Quick Answer

Start by limiting scope to workflows that can hold, release, reroute, or investigate funds, then assign mandatory role-based training with named escalation ownership. Build a role-to-obligation matrix, attach each module to retrievable case evidence, and run a 90-day rollout with hard gates so teams cannot advance without live-case verification. This approach shifts training from course completion tracking to a working control that supports consistent decisions and defensible records.

Build Training Around Real Payment Compliance Decisions#

If your team can hold, release, reroute, or investigate payouts, treat training as a control, not an HR checkbox. This guide lays out a phased rollout with clear owners, decision checkpoints, and escalation paths before money moves.

It is written for compliance, legal, finance, and risk leaders managing contractor, seller, or creator payouts across multiple markets. In that setting, small operational mistakes can turn into compliance gaps quickly when ownership and escalation are unclear.

Compliance training teaches people the laws and policies that apply to their jobs. In AML/BSA-oriented payment operations, training should be risk-based and role-specific. The person handling onboarding checks, the person approving payout release, and the person reviewing suspicious activity should not get the same depth of training.

Training should sit inside your compliance program, not beside it. In practice, training is a core control alongside written policies, recordkeeping, and internal audits. In AML/BSA contexts, it is commonly treated as a documented, recurring control for financial institutions and many fintechs handling money movement. Some frameworks also treat training as one of four AML program pillars, along with internal controls, independent testing, and a designated compliance officer.

The goal is not course completion alone. The goal is to run decisions inside live controls, policy gates, and a defensible audit trail. A useful check is whether you can reconstruct a real decision record: which policy applied, who reviewed it, what evidence they used, and where it escalated when it exceeded team authority.

Related: 3 Ways to Upskill Your Platform Finance Team: Payments Compliance and Automation Training.

Set your scope and risk tier before choosing training#

Set scope before curriculum. Define where decisions can change money movement, then train those workflows first.

Step 1 Choose the first in-scope payment surfaces#

Start with the payment operations that carry the most compliance risk in your current product and markets. Use one filter for first-wave scope: can this action block, hold, release, reroute, or investigate funds?

For each surface, name three things before you proceed: the operating owner, the jurisdiction or market, and the record that proves the decision. If you cannot point to the queue, case type, or audit artifact, narrow the scope again.

Step 2 Tier obligations using hard requirements first#

Build your first risk tiers around AML/CTF controls as the practical anchor. AML/CTF obligations tie directly to transaction monitoring, KYC processes, and reporting checkpoints such as SAR handling, so they are a defensible starting point for role depth and assessment.

Then layer in other applicable requirements by market, without forcing one global standard across all jurisdictions. Requirements and enforcement exposure vary by jurisdiction, so tier by jurisdiction-specific risk rather than a single global label.

Step 3 Set your internal decision rule for mandatory training#

Use a simple internal rule: if a workflow can block, hold, release, or reroute funds, treat it as high-priority for mandatory training and documented escalation ownership. That turns training into a control inside your compliance management system, not a standalone awareness activity.

Keep a short baseline module for broad coverage, but pair it with role-specific training plus monitoring and reporting. Otherwise, teams may complete training while live decisions drift, and that often shows up later as inconsistent handling or operational disruptions such as account suspensions.

If you want a deeper dive, read How to Build a Compliance Operations Team for a Scaling Payment Platform.

Prepare the inputs you need before day one#

Build the input pack before assigning training so people learn against real records and documents, not abstract policy.

Step 1 Gather your control inventory and tag known obligations#

Start with the controls you already run, and keep them in one sheet: control name, owner, payment surface, market, proving record, and named obligation.

For the obligation field, use the labels your team already use for that surface, and flag anything that still needs legal review.

Use one checkpoint: every row must point to a proving record you can retrieve.

Step 2 Pull baseline evidence from live operations#

Pull the baseline from live operations, not from memory. Collect retrievable records and audit-trail evidence.

Record version or date, owner, and review status so the baseline is usable when you update training later. If teams still scramble for records and hunt for audit trails instead of retrieving them quickly, log that as an exposure now.

Step 3 Inventory tax and documentation steps#

Map where Form 1099-K and related documentation handling appear in your payment flow, then note the owner, storage location, and follow-up trigger for each touchpoint.

Where Form 1099-K logic is in scope, keep a version or date checkpoint with the source material. IRS FS-2025-08 (Oct. 2025) describes Form 1099-K reporting context, notes that FAQ content may be updated, and states that controlling law governs tax liability.

If your materials mention thresholds, keep the context aligned to that same fact sheet. As described there, the reinstated TPSO condition uses both a gross-amount and transaction-count test (more than $20,000 and more than 200 transactions), and the prior ARPA background rule used a $600 trigger regardless of transaction count.

Step 4 Rank market exposure for first-wave coverage#

Prioritize the first training wave by known exposure, not by what is easiest to package.

A compact grid is enough: market, payment surface, open issue, evidence source, and decision owner. Start where gaps are highest impact, then expand once those paths are stable.

For a step-by-step walkthrough, see Internal Payment Audit Trail for Platform Compliance.

Step 1 map roles to obligations and escalation owners#

Build this as a routing matrix so no one has to guess who takes first action, who owns escalation, and where handling evidence is captured.

Without a defined matrix, teams fall back on tribal knowledge and ad hoc routing. That is where reports stall, land with the wrong handler level, or get handled inconsistently. A documented intake-to-assignment path by report category improves consistency and audit readiness.

Build the matrix as a routing document#

Treat the matrix as a decision tree with four routing inputs. A practical set for each row is:

- Report category

- Severity level

- First response owner

- Escalation owner

Use report categories from real operations. Add a severity field and keep triage simple at first. A three-tier model is a practical baseline, and Tier 1 (Low) can cover isolated issues with limited legal or financial exposure.

Map obligations to controls, not just to departments. Each row should make ownership operational and testable, including where evidence is captured.

Create one row per role and obligation#

Cover operations, legal/compliance, risk, finance, support/disputes, product, and engineering. Keep each row tied to what that role actually decides in production.

| Role | What to map in the matrix | First response owner | Escalation owner | Behavior-change sign-off |

|---|---|---|---|---|

| Operations | Intake and queue-routing obligations and controls | Named operations lead | Named escalation owner by severity | Control owner for the mapped obligation |

| Risk | Investigation-routing obligations and controls | Named risk lead | Named escalation owner by severity | Control owner for the mapped obligation |

| Support/disputes | Intake, triage, and case-handling obligations and controls | Named support/disputes lead | Named escalation owner by severity | Control owner for the mapped obligation |

| Finance | Documentation and reconciliation obligations and controls | Named finance lead | Named escalation owner by severity | Control owner for the mapped obligation |

| Product | Workflow or release obligations that affect controls | Named product lead | Named escalation owner by severity | Control owner for the mapped obligation |

| Engineering | Control logic and audit-trail obligations | Named engineering lead | Named escalation owner by severity | Control owner for the mapped obligation |

| Legal/compliance | Regulatory interpretation and exception obligations | Named legal/compliance lead | Senior escalation owner for highest severity | Control owner for the mapped obligation |

Add trigger-based handoffs#

Use named, observable triggers for escalation. Avoid vague rules such as "escalate when needed."

For each trigger, define who pauses current handling, who is notified, and who logs the handoff. Then test consistency by routing a small sample of recent cases using only the matrix. If reviewers do not land on the same owners, tighten the definitions.

Add an accountability field that proves change#

Do not stop at training completion. Add one accountability field per row for the person who signs off that the mapped control was followed in production.

Tie that sign-off to evidence paths such as reviewed case samples, QA checks, escalation records, or annotated queue decisions. If a role can materially change case handling, that role needs both a first-response owner and an escalation owner in the matrix.

Related reading: Digital Nomad Payment Infrastructure for Platform Teams: How to Build Traceable Cross-Border Payouts.

Step 2 build a curriculum by risk tier and decision impact#

Build the curriculum by risk tier, not as one generic catalog. Keep a baseline for all roles, deeper training for people who can change live outcomes, and specialist modules where the exposure is specific.

Separate baseline from decision-critical training#

Use Payments Compliance 101 and Payments Compliance 201 as internal labels so role depth is explicit.

- 101 (baseline): shared language, escalation routes, and required handoff evidence.

- 201 (decision-critical): roles that can change live outcomes in operations.

A useful check is whether reviewers in 201 route the same sample case to the same owner and evidence path consistently.

Assign specialist modules only where exposure is real#

Keep specialist topics out of general onboarding and assign them only to roles that actually touch those decisions. For tax-adjacent operations, keep the scope focused on intake, document handling, and escalation, not tax advice.

For FEIE awareness, use concrete checkpoints your team can apply:

| FEIE checkpoint | Article detail |

|---|---|

| Return filing | Claiming FEIE does not remove the need to file a return reporting the income |

| Physical presence test | 330 full days in 12 consecutive months |

| Full day | 24 consecutive hours |

| Missed 330-day test | Not excused by illness, family issues, vacation, or employer orders |

| Time in a foreign country in violation of U.S. law | Does not count |

| Form | Form 2555 (or 2555-EZ) |

For role-based certification depth and failure conditions, include concrete training artifacts:

- Require an annual standards-of-conduct certification check.

- Require intake/interview and quality-review certification for roles that prepare or review returns.

- Require a signed pre-service conduct agreement.

- Define formal sanctions for noncompliance.

Use the IRS Practice Unit as a training aid for document paths, but not as binding legal authority.

Add a pre-production readiness gate#

Course completion is not enough. Before anyone handles controlled queues solo, require a signed attestation and reviewed case samples tied to the role's escalation matrix.

Compare external options by role fit and launch speed#

If you evaluate external programs, verify fit and implementation details before making a purchase decision.

| Option | Role relevance to confirm | Implementation speed to confirm | Evidence to request |

|---|---|---|---|

| External program | Which matrix roles it actually supports | Enrollment, total hours, assessment cadence | Syllabus, assessment method, completion proof |

| Internal modules | Mapping to named obligations, queues, and escalation triggers | Assignment, review, and sign-off cycle by role | Module outline, case checklist, sign-off record |

Use external programs where the syllabus clearly matches your risk profile. Keep operator-facing training tied to your own controls and escalation paths.

We covered this in detail in Build a Global Contractor Payment Compliance Calendar for Monthly, Quarterly, and Annual Obligations.

Step 3 decide external certification versus internal sign-off#

Decide based on evidence needs: use external certification for more standardized validation, and internal sign-off to prove people can execute your procedures in your environment.

Do not treat completion alone as assurance. In CMMC materials, self-assessment and certification are separate paths, and the guidance itself is not legally binding. The takeaway is simple: guidance completion is not a legal safe harbor, and external certificates do not replace operational proof.

Use external certification for standardized depth#

Use external programs when you need a common benchmark across compliance, risk, legal, and audit stakeholders. Evaluate them as assessment tools, not as substitutes for readiness inside your own controls.

Before approving budget, require four items in writing:

- syllabus

- latest substantive update date

- assessment method

- completion evidence

If the evidence is only attendance or recall-level quizzes, treat that as exposure, not proof of decision quality.

Use internal sign-off for execution quality in your controls#

Use internal sign-off when your main risk is process variance. Test the exact steps that affect decisions, evidence handling, and escalation timing.

| Sign-off record element | What to include |

|---|---|

| Sample cases | Reviewed sample cases with decision notes |

| Checklist | Checklist of required evidence and escalation triggers |

| Owner sign-off | Named owner sign-off based on observed work |

| CAPs | CAP records for failed checks |

| Procedure changes | Dated procedure-change checklist when controls are modified |

A practical verification pattern is:

- interview: confirm escalation logic and ownership

- examine: review the evidence package and decision trail

- test: run live or simulated cases

When checks fail, route them through documented corrective action plans (CAPs) and retest before solo handling.

Screen options with the same fit test#

Use the same fit test whether you buy, build, or blend. Pilot one external option with a small cohort, keep internal practical checks for broader execution, and scale only when the results justify it.

| Candidate path | Role fit to verify | Update evidence to request | Operational applicability test |

|---|---|---|---|

| External certification option | Which roles need standardized external validation vs internal sign-off | Last syllabus revision date and change communication process | Applied assessment sample plus completion proof |

| Internal sign-off path | Which roles need decision-level validation in live workflows | Procedure-change checklist and version history | Case reconstruction, evidence quality, and escalation accuracy |

If a provider cannot show update cadence, applied assessment, and completion evidence, pause procurement. If your internal path cannot produce reviewed cases, CAPs, and checklist trails, it is not sign-off yet.

Step 4 connect training to live controls and system behavior#

Training only counts as a control when it shows up in daily work. Each module should map to a real decision point, required evidence, and a retained record. If it does not change operator behavior or case records, it is awareness, not control.

Translate modules into observable checkpoints#

For each module, define in writing:

- the trigger for review

- the decision the operator can make

- the minimum evidence required before moving the case

- the escalation owner when evidence is missing or conflicting

That keeps training testable and exposes content that is too abstract for decision-level sign-off.

Tie outcomes to records and reporting you can review#

Measure outcomes in artifacts, not completion rates. Use case records that show fair, consistent decisions and retention-ready evidence, then test whether a second reviewer can follow what happened from the stored record.

Your reporting view should also support practical oversight: compare actual reimbursements to expected payments, quantify underpayments, and use filters and search to review cases across operational levels.

Drill failure patterns before they hit production#

Drill the failure modes that actually break handling in production. Use case-study exercises focused on missed warning signals and alternative decisions, not recall quizzes. Prioritize recurring error patterns and require handlers to leave enough evidence for later review.

Set a clear checkpoint for the program: if reviewers cannot reliably follow decision trails in records, treat that as a remediation signal before scaling the module.

Step 5 build the reporting pack leaders and auditors expect#

Once training is tied to live controls, you need reporting that proves it. Build one repeatable pack on a fixed cadence so a leader or auditor can answer core evidence questions from a single place. It should make ownership, exceptions, and unresolved risk visible with traceable records.

Define one recurring pack and keep the contents fixed#

Use one format each cycle, even when multiple teams contribute. Keep the same section order so the pack is easy to review and defend.

Include, at minimum:

- completion by role

- overdue items and approved exceptions

- completion on updated modules versus remaining gaps

- clear control ownership

Keep the role-based requirements view, or training matrix, as the anchor. Show who was required, who is overdue, who has an approved exception, and who completed updated modules after changes. Include version context so leadership can see who completed the update and who still has gaps.

As a practical check, your team should be able to filter the cohort, export completion and overdue status, attach artifacts, add version context, and send the pack quickly. If that still depends on scattered spreadsheets, inboxes, shared drives, and HR folders, the pack is not audit-ready.

Break reporting out by obligation, not just by team#

Do not rely only on team rollups such as "support" or "risk ops." Add obligation-level lines for the requirements and control areas that apply to your platform. This is a management view to expose concentration risk, not a universal legal template.

Without that split, overall completion can look healthy while one obligation lane is slipping. If the dashboard cannot isolate that concentration, leadership sees activity but not exposure.

Attach proof, not just summary numbers#

Summary metrics are not enough. Attach evidence that makes the claims verifiable, such as decision logs, policy attestations, sample case reviews, and audit trail extracts.

These attachments are not universally mandated in every context, but they turn "training delivered" into "training proven." Keep a simple index at the front of the pack with each attachment, the period covered, and the owner. If records are incomplete, fix that before claiming readiness. Gaps in your audit trail often show up quickly in sample review.

Pair an executive metric with an operator metric#

Pair one executive metric with one operator metric per control area to avoid the familiar problem of a green dashboard and broken operations.

| Control area | Executive metric | Operator metric | Evidence attachment |

|---|---|---|---|

| Role-based completion | Completion and overdue status by required role | People missing required modules this cycle | Completion/overdue export, training matrix |

| Exceptions | Open exceptions by owner | Exceptions missing approved rationale or target date | Exception log, approval records |

| Updated modules | Completion on updated modules | People still assigned older versions | Version context report, assignment records |

| Ownership | Open actions by control owner | Control items without an assigned owner | Ownership register, action log |

If you can improve only one thing first, prioritize the evidence pack before dashboard polish. Continuous monitoring only helps when records are complete enough for another reviewer to verify what happened.

Before rollout, confirm your policy gates and audit records are operationally traceable in your implementation plan: Review the docs.

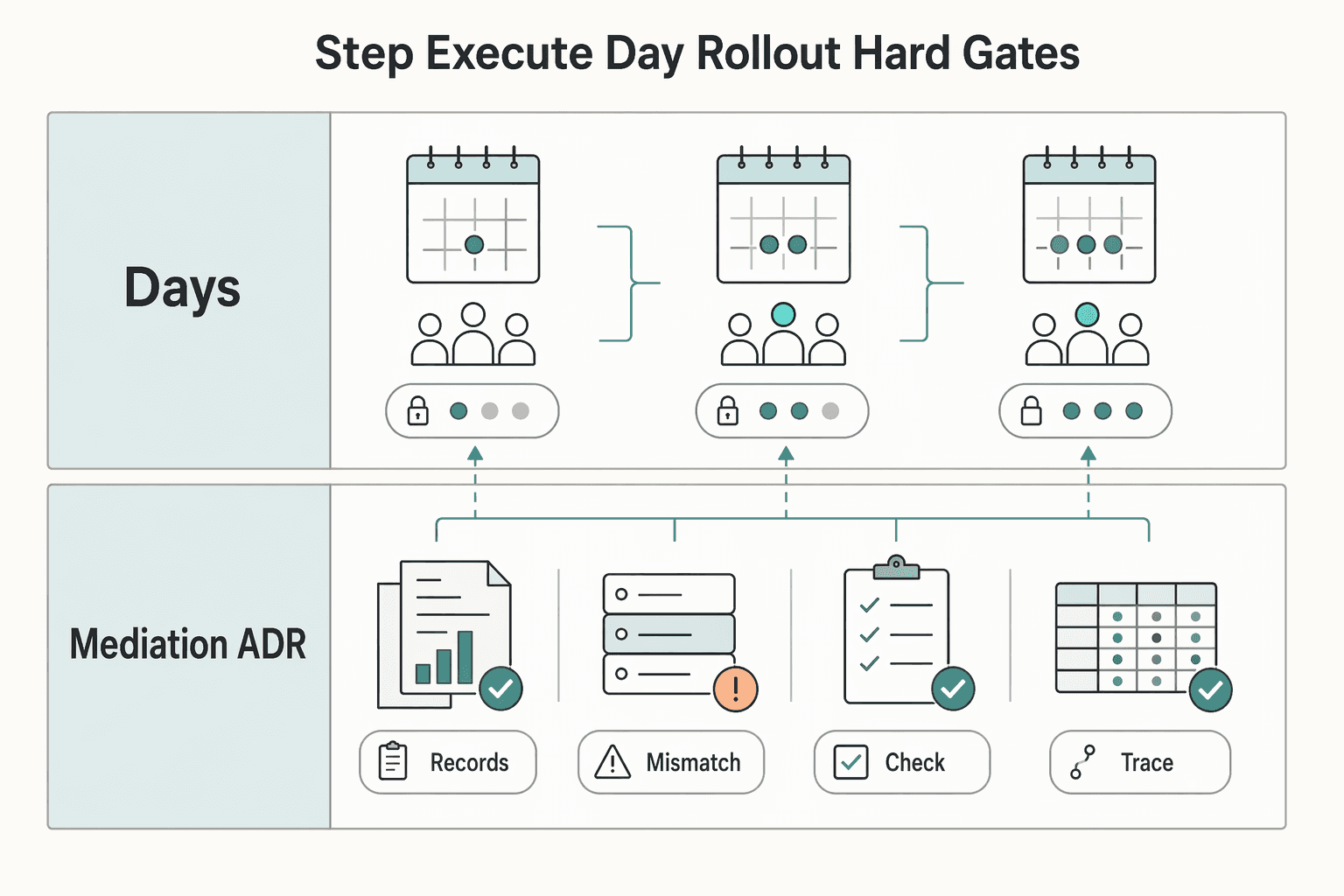

Step 6 execute a 90 day rollout with hard gates#

Run the rollout in phased waves, not all at once, and keep one hard rule throughout: no team moves to the next rollout wave until adoption and reporting gates are met.

| Phase | Main focus | Gate |

|---|---|---|

| Days 1-30 | Lock scope, role mapping, and baseline evidence | Learners can access training through SSO, roles come from a trusted system, and the monthly pack shows required, completed, and missing learners |

| Days 31-60 | Deliver role-specific depth and run simulation drills | Set an explicit 60-day decision gate based on evidence, not momentum |

| Days 61-90 | Supervise live production checks | Another reviewer should be able to reconstruct what happened from the operating record |

| Enforce remediation before broad rollout | If checkpoints fail, remediate before expanding access | Manual patching is a control warning signal |

- Days 1-30: lock scope, role mapping, and baseline evidence.

Set scope, map roles, and assign one mandatory foundation module to all in-scope roles. Treat SSO and HRIS-driven role assignment as adoption prerequisites so access and reporting do not drift into manual fixes. Your checkpoint is simple: learners can access training through SSO, roles come from a trusted system, and your monthly pack already shows required, completed, and missing learners. Capture baseline evidence up front and fix fragmented records before proceeding.

- Days 31-60: deliver role-specific depth and run simulation drills.

Use this phase for deeper, role-specific modules and drills. Look beyond correct answers and check whether execution is becoming consistent and evidence-backed. Set an explicit 60-day decision gate based on evidence, not momentum. Use realistic performance ranges early and focus on whether execution is becoming trustworthy.

- Days 61-90: supervise live production checks.

Test behavior change in production by reviewing live-case handling under supervision through your existing governance process. Go live on proven workflows first, stabilize them, then optimize using real operating data. Use traceability as the pass/fail check: another reviewer should be able to reconstruct what happened from the operating record.

- Enforce remediation before broad rollout.

If checkpoints fail, remediate before expanding access. Manual patching is a control warning signal. Admins fixing learner status by hand or side-file reconciliation show the rollout is not operationally ready. A hard-gated rollout may feel slower in the first 90 days, but it usually lowers ownership risk and rework caused by integrations, reporting complexity, content operations, and support load. If you need to compromise, reduce initial scope, not gate strength.

Mistakes that create regulatory surprises and how to recover#

Most regulatory surprises come from the same pattern: training is treated as content delivery, not control execution. The way back is to tie each module to a decision, an owner, and an auditable record, with explicit ownership for tax-adjacent steps.

Step 1. Tie each module to a control, an owner, and a record

Buying a catalog and calling it done creates a false sense of coverage. If a module is not linked to a control, a control owner, and an evidence artifact, it is hard to defend what changed in live operations.

Use a three-question check for every assigned module: what decision the learner can make, who signs off, and what record must exist afterward. If your only proof is completion status and a policy link, add the missing record requirement before expanding access.

Step 2. Assign training by decision impact, not by job title

Job titles do not reliably show exposure. Map training to decision impact instead: who can stop, release, classify, or escalate, and who is exposed to tax-adjacent decisions.

Use FEIE as a recognition-and-escalation case, not a generalist decision area. The exclusion applies only to a qualifying individual with foreign earned income, and eligible taxpayers still file a U.S. return reporting that income.

Step 3. Define trigger-based handoffs before edge cases happen

Weak escalation design turns small misses into larger regulatory risk. Define trigger-based handoffs with a named legal or compliance owner for tax-eligibility edge cases.

For FEIE awareness, keep one precise checkpoint in training: the physical presence test is 330 full days in a 12-consecutive-month period. A full day is 24 consecutive hours from midnight to midnight. The IRS also states this test does not depend on residence type, and missing the day count fails the test even for illness, family problems, vacation, or employer orders.

Step 4. Add explicit ownership for tax-adjacent steps

Tax-adjacent tasks are often where ownership gaps show up. Assign clear owners for FEIE eligibility checks and specialist escalation, even when the owner's role is recognition and routing rather than final determination.

Add recurring validity checks for sensitive handling. A useful control model is IRS VITA/TCE practice: annual conduct certification is required, Form 13615 is not valid until authorized personnel confirm identity, and conduct failures can bar future VITA/TCE activity indefinitely. Also label non-authoritative internal references clearly. IRS practice unit PDFs are not official pronouncements of law and should not be treated as binding authority.

How to refresh training when products and rules change#

Refresh training when decision-making changes, not only on a calendar. Completion can look healthy while actual understanding is uncertain, so treat refresh as a control update tied to real operating changes.

Step 1. Trigger refresh from changes in decisions and controls

Start with what changed in live operations. If a change shifts who can approve, escalate, or document a decision, trigger a refresh.

Use your Compliance Training Matrix as the first check. Confirm that role assignments, decision points, and required records still match production behavior. If they do not, reissue assignments and sign-off requirements.

Step 2. Rerun role mapping before reassigning modules

Do not just edit slides and keep the same audience. Rerun role mapping so training stays role-based and risk-weighted instead of check-the-box.

Reconfirm core accountabilities for each affected role: decision owner, escalation path, and evidence requirements. If any of those moved, update the module and control documentation together.

Step 3. Set a standing review owner for external content updates

If you rely on outside training or reference content, assign one owner to review revisions and decide whether internal controls need to change. The standard is impact on your decisions and escalation paths, not whether a provider published a new version.

That avoids passive recycling, where old modules stay live because completion looks high even when engagement is weak. One framework reports that 49% of employees admit to skim-reading or not listening to mandatory training. When a revision is material, pair the update with a short scenario check and updated manager acknowledgment.

Need the full breakdown? Read How to Set Up a Multi-Entity Payment Structure for Global Platform Operations.

Final takeaway and copy paste checklist#

Treat this as a control workflow, not a course catalog. Completion is only an input. The outcome is consistent, traceable, defensible decisions in live operations with records you can retrieve on demand.

- Define scope and risk tier by product surfaces and markets.

- Map roles to decisions and obligations with named handoffs for first response, escalation, and sign-off.

- Assign curriculum by decision impact, and document external versus internal sign-off logic.

- Link every module to live control evidence such as case notes, approvals, policy references, and escalation trails.

- Keep one reporting pack with roles, controls, exceptions, escalations, sample case reviews, attestations, and documentation follow-up.

- Roll out in gates to shift from reactive firefighting to preventive workflows, then test effectiveness in practice: was it designed well, is it applied in practice, and does it work in real operations?

Copy, adapt, and use this checklist:

- Scope defined by product surfaces and markets

- Role-to-obligation matrix completed, with applicable obligations explicitly documented

- Curriculum assigned by decision impact with external versus internal sign-off logic documented

- Escalation triggers documented for legal or compliance review

- Reporting pack live with audit trail evidence and documentation follow-up

- Effectiveness checks passed for design, implementation, and real-world operation

If you need to pressure-test control design and rollout coverage for your specific markets, talk with Gruv.

Frequently Asked Questions

What should a payment compliance training program include for a platform operations team?

Start with your own risk assessment, then map training to the decisions each role makes. Keep modules role-specific and tied to policy use, recordkeeping, and reporting expectations. In practice, that means onboarding support may need KYC training, while engineering may need training on how data flows affect AML screening.

Which roles should be trained first when we cannot train everyone at once?

Prioritize roles with direct transaction-system access and higher-risk decision authority first, then expand to lower-risk roles. That keeps high-risk decisions with people trained for the controls they actually operate.

How is payments-specific training different from generic bank compliance training?

Payments-specific training should map to your actual operations, data flows, and case handling, not only broad legal concepts. Generic content can cover fundamentals, but your team still needs role-level decision rules plus reporting and audit expectations. If training does not change case behavior, it is not an effective control.

When should we require ETA CPCP or another external certification instead of internal sign-off?

This material does not support a universal requirement for any external certification. Use external certification when you need specialist input for complex regulatory questions. Even with external training, confirm internally that people can apply your controls in live decisions.

What evidence proves training is operationally effective beyond completion rates?

Use behavior evidence, not attendance alone. Strong evidence includes monitoring and audit outputs, reporting records, and case documentation that shows how decisions were made. Completion rates are weak by themselves, and one cited framework reports that 49% of employees admit to skim-reading or not listening to mandatory training.

Which escalation triggers must always route to legal or compliance leadership?

There is no universal trigger list you can copy across platforms. Define escalation triggers from your risk assessment and control design, then document them clearly. When a question needs specialist regulatory interpretation, route it to legal or compliance leadership.

How often should we refresh training when regulations and payment models keep changing?

There is no single cadence that fits every platform. Refresh training whenever your risk assessment, control design, or role decision boundaries change. If role-based decisions and records no longer match current operations, treat training as out of date and update it.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- agr.mt.gov/Topics/E-G/FADC-Center-Pages/FADC-Success-St...trusted

- apply07.grants.gov/grantsws/rest/opportunity/att/download/345002trusted

- congress.gov/event/119th-congress/house-event/LC74985/texttrusted

- cpars.gov/cparsweb/assets/documents/CPARS-Guidance.pdftrusted

- department.va.gov/privacy/wp-content/uploads/sites/5/2024/09/F...trusted

- dhcs.ca.gov/Documents/Attachment%20Q.pdftrusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL1.pdftrusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2v2...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Build a Compliance Operations Team for a Scaling Payment Platform

Compliance ops usually breaks at scale because the operating design cannot keep up with payout complexity, not because teams stop working hard. If you expect payment volume to grow, design payout infrastructure, ownership, and evidence paths early so decisions stay clear and defensible.

Upskilling Platform Finance Teams for Payments Compliance and Automation

Cross-border platform payments still need control-focused training because the operating environment is messy. The Financial Stability Board continues to point to the same core cross-border problems: cost, speed, access, and transparency. Enhancing cross-border payments became a G20 priority in 2020. G20 leaders endorsed targets in 2021 across wholesale, retail, and remittances, but BIS has said the end-2027 timeline is unlikely to be met. Build your team's training for that reality, not for a near-term steady state.

What Is an Audit Trail? How Payment Platforms Build Tamper-Proof Transaction Logs for Compliance

For payout risk owners, a useful audit trail is one you can replay under pressure: who acted, what changed, when, and why it was allowed.