Quick Answer

Implement partial payments with a single source of truth for milestone status, invoice balance, and payout release. If approval changes, retries, and webhook events cannot be replayed cleanly, the billing model is not ready for scale.

How Partial Payments and Milestone Billing Work on a Platform#

Milestone billing is most reliable when each invoice is tied to a defined project checkpoint, a clear completion signal, and a billable amount. Without that chain, there is no clear link between progress and billing.

In practice, milestone billing means invoicing at project checkpoints instead of waiting until the end, with each invoice tied to project progress. The core setup is deciding what counts as complete, how down payments are settled during billing, and how partial invoices roll into a final invoice.

For the implementation layer, align milestone actions with Stripe's idempotent request guidance and payout reconciliation reports so retries and settlement evidence stay consistent.

Before you start#

Step 1. Define the billing chain from down payment to final invoice. Start with one explicit lifecycle: down payment, then partial milestone invoice or invoices, then final invoice. In milestone billing with down payment settlement, down payments already received are settled against the total billed amount during billing.

Before you automate anything, make sure your contract checkpoints match your system checkpoints. If commercial terms and tracked milestones do not match, your billing triggers may not be reliable.

Step 2. Make milestone completion a billing gate. Treat milestone completion as the release condition for billing. Milestone billing schedules identify what becomes billable as milestones are completed, and billing depends on completion status.

Use one shared record for milestone name, completion status, amount, and invoice eligibility. When authority is split across tools, invoice eligibility is harder to verify.

Step 3. Choose one transaction model and one billing source of truth. Pick one processing model per transaction and keep it consistent. Do not combine incompatible down payment handling and milestone billing logic in the same transaction flow.

If you are using project-linked sales orders or milestone schedules, decide where the authoritative billable amount lives. Then test one complete path: record the down payment, complete the milestone, issue the partial invoice, and confirm the remaining balance supports a clean final invoice.

This guide is for teams that need clear decisions and verifiable checkpoints. The next step is to build the implementation flow end to end so the model holds up in day-to-day operations.

Set the billing model before you touch product logic#

Define the billing model first, then build product logic around it.

Step 1. Write the commercial pattern on one page. Lock the billing shape before anyone builds states, webhooks, or invoice templates. For a milestone-billing workflow, you can name three stages in order: Down payment, milestone-triggered Partial payments, and the Closing invoice. For each stage, define the trigger, amount basis, and how any advance already collected is cleared. In SAP S/4HANA terms, a down payment agreement can sit in the sales order billing plan, and down payments are added during partial and final invoicing.

Use a simple checkpoint: someone outside the deal team should be able to answer these without extra context.

- What starts billing?

- Who confirms completion?

- What amount becomes billable?

- How does the down payment clear?

Step 2. Choose a primary trigger model before implementation. If invoice release depends on delivery acceptance or a project checkpoint, use Milestone billing. Salesforce describes milestone billing at project checkpoints, NetSuite ties billable amounts to milestones marked complete, and Oracle ties billing events to approval before invoicing is enabled.

If you are collecting a total amount through scheduled installments, use a payment-plan model. Partial.ly describes itself as payment-plan software that schedules and processes payments, and Stripe describes installment plans as partial payments against a total amount. If you mix date-based installments with acceptance-based invoice release, you are combining different billing triggers.

Step 3. Standardize names and test milestones before automation. Use one internal vocabulary across contract terms, product copy, finance procedures, and ERP mapping. Do not treat labels from vendor marketing pages or SAP Community member posts as operating standards. SAP Help is official documentation, while SAP Community pages can be member-authored blog content.

Before you automate, define clear acceptance criteria and a named approver for each milestone. If completion is still subjective or open to debate after the fact, consider delaying milestone-based invoice automation until the acceptance criteria are clearer.

Prepare prerequisites and ownership before implementation#

Once milestones are measurable, lock ownership before build starts. Clear ownership and release gates help reduce payout and reconciliation failures that usually show up later.

Before implementation starts#

Write one scope note by market, payee type, and program. Do not assume KYC, KYB, AML, and tax checks apply the same way everywhere.

Treat KYC as a real payout gate where your program requires it, and assign responsibility for collecting the required KYC data from users. For EU cross-border flows, decide whether VAT validation happens during onboarding or invoice setup. VIES can validate EU cross-border VAT registration, but it is a search tool that queries national databases, not your system of record.

Checkpoint: for each market, name the exact status required before payout release and the evidence retained.

Step 1. Assign owners by event#

Assign owners by event, not by department slogan. One practical split is product for state transitions, finance ops for reconciliation and exceptions, and engineering for webhook retries, duplicate defense, and idempotency behavior.

Engineering should explicitly own duplicate-event controls. Webhook endpoints can receive the same event more than once, so use idempotency keys for retry-safe requests and store processed event IDs to skip repeats.

Verification point: pick one event, such as milestone approval or payment success. One named owner should be able to explain who acts first, who can reverse, and where the processed event ID is logged.

Step 2. Define the minimum artifact set#

Define a minimum artifact set before implementation. Keep it small, current, and auditable:

- Billing terms: milestone trigger, amount basis, down-payment clearing rule

- Invoice state map: allowed transitions and approval evidence

- Payout policy matrix: release gates by market and payee type

- Exception queue definitions: severity, owner, response target

- Close checklist: required exports and proofs

Step 3. Separate compliance eligibility from commercial completion#

Keep compliance eligibility separate from commercial completion. A completed milestone does not automatically make a payout eligible.

Your payout policy matrix should state whether release requires completed KYC, business verification where applicable, AML controls, and beneficial ownership procedures required by your program.

Checkpoint: keep milestone approved, cash received, and payout eligible as distinct statuses.

Step 4. Set tax-data boundaries early#

Set tax-data boundaries early, especially for cross-border payouts. Define where W-9 or W-8BEN is collected, who reviews completeness, where it is stored, and which reporting path it feeds. Do not collect both forms for the same payee in the same tax posture.

Keep the handoff rules explicit. W-9 is furnished to the requester, not sent to the IRS by the payee, and W-8BEN is provided to the withholding agent or payer when requested. If US reporting applies, independent-contractor payments may require 1099-NEC, while nonemployee compensation to nonresident aliens is reported on 1042-S.

Verification point: test one US contractor flow and one non-US individual flow before launch. Then confirm the requested form, reviewer, and downstream reporting output.

For a step-by-step walkthrough, see Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

Build an invoice state model that finance can audit#

Use two separate tracks: one for milestone acceptance and one for cash collection. That separation is what keeps approved work from being mistaken for collected cash.

Step 1. Define the invoice-state path#

Define one invoice-state path where each state has a single meaning. A practical operating vocabulary is draft -> issued/open -> partially paid -> paid -> closed, but treat it as your internal model, not a universal lifecycle.

Map issued to a concrete platform event. In Stripe, invoices start as draft, and finalization sets status to open. If payment fails or is incomplete, the invoice remains open, so issued must not imply cash received.

Tie commercial events to explicit invoice records:

- Down payment as its own invoice event and invoice ID

- Milestone-triggered invoice as its own event and invoice ID

- Closing invoice as its own event after prior billed amounts are accounted for

Verification checkpoint:

- contract ID -> down-payment invoice ID

- milestone ID -> milestone invoice ID

- completion event -> closing-invoice ID

Step 2. Keep milestone states separate from payment states#

Keep milestone states separate from payment states, even when milestone approval triggers billing. At minimum, keep milestone pending, milestone approved, and milestone disputed/reversed distinct from invoice open, partially paid, and paid.

In SAP S/4HANA learning content, milestone billing links billing plans to project milestones, and milestone confirmation can disable the billing lock for the related billing-plan date. That clears a billing control. It does not confirm cash collection. Validate this behavior against your specific SAP product/version setup.

Design rule: if the invoice can still be unpaid, the status label must not read like settled cash.

Verification checkpoint: test a flow where the milestone is approved and the invoice is issued but payment does not arrive. Your model should still show approved milestone, open invoice, and no cash-received marker.

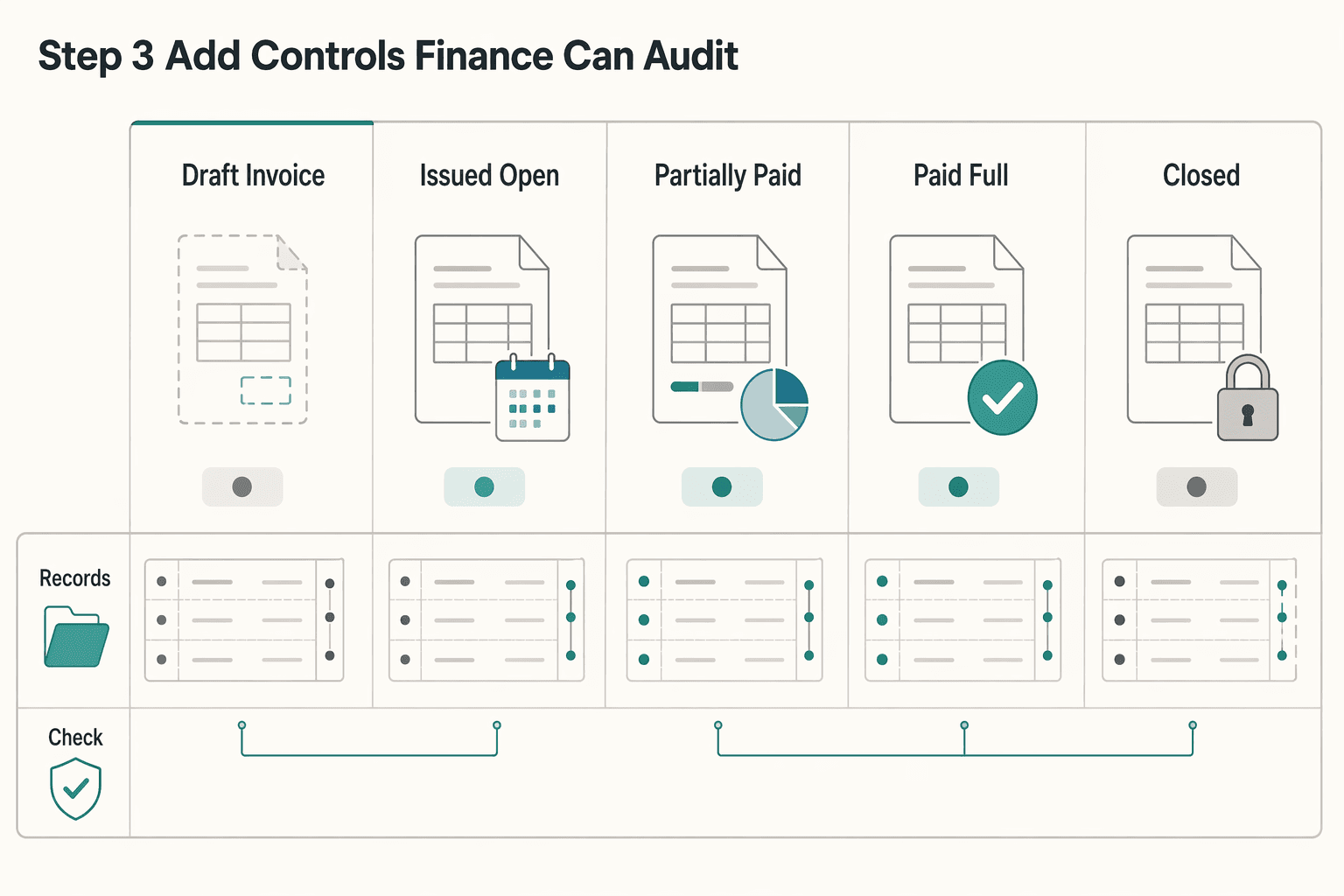

Step 3. Add controls finance can audit#

Add state-level controls so finance can audit movement, evidence, and reversals without rewriting history.

| State or step | Trigger source | Required evidence | Allowed reversals | Operator owner |

|---|---|---|---|---|

| Draft invoice | Contract terms, down-payment rule, or approved milestone trigger | Contract version, pricing basis, linked contract or milestone ID | Edit or cancel before finalization | Product or billing ops |

| Issued or open invoice | Finalization event in billing platform or ERP | Finalized invoice record, customer-facing invoice number, timestamp | Void or cancel only per policy before valid payment is applied | Billing ops |

| Partially paid | Invoice is open and payment received is below full amount | Payment reference, amount applied, invoice ID, receipt timestamp | Refund, return, or unapplied-cash correction as separate events | Finance ops |

| Paid in full | Full allocation of collected cash to invoice | Provider reference or bank proof showing invoice fully covered | Refund or return as a new event, not by deleting payment evidence | Finance ops |

| Closed | Paid in full, no open exceptions, and closing invoice complete where applicable | Payment trail, approval evidence, close approval if required | Reopen only through controlled exception with audit note | Finance ops |

Operational timing note: Stripe may wait 1 hour after successful webhook acknowledgment before attempting payment. It may still attempt to finalize and send after 72 hours if no successful webhook response is received. Do not treat invoice created or customer notified as payment-state evidence.

Step 4. Document ERP mappings and state authority#

Before go-live, document ERP field mappings and declare a single authority for each state family. If you use SAP ERP or an SAP sales-order-item billing plan, write the exact joins and ownership boundaries.

In SAP S/4HANA Cloud, the sales-order-item billing plan determines when a specific amount is billed. Standard key anchors include CustomerProject, SalesOrderItem, and BillingPlanItem.

Document control behavior too:

- A billing block can be set per billing-plan date.

- After successful billing, SAP can set billing status

C, which prevents the billed date from being billed again.

If your platform can still regenerate the same invoice after SAP marks a date C, you likely have dual-source drift.

Final check: export one billed sales-order item and show SalesOrderItem, BillingPlanItem, platform invoice ID, milestone ID if used, and current invoice state side by side. If the team cannot name the authority for issued, paid, and closed, fix that before implementation proceeds.

Need the full breakdown? Read How Platform Operators Should Plan PCI DSS Level and Cost.

Map every payment event to ledger journals and derived balances#

In this operating model, make the ledger authoritative, and auto-post only events that produce one deterministic accounting result. For each payment event, define an accounting event class, required references, and a replay-safe posting rule. If the resulting journal is ambiguous, route the event to exceptions first.

Step 1. Assign an accounting event to every commercial event#

Map each invoice and payment signal to an accounting event type before implementation. In milestone billing, billing-plan deadlines govern when partial milestone or final invoices are issued; posting those source documents can create receivable impact in the subledger and then transfer to the ledger.

Use event-type rule sets, not UI screens or API endpoints, as the posting boundary. Keep one posting rule per event family, and attach trace keys, such as milestone or billing-plan references, so finance can audit later.

| Event | Journal rule intent | Minimum references to store | Automation gate |

|---|---|---|---|

| Invoice issuance | Create the receivable-side accounting event for the issued invoice | invoice ID, contract ID, milestone ID or billing-plan item, issue timestamp | Post only after finalization or equivalent issued state |

| Payment success | Create the cash-application accounting event against the invoice | invoice ID, payment object ID, provider reference, amount, receipt timestamp | Post only when provider success is confirmed and invoice mapping is known |

| Payment failure | Apply your predefined non-posting or adjustment rule | invoice ID, payment attempt ID, failure code, timestamp | Automate only when the accounting outcome is defined in your rule set |

| Return or reversal | Create a linked return or reversal event | original invoice ID, original provider reference, return reference, amount | Require linkage to the original successful payment before posting |

| Offset or manual allocation | Move value between unapplied funds and invoice coverage per policy | source balance or credit reference, target invoice ID, operator ID, timestamp | Require approved allocation reason and audit trail |

| Closeout | Mark accounting completion after invoice and cash resolution | invoice ID, milestone set or completion event, close approval, settlement status | Post only when no open exceptions remain |

Do not assume one provider payload includes all references. In practice, you may need to assemble them from invoice records, payment objects, webhook events, and settlement reporting.

Step 2. Make derived balances follow posted events#

For this model, treat wallet, customer-balance, or available-funds views as projections from posted events plus settlement status. Keep reconciliation anchored to transaction artifacts that show funds moving into or out of balance.

Apply stricter handling for Virtual Accounts and bank-transfer collection: auto-reconciled transfers can post normally, but unmatched transfers should remain unapplied until manually linked to the correct invoice. Do not let projected balances imply invoice settlement when the invoice mapping is incomplete.

Verification checkpoint: trace one milestone invoice paid by bank transfer end to end, including invoice ID, transfer or payment reference, balance-transaction reference if present, and settlement batch or payout grouping.

Step 3. Add idempotency to every posting path#

Implement idempotency at both the request and posting layers so retries do not create duplicate journals. The posting key should represent the economic event, not just the HTTP call.

Store one immutable posting outcome per event type and reference set, then replay that same outcome on duplicates. Test duplicate delivery and retry chains, including provider duplicate events, webhook redelivery, and ERP import retry, to confirm you still get one receivable and one cash outcome.

Step 4. Require an evidence pack before auto-posting#

Auto-post when the event carries enough references to produce one accounting result. For payment-to-invoice posting, require invoice mapping plus payment or provider references. For payout reconciliation, include settlement-batch context where used.

Use a simple rule: if critical references are missing, do not auto-post. Send the event to exceptions with the missing field identified, such as an unmatched virtual-account credit, payment success without invoice mapping, or a return not linked to the original successful payment. This control is cheaper than repairing duplicate receivables, duplicate cash entries, or unexplained balances later.

Related: IT Staffing Platform Payments: How to Pay Developers and Consultants on Milestone and Retainer.

If you are turning this mapping table into implementation specs, use the Gruv docs to align event contracts, idempotency behavior, and status surfaces.

Choose collection rails and terms that match settlement reality#

Choose rails and terms based on when funds are actually confirmed and how finance will reconcile them. Rail and term mismatches usually show up as reconciliation and release errors: invoices look collectible, but cash confirmation and matching data do not line up with milestone logic.

Step 1. Match each milestone to the right rail#

Match each milestone to the confirmation pattern you need before work continues.

Use cards when you need a fast payment check at purchase time, since authorization is designed to verify cardholder or card validity and funds availability at that point.

Use SEPA Direct Debit when you want a payee-initiated pull and can document mandate capture and retrieval. Because this rail depends on payer consent through a direct debit mandate, do not make it a default if mandate evidence is weak.

Use SEPA Instant Credit Transfer where available when the buyer should push funds and you need near-immediate availability. SCT Inst is described as funds available within ten seconds and available 24/7/365, but coverage is not uniform across SEPA jurisdictions, so rollout should be corridor-specific.

Verification checkpoint: define the reconciliation artifact for each rail before launch. For cards and processor-based methods, use transaction-level settlement reporting tied to the merchant account. For bank transfer, use the bank credit plus the matching reference your collection flow requires.

Step 2. Define when Virtual Accounts are allowed#

Enable Virtual Accounts only when you will use their reporting detail to match deposits to invoices or counterparties. Their operational value is centralized cash with enough reconciliation detail to make matching workable.

Keep the release rule explicit: unmatched bank deposits are unapplied cash, not paid milestones. If a deposit lands without a reliable invoice match, investigate before milestone release or before issuing the next invoice.

For manual investigation, require a minimum evidence pack:

- virtual account identifier

- booking date

- amount

- payer name

- bank reference

- suspected customer

- operator allocation notes and final decision

Step 3. Write term logic that respects settlement timing#

Define term logic before launch, including due-on-acceptance versus net terms, grace windows, and the exact pause condition for future invoice issuance.

For any net-term model, specify the clock start event, such as milestone acceptance or invoice issue time, and apply it consistently. Then align that rule with settlement timing and payout cadence, since settlement and merchant payout can run on different schedules and payout batches close by configured payout frequency.

Operator test: walk one invoice through acceptance, issuance, due date, grace expiry, and pause logic. If teams disagree about when the next milestone invoice should be blocked, term logic is still too vague.

Step 4. Document Merchant of Record boundaries by region#

If some regions use a Merchant of Record, lock the region-to-entity mapping before invoice generation. The MoR is the entity legally authorized and responsible for processing customer payments, so this boundary drives liability and reconciliation ownership.

Store at least:

- invoicing entity

- merchant account

- region

- invoice ID

- contract ID

- settlement file reference used for reconciliation back to platform records

Do not merge MoR and non-MoR flows in one reconciliation view without an entity field, or receivable ownership and settlement matching can break.

Gate payout release with explicit compliance and risk controls#

Keep payout release on its own gate: release only from available funds to verified counterparties, not from milestone approval alone.

Step 1. Tie eligibility to available cash and account verification#

Treat payout eligibility as two conditions that must both be true: funds are available for payout, and the recipient account is cleared to receive payouts. Pending funds are not enough, because they are not yet withdrawable or spendable.

Do not run this gate from invoice or milestone status alone. KYC, KYB, and AML checks belong here, since missing or unverified information can pause payout capability. If your program includes CIP procedures, keep the required identity records and related retention controls, including 5-year retention where chapter-level BSA record rules apply.

Verification checkpoint: before an account enters a payout queue, confirm onboarding collected the required KYC or KYB data for that account context and that payouts are not currently restricted.

Step 2. Keep milestone approval separate from payout release logic#

Milestone approval should move work forward, but cash release should follow separate payout rules. Define an explicit rule matrix so, in your program, approved milestones become payout-eligible only when related funds are available and policy checks pass.

If cash is unpaid, pending, unmatched, or under review, keep payout blocked. Build reversal handling into the same policy: if money is returned after release marking, remove it from releasable funds and route the payout or transfer for review. Payout reversal and transfer reversal behavior can differ by stack, so your hold logic should reflect your actual balance flows.

Step 3. Require tax forms before payout activation where needed#

If your reporting or withholding obligations depend on payee context, make tax form collection a payout-activation gate. Do not leave W-form collection to month-end cleanup.

Use the form that matches the payee context. Use W-9 for providing a correct TIN to payers or brokers filing IRS information returns, W-8BEN-E for foreign entities in chapters 3 and 4 context, and W-8BEN for foreign individual beneficial-owner context. Where your program requires tax data, keep payouts disabled until the required tax data is complete.

A practical activation evidence pack includes:

- legal name and account ID

- KYC or KYB verification status

- beneficial ownership verification status where applicable

- CIP/identity verification record status

- tax form type and collection date

- operator decision and timestamp

Step 4. Execute releases in controlled payout batches#

Run releases through payout batches instead of ad hoc payout clicks. Batch execution gives you a formal approval point, a settlement-batch reference for reconciliation, and an audit trail for each release or hold decision.

Use role-based access so review and transmission permissions are controlled separately, and add second approval where your risk policy calls for it. Record batch ID, payee account, source invoice or milestone mapping, releasable amount, approval chain, and hold or override reasons.

Then monitor post-submit statuses. Payouts can fail or be canceled within 5 business days, and failed payouts can disable the external account used. Pause further releases for that payee until the account issue is fixed.

Integrate ERP and automate event flow without duplicate actions#

Set the record boundary first: keep the ERP as the system of record for GL and financial reporting, and define which system owns each operational state. That boundary helps reduce duplicate posting risk.

Step 1. Assign record ownership before integration build#

Avoid having the platform and SAP ERP or NetSuite both create and update the same financial record from the same event stream. A cleaner split is simple: the platform emits operational events, and the ERP books finance records.

Before go-live, publish a one-page ownership map for each object:

- who creates it

- who can amend it

- which external reference links platform and ERP records

Step 2. Define webhook contracts for duplicates and out-of-order delivery#

Assume duplicate deliveries and non-guaranteed event order in every consumer. For key events such as invoice paid, payment failed, return posted, and payout completed, include stable identifiers, event ID plus business reference, and a dedup key or idempotency key.

Keep dedup state durable, not in memory. Undelivered webhook events can be retried for up to three days, so replay protection must survive deploys and delayed delivery windows.

Step 3. Use ERP-native idempotent matching controls#

Where NetSuite is in scope, use external IDs with upsert or upsertList so retries match existing records instead of creating new ones. In SOAP upsert flows, identity is record type plus external ID. In async REST flows, use the unique-key idempotent retry mechanism.

Use upstream business references as external IDs. If retries generate new IDs, ERP-side duplicate protection cannot reliably match attempts.

Step 4. Replay-test automation and add guardrails when needed#

If you use SuiteScript or similar ERP automation, include replay and out-of-order delivery tests before production where practical. Verify duplicate events produce no second financial side effect, and out-of-order events are held or resolved deterministically instead of posted blindly.

If your ERP path can accept duplicate external references, consider adding a hard uniqueness control in your integration layer before launch. Validate with logs that duplicate attempts are detected, linked to the original reference, and suppressed.

Plan for failures, disputes, and reversals before launch day#

Duplicate protection helps, but it does not resolve late cash, returns, or disputes. Define those paths before launch so you do not release payouts against cash that is still open, unmatched, or reversed.

Step 1. Build the exception matrix around cash reality#

Start from the payment outcome operators will actually see, then define invoice state, payout impact, owner, and required evidence. Keep bank-transfer exceptions separate from card issues because timing and proof differ.

| Failure type | Temporary state you should use | Immediate operator action | Hard deadline or risk |

|---|---|---|---|

| Failed charge | Invoice remains unpaid or partially paid; next payout blocked | Retry collection or switch rail, confirm no cash journal posted | Risk is accidental payout release on an unpaid milestone |

| Delayed bank credit to virtual account | Payment stays open pending funds arrival; unmatched cash queue if money lands without auto-match | Reconcile against customer balance, invoice ID, and bank reference before applying cash | Unreconciled funds require manual action; long-aged balances can be auto-returned after 75 days |

| Return or reversal from bank rail | Return pending review; related balances marked for adjustment | Match return to original transfer using metadata and bank file reference, then post offset entry | Returns can be reported in separate files, so missed files create cash-versus-ledger drift |

| Pre-dispute or formal dispute | Disputed payment under review; related payout paused by policy | Review evidence, refund if appropriate, or respond through provider tooling | Formal dispute responses are usually due in 7 to 21 days; missing the deadline means automatic loss |

Verification check: for one example in each row, an operator should be able to confirm within two screens whether cash was received, matched, returned, or contested.

Step 2. Freeze future billing, not past truth#

When a milestone is disputed, freeze the next partial payments tied to that work as an internal control and stop related payout release, but keep prior journals immutable. If the economics change, post an explicit reversal or offset entry linked to the original invoice ID, milestone ID, and provider reference.

This matters most when approval and payment are decoupled. A bank transfer can remain open until funds arrive in the virtual account, so milestone approved cannot mean cash settled. Use this rule: no new payout or downstream billing step based only on milestone acceptance when the rail is asynchronous.

Verification point: if milestone 2 is disputed after milestone 1 was paid, earlier entries remain untouched and the disputed amount appears as a clearly dated reversal or offset.

Step 3. Set SLAs and escalation paths by failure type#

Use SLA queues by failure type, not one blanket SLA across rails. For card disputes, start internal handling the same day because external response windows are usually 7 to 21 days, and pre-disputes need their own queue. Early fraud warnings are time-sensitive: if you do nothing, they often escalate into fraud disputes, and a refund only helps as a reversal when processed very fast, usually within 2 hours.

For bank-transfer exceptions, assign manual reconciliation ownership up front. If funds land in customer balance and do not auto-match, the owner should investigate with the virtual account number, transfer reference, invoice ID, and return-file identifier. If you support rails with longer return rights, such as SEPA Direct Debit, document that exposure and monitor it longer. Refunds can be requested up to 8 weeks without justification, and unauthorized claims up to 13 months.

Write escalation as named roles and order, not department labels: operator, reconciliation lead, provider support or engineering when webhook or bank files are missing, then finance controller if close is affected. The escalation evidence pack should always include invoice ID, milestone ID, event ID, provider reference, bank statement or return-file reference, and payout batch status.

You might also find this useful: SEPA Payments for Platforms: Direct Debit Instant Transfer and Recurring Billing.

Close the month with a reconciliation pack your auditors can follow#

Close only when every open receivable, unresolved cash movement, and unreleased payout decision is traceable to evidence. If that trail is incomplete, the close is not done.

Step 1. Reconcile the four balances that usually break close#

Start with the four buckets where month-end drift usually shows up:

- Open invoices from your A/R aging report, for example, an A/R Aging Summary grouped by customer and billing period.

- Unapplied or unidentified cash, using a register that separates unidentified, on-account, and unapplied receipts.

- Returned or failed cash, reviewing receipt statuses such as NSF and REV, not only unapplied cash.

- Unreleased Payout batches, treating paid invoices and releasable payouts as separate checks when cash is returned or unmatched.

Verification point: for one invoice in each bucket, confirm invoice ID, provider reference, milestone ID, and current payout status.

Step 2. Export one standard pack every month#

Use the same export set every close: invoice aging, event logs, ledger export, payout status export, and exception queue outcomes. Event logs belong in this set because API activity creates timestamped events, for example in Stripe.

If your provider offers a payout reconciliation report, include it. For Stripe, that report is available only when automatic payouts are enabled. If you run manual payouts, include your own settlement-batch export and operator signoff instead.

Step 3. Attach compliance and tax artifacts only where needed#

Attach compliance and tax artifacts only when they affect release or reporting decisions, and store dated snapshots used at close. Typical examples are AML status snapshots where required for your entity and jurisdiction, VAT validation outcomes such as VIES checks, W-9 collection evidence, and 1099 audit traces where contractor reporting may require Form 1099-NEC.

If cross-border flows feed downstream personal tax prep, retain date-granular records for FEIE review and foreign-account records for FBAR conditions. Include whether aggregate foreign-account value exceeded $10,000 during the year.

Related reading: ARR vs MRR for Your Platform's Fundraising Story.

Track operating metrics and rollout gates that prove it works#

Run this as a canary, not a full launch. Start with one narrow, milestone-heavy cohort and expand only when the pilot is stable enough to close without extra cleanup.

Step 1. Start with a cohort you can inspect end to end#

Choose a canary group with a repetitive milestone pattern so operators can trace each record cleanly. For sampled pilot invoices, verify that acceptance events produce consistent invoice, payment, and journal outcomes, with no manual ledger repair after close.

If you use NetSuite, track late and uncompleted milestones during the pilot with dashboard searches or reports. Those signals can help surface pilot issues before broader scale.

Step 2. Track the KPIs that surface failure early#

Track these four operational KPIs throughout the pilot:

- invoice-to-cash cycle time

- duplicate-posting incidents

- return resolution time

- payout hold aging

Read them together, not in isolation. If you collect by ACH Direct Debit, success or failure acknowledgment can take up to 4 business days. A longer cash cycle can be normal in that window, while unresolved returns and aging payout holds are stronger warning signs.

Step 3. Set a clear go or no-go gate before scale#

Do not widen exposure until your internal gate passes: consistent journal outcomes by event type, reconciled ERP posting, and stable Payout batches completion. For Stripe-based payout operations, check the payout reconciliation report, including failed payouts, instead of relying only on dashboard totals.

Also test replay behavior. Stripe notes that webhook endpoints can receive the same event more than once, so idempotent request handling and duplicate-event controls should return the same result rather than posting cash twice.

Step 4. Define rollback before you need it#

If duplicate posting or payout-release errors rise above pilot baseline behavior, stop expansion and move Milestone billing transitions back to manual approval. The risk to prevent is a record that looks paid in product while ledger or payout state is wrong underneath.

Pause new automation for affected Payout batches until exceptions are reconciled, including unapplied or unidentified cash. If the team cannot explain an error with event logs and close-pack evidence, the rollout is not ready to scale.

Conclusion#

The version that holds up is the one you can trace end to end: contract terms to invoice state, transaction record, compliance decision, and payout release without manual reconstruction.

Treat milestone billing as shared operational infrastructure, not a product-only feature. When finance, product, and engineering work from the same state model, partial payments stay explainable instead of turning into reconciliation drift.

- Define invoice and milestone states with named owners.

Use explicit invoice statuses such as draft, open, paid, uncollectible, and void, and keep milestone approval separate from payment status. A partially paid invoice still has a remaining balance, so your UI, ERP sync, and ops queue should not treat it as closed.

Verification: pick one down payment, one milestone invoice, and one closing invoice and confirm each has a single owner for state transitions.

Red flag: if milestone approved can silently imply cash received, you already have payout and close risk.

- Map key events to deterministic accounting outcomes.

Outcomes should be repeatable for invoice issuance, payment success, payment failure, and final closeout. If you use SAP ERP or a sales order billing plan, document where milestone dates connect to invoice creation and where accounting authority lives.

Verification: for any event, an operator should be able to point to the required references, typically invoice ID, milestone ID, and settlement batch ID.

Failure mode: if a real event cannot produce one clear outcome, route it to exception handling instead of posting a temporary entry.

- Enforce idempotent webhook and ERP sync behavior before go-live.

Retries are normal, so API writes and event processing must prevent duplicate receivables, duplicate cash postings, or duplicate payout actions. This matters even more because undelivered events may be resent for up to three days, and manual recovery windows only go back 30 days.

Verification: replay the same payment-success event twice and confirm invoice state, accounting result, and ERP record count do not change after the first successful post.

Red flag: if your ERP accepts duplicate external references, fix that before production.

- Gate payout release on compliance completion and cash availability.

Release funds only when milestone status is approved, required KYC and AML/CFT controls are complete, and funds are actually available for payout. Add any program-specific KYB checks where required. Pending funds are not spendable, and payout eligibility should follow that. If you run batch execution, keep approval routing explicit so a batch is not processed before review.

Verification: for one sampled payout, confirm the audit trail shows who approved it, when cash became available, and the compliance status at release time.

Failure mode: approved work plus initiated payment is not enough if the balance is still pending.

- Run month-end reconciliation with a practical evidence pack before scaling.

Reconcile open invoices, unapplied cash, and unreleased payout batches as one close activity. A practical pack can include invoice aging, payout settlement batch detail, transaction history, and a view of open invoices and unapplied cash. Aging buckets like 1 to 30, 31 to 60, 61 to 90, and over 90 make stale balances visible quickly.

Verification: hand the pack to someone outside the daily queue and confirm they can explain one transaction from invoice creation to payout or hold decision.

Red flag: if month-end still depends on Slack archaeology, do not scale the flow yet.

When your pilot is ready for production controls, talk with Gruv to validate market coverage, compliance gates, and rollout design.

Frequently Asked Questions

What is the difference between milestone billing and a payment plan?

Definitions vary by contract, platform, and accounting policy, so avoid assuming one universal meaning. Use your own contract language and finance policy as the authority, and document billing triggers clearly so operations and finance interpret states the same way.

What is the minimum viable flow for partial payments on a platform?

There is no single universal minimum flow. Start with a flow your team can trace end to end without manual reconstruction, and simplify any step you cannot explain clearly in review.

How should partial payments post to the ledger and affect wallet balances?

There is no one-size-fits-all treatment. Define and document how invoice, payment, ledger, and wallet states relate in your system, and keep records linked so remaining balances can be explained later.

What controls prevent duplicate billing events and reconciliation drift?

Controls depend on your stack and risk model, so document ownership of invoice state and expected behavior for repeated or out-of-order events. Validate those rules in testing so duplicate or drift scenarios are visible and handled consistently.

How do down payment, milestone invoices, and closing invoice fit together operationally?

If your model uses these elements, define each billing event and its evidence requirements in your own process and contracts. Keep status tracking clear enough to answer what is billed, paid, and still open.

When should payouts be released if a milestone is approved but funds are not yet settled?

There is no universal release rule. Set payout timing in a written policy with your finance/legal owners, and document how exceptions are approved and recorded before release.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- docs.stripe.com/api/idempotent_requeststrusted

- docs.stripe.com/reports/payout-reconciliationtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- fatf-gafi.org/en/publications/Fatfrecommendations/Fatf-rec...external

- help.salesforce.com/s/articleViewexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: