Quick Answer

Start with form routing: for most entity cases you may stay on Form W-8BEN-E, but if facts indicate intermediary or partnership treatment, review Form W-8IMY before choosing an entity type. For a typical UK limited company, many teams select Corporation, yet the article stresses this is a facts-based decision, not a universal rule. Keep FATCA status separate from legal type, document why the path was chosen, and only release payouts after the withholding-agent-facing record matches the approved packet.

How a UK Limited Company Fits on Form W-8BEN-E#

If your team needs a practical answer on W-8BEN-E entity type UK, start with a simple goal: classify UK payees on Form W-8BEN-E using evidence and clear stop points, not habit or guesswork. This guide is for compliance, payments, legal, and finance operators who need a defensible record when a United Kingdom entity is being paid in a U.S. withholding context.

The boundary matters. Form W-8BEN-E is an IRS certificate "used by foreign entities to document their status for purposes of chapter 3 and chapter 4," so this guide stays focused on entity classification for U.S. withholding and reporting purposes. It is not a general guide to UK company law, and it is not a substitute for legal advice where the facts point to a different form path or an exception.

A few points are explicit in the IRS form language and should be treated as hard rules. Form W-8BEN-E is for entities, while individuals must use Form W-8BEN. The form goes to the withholding agent or payer. "Do not send to the IRS." The form also separates basic entity information from "Chapter 4 Status (FATCA status)." That is an early warning that legal form and FATCA classification are different decisions.

Other parts of this topic need more care. In practice, teams often start with a working assumption about how a typical UK limited company may complete Form W-8BEN-E, but that is only a starting point. IRS language does not say that every UK limited company must select one entity type, so this article does not treat a UK registration label as enough on its own. Where the source material is clear, we will say "rule." Where the conclusion depends on additional facts, we will say so and note what evidence should support it.

That distinction keeps your controls defensible. Your first checkpoint should be whether the payee is actually an entity and whether the facts point to a different form path before you move into detailed entity-type or Chapter 4/FATCA choices. For example, the W-8BEN-E form text itself lists foreign partnerships, foreign simple trusts, and foreign grantor trusts among cases that use Form W-8IMY, subject to exceptions. If your intake cannot explain why the entity form is the right form, stop there and record that decision before moving into entity type, FATCA, or treaty review.

The sections that follow stay anchored to the IRS form first, then add the operator judgment needed for typical UK onboarding cases. Where a conclusion depends on facts outside the form itself, you will see the tradeoff and the escalation trigger, not a blanket shortcut.

This pairs well with our guide on How to Get a Foreign TIN Without W-8BEN Filing Mistakes.

At-a-glance comparison for Corporation, Partnership, and Disregarded Entity#

Start with form routing, not the UK label: if the facts point to entity beneficial-owner treatment, keep Form W-8BEN-E in scope; if they point to partnership or intermediary treatment, move to Form W-8IMY review first.

| UK legal setup | Likely W-8 path | Key form parts | Typical FATCA direction | Do not confuse | Evidence required | Escalate when | Payout risk if misclassified |

|---|---|---|---|---|---|---|---|

| Corporation-style fact pattern (payee appears to be a separate entity acting for itself) | Form W-8BEN-E may be the working path if no W-8IMY trigger appears | Part I entity identification/entity type, plus separate Chapter 4 Status (FATCA status) | Review Chapter 4 separately from Part I entity type | Active NFFE is a FATCA classification, not a legal entity type field | Completed W-8BEN-E, confirmation payee is an entity (not an individual), and a short record of why entity beneficial-owner treatment fits | Facts suggest intermediary, partnership, or a different recipient/owner relationship | Withholding-agent rejection, onboarding delay, or incorrect withholding setup |

| Partnership-style fact pattern (pass-through or intermediary indicators) | Form W-8IMY is the flagged path for foreign partnerships (subject to instruction exceptions) | Stop before forcing W-8BEN-E entity type; verify whether facts fall under W-8BEN-E "Do NOT use this form" paths | FATCA review follows correct base-form routing, not the other way around | A Chapter 4 label does not fix the wrong base form; Active NFFE is not a substitute for W-8IMY review | Intake record showing partnership/intermediary indicators and who is acting for whom in the payment chain | Treaty-claim exception questions, mixed facts, or unclear role of the payee | Document rework, withholding-agent pushback, and first-payout delays |

| Disregarded-entity fact pattern (payment name differs from underlying owner name) | Case-specific; W-8BEN-E includes Part I field: "Name of disregarded entity receiving the payment (if applicable, see instructions)" | Part I legal name, disregarded-entity payment-name field, and separate Chapter 4 review | Keep owner identity and FATCA status as separate checks | Active NFFE does not answer who the proper certifying beneficial owner is | Clear file note on who owns the disregarded entity, who signs, and why payment name differs | Owner/certifier mismatch, unclear beneficial owner, or intermediary indicators | Name mismatch at payout, rejection, and manual remediation |

Keep two routing lines from the form explicit in your control notes: "Give this form to the withholding agent or payer. Do not send to the IRS." and "Any person acting as an intermediary ... W-8IMY." Apply those before debating Part I entity-type labels or Chapter 4 labels.

If you want a deeper dive, read W-8BEN-E Explained for Platforms: How to Handle Tax Forms from Foreign Business Entities.

Confirm the form is correct before choosing entity type#

Choose the IRS form first, then choose the entity type. If the form path is wrong, entity-type selection on Form W-8BEN-E will not fix it.

| First gate | What should trigger it | Route first | What to record |

|---|---|---|---|

| Individual check | Payee is a foreign individual, not an entity | Form W-8BEN or, for covered compensation exemption claims, evaluate Form 8233 | Why the payee was treated as an individual and which instruction language drove the routing |

| Intermediary or partnership check | Facts indicate intermediary status, or a foreign partnership / simple trust / grantor trust fact pattern | Form W-8IMY review before collecting a full W-8BEN-E packet | The intermediary or pass-through fact that stopped entity-type review |

| Effectively connected income check | Payee is claiming income is effectively connected with a U.S. trade or business (subject to the treaty-benefit caveat in the instructions) | Form W-8ECI review and legal escalation | Why ECI routing was considered and who approved escalation |

At intake, confirm who the payee is and who is certifying before you move forward. IRS instructions are explicit that Form W-8BEN-E is for entities and individuals must use Form W-8BEN; where compensation is claimed exempt from withholding, Form 8233 should be part of the review (its instructions note a section 1441 30% baseline).

Require a short decision note in the file citing the instruction rationale and the Internal Revenue Code references shown in the IRS instructions. If you cannot clearly explain why the case is W-8BEN-E instead of W-8BEN, W-8IMY, or W-8ECI, pause onboarding.

Apply entity-type decision rules for UK structures#

Set Part I, Line 4 (Type of entity) from documented legal facts, not from a default "UK company" assumption. Use Form W-8BEN-E only after the form-family gate is cleared, then approve the entity type only when the file supports it.

| UK structure signal | Line 4 handling | Verify before approval | Escalate when |

|---|---|---|---|

| UK incorporated entity with no pass-through/intermediary signals | Consider Corporation only if evidence supports it | Incorporation details, legal name match, signer authority, beneficial owner information, and tax IDs tied to the same entity | Ownership or payment facts suggest it acts for another person/entity |

| Pass-through or intermediary indicators in filings/ownership/payment flow | Test Partnership indicators and compare against Form W-8IMY path before accepting W-8BEN-E entity type | Beneficial owner status, whether it acts for others, and whether partnership-interest facts are present | Facts conflict between beneficial-owner and intermediary treatment |

| Disregarded-entity or branch facts appear | Do not finalize from front-page labels | Relationship between operating entity and legal owner, plus IDs for relevant parties | Any uncertainty on who should certify, or whether Part II/GIIN issues are in play |

The IRS instructions flag that Line 4 has been updated, so reviewers should treat this as an active classification control, not a static intake field.

Minimum evidence pack before final entity-type approval#

| Evidence item | Details |

|---|---|

| Incorporation details | For the UK entity |

| Beneficial owner information | Signer authority |

| Tax IDs | Foreign TIN, U.S. TIN (if any), and UK Unique Taxpayer Reference (UTR) where available |

- Incorporation details for the UK entity

- Beneficial owner information and signer authority

- Tax IDs held by the relevant party or parties, such as Foreign TIN, U.S. TIN (if any), and UK Unique Taxpayer Reference (UTR) where available

A practical check is to reconcile those records against the onboarding contract. If entity name, signer, and tax IDs do not align to the same payee logic, stop and re-route.

Partnership/intermediary risk branch#

If partnership indicators appear, treat classification as high risk until reviewed. The IRS W-8BEN-E instructions discuss section 1446(f), including withholding at 10% of amount realized on covered partnership-interest dispositions (unless an exception applies), with applicability references including transfers after January 29, 2021 and certain PTP transfers/distributions on or after January 1, 2023. That does not make every UK entity a partnership case, but it does make shortcut classification unsafe.

Disregarded-entity and branch edge cases#

Where a disregarded entity or branch is involved, require specialist escalation. Part II and GIIN questions may change who should certify, and available guidance does not provide enough rule detail to resolve those cases in routine ops without tax/legal review.

For a step-by-step walkthrough, see How a UK Limited Company Files W-8BEN-E for US Client Payments. If you want a quick next step for "W-8BEN-E entity type UK," try the W-8 form generator.

Keep FATCA status separate from legal entity type#

Treat legal entity type and Chapter 4 (FATCA status) as separate approvals. Do not enable payouts when they point in different directions.

| Decision point | What it answers | What to verify | Hold or escalate when |

|---|---|---|---|

| Legal entity type | What the payee legally is | Incorporation facts, legal name, signer authority, and tax IDs tied to the same entity | "Corporation" was selected by habit, not file evidence |

| Chapter 4 status | How the payee is classified for FATCA purposes | Selected status, internal consistency across the packet, and support from onboarding statements | FATCA answers conflict with the rest of onboarding or look copied from another file |

| GIIN context | Whether a GIIN is referenced in the packet | Exact value shown, entity-name match, and consistency across form and onboarding records | GIIN is missing where referenced, mismatched, or unclear |

A clean Part I answer does not settle Chapter 4. Many trading entities are presented as Active NFFE, but that should be a tested starting point, not a default. If the file cannot support the selected FATCA status, pause and escalate instead of approving on the strength of "Corporation" alone.

What your FATCA evidence pack should include#

| Evidence item | What to review |

|---|---|

| Completed FATCA certification fields on Form W-8BEN-E | Reviewed for consistency |

| Short payee declaration or onboarding statement | Explaining the selected Chapter 4 status |

| Reconciliation | FATCA choice and legal-entity facts describe the same payee |

| GIIN check | Exact match check and an escalation path for exceptions, if a GIIN is included or referenced |

Keep Form 8938 context separate from W-8BEN-E approval logic. IRS materials state that Form 8938 is attached to an annual return, that general reporting context can involve $50,000 or $75,000 thresholds for certain specified domestic entities, and that penalties can apply for failure to report. Use that as background only, not as a threshold test for this entity-type approval decision.

Approve only when legal entity type, Chapter 4 certification, and any GIIN details all align to the same payee with file support.

Validate treaty claims with documentation, not assumptions#

Approve a treaty claim only when the Form W-8BEN-E treaty fields and onboarding record are consistent. For a UK payee asserting the USA-UK Tax Treaty, verify that line 14, claim of tax treaty benefits, and any line 15, special rates and conditions, are complete, specific, and reviewed by the right owners.

| Treaty item | What to verify | Primary owner | Hold and escalate when |

|---|---|---|---|

| Line 14 treaty claim | Treaty country is the United Kingdom, entity name matches onboarding, and the claimant is the same entity named elsewhere in the packet | Tax review, with payments ops checking identity match | Treaty country conflicts with onboarding/incorporation data, or claimant identity is unclear |

| Line 15 special rates and conditions | Any reduced-rate or exemption statement is actually completed in the form or attachment | Tax review | Line 15 is blank, vague, or relies on email/portal notes instead of form support |

| Article 7 (Business Profits) reference | The citation is backed by a written payee or adviser explanation | Legal or tax specialist | Ops is asked to approve eligibility from the article number alone |

| Ownership and Base Erosion Test reference | If invoked, supporting documentation and named sign-off are present | Legal and tax | The test is referenced but no documented reviewer or basis is provided |

Treat Article 7 (Business Profits) as a specialist checkpoint, not an ops shortcut. The grounding here does not provide Article 7 eligibility criteria, so payments ops should require support and route substance review to tax or legal.

Apply the same standard to any Ownership and Base Erosion Test reference. Once that language appears, this is a technical treaty decision: your file should show who signed off, what documentation they relied on, and that the conclusion applies to the same entity named on the W-8BEN-E.

Your treaty evidence pack should include the completed W-8BEN-E with line 14 and any line 15 entries, the payee's treaty support statement or adviser memo, onboarding data for legal name/country/payee type, and an internal approval note naming tax, legal, and payments reviewers. Keep this with the withholding agent or payer record, since the form is provided to the payer and not sent to the IRS.

Set a hard stop if treaty statements conflict with onboarding data. If treaty country, entity identity, or form path does not align, do not activate payouts; hold release and escalate before first payment.

Build platform checkpoints from intake to payout release#

Release payout rails only after tax checks pass in a fixed order. The control objective is simple: keep the onboarding record and the withholding-agent-facing packet consistent from intake through first payout.

Keep the sequence fixed#

Use this order every time: collect tax profile, validate form path, validate entity type, validate Chapter 4 Status (FATCA status) and treaty fields, then release payout access. Later checks do not fix earlier routing errors.

| Checkpoint | What must be true before moving on | Primary owner | Hold and escalate when |

|---|---|---|---|

| Tax profile intake | Legal name, country, payee type, and tax IDs are captured; Foreign TIN and any U.S. Taxpayer Identification Number (TIN) are masked in general ops views | Onboarding ops | Name/country conflicts with onboarding records, or IDs are missing without documented reason |

| Form path validation | Entity cases route to Form W-8BEN-E; individuals route to Form W-8BEN; intermediary or partnership facts route to Form W-8IMY review; effectively connected income claims route to Form W-8ECI review | Payments ops with tax review | Selected form does not match the payee facts |

| Entity type validation | Selected entity type matches collected evidence, including Part I disregarded-entity details when applicable | Tax review | Disregarded-entity details are missing or inconsistent |

| FATCA and treaty validation | Chapter 4 Status (FATCA status) and treaty fields are complete and consistent with onboarding data | Tax or legal | FATCA or treaty entries conflict with entity/country/beneficial-owner details |

| Payout release | Approved tax packet is the same packet used to activate the payee; packet is maintained for the withholding agent or payer | Payments ops | Payee profile changed after approval, or activation data differs from the approved packet |

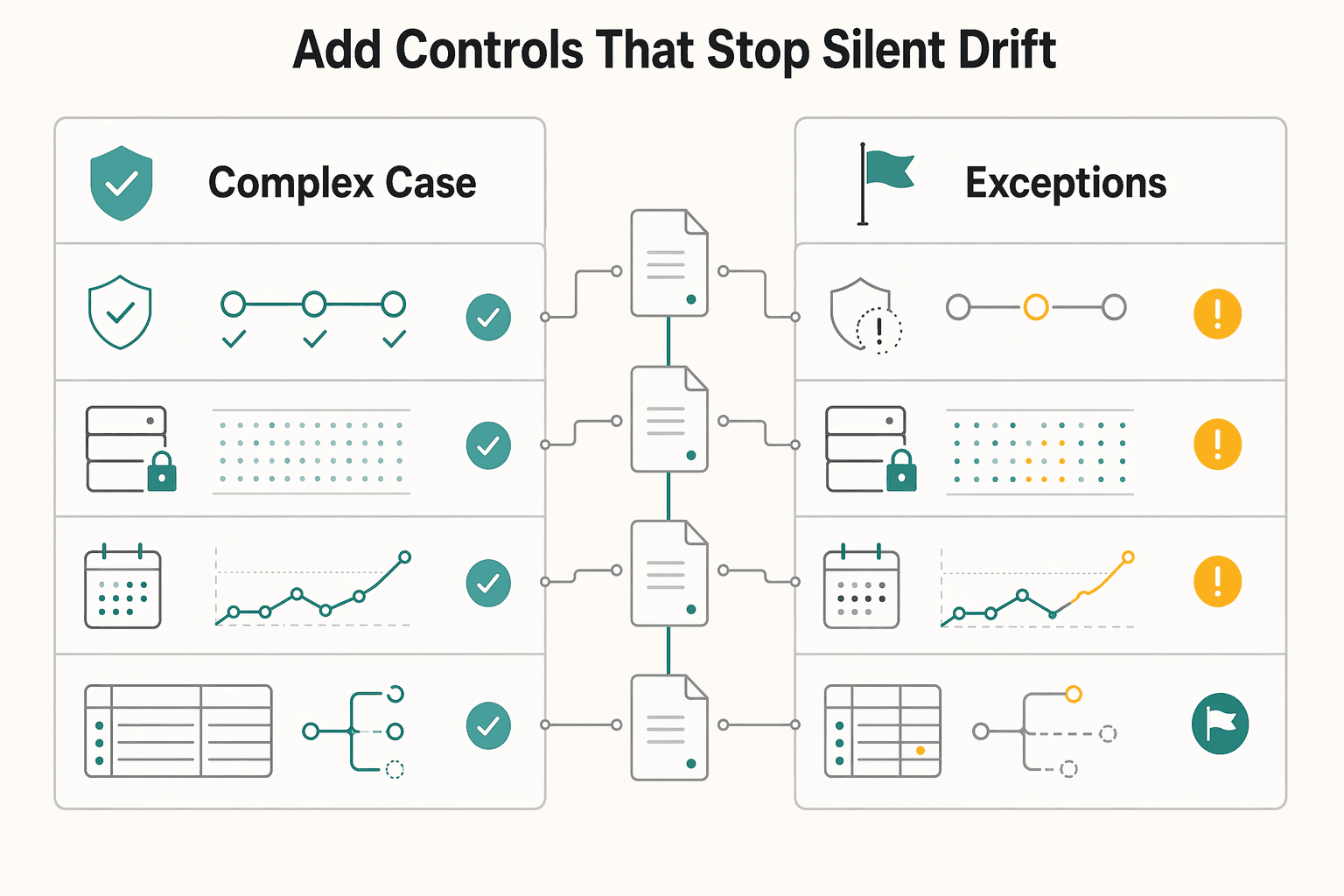

Add controls that stop silent drift#

Use policy gates, an audit trail, masked storage, and idempotent status transitions so retries cannot skip review states or produce duplicate approvals. Re-check withholding-agent-facing fields at first payout execution, not only at onboarding.

| Exception | Who approves | Override artifact / requirement |

|---|---|---|

| Form path or entity-type exception | Tax approves; legal reviews when facts suggest intermediary, partnership, disregarded-entity, or ECI treatment | Written decision note tied to the payee record |

| Treaty exception | Tax or legal approves | Approved W-8BEN-E package plus supporting treaty documentation already required in your process |

| Payout release after mismatch | Payments ops cannot self-override | Fresh approval note that records what changed and who revalidated |

A practical ownership matrix:

- Form path or entity-type exception: tax approves; legal reviews when facts suggest intermediary, partnership, disregarded-entity, or ECI treatment. Override artifact: written decision note tied to the payee record.

- Treaty exception: tax or legal approves. Override artifact: approved W-8BEN-E package plus supporting treaty documentation already required in your process.

- Payout release after mismatch: payments ops cannot self-override. Require a fresh approval note that records what changed and who revalidated.

Enforce one hard stop: no payout release when the approved tax packet and the live payee record do not align on the fields the withholding agent or payer will rely on.

Related: How to Fill Out Form W-8BEN-E for a Foreign Company.

Catch common failure modes before they become withholding incidents#

Most withholding incidents are preventable if you block three errors early: wrong form path, entity type/FATCA mix-ups, and incomplete treaty fields.

| Failure mode | What to verify now | Why it becomes expensive later | Hold and escalate when |

|---|---|---|---|

| Wrong form path | Confirm the payee is an entity before accepting Form W-8BEN-E; individuals must use Form W-8BEN | The withholding packet is invalid from the start, and payout can fail at release | Facts point to an individual, intermediary, foreign partnership/simple trust/grantor trust, or an effectively connected income claim that may require Form W-8IMY or Form W-8ECI |

| Entity type confused with FATCA status | Validate legal entity type separately from Chapter 4 Status (FATCA status) | A record can look complete but still fail withholding-agent review if these answers conflict | The file says "Corporation" but FATCA answers or support do not align |

| Treaty claim not fully supported | Check line 14 and any line 15 entries for completeness and consistency | Gaps usually appear late, after payment setup is already in motion | Treaty fields are partial, contradictory, or inconsistent with the payee packet |

The tradeoff is straightforward: tighter intake checks add friction up front, but they are usually cheaper than payout reversals and manual rework. Do not approve a "mostly complete" packet.

For rapid remediation, use this reset sequence:

- Freeze payout release and snapshot the live payee record the payer would rely on.

- Re-run form selection first; if facts support Form W-8BEN, Form W-8IMY, or Form W-8ECI, stop patching the old packet.

- Request a newly signed replacement form and the missing supporting tax information, including the Foreign TIN field evidence used in your workflow.

- Record a dated decision note, then release only after the corrected packet and live record match exactly.

Conclusion#

The real win here is not a clever one-line answer for a UK company. It is a classification decision you can defend later, backed by evidence, a recorded reviewer judgment, and a clear escalation path when the facts do not line up.

That matters because the failure mode is rarely just a messy form. It can be a withholding process delay, a stale certification that no one noticed, or a record that looked consistent at onboarding but no longer fits after a later ownership or tax-profile change. The IRS instructions for Form W-8BEN-E explicitly call out "When to provide Form W-8BEN-E to the withholding agent," "Change in circumstances," and "Expiration of Form W-8BEN-E." Those are not footnotes. They are lifecycle checkpoints your controls should mirror.

| Checkpoint | What your team is deciding | Evidence to keep in file | Stop and review when |

|---|---|---|---|

| Form selection | Whether Form W-8BEN-E is even the right form path | Signed form, onboarding profile, short decision note | The payee profile suggests a different form path or key facts are unclear |

| Entity type | The legal classification answer on the form | Entity details from onboarding and reviewer rationale | The selected type does not fit the payee facts on its face |

| FATCA status | The FATCA-related status answer, reviewed separately from entity type | Form responses and supporting declarations collected in intake | Entity-type and FATCA answers appear internally inconsistent |

| Ongoing validity | Whether the form can still be relied on | Date tracking, refresh history, change log | Facts changed, certification expired, or a correction was requested |

If you adopt only one operating rule, make it this: separate form selection, entity type, and FATCA status into distinct approval points. Do not let one answer stand in for another, and do not release payouts on a "probably fine" file. A short decision memo is often enough, but it needs to say what was reviewed, what evidence supported the answer, and why no escalation was required.

One useful boundary for teams that handle broader tax questions: Form W-8BEN-E is not the same thing as IRS asset reporting. Form 8938 is used to report specified foreign financial assets and is attached to the taxpayer's annual tax return. It has its own thresholds and penalties. In general, the IRS notes reportability when specified assets exceed $50,000, and warns of a penalty of $10,000 (and up to $50,000 for continued failure), with potential additional penalties including 40 percent on certain underpayments; criminal penalties may also apply. Some taxpayers may also have to file FinCEN Form 114 (FBAR). Keep those regimes separate in training and case handling.

The next step is operational, not theoretical. Build these checkpoints into onboarding controls, require a documented hold for edge cases or contradictory answers, and test those edge cases before you expand payout volume. That is how you make this process reliable.

Related reading: A Deep Dive into Form 5472 for Foreign-Owned US LLCs.

Frequently Asked Questions

What entity type should a UK limited company select on Form W-8BEN-E?

There is no blanket answer supported by the IRS excerpts used for this section, so do not hard-code one choice for every UK limited company. Tie the selection to the entity’s actual legal facts and keep a short decision note in the file showing why that answer was used.

Is Active NFFE the same thing as entity type on Form W-8BEN-E?

Do not treat one field as a substitute for the other when Active NFFE and entity type on Form W-8BEN-E appear in the same record. If a record contains both an entity-type answer and a FATCA-related answer, review them separately and escalate any pairing that does not make sense on its face.

When should a UK business use Form W-8IMY instead of Form W-8BEN-E?

That decision requires careful review, so this is a stop-and-review issue, not a guess-and-proceed issue. If anyone raises W-8IMY during intake, pause the packet, check the current IRS instructions, and document why you stayed on Form W-8BEN-E or moved off it.

When does a Disregarded Entity change how Form W-8BEN-E is completed?

The excerpts here do not provide the completion rules for Disregarded Entity cases. Operationally, treat any mention of disregarded status as a manual review trigger and do not release payout rails until the form path and supporting facts are confirmed.

Is Form W-8BEN-E sent to the IRS or to the withholding agent?

To the withholding agent. The IRS instructions explicitly reference “Giving Form W-8BEN-E to the withholding agent,” which is a useful checkpoint when your ops team is deciding where the signed form belongs and which live payee record the payer will rely on.

What minimum documents should a platform collect before accepting treaty claims?

The source pack for this section does not give a minimum treaty-document checklist, so avoid presenting one as IRS-backed. What you can do with confidence is require a complete, current form, align your intake with the withholding agent’s requirements, and hold any file where the claim looks incomplete or the facts may have changed.

What should we do if entity type and FATCA status appear inconsistent?

Stop the review and do not approve payout release on a "close enough" record. Ask for a corrected or refreshed form, compare it to the live onboarding profile, and note whether the issue is a simple correction or a possible “Change in circumstances.” The IRS instructions for Form W-8BEN-E include sections on both change in circumstances and expiration.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Should Collect and Validate Form W-8BEN-E for Foreign Entities

Treat Form W-8BEN-E collection as a payout control, not a paperwork task. If you are the withholding agent, you generally must obtain valid documentation before payment. Without it, IRS guidance says you generally must withhold 30% from the gross amount paid to a foreign payee.

How to Fill Out Form W-8BEN-E for a Foreign Company

Start here: Form W-8BEN-E is documentation for a foreign entity, not an IRS filing. You send it to the U.S. payer or withholding agent so they can classify the payment and determine whether they may treat your company as a foreign beneficial owner.

How to Invoice a US Client from Mexico as a Temporary Resident

If you want to invoice a US client from Mexico without payment friction, focus on three outcomes: the client's AP team accepts the invoice, your SAT record stays compliant, and your net receipt is predictable.