Quick Answer

Build your operating model around ownership clarity and evidence retrieval before transaction volume rises. Use one accountable owner per control lane, tie money movement steps to auditable records, and enforce a three-outcome launch gate with explicit stop authority. Then run recurring supervision on exception aging, stale evidence, and escalation drift. For cross-border intake, collect FEIE facts objectively, including the 330 full-day test and Form 2555 path, and route interpretation questions to specialist counsel.

Why compliance ops breaks at scale and how to prevent it#

Compliance ops usually breaks at scale because the operating design cannot keep up with payout complexity, not because teams stop working hard. If you expect payment volume to grow, design payout infrastructure, ownership, and evidence paths early so decisions stay clear and defensible.

For compliance, legal, finance, and risk owners running contractor payouts across markets, the warning signs are predictable. Reports stop matching, settlements get delayed, and manual reconciliation keeps expanding. These failures usually trace back to early architecture choices. Batch-heavy or tightly coupled designs create blind spots and delays, and make payment flows harder to trace. The commonly cited 10K-100K transactions/day range is a useful warning signal, not a universal rule.

This guide stays focused on operating design and control mechanics. It does not provide jurisdiction-specific legal advice or claim that one team structure works in every market. Use specialist counsel for market-specific obligations, and use this framework to clarify accountability, escalation, and evidence requirements, including capability reviews where needed, such as API-first infrastructure.

The target outcome is practical: clearer escalation points and auditable controls as payout complexity grows. At scale, even small mismatch rates can become material exposure. A 1% mismatch can imply about $10,000 in daily exposure, or roughly $3.6M annually. Prevention means fixing design gaps early instead of layering reactive approvals on later. For adjacent finance systems, see How to Build a Finance Tech Stack for a Payment Platform: Accounts Payable, Billing, Treasury, and Reporting.

Gather prerequisites before you design the team#

Before you size or split the team, get the operating facts straight. If you cannot explain who is moving money through your platform, how risk is monitored, which controls exist, who owns them, and where evidence lives, any org design will be guesswork.

| Prerequisite | What to do | Why it matters |

|---|---|---|

| Control inventory | Document active controls across KYC, transaction monitoring, and AML/sanctions, and name the current owner for each one | If ownership is unclear, treat that as a design blocker |

| Evidence pack and traceability | Pull a recent evidence pack, review the risk and operations signals your team already tracks, then confirm how risk is monitored in practice and who is responsible | Use a recent window that is large enough to be representative of current operations |

| Products in scope | List current support and planned additions, and tie rollout plans to updated review steps, exception handling, and ownership | This scope map shows where operational load and risk review will hit first |

| Control-environment assumptions | State which records and systems are authoritative when they disagree, and validate those assumptions in practice | If these assumptions are still disputed, pause team design until they are resolved |

- Collect the control inventory first.

Document active controls across key program areas such as KYC, transaction monitoring, and AML/sanctions, and name the current owner for each one. Separate policy ownership from operational execution, since each area can run as policy + operations even when "compliance" is treated as one function. If ownership is unclear, stop and treat that as a design blocker.

- Pull a recent evidence pack and test traceability.

Use a recent window that is large enough to reflect current operations. Review the risk and operations signals your team already tracks, then confirm you can answer clearly how risk is monitored in practice and who is responsible.

- Map what payment products are in scope now and next.

List current support and planned additions. This scope map shows where operational load and risk review will hit first. If rollout plans are not tied to updated review steps, exception handling, and ownership, fix that before adding headcount.

- Confirm control-environment assumptions before org design.

In embedded payments, your platform can be treated as part of the control environment. State which records and systems are authoritative when they disagree, and validate those assumptions in practice. If those assumptions are still disputed, pause team design until they are resolved.

If your record-of-truth model still needs work, How to Build a Deterministic Ledger for a Payment Platform is a useful companion.

Set operating boundaries and risk tiers first#

Set decision boundaries before you get pulled into cross-border tax edge cases. Use objective FEIE checkpoints for intake, then escalate interpretation to specialist counsel.

| FEIE intake point | Article fact |

|---|---|

| Applicability | The physical presence test applies to both U.S. citizens and U.S. residents |

| Basis | It is based on time abroad, not on residence type or return intent |

| Threshold | It requires 330 full days during any period of 12 consecutive months |

| Full day | A full day is 24 consecutive hours from midnight to midnight |

| Tax home | Days count only if the person's tax home is in a foreign country |

| Filing | FEIE is claimed on Form 2555, and excluded income is still reported on a U.S. return |

Mark specialist-counsel boundaries for cross-border tax questions.

Draw a hard line between operational routing and individualized tax guidance. Your team can collect facts and route, but it should escalate FEIE interpretation questions to specialist counsel.

For FEIE fact intake, stay objective. The physical presence test applies to both U.S. citizens and U.S. residents and is based on time abroad, not on residence type or return intent. It requires 330 full days during any period of 12 consecutive months. A full day is 24 consecutive hours from midnight to midnight, and days count only if the person's tax home is in a foreign country. FEIE is claimed on Form 2555, and excluded income is still reported on a U.S. return.

If tax home is unclear, travel gaps may break day counts, or time in-country may involve U.S. law violations, stop at fact collection and escalate. If the 330-day threshold is not met, the physical presence test is not met.

