Quick Answer

Finance teams shorten month-end close by automating repeatable matching, imports, and standard journal work while keeping approval gates, traceability, and exception review in place. To shorten month-end close with automation, map PSP settlements, bank statements, and ledger posting end to end, surface mismatches early, and leave audit-ready evidence for every automated action.

Why Finance Teams Automate the Close#

If you want to shorten month-end close with automation, treat close speed as a control-design problem first. You only move faster when matching, journal entries, and exception monitoring preserve authorization, traceability, and review.

The point is not just to move data faster. Internal accounting controls are meant to provide reasonable assurance that transactions are authorized and properly recorded. Period-end journal entries are a known risk area when entries are inappropriate or unauthorized. Durable automation has to do two jobs at once: remove repeatable manual work and leave evidence someone can follow later.

Start with the control points#

In payment environments, focus on three control points:

- Reconciliation: explain how PSP settlements map to bank cash and then to ledger impact.

- Journal entries: generate and post only when the underlying status is valid.

- Exceptions: surface mismatches early, not on the final close day.

Use a simple test for any automated action: can you trace it back to source evidence without rebuilding the story from memory? If not, the speed gain is fragile and auditability is weak.

Tie payouts, bank cash, and ledger posting together#

A single PSP payout can include funds from multiple transactions, so this is not a one-number check. You need to know which transactions are inside the payout and when cash actually lands in the bank.

That is why provider artifacts matter. Stripe frames payout reconciliation as identifying which transactions are included in a payout. Adyen's Settlement details report is built for transaction-level settlement work. PayPal positions reconciliation reports as finance and accounting artifacts for end-to-end close support. In practice, anchor matching and posting to provider evidence, not guessed summary totals.

When you validate the design, trace one recent payout end to end through the records below. If any link is missing, fix that before you scale automation volume.

- PSP settlement or reconciliation report

- related bank statement line

- resulting journal entry and general ledger effect

Design the escalation path before automation misses#

Automation failures can be quiet: unmatched bank lines or entries that post but do not align cleanly in the general ledger. An exception here is not a rounding footnote. It is a case where no matching application transaction is found for a bank statement line.

The goal is not to remove human review. It is to reserve it for true exceptions while keeping exception actions logged and traceable. If an auto-posted entry cannot be tied to reconciled source activity, route it to review. If a payout matches only at summary level but not at transaction level, route it to review instead of forcing it through.

That is the lens for the rest of this guide: payment-platform close across PSP settlements, bank statements, general ledger alignment, and escalation when automation gets close but not all the way there.

This pairs well with our guide on How Platform Operators Control Employee Expenses with Automation.

Set a close target your team can defend#

Set a close target that improves speed without weakening controls. Define success first, then measure whether automation actually reduces elapsed close time.

Define the close target#

Define "shorter" as elapsed cycle time, not effort. Use a fixed start and finish each month, such as from the initial monthly trial balance to completed agreed-upon monthly consolidated financial statements, so before-and-after comparisons stay valid.

Track quality alongside speed. Include checks for unresolved reconciling items at close and clear follow-up after sign-off. If you track reopen frequency, define what counts as a reopen internally and apply that definition consistently.

Baseline each lane#

Baseline each lane separately before automation:

| Lane | What to measure | Verification checkpoint |

|---|---|---|

| Transaction initiation | Initiated items and exceptions | Does each item trace to source evidence and an identified owner? |

| Recording and processing | Posted entries and exceptions | Do entries map to authorized activity and required reviews? |

| Reporting and reconciliation | Completed reconciliations vs unresolved reconciling items | Do reconciling items have follow-up owners and due dates? |

This keeps one lane from masking another. A close can look faster overall while unresolved work is pushed forward.

Set go-live acceptance checks#

Set two go-live acceptance checks and stick to them. First, confirm control activities are documented in policies and procedures, including approvals, transaction reviews, reconciliations, and follow-up of reconciling items. Second, do not allow approval gates to be bypassed, especially for initiating, authorizing, recording, and processing journal entries, and include procedures that address management override risk.

Pause if the baseline is unclear#

If the baseline is unclear, document a minimal Close Runbook before broad rollout. For each lane and unit, document owner, process objective and risk responsibility, cutoff rule, approval point, and completion evidence so someone outside the team can trace one close cycle without relying on memory.

Prepare the minimum inputs before automating anything#

If you want to move faster at month-end, do the prep before you touch matching rules or journal logic. The minimum bar is simple: you can hand someone a compact evidence pack, show who owns each source, and explain how matches work today.

Build an evidence pack from the last real cycle#

Build a close evidence pack from the last real cycle, not the process people assume they follow. One finance leader described well-documented procedures as "11 on a scale of 10" in importance for improving close. The point is practical: automation amplifies missing steps and undocumented exceptions.

Include four items that let someone else reconstruct the last close without relying on memory:

- the current Close Runbook

- the current Cutoff Rules

- the current Escalation Paths

- the last-cycle exception logs

Keep it compact but usable. The Close Runbook should show owner, cutoff point, approval point, and completion evidence by lane. Cutoff Rules should state when PSP settlements, bank activity, and ERP postings are treated as in-period. Escalation Paths should name a person with decision authority for blocked imports, unmatched items, and posting failures. Last-cycle exception logs should show what failed, who handled it, what evidence was used, and whether it carried forward.

Verify the pack with a trace test. Pick one payout and one unmatched bank line from the last close and trace both through the pack. If you cannot identify the applied rule, decision owner, and sign-off evidence, pause rollout. For PSP settlement work, include provider payout reconciliation evidence when available, especially for manual payouts where transaction composition is operator-controlled.

Confirm ownership across ERP, PSP, and banking feeds#

Confirm ownership across Enterprise Resource Planning (ERP), Payment Service Provider (PSP), and banking feeds before automation starts. Close design is cross-functional, and finance leadership is part of that governance, but each source and handoff still needs one accountable owner.

Be specific. For ERP, name who owns journal import mappings, posting failures, and period status. For PSP, name who owns settlement exports, payout reports, and provider-reference issues. For banking feeds, name who owns feed health, statement availability, and import credentials. If you use a close workspace, make the responsible person visible there instead of leaving ownership in chat history.

A quick test helps here: if the bank feed is stale on day one, who can fix it that same day? If the answer is a shared alias or "we ask in Slack," ownership is still incomplete.

Inventory how transaction matching works today#

Inventory how Transaction Matching works today, lane by lane, before adding new automation. Matching means loading transactions from one or more sources, applying predefined rules, and managing exceptions. You need a clear map of manual work, rule-based work, and suggested matches.

Do not blur those states together. Label each queue as manual review, rule-based auto-match, or suggested match requiring user action. If your team uses suggested matches, treat them as proposals until approval and audit trail are explicit.

Use a simple checkpoint: sample ten matches from the last cycle across PSP settlements and bank statements. Record the source pair, whether it was manual or rule-driven, whether a person accepted a suggestion, and who owned any exception. Hidden inconsistency can become a failure mode. Similar cases can get resolved differently, and automation can look faster only because the comparison logic was never stable.

Once the evidence pack, owner map, and matching inventory are complete, you are ready to map the close data path. Before that, tool selection is usually premature.

Need the full breakdown? Read Accounts Receivable Automation for Platforms to Collect from Enterprise Buyers at Scale.

Map your close data path before tool selection#

Do not buy new close automation until your map shows where exceptions start, who resolves them, and what evidence proves the resolution. Use the prep from the last section to build a source-to-ledger path in real work order, not org-chart order.

Map each lane in business sequence#

Map each lane in business sequence: PSP Settlements and Bank Statements into Reconciliation, then Journal Entries into the ERP and General Ledger. Keep final period close after review and matching controls, not before.

For payout lanes, document the join path from payout ID to underlying BalanceTransaction records. If automatic payouts are available, keep that setup where possible to preserve transaction-to-payout association. For bank lanes, map each imported statement line to the internal bank-ledger entry used in matching.

Checkpoint: trace one payout and one bank statement line from source record to match decision to posted journal. If any handoff is unclear, the map is not ready for automation.

Put timing failures on the map#

Treat asynchronous failures as expected control points, not edge cases. At minimum, flag late arrivals, duplicated events, and missing provider references.

Put timing boundaries directly on the map. Undelivered Stripe webhook events can be resent for up to three days, and event retrieval for backfill is limited to the last 30 days. Also mark settlement-file identifiers, such as batch number, date, or unique identifier, at ingestion so exception tracing can quickly isolate whether the break came from export, ingestion, or matching logic.

Add idempotency checkpoints#

Add Idempotency checkpoints anywhere retries can occur. If a retry can re-run ingestion, import, journal generation, or posting, require duplicate-processing guards before any new record is created.

Use one replay test before approving tooling: process the same event or settlement file twice and confirm you get one reconciled outcome with no duplicate journal entry. If the second pass creates a second posting or an extra pending exception, stop and fix the design gap first.

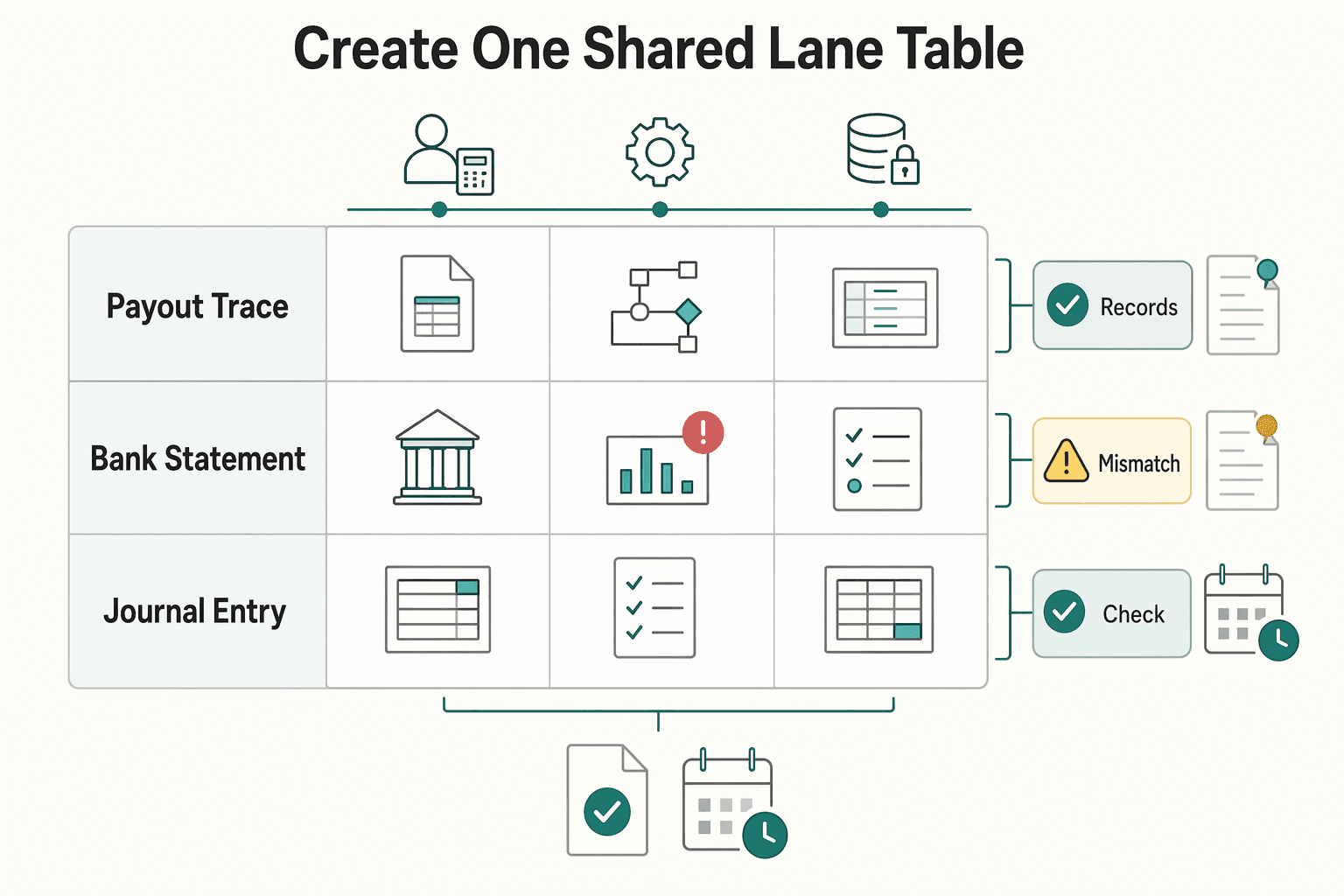

Create one shared lane table#

Create one lane table shared by finance, ops, and ERP owners:

| Lane | Source system | Owner | Cutoff Rules | Exception trigger | Audit Trail artifact |

|---|---|---|---|---|---|

| PSP settlement reconciliation | PSP payout report, payout ID, transaction-level records such as BalanceTransaction | Named PSP data owner | Define in-period activity window and late-arrival handling | Late arrival, missing provider reference, batch/date mismatch, duplicate import | Payout reconciliation report, payout ID trace, batch or unique file identifier, close-checklist note |

| Bank statement matching | Imported bank statements and internal bank-ledger entries | Named banking feed owner | Define statement-availability window and late-arrival handling | Unmatched line, duplicate processing | Statement line, matching decision, close-checklist system or user note |

| Journal entry posting | Match-approved journal import into ERP | Named ERP owner | Post after review and before final period close | Duplicate retry, posting failure | Journal import or posting status record, related system or user notes |

Keep named owners in the working version, and make sure audit artifacts show who acted and when. If you use a Period Close Checklist, pull its system and user notes into your close evidence.

If you are trying to shorten the month-end close, this map is the gate. You need origin, owner, cutoff, exception trigger, and audit evidence for every lane before tool selection.

Related reading: Best invoicing apps with Stripe for freelancers and small teams in 2026.

Automate transaction matching with explicit decision rules#

Start with deterministic matching for repeatable volume, and use suggestive matching as a human-in-the-loop assist for ambiguous items. This helps scale matching while keeping final decisions controlled.

Start with strict exact-match rules#

Set strict exact-match rules first, then expand only where needed. Follow a prioritized rule order, not one broad pass, with tighter keys like transaction number plus amount ahead of looser date-based logic.

Use date-window rules as secondary logic, not your anchor. For example, a rule like matching on amount when date is within 90 Previous Days can help after exact identifiers fail.

Checkpoint: run the rule set on a prior-period sample with both clean items and known exceptions. If a reviewer cannot explain why each auto-match happened, tighten the rule.

Route ambiguity to manual review#

Build ambiguity into the design and send it to manual review on purpose. If the tool finds multiple plausible matches, route the item to a human queue, and document any additional ambiguity conditions in your policy.

That is consistent with how suggestive matching is meant to work: recommendations are accepted or discarded by a person, and multi-match cases require human choice. Treat suggestions as triage support, not final proof.

Document each routing rule in your close controls:

- match keys

- allowed amount or date variance

- what your team classifies as ambiguous in the tool

- queue owner for review

Separate queues by source type#

Separate queues by source type where possible. Source-scoped rule design is supported in practice, for example categories like Payables, Receivables, Payroll, Journals, External, and the same principle applies to close operations.

Keep PSP Settlements and Bank Statements in distinct review queues where possible so owners, evidence checks, and resolution paths stay aligned. Reviewers should be able to filter to one source type and see owner, item age, and required evidence.

Require an audit trail for every outcome#

Require an Audit Trail record for every outcome: auto-match, suggested match accepted, suggested match rejected, and manual override. If the decision is not traceable to source evidence, it is not complete.

For each matched item, capture:

- source evidence ID

- matched internal transaction ID

- rule name or version that produced the result

- timestamp and actor, system or reviewer

- final status and reason for rejection or override when applicable

Final checkpoint: trace one auto-matched item from source evidence through match status to the downstream posting reference. That trace is what makes period-end evidence defensible.

Automate journal entries without losing control#

Once matching rules are stable, the next risk is posting. Automate repeatable journal entries, but gate posting on a status your team can defend, not on month-end pressure.

Define entry templates and a posting gate#

Define journal entry templates by event type with fixed account logic, required source references, and a named exception owner. In your process, release a template to Enterprise Resource Planning (ERP) only after the related approval status is valid. That is a control-design choice, not a universal ERP rule, but it helps keep unsupported items out of the General Ledger.

Keep the posting gate explicit in both workflow logic and close evidence. Oracle guidance places posting after entry, review, and approval, and calls for verifying approved batch status before posting. If your ERP uses status-based actions, treat Approved as the final gate before posting.

Checkpoint: for one sample batch, trace source evidence ID, match group ID, journal template name, approval status, and final posting reference.

Route approvals by materiality and risk#

Route approvals by materiality and risk, not by team habit. Oracle and Dynamics 365 both support amount-based and materiality-based approval routing for journals.

Separate low-risk repeatable entries from unusual ones. A recurring low-value accrual from a validated template may qualify for auto-approval under policy. High-value manual adjustments, first-time template outputs, or cross-ledger corrections should require review before posting.

Document rules in plain language, not only in ERP configuration:

- journal types eligible for auto-approval

- amount or materiality bands that trigger review

- risk flags that force human approval

- approvers, rejectors, and escalation owners

Add failure handling before you trust retries#

Treat posting failures as controlled incidents, not automatic retries. Oracle's Posting Execution report distinguishes successfully posted batches from error batches, and Oracle requires errors to be fixed before resubmission.

First, check whether the General Ledger changed at all. If the posting report shows mixed outcomes, do not blindly rerun the batch. Hold the batch, review the posting report, and use reversal handling where your ERP supports it. SAP, for example, supports reversing all entries tied to a run ID and creating reversal documents.

Checkpoint: for each failed batch, retain the posting report, batch ID, error reason, correction note, and any reversal document IDs before resubmission.

Compare expected versus posted before sign-off#

Before close sign-off, run a completeness check: compare posted journal entries with the transaction groups expected to produce them. This is an operator control, not a universal requirement, and it can surface missing postings, duplicate retries, or orphaned matches.

Run the check by event type and period cutoff, not only as a grand total. Then confirm posting completion with journal reports before period close. If counts do not align, pause sign-off and resolve the gap first.

Build exception monitoring that resolves issues before close day#

Once posting gates are in place, unresolved exceptions can pull close back into manual fire drills. Run exception monitoring as an active control: detect high-impact failures early, route them to named owners, and triage on a steady cadence instead of waiting for close day.

Configure alert classes around the breaks that actually delay close#

Set alert classes around the failure points that delay your payment close. This is a practical operating set, not a universal taxonomy.

Configure notifications for detectable conditions such as delinquency, due date, and status change. For example, trigger alerts when tasks become delinquent, pass key due dates, or move into statuses that can block close. The target is early action, not high alert volume.

Verification point: each alert should include enough context to act immediately. Include source lane, period, item ID or batch ID, current status, age, and next expected action.

Attach escalation paths with owner, SLA, and authority#

Each alert class needs an Escalation Path, not just a mailbox. Define a first owner, an SLA policy for response and resolution targets, and clear decision authority when resolution leaves the original team.

Use time-based escalation so unacted items are reassigned to specified users or roles after a set interval. This keeps exceptions from stalling in personal queues and improves close-status transparency across participating teams.

A simple structure works:

- delinquent exception tasks: an operations owner with authority to request missing evidence or trigger follow-up actions

- stale import or feed exceptions: a treasury or feed-operations owner with authority to run recovery steps or approve a documented fallback

- blocked posting exceptions: a finance operations or controllership owner with authority to correct, reverse, or defer posting with sign-off

A common failure mode is escalation without authority. If the escalated owner cannot approve a workaround or force source-team action, the queue can keep aging.

Run a daily triage and record the decision#

Run one daily exceptions queue and classify material items as fix-now, defer-with-risk-note, or investigate. This three-way split is an operating choice, not a mandate, but it prevents everything from becoming urgent or ignored.

Keep triage notes short and evidence-based: exception ID, close impact, decision path, owner, target time, and missing evidence. For deferred items, record the accepted risk, who accepted it, and what must happen before sign-off. This supports documented, transparent close activity status.

Checkpoint: after triage, you should be able to answer quickly what can still block close, who owns it, and when it escalates next.

Pause new rules if exception volume keeps climbing#

If exception volume rises across cycles, pause new automation-rule changes and fix input quality first. Rising volume can indicate fragmented workflows, inconsistent data, or limited visibility, not only a rule-coverage gap.

Use that pause to inspect data hygiene at the source and correct recurring quality issues before adding more rules. Data quality flaws can compromise decisions, so strengthening observability, audits, and governance on inputs can improve data quality before you layer new rules on top.

You might also find this useful: Usage-Based Billing for Platforms That Holds Up at Month-End Close.

Move from month-end sprint to continuous close#

The real gain can come from shifting work out of the final days. Keep accounts current throughout the month so month-end becomes more confirmation than cleanup.

Set a checkpoint cadence by lane#

Use a cadence your team can sustain in each lane, and tie it to real data arrival and posting windows, not the calendar alone. The goal is continuous monitoring of exceptions and ownership during the period, rather than a period-end catch-up.

At each checkpoint, confirm four things: what is unreconciled, the age of the oldest open item, who owns each material break, and whether anything can still block journal posting or general ledger completion.

Pull cutoff-rules validation forward#

Validate cutoff rules during the month, while there is still time to correct source timing, posting assumptions, or matching logic. Keep unresolved exception review in the same checkpoint so cutoff decisions and exception handling stay connected.

Record each material cutoff decision and exception action with the lane, rule applied, evidence reviewed, close impact, and approver. If an item is carried forward repeatedly without new evidence, treat it as an escalation signal.

Measure progress with fixed checkpoints#

Use the same checkpoints every cycle to measure whether work is actually moving earlier. Track backlog and age at a pre-close point, a near-close point, close day, and post-close review so results are comparable month to month.

Keep one close-level metric alongside backlog: cycle time in calendar days from trial balance to consolidated financial statements. If you use external benchmarks, treat them as historical context. For example, one APQC summary, published March 5, 2018, reported a median of 6.4 calendar days across 2,300 organizations.

Remove ceremony that does not reduce exceptions#

If checkpoint volume rises but unresolved exceptions still pile up near close, simplify. Focus continuous close on the lanes that delay sign-off most, clarify decision rights, and tighten dependency handling before you expand coverage.

Related: Month-End Close for Payment Platforms: A Step-by-Step Checklist for Finance Teams.

What should stay manual for control and compliance#

Do not automate judgment just because you automated timing. Keep manual review for items that can create control risk: unusual journal entries, first-time rule outputs, and exceptions with weak or conflicting source evidence.

Ring-fence unusual journal entries#

Unusual entries should remain high-scrutiny items and are strong candidates for pre-posting review before they hit the General Ledger. PCAOB guidance highlights fraud risk from inappropriate or unauthorized journal entries, including at period end.

Before sign-off, review the unusual or nonstandard entry population and confirm each item has:

- linked source support

- a named preparer or rule owner

- a recorded approver

If an entry comes from a first-time automation rule, apply human validation of both accounting treatment and evidence before treating that rule as trusted in the next cycle.

Keep humans at policy and ambiguity boundaries#

Use manual approval where Approval Gates intersect with ambiguous breaks, and where internal policy or jurisdictional requirements call for escalation on sensitive payouts. Automation can route and prefill, but a person should decide when the issue may involve a policy exception, cutoff judgment, or incomplete source support.

Define human-AI oversight responsibilities in writing: who can override suggested matches, who can approve payout-related exceptions, and what evidence is required when source support is incomplete.

Automate repeatability, not defensibility#

Automate repeatable matching and standard posting patterns. Keep operator review for decisions that determine Audit Trail defensibility.

Use this test: if you cannot clearly explain the decision with attached evidence, do not leave it fully automated. Control gaps in approvals, rule ownership, source support, or exception rationale become compliance risk. For SEC registrants, unresolved material weaknesses mean management cannot conclude ICFR is effective.

Fix the mistakes that usually derail close automation#

After you protect judgment-heavy work, close automation often fails on control design, not accounting theory. Teams get into trouble when they automate in the wrong order, trust the wrong success signal, or leave exception ownership unclear.

Lock cutoff rules before relaunching matching#

When Transaction Matching gets noisy at period end, fix cutoff logic first and relaunch matching second. Locking is part of period close, and accounting period locks are a key control to prevent GL-impacting postings in the wrong period.

Use tolerance limits as guardrails, not as a substitute for clean cutoff logic. A tolerance limit is only the permitted difference between values. Even if you use an example range like -10 to +10, do not copy it across every PSP, bank, and ledger lane.

Checkpoint: review boundary transactions around the period transition and confirm accounting date, source timestamp, settlement reference, and period assignment align with your close policy. If source data lacks enough reference attributes, matching stays ambiguous even with rule tuning.

Add post-write checks after ERP posting#

ERP posting success is not proof of GL correctness. Posting and matching are separate close controls, so you need both.

Add a post-write check whenever an automated journal batch lands. Compare what should post from matching outputs against what the GL actually received, including batch count, total amount, accounting period, and posting status by source group before sign-off.

This helps catch the "accepted but incomplete" failure pattern early, before it turns into a late close surprise.

Assign named owners to every alert path#

Exception monitoring can break down when alerts are unowned. The control point is explicit assignment.

Define a named assignee for each alert class, plus configured due-date expectations and escalation routing. Route unmatched or blocked items to the right handlers and approvers instead of dropping them into one shared queue.

Checkpoint: every open exception should show an assignee, created date, due date, and status. When unresolved, it should also show visible escalation history.

Enforce idempotency before adding retries#

Retries without idempotency create duplicate side effects. Make replay safety mandatory before you expand retry logic.

Attach a replay-safe key to each posting attempt or economic event, and block duplicate writes on replays. Keep key handling explicit, including constraints such as key length, for example up to 255 characters in Stripe. Also document retention behavior, for example possible removal once keys are at least 24 hours old, so duplicate-check windows are intentional.

Test with a forced timeout and replay the same request with the same key. Expected result: one journal effect, not two. Idempotency reduces duplicate risk at the request boundary, but you still need duplicate-entry guards and post-write ledger checks for downstream failures.

For a step-by-step walkthrough, see Accounting Automation for Platforms That Removes Manual Journals and Speeds Close.

Copy and paste month-end close automation checklist#

Use this as a go or no-go check before each close. If any item fails, pause automation expansion in that lane until control, owner, and evidence are clear.

Confirm the prerequisites#

Close automation is higher risk without a current Close Runbook, documented Cutoff Rules, explicit Escalation Paths, and named owners across ERP, PSP, and banking feeds. Validate cutoff by testing boundary transactions around period end and confirming period assignment matches policy. Treat unowned queues for stale imports, unmatched settlements, or blocked journal entries as a stop signal.

Validate the data path#

Trace one full lane from PSP settlements and bank statements through matching to posted general ledger outcomes. A successful import alone is not enough. You should be able to show end-to-end traceability to GL results. If you reconcile Stripe by payout batch, use payout reconciliation only when automatic payouts are enabled, then separately validate cash movement with the Bank reconciliation report.

Validate the controls#

Approval gates must block posting until an authorized reviewer approves the journal or batch. Test idempotency with a forced transient failure: resend the same request with the same key and confirm one accounting effect, not duplicate side effects. Confirm automated actions produce retained audit evidence, including action-level logs and GL-subledger linkage artifacts.

Run the close readiness checkpoint#

Before sign-off, maintain clear visibility on exceptions: assignee, age, status, and escalation state for every open item. Then verify posting integrity by comparing matched groups to posted results across batch counts, total amounts, posting status, and accounting period. Complete a final health check on reconciling differences and period-to-period variances.

Log carry-forward gaps#

Record what failed, what was deferred, and which fixes are needed in rules, source data, or ownership before the next Month-End Close cycle. Track elapsed close time in calendar days, including weekends, reopen events, and repeated exception types so process changes are based on evidence, not memory.

If you are turning this checklist into workflows, use the Gruv docs to map idempotent retries, status tracking, and audit-ready event handling.

Conclusion#

The durable way to shorten month-end close with automation is selective, not total. Automate repeatable matching and journal entry work while keeping approval gates, replay safety, and audit-ready evidence intact.

Automate where rules and evidence are stable#

Automate only where rules are stable and evidence is clear. The highest-value scope is repeatable matching and auto-created entries from clear variances, with exceptions surfaced clearly.

Use one checkpoint for every auto-action: trace source record to match result to posted outcome, and confirm the sign-off identity is captured at approval. If that chain breaks, the speed gain comes with more close risk. Do not automate posting until status is validated. If evidence is weak, conflicting, or new, route it to reviewer judgment.

Build controls into the process#

Design controls into the process, not as post-launch cleanup. Approvals, verifications, and tie-outs still need named ownership, explicit decision logic for unusual items, and documentation that explains what happened and why.

Keep close checklist records, exception logs, reconciliation artifacts, approval records, and posting results together as evidential matter for ICFR support. The target is a faster close with stronger traceability and control quality.

Validate retry safety before unattended execution#

Validate retry safety before you trust unattended execution. Idempotency protects retries from duplicate effects, but only within your practical retry-window design.

If duplicate journal entries are high risk, keep replay-safe references in your posting layer and add a pre-sign-off duplicate check. Do not assume an old idempotency key will always protect delayed retries.

Expand only after one full cycle#

Run one full cycle, then expand only where evidence is strongest. Measure cycle time as elapsed calendar days from initial trial balance run to completed consolidated financial statements, and use external benchmarks only as context, not as universal targets.

Before you expand scope, review:

- exception volume and exception age by lane

- rework incidents and root cause

- control-evidence completeness for auto-actions and approvals

If these hold, extend automation to the next repeatable lane. If not, fix data paths, ownership, or retry logic first. For a practical next cycle review, use this month-end close checklist.

If you want to pressure-test your close design against your payout and compliance requirements, talk to Gruv. ---

Frequently Asked Questions

What should finance teams automate first to shorten month-end close with automation?

Automate data ingest and matching first, not broad unattended posting. Start with imports from subsidiary-ledger and payment-system sources, then apply deterministic rules to high-volume repeatable patterns. Validate one full lane from source record to match result, and pause if cutoff rules are still disputed.

Which tasks should remain manual even after Reconciliation automation?

Keep manual approval for unusual journal entries, first-time rule outputs, and exceptions with weak or conflicting evidence. Journal-entry review remains a control point because inappropriate or unauthorized entries are a known fraud-risk area. If a payout exception changes financial interpretation or policy treatment, send it to a reviewer instead of auto-resolving it.

How is Continuous Close different from a traditional month-end process?

Continuous close shifts work from period-end batching to ongoing activity across the period through automation. Traditional month-end processes concentrate more work at period end, which can create backlog pressure when issues are unresolved. The practical goal is a steadier operating cadence with fewer late-stage surprises.

How do we reduce exceptions without hiding real breaks in PSP Settlements?

Tighten source data quality, cutoff discipline, and matching rules, but keep transaction-level evidence available for investigation. In Stripe, payout reconciliation reporting depends on automatic payouts, which preserve transaction-to-payout linkage. Review failed payouts as active exception signals, and in Adyen use the Settlement details report for transaction-level matching instead of relying only on net totals.

What metrics prove automation is actually improving close performance?

Track cycle time as elapsed calendar days from the initial trial balance run to completed consolidated financial statements. Pair speed metrics with control outcomes so close quality is not judged by speed alone. External benchmarks can provide context, but they are not universal targets.

How do we use AI Suggestive Matches without weakening controls or auditability?

Use AI suggestive matching after deterministic rules, and route low-confidence or tolerance-breaking items to manual review. Define who owns AI-risk decisions, who approves suggested matches, how escalations work, and how monitoring and periodic review are performed. Retain audit records linking each suggestion, reviewer action, and final match outcome.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- airc.nist.gov/airmf-resources/playbook/governtrusted

- docs.stripe.com/payouts/reconciliationtrusted

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- gao.gov/products/gao-25-107721trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-12-implement-contro...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-10-design-control-a...trusted

- nist.gov/itl/ai-risk-management-frameworktrusted

- nist.gov/itl/ai-risk-management-framework/nist-ai-rmf...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: