Quick Answer

Use a fixed close order: confirm scope and cutoffs, reconcile PSP Settlement Report to Bank Statement, then tie Subledger activity to the General Ledger (GL) before locking the period. Require AP and AR readiness, track unresolved breaks in an exception register, and allow accruals only when support is complete and the issue is timing-based. Finish with documented approvals and a reconciliation summary so reporting reflects posted, reviewable records.

Why month-end close is different for payment platforms#

Month-end close is a control process, not a calendar ritual. You are proving the prior month's financial activity is complete, reviewed, and consistent enough to close with confidence. In practice, that means records across systems and reports align before the period is treated as closed.

Close work covers reconciliations, journal entry review, accrual posting, and financial reporting. The objective is simple: every transaction is captured, and the resulting numbers reflect the company's true financial position. Because close is cross-functional, quality depends on timely, usable inputs from multiple teams and systems.

Treat close as proof, not output#

A finished income statement and balance sheet are not enough on their own. A strong close means the underlying records were checked, exceptions documented, and manual changes supported. If reports go out while supporting files are late, incomplete, or still disputed, you have output without control.

This article treats close as a proof process from start to finish. The focus is not just posting entries, but confirming reconciliations happened, accruals were justified, and reviewers can trace entries back to source records.

What this checklist helps you do#

The sections that follow give your team a close sequence you can run right away. They help you:

- define period scope and deadlines

- assign owners and handoffs across finance and partner teams

- move from reconciliation to adjustments and exception handling with clear decision points

The goal is controlled execution first, then speed. Many teams target a 5-10 business day close, but benchmarks vary. Some teams still take six days or more, and a meaningful share take more than 10 days. The better signal is whether your team can explain how the numbers were assembled and approved.

Where closes usually break#

Close quality usually breaks at the inputs. One late accrual, missing invoice, or unapproved journal entry can delay the timeline and trigger rework across multiple owners.

Manual, multi-source input is another common failure mode. Rekeying data across spreadsheets or stitching figures from multiple exports increases the risk of transposition errors, missed entries, and wrong classifications. A useful early control is to confirm each figure has a current source file, a clear owner, and a reviewer before it reaches final posting. When that chain is missing, teams often discover the problem only after reporting drafts are already circulating, when fixes are slower and more disruptive.

Related: How Finance Teams Shorten Month-End Close With Automation.

Define the close scope before work starts#

Write the close scope before reconciliation starts. If scope is vague, your team will spend close time debating what belongs in the period instead of closing it.

| Scope item | What to define | Why it matters |

|---|---|---|

| Period boundary | What is in scope, what is deferred, and which date controls close treatment | Helps reviewers decide whether an exception belongs in this period |

| Definition of complete | Required Journal Entry reviews, Accrual postings, and expected support for manual entries; AP and AR subledgers closed before final postings | Prevents reporting numbers when key support is still missing |

| Ownership and sign-off | Task owners and which issues block sign-off versus move to post-close cleanup | Avoids mid-close severity debates and keeps escalation cleaner |

| Period-lock authority | The lock decision point, who can lock or reopen the period, and the exception path for late items | Prevents informal changes after sign-off from weakening earlier controls |

- Set the period boundary up front.

List what is in scope for this close and what is intentionally deferred. Keep it specific enough that a reviewer can look at an exception and quickly decide whether it belongs in this period. If different functions work from different operational dates or export windows, state which date controls close treatment so people are not arguing over timing during review.

- Define "complete" in accounting terms, not calendar terms.

State which Journal Entry reviews and Accrual postings are required for this close and what support is expected for manual entries. A practical checkpoint is confirming AP and AR have closed their subledgers before final postings. If key support is missing when numbers are reported, your close definition is too loose.

- Set ownership and sign-off rules before execution.

Assign clear owners for each close task and document which issues block sign-off versus which are logged for post-close cleanup under your policy. This prevents mid-close debates about severity and keeps decisions consistent. It also makes escalation cleaner, because people know whether they need a decision, a file, or a formal exception.

- Document period-lock criteria and authority.

If your process uses a period lock, define the lock decision point, who can lock or reopen the period, and how late items move through a controlled exception path. A late accrual, missing invoice, or unapproved journal entry can throw off the process if this is not explicit. If periods can be changed informally after sign-off, earlier controls lose force.

A short scope checklist is enough if it is current and version-controlled. Because close is cross-functional, settling scope early protects accuracy and avoids preventable delays.

For a deeper walkthrough of reconciling PSP settlements, bank statements, and the ledger, read Month-End Close Checklist for Payment Platforms: Reconciling PSP Settlements Bank Statements and Ledger.

Set owners, cutoffs, and handoffs by function#

Once scope is clear, make ownership and timing just as explicit. Many close delays are handoff problems, not technical ones.

Assign owners and backups by close lane#

Use named owners for each lane in your close process, and set a backup for each one. In most close cycles, that includes Accounts Payable (AP), Accounts Receivable (AR), reconciliation, and final review, with inputs from teams like Sales, HR, and Procurement.

Before final postings, require a concrete readiness check: AP and AR should confirm their subledgers are closed or clearly state what remains open and why. A backup should be able to do more than attend status meetings. They should be ready to step in with current status, open items, and escalation context.

Publish cutoffs for source inputs#

Set and publish cutoff expectations for the inputs your close depends on. Keep those cutoffs visible in the close ticket or calendar so every function is working to the same timeline.

After cutoff, track exactly which input version is in scope for the close. If a file is revised later, treat it as an exception and review the impact before replacing anything downstream. In practice, the team should be able to answer two simple questions at any time: which file version are we using, and who approved that version for close use?

Define handoff evidence and escalation#

Define what each handoff must include so "done" is auditable, not implied. Each handoff should make clear what is complete, what remains open, and who owns the next decision.

Set an escalation path for missed cutoffs. A slipped handoff can throw off the full close process, so if it happens, log it, assign the next action, and state the expected impact on posting timing before final review. Handoffs should also state whether the work is final, provisional, or waiting on one named dependency. That small label saves review time and helps reduce late surprises and rework.

For a step-by-step walkthrough, see Measure AP Automation ROI for Payment Platform Finance Teams.

Assemble the evidence pack before day-zero reconciliation#

Do not let reconciliation start as a file hunt. Build and validate the evidence pack before Day 0 so the team starts from a stable source set. Close work can begin before the period boundary, and a weak checklist review can create false-close risk.

| Prep step | Requirement | Control purpose |

|---|---|---|

| Ready to reconcile | Use the same evidence-set structure each month with clear source context and ownership | Lets another reviewer pick up the pack without extra explanation |

| Pre-Day 0 staging | Assemble and stage inputs before Day 0 | Reduces month-end load and shifts time toward decisions instead of file collection and cleanup |

| Pre-reconciliation review gate | Confirm the pack is complete, consistent, and in scope before reconciliation starts | Catches material changes and checklist-review gaps before active close work |

| Reviewed version set | Document the in-scope source set, who approved it, when it was approved, and log exceptions | Keeps later information on an explicit exception path instead of drifting into the close unnoticed |

Use one controlled close folder, one agreed artifact list, and one review checkpoint before anyone starts matching differences. Keep the format reusable month to month so execution stays consistent, even if the tool is simple.

1. Standardize what "ready to reconcile" means#

Define the evidence set your team needs for this close cycle and require the same structure each month. The goal is repeatability: everyone can find the same inputs in the same place, with clear ownership. A pack is not ready just because the files exist. It is ready when the source context and owner are clear enough that another reviewer can pick it up without extra explanation.

2. Pull work forward before Day 0#

Do not wait for Day 0 to assemble and stage inputs. Pre-close preparation reduces month-end load and lets the team spend close time on decisions, not collection and cleanup. The earlier you detect missing or inconsistent inputs, the more likely you can fix them before close pressure peaks.

3. Run a pre-reconciliation review gate#

Before reconciliation starts, confirm the pack is complete, consistent, and in scope for the close cycle. If anything material changes after review, treat it as an exception and re-evaluate the impact before replacing files in active close work. This gate is also where teams catch checklist-review gaps that can create false confidence in close readiness.

4. Document the reviewed version set and log exceptions#

Once reviewed, document the in-scope source set for the close window and record who approved it and when. As account volume grows, this control matters more because higher volume increases effort and expands exposure to journal entry errors. Documenting the reviewed set does not mean you ignore later information. It means later information follows an explicit exception path instead of drifting into the close unnoticed.

Reconcile in strict order from provider data to books#

For month-end close, keep reconciliation steps in a consistent order. Start with external records, move inward, and apply period-lock decisions through documented policy once exceptions are addressed.

This checklist does not assume one universal payment-platform sequence, payout-status rule, VBA treatment, or numeric lock threshold. Document those controls as internal policy and apply them consistently each month.

1. Start with external evidence, then move inward#

Begin with the most external records available for the close window, then move toward book balances. If your process includes files such as a PSP Settlement Report and Bank Statement, treat their order as an internal policy choice rather than a universally proven requirement. Starting with independent evidence helps reduce the temptation to force operational detail to fit what is already in the books.

2. Keep one progression and separate each check#

Do not collapse multiple checks into one pass. One policy-based progression is:

| Stage | Evidence pair | Decision this stage supports |

|---|---|---|

| External to cash | External report to bank activity | Whether reported movement is reflected in bank records for the period |

| Cash to detail | Bank activity to internal transaction detail | Whether cash movement is captured completely and in-period |

| Detail to books | Internal transaction detail to General Ledger (GL) | Whether accounting presentation reflects approved detail |

When a break appears, stop at the first stage where it appears and work from there. Do not carry a variance forward and then "solve" it with a later true-up in the General Ledger (GL). That may create a tie on paper while leaving the actual break unidentified.

3. Treat pending operational status as exceptions until policy says otherwise#

Keep unresolved items in an exception lane instead of netting them into final close entries. Operational statuses can help explain differences, but they are not automatic proof that cash is fully settled. The practical question is whether the status helps explain the difference under your policy, not whether it lets you ignore the difference.

4. Apply a written lock decision at cutoff#

Define your rule in advance for unresolved differences at month-end cutoff. If support is incomplete or differences remain unexplained, follow the lock-or-hold path in policy. If provisional posting is allowed by policy, require clear documentation, approval, and follow-up resolution steps. That written rule protects the team from changing standards late in the close just to keep the calendar moving.

Post adjustments with explicit accounting rules#

Adjustments should explain the month, not force it to look finished. Journal Entry and Accrual postings are standard close work, and each one should trace in the General Ledger (GL) to what it represents and why it belongs in-period.

- Separate true accruals from unresolved cash exceptions.

If a settlement or bank difference is still unexplained, treat it as an exception to investigate rather than using an accrual only to make balances tie. Accrued expenses, deferred revenue, and other close entries should come from known activity or a defensible estimate. Before you post, confirm the entry points to a source record or documented estimate method; if it does neither, flag it for review. Your close file should make that distinction visible enough that a reviewer can tell whether the entry reflects known activity or an open reconciliation question.

- Anchor revenue-side entries to your written

Revenue Recognitionpolicy andASC 606.

Record revenue when it is earned, not necessarily when cash is received, and apply the same policy logic every month. For each revenue adjustment, keep a clear trail from policy to contract or billing support to posted amount, aligned to your ASC 606 five-step approach. This matters most where manual tracking is still involved, because that is where error risk and weak audit trails show up fastest. If the policy outcome is unclear, resolve the policy question before close instead of burying it in a manual entry.

- Keep clear support for each manual entry.

For every manual Journal Entry, keep source support in the close file and include reviewer sign-off when your control process requires it. The source can be a contract extract, invoice, usage summary, reconciliation worksheet, or estimate memo. The sign-off format can follow your internal process as long as it is attributable. Good support should let a reviewer quickly identify the evidence and trace the math without rebuilding the entry from scratch.

- Document follow-up intent for temporary entries.

As you approach period close in your financial system, note what should happen next for each provisional accrual or reclass and who owns that follow-up. This helps keep temporary entries from lingering into later closes and creating avoidable cleanup.

For a broader view of how month-end and quarter-end close should be structured, read What Is an Accounting Cycle? How Payment Platforms Should Structure Month-End and Quarter-End Close.

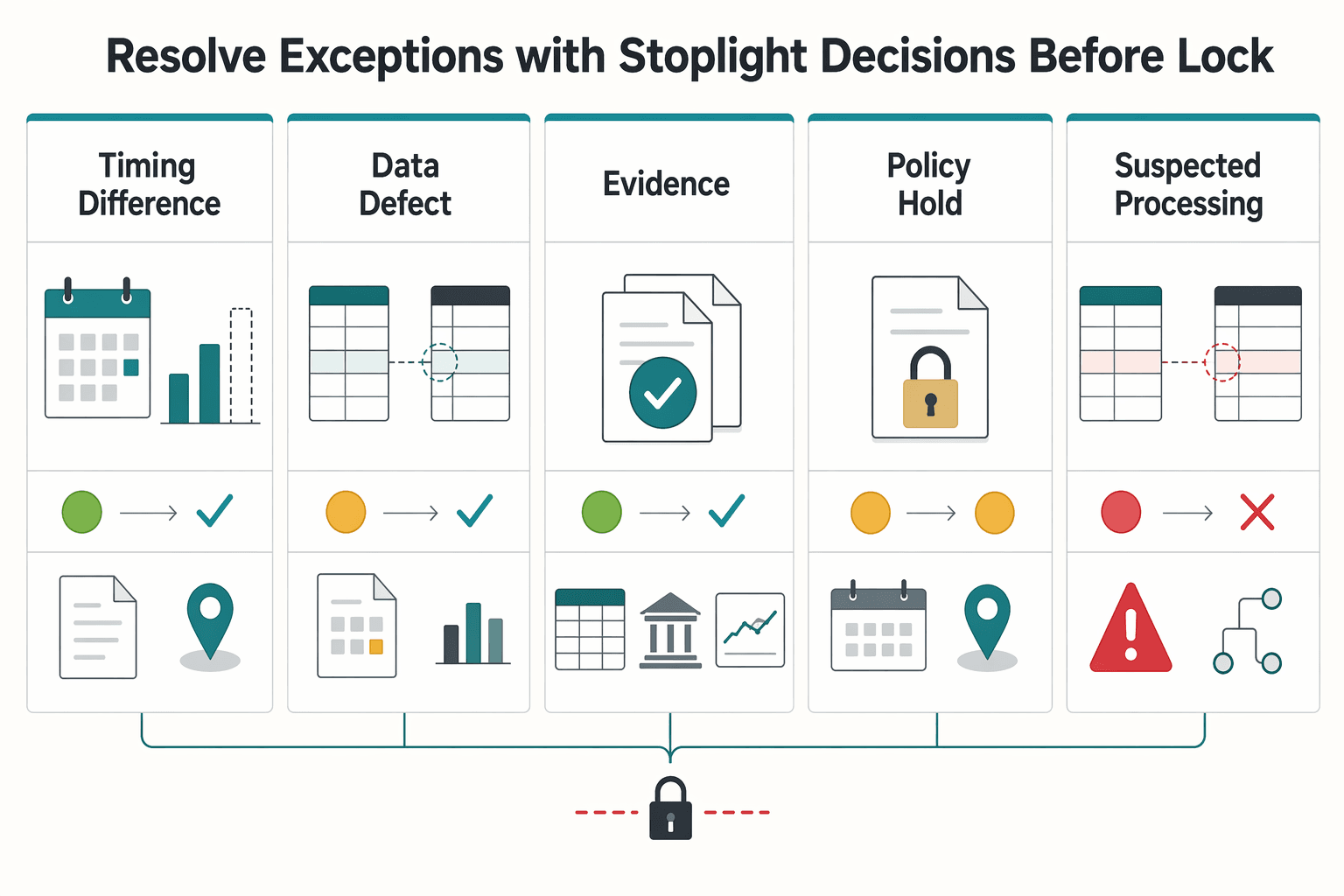

Resolve exceptions with stoplight decisions before lock#

By this stage, every remaining break needs a clear decision. Resolve supported items, carry only what policy allows, and block lock when evidence is still weak. This matters most when exceptions touch finance Critical Data Elements such as General Ledger (GL) and subledger journals, FX rates, or Bank Statement data.

Classify the break before choosing the fix: timing difference, data defect, missing document, policy hold, or suspected processing error. A mismatch alone is not a category. For example, a 500 vs 620 row difference can come from timing, bad exports, or a real processing issue, and each one needs a different response.

| Break type | Default stoplight | Pre-lock evidence test | Close treatment |

|---|---|---|---|

| Timing difference | Yellow | Dated proof the item exists and is expected to clear | Allow controlled Accrual only when impact and reversal path are documented |

| Data defect | Red | Corrected extract, reconciled counts, and reliable source fields/version | Block lock if source integrity is uncertain |

| Missing document | Yellow to Red | Missing item identified, owner assigned, impact known, support sufficiency checked | Close through only if support remains sufficient; otherwise block |

| Policy hold | Red | Accounting treatment agreed and documented with the relevant owners | Block when the hold is financially material |

| Suspected processing error | Red | Root cause isolated and downstream posting impact reviewed | Do not lock until impact is contained |

Use a hard if-then rule: if the issue is timing-only and source integrity is intact, you may use a controlled Accrual; if source integrity is unknown, do not accrue just to force completion. Keep lineage evidence from operational event to close file to ledger effect, because control evidence depends on traceability.

Treat unresolved holds as close-relevant when they gate cash movement or settlement outcomes and materially affect balances.

Track every open item in an exception register with owner, target date, stoplight status, affected account (Accounts Receivable (AR) / Accounts Payable (AP) or other), estimated financial impact, and evidence reference. Maintain a carry-forward register so unresolved items are reviewed at next month kickoff instead of being rediscovered mid-close. If the status changes, update the same record rather than recreating the issue in a new place; close control gets weaker when the history of one exception is scattered across tickets, files, and chat notes.

Automate the high-friction steps first#

Automation helps most when it removes repetitive work without weakening review. Start with the high-volume checks that happen every month, and keep period-lock judgment as a control gate.

- Start with repetitive reconciliation tasks.

Use automation to gather and compare core period records such as transactions, invoices, bank statements, and supporting records. This is where automation can improve speed and reduce manual error.

- Protect input quality before trusting output.

Month-end close depends on clean, timely inputs from multiple systems and teams. Before each run, confirm your inputs are complete and current for the period so the automated result is usable for review. An automated tie built on stale or incomplete files is still a bad tie, just produced faster.

- Use automation to surface exceptions, not bypass them.

Let automation flag breaks for finance review, then resolve the items that can derail timelines, including late accruals, missing invoices, or unapproved journal entries. This keeps control focused on real exceptions instead of mechanical checks.

- Keep management review and lock decisions explicit.

Automation can prepare evidence and improve consistency, but management still needs to review completeness and accuracy before the period is locked. That final checkpoint should stay explicit before period lock. If your tooling makes sign-off easier, use it to organize support and approvals, not to obscure that lock decisions still require management review.

Apply compliance and tax gates that change close completeness#

Some dependencies sit outside core accounting, but they still affect whether the period is truly close-ready. If a compliance or tax item can affect reporting completeness or management sign-off, treat it as a formal close gate or a named exception.

- Treat KYC, KYB, and AML as dated status evidence, not assumptions.

This checklist does not set universal completion standards or payout-blocking rules for Know Your Customer, Know Your Business, or Anti-Money Laundering checks; use your own policy and provider terms. For close control, confirm the current status source, freeze the extract date, and attach that evidence to the close file. The key control is proving what status you relied on at lock time.

- Keep tax-document dependencies visible when your flows depend on them.

For W-8, W-9, Form 1099, VAT, and FBAR items, this section does not establish thresholds or filing rules from the supplied sources. Still, track these items in the exception register when they affect reporting or downstream tax work, and record the document export version, owner, and as-of date. Visibility matters because these dependencies are easy to overlook when the accounting numbers tie.

- For FEIE, keep the rule narrow and documented.

IRS language here applies only to a qualifying individual with foreign earned income who reports that income on a U.S. return. If FEIE planning affects close, verify the physical presence test: 330 full days in a 12 consecutive months window, with each full day defined as 24 consecutive hours beginning and ending at midnight, and only while the person's tax home is in a foreign country.

- Escalate timing and partial-year FEIE issues before period lock.

Missing the 330-day mark fails the physical presence test regardless of reason. Income is generally earned in the year the work is performed even if payment is later, and partial-year qualification requires reducing the maximum exclusion based on qualifying days. If leadership is relying on FEIE, require a dated support pack before lock: day-count calendar, work-period summary, and any IRS adverse-conditions waiver reference being used. If that pack is incomplete, do not treat the issue as implicitly resolved just because it sits outside the core ledger workflow.

Run sanity checks and sign-off gates#

Before you freeze the period, make sure the close can stand on its own evidence. At this point, your ledgers, operational files, and exception record should align well enough to support reporting you can trust.

| Final check | What to confirm | If not true |

|---|---|---|

| Opening-to-closing tie | Movement across in-scope books is explained by posted activity and approved adjustments using a consistent as-of date | Keep it open if the tie depends on draft or unposted entries |

| Operational completeness | Expected artifacts such as Payout Batch files, settlement reports, and exception logs are attached and approved | Route changed approved source files through cut-off policy instead of swapping them in silently |

| Orphan-item review | Unmatched deposits or unposted Journal Entry drafts have a documented disposition | Treat unclear items at freeze time as an open blocker or approved exception per policy |

| Sign-off pack | Reconciliation summary, exception register, approval records, and period-lock confirmation are together and traceable | Do not freeze until items affecting balance completeness, cash movement, or the audit trail are posted or documented as approved exceptions |

Keep this gate repeatable: the same phases, the same order, and the same definition of done each cycle.

- Tie movement from opening to closing across in-scope books.

Reconcile opening to closing balances across the books in scope (for example, GL, Subledger, Accounts Payable (AP), and Accounts Receivable (AR)), using a consistent as-of date for each extract. Confirm movement is explained by posted activity and approved adjustments reflected in the books. If a tie depends on draft or unposted entries, keep it open until the supporting activity is finalized. The test is not whether totals look plausible. It is whether the path from opening balance to closing balance is explained by posted, supported activity.

- Confirm operational completeness with approved artifacts.

Verify the operational artifacts your close process expects (such as Payout Batch files, settlement reports, and exception logs) are attached and approved by the relevant owner. Keep owner, status, approvals, and documentation visible in one place. If an approved source file changes, route it through your cut-off policy instead of swapping it in silently. A reviewer should be able to see, without hunting, which artifacts are final and which are still open.

- Make orphan-item review explicit.

Review orphan items (for example, unmatched deposits or unposted Journal Entry drafts) and document a clear disposition for each one. If disposition is unclear by freeze time, treat it as an open blocker or approved exception per your policy. Orphan review is where hidden work often surfaces, especially items that exist in operational workflows but never made it into the accounting path.

- Assemble the sign-off pack before lock.

Include the reconciliation summary, exception register, approval records, and period-lock confirmation. Keep the full pack together with ownership and status history so approvals and documentation stay traceable. Finalize, document, then freeze. A useful final test is simple: could another reviewer understand why the period was locked using only the sign-off pack and the approved source files?

If an item could affect balance completeness, cash movement, or the audit trail, do not freeze until it is posted or documented as an approved exception under your close policy.

If your sign-off still depends on chasing payout files across tools, standardize status tracking and exception visibility with Gruv Payouts.

Conclusion#

A strong month-end close is driven by preparation, ownership, and clean inputs, not speed alone. Treat the close as a controlled process, not the end of a scramble.

The standard is straightforward: record every transaction, complete reconciliations, review and approve journal entries, post accruals with support, and produce reports from the same finalized data set so results reflect the company's true financial position. Speed matters only after those controls are stable. Many teams aim for a three-day close, but common targets are still 5-10 business days, and one benchmark says 50% take six days or more.

If you keep only three rules from this checklist, keep these:

- Standardize inputs before close starts.

Close is more predictable when inputs arrive on time, in a consistent format, with clear ownership. Confirm core artifacts are ready, including bank statements, invoice support, and the journal-entry queue. A late accrual, missing invoice, or unapproved entry can disrupt the entire close.

- Run reconciliations and reviews in a consistent monthly sequence.

A stable order reduces handoff confusion. Work through key checkpoints before finalizing close: reconciliations, journal-entry review and approval, accrual posting with support, and final reporting from closed books.

- Escalate exceptions early and assign ownership.

It only takes one unresolved issue to put the timeline at risk. Track exceptions with clear owners and deadlines so problems are resolved before reporting is finalized.

Improve one cycle at a time: run the checklist, log misses, tighten decision rules, and apply those fixes in the next close. Better preparation improves execution, and predictable execution reduces errors, avoids last-minute scrambling, and gives stakeholders more consistent reporting.

When you are ready to turn this checklist into a repeatable operating flow, start with the integration patterns in Gruv docs.

Frequently Asked Questions

What makes month-end close for payment platforms different from a generic AP and AR close?

The main difference in this grounding is coordination pressure. Month-end close depends on clean, on-time inputs from multiple systems and teams. If you run it like a simple AP or AR cycle, integration gaps and late inputs can surface late in the process. The work is still accounting work, but cross-system handoffs need tighter coordination.

What exact order should finance teams follow from data cutoff to period lock?

The grounding supports a consistent checklist order rather than one universal exact sequence: collect clean inputs, run reconciliations, post journal entries and accruals, prepare reporting, then lock. Keep the sequence stable so ownership stays clear. If key inputs or approvals are still unresolved, you are not ready to lock.

What are the most common causes of close delays in payment operations?

The usual causes are multi-system data that does not integrate cleanly and late critical items. A single late accrual, missing invoice, or unapproved journal entry can hold up the whole process. Delaying prep work also increases reporting pressure near deadline. Delays often trace back to earlier handoff or input gaps.

Which close steps should we automate first, and which should stay manual?

This grounding does not prescribe a specific automation order. It supports standardizing repeatable tasks first, such as pulling data from multiple systems and tracking checklist ownership. It does not provide evidence for fully automating judgment-heavy exception decisions or approvals.

How do we decide whether to block close or post a controlled accrual?

There is no universal threshold in this grounding for when to block versus accrue. If completeness, support, or approval is unclear, treat it as unresolved and do not lock yet. If the issue is timing-based and documentation is complete, teams may choose a controlled accrual under internal policy.

How do we measure close quality beyond “we finished on time”?

Time alone is not enough, and benchmarks vary: some teams target three days, some guidance cites 5-10 business days, and one benchmark says 50% take 6 days or more. Measure quality by completion and evidence: bank accounts and statements reviewed, reconciliations and journal entries completed, and key financial statements prepared. Also check whether work was deferred until deadline, since deferred close work increases reporting pressure.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- admin.ks.gov/media/cms/SoK_OPC_Procurement_Manual_11_3b8e...trusted

- energy.gov/sites/default/files/2025-07/doe-financial-ma...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- lbb.texas.gov/Documents/Appropriations_Bills/89/House/Hse_...trusted

- ofm.wa.gov/wp-content/uploads/sites/default/files/publi...trusted

- sos.ms.gov/ACProposed/00022285b.pdftrusted

- uanlink.ohioauditor.gov/pdf/uan_win_software/accountingmanual.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Month-End Close for Payment Platforms with PSP Settlement Control

Month-end close often breaks down when PSP settlement is treated as a side reconciliation. For payment platforms, settlement is often the clearest record of what cash should have moved, so it should drive the close rather than being checked after journals are drafted. If you run close across multiple PSPs, you need that settlement record to lead the review before your team starts defending journal entries.

How Finance Teams Shorten Month-End Close With Automation

---

Accounting Cycle for Payment Platforms: How to Structure Month-End and Quarter-End Close

Month-end close on payment platforms usually breaks in three places: timing mismatch, explanation debt, and unclear ownership. The fix is to choose a close structure you can actually run, assign clear ownership for each tie-out, and set verification checkpoints for month-end and quarter-end. That keeps financial statements accurate without pushing cleanup into the next period.