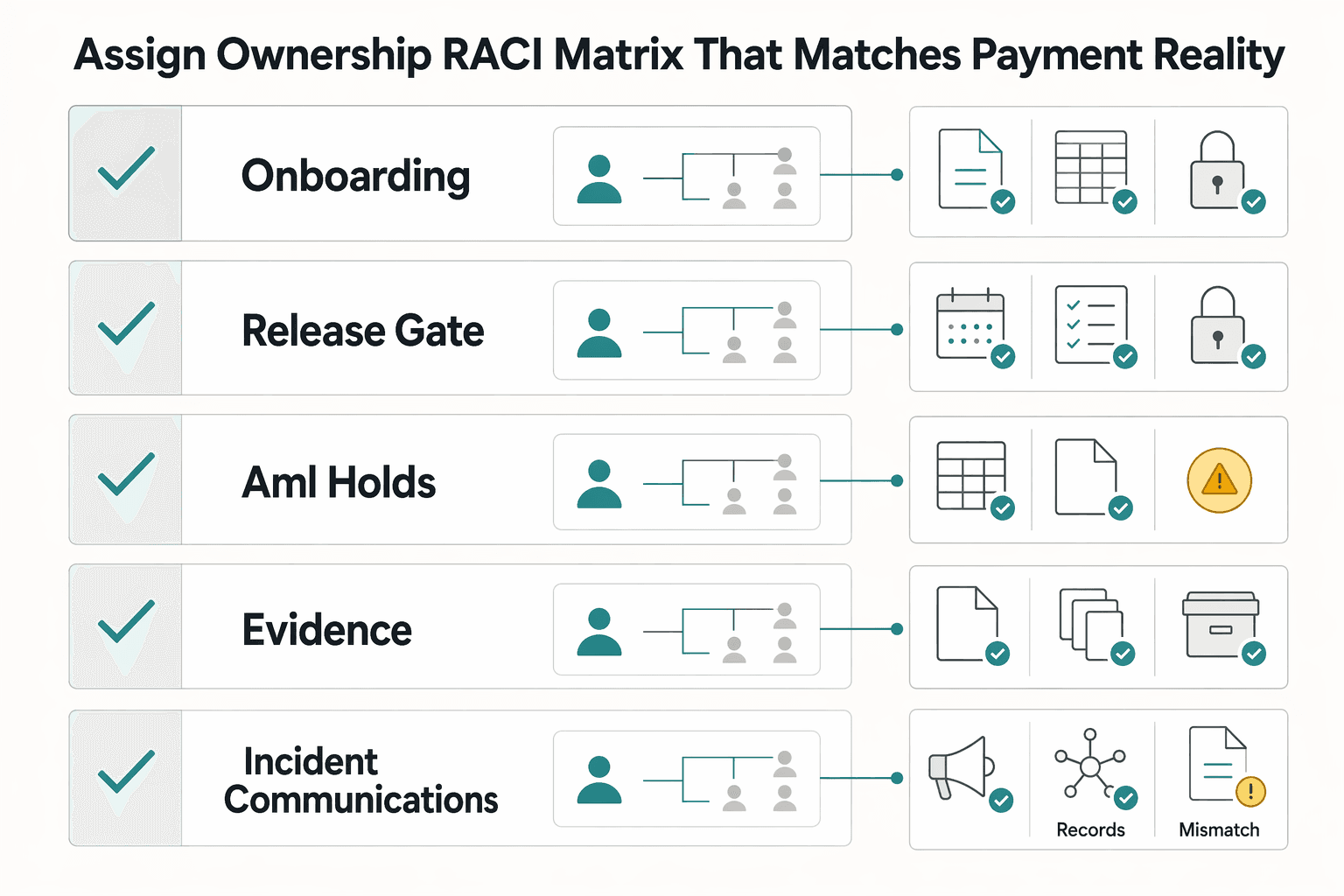

Assign ownership with a RACI matrix that matches payment reality#

Once scope is set, assign names to each control area. A RACI matrix helps keep payment controls from turning into shared but ownerless work. The core rule is simple: each control area has one accountable individual, even when multiple teams execute the work.

Build the matrix around control areas, not departments.

Build the matrix around where work breaks in practice, not around department labels. RACI has four components: Responsible, Accountable, Consulted, and Informed. More than one person can be responsible, but accountability should sit with one decision-maker who owns completion.

For a payment platform, common control-area rows can include:

- onboarding

- payout approval

- AML holds

- tax-document collection

- incident communications

Then include roles such as legal, risk/compliance, finance, and other delivery teams where they fit each row.

Put control-to-system mapping in the same table.

Keep people ownership and control evidence in one place. The practical matrix should show who owns the control, where it runs, and what record proves it happened.

| Control area | A: one named owner | R: contributors | C: roles to consult | I: roles to inform | System and evidence fields to capture |

|---|---|---|---|---|---|

| Onboarding | Owner name | [contributors] | [roles] | [roles] | intake system, access owner, audit-trail location |

| Payout approval | Owner name | [contributors] | [roles] | [roles] | approval workflow location, decision record, reconciliation record |

| AML holds | Owner name | [contributors] | [roles] | [roles] | case ID, trigger source, release/reject record |

| Tax-document collection | Owner name | [contributors] | [roles] | [roles] | intake location, validation status, audit-trail record |

| Incident communications | Owner name | [contributors] | [roles] | [roles] | status source, approved message owner, communication log |

If someone can name the accountable owner but not the evidence location, the matrix is incomplete.

Eliminate dual accountability and define handoffs during planning.

Dual accountability is where delays and errors start. If one team assumes another owns final approval, launches stall and exceptions linger.

Be explicit in each row: one accountable person, with other teams marked as responsible or consulted. Add handoff checkpoints during planning so ownership is clear before launch decisions:

- Scope checkpoint

If a feature changes payment or compliance controls, update the matrix row before build commitments are finalized.

- Change checkpoint

If system logic, permissions, or event handling changes, confirm whether accountable ownership also changes.

- Pre-launch checkpoint

Before go-live approval, confirm owner names, evidence fields, and escalation contacts are complete.

Test the matrix against real cases, not theory.

A matrix that works only on paper is not enough. Validate it with live examples, not just planning docs. Trace one onboarding review, one risk hold, and one incident. Then confirm who was accountable, who acted, who was consulted, what record proves the decision, and who communicated the outcome.

If answers vary by person, ownership is still unclear. If proof depends on manual reconstruction because evidence is hard to access, the matrix is likely incomplete.

Tie the matrix to your existing planning artifacts, such as milestones or roadmaps. Decision frameworks can help teams compare options, but they do not replace RACI when you need clear execution ownership. For a step-by-step walkthrough, see How to Set Up a Multi-Entity Payment Structure for Global Platform Operations.

Define launch gates with approve, conditional approve, and block outcomes#

Define one pre-launch quality gate with only three outcomes: approve, conditional approve, or block. At scale, ad hoc approvals break down, so keep the decision explicit and tied to evidence.

Set criteria against release-specific control risk.

Judge each release against the specific control risk it changes. For each release, assess control-test completeness, decision records, and audit trail completeness. Keep the review scoped to what changed, and use risk-adaptive checks based on customer type, transaction size, and regional requirements where relevant.

For compliance-sensitive verification controls, require evidence that the relevant changes were authorized, tested, and approved before implementation. If the team cannot clearly show what changed, how it was tested, and what decision record exists, do not treat the gate as complete.

Use a strict three-outcome decision rule.

| Outcome | When to use it | Required follow-up |

|---|---|---|

| Approve | Gate criteria are met and evidence is complete. | Proceed with normal launch controls. |

| Conditional approve | Remaining gaps are low-risk observability or documentation issues. | Add dated remediation, one owner, and escalation if remediation slips. |

| Block | Unresolved high-risk gaps affect compliance or verification controls, or key control behavior is unclear. | Escalate before launch. |

If open issues could weaken verification controls, increase fraud or failed-transaction risk, or create compliance exposure, block.

Require auditable signoff artifacts.

Do not rely on verbal approval or scattered chat logs. Require a signoff pack with change rationale, control-test evidence, and explicit approvals.

Your audit trail should include timestamped approvals, versions, and rationale. It should also include searchable, exportable change history showing who made the production-affecting change, when, and who approved it. Keep segregation of duties intact so the change creator is not the sole approver for production promotion.

Treat weak evidence as a launch blocker.

Weak evidence is not a paperwork issue. It is a launch-readiness gap. A quality gate works only if it blocks or records compliance before progression. If evidence depends on manual SQL or config edits without version control, or on reconstruction after the fact, treat that as a blocker now.

If you are formalizing approve/conditional/block criteria, review the implementation patterns in Gruv's developer docs.

Map controls to each money movement step#

Make the money path visible from start to finish, then map controls to each step. In embedded payments, that matters because your platform can be treated as part of the control environment, not just a front end.

Draw the operating path first.

Map the real sequence your teams run: onboarding, funding, payout release, and reconciliation, plus the points where screening or approvals affect whether funds can move. Build it per product flow, not as one generic diagram.

If Gruv modules are in scope, mark them explicitly:

Virtual Bank Accounts (VBAs): where enabled, where incoming bank-transfer funds are received and unmatched deposits are investigated.Merchant of Record (MoR): where enabled, where MoR responsibilities and exception ownership are defined.Payout batches: where approvals and provider submission occur.

Tie each step to a system record.

For each step, document the record you would use in a review: who initiated it, what decision was made, what provider or batch reference exists, and where review evidence is stored. If your flow uses webhooks, also document duplicate-delivery handling so repeated events do not trigger unintended downstream actions.

Use a simple map like this:

| Money movement step | Record to map | Failure state to plan for |

|---|---|---|

| Onboarding and approval | Decision record, approver, timestamp, related account | Stale status used in a later release decision |

| Funding and allocation | Funding event reference, internal match result, owner | Unmatched or misapplied funds |

| Payout release and submission | Approval record, payout batch ID, provider submission reference | Duplicate processing or release during a hold |

| Reconciliation and exceptions | Return or settlement record, exception owner, resolution log | Held or returned funds left unresolved |

Define failure handling at the same detail level.

Do not map only the happy path. Add explicit handling for stale data, duplicate event delivery, unmatched funds, and held or returned funds, including who owns each exception and what evidence you keep during resolution.

If any part of payout operations still depends on manual uploads, treat that as a scaling risk. As volume grows, manual uploads become error-prone and inconsistent, while automated bulk payout requests are easier to trace and review.

Confirm accountability and cross-team ownership.

Set ownership across engineering, finance, and compliance for each mapped step, because payout integration is not only an API task. Use clear first-line execution, second-line oversight, and third-line assurance so approvals, exceptions, and reviews stay auditable as volume scales.

Keep the scope broad enough. Compliance in payment flows is not only AML or KYC. Include the controls that affect fee disclosure and dispute handling where they apply to your program. For a finance-side view of the same process, read Finance Operations Priorities for Payment Platform CFOs.

Build the reporting checklist your team reviews every week#

Treat the reporting pack as evidence supervision, not a dashboard tour. If a metric cannot be traced to a source record, reconciliation record, or control evidence sample, it does not belong in the weekly review.

Define daily checks from live queues.

Start with the queues that can block operations or let compliance debt accumulate. Daily checks should focus on open control exceptions, stale evidence, reconciliation breaks, and contractor-payment documentation issues.

For each check, define the source record your team trusts:

- Control exceptions: current exception queue with owner and last update.

- Evidence freshness: evidence register showing what is outdated or missing.

- Reconciliation breaks: underlying reconciliation records behind the summary KPI.

- Contractor-payment documentation: W-9 collection status, TIN validation status, and record-accuracy exceptions.

Run a quick verification pass each day. Sample one item per queue and confirm owner, current status, and whether onboarding or payment processing is blocked.

Review weekly quality signals, not just volume.

Weekly review should test control quality, not just throughput. Include supervision quality, documentation quality, duplicated controls, and framework coverage gaps.

Sample real cases each week and confirm the documentation and linked evidence are complete enough to reconstruct what happened. If that chain is incomplete, treat it as a control weakness even if headline metrics look healthy. For a deeper discussion of audit-trail design, see What Is an Audit Trail? How Payment Platforms Build Tamper-Proof Transaction Logs for Compliance.

Add monthly control and tax-document checks.

Monthly review should surface slow failures before quarter-end or year-end bottlenecks. Track control exceptions, documentation updates, and contractor-payment documentation status.

Use this review to flag duplicated controls and coverage gaps across frameworks, and keep shared controls mapped once across programs. For contractor-payment operations, include explicit status checks for W-9 collection, TIN validation, and record accuracy, with clear owners for blocked items and cleanup.

Put cadence, thresholds, and owners in one table.

Keep checklist items, internal trigger rules, and escalation owners in one table so routing does not depend on memory.

| Cadence | Checks to include | Threshold rule to document | Primary owner | Escalate to |

|---|---|---|---|---|

| Daily | Open control exceptions, stale evidence, reconciliation breaks, contractor-payment documentation issues | Internal trigger for unusual growth, aging, or unresolved blocks | Compliance ops or onboarding ops | Compliance lead, engineering on-call, or payments ops lead |

| Weekly | Supervision quality, documentation quality, duplicated controls, framework coverage gaps | Internal trigger for quality drift, repeated gaps, or missing evidence | Risk or compliance manager | Head of Compliance, product owner, or engineering manager |

| Monthly | Control exceptions, documentation updates, W-9/TIN/record-accuracy status | Internal trigger for unresolved exceptions, overdue updates, or documentation backlog | Compliance lead or tax owner | Legal, finance leadership, or executive sponsor |

Close each cycle with one reconciled leadership summary: metrics snapshot, incident log, remediation status, and open risks. If the summary and underlying data disagree, fix the report before review. If you want a deeper dive, read How to Build a Payment Compliance Training Program for Your Platform Operations Team.

Set escalation SLAs before incidents force you to improvise#

Set escalation SLAs before incidents happen so responders do not improvise under pressure. Define severity and routing, assign one accountable owner per escalation, and alert early enough to act before a breach window closes.

| Routing input | What to document | Article note |

|---|---|---|

| Incident type | Incident type and impacted workflow | Different incident types can require different escalation routes |

| Severity | Current severity level | Use severity labels to push incidents into the right workflow immediately |

| Duration | Incident duration and trend | Different durations can require different escalation routes |

| Scope | Scope of impact across systems or teams | Different impact scope can require different escalation routes |

Classify incidents by severity and scope.

Not all incidents should follow the same path. Different incident types, durations, and impact scope can require different escalation routes.

Route lower-severity issues to junior responders and higher-severity issues to senior or specialized responders. Use severity labels to push incidents into the right workflow immediately, similar to SEV 3 versus SEV 1 routing.

Document your core routing inputs in writing:

- incident type and impacted workflow

- current severity level

- incident duration and trend

- scope of impact across systems or teams

Add a practical checkpoint. Responders should be able to escalate directly within the incident ticket, with the next contact and backup path visible in that workflow.

Name escalation and handoff authority before you need it.

Name authority in advance: who can take over an incident, who is the backup path, and who owns cross-team communication while the incident is open. Keep one point person accountable for progress so escalations do not stall between teams.

Before major state changes, require a ticket-linked handoff pack:

- incident summary and current severity

- affected systems or workflows

- reason for escalation and current owner

- linked ticket context and relevant system references

- next decision checkpoint and approver

Alert before the SLA boundary, not at it.

Alerts that fire at the exact breach point are usually too late. Set them before the SLA boundary so backup responders have time to step in.

A practical benchmark is alerting at 50% of the degradation budget. Apply that same logic to escalation windows so backup responders can review context and decide whether the issue is contained or expanding.

Prewrite internal incident messages from one approved source.

Prewrite internal incident updates and anchor teams to one approved status source. This can reduce message drift across support, finance, and operations during high-impact incidents.

Keep templates short and operational:

- what happened

- what is affected

- current containment status

- what teams should say externally

- when the next update is due

One owner, one ticket, and one status source helps keep escalation communication consistent. We covered this in detail in Internal Payment Audit Trail for Platform Compliance.

Reduce manual reviews without increasing regulatory risk#

A safer way to reduce manual review volume is to tune controls in small, evidence-backed steps, not to loosen checks broadly. Start with conservative verification rules, then relax only where your own case evidence shows noise rather than material risk.

Start conservative and isolate one rule family at a time.

KYC-driven identity verification is a core fraud-prevention control, so treat early review volume as a signal to analyze before changing rules. If you change multiple onboarding controls together, you lose attribution for what improved speed versus what weakened detection.

Change one rule family per release window. Keep each change note short: current rule, proposed rule, reason, expected effect. Keep the evidence path intact from decision input to decision output to exportable audit trail, because lower queue volume is not a win if reviewability breaks. This is where audit trail discipline matters.

Split noisy false positives from material true positives.

Separate high-cost false positives from high-risk true positives so analyst time stays focused on material risk. A quick reviewed-case classification is enough to start:

- Cases cleared quickly because logic was broad, data already existed, or a mismatch was operationally harmless

- Cases that surfaced a real identity, business, or AML concern

- Cases delayed because control output lacked enough linked evidence

If one control issue creates separate manual analysis in risk and compliance, fix that linkage before loosening rules. A practical checkpoint is that one control test should support both risk validation and compliance audit needs.

Validate changes before production with test evidence.

In real-time payment operations, compliance runs alongside payment execution, so rule changes need pre-production evidence. Use pre-production testing for forward behavior and, where possible, historical replay for old-versus-new comparison.

For each change, keep an evidence pack with:

- Exact rule logic changed

- Sample test or replay cases under old and new logic

- Expected impact on manual review volume

- Expected impact on AML alert quality

- Named signoff and rollback owner

Treat "faster approvals with unclear alert impact" as a warning, not a success.

Track outcomes after release and roll back when quality drops.

After release, track AML alerts, approval time, and rework rate together. Approval time shows queue movement, rework rate shows whether work shifted downstream, and alert trends show whether signal quality held.

Review quickly, not just on a long cycle. In an integrated risk-and-compliance model, control-effectiveness changes should update both risk exposure and compliance status. If speed improves while review quality drops, roll back and document why.

Decide what to build in-house and what to buy#

Make the ownership decision by control area, not as one all-or-nothing call. If your team cannot run alert generation and queue processes reliably over time, buying core compliance infrastructure can be the lower-risk path while you keep policy ownership, approvals, and exceptions in-house.

Separate decisions by control area.

Do not force one answer across every compliance control. The core question is whether you want full lifecycle ownership from launch to sunset, including training, maintenance, and support. Custom builds can take months, or even years, while proven pre-built options are often faster and lower risk.

| Area | Build in-house if | Buy if | Verification point |

|---|---|---|---|

| Alert generation | you can design, maintain, and continuously operate alert generation | you need production capability sooner with lower delivery risk | you can consistently generate and review alerts |

| Queue operations | you can establish and run a queue process with clear ownership | you cannot operate queue handling consistently today | queue intake, review, and escalation are documented and operating |

| Policy exceptions and governance | you can own lifecycle governance, including training and support | you want less platform operating burden while retaining approval authority | exceptions are documented and formally approved |

Judge options on operating reality.

Judge tools on what happens after launch, not just on what looks good in a demo. Use criteria that still matter later: implementation burden, control visibility, and whether review and escalation responsibilities are clear. A strong demo is not enough if you cannot show how alerts are handled and what evidence is retained when a case is cleared.

Use your exceptions process as a governance checkpoint. If policy exceptions cannot be documented and formally approved, governance is weak regardless of whether you build or buy.

Document the decision and re-check when scope changes.

Treat this as a durable choice, because switching paths later can be messy and time-consuming. Record why you built or bought, what evidence must be retained, who owns ongoing operations, and who responds when controls fail.

Revisit that decision when your operating footprint changes materially. Scope changes can alter queue pressure, alert timing, and evidence needs. This pairs well with our guide on Build a Global Contractor Payment Compliance Calendar for Monthly, Quarterly, and Annual Obligations.

Expand across markets in controlled phases#

Expand in phases only when your current fraud and compliance operations can absorb more volume without losing decision quality.

Launch where operating control is already stable.

Prioritize operational readiness before adding a new market. If your setup still depends on static rules and engineering-dependent changes, expansion can expose that lag as fraud patterns shift. Treat launch readiness as your ability to adjust decision logic quickly, test changes safely, and keep existing integrations stable.

Add local controls one layer at a time.

Do not switch on every local workflow at once. Add one layer, confirm it works end to end, then add the next. If a new layer cannot be monitored and reviewed reliably, keep it in pilot scope until it can.

Keep the decision path consistent across markets.

As local checks vary, keep a consistent decisioning layer so trusted risk data and existing integrations stay in place while logic evolves. This makes it easier to test rules and models in parallel without disrupting low-latency payment decisions.

At scale, the tradeoff is constant. Too much friction can slow growth, while missed fraud can erode trust and unit economics. Teams that can test and deploy logic quickly, including parallel runs, are better positioned to expand without losing control.

Common mistakes and how to recover quickly#

After phased expansion, breakdowns often come from ownership and evidence discipline, not obscure rules. Recovery is usually faster when decision rights are clear, evidence is easy to retrieve, and process changes are checked before they affect live outcomes.

Bring compliance in before build locks.

If compliance enters after product flows are fixed, risk exposure can rise as payment responsibilities expand. Set the operating model before detailed flow design, and confirm clear answers to three questions: who is moving money, how risk is monitored, and what happens when something looks wrong.

Remove escalation ambiguity.

When escalation ownership is unclear, incidents can stall across teams. Recover by documenting accountable owners, handoff rules, and backup coverage so pressure decisions do not depend on ad hoc chat threads.

A practical structure is three layers of accountability: first-line operational ownership, second-line compliance oversight, and third-line independent assurance.

Tie monitoring to retrievable evidence.

Dashboards without retrievable records can create reactive fire drills. For high-priority alerts, reviewers should be able to reach the underlying transaction and review records without rebuilding the case manually.

This is where spreadsheet-led operations tend to fail. Context gets fragmented, obligations are missed, and review slows down. Deadline fragmentation across states is a common stress point, and the coordination burden grows quickly as state count rises. For more on evidence design, see What Is an Audit Trail? How Payment Platforms Build Tamper-Proof Transaction Logs for Compliance.

Check automation changes before rollout.

Automation can reduce spreadsheet workload, but unchecked changes can still create missed obligations and reactive fire drills. Before rollout, test proposed logic against recent cases and verify escalation paths still hold under real patterns.

If reviewers cannot explain why outcomes changed, treat that as a control warning and pause deployment until the change is understood. Related: The Payment Operations Maturity Model: How to Benchmark Your Platform Finance Team.

Conclusion and copy-paste implementation checklist#

If you want compliance ops to hold up under more volume, more rails, or more markets, focus on three things first: clear ownership, retrievable evidence, and explicit stop authority for money movement. Use this checklist as a final readiness pass.

- Confirm scope in writing.

Document the products, payment rails, jurisdictions, and third parties currently live. Keep one shared version across product, compliance, legal, finance, and engineering so incident reviewers can see which flows and external touchpoints are in scope.

- Publish ownership with one accountable owner per control.

Maintain a RACI for onboarding, review, payout release, incident communication, reporting, and evidence retention. Avoid split final authority; name one accountable owner per control and list supporting roles separately.

- Enforce launch gates with explicit outcomes.

Define clear approval outcomes (approve, conditional approve, or block) with criteria written before release pressure rises. For conditional approvals, require a dated owner, post-release evidence requirements, and rollback criteria. For blocks, state what must be fixed before review resumes.

- Run one reporting pack leadership can trust.

Keep backlog shape, false-positive movement, unresolved escalations, and evidence completeness in one reconciled view. As a useful benchmark, OCC payment-systems risk management explicitly includes internal controls and management and board reports.

- Test and tune only when the process is mature.

Do not automate unstable review logic. Use process maturity as the automation-readiness check so automation does not scale inconsistency.

- Set escalation paths and freeze authority before incidents.

Define who can freeze affected flows, who can approve release, and what evidence is required before movement resumes. The key is clear handoffs and one agreed status source across legal, support, finance, and product.

- Expand only after control and evidence readiness is proven.

Roll out new markets or rails only after ownership, reporting, and retrievable records meet your baseline. Keep third-party risk management in scope, and organize artifacts so partner or examiner-style review is straightforward, including materials such as an Internal Control Questionnaire and, when relevant, the 12 CFR 7.1026 Compliance Worksheet.

When you are ready to map this control framework to your payout operations and market rollout plan, talk with Gruv.

Frequently Asked Questions

What is the minimum viable compliance ops team for a scaling payment platform?

There is no fixed minimum headcount, but there is a minimum separation of responsibility. You need first-line operational ownership, second-line compliance oversight, and access to independent assurance, even if that third-line support is lightweight early on. If one person is onboarding users, deciding AML exceptions, and signing off launches alone, that concentration creates a control gap.

When should compliance approve, conditionally approve, or block a launch?

There is no single numeric cutoff. Approve when controls are working in practice and evidence is retrievable, not just documented. Use conditional approval for limited, low-risk gaps with a named owner and remediation plan that do not weaken core onboarding or money-movement controls. Block when unresolved gaps affect onboarding, money movement, or your ability to produce complete records for review or partner due diligence.

How do you cut manual reviews without weakening AML coverage?

Start conservative, then relax rules only where your own review data shows unnecessary manual review. Test proposed changes in a controlled mode and compare outcomes before release. If volume drops but reviewers cannot explain why the changed cases remain low risk, roll the change back and reassess.

What must be on a compliance operations dashboard each week?

Each weekly view should combine workload, manual-review trends, unresolved escalations, and evidence-completeness checks. Keep incident status, remediation progress, and open risks in one leadership pack so decisions are made from the same picture. A practical check is whether a sampled alert can be traced quickly to the underlying transaction and retained records.

Which escalation triggers require immediate legal or executive review?

Common immediate-escalation triggers include unresolved AML concerns that could affect customer fund movement, missing evidence for live money movement, or cross-market uncertainty that could change customer treatment at scale. If an issue could force a launch block or weaken your response to partner due diligence, involve legal or an executive early.

How do you choose build versus buy for compliance infrastructure?

There is no universal answer. Buy core tooling when your team cannot reliably sustain monitoring, rule tuning, evidence retention, and escalation responsiveness internally, while keeping policy ownership and final decisions in-house. Build when you need tighter control visibility and can support the operational burden, and ensure either path gives you exportable records, usable history, and clear failure ownership.

How should a platform phase controls when entering new markets?

Phase expansion by control readiness, not revenue demand alone. Start in markets where your existing onboarding and AML controls can meet a consistent evidence standard, then add market-specific obligations gradually. Before launch, confirm each market flow can produce exportable records end to end.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- azdhs.gov/documents/preparedness/emergency-medical-ser...trusted

- dema.az.gov/sites/default/files/2025-09/Annual_Report_20...trusted

- fcic-static.law.stanford.edu/cdn_media/fcic-testimony/First%20Public%20He...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- mohave.gov/media/qimh4dfw/mohave-county-eop-7125.pdftrusted

- occ.gov/publications-and-resources/publications/comp...trusted

- policies.trinity.edu/a8376318-ebd6-421f-be63-acf8c88376a1_6384531...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: