Quick Answer

Split the work into expansion readiness and filing readiness, then approve only flows that are traceable from source event to journal entry. Use go/no-go gates for duplicate-safe webhook handling, idempotency keys, settlement reconciliation, and named reviewer sign-off. Keep new PSP routes, VBA paths, or payout rails in pre-launch status until finance can reproduce month-end support without spreadsheet reconstruction. This is the operating standard that keeps growth decisions compatible with SOX Section 404 and Form 10-K/10-Q obligations.

Why IPO Readiness Starts in Financial Operations#

Start with the right split#

Use this checklist to separate expansion readiness from filing readiness before you commit to new markets. A payment platform can be ready to launch in a new country or vertical yet still be unready for IPO scrutiny. Filing readiness brings its own requirements: SEC effectiveness before securities can be sold, ongoing Exchange Act reporting, and CEO/CFO certification tied to Form 10-K and Form 10-Q.

That split matters because finance operations are not a cleanup step. If you add markets, PSPs, and payout paths before you can produce clean records, approvals, and reconciliations, you raise the risk of reporting and control problems that are much harder to unwind later. Here, SOX Section 404 and ICFR set control expectations for how money movement, exceptions, and close evidence need to work.

Start early. Many companies begin IPO-readiness work about 12 to 24 months before going public. For payment platforms, that lead time is less about calendar padding and more about whether finance and payments operations can support public-company reporting without heavy manual backfills or person-dependent explanations.

Who this is for#

This is for founders, CFOs, finance leads, payments operators, and cross-functional owners deciding where to launch next when the limiting factor is operational credibility, not topline ambition. If your team is comparing countries, verticals, or money-movement routes, the question is not only whether demand exists, but whether your records and controls will hold up under ongoing reporting obligations and internal certification requirements.

This is especially relevant for cross-border platforms. Regulatory and supervisory approaches to PSPs vary by jurisdiction, and those differences can increase compliance complexity and slow processing. A market may look commercially attractive and still be the wrong near-term choice if settlement evidence, exception handling, and close mechanics are not reliable enough.

What you will leave with#

You will leave with a decision sequence to use before approving expansion or claiming readiness. It includes explicit go or no-go checkpoints, evidence expectations, and named ownership across finance, payments ops, compliance, and engineering. The sections that follow give you three things:

- A sequencing rule that keeps market-entry decisions separate from IPO-readiness decisions.

- Concrete checkpoints for traceable records, reconciliation outputs, and approval evidence that support SEC reporting and ICFR expectations.

- Clear ownership for settlement integrity, control evidence, exception handling, and policy gating.

Use one standard for every decision. If a new market or payment flow cannot produce records you can reproduce and explain, it is not ready, even if the revenue case is strong.

For a practical look at automating payment operations, see How Platforms Are Using AI to Automate Payment Operations: Use Cases and ROI.

Separate expansion readiness from filing readiness on day one#

Keep expansion readiness and filing readiness on separate decision tracks from day one. A country or vertical can be launch-ready on local authorization requirements and still be unready for an Initial Public Offering (IPO) if your records and controls cannot support U.S. Securities and Exchange Commission (SEC) reporting.

Track 1 versus Track 2#

Market-entry readiness is jurisdiction-specific. In the UK, firms may need FCA authorisation or registration to provide payment services or issue e-money. In the EU, PSD2 identifies eight types of payment services that require a licence. That is a launch-access decision.

Filing readiness is different. It is a reporting and control decision. Form S-1 disclosure ties to Regulation S-K for non-financial disclosures and Regulation S-X for financial statement form and content. After listing, obligations continue through Form 10-K and Form 10-Q, including CEO/CFO certifications and quarterly evaluation of disclosure controls.

Treat ICFR and SOX as build constraints#

Treat internal control over financial reporting (ICFR) and SOX Section 404 as design constraints, not cleanup work after growth. Management must state responsibility for adequate internal control over financial reporting and assess effectiveness.

Use a simple internal checkpoint. Pull one sample transaction packet from source event to ledger impact to month-end support. If finance cannot produce source records, processing steps, reconciliation output, and approver evidence without reconstruction, that launch path is not filing-ready.

Set an internal gate and owner map#

Set an explicit internal rule: if a launch path cannot produce traceable records that could support SEC financial reporting, defer it or narrow the scope.

Assign ownership before approval. For example, finance can own control evidence and retention, payments ops can own settlement integrity, and compliance can own policy gating, including launch-blocking requirements.

A common failure mode is approving a market on demand strength, then discovering at quarter close that the flow cannot be explained cleanly. That is the point where expansion speed turns into reporting risk.

Build a country-and-vertical decision matrix before committing GTM#

Build one matrix that scores controllability as heavily as revenue, and make the sequencing rule explicit. If two markets have similar upside, choose the one with cleaner controls and stronger evidence generation.

Score the real payment path, not market headlines#

Do not greenlight a market based on provider support alone. PSP availability and payout behavior vary by country, region, and industry, settlement currency options vary by country and region, and local payout gaps can force cross-border settlement that changes how the operation works.

| Matrix area | What to score | Decision checkpoint | Red flag |

|---|---|---|---|

| PSP coverage and payouts | Provider support, payout behavior by market/vertical, settlement currencies by market | Confirm exact market + vertical coverage and payout flow before GTM commit | "Supported" market, but payout restrictions or unmapped cross-border settlement |

| Disputes and MoR fit | Chargeback fee and dispute workload, plus Merchant of Record (MoR) ownership fit | Validate who is legally responsible for payment processing and transaction compliance obligations | High dispute burden with unclear legal/operational ownership |

| Compliance friction | KYC, KYB, and AML obligations by program and market | Use market-program specific requirements, not one global checklist | Teams assume one onboarding package works everywhere |

| Collections rails (including VBAs) | Virtual Bank Account availability, unresolved transfer handling, and return behavior for ACH paths | Test matched and unmatched transfer paths end to end | Auto-match failures create manual queues that must be reconciled |

Add compliance columns by market and by program#

AML is risk-based and implemented differently across jurisdictions, so your matrix should capture market and program differences directly. If your flow includes U.S. legal entities, treat beneficial-owner identification at account opening as a required onboarding control, with clear capture and review evidence.

Treat collection rails as exception systems#

VBAs can support transfer collection, but unreconciled transfers can still create manual reconciliation work. Score that investigation burden up front, not after launch.

For U.S. ACH collection paths, include return-rate monitoring in matrix scoring:

- Unauthorized return rate threshold:

0.5% - Administrative and overall return-rate inquiry/evaluation levels:

3.0%and15.0%

Make sequencing control-first#

Write the rule before the internal debate starts. Faster launch does not win by default when the control burden is materially higher. A depth-first sequence is often the safer path, especially as payment and banking setups become more fragmented.

For a control-focused view of enterprise diligence, see SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For.

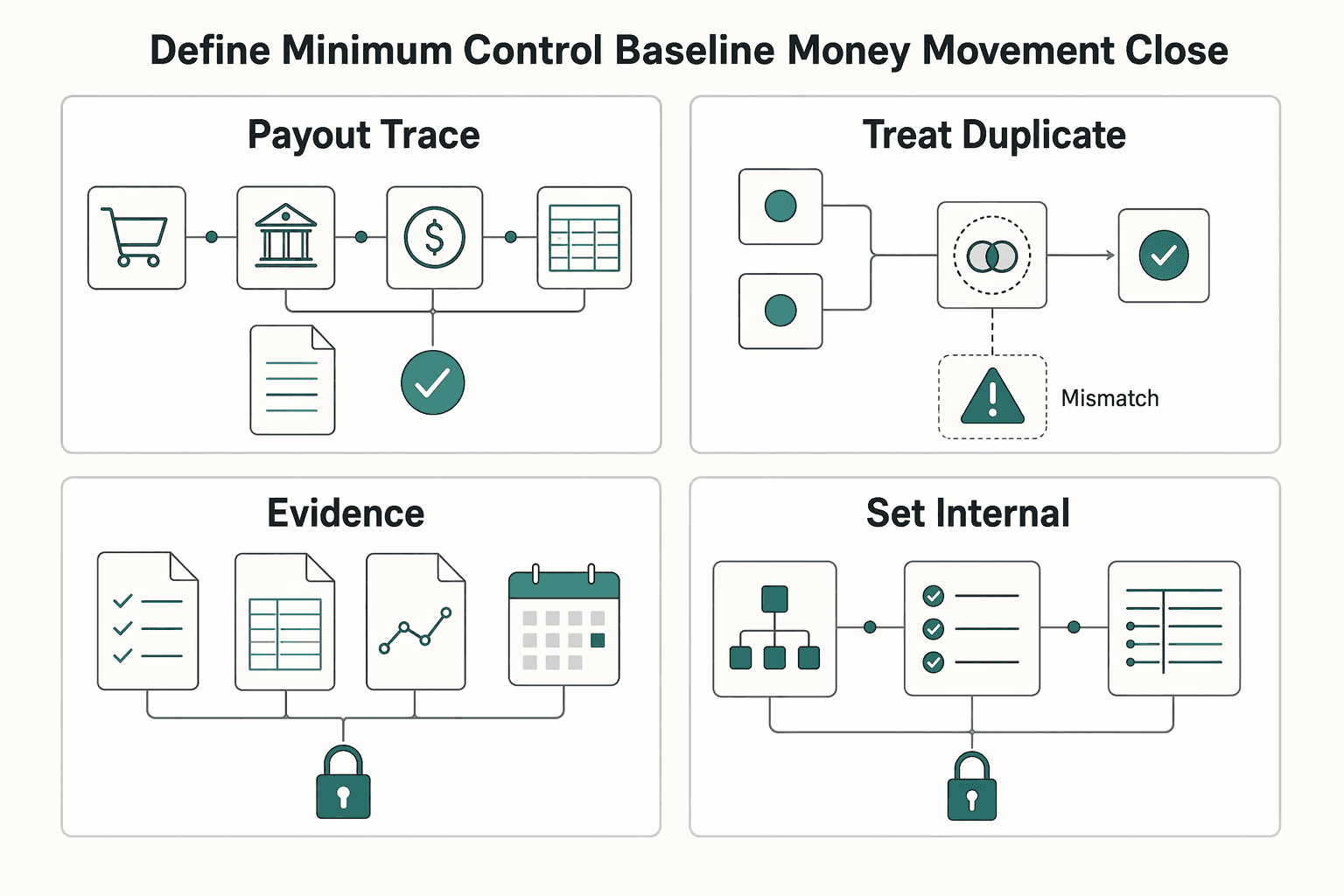

Define the minimum control baseline for money movement and close#

Your launch matrix helps you decide where to go. This baseline tells you whether a flow is ready at all. If you cannot trace a transaction from origination to the ledger and support the month-end evidence, treat that rail as not ready for expansion or an IPO path.

ICFR is not optional cleanup. Issuers must evaluate ICFR effectiveness at each fiscal year end, file management's annual ICFR report, and retain evidential documentation. In practice, your stack needs to produce records a reviewer can follow, not just balances that happen to look right at close.

- Map request-to-ledger traceability for every flow.

Use the AS 2201 walkthrough concept. Can someone follow one transaction from origination through your systems into financial records? For payment flows, map invoice or payment request, PSP event, settlement batch, bank movement or VBA credit or return, payout, reversal, and final journal entry. Keep stable identifiers at each step: internal transaction ID, PSP event ID, settlement or file reference, bank or VBA reference, payout batch ID where relevant, and journal ID. If a step depends on ad hoc exports or analyst memory, that control point is weak.

- Treat duplicate-safe processing as a hard rule.

Duplicate posting is a books-and-records risk. Webhook duplicates are an expected condition, and event-ID logging is a standard guard. For retryable requests, use idempotency keys so retries do not repeat the operation. Record the provider event ID or idempotency key, operation type, first processing result, and resulting journal reference. Then replay the same webhook or retry condition and confirm no second journal posts. Also account for idempotency-key retention behavior, for example Stripe notes keys can be removed once they are at least 24 hours old, when defining your own duplicate-detection window.

- Define month-end evidence by flow, not as one generic close binder.

SEC standards do not mandate your artifact names, but they do require records that fairly reflect transactions and support financial reporting. Each major flow should show how recorded amounts tie to asset movement and how differences are handled.

| Flow | Example month-end evidence | Reviewer checkpoint | | --- | --- | --- | | PSP settlements | Reconciliation from provider report to bank receipt to ledger, including fees/reserves treatment | Reviewer can trace one settlement line to the journal without ad hoc transformation | | VBA credits and returns | Unmatched-item log, return investigation status, aging of open exceptions | Reviewer can see unresolved items, ownership, and whether balances remain valid | | Payouts and reversals | Payout batch reconciliation, failed/reversed payout exceptions, approval evidence for corrections | Reviewer can tie payout population to cash movement and confirm reversals did not create duplicate postings |

Attach sign-off to each flow, not only to a global close approval. If recorded accountability and existing assets differ, the evidence should show follow-up, not just a net adjustment.

- Set an internal no-go-live checkpoint for new rails/routes.

Use a hard internal gate for new rails and routes: do not launch a new PSP route, VBA path, or payout rail until reconciliation is reproducible end to end from source event to ledger journal. If finance and engineering cannot both repeat the result, the route is still experimental. For this gate, keep field mapping, a sample source event or file, expected journal logic, reconciliation output, exception path, and named reviewer approval. Watch for red flags: manual CSV edits before posting, unmatched items without owners, or temporary journals outside the normal trace. Those shortcuts get expensive later, especially when management cannot conclude ICFR is effective if material weaknesses exist.

Related: Month-End Close for Payment Platforms: A Step-by-Step Checklist for Finance Teams.

Sequence execution in three phases with clear exit criteria#

Once the minimum control baseline is in place, sequence execution with evidence-based gates. If phase-exit evidence is incomplete, do not advance. Reduce launch scope instead of piling on manual compensating steps. Treat these phase labels as an operating model, not a regulatory sequence.

| Phase | Core work | Exit evidence |

|---|---|---|

| Phase 1 stabilize | Stabilize the markets and rails carrying the most volume | Each top-volume market has a repeatable trail from source event to cash movement to ledger journal, with clear review evidence and follow-up on differences |

| Phase 2 standardize | Standardize the control design to a suitable, recognized control framework and document reporting support | Control narratives for each reportable money-movement flow; documented exception-handling expectations with named owners, aging logic, and escalation paths; reviewer sign-off rules; reporting flows showing how ledger balances roll into external reporting support |

| Phase 3 scale | Scale only when evidence is repeatable, reviewer ownership is explicit, and failure recovery is tested | Run controlled failure tests before adding markets or routes, then confirm exception handling, approvals, reprocessing, and final ledger outcomes remain auditable |

Phase 1 stabilize#

Start by stabilizing the markets and rails carrying the most volume, and make coverage the goal. Exit this phase only when each top-volume market has a repeatable trail from source event to cash movement to ledger journal, with clear review evidence and follow-up on differences.

Use a strict checkpoint during close. Sample settlement activity, a returned credit, and a payout reversal. If a reviewer cannot trace each item without analyst memory, pre-posting spreadsheet edits, or side-channel explanations, stay in Phase 1.

Phase 2 standardize#

Standardize the control design to a suitable, recognized control framework and document reporting support so it is defensible in an IPO process. This phase should line up with regulatory timing. Disclosure controls are evaluated at quarter-end, and management's ICFR assessment is annual at fiscal year-end.

Before exit, document:

- control narratives for each reportable money-movement flow

- documented exception-handling expectations with named owners, aging logic, and escalation paths

- reviewer sign-off rules for reconciliations, corrections, and unresolved items

- reporting flows showing how ledger balances roll into external reporting support

If you expect to be subject to SOX Section 404(b), make sure the annual-report package can support auditor evidence. If you are still eligible as an Emerging Growth Company, that accommodation does not reduce the need for strong management evidence.

Phase 3 scale#

Scale only when evidence is repeatable, reviewer ownership is explicit, and failure recovery is tested. "The close worked" is not enough for phase exit.

Run controlled failure tests before adding markets or routes. Then confirm exception handling, approvals, reprocessing, and final ledger outcomes remain auditable. If recovery depends on a single operator workaround, reduce scope and keep the market in pre-scale status.

Related reading: Gig Worker Financial Wellness: How Platforms Can Offer Savings and Insurance as Benefits.

Assemble the evidence pack auditors and bankers will actually request#

Build this as a standing, approved evidence pack before diligence starts. Keep quarter-by-quarter control-change history rather than a year-end snapshot. Tie each artifact to ICFR and SEC reporting support so management can show responsibility, evidence, and conclusions without relying on oral reconstruction.

Request lists vary by deal, but the core diligence test is usually the same: can an auditor or underwriter follow the record from objective to evidence to conclusion? Regulation S-K Item 308 is the anchor for management's ICFR responsibility and assessment, so this pack should map to financial-reporting objectives, not team preference.

| Core artifact | What it should prove | Verification checkpoint |

|---|---|---|

| Control narratives | The flow, owner, review point, and recognized control framework used for evaluation | Narrative names the control owner, source records, review evidence, and related financial statement assertion |

| ICFR test results | What was tested, what evidence was obtained, and what conclusion was reached | Failed tests link to remediation, retest date, and approver sign-off |

| Reconciliation support (where used) | That source events, cash movement, and ledger impact can be tied back to reporting support | Reviewer sign-off is dated, differences are explained, and unresolved items are visible |

| Change logs | What changed in the quarter, why it changed, and who approved it | Every material control change has an effective date, approver, and reference to updated documentation |

Add compliance records where money movement can be stopped or released#

If payouts or account activation can be blocked, released, or escalated, keep the full case trail. Include written CIP procedures, beneficial-ownership procedures for legal-entity customers, AML internal-control records, independent testing results, and hold-release evidence showing who reviewed what and how the case ended.

Use an AML hold-release case as a spot check. If you cannot quickly pull the hold reason, escalation notes, release approval, and final disposition, treat that as a real diligence gap. Keep supporting records retrievable and retained under your applicable rules, using five years as a common Chapter X baseline in the cited BSA context.

Add tax evidence only when the product actually triggers it#

If your platform collects tax forms or issues information returns, keep the control evidence, not just form copies. For Form W-9, show controls that support collection of a correct TIN for information-return reporting. For Form W-8, track form type, collection date, and expiry logic. A signed Form W-8BEN generally runs through the last day of the third succeeding calendar year unless circumstances change.

For Form 1099 workflows, keep evidence for completeness checks, exception handling on missing or invalid tax data, reviewer approvals, and filing calendars. January 31 is the key date for Form 1099-NEC recipient furnishing and IRS filing. If you mask recipient-facing data, make sure IRS-filed copies follow the no-truncation rule.

Version control is part of the evidence#

Treat versioning and approvals as part of the control evidence itself. PCAOB documentation standards focus on procedures performed, evidence obtained, and conclusions reached, so an undated file in a shared drive is weak support even when the underlying work is sound.

Use an approval record with artifact ID, version, approver, timestamp, and reason for change. If approvals live only in Slack or email and are not tied to the final artifact, close that gap before diligence. If you cannot produce the current approved narrative, the last failed test, and related remediation history in minutes, keep scope narrow and stay in standardize mode.

Choose product architecture that lowers audit and control overhead#

Choose the architecture that keeps responsibility, reconciliation logic, and control evidence consistent across flows. For IPO readiness, fewer responsibility switches, identifier translations, and manual reconciliation paths can make ICFR and SOX evidence easier to defend.

- Pick Merchant of Record deliberately, not by default.

Merchant of Record (MoR) can reduce ambiguity when one entity's payment-processing responsibility is clear, stable, and documented. Verify MoR by charge model in each PSP implementation, not just by contract. In Stripe Connect, direct charges make the connected account the MoR, while indirect charges without on_behalf_of make the platform the MoR. That implementation choice changes control ownership and dispute accountability.

- Use Virtual Bank Accounts only when the full lifecycle is observable.

Virtual bank account flows are strongest when payments can be matched through the account number, transfer reference, and amount, with a clear trail into the ledger. Keep scope narrow if unmatched items depend on spreadsheet-only handling. A practical check is whether finance can retrieve the transfer reference, auto-reconciliation result, manual action (if any), and final posting from one review trail. If auto-reconciliation fails and items remain pending until manual clearance, fix that control path before expanding usage.

- Standardize reference mapping before adding PSP complexity.

Define one approved mapping contract for how PSP reference identifiers and merchant references drive matching and posting. This is a common point where market-by-market control drift can start if standards are loose. Some providers require multiple report families for complete monthly reconciliation, so your mapping spec should explicitly name source reports, matching identifiers, and posting rules for payments, refunds, disputes, and reversals.

- Treat each custom rail as a control-scope increase.

A custom rail can increase control scope, especially when it introduces separate reconciliation logic or manual fallback steps. If a new route needs separate reconciliation logic or manual fallback, your ICFR and SOX burden can increase. Unless the economics or control need is clear, consolidate on fewer repeatable PSP patterns and defer edge-case rails.

Handle compliance and tax gating without blocking growth#

Gate funds movement first, then sequence secondary compliance tooling. Near an IPO, weak payout controls and incomplete tax records can create significant risk, while some reporting enhancements can be sequenced.

Set payout release rules by risk tier#

Use a risk-based onboarding and payout policy, not one universal release rule. U.S. supervisory guidance supports risk-based customer due diligence, and entity onboarding should include beneficial ownership verification for legal entity customers.

| Risk tier | Minimum onboarding evidence | Payout posture | Escalation rule |

|---|---|---|---|

| Low | Basic KYC/KYB and AML screening | Release after required checks pass | Auto-release only when required fields and screening results are complete |

| Medium | Low-tier evidence plus beneficial ownership verification for entities and review of mismatches or missing fields | Delay first payout until review closes | Route false positives and document mismatches to a named compliance reviewer |

| High | Risk-profile-based enhanced review, ongoing suspicious-activity monitoring, documented analyst decision | Hold payouts pending approval | Require release approval, rationale, and case record before funds move |

The key control is the review trail, not just a pass/fail result. Keep linked evidence for the trigger, documents reviewed, analyst decision, release approver, and timestamp.

If your model falls within money services business scope, treat the AML program as a launch gate, not a post-launch enhancement. The program should be commensurate with your location, size, and transaction profile.

Separate blockers from sequenced work#

Keep the launch gate narrow and strict. Controls that protect funds flow are blockers. Reporting improvements can be sequenced later only if they do not weaken onboarding, payout release, or suspicious-activity handling.

- Launch blockers

- KYC, KYB, and AML checks required before payout release * Beneficial ownership verification where entity onboarding requires it * Named escalation path for holds, false positives, and suspicious-activity review * Evidence retention for approvals, overrides, and release decisions

- Post-launch enhancements

- Improved compliance reporting views * Queue analytics and reviewer productivity tooling * Secondary exports for finance or management reporting

If launch depends on manual payout releases without evidence, defer it or narrow scope. If the gap is reporting on top of a controlled hold-and-release process, sequence that work later.

Align tax-document operations early#

Apply the same gating logic to tax operations. Collect a W-9 form when payer information reporting requires a correct TIN. For foreign entities, collect the appropriate W-8 form (commonly Form W-8BEN-E) to document foreign entity status for U.S. withholding and reporting. If payouts create Form 1099 obligations, establish the handoff early so records are complete before the January 31 filing deadline referenced for Form 1099-NEC instructions.

| Workflow | Use when | Key form or deadline |

|---|---|---|

| W-9 | Payer information reporting requires a correct TIN | Collect a W-9 form |

| W-8 | For foreign entities to document foreign entity status for U.S. withholding and reporting | Collect the appropriate W-8 form, commonly Form W-8BEN-E |

| Form 1099 | Payouts create Form 1099 obligations | Establish the handoff early before the January 31 filing deadline referenced for Form 1099-NEC instructions |

| FBAR | U.S. persons have aggregate foreign account value above $10,000 during the calendar year | Due April 15 with an automatic extension to October 15 |

| FEIE | Separate individual workflow | Claim through Form 2555 |

Keep Foreign Bank Account Report (FBAR) and Foreign Earned Income Exclusion (FEIE) as separate workflows. FBAR is an annual reporting obligation for U.S. persons when aggregate foreign account value exceeds $10,000 during the calendar year, due April 15 with an automatic extension to October 15. FEIE is a separate individual workflow claimed through Form 2555. Do not treat FBAR or FEIE as substitutes for W-9 or W-8 documentation.

For this checklist, use a simple tradeoff rule. Favor stricter onboarding when it materially improves evidence quality for higher-risk cases near IPO milestones.

Stress-test failure modes before adding markets#

Do not add markets until your team can break core payment flows on purpose and still preserve ledger accuracy, approvals, and audit evidence. This is an ICFR-oriented test of whether controls hold under stress, not just on clean operating days.

Simulate failures that can distort close#

Prioritize scenarios that can change balances, delay reconciliation, or create duplicate activity:

| Scenario | What to test | Passing evidence |

|---|---|---|

| Delayed PSP settlement files | Verify finance can separate pending from posted activity | A dated exception record, documented handling of provisional entries, and a clean tie from source transactions to final settlement data |

| Duplicate webhook delivery and retries | Replay the same webhook event and retry the same API request with the same idempotency key | One business event creates one ledger impact, while duplicates are detected, logged, and suppressed |

| Unmatched inbound deposits or references | Inject deposits with missing or conflicting reference data | The exception queue keeps bank reference, amount, receipt time, owner, and final disposition |

| Payout batch partial failures | Simulate batches where some payouts settle and others fail or return | Batch-level evidence includes counts, credits, and debits, not only net totals; reprocessing captures the original payout ID, failure reason, destination-data correction, if any, approver, and retry outcome |

- Delayed PSP settlement files

Hold back expected settlement inputs and verify finance can separate pending from posted activity. Where settlement reporting follows a fixed daily window (for example, 12:00PM daily), test late, incomplete, and post-close arrival cases. Passing means a dated exception record, documented handling of provisional entries, and a clean tie from source transactions to final settlement data.

- Duplicate webhook delivery and retries

Replay the same webhook event and retry the same API request with the same idempotency key. Passing means one business event creates one ledger impact, while duplicates are detected, logged, and suppressed.

- Unmatched inbound deposits or references

Inject deposits with missing or conflicting reference data and verify the exception queue keeps bank reference, amount, receipt time, owner, and final disposition. Keep items unmatched until supporting evidence allows allocation.

- Payout batch partial failures

Simulate batches where some payouts settle and others fail or return. Reconciliation should use batch-level evidence, including counts, credits, and debits, not only net totals. Reprocessing should capture the original payout ID, failure reason, destination-data correction, if any, approver, and retry outcome.

Stress KYC/CIP and resilience controls under load#

Test throughput pressure, not just transaction defects. Because CIP sits inside AML compliance, run volume-spike scenarios where identity verification timing is stressed after account opening, and confirm retry loops do not create inconsistent statuses.

Run outage and failover exercises without compromising production environments. If a primary PSP path is unavailable, fallback handling should preserve event identity and journal traceability so recovery does not create duplicate postings or orphaned entries.

Require evidence that maps to ICFR objectives#

Every exception queue, approval, and reprocessing path should map to reliable external financial reporting controls. For each drill, retain the trigger, reviewed records, analyst decision, approver, timestamps, and final ledger outcome.

Treat early signals as control gaps even before a visible misstatement. Rising exception aging, manual duplicate reversals, or payout reissues that cannot be tied to the original batch can be escalation triggers.

Make postmortems change the control#

Keep postmortems short but action-forcing. Record:

- failed scenario and impacted balance/assertion

- detection point and evidence used

- temporary containment

- permanent control or product change

- owner, remediation due date, and retest date

If the same failure repeats, do not add another manual patch. Fix the control design, narrow scope, or defer the market.

For a step-by-step walkthrough, see Webhook Payment Automation for Platforms: Production-Safe Vendor Criteria.

Run sanity checks before each expansion or filing decision#

Use four binary checks before approving a new market or moving toward an IPO. If any answer is no, pause expansion and fix the control first.

- Can finance rebuild key balances from ledger journals and underlying transaction records?

Require the team to reproduce key balances directly from ledger journals and source references, without ad hoc spreadsheet remapping, manual netting, or post-close logic outside controlled posting rules. If the same balance cannot be tied out by different reviewers without new transformations, treat it as a books-and-records control gap.

- Are ICFR owners explicit and judged on evidence quality?

ICFR ownership cannot sit vaguely with "finance" or "ops." Name the control owner, reviewer, and approver for each close-critical control, and judge performance on complete, dated, independently reviewable evidence, not ticket closure. Red flags include timestamp-free screenshots, approvals buried in chat, and exception logs with no named decision-maker.

- Do KYC, KYB, and AML gates reflect actual market exposure?

Your controls should match the countries, customer types, products, and payout paths you actually run. Confirm beneficial-owner capture at new account opening where applicable (including exclusions, exemptions, and institution-specific relief), and confirm ongoing risk-based due diligence is enforced in product behavior and review queues, not just written in policy text. A single global policy with undocumented local carve-outs is usually weak enforcement.

- Would this month survive mock SEC diligence without backfilling?

Take one recent month and run it like external review. The pack should already include reconciliations, control narratives, exception aging, change logs, and management sign-off in a form an experienced outsider can follow without prior context. If evidence must be recreated after the fact, treat that as a filing-readiness risk.

Practical threshold: if you cannot assemble that pack under a Form 10-K timeline of 60, 75, or 90 days, depending on filer status, your control environment is not ready for more surface area.

For an operational approach to ongoing risk controls, see Continuous KYC Monitoring for Payment Platforms Beyond One-Time Checks.

Conclusion#

For IPO readiness, sequencing can be decisive. Validate one market's operating fit first, then scale only where your control evidence can withstand ICFR and SEC scrutiny.

A payment platform is not ready because policies exist on paper. It is ready when a walkthrough can trace a transaction from origination through the company's processes and information systems into financial records, with complete, reviewable evidence.

That standard matters because ICFR is about reporting reliability. Management's annual report must include its assessment of ICFR effectiveness as of fiscal year-end. If a material weakness exists, management cannot conclude ICFR is effective. A clean set of financial statements alone does not remove ICFR failure risk.

The timeline is usually measured in 12 to 24 months, not the quarter before filing. Material weaknesses are frequently disclosed in initial registration statements, which is exactly why control design has to start well before the filing window.

Use a hard operating gate before expansion:

- Rebuild one market's key balances from source transactions, settlement activity, bank activity, and ledger journals.

- Verify the evidence pack is complete: dated reconciliations, exception logs and aging, and reviewer approvals.

- Make an expand-or-defer decision based on traceability and control evidence, not growth pressure.

If you qualify as an Emerging Growth Company, you may have scaled accommodations, including no auditor attestation under SOX 404(b), potentially for the first five fiscal years after IPO. That changes part of the compliance timing, not the need for controls that operate reliably in daily practice. If you want a market-by-market IPO-readiness review focused on controls and traceability, book a readiness walkthrough.

Frequently Asked Questions

What is the minimum IPO readiness checklist for a payment platform finance team?

At minimum, your team should be able to support key cash and revenue balances with underlying transaction, settlement, bank, and ledger records. You also need defined ICFR ownership, disclosure controls that support timely reporting, and retained evidential matter for management’s assessment. Before filing, that baseline includes management’s annual ICFR report plus required principal executive and principal financial officer certifications on quarterly and annual reporting.

How is a payment-platform checklist different from a generic CFO IPO checklist?

A generic IPO checklist often stays at close, governance, and disclosure readiness. A payment-platform checklist should also separate tax reporting lanes explicitly, including when transactions belong on Form 1099-K rather than Form 1099-NEC or Form 1099-MISC.

Which controls are required before market expansion versus before filing?

Before expansion, focus on controls and evidence that remain reliable in the new market and align to the actual model and jurisdiction. Where beneficial-owner procedures apply, they should be written and operating at onboarding, not deferred. Before filing, the standard rises to SEC-ready disclosure controls, a documented ICFR evaluation, and evidential matter strong enough to support management’s conclusion.

How should teams prioritize ICFR, SOX, SEC reporting, fraud controls, and governance by phase?

Use a top-down, risk-based order. Start with the highest-risk financial reporting flows, then formalize ICFR and disclosure controls with clear review evidence, and then scale governance and reporting layers. Controls that materially affect how information is recorded, processed, summarized, and reported should be prioritized early because they directly affect reporting reliability.

What details are usually missing from generic IPO checklists for multi-country payment operations?

Generic lists often understate tax-document workflow detail, including W-9 collection and the split between 1099-K and 1099-NEC/1099-MISC handling. They can also miss the need for consistent evidential matter across markets and providers for management’s assessment. Compare your close pack against a payments-specific checklist like this one.

When should we choose MoR over direct PSP expansion for IPO readiness?

A Merchant of Record model can be one option, but it is not a universal transfer of responsibility. Do not assume the label always transfers responsibility in the same way, because MoR treatment is context-sensitive and can differ by structure. Before relying on it, validate responsibilities across contracts, settlement ownership, disputes, tax handling, and regulatory obligations, and factor in that recent U.S. enforcement has scrutinized claimed MoR and reseller models when operations did not match the label.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-17/chapter-II/part-240/subpart...trusted

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- sec.gov/files/rules/final/33-8238_0.htmtrusted

- sec.gov/resources-small-businesses/going-public/exch...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: