Quick Answer

Start with three tracks: compliance gates, reconciliation discipline, and automation judgment. For each payout path, define who approves, who blocks, what evidence must exist, and how retries are deduplicated. Then run a phased rollout with baseline metrics, role drills, and live escalation checks so ICFR and SOX documentation remains usable as payout volume grows.

What Finance Teams Need to Own in Payments Compliance and Automation#

Cross-border platform payments still need control-focused training because the operating environment is messy. The Financial Stability Board continues to point to the same core cross-border problems: cost, speed, access, and transparency. Enhancing cross-border payments became a G20 priority in 2020. G20 leaders endorsed targets in 2021 across wholesale, retail, and remittances, but BIS has said the end-2027 timeline is unlikely to be met. Build your team's training for that reality, not for a near-term steady state.

This article stays on execution. If your team handles payout release, settlements, reconciliation, or exceptions, the test is simple: can they show who made a decision, what evidence supported it, and where that evidence is stored when someone asks later?

The operating bar is simple. Controls should support reliable financial reporting and compliance with laws and regulations. Good training is not just policy awareness. It prepares people to run decision points under pressure and document the outcome, so blocked payouts, duplicate sends, or settlement mismatches can be explained from records instead of memory.

If you need a fast reality check, start with one live payout path and pressure-test it with four questions:

- Who can release the payment?

- Who can stop it?

- What record proves each action?

- How fast can someone reconstruct the chain from ledger entry to provider or bank status?

If those answers live across inboxes, chats, and tribal knowledge, the problem is control design and role clarity.

The rest of this article uses upskilling tracks tied to payment outcomes. The focus is day-to-day decision quality in areas that often create operational noise: ledger integrity, settlement visibility, exception handling, and compliance gates.

Two scope points matter up front. First, compliance is jurisdictional. FATF sets expectations for AML/CFT implementation through national systems, so controls may need to vary by market or program. Second, some requirements call for documented procedures, not general awareness. For example, Regulation E remittance error resolution requires written policies and procedures designed to ensure compliance. The examples here assume cross-border platform operations, where coverage varies by market and program. Local counsel should confirm what is mandatory.

For a step-by-step walkthrough, see IndieHacker Platform Guide: How to Add Revenue Share Payments Without a Finance Team.

Build the mental model before you assign training#

Train on control ownership before tools. If your team cannot say who approves a payout hold, who can clear it, and where the supporting record lives, the gap is not software skill. It is control design.

In practice, teams often operationalize compliance automation as policy gates plus evidence capture. For payment operations, that usually includes risk-based CDD/KYC, sanctions screening, and an audit trail showing what was flagged, who reviewed it, what was decided, and why. Under 31 CFR 1020.210, U.S. AML program expectations center on internal controls, designated day-to-day compliance responsibility, independent testing, personnel training, and ongoing monitoring for suspicious transactions.

Treat the tool like decision execution#

Treat the tool as a way to execute decisions under pressure, not as the control itself. A Decision Tree and Control Matrix are useful internal formats because they force clarity on roles and evidence, even though regulators do not require those specific names. For each gate, define:

- owner for approval or escalation

- trigger condition

- evidence artifact to retain

- fallback action if the gate or data feed fails

Then run one quick check. Pick a blocked payout and ask someone outside the case to reconstruct the path from alert to final disposition using records only. If they need chat history, inboxes, or memory, start training with evidence discipline.

Keep regulatory intelligence in its place#

Regulatory intelligence matters, but it is still an input. It does not replace approvals or escalation judgment. FATF treats the risk-based approach as central, updates recommendations over time, and expects implementation to be adapted to local circumstances. Your team still needs documented override rules, named approvers, and clear escalation logic when rules change during live payment flows.

Outsourcing does not outsource accountability. If a third party runs screening, your institution still owns compliance responsibility and recordkeeping obligations. Retention is rule-dependent. Some BSA records are retained for five years, while certain OFAC records must be available for examination for at least 10 years.

If you need to build the budget case for this work, see AP Automation ROI Calculator: How to Build the Business Case for Your Finance Team.

Map the three payment operations that break first at scale#

Map payout execution, reconciliation, and compliance holds as end-to-end control flows. If your team cannot reconstruct one real case in each flow from system evidence alone, training is still too tool-led and not operational enough.

Payout execution#

Start by mapping payout execution from final internal approval through provider response, not just to the API request. Capture the approver, payout instruction, idempotency key, provider reference, and each later status update from webhook or file, because retries are normal and provider responses are often asynchronous.

Two failure modes to watch for are duplicate sends after retries or manual resubmissions, and duplicate internal state changes from webhook replay. Validate the map with one payout: one approval, one idempotency key, one provider-side object, and one deduplicated status-event sequence. Treat posted as a progress state, not final proof that funds reached the recipient.

Reconciliation#

Reconciliation should be mapped from ledger journals to provider records to bank activity. Treat it as a control process for comparing bank-side cash activity to accounting records and investigating differences, not just a reporting task.

List the classes of Ledger-to-Bank Breaks you actually see and assign an owner to each. Typical examples include a journal with no matching bank movement yet, a bank movement with no journal, an amount mismatch, a reference mismatch, or provider status changes. Failed or returned payouts that did not update the ledger correctly belong in the same group. Require evidence for every disposition: journal ID, provider reference, bank line, payout or settlement status, and a short resolution note.

Compliance holds#

Compliance holds need the same end-to-end mapping, with explicit authority. Show who can block, who can clear, and who documents the decision. Keep the map tied to required records. For U.S. legal-entity customers, written procedures to identify and verify beneficial owners should connect to hold handling when customer data is involved.

One failure mode to guard against is the orphan hold with no clear approval path. Your map should show alert source, current risk context, reviewer, escalation path, and final rationale. If a U.S. bank-partner process requires suspicious activity review, include timing rules in the escalation logic. SAR filing is generally due within 30 calendar days, with a limited extension up to 60 calendar days when no suspect is identified.

One page per escalation path#

Once you map those three flows, make them usable in real operations. For each one, require a one-page escalation sheet that someone on call can use immediately:

- trigger condition and where it appears

- same-day vs next-day handling rule based on risk and cash impact

- named approver for clearance, override approver, and backup approver

- evidence required before release, rejection, or write-off

- fallback action if the provider feed, webhook, or bank file is unavailable

This is where training gets operational. You are moving blocked or broken payments safely, with records that still make sense later.

Way one train your team to operate compliance gates not just pass audits#

Train your team to make payout release decisions across KYC controls, sanctions screening, and transaction monitoring together, not as separate audit topics. If a payout can be blocked at any gate without a named owner, required evidence, and a defined internal response target, treat that as an operations defect.

Teach how the gates interact in a real release decision#

Before you release a blocked payout, your Finance Ops team and product owners should answer three distinct questions.

KYC and customer due diligence answer whether you can rely on the customer record. For covered U.S. financial institutions, 31 CFR 1010.230 requires written procedures reasonably designed to identify and verify beneficial owners of legal entity customers, so incomplete ownership data is a release risk when ownership data affects the decision.

Sanctions screening answers whether individuals, entities, or transactions match sanctions lists, and it is part of AML/CTF compliance work. Transaction monitoring answers whether activity appears suspicious based on behavior and context. Under 31 CFR 1020.210, ongoing monitoring includes identifying and reporting suspicious transactions and, on a risk basis, maintaining and updating customer information.

Do not collapse those questions into one generic compliance queue. Transaction monitoring is a subset of broader monitoring for suspicious activity. A payout might pass KYC and sanctions checks but still need suspicious-activity review. Or it might fail sanctions screening without a monitoring alert. Train operators to name which gate fired, what that means, and what evidence is needed to clear it.

| Gate | Release question | Evidence artifact to check | Common failure mode |

|---|---|---|---|

| KYC controls | Can we rely on the customer identity and profile data? | customer record version, reviewer notes, beneficial-owner record for legal entities where applicable | payout released against incomplete or outdated customer data |

| Sanctions screening | Is the party or transaction matched to a sanctions list? | screening result, case ID, match rationale, reviewer disposition | false positive closed with no retained basis for the decision |

| Transaction monitoring | Does the activity require suspicious-activity escalation or additional review? | alert ID, risk rationale, escalation outcome, linked transaction history | repeat alerts handled as isolated cases with no prior-case context |

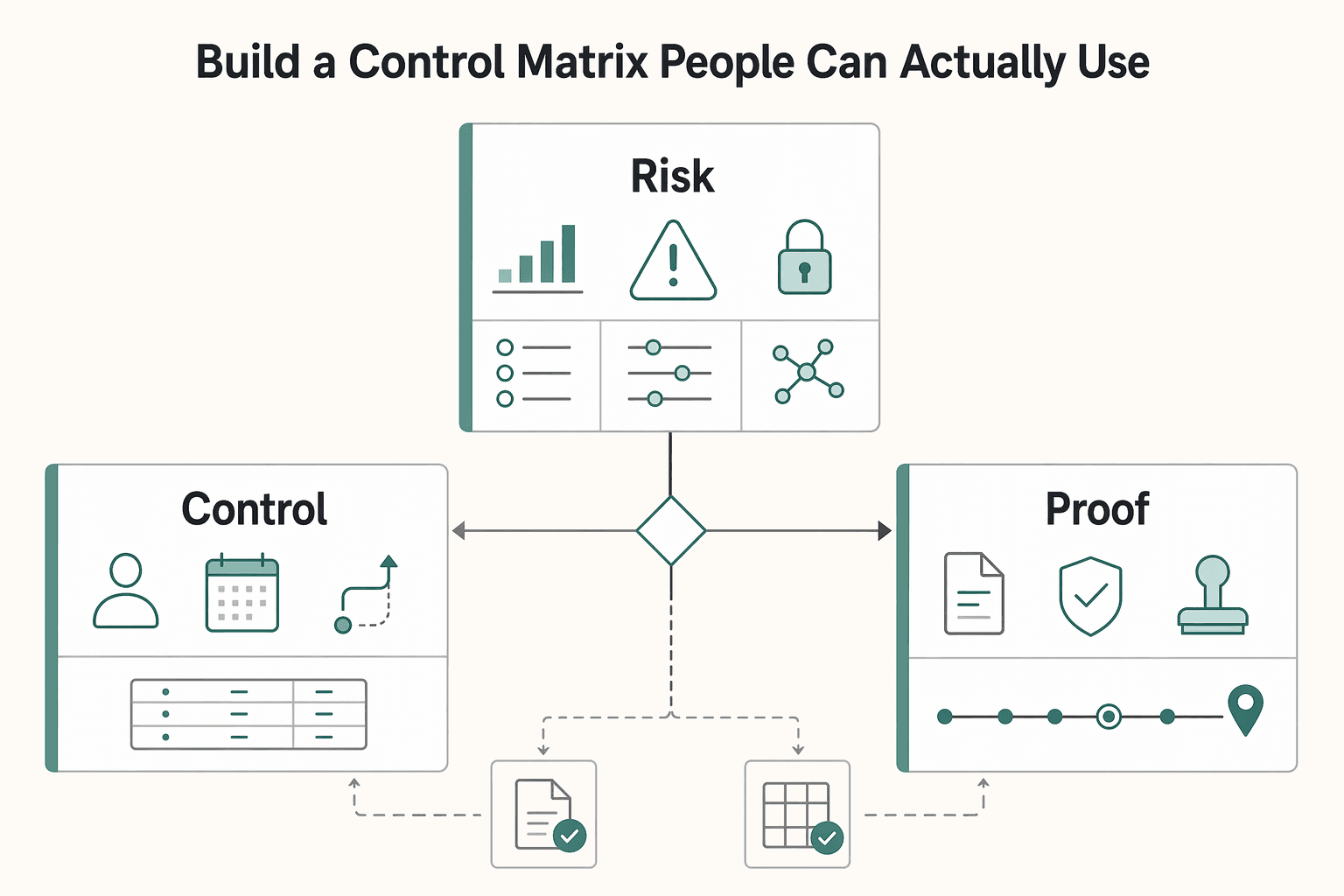

Build a control matrix people can actually use#

A control matrix is not explicitly required by the cited rules, but it is one of the simplest ways to make policy executable. For each gate, document the control owner, the evidence required before release, the fallback action when the normal review path is unavailable, and the exact audit-trail location for the case record. Include your internal response target so blocked payouts do not become orphan work.

Test the matrix on one live blocked payout. A trained operator should be able to find the decision record, the relevant alert or screening case, the approver, the disposition time, and the provider payout reference without cross-team guesswork. If they cannot, the process is still too abstract.

Fallback design is where controls get tested for real. If a screening feed is unavailable, your team needs a documented path for hold, manual review, or a limited alternate check based on your risk program. That path still has to be visible in the audit trail.

Treat missing ownership as a production problem#

31 CFR 1020.210 is explicit on two operational requirements: designate individual(s) responsible for day-to-day compliance and train appropriate personnel. In practice, that should include product owners when product changes can affect screening inputs, alert volume, case routing, and evidence capture.

The red flag is a blocked payout everyone can explain but nobody owns. You may see that in urgent vendor payouts, repeat sanctions false positives on the same counterparty, and recurring monitoring alerts with no linked prior disposition. When that happens, fix ownership and queue design, not just the single case.

Drill speed versus risk before real escalations#

Speed pressure exposes weak controls, so train for that tradeoff before it shows up in production. Use scenario drills to practice risk-based decisions under time pressure. Apply enhanced measures when risk is higher and simplified measures when risk is lower, without bypassing the gate that fired.

Run drills on:

- a sanctions false positive on a common-name vendor with urgent payment pressure

- a repeat monitoring alert where the team must decide whether prior evidence is still valid

- an urgent payout that requires customer-information updates before release

For each drill, require a clear decision, owner, evidence pack, and fallback path if the primary reviewer is unavailable. Watch for undocumented overrides: a release under pressure with no rationale, reviewer, or link to the cleared gate.

If your team is documenting ownership alongside training, use How to Write a Payments and Compliance Policy for Your Gig Platform as a practical starting point.

Way two train reconciliation muscle where finance teams actually lose trust#

Trust usually breaks when reconciliation starts from an export instead of the transaction trail. Train the team to reconcile in sequence: ledger event, provider reference, bank movement, settlement status, then reporting export. That sequence is an operating standard, not a SOX requirement, and it makes it much easier to isolate where confidence failed.

This is the reconciliation version of the ownership discipline from the prior section. If you cannot produce the event chain and supporting records, you may have an ICFR evidence problem, not just a workflow inconvenience.

Reconcile in the order the money moved#

Start with the ledger event that says money should have moved. Match it to the provider identifier, then the bank movement, then settlement output, and only then confirm the reporting export.

Use provider-native evidence, not reconstructed summaries. In Stripe, every funds movement creates a BalanceTransaction, which can serve as a reconciliation anchor. In Adyen, use the Psp Reference plus the Settlement details report to verify settled transactions, costs, and whether credits minus debits match the payout total.

Operator checkpoint: for one random payout, the reviewer should be able to produce the journal entry ID, provider reference, bank statement line, settlement record, and reporting export row without engineering intervention.

Common ledger-to-bank breaks#

| Symptom | Likely root cause | Owner | Verification evidence |

|---|---|---|---|

| Ledger shows payout cleared, but no matching bank movement | Payout created but not released, rejected, or still pending settlement | Finance Ops / Payments Ops | Journal entry, provider payout ID, BalanceTransaction or Psp Reference, bank statement for expected date |

| Bank deposit does not match ledger batch total | Fees, reserves, chargebacks, or other debits netted in settlement but not reflected in ledger | Finance / Accounting | Settlement-detail report, provider fee lines, net payout calculation, ledger posting logic |

| Bank movement exists, but ledger has no matching event | Missed manual journal, duplicate bank-line mapping, or posting failure | Accounting (Engineering if ingestion failed) | Bank statement line, import log, posting job record, missing/failed journal evidence |

| Reporting export disagrees with reconciled totals | Stale export, filter error, cutoff mismatch, or incomplete status mapping | Finance Systems / BI | Export timestamp, report filters, settlement status definitions, reconciled source records |

If the same break pattern keeps repeating by provider, payout type, or fee class, treat it as a mapping or posting logic issue, not a reviewer effort issue.

Make ICFR and SOX concrete at month end#

ICFR and SOX become useful when you translate them into reviewable actions on high-risk flows. SEC guidance supports a top-down, risk-based ICFR evaluation. Management's assessment is as of fiscal year-end. Month-end training should focus on the accounts that could misstate external reporting and on keeping evidence for each conclusion.

For reconciliation controls, require clear documentation of who reviewed each open item, what evidence they used, and why the item stayed open or was cleared. Set an internal escalation rule for unexplained ledger-to-bank breaks based on risk and materiality, and route potential control failures to finance leadership with clear ownership.

Run a regular exception review with deadlines#

Consistency comes from cadence, not one-off cleanup. Use a recurring exception review, weekly is common, to make this behavior stick. For every unresolved break, require a risk rating, owner, target resolution date, and explicit missing evidence.

Keep the discussion to three checks: is the amount financially meaningful, is the cause understood, and is the evidence sufficient for the current treatment. When cause or evidence remains unresolved across cycles, escalate priority and fix the underlying process.

Way three train automation judgment so retries and exceptions stay safe#

Use automation to clear low-risk volume, and keep a human in the loop anywhere retries, duplicates, or risk exposure could produce a bad payout. The goal is not to automate more steps. It is to train the team on which decisions can run automatically, which must pause, and what evidence proves the system behaved correctly.

Keep manual approval where the risk is real#

Automate repeatable checks with clear inputs and evidence, and send context-heavy risk decisions to human review. Adyen recommends manual review for high-risk regions and high transaction values, and FATF urges enhanced due diligence for jurisdictions it identifies as high risk.

Use three practical paths:

- Auto-approve standard low-risk payouts with complete data and no adverse signals.

- Queue payouts that need enhanced due diligence, policy interpretation, or exception handling.

- Block payouts with confirmed duplicate or fraud signals until resolved.

Define Idempotency Control as an operating standard#

Retry safety should be treated as a control requirement, not an engineering preference. Stripe supports idempotent requests to safely retry without creating a second object. It allows idempotency keys up to 255 characters and notes keys can be pruned after at least 24 hours. For PayPal REST POST calls, use PayPal-Request-Id. PayPal states omitting it can duplicate the request.

Train and review two checks every time:

- API retries: show the original request ID or idempotency key, the retry, and proof that only one business effect occurred.

- Webhooks: show processed event ID logs and deduplication results, since duplicate webhook deliveries can occur.

Prefer identifier-based deduplication with explicit replay handling, not timing-based assumptions.

Use a Decision Tree with only three outcomes#

Keep the routing outcomes explicit: auto-approve, queue, or block. Rule order matters because evaluation can stop after the first match.

| Path | Use when | Required evidence | Owner |

|---|---|---|---|

| Auto approve | Low-risk payout, complete beneficiary data, no duplicate or fraud signal | Request ID, screening result, payout instruction, audit log | Finance Ops / product-defined rules |

| Queue | High-risk region, elevated value band, unusual pattern, policy exception | Case record, reason code, reviewer decision, supporting documents | Manual review queue |

| Block | Duplicate signal, fraud hit, missing mandatory data | Blocking rule hit, event log, hold reason, escalation record | Compliance / risk / payments ops |

If you use risk scoring, train on the exact in-tool thresholds. For Stripe Radar, scores are 0-99, with 65+ elevated risk and 75+ high risk. Use those values only where Stripe Radar is in scope.

Make incidents change the controls#

An incident review should change the control set in some visible way through preventive follow-up actions. Require each postmortem to produce preventive actions, such as one automation lesson and one Control Matrix update. A postmortem is a written record of incident impact and response, and its value is the follow-up that reduces recurrence risk.

If a duplicate payout follows a retry, update controls to require idempotency keys on payout creation and request-ID evidence in review. If a webhook replay reopens a resolved exception, update the matrix for event-ID logging, replay handling, and owner checks. That is where ICFR for platforms becomes operational in day-to-day payment decisions.

Related: How to Make the Case for AP Automation to Your CFO: A Platform Finance Team Playbook.

Roll out in 30 60 90 days with owners and proof points#

Do not roll this out everywhere at once. Use a three-phase 30 60 90 plan and move forward only when each phase shows control quality with documented evidence your CFO and ICFR reviewers can use.

Start with a baseline you can defend#

The first 30 days should establish a documented current state before you expand scope. In control terms, that baseline is the reference point for monitoring whether control performance is improving.

Track the operating signals that matter here: reconciliations, trend checks, data checks, and exception tracking. For each metric, lock the definition, owner, source report, and review period. Then store sample reconciliations and open-case inventories with the metric file. If Finance Ops and product use different denominators or different definitions of an open exception, the baseline is not reliable.

Do not start drills before the measurement logic is stable, or you risk reporting false improvement from counting changes instead of control changes.

Run drills by role, using real operating cases#

Days 31 to 60 should test role-specific judgment, not generic completion. Training should match actual responsibilities, and the exercises should use real operating cases from your environment.

For each drill, document assumptions, objective, expected decision, pass or fail criteria, issues found, remediation owner, and target date. Run drills at defined intervals, and rerun the relevant scenarios when significant operating changes affect the environment.

Harden live monitoring and escalation#

Days 61 to 90 should turn training into operating discipline. Build live checkpoints into regular reviews, define measurable escalation criteria, and run a monthly control review tied to ICFR evidence.

That monthly cadence is an operating choice, not a rule requirement. It supports ongoing monitoring while preparing management for ICFR effectiveness evaluation at the end of each fiscal year and for assessing material ICFR changes during a fiscal quarter.

If issues repeat, remain uncorrected at cycle end, or quality worsens against the baseline, they should not sit in watch status. Assign an owner, due date, and a clear decision on whether to pause expansion.

| Phase | Recommended owner | Artifacts due | Pass criteria | Rollback trigger |

|---|---|---|---|---|

| Days 1 to 30 baseline | Finance Ops lead with controller or CFO sponsor | Metric definitions, baseline report, sample reconciliations, exception inventory, trend/data-check log | Metrics are documented, reproducible, and reviewed by owners; trend starting point is clear | Definitions disputed, source data unreliable, or baseline cannot be reproduced |

| Days 31 to 60 role drills | Finance Ops, product, and engineering managers | Scenario pack, assessment metrics, attendance by role, issue log, remediation owners and dates | Each role can execute decisions and show evidence location; defects are logged with dates | Exercises surface repeated critical defects with no owner or no target date |

| Days 61 to 90 live hardening | Finance leadership with risk and operations owners | Escalation criteria, monthly control-review pack, trend analysis, reconciliation checks, change log | Live monitoring is operating, escalations are timely, and monthly review is linked to ICFR evidence | Control-quality signals worsen versus baseline, or issues remain uncorrected at cycle end |

Advance phases only when the evidence pack shows controls are operating better, or at least no worse, in live operations.

Related reading: Partial Payments and Milestone Billing: How to Implement Flexible Invoice Terms on Your Platform.

When you translate the 30/60/90 plan into operating runbooks, use Gruv docs to align payout statuses, webhooks, and reconciliation evidence with each phase.

Use one scorecard that your CFO and operators both trust#

Use one scorecard with four practical KPIs and shared definitions. If a metric does not trigger a clear next action for operators or a clear control judgment for leadership, remove it.

Set one rule for every KPI: one owner, one source report, one threshold, and one threshold action. This is control discipline, not reporting style. Untimely detection or correction is itself a control-deficiency signal.

| KPI | What to verify | Primary owner | Threshold action | Why executives care |

|---|---|---|---|---|

| Payout success stability (internal definition) | Define the rate by rail or corridor and track trend stability against a fixed denominator. For ACH where relevant, include return-rate monitoring. | Payments or Finance Ops lead | If your threshold is breached beyond the allowable period, trigger incident review and corridor-level root cause analysis. | Shows whether payment quality is holding as volume and change activity increase. |

| Unresolved ledger-to-bank breaks (internal definition) | Define what counts as a break, then confirm each open item has a linked ledger event, provider reference, bank-movement status, assignee, and open date. | Reconciliation lead | If count or age crosses your internal limit, escalate for remediation review instead of rolling items forward. | Persistent breaks weaken reporting confidence and month-end control effectiveness. |

| Exception aging | Track aging buckets and oldest open-item age, not only total count. | Operations queue owner | If oldest-item age exceeds the agreed limit, force a clearance decision or escalation. | Aging shows whether issues are corrected on a timely basis. |

| Audit trail completeness | Verify you can reconstruct the transaction sequence from approval through payout and reconciliation. | Control owner for the flow | If key events cannot be reconstructed, treat it as an evidence defect and pause expansion of that flow. | In-scope issuers need defensible ICFR/SOX evidence. |

Keep one metric set, but show two views#

Keep one metric set and present two views of the same data: an operator view for daily queue health and an executive view for weekly or monthly trend. The operator view focuses on what is stuck, how old it is, where breaks are building, and where evidence is missing. The executive view focuses on whether risk is rising, whether controls remain effective after change, and which issues may affect ICFR.

For applicable issuers, SOX Section 404 makes this practical: management has annual ICFR reporting responsibility and must evaluate ICFR changes during fiscal quarters. Your executive view should show trend, breach history, and timeliness of detection and correction, not just current counts.

Define the checks before you trust the numbers#

Do not trust the scorecard until the definitions are locked. Two common failures are denominator drift, where the trend improves only because the counting changed, and false completeness, where events exist but you still cannot reconstruct the sequence.

For each KPI, keep a short metric spec: formula, denominator, source report, lookback period, allowable breach duration, owner, reviewer, and two sample cases. For ACH corridors, anchor checks to known thresholds. Use the 0.5% unauthorized return-rate threshold and the 3.0% administrative plus 15.0% overall inquiry or evaluation levels, calculated over the preceding 60 days or two calendar months.

Add AP Automation economics without forcing a savings story#

Bring AP Automation business-case metrics into the same review so performance changes are measured against spend and staffing plans. Useful metrics include cost per invoice processed, first-time error-free disbursement rate, and invoice-to-payment cycle time.

This keeps the conversation grounded in tradeoffs. If control quality improves while cost per invoice rises, review whether the increase reflects deliberate control coverage. If tooling spend rises and first-time error-free disbursement does not improve, investigate ownership, process design, and training before treating the spend as effective.

Split ownership clearly across finance ops product and engineering#

Use a single RACI-style ownership map so policy ownership and system ownership do not blur during change. One workable model is that finance ops is accountable for ICFR evidence quality, product is accountable for compliance automation decision logic and change governance, and engineering is accountable for idempotency and webhook or event reliability.

| Area | Primary owner | What they are accountable for | What to verify |

|---|---|---|---|

| ICFR evidence and control execution | Finance Ops | Evidence can support management's ICFR assessment, control steps were performed, exceptions were cleared or escalated, and audit-trail gaps are visible | Each key control has retained evidential documentation, a named reviewer, date performed, and linked exception resolution |

| Compliance automation behavior | Product | Decision rules reflect policy intent, overrides are documented, and logic changes follow formal approval | Current rule set matches the approved policy version, and the change log shows approver, effective date, and expected impact |

| Idempotency control and event handling | Engineering | Retries do not create duplicate effects, event integrity is preserved, and duplicate or delayed webhooks are handled safely | Signature verification is active, duplicate-delivery handling is tested, replay behavior is documented, and recovery steps are observable in logs |

Keep the finance line clear: management is responsible for establishing and maintaining adequate ICFR and must maintain evidential matter for the assessment. Finance does not need to own the code, but it should own whether the evidence pack can reconstruct what happened, why it was allowed, and who reviewed it. If you cannot produce that quickly, treat it as a control issue, not a reporting inconvenience.

Product should be accountable for turning policy into behavior. When compliance automation logic changes, route the change through a small approval forum such as a Configuration Control Board or equivalent. A common failure is role confusion: compliance defines the rule, product translates it into decision logic, and finance verifies the evidence output.

Measure engineering on failure handling, not uptime alone. Webhook endpoints can receive duplicate deliveries, so handlers must be duplicate-safe and observable. For teams using Stripe, idempotency keys can be up to 255 characters and may be removed after at least 24 hours. Retain request, key, event, and outcome logs long enough to explain retries or duplicate-payment claims.

Avoid the training mistakes that keep teams course complete but control weak#

Course completion alone is not control strength. If training is not tied to real payout failures, escalation decisions, and evidence gaps, teams may pass quizzes but still fail the controls your payment operations rely on.

Do not confuse a big course library with useful coverage#

Large course catalogs can help with baseline knowledge, but they do not prove decision quality in high-risk payment workflows. Coursera for Business promotes 10,600+ courses, and UpSkill LMS supports usage tracking and completion reporting. Those are delivery capabilities, not evidence that your team can explain why an alert was cleared, who approved an override, or how a recurring Ledger-to-Bank Break was resolved.

Start with your own failure history, then map training to those patterns. Use recent incidents and exceptions to build targeted exercises for issues such as duplicate payout claims, recurring Ledger-to-Bank Breaks, sanctions false positives, stale hold queues, and missing approval evidence. A practical check is whether an analyst can reconstruct one real case end to end, including reference, disposition reason, approver, escalation timestamp, and stored evidence.

Regulatory intelligence is an input, not the decision owner#

Regulatory intelligence tools are useful inputs, not substitutes for ownership. Vixio describes its offer as expert-led regulatory intelligence plus automation, but accountability for sanctions decisions, policy approvals, and escalation logic still sits with your team.

The control test is internal ownership and evidence. FCA guidance expects senior management responsibility for sanctions risk and expects firms to show sanctions issues are escalated where warranted. If a team can only say the tool flagged a rule change but cannot identify who reviewed, approved, and owns post-go-live exceptions, the gap is still yours.

For programs in NYDFS scope, that bar is explicit: institutions must certify transaction-monitoring and filtering compliance annually by April 15 for the prior calendar year. Keep dated proof of rule changes, testing, escalation records, and reviewer sign-off. Alert feeds alone are not enough.

Completion rates are weak if exceptions stay open#

Completion rates are useful, but they are a weak primary metric if exceptions remain unresolved. FATF frames ongoing employee training as part of internal controls, FFIEC includes training and independent testing in OFAC expectations, and DOJ evaluates whether compliance programs work in practice rather than by a rigid formula.

Track operating signals that show whether training changed behavior:

- unresolved exceptions that reopen repeatedly

- stale controls after policy changes

- recurring Ledger-to-Bank Breaks with the same root cause

- sanctions or transaction-monitoring dispositions without documented rationale or escalation trail

Run scenario drills before production volume exposes weak controls. Use real queue patterns, document expected vs. actual decisions, capture named approvers, and record remediation. The consequence of weak controls is real: the FCA fined Starling Bank £28,959,426 and said financial-crime controls did not keep pace with growth.

Confirm country and program differences before you standardize#

Standardize the control structure, not the legal assumptions. One checklist across markets can either over-block valid transactions or miss obligations that apply only in certain jurisdictions or program types.

Use your Control Matrix to label items as always-required, market-required, or where supported. This is internal control discipline, not a regulator-mandated formula.

| Jurisdiction or program context | Grounded difference to reflect in controls |

|---|---|

| U.S. remittance programs | Remittance rules apply to providers that regularly send consumer funds electronically from the U.S. abroad; CFPB examples note transfers must be more than $15, and oversight can involve both the CFPB and state licensing agencies. |

| UK payment services and sanctions | Payment services scope includes execution of payment transactions; sanctions obligations are assessed on case facts and the specific legal requirements that apply. |

| EU payment services | Authorization status is a gate for providing payment services, and PSD2 Article 21 sets a recordkeeping minimum of at least 5 years. |

When requirements are unclear, consider independent legal advice before finalizing policy gates. A risk-based approach does not mean identical controls everywhere. FATF ties controls to national legal and regulatory context, and U.S. AML rules require programs to be commensurate with location, size, and business profile.

As an internal governance practice, keep a dated change log that ties each regulatory update or provider-rule change to the exact Control Matrix edit it triggered. If you make a 2026 update, record your review date in the same entry. At minimum, record:

- jurisdiction and program affected

- regulatory change date and your review date

- specific control or checklist item changed

- owner, approver, and rollout date

- evidence-retention impact, including any

5-yearfloor where relevant

Conclusion#

Train controls, reconciliation, and automation judgment in parallel, then verify performance with operating evidence. That is the practical path because internal control is a management process, not a training artifact. It only holds when your team can execute it in live operations.

For payments teams, training belongs inside ongoing compliance. In bank AML programs, required elements include internal controls for ongoing compliance and training for appropriate personnel, and ongoing monitoring is part of normal operations, including reconciliations. If the team cannot clearly explain a blocked payout, a retry, or a ledger break with system evidence, the control is not mature.

Use one end-to-end payout decision as your reality check. You should be able to show the policy gate, who approved or blocked the action, when status changed, and the system evidence supporting the final outcome. If that chain breaks, the gap is usually ownership, evidence quality, or decision design.

Scale only after the pilot shows control performance is consistent in practice. A phased rollout is the safer pattern. The FedNow pilot used three phases, and broader guidance treats piloting as the stage before full rollout. You do not need a regulator-mandated 30/60/90 template, but you do need phased checkpoints, named owners, and a stop signal when control quality drops.

Next step: keep the scope narrow, run 30/60/90 checkpoints on a limited payout corridor or class, and expand only after the scorecard holds. Prioritize exception resolution with transaction-level evidence, unresolved-break aging, and audit-trail completeness for approvals, blocks, overrides, and retries. For a deeper control framework, see ICFR (Internal Control Over Financial Reporting) for Platforms: SOX Compliance Without a Big Finance Team.

To pressure-test your control design against real market and program constraints, start a scoped conversation with the Gruv team.

Frequently Asked Questions

What should platform finance teams be trained on first for payments compliance automation?

Train control ownership and decision evidence before tool clicks. Include everyone whose duties require knowledge of the BSA, and cover regulations, supervisory guidance, and your internal procedures. Prioritize clarity on who can block, release, or override a payout and how that decision is documented.

Which three payment operations fail most often when payout volume scales?

There is no universal ranking across all platform models, but payout execution, reconciliation, and compliance holds are common pressure points as volume scales. Payout execution is vulnerable when retries are not duplicate-safe, and webhook delivery failures can compound this risk (for example, Stripe may retry deliveries for up to three days in live mode). Reconciliation degrades when teams rely on summaries instead of transaction-level settlement evidence, and compliance holds weaken when high-risk areas are identified without clear internal controls.

When should we automate a decision and when should we require manual review?

Use a risk-based approach: automate low-risk, repeatable decisions with stable evidence, and require manual review for higher-risk or unclear cases. This is especially important in sanctions and related controls where higher-risk areas need explicit internal control responses. If a reviewer would reasonably need more context before approval, keep the decision out of auto-release.

What events must always be captured in the audit trail?

At minimum, capture who did what, when, and from where, plus the action outcome. Include successful and unsuccessful logon attempts and other critical actions that affect access or money movement. The log should support reconstructing a disputed payout end to end.

How do we prove training improved reconciliation and payout reliability?

Use operating evidence and control testing, not only course completion rates. Robust monitoring and testing should show whether control weaknesses are still appearing after training. Improvement is demonstrated when teams resolve reconciliation issues with transaction-level settlement evidence instead of ad hoc workarounds.

How often should we refresh controls when regulations or provider rules change?

There is no single regulator-mandated cadence to copy, but refreshes should be periodic and incorporate current regulatory developments and changes. Update controls and training when regulatory changes alter your decision logic, evidence requirements, or escalation paths. Record each update in your change log so the change history is auditable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/05trusted

- bsaaml.ffiec.gov/docs/manual/04_AssessingTheBSAAMLComplianceP...trusted

- consumerfinance.gov/rules-policy/regulations/1005/33trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-16-perform-monitori...trusted

- ithandbook.ffiec.gov/it-booklets/business-continuity-management/v...trusted

- occ.gov/publications-and-resources/publications/comp...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: