Quick Answer

Use Form W-8BEN-E when a U.S. client is paying your non-U.S. entity, and deliver it to that payer before funds are paid or credited. Complete identity and classification fields using records that already match your legal setup, and make treaty entries only when they are fully supportable. Sign through an authorized person in Part XXX and keep proof of submission. If you skip or misroute the form, default 30% withholding risk can rise.

The CEO's Playbook for Form W-8BEN-E: A Framework for Establishing Credibility and Eliminating Payment Friction#

Start here: Form W-8BEN-E is documentation for a foreign entity, not an IRS filing. You send it to the U.S. payer or withholding agent so they can classify the payment and determine whether they may treat your company as a foreign beneficial owner.

Step 1. Put it in your onboarding packet, not in a "tax later" pile. Keep the W-8BEN-E with your contract, vendor setup details, invoice details, and bank instructions. A valid form helps reduce default 30% withholding risk when foreign-status documentation is missing or unreliable. If the payer asks for the form and you do not provide it, 30% withholding may apply. Backup withholding rules can also become relevant in some cases.

Step 2. Send it before the first payment is paid or credited. Timing matters here. Send it during onboarding, before money moves, and send it to the actual payer or withholding agent. Before you send it, confirm your legal entity name matches your contract and invoice records.

| Workflow point | If you submit a complete form early | If you submit late or incomplete |

|---|---|---|

| Documentation status | Payer has Form W-8BEN-E before income is paid or credited | Payer may not be able to treat the payee as a documented foreign beneficial owner yet |

| Compliance risk signal to payer | Supports documented withholding classification | Missing documentation can trigger default 30% withholding treatment |

Step 3. Keep records and monitor for changes. A W-8BEN-E is generally valid from the signature date through the last day of the third succeeding calendar year, unless your circumstances change earlier. Retain the signed form, proof of delivery, such as an email or portal confirmation, and the exact version you sent. Bring in a tax advisor if the facts are not standard, especially around entity classification, treaty claims, or form selection.

Operator checklist

- Send it with onboarding, before income is paid or credited.

- Send it to the U.S. payer or withholding agent, not the IRS.

- Retain the signed form, proof of delivery, and related contract and invoice records.

- Escalate if ownership, entity type, treaty position, or other core facts are unclear or unusual.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

W-8BEN vs. W-8BEN-E: The One-Minute Decision#

Use a simple two-step screen: first confirm whether W-8BEN-E applies under current IRS eligibility checkpoints, then make sure your onboarding records tell the same story.

Ask one question first#

Is the U.S. payer paying a foreign entity, or paying you as an individual? If payment is going to a foreign entity, W-8BEN-E may be the right form, but confirm that against current IRS instructions. The IRS instructions frame W-8BEN-E as an entity certificate for U.S. withholding and reporting, and they include both Who Must Provide Form W-8BEN-E and Do not use Form W-8BEN-E checkpoints.

If payment is going to you personally, do not default to the entity form. Confirm the applicable form in current IRS instructions and your payer onboarding packet.

Run a mismatch check before you submit#

Before you choose the form, compare the named payee across:

- Your U.S. contract or SOW

- Your invoice

- Your payout profile or receiving account details

If those records do not point to the same legal identity, stop and resolve that first. Inaccurate legal identity details can cause processing delays or errors.

Quick comparison#

| Decision field | W-8BEN | W-8BEN-E |

|---|---|---|

| What this section can confirm | Not established here; verify in current IRS instructions and payer onboarding packet | Entity certificate for U.S. withholding and reporting |

| Eligibility check | Verify in current IRS instructions and payer onboarding packet | Use the IRS Who Must Provide Form W-8BEN-E and Do not use Form W-8BEN-E checkpoints |

| Submission timing/recipient | Verify in current IRS instructions and payer onboarding packet | Follow IRS guidance on when to provide it to the withholding agent |

| Possible pause trigger | Identity mismatches across onboarding records can delay processing | IRS Do not use Form W-8BEN-E ineligibility path, plus identity mismatches |

Edge-case guardrail (single-owner/pass-through structures)#

If your legal form and tax classification do not clearly align, pause before you file. The W-8BEN-E instructions explicitly flag Disregarded entity, which is your cue to confirm treatment with an advisor when the structure is not straightforward.

Fast self-check scenarios#

| Records status | Next step |

|---|---|

| Contract, invoice, and payout details all show you personally | Verify the applicable form in current instructions before filing |

| Contract, invoice, and payout details all show the same foreign entity | Verify W-8BEN-E eligibility in current instructions before filing |

| Contract, invoice, and payout details show different names | Fix the records or get advisor confirmation before submitting either form |

Related: Tbilisi, Georgia: The Ultimate Digital Nomad Guide (2025).

Your 10-Minute Playbook: Completing Form W-8BEN-E with CEO Confidence#

Your goal is simple: give the payer a W-8BEN-E they can rely on without follow-up. That means clean identity fields, the right Chapter 3 and Chapter 4 statuses, supportable treaty details when claimed, and an authorized signer.

Start with the current form and reconcile your records#

Start with the current IRS form, then reconcile your records before you enter anything. The IRS page last reviewed on 23-Jan-2026 points to Form W-8BEN-E (Rev. October 2021). Use this form for entities; individuals use Form W-8BEN.

Give the form to the payer or withholding agent before income is paid or credited, not to the IRS. If it is requested and not provided, withholding can apply at 30% (or backup withholding in some cases).

Use one consistent legal identity across your contract payee, invoice, payout profile, formation record, and tax registration record. If those do not match, fix that first.

Complete Part I with matching legal identity details#

Part I is where avoidable errors start, so treat it as a legal identity and classification check.

| Field | What to enter | How to validate before sending | Common issue to avoid |

|---|---|---|---|

| Legal identity details | Entity information that matches your official records | Match against contract, invoice, payout profile, and entity records | Mismatched names or records across documents |

| Chapter 3 Status (line 4) | One entity-type box only | Confirm it matches your actual legal or tax classification | Multiple boxes or a classification that conflicts with records |

| Chapter 4 Status (line 5) | FATCA status that applies to your entity | Confirm status and complete the related certification section as required | Picking a status you cannot support |

| U.S. TIN / foreign TIN / line 9c | Enter available TINs; use line 9c only if FTIN is not legally required | Validate against tax registration records | Missing or incorrect identification support when making a treaty claim |

Decision cues:

- A missing U.S. TIN does not automatically block treaty relief. IRS treaty guidance allows U.S. or foreign TIN support.

- If your entity classification is unclear, for example corporation vs partnership vs disregarded or hybrid treatment, stop and confirm before filing.

Use Part III only for supportable treaty claims#

Use Part III only when you can complete the treaty claim all the way through. Line 15 requires the treaty article, paragraph, and claimed withholding rate details.

For line 14a, enter the treaty-residence country. For line 15, verify the article, rate, and related treaty details using IRS tax treaty tables.

| Treaty claim state | What it looks like | Expected payment handling | Follow-up burden |

|---|---|---|---|

| Complete claim | Treaty country, article, paragraph, rate, and TIN support are present | Withholding agent may be able to apply reduced or exempt treatment if accepted | Lower |

| Incomplete claim | Missing or vague article, paragraph, rate, or TIN support | Withholding may default to standard rates until resolved | Higher |

If you cannot verify the article and rate from IRS tables, do not force a weak treaty claim.

Sign Part XXX only with an authorized signer#

Only sign Part XXX if the signer is authorized and the form is accurate. The certification is under penalties of perjury. The signer also agrees to provide a new form within 30 days if a change in circumstances makes the current form incorrect.

Run a final pre-send check#

Before you send it, run this quick check:

| Check | What to confirm |

|---|---|

| Identity alignment | Confirm legal name, country details, treaty residence if claimed, contract payee, invoice, and payout profile all align |

| Status selection | Re-check Chapter 3 and Chapter 4 selections against your actual entity status |

| TIN entries | Verify TIN entries and whether line 9c is being used correctly |

| Treaty claim | If claiming treaty benefits, confirm the treaty article, paragraph, and rate from IRS treaty tables |

| Signer authority | Confirm signer authority and readiness to reissue within 30 days after a relevant change |

| Escalation | Stop and escalate to a qualified tax advisor if you are unsure about entity classification, FATCA status, hybrid treatment, or treaty eligibility |

For related foreign tax credit guidance, see How to Fill Out Form 1116 (Foreign Tax Credit).

Before you send the form to a client, create a clean draft you can verify line by line with the W-8 Form Generator.

The Three Hidden Risks in Form W-8BEN-E (And How to Avoid Them)#

W-8BEN-E issues usually come from three operational misses: a classification mismatch, a weak treaty claim on line 14, or a form that enters the wrong client process and stalls.

Catch classification mismatches before review#

The first risk is a classification mismatch. If your Chapter 3 or Chapter 4 selections do not match your legal records, expect follow-up questions and delays.

Fix this before sending: reconcile the legal name, country of organization, Chapter 3 status, Chapter 4 status, and tax IDs across your entity records and onboarding details. If you use line 9c, use it only when an FTIN is not legally required to be obtained.

Do not pick a status first and make the rest of the form fit it. If your entity treatment is unclear, stop and get advisor review before submission.

Make treaty claims only when you can support them#

The second risk is an unsupported treaty claim, and it starts at line 14.

Before you send it, verify your treaty basis against IRS treaty materials. If your treaty does not contain a limitation on benefits article, handle line 14 accordingly instead of assuming it follows the same pattern as other treaties. If you cannot support the claim cleanly, remove it and escalate before resubmitting.

Send the form through the right client path#

The third risk is routing: the form reaches the wrong team and sits. You need a clear owner and intake path in the client process.

Ask one onboarding question early: who owns non-U.S. tax-form review, and what submission path should you use? If ownership is unclear or the form is bouncing between teams, pause and resolve routing before submission.

| Risk | Early warning sign | Pre-send check | Escalate when |

|---|---|---|---|

| FATCA or classification mismatch | Clarification request on entity tax status | Reconcile legal name, country of organization, Chapter 3 or 4 status, and line 9c use to records | Entity classification is unclear or records conflict |

| Weak treaty claim (line 14) | Follow-up asks for treaty basis or missing detail | Verify treaty basis for line 14 from IRS treaty materials | You cannot support the claim cleanly |

| Wrong delivery path | No clear owner, delayed confirmation, or internal forwarding | Confirm tax-form review owner and submission path | Client cannot confirm intake ownership |

| Withholding detail needs legal validation | Compliance flags partnership-interest transfer withholding | For certain section 1446(f) transfers, verify whether withholding applies, including the 10% amount-realized rule unless an exception applies | Section 1446(f) or related transfer issues appear |

Use these defaults:

- Match classification to records first. If unclear, stop and escalate.

- Use line 14 only when the treaty claim is fully supportable.

- Confirm the tax-form review owner and intake route before sending.

- If section 1446(f) or partnership-interest transfer issues appear, pause and get advisor review before submission.

Related: How to Fill Out Form W-8BEN for a Foreign Freelancer.

Beyond the Form: Integrating the W-8BEN-E into Your Onboarding System#

Treat W-8BEN-E as a repeatable onboarding control, not a one-time form. The goal is straightforward: send the entity certificate to the payer or withholding agent before the first payment, confirm receipt, and keep a clear update trail when facts change.

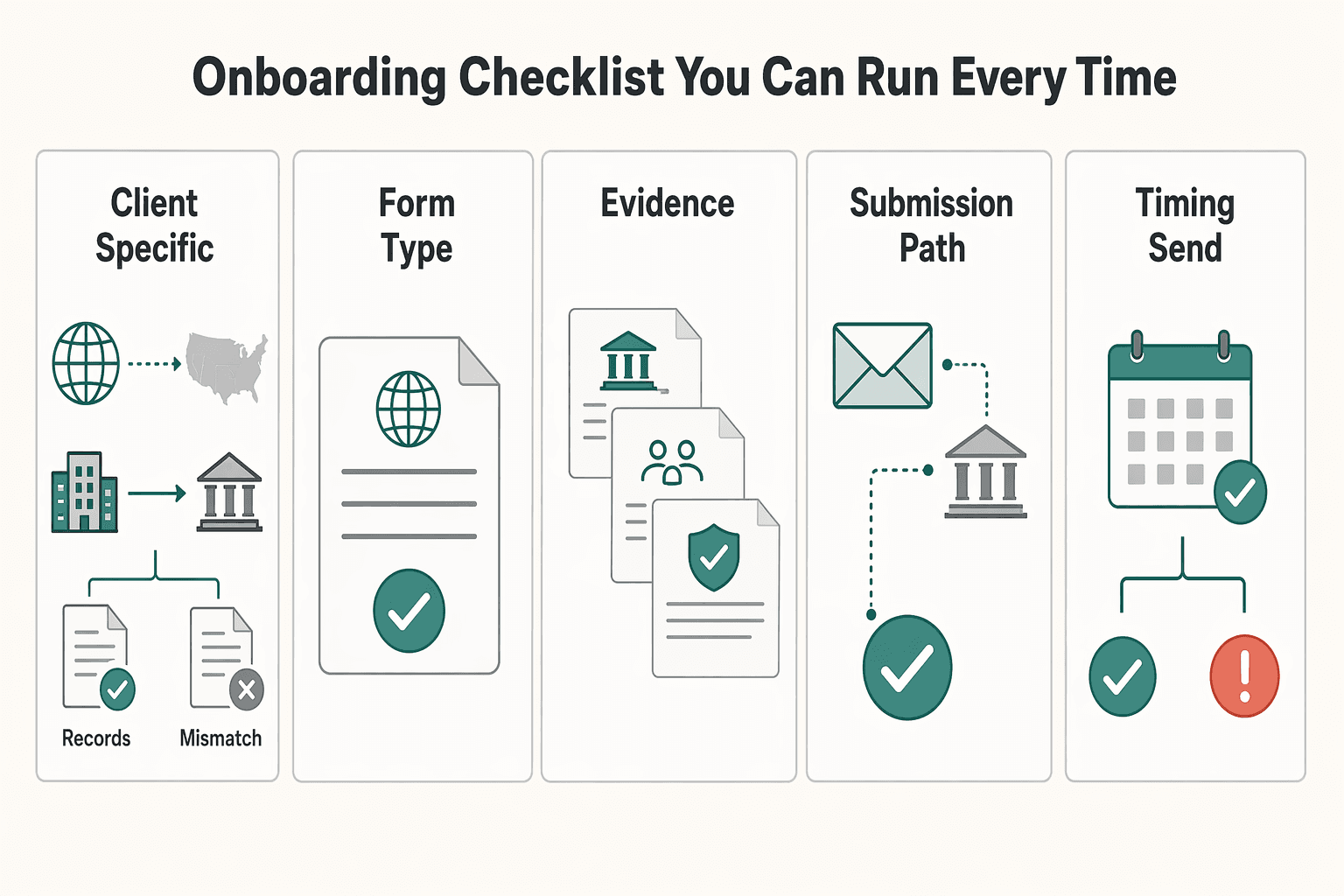

Onboarding checklist you can run every time#

| Step | Action |

|---|---|

| Client-specific packet | Send a client-specific packet. Separate withholding agents generally require separate forms. |

| Form type | Use W-8BEN-E only for entities. Individuals use W-8BEN. |

| Included documents | Include the signed W-8BEN-E and any client-requested onboarding documents. |

| Submission path | Send it through the payer or withholding-agent path the client names. Do not send it to the IRS. |

| Timing | Send it at onboarding start, or at the latest before the first payout is scheduled. |

| Receipt confirmation | Ask for written confirmation of receipt and who owns withholding or tax-form review. |

| Client record | Log the submission date, recipient, and confirmation status in your client record. |

| Follow-up | Follow up before payout if confirmation is missing. |

| Client-side role | What to send first | Why this handoff matters |

|---|---|---|

| Procurement / vendor onboarding | Core vendor packet + signed W-8BEN-E | Helps route documentation into the payer-side withholding workflow |

| Accounts payable | Approved W-8BEN-E + payment setup details | Payment timing and withholding timing are linked, so clear records matter before disbursement |

| Legal / tax reviewer | Signed W-8BEN-E + treaty-claim support, if a treaty claim is made | Supports classification and treaty-position review when claims or conflicts need validation |

Validity and renewal control#

Track validity in your client record and run two controls:

- Set a pre-expiry reminder.

- Assign a resend task to the client contact who confirmed receipt last time.

Keep prior versions and log replacement dates instead of overwriting history. As a baseline, the default validity period runs through the last day of the third succeeding calendar year unless a change in circumstances makes the form incorrect earlier. If facts change, notify the withholding agent within 30 days and update the form workflow.

Client hub mini-SOP (storage and retrieval)#

Good storage makes repeat requests easier. Use a consistent internal template, for example:

- Client legal name

- Your entity legal name

- Signed date

- Submission date

- Recipient name or email

- Classification summary

- Treaty-claim flag and article reference, if used

- Receipt confirmation status

- Validity rule in use

- Reminder date

- Current file version

Use clear versioning, such as dated filenames and a superseded note on older files. That makes it easier to retrieve the exact submitted version quickly for client re-requests or accountant review.

Escalate to a tax advisor now if#

- Your entity classification changed or form fit is now unclear.

- Your treaty position changed, including residency basis or the treaty article relied on.

- Client tax records conflict with your known facts.

- A change in circumstances affects Chapter 4 status, and you may need to notify the withholding agent within 30 days.

For a separate reporting workflow, see How to Fill Out FBAR (FinCEN Form 114) Step by Step.

From Compliance Anxiety to Competitive Advantage#

Use your withholding documentation as a repeatable onboarding process, not a last-minute response. That is how you reduce avoidable payment friction and cleanup work later. You cannot guarantee the outcome, but you can lower the risk of delays and messy finance back-and-forth.

Under 26 CFR § 1.1441-1, withholding rules apply when payment is made to a foreign person, so tax and AP reviewers typically look for complete, consistent records before release. That consistency matters later too. IRS refund validation has included matching 18 fields on Form 1042-S, and TAS reported that even small discrepancies could cause refund-claim rejection. TAS also reported that Chapter 3 and Chapter 4 refunds were sometimes frozen for long periods during documentation matching, including cases of up to one year or longer.

| Workflow point | Reactive process | Systemized process |

|---|---|---|

| Timing of submission | Send the form only after AP asks | Send the signed form with contract and vendor setup materials |

| Accuracy checks | Complete once and submit | Reconcile legal name, entity details, country, and tax IDs across form, contract, invoice, and vendor profile before sending |

| Renewal process | Wait for client reminders | Track your own renewal reminder based on the current verified rule |

| Document storage | Search email threads when asked | Store the signed PDF, related approval emails, and support notes in one place |

| AP follow-up | Respond after a hold appears | Confirm the correct reviewer, receipt, and any missing fields before the payment run |

With finance and procurement teams, trust comes from specific behaviors: matching entity details exactly, routing to the right reviewer, and producing the latest signed file quickly when asked. Those are the signals that you are easy to onboard and easy to pay.

- Send your current signed form to the correct client contact and get written receipt confirmation.

- Reconcile the form against your contract, invoice, and vendor record before the next payment run.

- Create a renewal reminder based on the current verified rule.

For a related example, see A UK Limited Company's Guide to Filling Out Form W-8BEN-E. If you want to confirm whether Gruv supports your market and compliance setup for cross-border payments, contact the team.

Frequently Asked Questions

Which form do I use: W-8BEN or W-8BEN-E?

Use W-8BEN if you are a foreign individual or sole proprietor, and use W-8BEN-E if you are billing through a non-U.S. entity. | Form | Who uses it | When to use it | Common misfile risk | |---|---|---|---| | W-8BEN | Foreign individual or sole proprietor | You contract in your own name, not through a separate legal entity | An entity uses it and the payer treats it as invalid | | W-8BEN-E | Foreign entity | You invoice through a separate legal business entity | An individual uses it, or an entity uses W-8BEN and triggers withholding issues | Action step: match the form to the legal name on your contract and invoice before sending anything.

What does Active NFFE mean on the form?

Active NFFE is one possible Chapter 4 status for a non-financial foreign entity, and guidance points to selecting it and completing Part XXV when it fits your facts. Action step: verify current eligibility criteria before filing, including passive-income and passive-asset tests.

Do I need a tax ID to claim treaty benefits?

If you are claiming treaty benefits, guidance indicates you generally need a U.S. or foreign tax ID. Action step: before completing Part III boxes 14 and 15, confirm your tax ID and treaty basis are fully supportable.

Where do I send the completed form?

Send the form to the U.S. payer or withholding agent, not directly to the IRS in the normal onboarding flow. Action step: confirm who owns tax-form review on the client side and get receipt confirmation.

What happens if I send the wrong form or skip it?

The payer can treat the form as invalid and apply default withholding treatment, often 30% in practice. Action step: if your form is rejected, pause payout setup and reconcile the entity name, form type, and any treaty claim before resubmitting.

How long is the form valid?

Do not rely on old validity rules, because validity and change-in-circumstances handling should be confirmed against current IRS instructions. Action step: verify the current IRS instructions before filing, then set reminders from the rule you confirmed.

When should you ask a tax advisor?

Escalate early when entity classification is unclear, treaty-claim support is uncertain, or client onboarding requirements conflict with your facts. Action step: consult an independent U.S. tax advisor before signing if you are unsure about W-8BEN vs W-8BEN-E, Active NFFE, or Part III boxes 14 and 15.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

How to Fill Out Form W-8BEN for a Foreign Freelancer

For many global professionals, Form W-8BEN is the first real point of friction in a U.S. client relationship. It often gets treated like routine paperwork. That is the wrong frame. If you run a business of one, this form is an early operating decision that affects cash flow, onboarding speed, and how much confidence a client has in your setup.