Quick Answer

FTIN validation in platform onboarding means collecting and checking a foreign tax ID only on the onboarding branches where your tax form workflow actually requires it. For most teams, the defensible checks are completeness, country consistency, format, and documented missing-FTIN exceptions, not blind trust or a fake global verification API. If the correct W-8 branch is unclear, hold the record and route it to review before payout activation.

FTIN validation for platform onboarding starts with the right form branch#

FTIN validation is not a universal requirement for every non-U.S. user. It is a branch-specific control that matters only when your onboarding flow actually relies on a foreign tax form, a substitute tax-residency certification, or a withholding workflow that needs the foreign tax ID to be present, explained, or reviewed.

We recommend starting with the official wording in the IRS Instructions for Form W-8BEN, the IRS Instructions for Form W-8BEN-E, and the IRS Instructions for the Requester of Forms W-8. Those three pages tell you more than a generic tax blog can: which line matters, when the FTIN field becomes mandatory, when a missing FTIN can still be acceptable, and when the form becomes invalid for the payer's purposes.

FTIN means a foreign tax identifying number issued by the user's jurisdiction of tax residence. In platform onboarding, the practical question is not "Do we ask every foreign seller, contractor, or creator for an FTIN?" The practical question is "Which form path are we actually using, and what does that path require before the account can move forward?"

Before you change the form#

Map the onboarding branch before you add a field, vendor call, or hard fail. If your product team drops an FTIN field into a global signup form without first mapping the tax form, tax residence, and payout branch behind it, you get a familiar bad outcome: extra friction for low-risk records and weak evidence for the records that actually needed careful review.

At minimum, document these controls before you ship:

- which users go to a U.S. payee branch and which users go to a foreign payee branch

- which branch requests Form W-9 versus Form W-8BEN versus Form W-8BEN-E

- whether your workflow ever relies on the specific W-8 account-holder FTIN rules described in the IRS instructions

- what exact condition allows a missing FTIN to pass review

- which system stores the explanation, evidence, and reviewer decision

If you are redesigning the whole intake flow, pair this article with Contractor Onboarding Best Practices to Reduce Drop-Off and Contractor Onboarding Checklist for KYC, Tax, and Bank Verification. FTIN validation works best when it sits inside one coherent onboarding branch, not when it is bolted onto a generic registration page.

When is an FTIN actually required?#

An FTIN is required only on the branches where the applicable W-8 instructions or your approved treaty workflow make it required. That sounds obvious, but it is the single biggest place platform teams get sloppy because the phrase "foreign tax ID" looks generic while the legal rule is tied to a specific form, line, and use case.

For individuals, the IRS instructions say that a person providing Form W-8BEN as an account holder with respect to a financial account held at a U.S. office of a financial institution and receiving U.S.-source income reportable on Form 1042-S must provide the FTIN on line 6a unless an allowed exception applies. For entities, the parallel operational reference is Form W-8BEN-E line 9b.

That does not mean every platform falls into that exact account-holder context. Many marketplaces, software platforms, and payout programs collect W-8 forms for withholding or reporting readiness without being a U.S. branch of a bank documenting an account holder under the account-holder rule in the W-8 instructions. If that is your model, we recommend treating the bank-specific rule as one branch test, not as a universal requirement for every foreign user.

It also does not mean the FTIN question disappears outside the account-holder branch. The W-8BEN and W-8BEN-E instructions also explain that an FTIN may be furnished for treaty-benefit purposes where the instructions allow it instead of a U.S. TIN. That is why your decision tree must separate the account-holder rule from the treaty-claim rule instead of collapsing them into one checkbox.

| Onboarding branch | When FTIN is normally expected | What to do operationally | Escalate when |

|---|---|---|---|

| Individual on Form W-8BEN in the IRS account-holder context | Usually required on line 6a unless an allowed exception applies | Collect the FTIN or a permitted no-FTIN explanation before approval | The record has no FTIN, no line 6b basis, and no written explanation |

| Entity on Form W-8BEN-E in the IRS account-holder context | Usually required on line 9b unless an allowed exception applies | Collect the FTIN or the line 9c basis and keep the explanation tied to the form | The form branch is right but the FTIN state is unresolved |

| Individual treaty-benefit review outside the account-holder branch | May be relevant where the instructions allow the FTIN to support the treaty claim | Route through a treaty-claim review rule, not a generic signup validator | The reviewer cannot tell whether the claim needs an FTIN, a U.S. TIN, or more treaty detail |

| Entity treaty-benefit review outside the account-holder branch | May be relevant where the entity uses the FTIN instead of a U.S. TIN under the instructions | Keep the treaty claim separate from your account-holder branch logic | The entity type, residence, or claim basis is unclear |

| Domestic or U.S. payee on a W-9 path | No FTIN collection path | Use the U.S. TIN and name workflow instead | The profile mixes W-9 data with a foreign-payee branch |

What the requirement does not mean#

The presence of an FTIN rule in the W-8 instructions does not justify broad product shortcuts. Teams still need to choose the correct payee type, the correct W-8 versus W-9 branch, the correct treaty path when treaty benefits are claimed, and the correct downstream withholding or reporting workflow.

- It does not mean every foreign user must provide an FTIN at signup.

- It does not mean an FTIN alone proves the right form was used.

- It does not mean one "foreign tax ID" field is enough for every country and entity type.

- It does not mean payout should be enabled before the branch and exception logic are clear.

If your team keeps stumbling over entity classification, use W-8BEN-E Entity Type for a UK Limited Company as a reminder that entity paths break long before validation APIs do. If your real problem is downstream reporting readiness, review IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments and IRS Form 1042-S: How Platforms Report U.S.-Source Income for Foreign Contractors before you widen the FTIN rule.

When can you accept a missing FTIN?#

A missing FTIN can be acceptable only when the form instructions allow it and your record keeps the reason. This is where bounded provenance matters most: if you cannot show why the FTIN was not collected, you do not have a defensible exception, you have a blank field.

On Form W-8BEN, line 6b is the explicit no-FTIN mechanism for account holders otherwise required to provide an FTIN on line 6a when they are not legally required to obtain one from their jurisdiction of residence, including where that jurisdiction does not issue TINs. On Form W-8BEN-E, the parallel mechanism is line 9c for the entity account-holder branch.

The IRS also maintains a List of Jurisdictions That Do Not Issue Foreign TINs. That page matters operationally because it gives teams a stable external reference for one narrow class of missing-FTIN cases. It should sit inside your reviewer packet, not inside a teammate's memory.

The requester instructions tighten the rule further. If the FTIN was required and you did not obtain it, and the account holder did not check the applicable no-FTIN box or provide another reasonable explanation, the requester instructions say the form must be treated as invalid for payments of U.S.-source income reportable on Form 1042-S. That is exactly why blank FTIN fields should not slide through a straight-through approval lane.

| Missing-FTIN scenario | What the official materials support | What your platform should retain |

|---|---|---|

| Jurisdiction appears on the IRS no-FTIN list | The IRS list gives a specific basis for not obtaining an FTIN in that narrow case | A snapshot or link to the list entry, the user's tax residence, and the reviewer decision |

| User is not legally required to obtain an FTIN and checks the form box | W-8BEN line 6b or W-8BEN-E line 9c can serve as the explanation in the applicable account-holder context | The exact form version, the checked box, and the profile version reviewed |

| User gives another written explanation | Requester instructions allow another reasonable written explanation on the form, in the margin, or on an attached statement | The statement itself, the reason it was accepted, and the reviewer name |

| FTIN is required but there is no box check and no explanation | The form should not be treated as valid for the applicable 1042-S-reportable payment context | A hold reason, escalation path, and timestamp rather than a silent approval |

| The user is actually on a domestic or U.S. payee path | This is not a missing-FTIN exception at all; it is a wrong-branch issue | A branch-correction action and a request for the right tax form |

Do not invent extra exception codes#

Platforms often overcomplicate this by creating fifteen internal exception labels that never map back to the actual form. That is backwards. We recommend mirroring what the official form and requester instructions already allow before you add internal workflow labels such as "awaiting review" or "needs treaty analysis."

- Keep one code for an allowed form-box explanation.

- Keep one code for an allowed written explanation.

- Keep one code for a wrong-branch record that needs correction.

- Keep one code for unresolved legal or treaty review.

That structure reduces cleanup later because the reviewer can tie the internal code back to the document rule that justified it. If your platform also manages treaty-based withholding decisions, pair this section with US-UK Tax Treaty Contractor Payments and Platform Withholding so teams do not confuse a missing-FTIN issue with a treaty-eligibility issue.

What can you actually validate when an FTIN is present?#

In most platform workflows, you can validate completeness, consistency, and format. You usually cannot prove live issuance from the IRS, and you should not pretend you can. A promotion-ready workflow is honest about that boundary and still records enough evidence to show why the ID was accepted or escalated.

The requester instructions are useful here because they set the right reliance standard. They say you may rely on an FTIN provided on a Form W-8 unless you know or have reason to know it is incorrect. That gives you a practical operating model: run reasonableness checks, collect documentary support when the branch demands it, and escalate contradictions instead of trying to build a fake certainty engine.

Do not confuse that standard with the IRS TIN Matching service. TIN Matching is a pre-filing U.S. service for validating name and TIN combinations before information returns are filed. It is a useful reference for your U.S. TIN branch, but it is not a global FTIN validator for foreign-country tax IDs.

For format checks, a practical reference is the OECD TIN on the Web portal together with the local tax authority guidance for the jurisdiction you are reviewing. Use those sources to check expected structure, labeling, and country fit. Use your case record to prove what you checked and when you checked it.

| Validation layer | What to compare | What counts as a pass | When to escalate |

|---|---|---|---|

| Completeness | FTIN field, issuing country, and form branch | The required field is present or a permitted exception is fully documented | Required fields are blank or the branch is unclear |

| Country fit | Tax residence on the form versus the country that issued the FTIN | The country relationship makes sense for the stated tax residence | The ID country conflicts with the stated residence and no explanation exists |

| Format and structure | Character set, length, separators, and pattern against a country reference | The FTIN resembles the expected local pattern | The format is implausible, truncated, or clearly copied from another country branch |

| Form-path consistency | Individual versus entity path and W-8BEN versus W-8BEN-E usage | The identifier is attached to the correct user type and form | An entity is using an individual branch or the branch contradicts the profile |

| Exception handling | Line 6b or 9c or other written explanation | The reason is present and attached to the same record as the form | The explanation is missing, stale, or stored in a separate system with no link |

| Change control | Whether tax residence, legal name, or form state changed after validation | The validation still matches the live profile | A later change makes the original FTIN review unreliable |

A practical validation stack#

We recommend running cheap, explainable checks first and saving judgment-heavy review for the narrow slice of cases that need it. That order keeps your product fast for clean records without hiding the risky cases inside a pass/fail API response.

- Validate that the user is on the right W-8 or W-9 branch before reading the FTIN field.

- Check whether the FTIN is required, optional, or replaced by an allowed exception on that branch.

- Compare the FTIN structure to a country reference and the tax residence shown on the record.

- Review attached explanations or documentary support when the form relies on a no-FTIN basis.

- Hold, approve, or escalate the record only after the branch, FTIN state, and evidence all line up.

If you are trying to embed these checks into a broader payments workflow, Gruv's Platform Payments Guide and Mass Payouts for Gig Platforms are the adjacent architecture reads. The core point is the same: the best control is the one operations can replay under pressure.

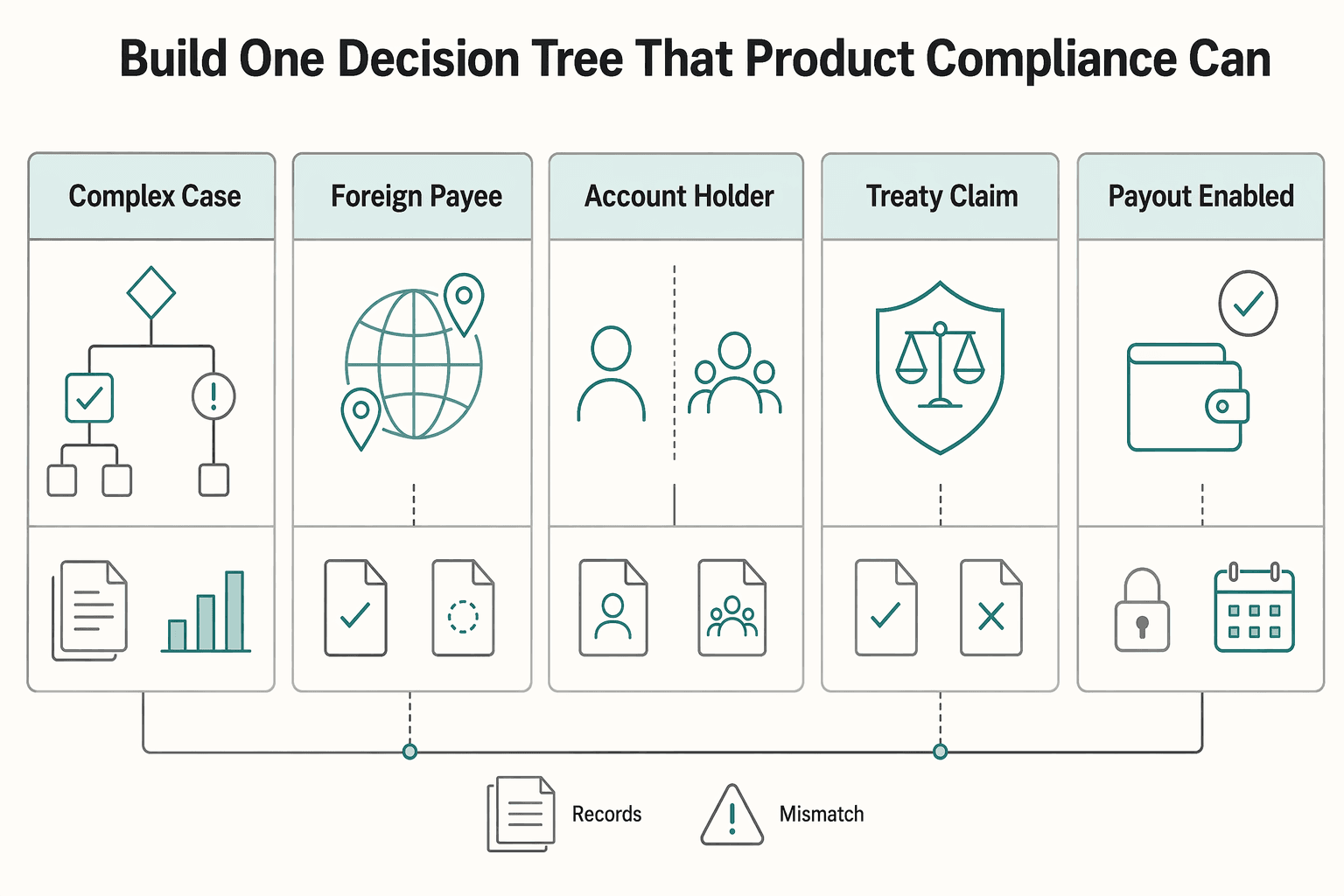

Build one decision tree that product and compliance can both defend#

A usable FTIN workflow needs one decision tree, not five conflicting rules spread across onboarding, support, payouts, and tax ops. The branch logic should drive the UI, the validation sequence, the hold reason, and the evidence packet so every team can tell the same story about the same record.

The core inputs are simple even if the downstream law is not: individual versus entity, U.S. versus foreign payee branch, W-9 versus W-8 path, treaty claim versus no treaty claim, and payout-enabled versus account-only state. Once those inputs are explicit, the FTIN rule becomes much easier to explain because it attaches to a narrow slice of the tree instead of the whole product.

One important safeguard is to keep the account-holder branch separate from your generic foreign-payee branch. If your platform never operates in the account-holder scenario described in the W-8 requester instructions, do not inherit that rule as if it applied to every foreign creator or contractor. Your internal matrix should say exactly when you are using the account-holder rule and when you are not.

| Decision input | Why it matters for FTIN collection | Safe default when unresolved |

|---|---|---|

| Payee type: individual or entity | Determines W-8BEN versus W-8BEN-E and the line number that matters | Stop automation and correct the branch |

| U.S. or foreign payee path | Separates W-9 and U.S. TIN logic from foreign-form logic | Treat as a branch error, not an FTIN exception |

| Account-holder context or not | Controls whether the line 6a or 9b requirement is the operative rule | Route to compliance or tax review |

| Treaty claim or not | Affects whether the FTIN may be used as part of the treaty workflow | Do not auto-approve a treaty claim on guesswork |

| Payout-enabled or account-only state | Tells you whether the unresolved FTIN issue should block money movement | Keep payout disabled until the branch and evidence are clear |

| Exception reason present or absent | Determines whether a missing FTIN is acceptable or not | Escalate to manual review before release |

Route unclear cases before payout activation#

Our default is simple: if the correct branch is unclear, do not enable payouts. That is not because every mismatch is fraudulent. It is because incomplete tax-profile decisions turn into slow, expensive cleanup later when payment volume, withholding deadlines, or reporting cycles compress the time your team has to think.

- Block straight-through approval when the form type and payee type do not line up.

- Block payout release when an FTIN is required but the reason for absence is missing.

- Require a named reviewer when an alternative written explanation is used.

- Recheck the live profile after the reviewer acts so later edits do not silently undo the decision.

This is the same product discipline behind Invisible Payouts: How to Remove Payment Friction Without Losing Contractor Compliance. Money movement should follow a clean tax profile, not lead it.

Change in circumstances should reopen the FTIN review#

The IRS instructions also give you a clean trigger for revalidation: a change in circumstances that makes the form incorrect. For W-8BEN, the instructions tell the form provider to notify the withholding agent or financial institution within 30 days when a change in circumstances makes the information incorrect, and to furnish a new form. The requester instructions also treat change in circumstances as a reason the existing form becomes unreliable.

Operationally, that means your platform should not treat FTIN review as a one-time checkbox. If tax residence, legal name, entity classification, treaty-claim basis, or form type changes after approval, you should reopen the case and rerun the branch decision. The requester instructions also explain that Forms W-8 generally stay valid until the last day of the third succeeding calendar year unless a change in circumstances happens sooner. That is a useful retention and reminder rule, but the earlier trigger is the one that matters for live onboarding quality.

- country of tax residence changes

- legal name or entity type changes

- W-8 path changes to W-9 or vice versa

- a treaty-benefit claim is added, removed, or materially revised

If your compliance team already runs periodic refresh for business identity, align the FTIN recheck with Continuous KYB for Platforms: How to Refresh Business Verification Without Re-Onboarding Everyone. The important point is to keep one governed refresh calendar instead of two competing review loops.

Store evidence that explains why you accepted, held, or escalated the FTIN#

A promotion-ready FTIN workflow is not just a field plus a green check. It is a case record that lets a second reviewer understand what form was used, whether the FTIN was required, what was actually provided, which source or explanation justified the outcome, and when the decision was made.

This is where many teams fail the quality test even after they fix the form. The FTIN itself may be fine, but the evidence is scattered across the product database, support notes, and reviewer memory. That is not a validation process. It is a reconstruction exercise waiting to happen.

We prefer one case packet tied to one user or payee record. That packet should tell the same story to product, payments, tax ops, and compliance. If different teams need different screens, fine. They should still all read from the same underlying decision record.

| Evidence field | Why it matters | What good looks like |

|---|---|---|

| Form type and form version | Explains which FTIN rule you applied | W-8BEN or W-8BEN-E recorded with submission date and version |

| Tax residence and issuing jurisdiction | Lets reviewers test country consistency | Residence country on the form tied to the country used for format review |

| FTIN state | Shows whether the record contains an FTIN or an allowed missing-FTIN reason | Masked FTIN plus a separate indicator for line 6b, line 9c, or attached explanation |

| Source used for the check | Shows how the reviewer judged structure or exception eligibility | Link to the IRS instruction, IRS list, OECD page, or local tax authority guidance used |

| Reviewer and decision timestamp | Makes the outcome traceable and auditable | Named reviewer or system actor plus UTC timestamp |

| Profile version reviewed | Prevents stale approvals after later edits | A record version, event ID, or equivalent change marker tied to the decision |

Keep the explanation attached to the same record#

The requester instructions explicitly allow certain explanations on the form, in the margins, or on a separate attached statement. That sounds like a small procedural detail, but it should shape your data model. Do not accept explanations that live only in chat, in an email inbox, or in a support macro with no stable link back to the form that was reviewed.

A defensible packet should make it easy to answer these questions without another roundtrip:

- Which form branch was used and why?

- Was the FTIN present, absent with an allowed reason, or unresolved?

- What source was consulted to judge the country or format?

- Who accepted or escalated the record?

- Did the live profile change after the validation ran?

If you also care about 1042-S readiness later in the lifecycle, keep the tax-profile packet tied to the downstream reporting record. That way the same reviewer can move from intake evidence to withholding or reporting status without rebuilding context from scratch.

Model the FTIN field so review and revalidation both work#

A promotion-ready FTIN control needs a durable data model, not just a single text box. If product stores only one free-text value called "tax ID," reviewers cannot reliably tell whether they are looking at an FTIN, a U.S. TIN, a local identifier the user typed in the wrong field, or a stale value copied from a prior branch. That ambiguity is how clean intake work turns into manual repair later.

We treat FTIN collection as a small data contract. Capture the branch that asked for the identifier, the country of tax residence, the issuing jurisdiction, the identifier type, the actual FTIN state, and the exception basis when the FTIN is not present. If you ever need to show why the field was optional, that context matters as much as the value itself.

This is also where product and compliance usually need the same answer expressed in different ways. Product wants a stable payload and predictable validation rules. Compliance wants a record that shows what the user entered, what the system checked, and why the case was accepted or held. A good FTIN schema serves both by making the branch and the exception state explicit instead of hiding them in notes.

Separate the identifier from the explanation#

Do not overload the FTIN field to carry both the number and the reason it is missing. The W-8 instructions already distinguish between a provided FTIN and a documented reason for not providing one. Your system should do the same. Otherwise, a reviewer cannot tell whether a string inside the field is an actual foreign tax ID, a support note, or a copied comment from a prior remediation attempt.

A minimal field design usually includes:

- tax form branch, such as W-8BEN, W-8BEN-E, or a substitute form path

- identifier type, so FTIN is not mixed with SSN, EIN, ITIN, or a local registration number

- issuing jurisdiction and tax residence as separate values

- FTIN state, such as present, missing with allowed box, missing with attached explanation, or unresolved

- evidence reference showing which source or reviewer justified the outcome

That structure also makes it easier to build clear user messaging. Instead of telling a user only that the "tax ID is invalid," you can tell them whether the issue is the wrong branch, a required FTIN that is still missing, a format mismatch for the stated country, or an explanation that needs review.

Make changes traceable instead of overwriting history#

FTIN workflows break down when the latest value overwrites the reason the previous value was accepted or rejected. If a user changes tax residence, replaces the FTIN, or uploads a new explanation, you want a traceable history showing which version was reviewed and what changed after that review. Without that history, later approvals look final even when the underlying facts moved.

At minimum, log the old value, new value, actor, timestamp, channel, and case reference when a tax identifier or its explanation changes. That gives your team a way to answer a practical question that comes up constantly in payout and withholding operations: was this the FTIN the reviewer actually approved, or a later edit that should have reopened the case?

If your platform already uses event-based workflow state for payouts or identity checks, wire the FTIN decision into the same event stream. That keeps tax-profile changes visible to the same teams that manage holds, releases, and rechecks, and it reduces the chance that a corrected FTIN quietly bypasses the review path.

This section sounds operational rather than legal because that is exactly the point. The legal rule tells you when an FTIN matters. The data model determines whether your team can still prove what happened three months later when a user edits the profile, a payout is about to release, or a downstream reporting process needs the same tax decision again.

Common FTIN onboarding mistakes and the fastest way to recover#

Most FTIN failures are workflow failures, not obscure tax-law failures. The pattern is usually the same: a team overgeneralizes a real rule, ships a blunt field or hard fail, then spends months cleaning up the records that never should have taken that path.

Asking every foreign user for an FTIN#

This creates friction on the wrong records and weak evidence on the right ones. Recovery is straightforward: pull the field out of the global branch, map the tax forms you actually use, and reintroduce the FTIN request only where your matrix says it belongs.

Treating IRS TIN Matching as a foreign-ID validator#

This is a category error. TIN Matching validates U.S. name and TIN combinations in a pre-filing information-return workflow. Recovery means separating your U.S. TIN branch from your foreign-ID branch and documenting different checks for each.

Accepting a blank FTIN with no documented reason#

A blank field is not the same as an allowed exception. Recovery means rebuilding the queue around three states only: FTIN present, FTIN absent with a supported reason, and FTIN unresolved. Everything else should be a branch error or a review case.

Letting form changes bypass revalidation#

A clean review at onboarding does not survive later data drift by magic. Recovery means wiring change events into the tax-profile workflow so a residence change, entity change, or treaty-claim change automatically reopens the decision.

Storing only the final answer and not the reason#

If your audit trail says only "approved" or "held," your team still has to reconstruct the actual logic later. Recovery means adding the branch, rule basis, source used, and profile version to the decision record so the outcome can be defended without interviewing the original reviewer.

The fastest cleanup sequence is usually:

- freeze the global FTIN rule if it is clearly overbroad

- rebuild the decision tree around W-9, W-8BEN, and W-8BEN-E branches

- backfill allowed missing-FTIN reasons on records that already have support

- reopen payout-ready records that still have unresolved tax-ID state

- add a change-triggered revalidation loop so the same issue does not return next quarter

That repair path is usually cheaper than another broad vendor integration because the main problem is often decision design, not the lack of one more external check.

Use this go-live checklist before you enable payouts#

You are ready to launch only when the branch logic, missing-FTIN handling, validation checks, and case record all tell the same story. If even one of those layers is still fuzzy, the cheaper move is to hold rollout for a short fix now rather than absorb a long tail of manual review later.

- Publish one branch matrix covering W-9, W-8BEN, and W-8BEN-E usage.

- Define exactly where FTIN is required, optional, or replaced by an allowed exception.

- Link each allowed missing-FTIN state to the box check or written explanation that supports it.

- Implement reasonableness checks for country fit, format, and profile consistency.

- Block payout release when the branch, FTIN state, or explanation is unresolved.

- Store the reviewer, source used, and profile version with every manual decision.

- Set revalidation triggers for changes in tax residence, legal name, entity type, or form path.

For the broader onboarding and payout architecture around this control, see Contractor Onboarding Checklist for KYC, Tax, and Bank Verification, Invisible Payouts, and Gruv's Platform Payments Guide. If your team still cannot map the correct W-8 branch with confidence, stop at that point and get tax review before you automate more logic.

Frequently Asked Questions

What does FTIN validation mean in platform onboarding?

It means collecting and checking a foreign tax ID only on the onboarding branches where your tax documentation workflow actually requires it. In practice, most teams validate the right form branch, the stated tax residence, the FTIN field or allowed exception, and the evidence kept with the record.

When should a platform require an FTIN?

Require it only when the applicable W-8 instructions or your approved treaty-benefit workflow call for it. The common operational references are W-8BEN line 6a and W-8BEN-E line 9b for certain account-holder contexts, plus any narrower internal rules your tax team has approved.

Can a platform accept a W-8 with no FTIN?

Sometimes, yes. The platform must retain the allowed box check or another reasonable written explanation and keep the form on the correct branch. If the FTIN is required and there is no permitted explanation, the record should not be auto-approved.

Can IRS TIN Matching validate a foreign tax ID?

No. IRS TIN Matching is a U.S. pre-filing service for validating name and TIN combinations used on information returns. It is not a global FTIN validator.

What should a platform actually check when an FTIN is present?

Check completeness, issuing country versus tax residence, format against a country reference, consistency with the W-8 path, and whether the record changed after the check ran. That is usually more defensible than pretending you can confirm live issuance everywhere.

What should trigger FTIN revalidation after onboarding?

Revalidate when tax residence, legal name, entity classification, form type, treaty-claim status, or the explanation for a missing FTIN changes. Any material change that affects the correctness of the form should reopen the decision.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: