout execution | payout report | cash-out reliability |

| Payout retry aging or acknowledgment lag | oldest retry age or p95 time from submission to acknowledgment | payout execution | payout report and webhooks | stuck-money diagnosis |

Add one stoplight field, but keep the evidence behind it#

A single stoplight per metric is useful because it makes the action path explicit: monitor, investigate, escalate. Drive that status from each metric's trigger rule, then verify the underlying records before you treat the dashboard state as final.

When a metric turns amber or red, pull a small sample through the whole chain. Start with the source event, then the warehouse record, dashboard card, and the operational exception view you use. If the team cannot produce that chain quickly, the metric is not yet reliable for executive decisions.

If you want a deeper dive, read How to Present Payment Operations Metrics to Your Board: KPIs That Matter to Investors.

Set ownership thresholds and first response actions#

Metrics only run operations when ownership and first response are explicit. For each dashboard KPI, document four fields on the card itself: primary owner, backup owner, escalation path, and expected response window.

Not every metric is a KPI, so make the difference clear. Some cards trigger action. Others provide context. If a card turns amber or red and the team still has to ask who owns first verification, it is not operational yet.

Make ownership follow the stage where evidence appears first#

Assign the primary owner to the team that can verify the first source evidence for that metric. Assign the backup owner from the next dependent stage so incidents do not stall inside one team. Keep the escalation path role-specific in your org, not broad labels like "payments" or "finance," so investigations do not disappear into a shared queue.

Set response windows by impact and data freshness#

Use response windows, but do not force one blanket SLA across all KPIs. Operational KPIs are often monitored in real time, yet first response still has to match both impact and data trust at alert time.

Use two checks before escalation:

- How quickly could this issue affect customers, sellers, or cash if it is real?

- How fresh and trustworthy is the underlying data right now?

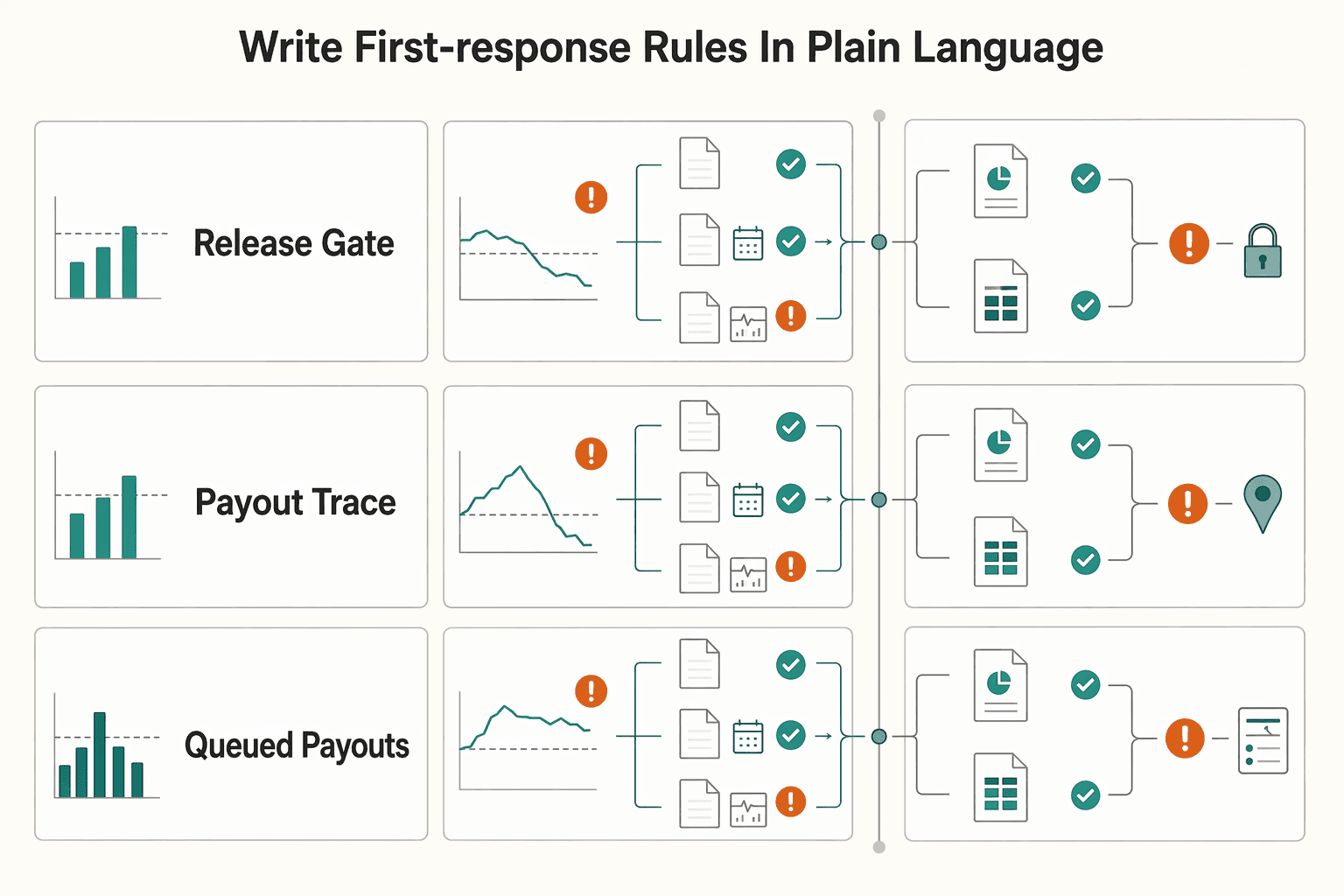

Write first-response rules in plain language#

When related metrics diverge, start with diagnostics before policy changes. Compare KPI performance to its objective, then confirm the issue against source evidence so you do not mistake a mapping or freshness problem for a real incident.

| Metric pattern | First diagnostic query | First owner | Avoid first |

|---|---|---|---|

| Payment failure rate rises while approval rate is stable | Check checkout step, processor slice, top decline-code cluster, and retry behavior | payments ops | Do not jump to pricing or fraud-policy changes before diagnostics |

| Approval rate falls | Check whether issuer, BIN, market, or payment-method mix changed | payments ops | Do not rely on one blended average alone |

| Settlement lag rises while payment success looks healthy | Check settlement report timing, payout calendar, and unmatched exceptions | finance ops | Do not call the payment flow healthy until cash timing matches |

| Queued payouts and pending balances both climb | Check funding position, provider acknowledgments, reserve holds, and beneficiary failures | treasury or payout ops | Do not widen payout windows before you know whether the issue is liquidity or execution |

Keep a short incident evidence pack for each red KPI: card definition, refresh timestamp, first diagnostic output, affected slices, and sample record IDs. That keeps response quality high when alert volume rises. Related reading: Finance Operations Priorities for Payment Platform CFOs.

If you are formalizing trigger bands and first-response playbooks, review how Gruv handles compliance-gated payouts, idempotent retries, and status visibility in Payouts, where supported.

Build a single source of truth across tools#

Once owners and response windows are clear, a common failure point is definition drift. If payment success rate, payment failure rate, or break counts change by screen, teams spend their time reconciling reports instead of fixing operations.

Define the policy once#

Treat your Single Source of Truth as a written operating policy, not a principle. For each operational metric, document:

- shared KPI definition and calculation logic

- consistent reporting window and timestamp rules

- consistent status definitions across systems

The goal is internal consistency, not an industry-wide schema. A central metrics layer helps because business logic gets defined once instead of being repeated differently across dashboards and reports. When logic changes, update it once and let downstream tools inherit the change.

A quick control works well here. Pick one KPI card, trace a few records from source data to warehouse table to final card, and confirm the logic and labels stay consistent. If they do not, fix the mapping before debating performance.

Put durable history in the data warehouse#

For finance review and executive reporting, keep durable history in the data warehouse or reconciliation layer. Adyen's Settlement details report exists to reconcile settlements at the transaction level, and its payment accounting report exists to match fees to payment statuses for invoice reconciliation. That separation is the point: finance needs a durable record that can explain what happened after the processor UI turns green.

For period-close checks, compare gross processed volume, net settled volume, refund totals, dispute totals, and unmatched items across the warehouse and provider reports before you publish a board-ready number.

Keep a short finance evidence pack: metric definition, warehouse refresh timestamp, comparison snapshot, unmatched count, and open exceptions affecting the period.

Be explicit about what alerts trust#

Alert noise often starts with an unclear read path. If one KPI reads from partial ingestion while another reads from validated warehouse tables, teams can page on unstable states and then waste time explaining why the numbers disagree.

For each alerting metric, declare the read path and limitation: near real-time events, validated warehouse tables, or provider-facing feeds. Use faster views for rapid response and validated views for finance control. If those views diverge, label one view operational and the other reconciled, then treat the gap as a data-quality investigation first.

For a deeper look at freshness-versus-validation design, see Building a Real-Time Payment Analytics Dashboard: Metrics Architecture and Computation. This pairs well with our guide on How to Build a Payment Health Dashboard for Your Platform.

Stop data distortion from duplicates and async events#

Duplicate control and status timing directly shape KPI trust. If you do not control them, you can distort reconciliation and financial reporting outputs and misread recovery trends.

Write idempotency into the metric policy#

Define idempotency in the metric policy so retries and reposts are not counted as new underlying outcomes. Document the event or transaction fingerprint that represents the same payment intent.

Use a staged control flow: ingest, normalize, exact match, review, then post, with audit logs across each step. Normalize payment ID, order ID, seller ID, currency, amount, and retry sequence before you count a new attempt, or duplicate webhooks and client retries can inflate both failure and recovery rates.

Keep review evidence explicit:

- idempotency key or equivalent transaction fingerprint

- normalized fields used in duplicate checks

- raw event timestamp and posted timestamp

- final duplicate decision and who or what made it

- audit-log reference for traceability

For finance-facing reporting, keep durable traceability from raw event to posted entry. Finance should be able to retrieve the duplicate decision, raw timestamps, posted timestamps, and audit trail without rebuilding the story from screenshots.

Separate user retries from system retries#

Treat user retries and system retries as different signals where your data supports that split. If you collapse them into one bucket, diagnosis gets harder and failure or recovery trends become harder to trust.

For headline KPIs, deduplicate at the customer-flow level, then keep retry-type cuts for investigation. If increases are mostly repost activity, check retry logic and posting controls first before drawing broader conclusions.

Mark async updates as provisional in BI#

When provider updates arrive asynchronously, keep reporting state explicit. For finance or executive views, consider flagging those records as provisional until matching confirms the outcome.

Show that status in BI instead of burying it inside query logic. Stripe's payout reconciliation report and Adyen's Company Payout report are good reminders that submission, provider acknowledgment, and final payout completion are separate events. If provisional and reconciled records are mixed without a visible flag, readers may treat moving numbers as final.

Also monitor the semantic layer itself. If a KPI changes meaning when you add a dimension, a filter, or a status mapping, investigate metric logic before blaming ingestion.

Check raw counts against deduplicated counts every cycle#

Run one control every reporting cycle: compare raw event counts with deduplicated KPI counts and log the variance. You do not need a universal threshold, but the gap should be explainable by known retries, async updates, or review-stage exclusions.

If the variance shifts unexpectedly, export process records to CSV and inspect concrete examples, not just aggregates. Build an investigation pack with count deltas, sample duplicate groups, provisional-to-final changes, and open exceptions before promoting numbers to executive reporting.

Connect revenue metrics to reconciliation and settlements#

Revenue metrics are useful early signals, but they are not enough on their own. Card-network dispute monitoring can escalate separately from authorization performance, so treat revenue leakage and recovery as operational indicators and interpret them alongside dispute, settlement, and reconciliation views.

Treat processor outcomes as the first view, not the last word#

Payment provider dashboards are useful for fast visibility, but they are only one layer. Settlement details reports and payout reconciliation reports exist because processor outcome screens and finance reconciliation screens answer different questions.

For your dashboard, review revenue leakage and revenue recovery alongside settlement status and matching exceptions. If a payment looks recovered in processor reporting but appears duplicated or unmatched in accounting or reconciliation views, keep it in exception handling until the break is understood.

When comparing high-impact records across systems, trace items end to end. If boundaries, timestamps, or statuses do not align, log them as open exceptions instead of forcing agreement in reporting logic.

Link front-door conversion metrics to back-office controls#

Failed authorizations and downstream control breaks answer different questions, so keep them separate. Failed authorizations show front-door conversion friction. Settlement and unmatched-item views can help show whether payment outcomes are closing in back-office operations.

A useful operating pattern is to investigate where the signal changes first. Check processor outcomes when authorization metrics move. Then use reconciliation and finance tooling to investigate leakage shifts that do not show the same movement in processor views. Cross-system comparisons get messy when boundaries, status mapping, or timing rules are mixed, so keep those rules explicit and stable over time.

Benchmarks need the same discipline. Use them carefully, and only compare trends when system boundaries and definitions stay aligned month to month.

Build a monthly evidence pack you can defend#

Keep a compact evidence pack that explains context behind the trend, not just the totals. Depending on your workflow, that pack can include:

- how duplicate attempts were handled before KPI interpretation

- the system boundaries and definitions used for cross-system comparisons

- the context used when benchmarks are applied

Totals alone can hide repeat break patterns. Keep the evidence pack close to KPI review. If you want a deeper design pattern for this layer, How to Build a Payment Reconciliation Dashboard for Your Subscription Platform is a useful companion.

For a step-by-step walkthrough, see Customer Success Metrics That Catch Payment Ops Failures Early.

Add payout execution and reserve controls for marketplace risk#

Once reconciliation and settlements are in view, outbound money needs equal attention. Stripe's account balances guide separates available and pending funds for Connect users, and that is exactly how a marketplace CFO should frame the liquidity side of payout risk.

Watch the payout queue, not just the final failure count#

Start with four payout-health signals: queued payouts, failed payouts, retry aging, and provider acknowledgment lag. These show where money is stuck before final outcomes tell the full story.

Define each one by lifecycle stage, not by broad status labels. If you cannot trace initiation, provider acknowledgment, and final funding state, queue metrics can mix true backlog with missing status updates.

| Metric | What it tells you | Verification detail | Common failure mode |

|---|---|---|---|

| Queued payouts | obligations waiting to move | check oldest item age, program, and whether an acknowledgment exists | internal holds mixed with provider-side delay |

| Failed payouts | submitted payouts rejected or returned | review provider code, beneficiary field, and rail | invalid beneficiary data or market-specific gate |

| Retry aging | how long open retries have stayed unresolved | separate first retry from repeated retries on the same payout ID | auto-retries hide the root cause |

| Provider acknowledgment lag | delay between submission and provider receipt | compare send timestamp to provider or webhook timestamp | event-ingestion delay mistaken for provider delay |

Sample records daily, not just trend lines. Validate payout ID, provider submission timestamp, acknowledgment timestamp, retry count, and owner on older queued items so you catch missing webhooks and bad status mapping early.

Pair payout obligations with funding and reserve visibility#

Payout reliability is also a liquidity control problem. Track payout obligations next to funding visibility and reserve balances, or queue growth can be misread as an execution-only failure.

This matters even more when faster payout options are in scope. According to the FedNow Service overview, instant payments clear and settle in near real time with 24x7x365 processing, while Nacha says Same Day ACH can move eligible payments of up to $1 million in a few hours. Data from Nacha's 2025 ACH Network Volume and Value Statistics shows Same Day ACH reached $3.9 trillion in 2025 inside an ACH network that processed $93 trillion overall. Set payout aging thresholds by rail and program, not as one global standard.

Keep a compact monthly evidence pack:

- payout-obligation aging by program or market

- available funding position versus scheduled payout volume

- reserve-held amounts and releases visible to ops and finance

- oldest blocked payouts with reason code, beneficiary country, and provider

When reserve movement is not visible beside payout demand, funding constraints can look like execution defects.

Use the right first response when failures rise#

If failed payouts rise while inbound success stays stable, start with provider routing and beneficiary-data quality checks before widening payout windows.

Routing can change outcomes based on value, urgency, and destination-bank capability, so routing or rail mismatch can contribute to failures without any front-door change. Beneficiary-data and localization issues can also trigger hard rejections at the gate.

Market-specific compliance requirements, including mandatory reporting, tax withholdings, and purpose-code rules, can vary by market and program. Confirm where those controls apply before setting universal queue-age or failure-rate thresholds, or you risk treating compliance holds as execution failures.

For more detail, read IPO Readiness for Payment Platforms Starts in Financial Operations.

What should a marketplace CFO monitor daily vs weekly#

A practical split is two cadences: a narrow daily page for exceptions and a weekly page for trend and cause analysis. The exact mix is yours to define, but the cadence should follow how quickly cash risk or seller impact can spread.

| Cadence | Metrics to review | Why this cadence works | Required evidence |

|---|---|---|---|

| Daily | approval drift, decline mix, payment failure rate, unmatched settlements, available versus pending balance, queued payouts | these are the signals most likely to change cash or seller experience before day end | record-level drill-down, owner, refresh timestamp |

| Weekly | segment trends, refund and dispute movement, fee variance, payout failure by rail or market | weekly review exposes pattern change without drowning the team in hourly noise | segment slices, exception summaries, threshold notes |

| Monthly | threshold changes, owner changes, retired metrics, board-ready summary | monthly governance is where you tune the metric contract itself | approved rationale, updated dictionary, review calendar |

Daily view#

Treat the daily page as an exception queue you can act on before the day ends. Keep the scope tight to a small set of high-signal KPIs aligned to your goals, each with predetermined thresholds and alerts.

Make drill-down quality non-negotiable. Every alert should trace to underlying records, break category, owner, and last refresh timestamp. If a tile cannot trace to a real record, it is not decision-ready.

Weekly view#

Use the weekly review for patterns, not noise. Compare trend views with static counts, and focus on whether movement is improving or drifting in ways that require investigation.

Prioritize trend and drill-down views over static counts. If daily alerts stay stable but weekly trends drift, investigate root causes before changing broader finance targets.

Monthly governance#

If you run a monthly governance review, treat it as an internal operating choice rather than a fixed external rule. Use it to tune thresholds, review ownership, and retire or replace metrics that no longer drive decisions.

Keep one executive page and one operator page, tailored by stakeholder, so decisions stay fast and information overload stays low. Record threshold or ownership changes and retired metrics with a short rationale.

Launch in 30 days with verification checkpoints#

A 30-day cadence can work as a practical example if you keep the sequence tight: define metrics first, validate mapping second, then ship and govern. If definitions are still unsettled in week 2, pause implementation and finish the metric contract first.

Week 1#

Finalize one metric dictionary for core payment KPIs before scaling dashboard logic. At minimum, define formula, source, owner, and status mapping so different teams can compute the same result from the same event slice.

Use this week's checkpoint as sign-off on the dictionary itself, not on visuals. Keep provider-specific labels out of executive KPI language, or you will create mismatches before launch.

Week 2#

Integrate events from the relevant backend services, centralize and normalize the data, then validate the mapping record by record. Real-time dashboards depend on ingesting events from multiple services and continuously computing rolling metrics, so translation errors can appear if you skip trace checks.

For verification, trace a small transaction sample from source record to normalized data row to dashboard tile and alert rule. Confirm event IDs, timestamps, and final status mapping, especially where events arrive late or repeat.

Week 3#

Run the dashboard against 30 to 60 days of historical data and simulate alerts before you expose it to executives. The goal is to see whether thresholds fire on the right incidents and whether the evidence pack supports a fast diagnosis.

Write the hypothesis for each alert, define the primary metric and guardrails, then document what would have triggered action. If surfaces disagree on direction, treat metric integrity as the first issue to resolve.

Week 4#

Publish production access after verifying dashboard behavior and alert routing, then lock in the operating cadence.

Close with documented governance for ongoing quality and distribution across cross-functional stakeholders. Final launch artifacts should include the approved dictionary, mapping verification notes, threshold dry-run decision, owner list, and review calendar.

Conclusion#

A strong payment operations dashboard is a decision system, not just a reporting surface. It connects each KPI to ownership, report lineage, and a clear first action.

Keep the distinction between metrics and KPIs explicit. A metric is any performance data you track. An operational KPI shows how well day-to-day work is being executed. When those get blurred, teams can lose clarity on what to act on.

Execution should stay disciplined and sequential. Define each metric, map it to the payment lifecycle, then tie it to settlement, accounting, balance, or payout evidence before you automate alerts. Dashboards help because they make operating efficiency easier to see, but clear definitions and consistent records make them usable for decisions.

Use monitoring cadence by purpose: operational metrics for near real-time feedback, and strategic KPIs for longer-term progress. Review KPI movement alongside the underlying operational metrics each reporting cycle, especially after changes to retry strategy.

Watch for the common failure mode: a dashboard that shows healthy approval while disputes, unmatched settlements, or payout backlog worsen off-screen. A blended green KPI is not a control system.

If you are operationalizing payment operations dashboard metrics, do it in this order:

- Build the metric table first: definition, source, lifecycle stage, owner, and intended action.

- Assign owners second: who investigates, who approves changes, and who is escalated.

- Automate alerts and executive reporting last: only from trusted states that have passed verification.

For a deeper implementation view, see Building a Real-Time Payment Analytics Dashboard: Metrics Architecture and Computation.

When you are ready to implement a single operational source of truth across collection, balances, and payout flows, start with the integration and event model in the Gruv docs.

Frequently Asked Questions

What metrics belong in a payment operations dashboard for a marketplace CFO?

Start with approval and payment success rates, decline reason mix, authorization latency, refunds, disputes, settlement lag, reconciliation breaks, available versus pending balances, queued payouts, failed payouts, and payout retry aging. A useful CFO view also shows amount-based versions of those metrics so finance can tie operational movement to cash movement.

What is the difference between approval rate, acceptance rate, and payment success rate?

Do not treat approval rate, acceptance rate, and payment success rate as interchangeable. Providers expose different payment stages and reports, so your team should publish a metric contract with numerator, denominator, retry treatment, time window, and source system on every executive card.

How do you prevent duplicate attempts from distorting payment KPI reporting?

Count raw attempts and deduplicated intents separately. Use an idempotency key or stable payment fingerprint, preserve raw and posted timestamps, and review the variance between raw events and dashboard totals every reporting cycle.

Which payment metrics should be tracked daily versus weekly?

Monitor fast-moving exception metrics daily and trend metrics weekly. Daily views usually cover approval-rate drift, dispute spikes, reconciliation breaks, available versus pending balances, and queued payouts; weekly reviews compare segments, thresholds, and owner actions.

How do you connect payment KPIs to reconciliation and payout reliability?

Pair customer-facing outcome metrics with back-office evidence such as settlement details, payment accounting, payout reconciliation, and unmatched exception counts. If approval rate looks healthy while settlement breaks or payout aging rises, the dashboard should surface that gap immediately.

How do you choose thresholds and owners for each metric without over-alerting?

Start from your own baseline and alert only when a metric has a clear first action. Put the owner, backup, escalation path, review window, and filter context on the card itself so alerting stays tied to evidence instead of noise.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- docs.stripe.com/declines/cardtrusted

- docs.stripe.com/disputes/monitoring-programstrusted

- federalreserve.gov/paymentsystems/fr-payments-study.htmtrusted

- federalreserve.gov/paymentsystems/fednow_about.htmtrusted

- docs.adyen.com/reporting/reports-and-the-payments-lifecycleexternal

- docs.adyen.com/reporting/received-payment-details-reportexternal

- nacha.org/same-day-achexternal

- nacha.org/content/ach-network-volume-and-value-statisticsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: