Quick Answer

Start by matching the field label to the identifier being requested. For how to get a foreign tin, confirm first whether the payer needs an FTIN on Form W-8BEN or a U.S. number such as an ITIN. Use Form W-7 only when an ITIN is required, and keep your submission details plus rejection text together for a clean retry. When FTIN is unavailable, provide one supportable exception basis and get written acceptance before the next payout cycle.

You are here to get the right tax ID the first time#

Start by identifying the exact number the form asks for, then match that request to the right ID type. A common avoidable mistake is treating different tax IDs as interchangeable. If a field label conflicts with what you expected, follow the label first and resolve the mismatch before you submit anything.

TIN is the umbrella term used by the IRS to administer tax laws. It is required on returns, statements, and other tax documents, and it can be required on a withholding certificate for certain claims.

For U.S.-issued IDs, keep this straight:

SSN: issued by the Social Security Administration.- Other U.S. TINs: issued by the IRS.

- If you are not eligible for an SSN, apply for an ITIN with

Form W-7. - ITIN applications can be filed by mail or in person.

Before you submit#

- Read the exact field label and confirm what type of taxpayer number it requests.

- If a U.S. number is required, check SSN eligibility first. If you are not eligible, use the ITIN path with

Form W-7and the return documents listed in that process, such asForm 1040orForm 1040-NR. - Save your first submission details and any rejection message so you can fix an ID-type mismatch first if it gets rejected.

Copy-paste checklist#

- I confirmed the exact field request before entering any number.

- I matched the request to the correct ID type instead of guessing.

- I verified whether a U.S. number was actually required.

- If a U.S. number was required, I checked SSN eligibility before starting ITIN steps.

- I saved the submission and any rejection text for a clean resubmission if needed.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Start with the ID match before you file anything#

Do the ID match first. TIN is an umbrella term, so by itself it does not tell you which subtype belongs in the field.

| ID type | Article says | Use or caution |

|---|---|---|

| TIN | Umbrella term used by the IRS to administer tax laws | By itself, it does not tell you which subtype belongs in the field |

| SSN | Issued by the Social Security Administration | Check SSN eligibility first when a U.S. number is required |

| ITIN | 9-digit IRS number; apply with Form W-7 if not eligible for an SSN | Does not authorize legal work in the U.S. |

| ATIN | Specific to pending U.S. adoptions | Do not enter it unless instructions explicitly make it applicable |

- Classify the field first.

Read the exact field label and payer instructions so you know whether it expects a U.S. taxpayer ID or another identifier.

- Follow the field instructions exactly.

Do not start a U.S. TIN application path unless the form explicitly requires a U.S. number.

- If it asks for a U.S. number, follow IRS subtype rules.

An SSN is issued by the SSA, while other TINs are issued by the IRS. If you are not eligible for an SSN, use Form W-7 to apply for an ITIN, which is a 9-digit IRS number.

- Do not substitute unrelated ID types.

Do not enter ATIN or SSN unless the instructions explicitly make them applicable. ATIN is specific to pending U.S. adoptions, and an ITIN does not authorize legal work in the U.S.

IRS TIN Matching is a pre-filing service for payers or authorized agents on the IRS Payer Account File, not a self-serve tool for individual filers.

Stop and fix before submission if:

- You cannot tell what identifier type the field is asking for.

- You are starting

Form W-7without confirming that a U.S. number is actually required. - You are about to enter

SSNorATINas a placeholder.

Related: Tbilisi, Georgia: The Ultimate Digital Nomad Guide (2026).

Prepare your evidence pack before you contact any authority#

Prepare one evidence pack before you contact anyone. That way your records are ready if questions come up. Keep these record groups in one folder:

| Record | What to keep |

|---|---|

| Identity and foreign-status proof | Current identity and foreign-status proof |

| W-8BEN history | Latest and prior Form W-8BEN submissions, including any rejection text |

| Taxpayer profile | One-page profile with the exact name and ID formatting already used in counterparty and withholding-agent records |

| Usage log | Form on file, submission date, last status, and whether Form 1042-S may be relevant |

Use consistent file naming with date and form type so you can pull the exact version quickly if a payer asks for clarification.

For U.S. ITIN paths, keep document standards in view: supporting documents must prove identity and foreign status, be original documents or certified copies, and be current at submission. If you move to an ITIN application package, keep Form W-7 and a U.S. federal income tax return together in a separate subfolder.

Maintain a one-page usage log for each platform: form on file, submission date, last status, and whether Form 1042-S may be relevant for reporting U.S.-source income and withheld amounts. Review this log before each resubmission to keep profile data and form history aligned.

If your status is cross-border, recently changed, or inconsistent across payers, treat that as an escalation signal and pause before contacting authorities again.

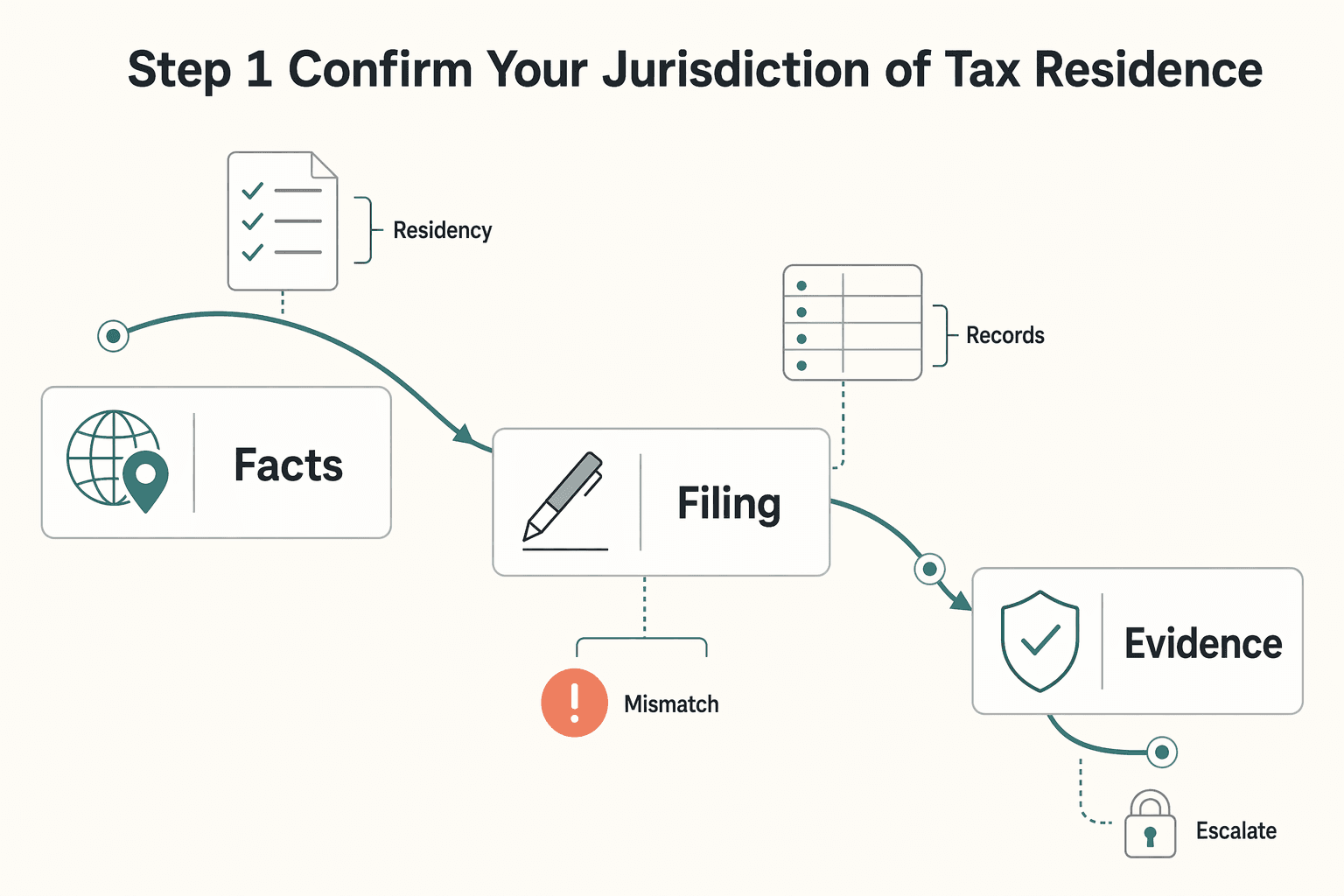

Step 1 confirm your jurisdiction of tax residence#

Pick one working jurisdiction of tax residence for this filing cycle before you complete any FTIN fields. If that jurisdiction is unclear, pause and resolve it first so forms and account records stay aligned.

- Write your working residency position.

State the single country you are treating as your tax residence for this cycle and keep that note with your filing documents.

- Confirm through the official tax authority channel.

Use the authority process first, not third-party summaries. If your path involves U.S. residency certification, the IRS provides that certification on Form 6166, and requesting it requires Form 8802 (mandatory). The IRS also charges a user fee to process Form 8802.

- Keep document types separate.

Treat Form 6166 as a residency certificate only, not a TIN or FTIN, so your identifier fields and residency proof are not mixed.

- Apply the escalation rule before filing.

If your facts support more than one possible residence country, or your profile data conflicts with your evidence, escalate before submitting anything instead of guessing.

If your records mention more than one country, note why one is your active position for this cycle and save that note with the same evidence pack. Before moving on, verify that your jurisdiction note and draft filing fields point to the same country.

Step 2 identify the issuing authority and accepted document path#

Keep the tracks separate. For a foreign TIN or FTIN, start with your tax-residence country's tax authority. Use IRS Form W-7 only if you are applying for a U.S. ITIN.

- Confirm the issuing authority and process for your taxpayer category.

Contact the tax authority in your country of residence and ask for the official process to obtain or confirm your TIN. Ask which office or portal handles your category, since TIN structure and syntax are set by national authorities and can differ by individual category. If you get guidance by phone, write a dated internal note with the contact channel and what you were told. Checkpoint: You have the authority name, submission channel, and a written response or reference number.

- Align accepted documents with your Form W-8 profile fields.

Confirm what identity and status documents they accept, then match those details in your W-8 draft so names, country fields, and TIN formatting stay consistent. If you use an online TIN syntax check, treat it as format-only validation, not identity or existence confirmation. Checkpoint: Your W-8 draft matches authority-facing records exactly.

- Keep a review-ready evidence file.

Save screenshots, receipts, and correspondence as you submit or verify, including dates and reference numbers. This gives you a clear record if a withholding agent flags missing or incorrect TIN details. Checkpoint: You can show who issued the number, what number was provided, and what record supports it.

- Run a contrast check before using Form W-7.

Form W-7 and its instructions are for applying for an ITIN with the IRS, not for obtaining a foreign-issued TIN. The ITIN application can be submitted by mail or in person, and IRS instructions include a U.S. federal return package (Form 1040 or Form 1040-NR). Checkpoint: Your task list names one path only: foreign authority TIN or FTIN, or IRS ITIN.

You might also find this useful: A Freelancer's Guide to Understanding Inflation and Interest Rates.

Step 3 complete W-8BEN fields so they pass review#

At this stage, consistency across Form W-8BEN, your account profile, and your tax records is the main review check. Field-level mismatches across screens can create avoidable follow-up.

If you are still finalizing your FTIN path, use this as a strict alignment pass before submission.

- Copy identity and residence fields exactly.

Use the same legal name format and tax-residence country shown in your account and tax records. Keep spelling, order, and abbreviations consistent. Checkpoint: Legal name and residence country match across your account profile and Form W-8BEN.

- Handle line 6 and line 6b with one clear rule.

Line 6 is for an FTIN when you are otherwise required to provide one. Line 6b is for cases where you are not legally required to obtain an FTIN from your jurisdiction of residence. Checkpoint: Either line 6 includes your FTIN, or line 6b is checked based on that legal condition.

- Reconcile every W-8 data entry point before submitting.

If your payer collects tax data in multiple screens or forms, update each one and run a final consistency check. Checkpoint: The same TIN or FTIN status and tax-residence country appear everywhere your payer stores tax details.

- Save the submitted version for later 1042-S reconciliation.

Keep the exact submitted W-8BEN and any submission confirmation from your payer. You may want that record later because Form 1042-S is used to report income and amounts withheld. Checkpoint: You can produce one record set with the submitted form and proof of submission.

Red flag rule: if you cannot explain in one sentence why line 6 is filled or why line 6b is checked, pause and fix it before filing.

Step 4 handle missing FTIN cases without creating new risk#

Use one clear, supportable exception rationale in your Form W-8BEN package so the withholding agent can review it without conflicting signals.

If you are still working through the FTIN issue, treat this as an exception test, not a workaround. Start by checking the IRS list of jurisdictions that do not issue foreign TINs. Recheck it each filing cycle because the IRS indicates that list can be updated.

An avoidable failure mode is sending one explanation in the form and a different explanation in a support ticket. Keep one position across all records.

- Choose one exception basis and keep it consistent.

Use a single basis that matches your facts: your jurisdiction is on the IRS list because it does not issue a foreign TIN, or it appears in the IRS exception context for restrictions on collecting or disclosing residents' foreign TINs. Checkpoint: Your form entries and explanation use one basis only.

- State that basis directly for the withholding agent.

Include a short note with your Form W-8BEN package that names your tax-residence jurisdiction, your FTIN status, and why the number is missing. Keep it specific and factual so it matches the form. Checkpoint: A reviewer can match your note to your W-8BEN entries without interpretation.

- Keep documentation that supports what you submitted.

Save the exact explanation text you filed, the date you checked the IRS list, and any related platform correspondence in one place. Checkpoint: You can show one record set with your basis, submission, and response history.

- Escalate if the same explanation keeps getting rejected.

If a platform continues to reject the same rationale, stop rewriting variants and consider escalating to a tax professional before resubmitting. Checkpoint: Your next step after repeat rejection is escalation, not another wording change.

Publication 1281 says payers may need to withhold a specified percentage when information returns have missing or incorrect TIN data. It states a 24% rate for subject payments after December 31, 2017. That does not mean backup withholding applies to every missing-FTIN case, but it is a practical reason to document your exception path carefully.

Step 5 submit, verify acceptance, and set a renewal trigger#

After submission, treat this as a control step: confirm acceptance, track what gets reported, and trigger updates when your facts change. Save the acceptance message with the same discipline as the form itself.

| Control | Action | Note |

|---|---|---|

| Acceptance archive | Save the accepted Form W-8BEN version and the acceptance message together | Be able to identify the accepted version, acceptance date, and storage location |

| W-8BEN reminder | Keep a reminder for your Form W-8BEN status | Do not mix it with ITIN renewal logic |

| ITIN renewal | Track renewal separately when relevant | An ITIN expires on December 31 after 3 consecutive tax years of non-use on a federal return and may still be used on information returns when expired |

| Form 1042-S reconciliation | Compare each Form 1042-S against account tax settings and request correction if needed | Keep a short yearly reconciliation note |

| Residency-change review | Trigger a fresh tax-profile review after a move or split-year pattern | Log the date of change, locations involved, and whether you submitted updated tax information |

- Confirm acceptance in writing and archive the exact accepted file.

Save the accepted Form W-8BEN version and the acceptance message together so you can quickly prove what was approved and when. Checkpoint: You can identify the accepted version, acceptance date, and storage location immediately.

- Set renewal reminders without mixing separate rule sets.

Keep a reminder for your Form W-8BEN status, and track ITIN renewal separately when relevant. IRS guidance says an ITIN expires on December 31 after 3 consecutive tax years of non-use on a federal return, must be renewed if it will be included on a federal tax return, and may still be used on information returns when expired. Red flag: Treating ITIN renewal logic as the same thing as W-8BEN timing.

- Reconcile account tax settings against each Form 1042-S issued.

Use Form 1042-S as a reporting check because it reports foreign-person income and amounts withheld. Compare the issued form against your account tax settings and request correction if they do not match. Checkpoint: Keep a short yearly reconciliation note with the form and your comparison record.

- Add a residency-change trigger for a fresh tax-profile review.

Any move or split-year pattern should trigger a review before the next payment cycle. Residency can be fact-based rather than label-based, and California guidance illustrates this: part-year treatment can differ between worldwide income while resident and California-source income while nonresident. Checkpoint: Log the date of change, locations involved, and whether you submitted updated tax information.

If you are still working through tax-profile details, this is where compliant files can break: after acceptance, when records are not updated as facts change.

Common mistakes and how to recover fast#

Fast recovery starts with one move: map the request to the correct ID type before you resubmit anything. Delays often come from mixing an ITIN path with an FTIN request in the same Form W-8 workflow.

IRS terminology is your anchor. TIN is the umbrella category, and ITIN is one TIN subtype. TIN requirements can apply on withholding certificates depending on what the beneficial owner is claiming. If your record mixes ID types, the withholding agent may treat the file as incomplete.

Another practical issue is partial updates: one record gets corrected, but another still carries the old ID label. Review every entry point before you send the next version.

- Label the requested ID type from the requester instructions first.

If the request is for FTIN details on Form W-8BEN, treat it as an FTIN path and keep that label consistent across your file. Checkpoint: Save the request text and add a one-line note: Requested ID type = FTIN or ITIN.

- Keep one form path tied to one number type.

Do not submit a record that signals FTIN in one place and ITIN in another. The requester instructions place responsibilities on the withholding agent to obtain Form W-8 documentation, so consistency matters. Checkpoint: Before resubmitting, verify these items match: ID type label and the number field on Form W-8BEN.

- If FTIN is not legally required, use one documented explanation.

The requester instructions include an FTIN not legally required case. If that applies, submit one clear explanation and keep it with the same form record. Failure mode: Changing the explanation between submissions without a change in facts.

- Escalate with evidence if rejection continues.

If you keep getting rejected after using one consistent ID mapping and explanation, escalate with your evidence set instead of repeatedly rewriting the same file. Checkpoint: Keep the rejection message(s), submitted Form W-8BEN version, and your ID-mapping note together.

When people ask how to get a foreign tin, the practical fix is disciplined remapping. Pick the right ID type, keep one coherent record, and make each resubmission easy to verify. If you need a quick next step, Browse Gruv tools.

Know when to escalate to a tax professional#

After you fix obvious ID-type errors, escalate when the remaining risk is interpretation, not paperwork. If you cannot defend your position clearly across residency, foreign-asset reporting, and withholding records, get professional review before you file again.

- Pause when residency is split across countries.

If you cannot confidently identify one jurisdiction of tax residence for the current filing cycle, escalate before another submission. Checkpoint: Keep a one-page residency memo with move dates, work location, and the country tied to your current TIN or FTIN. If that memo still supports competing answers, escalate.

- Escalate when Form 8938, FATCA, and FBAR may overlap.

Form 8938 is used to report specified foreign financial assets when total value exceeds the applicable threshold, and filing Form 8938 does not replace a separate FBAR filing when FBAR is otherwise required. Use professional review if you are unsure which threshold category applies, because thresholds can vary by situation. Red flag: If you are asking whether one filing covers the other, escalate before submitting either one.

- Escalate when structure choices could change your filing posture.

If your entity setup, contract model, or income characterization changed during the year, do not guess on treatment. If you are uncertain whether this affects your filing treatment, escalate for a written determination.

- Escalate after repeated rejection by a withholding agent.

If a withholding agent keeps rejecting a complete package, the issue may be interpretation rather than missing documents. Repeated rewrites may create inconsistent records and delay payment. Checkpoint: Send one escalation bundle with rejection messages, submitted form copies, and your ID-mapping note. If normal IRS channels have gone nowhere, Taxpayer Advocate Service may be the next escalation path.

Keep compliance operational with Gruv records and controls#

The target is simple: keep visibility before funds move. You want one traceable path from the tax-profile request, to the accepted tax form, to the final Form 1042-S outcome.

- Step 1: Enable protected tax-data collection.

Use Gruv tax-document intake and storage controls with masked and encrypted handling where enabled, especially for tax ID fields. Keep raw identifiers out of chat threads and ticket notes so access and edits stay controlled. Checkpoint: Each profile has a documented audit trail for key lifecycle events and document versioning.

- Step 2: Tie reconciliation artifacts to payment events.

Start reconciliation when payments happen, not at year-end. Form 1042-S is used to report income and amounts withheld described in its instructions, so each payout should be linked to the tax-profile version active at that time, with a short reconciliation note when Form 1042-S is issued. If reported amounts or profile attributes do not match the payment trail, open a correction case immediately. Checkpoint: Every payment record points to the active tax-profile snapshot (for example, W-8/W-8BEN where applicable) and a matching reconciliation note.

- Step 3: Treat IRS updates as control triggers.

Monitor Form 1042-S and its instructions as required review events. The IRS lists a 2026 revision, publishes instructions, and provides an index of prior revisions and updates. Use those changes to review templates, mappings, and country-code references used in reporting. This matters even more if payments include categories called out in Form 1042-S materials, such as specified federal procurement payments to foreign persons subject to section 5000C withholding or effectively connected income distributions from a publicly traded partnership or nominee. Checkpoint: Maintain a dated change log showing when instructions were reviewed and what records were updated.

- Step 4: Apply policy gates before payout when tax data is incomplete.

Catch unresolved tax-profile gaps before funds move where supported. If a required form is missing, profile data conflicts, or reconciliation shows an unresolved mismatch, route the case to manual review instead of paying first and fixing later. Checkpoint: Each blocked payout includes a reason code, owner, and closure evidence in the same case file.

Final takeaway and copy-paste checklist#

Use this as your final pre-submit gate: confirm the number type, keep records consistent, and escalate early when facts are mixed.

- Confirm the requested ID type before entering any number.

If you are using an ITIN, it is a 9-digit IRS number for federal tax purposes only and does not authorize legal U.S. work.

- Use one clear tax-residence position for this filing cycle.

Keep your jurisdiction details consistent across forms and supporting records. If more than one residency position appears plausible, pause and escalate before submitting.

- If Form W-8BEN is requested, keep records consistent and follow written instructions.

Use consistent identity and country details across your submission materials, and keep the submitted version and related confirmation records together.

- Do not guess on FTIN or country-specific details.

If requirements are unclear or instructions conflict, escalate for written guidance before resubmitting.

- Check Form 8938 and FBAR overlap before finalizing.

Form 8938 is attached to your annual return and filed by that return's due date, including extensions, when applicable thresholds are met. Filing Form 8938 does not remove a separate FinCEN Form 114 (FBAR) requirement where FBAR otherwise applies, and thresholds vary by taxpayer situation, with a $50,000 baseline cited for certain U.S. taxpayers. If no income tax return is required for the year, Form 8938 is not required.

- Escalate early when uncertainty remains.

Escalate when residency facts are mixed or Form 8938 and FBAR obligations may overlap. Ask for written guidance and provide a single, organized evidence pack.

Frequently Asked Questions

What is the difference between an FTIN, ITIN, and EIN?

Use TIN as the starting point: it is an identification number used by the IRS to administer tax laws. This grounding pack supports ITIN as an IRS individual tax identification number and confirms U.S. issuer boundaries for SSNs versus other U.S. TINs. It does not provide a complete FTIN versus ITIN versus EIN technical comparison, so treat that distinction as form-specific and jurisdiction-specific.

Who issues a Foreign Taxpayer Identification Number?

This grounding pack does not name one universal foreign issuer for FTINs. Treat issuer identity as a country-specific question tied to your tax residence and filing context. Confirm the issuing authority before submission so your number type matches what the withholding agent expects.

Can I submit Form W-8BEN without an FTIN?

This grounding pack does not provide a universal yes-or-no answer. It does confirm that TIN requirements apply on withholding certificates for certain claims, including some treaty-benefit claims. If your filing depends on those claims, verify requirements before submission instead of assuming a blank field is acceptable.

What should I do if my country does not issue TINs?

This section does not provide country-by-country issuance rules. Use the payer or withholding-agent instructions and keep your explanation consistent across submissions. If instructions remain unclear, pause and confirm requirements before refiling.

When do I need Form W-7 and an ITIN instead of an FTIN?

Use Form W-7 when you are applying for an IRS Individual Taxpayer Identification Number. IRS guidance in this pack states that individuals not eligible for an SSN may apply for an ITIN if they have a valid tax reason. Keep that boundary clear: use the W-7 and ITIN path when your facts require a U.S. ITIN.

Does receiving Form 1042-S mean I owe U.S. tax?

This grounding pack does not state that receiving Form 1042-S by itself means U.S. tax is owed. It does support that Form 1042-S is used to report income and amounts withheld. Treat it as a reporting record and reconcile it with your filings and tax position before drawing conclusions.

Try a related tool

Tomás breaks down Portugal-specific workflows for global professionals—what to do first, what to avoid, and how to keep your move compliant without losing momentum.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

How Inflation and Interest Rates Affect Freelancer Cashflow, Rates, and Payment Terms

**Treat delayed cash collection and payment fees as measurable cost centers, then reduce them with terms, billing cadence, and payment-rail choices.** If you are the CEO of a business-of-one, cash collection is not admin. It is your core system. The real damage often shows up in the gap between delivery and settlement, plus the fees and friction that quietly reduce what you actually keep.