Quick Answer

Handle contractor payment corrections as controlled finance cases with a case record before any recalculation starts. Use retroactive pay only when a prior payment was made but was short, and treat back pay as an internal label unless your policy defines it. Gather the agreement, rate history, pay-period records, and prior payout evidence first, then calculate, approve, execute, post to the platform ledger, and reconcile.

What Back Pay and Retroactive Payments Mean for Contractor Payouts#

If you run contractor payouts, treat payment corrections as controlled finance cases, not one-off support fixes. We see teams lose the trail once a missed payout or underpayment gets patched across tickets, spreadsheets, processor dashboards, and a later payout cycle, because then finance, audit, and the contractor all ask different versions of the same question: what exactly happened?

Before you start#

Set one non-negotiable rule: every contractor or freelancer correction gets a case record before recalculation starts. That record should include the governing agreement terms, affected pay period, prior payout references, incident notes, and jurisdiction facts captured at intake. If those basics are missing, the case is not ready for release.

Use this sequence:

- Classify the issue so teams agree on what is being corrected.

- Assemble the evidence packet from source records before changing amounts.

- Calculate and approve the correction with clear separation between review and release.

- Execute, post, and reconcile so the approved amount, payout result, and ledger entry match.

This is operating discipline, not a legal standard.

Keep the scope tight#

This guide is about platform operations for contractor and freelancer payment corrections. It is not broad employee HR policy, and it does not assume employee payroll guidance automatically applies to independent contractors. That distinction matters because many retroactive-pay explainers are written for employees. QuickBooks , for example, frames retroactive pay for hourly and salaried employees.

The scope here is practical: you are correcting a prior payment outcome for a non-employee payee, and you need a record that finance, ops, product, and audit can all follow. If you are tightening the primary payout path at the same time, Invisible Payouts for Contractors is a useful companion for drawing the line between automation and human review.

Anchor decisions in the right documents#

When payment terms are disputed, the governing document matters more than memory. Formal contracting frameworks such as FAR Part 52 pair clause text with instructions for use. Use the same discipline here by working from the agreement version, rate history, and pay-period records that were in force at the time.

Apply that same caution to legal research. FederalRegister.gov states its XML version does not itself provide legal notice or judicial notice and should be verified against an official Federal Register edition. Treat that verification as a real checkpoint, not a formality.

What good looks like at close#

A clean correction is more than a successful payout. At close, you should be able to show:

- who opened the case and how it was classified

- which source records supported the correction

- who approved the amount

- which provider reference confirms execution

- whether the ledger posted the same figure

Compliance-heavy programs often pair contract obligations with active monitoring and specific checkpoints. Ohio guidance , for example, ties wage-rate compliance to payroll monitoring and sets a submission checkpoint of one week after bids are received for required forms. You do not need to copy that model, but the operating lesson is useful: define checkpoints early, verify against source records, and do not close cases with unresolved gaps.

From there, the next decision drives everything else: are you fixing unpaid prior-period amounts, or correcting money that was already sent?

Set the line between back pay and retroactive pay#

Use retroactive pay only for past underpayments where a payment was already issued. Treat any back pay label as an internal platform definition unless your own policy defines it clearly. The available source material supports retro pay as an underpayment correction, but it frames the issue in employee-payroll terms, not as a contractor-specific legal classification standard.

Step 1#

Define retroactive pay precisely at intake. Apply it only when the record shows the contractor was paid for a prior period and that payment was short. A reviewer should be able to point to both numbers in the case: what should have been paid and what was actually paid.

Confirm there is an existing payout reference, ledger event, or provider record for that period. If you cannot verify money was sent, do not classify the case as retroactive yet. If you do not have a clean internal state model for that proof, Payment Status Visibility: Real-Time Payout Tracking is the next workflow to fix.

Step 2#

Define back pay as an internal platform label and document that scope. The material here does not provide a direct back-pay definition, so do not present one as a sourced contractor legal rule. Write the definition your finance, ops, and audit teams will use, then apply it consistently.

That consistency matters because retro corrections already require reopening prior records and approvals. If case labels drift, reconciliation and reporting get messy fast.

Step 3#

Record the selected type in both the case record and the audit trail. Keep the label, affected period, and evidence for why that label was chosen in the case record, then mirror that choice in the audit trail for downstream reconciliation.

Use a minimum classification evidence pack:

- pay period ID

- original calculated amount

- actual amount paid, if any

- payout or ledger reference

- incident note on missed or late-finalized inputs

If actual amount paid is blank or disputed, pause and verify before calculation starts. This is the branch point that keeps approval, execution, and reporting clean.

Map correction triggers to incident types before you touch money#

Do not start with the amount. Start with the cause. If you skip trigger classification, approvals, exception handling, and reporting all collapse into one generic path.

Step 1 Define a fixed trigger map#

Use a small internal trigger set and require one primary trigger per case. In this workflow, treat labels such as payroll error, missed bonus, missed commission, overtime wages mismatch, minimum wage shortfall, and independent contractor misclassification review as operating categories for triage and reporting, not a legal taxonomy.

Keep category names stable quarter to quarter so trend reporting stays comparable. Your first checkpoint is simple: one primary trigger, one evidence note for that choice, and one owner chain before anyone touches money.

| Trigger | Validate first | Minimum owner path | Hold condition |

|---|---|---|---|

| Payroll error | Original input or rate vs. what was paid | Ops validates, finance approves amount, payments executes, finance closes | Missing prior payout or ledger reference |

| Missed bonus | Bonus terms, earning event, affected period | Business owner validates facts, finance approves, payments executes, finance closes | Bonus rule or approval record missing |

| Missed commission | Commission rule, source transactions, prior payout status | Revenue or ops validates, finance approves, payments executes, finance closes | Source transactions incomplete or disputed |

| Overtime wages mismatch | Hours basis, rate basis, affected period | Ops validates, finance approves, payments executes, finance closes | Hours record or applicable context unclear |

| Minimum wage shortfall | Applicable floor, time or output record, affected period | Ops validates, finance approves, payments executes, finance closes | Worker location or applicable rule missing |

| Independent contractor misclassification review | Contract facts, working arrangement, jurisdiction context | Ops gathers facts, legal or compliance reviews, finance waits, separate closeout signoff | Legal-status dispute or adverse-action risk |

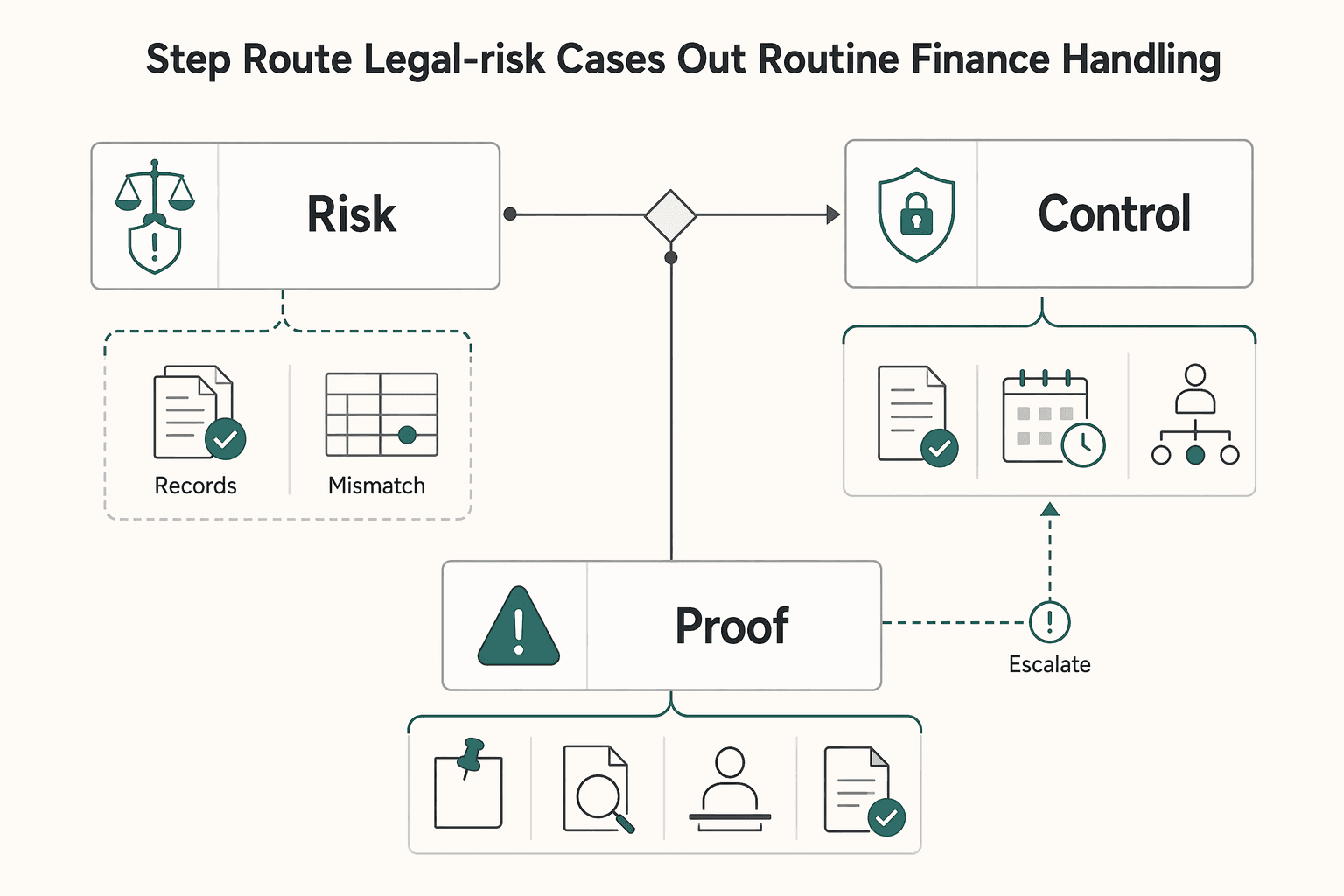

Step 2 Route legal-risk cases out of routine finance handling#

If the signal is worker-status risk, stop the normal finance correction flow and route the case to legal or compliance. Finance can gather records, but it should not decide status on its own.

Make that exception branch explicit: who approves what, when data syncs, what happens when information is missing, and how exceptions are handled. Where review may lead to adverse assessment, use a stricter control pattern with written notice of basis, an opportunity to submit evidence, and a neutral decision-maker before finalization.

Step 3 Assign ownership by trigger, not by team habit#

For each trigger, assign four roles: fact validator, amount approver, payout executor, and closeout signoff owner. Keep amount approval separate from payout execution to reduce missed-approval risk.

At close, confirm the final record includes the trigger, named owners, exception status, and routing evidence. If the trigger changes after approval, reopen and reapprove so the audit trail, reconciliation, and reporting stay aligned.

Prepare the correction packet before calculation starts#

Build the packet before anyone touches the amount. If the case is missing a clear pay period, rate history, or prior payout reference, hold it.

| Packet item | Include |

|---|---|

| Original contract or pricing terms in force | Include the original contract or pricing terms in force. |

| Rate history | Include rate history, and do not attach only the latest contract if amendments or rate changes exist. |

| Pay-period records | Use the payment period covered and payment date, not just an invoice date or work date. |

| Prior payout references | For paid but wrong amount cases, include the prior payout reference. |

| Incident notes | Keep notes short: who raised the issue, suspected trigger, affected periods, and whether the worker disputes the amount. |

| Pay basis, rate fields, additions or deductions | Where records support it, include them so reconciliation has a concrete trail. |

Step 1 Assemble the minimum evidence packet#

Use one fixed minimum packet for every correction case, even when the amount looks obvious. Include the original contract or pricing terms in force, rate history, pay-period records, prior payout references, and incident notes on what failed and when it was found.

Your checkpoint is the payment period covered and payment date, not just an invoice date or work date. Where records support it, include pay basis, rate fields, and any additions or deductions tied to that period so reconciliation has a concrete trail. If your month-end close still depends on spreadsheet exports, QuickBooks Online payout reconciliation for contractor platforms is a useful companion on the finance side.

Keep incident notes short and useful: who raised the issue, suspected trigger, affected periods, and whether the worker disputes the amount. Do not attach only the latest contract if amendments or rate changes exist.

Step 2 Pull source events from the platform ledger first#

Start from platform-ledger events for calculation input, then use processor or bank records to resolve mismatches. That keeps the correction tied to the same internal entries you will use later for reconciliation and general-ledger posting.

Before opening external exports, confirm the case traces to the original internal transaction or payout events. For "paid but wrong amount" cases, include the prior payout reference. Where supported, use payout ID filtering to inspect the transactions included in that payout. For the system boundary between payout events and journals, ERP integration for payment platforms shows how to keep those references intact downstream.

If you start from processor statements instead, settlement timing, fees, and payout grouping can get mixed up with the underlying earning event. That is how a simple correction turns into a second one.

Step 3 Attach jurisdiction context before anyone calculates#

Add jurisdiction, worker location, and payout corridor before amount calculation. This is not a closeout field. It affects whether the payout path is even feasible and whether the case needs a different compliance or reporting route.

For cross-border cases, confirm the corridor is supported for the platform and connected-account regions. If worker location is unclear or the corridor is unsupported, pause and escalate before approval. For U.S.-source payments to nonresident individuals, reporting and withholding can follow a different path than domestic contractor corrections, so that context needs to be set up front.

Step 4 Name every affected pay element explicitly#

Do not leave the packet as a single "underpayment" line. List affected components explicitly: base amount, bonus, commission, overtime, or other adjustment categories your platform uses.

If overtime is involved, flag components that can affect regular-rate math, including commission and bonus amounts, and map them to the correct pay periods, especially when hours above 40 in a workweek are part of the issue.

Final pre-calculation checkpoint: each component has an evidence source and a period tag. If bonus or commission appears only in notes and not as an affected element, send the packet back for completion.

Calculate the owed amount and choose the right payment method#

Calculate the correction from documented components, then choose the payment method from a written operating rule with independent approval checks. The material here does not provide contractor-specific formulas or a mandated choice between a standalone payment and a batched payout, so do not release funds until your internal rule is explicit.

Step 1 Rebuild the amount by component#

Keep each affected pay element as its own line item through review, with period, source record, and reason for inclusion.

Checkpoint: every line traces to evidence already in the correction packet.

If the case arrives as one net adjustment with no component trail, send it back for rebuild.

Step 2 Verify non-obvious assumptions against authoritative editions#

If a calculation or routing decision depends on interpreting external guidance, verify it against an authoritative edition before approval. FederalRegister.gov states its web presentation is not the official legal edition and points to a printed PDF for verification. IRS bulletin synopses are also described as non-authoritative aids.

Checkpoint: the case file names the exact authoritative document used for each non-obvious assumption.

Step 3 Choose method using documented operational requirements#

Select the disbursement path through documented operational requirements, not operator habit. Record the rule used, the facts that triggered it, and the required confirmation step before release.

Checkpoint: the file shows the method selected, the decision reason, and confirmation completed. When the real question is cadence rather than urgency, Payment Scheduling for Platforms can help you separate off-cycle exceptions from routine batches.

Step 4 Separate calculation review from payout release#

Treat amount validation and payout execution as two approvals, even in a small team. One reviewer confirms the calculation build. A different reviewer confirms method, destination, and references at release.

Checkpoint: a short approval record ties the approved amount, chosen method, and payout-creation references together before funds move.

Route approvals and compliance checks before release#

Release should be its own control point. By the time a case reaches payout creation, contract facts and internal checks should already tell you which route applies.

Step 1 Map approval routing to documented case risk#

Set approval tiers in internal policy, then record the selected route on the case before payout creation. If the correction depends on contract scope, rate terms, or renewal period, require the governing agreement and change record in the file, not email summaries. In the Michigan contract terms, required work is tied to Schedule A services and deliverables, and renewal-option exercise is documented through a Contract Change Notice.

Step 2 Complete required checks and stabilize the case packet before release#

Run the checks your platform and policy already require before you move a case to release, then keep the reviewed inputs stable through final approval. That sequence is an operating control, not a rule created by the cited sources, but it reduces approved-versus-sent mismatches.

A practical checkpoint is an approval record that shows the approved amount, source packet version, and release-ready payment reference. If the period, rate, or destination changes, reopen review. We use the same evidence discipline when mapping correction controls into broader audit programs; Global Payment Compliance Certifications for Platforms is the wider governance companion.

Step 3 Record timing exceptions with explicit rationale#

When you pay outside the normal batch rhythm, capture a clear internal reason and approver note. That documentation is a policy control, not a cited legal mandate, but it preserves why one case was handled off-cycle and another was not.

Avoid vague notes. Finance and audit need to be able to sort exceptions later.

Step 4 Escalate cases with missing governing facts before release#

If key jurisdiction or contract facts are incomplete, escalate instead of finalizing release on assumptions. The case file should identify the worker location, payout corridor, and contract version for the affected work period.

When clause interpretation is part of the decision, anchor the review to the governing clause text and applicable usage instructions, including FAR Part 52 and 52.104 for federal clauses.

Execute correction payouts with idempotent controls#

Once a case is approved and inputs are locked, execution should be boring. Retries should be safe, failures should leave the main path, and records should be clear without digging through logs later.

Step 1 Create a correction instruction that is safe to retry#

Create one payout instruction for the approved case and attach an idempotency control. If a call times out, a worker restarts, or someone resubmits, the same instruction should replay as the same instruction instead of creating another payment. That matters because idempotency breaches are a known payment-platform failure mode.

Keep the instruction tied to the approved case version, including how the case is labeled (back pay or retroactive pay) and the covered period in your internal record. Before submission, confirm you are executing the current approved instruction, not a superseded one. If you need the event contract underneath that control, Payment Webhooks Best Practices is the right follow-on.

Step 2 Track execution states and route failures to an exception path#

Do not treat provider submission as final. Use explicit internal states so operators can see whether a correction is waiting, progressing, failed, or ambiguous, then move non-clean outcomes to an exception path for review.

Dead Letter Queue processing is cited as a resilience countermeasure and fits correction handling well. The practical rule is simple: when outcome is unclear, investigate the existing instruction and provider evidence first instead of issuing a second send. If you batch thousands of payouts together, Guide to Bulk Payment Processing is a useful pattern library for separating clean execution from exception queues.

Step 3 Keep contractor messaging aligned to the approved correction case#

If your workflow includes contractor-facing notice, make it specific enough to reduce confusion and support churn. The message should match the approved case record and the executed instruction, including whether the correction is labeled as back pay or retroactive pay in your system and what work period it covers.

Consistency is the checkpoint here. When support, finance, and the contractor see different descriptions for the same correction, disputes take longer to resolve.

Step 4 Record provider and execution evidence in the audit trail#

As execution progresses, write provider references and key execution metadata into your audit trail so reconciliation and incident review can follow one traceable path. If your architecture supports distributed tracing, link payout events to that trace context. Distributed tracing is specifically described as supporting scalable money movement and operational resilience.

This serves the same control goal as idempotency and constant ledger reconciliation. If a payout state is marked complete but the trail is missing usable execution evidence, treat the record as incomplete and fix that gap before closing the case.

Post ledger entries and close reconciliation and settlement#

Do not close a correction from payout status alone. Close it from the records that show what was approved, what was executed, and what was recorded.

| Close check | Requirement |

|---|---|

| Approved vs executed | The approved case amount and the executed amount are either aligned or clearly explained. |

| Executed vs posted | The executed amount and the ledger posting are either aligned or clearly explained. |

| Delta note | Be specific and point to concrete evidence, such as split execution or retry outcomes, not a generic resolved status. |

| Settlement and statement evidence | Attach the correction record to settlement and provider or bank statement evidence before close. |

Step 1 Post the correction journal to the platform ledger#

Post the correction journal to the platform ledger before treating balances or reports as final. Use the ledger entry as the anchor record, and have downstream views reflect that entry instead of manual adjustments in dashboards or spreadsheets.

Make the posting traceable to the case record so a reviewer can follow one path from case ID to ledger posting and execution evidence. If someone applied a view-level or spreadsheet fix first, unwind it and rebuild from the ledger event trail. We see this break most often when external references do not map cleanly back to internal journals, which is why Virtual Accounts for Client Payment Reconciliation is worth reviewing.

Step 2 Reconcile approval, execution, and recorded posting with explicit evidence#

Use a consistent close check that compares the approved case record, execution evidence, and ledger posting for the same correction. Keep the close packet concise, but complete enough to support review with timely, accurate, relevant, and complete information.

For each case, confirm:

- The approved case amount and the executed amount are either aligned or clearly explained.

- The executed amount and the ledger posting are either aligned or clearly explained.

- Any delta note is specific and points to concrete evidence, such as split execution or retry outcomes, not a generic "resolved" status.

Step 3 Tie close records to settlement and statement artifacts#

Before close, attach the correction record to your settlement and provider or bank statement evidence so completion is verifiable end to end. Treat status screens as informational and rely on your official close artifacts for sign-off.

Define close criteria in your operating policy and apply them consistently. If references are missing or differences are unresolved, do not soft-close the case.

Handle cross-border and tax reporting implications early#

Do not release a correction until its reporting path is explicit, reviewable, and backed by reliable sources. Route by jurisdiction first, then run tax and reporting review in parallel with payout execution.

Step 1 Route by jurisdiction before release approval#

Assign each case to a jurisdiction owner or queue before approval. Require a confirmed jurisdiction value in the case record, and pause the case if country context is unclear instead of backfilling rationale after funds move.

Treat generic labels like "international contractor" as incomplete unless they tie to a source record. If the source record is missing, hold the case.

Step 2 Flag U.S. cases for reporting-owner review#

For United States cases, add an explicit reporting-review flag when a correction could affect year-end reporting classification paths, including workflows that may involve 1099-NEC or 1099-MISC. Keep payout ops from making final form-treatment calls on the fly, and route the case to the reporting owner.

Keep the case note short and specific: reporting review required, affected period, and correction amount. Do not treat a placeholder note as a final tax conclusion. If you need a handoff artifact for U.S. contractor reporting review, use the 1099 Filing Threshold Calculator for Platforms alongside the case note rather than relying on memory.

Step 3 Separate tax-impact notes from payout-execution notes#

Keep two note tracks: one for execution facts such as approval, release status, provider reference, and ledger posting, and one for tax or reporting implications such as jurisdiction, reporting-review trigger, and source-quality status. That lets finance update reporting context without reopening payment execution tasks.

Your close check is simple: a reviewer can read reporting status without tracing execution events, and can read execution evidence without guessing reporting status.

Step 4 Validate source quality before treating guidance as final#

Use source-confidence checks before finalizing reporting decisions. IRS Internal Revenue Bulletin synopses, including issue 2024-34, August 19, 2024, are reader aids and not authoritative interpretations. FederalRegister.gov also states its web version is not an official legal edition, and its XML view does not provide legal notice.

If Federal Register material is part of the decision, verify against the linked official PDF on govinfo.gov. Also account for availability risk, including a 500 server error state. If evidence is unofficial, incomplete, or unavailable, hold the case and escalate.

Recover from common failures without creating duplicate liability#

When a correction case goes sideways, certainty matters more than speed. Do not take another payment action until the record clearly shows what happened in the first one.

Step 1 Pause unresolved cases before further payment action#

If execution status is unclear, hold the case and treat it as an incident until ownership, current status, and next decision are explicit in the record. That is how you stop a documentation gap from turning into duplicate liability. We recommend pairing that hold rule with the return-and-reject playbook in Rejected Payment Recovery for Contractor Payout Platforms.

Step 2 Separate execution facts from policy/legal support#

Keep the incident record clear about what is confirmed and what is still pending. If the decision depends on a legal or policy interpretation, mark that basis as unverified until it is checked against an official source.

Step 3 Verify legal references against official editions#

For Federal Register materials, do not treat the FederalRegister.gov page alone as final authority. The page itself states it is not an official legal edition and says legal research should be verified against an official edition. It also states the XML rendition does not provide legal notice or judicial notice, and that each posted document includes a link to the corresponding official PDF on govinfo.gov.

Step 4 Close with a prevention-focused post-incident checklist#

Before closing, capture what failed, what was verified, what evidence was used, and who owns the control fix. If the same discrepancy repeats, treat it as a control defect, not a one-off cleanup task.

Build the monthly correction report finance and audit will trust#

A monthly report is credible when each case reads like a controlled change record: exact scope, exact document labels, and evidence a reviewer can verify quickly.

| Report field | What to use |

|---|---|

| Agreement reference | Use the exact document label, such as MASTER AGREEMENT NUMBER MA-2017-11. |

| Amendment identifier | Use the exact document label, such as Amendment Number 2. |

| What item changed | Use the named changed item Exhibit 8, Fees, Pricing and Payment Terms. |

| Effective date | Capture the effective date, such as August 14, 2024. |

| Execution date | Capture the execution date, such as 08/27/2024. |

| Current status | Capture current status. |

| Evidence link | Link each row to the underlying signed record and execution metadata. |

Step 1 Keep the report structure stable#

Use fixed columns for each case so reviewers can scan and compare month to month. At minimum, capture the agreement reference, amendment identifier, what item changed, effective date, execution date, and current status.

Step 2 Link each row to verifiable evidence#

Each row should link to the underlying signed record and execution metadata, and the row text should use exact document labels. For example, use labels such as Amendment Number 2, MASTER AGREEMENT NUMBER MA-2017-11, and the named changed item Exhibit 8, Fees, Pricing and Payment Terms, with dates like August 14, 2024 for effective and 08/27/2024 for executed.

Also keep scope tight. If the amendment documentation states that only specific exhibits were replaced and all other terms remain in force, the report should reflect that and nothing broader.

Step 3 Export a clean monthly review package#

Publish a clean monthly package with one row per case and durable links to the signed source records. Keep it review-ready so finance and audit can verify what changed, when it changed, and who executed it without rebuilding context from raw logs. We use the same package to track trend drift, and Payment Benchmarking for Platforms gives you a cleaner frame for comparing correction volume, delay rate, and exception mix over time.

Your next move: the correction checklist#

Use a fixed closeout checklist anchored to the executed agreement package. If a required artifact is missing, keep the case open.

- Confirm the case label. Verify the record still reflects the approved case type (

back payorretroactive pay) and current approval notes. If the case theory changed after calculation, route it back for reapproval. - Validate the governing agreement package. Review the current executed agreement package, not drafts, email threads, or earlier proposals, since the executed package supersedes prior communications. Confirm Effective Date, expiration date, Contract Amount, both signatures, and

Appendix B - Payment Provisionswhen applicable. - Check period and date alignment before money moves. Confirm the affected pay period or service window aligns with the executed agreement dates. If the governing agreement is zero-dollar (

$0.00), do not assume payment is owed. - Recalculate by approved pay elements. Rework the correction amount by each pay element recognized in your approved agreement or policy model, and make the calculation traceable to documented terms or approved modifications.

- Run approvals and clause-control checks. Complete the required approvals and compliance gates for the case, then lock calculation inputs after signoff. If payment terms or clauses change, use a documented modification path. For formal procurement contexts, see Part 52 and

52.104procedures. - Execute with duplicate-prevention controls and outcome tracking. Release the correction using your stack's duplicate-prevention control, and track status to a final provider outcome. If status is unclear, do not resend until the outcome is verified.

- Post and verify ledger records, then treat settlement separately. Post the correction in the platform ledger and verify it matches the approved correction and payout reference. Run settlement as a distinct close check and attach the provider or bank reference used by finance.

- Close reconciliation and archive the audit trail. Close reconciliation with the core records attached: approved case, execution reference, posting reference, and any exception note. Archive the final audit trail with agreement artifacts, approvals, and reporting flags (

1099-NEC/1099-MISCwhere applicable).

Your move is simple: if you can trace the case from trigger to payout evidence and ledger posting, you can close it. We treat that trace as the close gate, and we reopen the case before the next payout cycle when the trail is incomplete.

Frequently Asked Questions

What is the operational difference between back pay and retroactive pay for contractors?

Retroactive pay is a correction for an underpayment after a payment was already issued. Use back pay only as your internal label for prior-period work that your policy treats as unpaid rather than underpaid, and document that definition clearly. Operationally, both start as payment discrepancies and then split into separate case types.

When should a platform issue a standalone lump-sum payment instead of waiting for the next payout batch?

There is no universal timing rule in the available guidance, and country rules may differ. Use your internal policy after you classify the case correctly, confirm jurisdiction-specific constraints, and document why the case is being paid off-cycle. If your policy is unclear, treat this as a workflow decision point rather than a fixed global rule.

Which checks must be complete before releasing a contractor correction payout?

At minimum, confirm the pay period being corrected and capture the calculation inputs required for that case, including hours worked for hourly workers where relevant. Then verify whether the case is retroactive pay or your internal back pay case type so the amount is framed correctly. Complete any location-aware review before release when the contractor base spans multiple countries.

How should teams handle correction cases when rules differ by jurisdiction?

Use a location-aware process, not a single global assumption. Route cases through jurisdiction checks before final payout decisions, and keep the workflow explicit about where legal or policy validation happens.

What are the most common causes of contractor payment corrections at scale?

Common triggers include payroll errors, missed commissions or bonuses, and missed hours or overtime wages. These issues usually surface as discrepancies first and then map to the right correction type. Classifying the trigger early helps prevent rework during approval and reconciliation.

How do you avoid duplicate payouts when retries or provider timeouts happen?

Use a payout instruction that is safe to retry and tie it to the approved case version. Confirm the outcome of the first instruction before issuing another correction payout, and route unclear outcomes to an exception path. If status is uncertain, do not resend until provider evidence is verified.

What records should be retained so reconciliation, settlement, and year-end reporting stay clean?

Keep the records that let you reconstruct what was corrected, for which pay period, and how the amount was calculated. That includes the contract or pricing terms in force, rate history, pay-period records, prior payout references, incident notes, and any hours for hourly workers where relevant. Retain approval, execution, ledger posting, settlement, and reporting-review records so the case can be reconciled end to end.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/part-52trusted

- acquisition.gov/far/52.104trusted

- docs.stripe.com/payouts/reconciliationtrusted

- docs.stripe.com/connect/cross-border-payoutstrusted

- dol.gov/general/topic/wages/wagesrecordkeepingtrusted

- dol.gov/agencies/whd/fact-sheets/56a-regular-ratetrusted

- ecfr.gov/current/title-29/subtitle-B/chapter-V/subcha...trusted

- irs.gov/businesses/small-businesses-self-employed/fo...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: