Quick Answer

Start with Stripe Invoicing if you want the most direct path from invoice to payment, then test Wave and Zoho Invoice only if they improve reconciliation in your real workflow. For the best invoicing apps with stripe, the article’s decision rule is risk-first: choose the setup that makes late payments, failed charges, and dispute follow-up easiest to see and resolve. Validate with a three-invoice trial before rollout.

Best invoicing apps with Stripe for freelancers and small teams in 2026#

The best invoicing apps with Stripe are not the ones with the prettiest templates or the longest feature list. The right choice is the one that makes late payment less likely, cuts time spent chasing status updates, and reduces the chance that you discover too late that a payment failed, was disputed, or got held for review.

That matters more in 2026 because the market is crowded and the rankings do not agree. CNBC published a five-tool invoicing and billing shortlist for small businesses. BigTime compared 15 billing tools in a roundup updated February 27, 2026, and Unibee published a 16-platform roundup on February 2, 2026. GetApp was still refreshing its Stripe-integrated billing and invoicing listings in March 2026. The point is simple: there is no universal winner, only a better fit for your risk profile.

Billing software is supposed to do a few basic jobs well: create invoices, automate billing, and accept online payments. Teams usually get burned not on the promise, but on the handoff. BigTime points out that billing breakdowns can quickly lead to payment delays and overdue balances. For a freelancer, that can make it harder to cover rent or contractor payments on time. For a small team, it can make accounts receivable murkier right when you need clear next actions. Use this guide with a simple lens:

- Cashflow first: Favor tools that make it easier to collect on time, see outstanding balances clearly, and remove avoidable friction at checkout.

- Operational detail over hype: You need a side-by-side shortlist, decision rules, and a pre-send checklist you can actually reuse.

- Failure handling counts: Pay attention to chargeback exposure, payment-review holds, failed payments, and client terms that create collection risk.

If you only send a few bills a month, simplicity still matters, but not at the cost of visibility. In trial, you should be able to confirm what your client sees when they open the payment request, whether bank transfer and card options work the way you expect, and where status changes actually appear. A clean email is not enough if you still need three tools and a spreadsheet to confirm whether money is coming in.

One red flag to keep in mind as you read: sponsored placement and referral-heavy roundups are not proof that a product will reduce risk in your business. GetApp explicitly says it lists providers beyond those that pay it, which is a good reminder to verify behavior yourself. Before you switch, test the boring parts: a live send, a failed-payment path, and what evidence you can pull if a client says they never received or approved the charge.

That thread runs through the rest of this guide. The goal is not to find a number one app. It is to help you choose a Stripe-connected billing setup that keeps accounts receivable cleaner, the payment path clearer, and surprises smaller.

How to pick the right Stripe invoicing app for your risk profile#

Pick for your biggest failure mode, not template polish. This section is for freelancers, creators, and small teams that rely on Stripe for predictable accounts receivable. If you need an ERP rollout or finance architecture first, you are solving a different problem than choosing invoicing software.

Score these four non-negotiables#

| Checkpoint | What to confirm | Grounded detail |

|---|---|---|

| Stripe integration depth | Billing status, payment status, payout visibility, and fee visibility in one workflow | US standard domestic card price is 2.9% + 30¢, with add-ons of 0.5% for manually entered cards, 1.5% for international cards, and 1% for currency conversion |

| Automated reconciliation | Trace one paid invoice to the Stripe payment and then to the payout in your actual export workflow | Red flag: "paid" status with unclear fee lines, exceptions, or payout timing |

| Bank transfer plus card support | Use the payment mix your clients actually use and confirm country-specific pricing | New Zealand pricing shows 2.65% + NZ$0.30 for domestic cards and 3.7% + NZ$0.30 for international cards, with an update noted from 1 May 2026 |

| Dispute and chargeback handling | Test failed cards, delayed payouts, disputes, and what evidence you can pull | Stripe groups payments risk into credit risk, fraud risk, and account takeovers |

- Stripe integration depth

Check whether the app shows billing status, payment status, and payout visibility in one workflow. Check fee visibility too: Stripe's US standard domestic card price is 2.9% + 30¢, with add-ons of 0.5% for manually entered cards, 1.5% for international cards, and 1% for currency conversion. If that trail is hard to see, margin leakage is easy to miss.

- Automated reconciliation

If bookkeeping drag is your main pain, prioritize this over design. Confirm that one paid invoice can be traced cleanly to the Stripe payment and then to the payout in your actual export workflow. A common red flag is "paid" status with unclear fee lines, exceptions, or payout timing.

- Bank transfer plus card payment support

Use the payment mix your clients actually use. Do not assume one global Stripe rate: pricing varies by country and payment context. On Stripe's New Zealand pricing page, domestic cards show 2.65% + NZ$0.30 and international cards show 3.7% + NZ$0.30, with an update noted from 1 May 2026.

- Dispute and chargeback handling

Assume some risk remains and test the ugly path early. Stripe groups payments risk into credit risk, fraud risk, and account takeovers, and says this risk cannot be fully eliminated. Verify what happens on failed cards, delayed payouts, and disputes, including what evidence you can pull.

If late payment is your biggest issue, prioritize reminder automation and cleaner payment UX. If month-end cleanup is the bigger cost, prioritize reconciliation and export quality even if setup takes longer. For related context, see How to Use Stripe Payment Links for Easy Invoicing. If you want a quick next step for "best invoicing apps with stripe," try the free invoice generator.

Quick comparison table of top Stripe-compatible invoicing options#

If you want the fewest unknowns, start with Stripe Invoicing. With Wave and Zoho Invoice plus Zoho Books, the main risk is operational uncertainty that still needs direct vendor confirmation before you rely on them for collections, retries, and month-end close.

| Option | Best for | Setup speed | Stripe-native depth | Automated reconciliation | Tax-document support | Failure visibility, retry behavior, and held or disputed payments | Verification checkpoint in trial | Known limitation |

|---|---|---|---|---|---|---|---|---|

| Stripe Invoicing | Teams already on Stripe that want the shortest billing-to-payment path | Usually fastest if Stripe is already live | Highest confidence in this table because pricing and payment rails are Stripe-native. Stripe publishes country-specific pricing, including 2.9% + 30¢ for US domestic cards and 0.8% ACH Direct Debit with a $5.00 cap | Strongest candidate for direct billing-to-payment matching, but still confirm payout-timing visibility in the views and exports you use | W-8, W-9, and Form 1099 support not established in this section's sources. Confirm collection and export path | Public pricing is transparent; exact retry and dispute handling should still be tested in your account. Confirm what changes when a payment is failed, held, or disputed | Run three tests: one card payment, one bank transfer or ACH path, and one failed payment. Confirm hosted pay-page behavior, guest payment behavior, and whether payout timing is visible without extra reporting work | Confirm international payout-cost detail directly with the provider |

| Wave | Lighter billing needs where you want a simpler tool layer on top of Stripe payments | Likely quick, but confirm in a live setup | Stripe-compatible rather than Stripe-native based on the evidence used here | Test whether one paid bill maps cleanly to Stripe fees and final payout date | Not established here. Ask for the exact W-8, W-9, and 1099 collection or export path | The reviewed public material did not confirm retry logic, dispute screens, or how held payments appear. Get that answer in writing if cash-flow risk matters | Confirm bank transfer availability, whether the pay page is hosted or embedded, and what the client sees after a failed attempt | Confirm pricing and policy detail directly with the provider |

| Zoho Invoice + Zoho Books | Small teams that may need billing plus stronger accounting structure than billing-only tools | Usually more setup because there are more moving parts | Stripe integration depth was not verified here beyond shortlist fit | Main reason to trial it, but prove sync, fee lines, and payout matching in your own ledger | Not established here. Confirm document capture, storage, and Form 1099 reporting path | Failure visibility and retry behavior were not confirmed in the reviewed public material for this section. Ask what happens to billing, payment, and accounting status when a charge fails or is disputed | Run the same three-test set and inspect both the billing layer and books layer for status drift | More surfaces to reconcile means more chances for status mismatch if setup is loose |

The practical split is simple: Stripe gives you the clearest public fee baseline, while third-party tools add a second layer where pricing, retry rules, dispute views, and tax-document handling often need direct confirmation. Stripe also does not publish one universal global rate card. It uses country-specific pricing, and your cost profile can change by market. New Zealand, for example, lists 2.65% + NZ$0.30 for domestic cards and 3.7% + NZ$0.30 for international cards, with new pricing effective 1 May 2026.

In trial, prioritize proof over polish. Ask each vendor to show the exact screen or export where you can trace billing status, payment status, Stripe fee impact, and payout timing. If they cannot show that in a live demo or test account, assume you will rebuild that paper trail yourself when a payment is late or disputed.

If you use Stripe Connect to send payouts to connected accounts, pricing model choice is a real checkpoint. Under "Stripe handles pricing," the platform does not incur additional account, payout-volume, tax-reporting, or per-payout fees. Under "You handle pricing," Stripe lists $2 per monthly active account and 0.25% + 25¢ per payout sent.

That is not the standard solo-freelancer setup, but if you collect on behalf of others, it is a material cost and risk input.

Stripe Invoicing#

If you already run payments in Stripe, Stripe Invoicing is usually the shortest path from invoice creation to payment with minimal integration overhead. It works best when you want faster collections and simpler accounts receivable operations, not deeper ERP-style finance controls.

Stripe says you can create and send invoices in minutes with no code, and customers pay through a Stripe-hosted invoice page. It also frames the product around accounts receivable automation, including automatic reminders, AI-powered dunning, and reconciliation support.

In practical terms, Stripe highlights:

- Card and bank transfer payment options in the invoice flow

- A self-serve portal where customers can view, pay, and manage invoices

- Invoicing in 25+ languages and 135+ currencies

Stripe also reports that 87% of Stripe invoices are paid within 24 hours. Treat that as a Stripe platform statistic, not a guarantee for your specific business.

The core tradeoff is month-end depth. If you need ERP-style reporting, complex revenue controls, or broader finance views across entities, Stripe Invoicing alone may not be enough, and you may still need separate accounting tooling.

Best fit: solo creators and small teams sending recurring client invoices who want billing and payment activity in one Stripe workflow. If you also plan to use Stripe Payment Links, verify that path separately; this source pack supports Stripe-hosted invoice pages but does not establish Payment Links as an invoicing feature.

Related reading: How to Automate Invoicing with Stripe for a Webflow Site.

Wave#

Wave is a practical pick when you want simple invoicing and low setup friction, not deep finance controls. Its value is getting you to a first invoice quickly with a lighter operating load early on.

Wave positions its online payments flow around getting paid faster with minimal setup, lower fees, and faster processing times. That fits freelancers and small service businesses that need a clear billing path more than a complex finance stack.

Where Wave earns a look#

Wave is strongest if you are budget-sensitive and want to keep admin overhead low. If you are still building your process, a lightweight setup can matter more than having every reporting view on day one.

For payment-cost context, use Stripe as a benchmark reference point. Stripe says its standard model has no setup fees, monthly fees, or hidden fees, and its US pricing page lists 2.9% + 30¢ per successful domestic card transaction. Stripe also lists 0.8% for ACH Direct Debit with a $5.00 cap. These are Stripe benchmarks, not Wave fees.

The tradeoff to be honest about#

Keep the scope clear: Wave's speed-and-setup positioning suits straightforward billing, but deep Stripe-native behavior, advanced reporting, and multi-entity controls are worth verifying directly in trial if those are likely pain points for you.

What to verify before you commit#

Test Wave with a real invoice before rollout:

- Send one live bill and confirm the payment path is clear from invoice to paid confirmation.

- Compare your expected costs against Stripe's published benchmarks, especially for card-heavy client mixes.

- Check what records you can export after payment so reconciliation is workable.

- If bank transfer matters to your workflow, verify it directly in your account before committing to Wave.

If you serve multiple regions, validate pricing by country before you set rates. Stripe's New Zealand page, for example, shows 2.65% + NZ$0.30 for domestic cards and notes new pricing effective 1 May 2026, which is a reminder that fee assumptions are market-specific.

Zoho Invoice with Zoho Books#

If you want Stripe-enabled invoicing inside a broader tool network, this is a strong option to test. Zoho Invoice advertises 55+ integrations, and it explicitly says its Stripe integration can collect one-time and recurring payments from multiple countries. That is the core supported value here.

Why it earns a look#

This fits small teams that need simple client-facing invoices but do not want to stay in a single-tool setup forever. Zoho Invoice also lists other payment gateway options, including Zoho Payments and PayPal. On the same integrations page, Zoho says Zoho Payments supports cards and ACH (available upon request), and PayPal supports cards, BNPL, and Venmo.

If you are considering Zoho Books for bookkeeping, Zoho Invoice is a practical front-end candidate to validate with real workflows before rollout.

The tradeoff to respect#

The added flexibility means more setup decisions than Stripe Invoicing alone. The grounding here supports Stripe collection and a broad integrations catalog, but it does not confirm specific Zoho Books sync behavior, reconciliation flows, or month-end outcomes. Do not assume those details; test them directly.

What to verify before rollout#

- Send one one-time invoice and one recurring invoice with Stripe connected, then confirm payment status updates where your team actually works.

- Validate your real country mix. Zoho says Stripe collection works across multiple countries, not every market.

- Keep a small evidence pack after payment (invoice number, customer, date paid, status) so you can compare billing output with your records.

- If you plan to pair with Zoho Books, run a live mini-pilot before migration and check for record clarity after payment.

When to choose Stripe Invoicing versus a third-party app#

Start with Stripe Invoicing when speed, fewer integration points, and predictable fee math are your top priorities; move to a third-party layer only if it clearly reduces your reporting and recordkeeping burden in practice.

| Scenario | Pricing detail | Scope |

|---|---|---|

| US domestic cards | 2.9% + 30¢ | Page example for domestic card payments |

| US ACH Direct Debit | 0.8% with a $5.00 cap | Page example for bank-based payments |

| US international cards add-on | 1.5% | Possible add-on to the base example |

| US currency conversion add-on | 1% | Possible add-on to the base example |

| NZ domestic cards | 2.65% + NZ$0.30 | Page example |

| NZ international cards | 3.7% + NZ$0.30 | Page example |

| NZ currency conversion extra | 2% | Noted effective 1 May 2026 |

| Connect under "You handle pricing" | $2 per monthly active account and 0.25% + 25¢ per payout sent | Include if connected accounts or downstream payouts are part of the workflow |

| Connect under "Stripe handles pricing" | No additional account, payout-volume, tax-reporting, or per-payout fees | Stripe states the platform does not incur these fees under this model |

- Choose Stripe Invoicing first when you want the fastest setup and one place to track invoice status. Stripe's standard model is pay-as-you-go with no setup fees, monthly fees, or hidden fees.

- Choose a third-party app only when you can show that the extra layer improves month-end accuracy and handoffs enough to justify more setup and process overhead.

Before you decide, compare your real payment mix instead of assuming one universal fee:

- US page examples: 2.9% + 30¢ domestic cards, 0.8% ACH Direct Debit with a $5.00 cap, plus possible add-ons like 1.5% for international cards and 1% for currency conversion.

- NZ page examples: 2.65% + NZ$0.30 domestic cards, 3.7% + NZ$0.30 international cards, and 2% extra for currency conversion (noted effective 1 May 2026).

If connected accounts or downstream payouts are part of your workflow, include Connect pricing in the decision. Under "You handle pricing," Stripe lists $2 per monthly active account and 0.25% + 25¢ per payout sent; under "Stripe handles pricing," Stripe states the platform does not incur additional account, payout-volume, tax-reporting, or per-payout fees.

Use a live test before rollout: run 3 invoices (one card payment, one bank transfer, one failed payment) and confirm end-to-end status clarity from sent to paid/failed. If your team cannot quickly see what happened and what to do next from a repeatable workflow, keep the setup simpler.

For a step-by-step walkthrough, see How to use 'Stripe Invoicing' to set up a recurring retainer with a client.

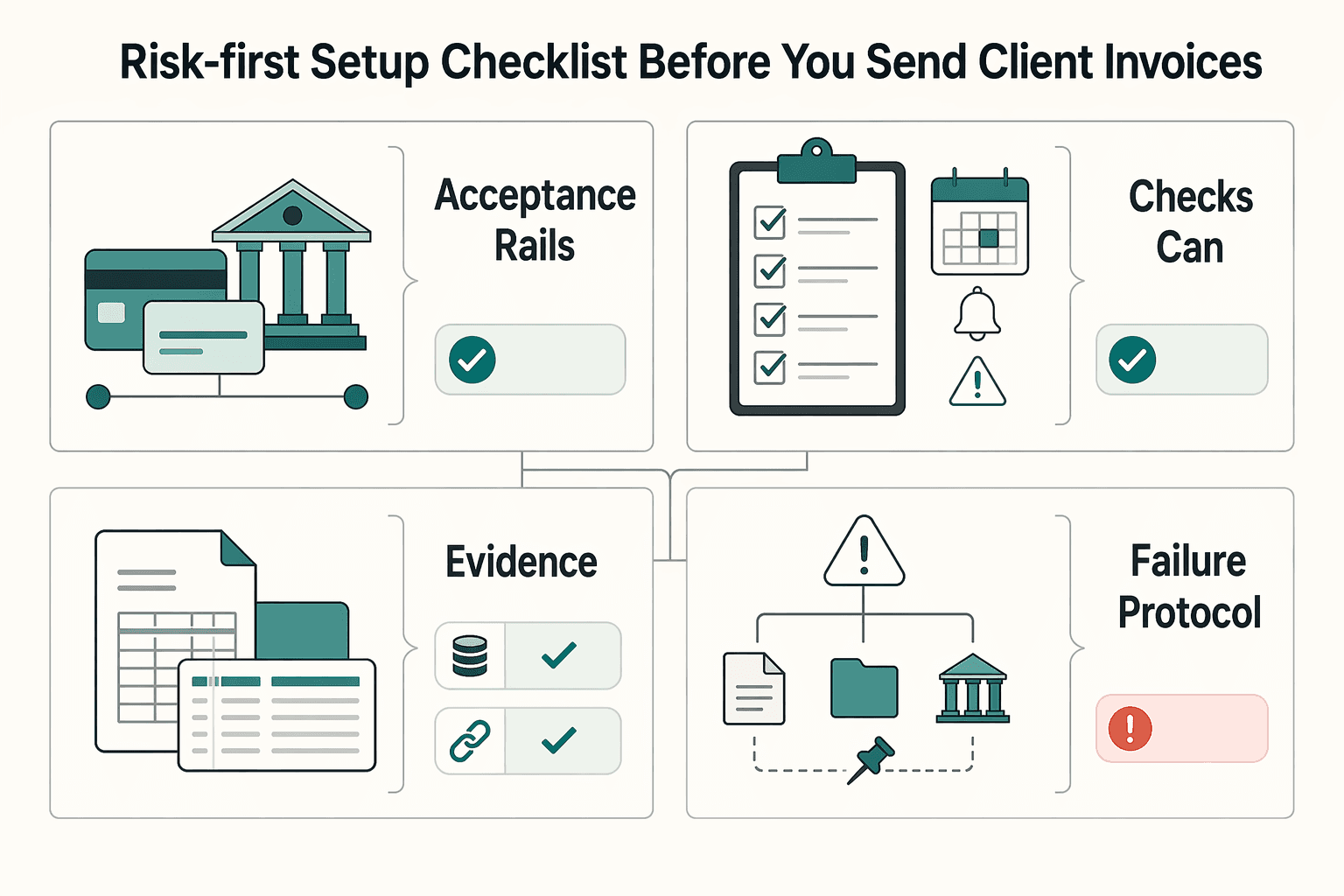

Risk-first setup checklist before you send client invoices#

Even a strong Stripe-connected invoicing setup will not protect cashflow if your terms, records, and exception handling are unclear. Once you choose Stripe Invoicing or a third-party layer, lock these four items before you send a live bill.

| Setup area | What to lock | Go-live check |

|---|---|---|

| Acceptance rails and invoice terms | Choose card payment, bank transfer, or both, then set due date, reminder timing, late-fee policy, and dispute steps | Check one draft invoice and confirm payment method, due date, and contact instructions are visible in one place |

| Checks that can delay or interrupt payment | Identify onboarding or compliance checks that can hold payment and document who owns each step | Run one end-to-end test from invoice sent to payment outcome and note every point where status can stall outside the invoicing screen |

| Tax and records pack | Define your collection path for W-8 or W-9 and your recurring export routine; note TIN validation and possible 1099-NEC, 1099-MISC, or 1042-S reporting | Assign ownership for tracking and export review before volume grows |

| Failure protocol | Define a response path for payment failure, disputes, and payment holds with trigger, owner, client communication step, evidence to save, and escalation timing | Keep named owners so follow-up does not slow down when an exception happens |

- Freeze your acceptance rails and invoice terms

Set your payment rails first: card payment, bank transfer, or both. Then set repeatable terms your team will use every time: due date, reminder timing, late-fee policy, and dispute steps. Stripe says invoices can be created and sent in minutes with no code, so speed is useful, but only after the rules are in place.

Before you go live, check one draft invoice and confirm payment method, due date, and contact instructions are all visible in one place. If your team has to reconstruct terms from old emails during a nonpayment or dispute, the setup is not ready.

- Map checks that can delay or interrupt payment

Identify any onboarding or compliance checks that can hold payment, and document who owns each step. The key is operational clarity: who reviews flags, where records are stored, and how the client is updated if payment timing changes.

Run one end-to-end test from invoice sent to payment outcome and note every point where status can stall outside the invoicing screen. If no single owner is named for follow-up, fix that before volume grows.

- Build the tax and records pack before volume grows

Define your collection path for W-8 or W-9 and your recurring export routine before you scale. For US reporting workflows, TIN validation is a core control, and Routable describes 1099 automation as combining W-9 collection, TIN validation, payment tracking, and IRS filing in one flow.

If your workflow may require 1099-NEC, 1099-MISC, or 1042-S reporting later, collect the required data during onboarding and assign ownership for tracking and export review. Connecting accounting software to Stripe can reduce manual entry, but only if the fields you need are captured cleanly in exports.

- Write a failure protocol with named owners

Define a short response path for payment failure, disputes, and payment holds before they happen. Keep it practical: trigger, owner, client communication step, evidence to save, and escalation timing.

Automation helps only when the exception path is as clear as the normal path. If ownership is shared and unclear, follow-up slows down and risk rises.

Choose for risk reduction, then optimize for convenience#

Choose the tool that reduces your main failure mode first, then optimize for convenience.

- If late payment is the problem, pick the shortest path from invoice to payment.

Focus convenience on the buyer step: make the payment action obvious and status easy to read. If your current setup already sends invoices quickly, avoid switching just for a longer feature list. HubiFi's November 20, 2025 roundup covered 10 Stripe accounting integrations, a useful reminder that more options do not automatically reduce late payment. Use a simple test: send one normal invoice and confirm you can clearly see open, paid, and overdue states. If you cannot tell whether a client ignored the invoice or payment got stuck, convenience is cosmetic.

- If reconciliation drag is the problem, prioritize a single source of truth over invoice polish.

HubiFi warns that when Stripe sales data and financial records live in different systems, you lose a true real-time view. The key check for Stripe Invoicing, Zoho Invoice, or any synced stack is whether sales, fees, and refunds match accurately without manual rebuilds at month end. Validate mapping, not just feature checkboxes. HubiFi is explicit that integration quality depends on active management, including correct data mapping and a consistent reconciliation workflow. Your evidence pack should clearly show the billing record, payment status, fees, refunds, and a usable export.

- If dispute exposure or operational complexity is rising, review on a fixed cadence and upgrade before failures pile up.

Treat cadence as an operating habit, not a formal requirement. As volume grows or multi-currency needs expand, HubiFi's priorities become more important: automated transaction recording, multi-currency support, and scalability. The tradeoff is straightforward: a simpler stack is faster to launch, while a broader stack can reduce cleanup later. Rillion's 2026 invoice capture writeup says work that used to take hours can be done in minutes. If manual entry is creeping back in or exception handling is slowing down, optimize beyond convenience.

Frequently Asked Questions

What is the best invoicing app with Stripe for freelancers?

There is no universal winner. If you want the fewest moving parts, Stripe Invoicing can be a clean place to start. If you need broader bookkeeping structure, compare it against tools like Wave or Zoho Invoice based on your actual failure point, not brand familiarity.

Should I use Stripe Invoicing or an app that integrates with Stripe?

Use Stripe Invoicing first if you want to keep invoicing and payment collection in Stripe. A separate app can make more sense when you need stronger accounting context or other records around the bill, but each added sync is another place for status confusion. One concrete pricing detail matters here: Stripe Invoicing Starter is 0.4% per paid invoice and Plus is 0.5% per paid invoice, and Stripe says that pricing applies to one-time invoices only.

Which Stripe-compatible invoicing tools are best for reducing late payments?

Pick the option that makes the client’s payment step obvious and makes overdue status hard for you to miss. In practice, your trial should answer three things: can the client pay from the billing page without friction, can you see whether it is open or paid in one screen, and do failed or delayed payments show up clearly enough for same day follow-up. If you cannot tell the difference between “client ignored it” and “payment got stuck,” late-payment work will pile up fast.

What features matter most if I invoice international clients with Stripe?

The biggest checkpoint is whether you need true e-invoicing, which Stripe defines as sending or receiving invoices in a standardized, machine-readable electronic format. Stripe says Stripe Billing and Stripe Invoicing do not directly generate or send e-invoices, and that country requirements vary. If local rules require that format, you should review Stripe App Marketplace partner options before you switch.

How should I compare Wave, Zoho Invoice, and Stripe Invoicing if I care about cashflow risk?

Compare them on visibility and evidence, not review averages alone. Capterra’s comparison page last updated March 13th, 2026 showed Zoho Invoice at 4.7 (822) and Wave at 4.4 (1,717), but those numbers do not tell you how either tool exposes failed payments, holds, disputes, or bank transfer status. If cashflow risk is the issue, the better app is the one where you can prove what happened to a bill in minutes.

What should I verify in a trial before switching my invoicing stack?

Send three test bills: one paid normally, one left unpaid, and one that simulates a failure or exception. Then confirm the exact evidence pack you would need later: number, customer name, payment status, payout visibility, and an export you can actually use at month end. Also check a small pricing detail before rollout: Stripe says users are charged for invoicing only when an invoice is paid through Stripe, and Starter no longer includes the old 25 free invoices per month that ended on November 1, 2023.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- cpuc.ca.gov/-/media/cpuc-website/divisions/energy-divisi...trusted

- docs.stripe.com/global-payouts/pricingtrusted

- stripe.com/resources/more/invoice-software-for-small-bu...trusted

- stripe.com/pricingtrusted

- support.stripe.com/questions/stripe-invoicing-pricingtrusted

- support.stripe.com/questions/what-is-e-invoicing-and-how-to-do-ittrusted

- bigtime.net/blogs/billing-softwareexternal

- blog.bloom.io/invoicing-software-for-freelancersexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

How to Use Stripe Payment Links for Easy Invoicing

---

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.