Quick Answer

Use Form W-8BEN-E before your first US payment run when you invoice through a UK company. For a uk limited company w-8ben-e filing, complete entity details from source records, align Chapter 3 and Chapter 4 status, and make your treaty basis clear in Part III so the payer can rely on it. Send the signed form through the withholding-agent intake path, keep proof of receipt, and replace it if facts change. If classification or treaty position is uncertain, pause and get technical review before submission.

How to turn a mandatory compliance document into a practical shield against a 30% withholding tax while keeping payments moving.

The Strategic Imperative: From Bureaucratic Hurdle to Financial Shield#

Use Form W-8BEN-E as a payment control during U.S. client onboarding, not as generic paperwork. It gives the payer documentation it can rely on for your foreign entity status. Where eligible, it also supports a treaty-rate claim instead of default chapter 3 withholding on amounts subject to withholding.

That is why finance teams are strict about it. A withholding agent must withhold 30 percent on amounts subject to withholding paid to a foreign payee unless it can reliably associate the payment with valid documentation. If documentation is missing or weak, presumption rules can block reduced-rate treatment. In practice, no usable form often means withholding or delay first, cleanup later.

| Situation | Payout timing | Amount withheld | Admin friction |

|---|---|---|---|

| W-8BEN-E on file and accepted by payer | Can stay on normal AP timing because tax status is already documented | No default 30 percent withholding where the payer can rely on your documentation | Lower friction. Payment can move without tax-status rework |

| No form on file before payment run | May be delayed while AP, procurement, or tax requests documents | Default 30 percent may be withheld on amounts subject to withholding | High friction. Multiple follow-ups after invoicing |

| Form submitted but incomplete or inconsistent | May pause while payer requests corrections or declines reliance | Reduced-rate treatment may be denied until documentation is fixed | Medium to high friction. Extra back-and-forth and first-payment risk |

Why your client enforces this#

The strictness is structural, not personal. The payer may be the withholding agent, and withholding agents are directly liable if required tax is not withheld. That exposure includes tax, interest, and penalties, so your client wants the correct IRS form and usable documentation delivered to them, not the IRS.

What the form is doing operationally#

At minimum, the form documents your company's foreign status for U.S. withholding and reporting. If you are claiming treaty benefits, this is also the document used to present that claim to the withholding agent. Treaty treatment is not automatic. The payer must be able to rely on the form, and eligibility still depends on requirements such as treaty residence and beneficial ownership.

| Operational point | Article detail |

|---|---|

| Foreign status documentation | At minimum, the form documents your company's foreign status for U.S. withholding and reporting. |

| Treaty claim support | If you are claiming treaty benefits, this is also the document used to present that claim to the withholding agent. |

| Treaty eligibility | Treaty treatment is not automatic. The payer must be able to rely on the form, and eligibility still depends on requirements such as treaty residence and beneficial ownership. |

| Payer-side delivery | Before the first invoice, confirm that the form is with the payer-side tax or AP onboarding team, not only your commercial contact. |

| Proof of receipt | Keep your copy and proof of receipt, such as an email or portal confirmation, because withholding decisions are made when payment is processed. |

Before the first invoice, make sure the form reaches the payer-side tax or AP onboarding team, not just your commercial contact, and keep proof of receipt because withholding decisions are made when payment is processed.

You can usually handle this yourself when the facts are straightforward. Bring in a cross-border tax adviser if you are unsure about entity classification, beneficial ownership, or possible U.S. permanent-establishment exposure. That is where document completion can turn into a tax position. Before you start filling in the form, gather the records that let you answer those points cleanly. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

The Pre-Flight Checklist: Assemble These Four Items Before You Begin#

Do the prep before you open the form. It gives your U.S. payer a cleaner record to rely on and cuts avoidable follow-up.

Plain-language terms:

- Unique Taxpayer Reference (UTR): the number HMRC says you need to use its online Self Assessment filing service.

- Withholding agent: the recipient the IRS instructions refer to for where to provide Form W-8BEN.

- Expiration: IRS instructions include an expiration topic for Form W-8BEN.

- Change in circumstances: IRS instructions include updates when circumstances change.

| Checklist item | Why your U.S. payer needs it | Common rejection trigger |

|---|---|---|

| Self Assessment registration/reactivation status | To confirm your HMRC account is usable before filing steps start | First-time registration not completed, or an older account not reactivated when needed |

| HMRC UTR and account access | To support the tax-account details you are relying on | UTR is missing, copied incorrectly, or not available from HMRC records |

| Filing timeline check | To avoid timing errors across notification, filing, and payment steps | Deadlines or earliest filing date are assumed instead of confirmed |

| Current IRS form + instructions check | To keep current documentation and submission handling aligned with IRS instructions | Old template, missed "do not use" gate, or no plan to provide it to the withholding agent |

- Confirm Self Assessment registration/reactivation status.

What to gather: whether you need first-time registration or reactivation of an existing account. Where to verify it: HMRC Self Assessment registration and account guidance. HMRC says you can notify HMRC by registering for Self Assessment, and first-time filers must register before using online filing. What goes wrong if mismatched: filing can be delayed if an existing account needed reactivation first.

- Locate your UTR and confirm source access.

What to gather: your UTR and the HMRC letter or account screen showing it. Where to verify it: HMRC correspondence and your HMRC online account. HMRC's filing guidance states that you need your UTR to use the online service. What goes wrong if mismatched: wrong number, wrong taxpayer, or no proof when follow-up questions arrive.

- Run a quick filing-timeline check before submission.

What to gather: your applicable dates for notification, earliest filing, and payment. Where to verify it: HMRC guidance for your tax year. HMRC notes filing can start on or after 6 April following the tax year end, and it lists 31 January for paying the Self Assessment bill; for the stated prior-year scenario, notifying HMRC after 5 October 2025 can trigger a penalty. What goes wrong if mismatched: avoidable late steps or last-minute rework.

- Use a fresh IRS form copy and read the instruction gates.

What to gather: the current IRS form PDF and instructions you are relying on. Where to verify it: the IRS website, not cached files. IRS instructions include a "do not use" gate, where to give Form W-8BEN (the withholding agent), plus expiration and change-in-circumstances prompts. What goes wrong if mismatched: stale templates or missed instruction checks.

If you are unsure about entity classification or signing authority, pause and confirm with your accountant or a cross-border adviser before you submit anything. You might also find this useful: How to Fill Out Form W-8BEN-E for a Foreign Company.

Before you send anything to a U.S. client, create a clean first draft with the W-8 Form Generator.

The Execution: A Zero-Error Walkthrough for UK Directors#

Complete the form from source records and fill it out so the payer can rely on it before payment. The usual failure points are classification mismatch, an unsupported treaty claim, or unclear signing authority.

| Form field group | What you should enter | Common validation failure | Quick self-check before sending |

|---|---|---|---|

| Beneficial owner identification | Your company's exact legal name, country of incorporation or organization, registered address, and the foreign tax number your records support | Trade name used, address mismatch, or tax ID entered from memory | Does every name and address match your company records and payer profile? |

| Entity and FATCA status | One Chapter 3 entity type only, plus the separate Chapter 4 status your facts support | Treating Chapter 3 and Chapter 4 as the same, or guessing the FATCA box | Have you confirmed both selections for this entity, not copied from an old form? |

| Treaty claim | Treaty country, treaty article or paragraph, claimed rate, and why you meet the conditions | Citing an article without stating conditions, or using generic wording | Does the article match this income type and your actual U.S. footprint? |

| Certification and signature | Signature, date, printed name, and signer capacity for the entity on line 1 | Signed by a day-to-day contact without authority | Can you show why this signer is authorized if asked? |

Part I identification#

Start with the company, not yourself. Form W-8BEN-E is for entities, while individuals use Form W-8BEN. Enter your UK limited company's legal name exactly as registered, and use the registered address.

Keep classification precise. Chapter 3 Status is your entity type and requires one selection. Chapter 4 Status is your FATCA status and is a separate decision. Do not reuse old selections without checking whether the entity's facts have changed. For the foreign tax number, enter the foreign TIN you can support from your records. Do not complete this from memory.

Part III treaty claim#

This is the main withholding decision point. You need to identify the treaty article or paragraph and explain why you meet the conditions, not just state that a treaty applies.

For business profits, the U.S.-U.K. treaty analysis often turns on whether profits are attributable to a U.S. permanent establishment. Use treaty language that matches your actual facts and income type.

Your payer must not apply a treaty rate if it knows or has reason to know the claim is ineligible. Before you send it, read line 15 like a reviewer. The article, rate, and eligibility rationale should be clear without guesswork.

Status certification#

After selecting Chapter 4 status in Part I, complete the matching certification section for that status. Keep the two aligned. The practical test is simple: could you support what you certified if the payer asks follow-up questions about your business activity, income profile, or ownership?

Final certification#

Sign as an authorized representative for the entity on line 1, and make sure the printed name, date, and capacity are clear. Also plan for updates over the life of the form. It generally remains valid through the last day of the third succeeding calendar year. You must provide a new form within 30 days if a change in circumstances makes the existing one incorrect.

Pause and escalate#

Do not guess through the technical parts. Stop and get professional review before you send the form if any of these apply:

| Escalation trigger | Why it matters | Next step |

|---|---|---|

| Treaty article or paragraph is unclear | The article or paragraph and conditions may not match the payment and facts. | Stop and get professional review before sending the form. |

| U.S. activity could affect permanent-establishment treatment | Permanent-establishment treatment can affect the treaty analysis. | Stop and get professional review before sending the form. |

| Income may be effectively connected income | Form W-8BEN-E is not the right form for that income path. | Form W-8ECI may be required. |

| Entity setup is complex enough that treaty entitlement is unclear | Treaty entitlement is unclear. | Stop and get professional review before sending the form. |

If income is effectively connected, Form W-8BEN-E is not the right form for that income path, and Form W-8ECI may be required. Once the form is clean, send it to the withholding agent or payer, not the IRS. Related: Understanding the UK's Statutory Residence Test (SRT).

The Post-Submission Protocol: Securing Your Compliance and Cash Flow#

A correct form can still fail if it is routed badly, goes stale, or is hard to retrieve. After you sign, treat it as a live payment-control document.

| Post-submission task | Why it matters | What can break cash flow if skipped |

|---|---|---|

| Send through the payer's withholding-agent intake process | IRS instructions direct you to give Form W-8BEN-E to the withholding agent | The form reaches a business contact but never enters the payment-control process |

| Track expiration and changes in circumstances | IRS instructions flag both expiration and change in circumstances | The payer pauses payment until a replacement form is reviewed |

| Store a retrievable record set | You need to show what was sent, when, and what supported it | A status query turns into delay because the signed form or receipt trail is missing |

Send it where payment controls are handled#

Submit the signed form through the payer's withholding-agent process, using the channel the payer designates for this documentation when it has one. Sending it only to a commercial contact is not a reliable control.

Do not rely on a casual forward. Use the payer's intake route and keep a record of how and when you sent it. The goal is simple: clear proof that the form entered the payer's payment process.

Operational gaps can derail a good document. HMRC gives a similar process warning in another context: filing without required account reactivation can delay a tax return. Treat payer intake the same way. If a required step is missed, payment can stall. Do this now: send the signed form through the payer's designated intake path and log the submission details.

Track validity, not just send date#

This is an ongoing control, not a one-time task. IRS instructions flag both Expiration of Form W-8BEN-E and Change in circumstances, so monitor both the calendar and the facts you certified.

Record an internal review date for expiration checks, then set reminders that fit the payer's review cycle and your invoice cadence. Also set an event-triggered review for any change in circumstances that could affect the submitted form.

If you cannot quickly answer, "Is this still valid today?", your control is too weak. Do this now: record your next review date, and set both time-based and change-triggered reminders.

Build a compliance vault you can actually use#

Keep the signed form and submission trail together in one retrievable location. If it helps your workflow, use a consistent filename and store the related submission and receipt records beside it.

Do not keep only the final PDF. Keep the full support trail: what was signed, what was sent, and confirmation or receipt details where available. Also keep related records you already retain for compliance, for example bank statements or receipts where relevant. In practice, retrieval speed is often what prevents payment delays when a payer asks follow-up questions.

If the payer rejects the form or disputes the status, pause and clarify what changed before you resubmit. Do this now: create the folder, save the signed form, and attach the related submission and receipt records.

For a step-by-step walkthrough, see How to Fill Out Form W-8BEN for a Foreign Freelancer.

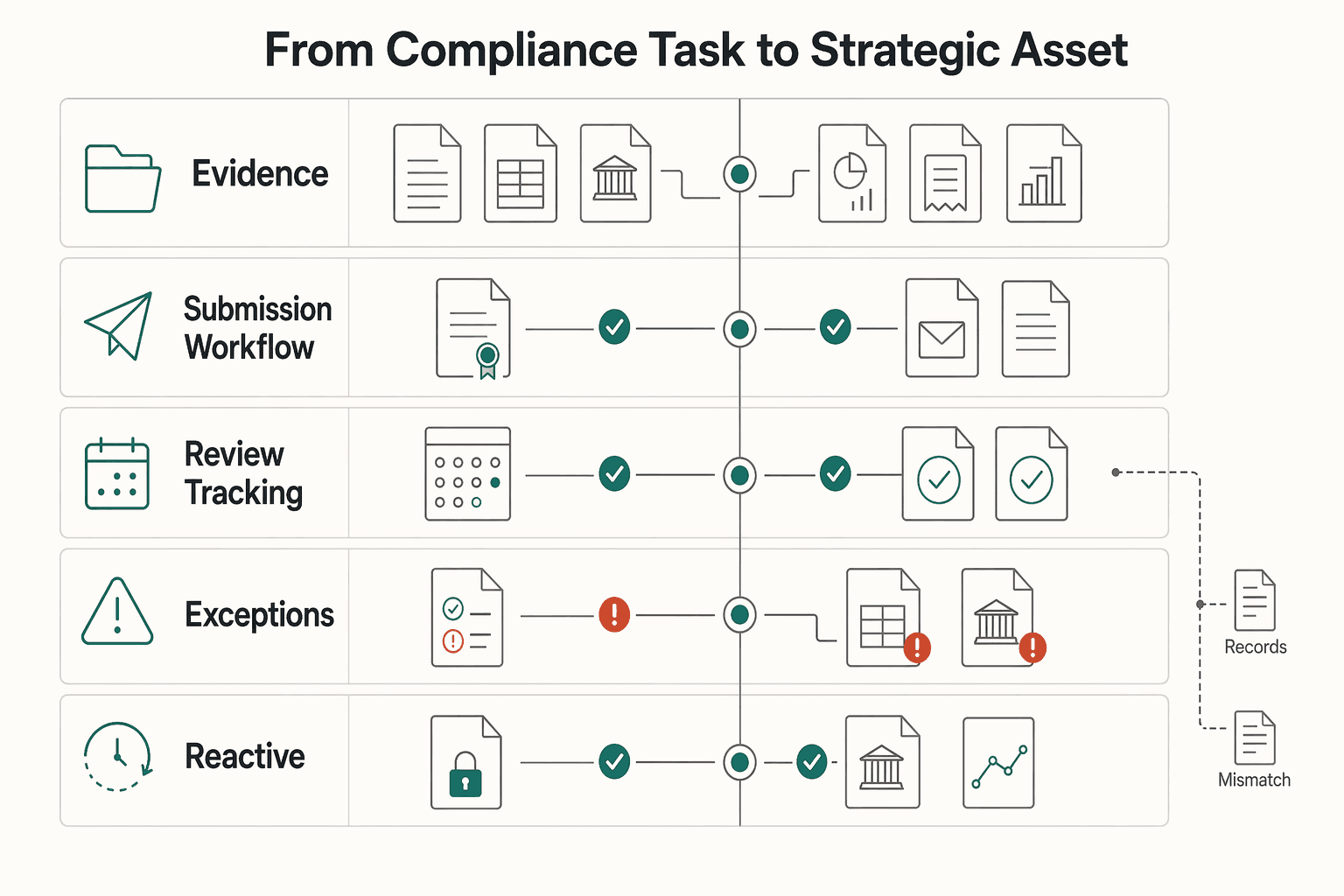

From Compliance Task to Strategic Asset#

Treat this as a repeatable control, not a one-off form task. Standardize your documentation, submission, review, and exception checks so payments keep moving with less friction.

| Control area | What to do |

|---|---|

| Documentation standard | Keep one current folder with consistent company details. Include your submitted form or submission confirmation, and the records you already need for tax work, for example bank statements or receipts. |

| Submission workflow | Use the payer's actual intake channel, then confirm the record is accepted in their system. |

| Review tracking | Set calendar reminders to review your documentation before payment problems force a fix. Use current filing instructions, and avoid draft IRS materials labeled Caution: DRAFT, NOT FOR FILING. |

| Exception handling | When key payee details change, pause and confirm whether updated documentation is required. |

- Documentation standard

Keep one current folder with consistent company details. Include your submitted form or submission confirmation, and the records you already need for tax work, for example bank statements or receipts.

- Submission workflow

Use the payer's actual intake channel, then confirm the record is accepted in their system. Do not assume an emailed attachment updated their records.

- Review tracking

Set calendar reminders to review your documentation before payment problems force a fix. Use current filing instructions, and avoid draft IRS materials labeled "Caution: DRAFT, NOT FOR FILING."

- Exception handling

When key payee details change, pause and confirm whether updated documentation is required. This is a practical control that can reduce rework during onboarding or payment processing.

| Handling style | Timing | Cash-flow predictability | Payer friction | Error recovery |

|---|---|---|---|---|

| Reactive | After a payer request or payment issue | Typically lower | Typically higher under time pressure | Often slower, with more back-and-forth |

| Early | Before onboarding or the next payment cycle | Typically higher | Typically lower because records are ready | Often faster because the audit trail is easier to follow |

Run this alongside your UK compliance calendar. You'll need your UTR to use HMRC's online filing service. First-time filers must register before using it. Late notification can trigger penalties after 5 October 2025 for the cited year. Filing can also be delayed if an existing account is not reactivated when required.

If your facts, entity classification, or treaty position are unclear, stop and validate them with a qualified adviser before you rely on treaty-based withholding assumptions.

We covered this in A Guide to VAT Registration for a UK Company Selling to the US.

If you want your cross-border payments and tax-document steps handled in one operational flow where supported, explore Gruv for freelancers.

Frequently Asked Questions

Which form do you use: W-8BEN or W-8BEN-E?

Do not guess the form type. Confirm what applies to your payee setup using the payer’s onboarding requirements, then cross-check the IRS instructions. The IRS instructions for Form W-8BEN-E include both “Who Must Provide Form W-8BEN-E” and “Do not use Form W-8BEN-E,” so review those sections before submission. | Form type | What to verify first | Common mistake | What your U.S. payer may do next | | --- | --- | --- | --- | | W-8BEN | Confirm with the payer that this is the form expected for your file | Choosing it without confirming requirements first | Pauses processing until the form choice is clarified | | W-8BEN-E | Review “Who Must Provide Form W-8BEN-E” and “Do not use Form W-8BEN-E” in the IRS instructions | Submitting before confirming scope and current status | Requests clarification or a corrected submission | | Not sure yet | Mixed setup or recent restructuring | Guessing instead of confirming payee status first | Pauses processing and routes to tax or compliance review |

What does “Active NFFE” mean in plain English?

Treat it as a technical classification question, and verify the correct treatment before filing, especially for holding structures, IP-owning entities, or mixed-income setups.

What if you spot a mistake after sending the form?

Treat it as an operations fix and close the loop in writing. The IRS instructions explicitly include “Change in circumstances” and “Expiration of Form W-8BEN-E,” so if details are wrong or no longer current, submit an updated form through the withholding agent workflow and confirm records were updated.

When can you handle this internally, and when should you escalate?

Handle it internally when the issue is administrative, such as formatting, signature, date, or routing. Escalate to a qualified tax adviser when classification is unclear, your treaty position is uncertain, or you are in repeated payer rejection cycles without a clear basis. Rejections without clear reasoning are a signal to stop making iterative edits and get technical review.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

How to Fill Out Form W-8BEN-E for a Foreign Company

Start here: Form W-8BEN-E is documentation for a foreign entity, not an IRS filing. You send it to the U.S. payer or withholding agent so they can classify the payment and determine whether they may treat your company as a foreign beneficial owner.