Quick Answer

Yes: virtual accounts for payment reconciliation are useful when inbound deposits frequently need manual interpretation and each credit can be mapped to a single owner record. They work as routing identifiers tied to a physical settlement account, not separate balances, so success depends on deterministic posting logic rather than labels alone. Validate fit rail by rail, confirm repeatable handling for credits, holds, and returns, and phase rollout when mapping quality differs across ACH, SWIFT, wires, SEPA, or enabled stablecoin flows.

How Virtual Accounts Simplify Client-Level Reconciliation#

Virtual accounts are most useful when your core problem is client-level attribution of high-volume inbound transfers. They can reduce manual matching, but they do not remove the harder work around account design, posting logic, exception handling, and compliance review.

The model only works if your team starts with the right mental model: a virtual account is a sub-accounting identifier linked to a physical demand deposit account, not a separate funded balance. Transactions still post to the linked physical account, and your records determine which customer, entity, or contract gets credited.

Teams adopt this for a simple reason: in multi-payer environments, manual reconciliation is slow, error-prone, and operationally heavy. A common setup is to issue dedicated deposit instructions per beneficiary or counterparty so incoming funds can be matched one to one, instead of relying on free-text remittance references that can be incomplete or wrong.

This guide focuses on inbound attribution across rails seen in provider implementations: SWIFT, ACH, Domestic Wires, and selected stablecoin deposit flows where enabled. Support and rollout conditions vary by provider, legal-entity structure, technology requirements, and staffing capacity, so rail-by-rail planning is usually safer than assuming one uniform rollout path.

Keep failure modes in scope from the start. Payer input errors can still misroute funds when account details are entered incorrectly, and missing or incorrect references can remain common. One provider cites 2022 client feedback that up to 30% of inbound payments were incorrect or missing the right references, so the goal is not perfect data. The goal is deterministic matching for more volume and a smaller, better-defined exception queue.

Before you commit build time, pressure-test one question: can every inbound credit carry enough account-identifying and provider reference data to follow one posting path without human interpretation? If not, manual work can shift from finance to support or payments ops. If yes on some rails but not others, phase the rollout.

Treat compliance as part of attribution design, not a late overlay. Better visibility into origin of funds can support stronger monitoring and KYCC controls, but only if you define up front which fields are tied to each virtual account, what evidence is retained, and where holds or reviews can interrupt downstream movement without breaking traceability.

The rest of this guide gives you concrete checkpoints for fit, architecture, failure handling, compliance gates, and launch verification. If you are evaluating virtual accounts for payment reconciliation, the usual win comes from narrowing scope first, then expanding only after attribution is reliable in production.

Start with a precise definition so teams do not design the wrong thing#

A virtual account is a non-physical sub-account linked to a main bank account, not a separate physical account. In practice, you might assign one to a specific purpose, such as receiving payments from a particular customer.

The key design point is that segmentation is logical, not physical. The main account remains the anchor, and your records determine how each incoming payment is attributed. Cleaner attribution can reduce errors and discrepancies, but you still need to match records and resolve breaks.

Be careful with labels that sound more precise than the evidence supports. In the material behind this guide, terms like "virtual account number" and "Virtual IBAN" are not fully defined mechanisms. The ECB material supports SEPA as euro retail-payments context, but it does not define Virtual IBAN behavior.

Before building around the concept, run a simple reconciliation check with sample data: gather documents, match records, resolve discrepancies, and finalize adjustments. Confirm each identifier maps to one intended customer purpose and to the same main account across the records your team actually uses.

Decide if virtual accounts actually fit your payment pattern#

Virtual accounts are usually a stronger fit when your recurring problem is payer attribution on inbound payments. They are less useful when attribution is already clear and most breaks come from internal mapping, posting, or control design. The value comes from the identifier layer: these are sub-ledger records linked to a physical account, each with a unique identifier, while transactions still post to the linked physical account.

Check whether attribution is the bottleneck#

Start with recent inbound exceptions and separate attribution problems from internal processing problems.

- Stronger fit: repeated unknown or ambiguous payer attribution, where mapping an identifier to a customer, entity, department, or project could reduce manual investigation.

- Weaker fit: attribution is already reliable, and most breaks come from internal mapping, posting, or control design.

Assess fit by rail, not by theory#

Treat each inbound rail as its own fit check. ACH and wire settlement flows are handled as distinct flows in OCC guidance, so do not assume one matching design behaves the same way everywhere.

| Fit check | What to verify |

|---|---|

| Reference fields | Arrive consistently enough to support matching |

| Account identifier | Maps to the intended owner record |

| Timing and exception cases | Still resolve to the same record path |

For each rail, verify with real samples that those three checks actually hold.

Count operating cost before rollout#

Better attribution does not make rollout light. You still need legal-entity, technology, and resource readiness, and implementation is usually more straightforward in simpler legal-entity structures.

Before you scale, make sure you can run identifier lifecycle operations cleanly: create, map, update, retire, and audit identifiers without ownership drift.

Practical decision rule#

Adopt this model when inbound attribution errors are a repeated operational blocker and you can govern identifier lifecycle with discipline. Hold off when exceptions are infrequent or mostly caused by internal control and mapping gaps.

For the general ledger side of the workflow, see Account Reconciliation for Payment Platforms: How to Automate the Match Between Payouts and GL Entries.

Choose your account architecture and attribution model up front#

Lock your attribution model before provisioning accounts. The bigger risk is not choosing the "wrong" account type. It is letting bank identifiers, your internal records, and your ERP use different owner keys, then trying to reconcile that mismatch at close.

For payment reconciliation, shared account memo matching, Virtual Account Numbers, and Virtual IBAN are all options teams evaluate. The sources here do not support a universal ranking across them, so outcomes should be validated in your environment with clear ownership discipline, mapping rules, and change control.

Compare the options by what must be true#

Do not force a universal ranking for accuracy, onboarding friction, or operating effort. Those outcomes depend on your provider setup, payer behavior, entity structure, and internal controls.

| Option | Attribution accuracy depends on | Onboarding friction depends on | Operational overhead sits in |

|---|---|---|---|

| Shared account with memo matching | Validate with real inbound samples and deterministic owner matching checks | Validate with your payer communication and adoption process | Validate through pilot operations and exception tracking |

| Virtual Account Numbers | Validate with real inbound samples and deterministic owner matching checks | Validate with your payer communication and adoption process | Validate through pilot operations and exception tracking |

| Virtual IBAN | Validate with real inbound samples and deterministic owner matching checks | Validate with your payer communication and adoption process | Validate through pilot operations and exception tracking |

Test each option with real inbound samples. Can you prove each payment lands on one owner record without operator guesswork from free text?

Pick one primary attribution key per flow#

Choose one primary owner key for each flow, then keep that same key through bank intake, internal posting, and ERP export. The exact key set is implementation-specific, so define it explicitly and keep it consistent within the flow.

Mirror that key in both your internal records and ERP dimensions. Keep other fields as linked attributes, not competing owner definitions.

If ownership is entity-based, LEI can be a stabilizing identifier. ESRB Occasional Paper No 18 / September 2021 describes LEI as a way to unequivocally identify legal entities in financial transactions and links LEI use to operational efficiency and more accurate exposure calculation.

Also treat attribution as a sequence, not a single field. The CMS Payment and Attribution Methodologies (PY 2025, Version 1.0 December 2024) explicitly separates attribution steps and methods, and your process should do the same with clear checkpoints.

Assign lifecycle ownership and make changes traceable#

Set explicit ownership for who creates, rotates, retires, and audits identifiers, and who approves changes. Then version those changes so mapping history is auditable.

At minimum, keep a dated registry of identifier, current owner, prior owner when reassigned, status, effective timestamp, approver, and reason. That helps prevent silent ownership drift and mismatched effective dates across product, internal records, and ERP.

A practical schema principle is consistency: one canonical field set and one change history. FOCUS v1.3 defines a common billing-data schema with minimum requirements, and it also states implementation risk is assumed by the implementer. That is a useful reminder that documentation is not a control unless ownership is enforced.

Phase by entity when structure gets messy#

When entity structure or regional setup is complex, phase by entity instead of launching one global model at once. The ESRB paper notes challenges to further LEI expansion, which is a practical signal that cross-entity identification can get harder as scope widens.

Start narrow, prove deterministic ownership and traceability, then expand in controlled stages.

Map payment rails and settlement behavior before writing code#

Build the rail matrix before you write webhook handlers, so product, ops, and finance are working from one status model. A virtual account does not hold funds itself, and settlement lands in an underlying master account, so your internal statuses should reflect settlement reality rather than provider event labels alone.

Build a rail matrix your teams can actually use#

For each rail or program you support, for example SWIFT, ACH, Domestic Wires, SEPA, or USDC, keep one shared matrix that records provider payload fields, your internal status meanings, and the posting path into your records.

| Rail | Capture from provider payloads | Define internally | Variance to flag |

|---|---|---|---|

| SWIFT | Provider reference, exposed remittance/reference fields, account identifier used | What "detected," "credited," "held," and "returned" mean in your workflow | Provider coverage, country/program setup, payload shape |

| ACH | Provider reference, exposed payer/reference fields, account identifier used | Status meanings and the posting path | Provider/program differences by market |

| Domestic Wires | Provider reference and account identifier used | Status triggers and posting path | Jurisdiction and provider differences |

| SEPA | Provider reference, exposed remittance-style fields, account identifier used | Customer-visible vs internal-only state changes | Country and provider support differences |

| USDC | Provider transfer/transaction reference, receiving identifier used | Detection, hold/review, and posting rules | Stablecoin availability, compliance gating, market support |

The goal is practical alignment: one primary join key, clear optional fields, and one posting path per payment.

Define status words once and use them everywhere#

Write explicit definitions for "credited," "held," and "returned" for each rail and provider program, then use those same definitions in UI copy, ops SOPs, and finance posting rules. Real-time webhooks are useful event signals for automation, but you should not treat them as final settlement by default.

Mark provider and country variance in plain sight#

Do not hide variance in side notes. Regulatory permissions and geographic coverage differ across providers and markets, and support for rails or stablecoin programs may differ by program and country. If KYC data collection and provider-side verification are prerequisites before account issuance, list them as gating conditions in the matrix.

Verification checkpoint before any production posting#

Before go-live, run sample inbound events per rail and prove each payment maps to one, and only one, posting route. Your evidence set should include sample payloads, the chosen provider reference, the received account identifier, the expected state transition, and the resulting ERP export outcome. If that mapping is still ambiguous, keep that rail out of production scope.

For a step-by-step walkthrough, see Key Best Practices for Improving Accounts Payable on a Two-Sided Payment Platform.

Design the reconciliation event model in your ledger and ERP#

Keep provider events as inputs, and let your internal posting model decide what gets exported to the ERP. That matches how virtual account setups work: identifiers sit under a linked physical bank account, transactions post to that physical account, and the identifier gives you attribution for a customer, department, project, or legal entity.

Make the event chain visible from first signal to ERP export#

Document one end-to-end chain instead of scattered logs: payment detected, reference data received, internal record written, export to ERP.

If a payment includes remittance detail, including addendum data on some business payments, store it with the event so AR and invoice reconciliation teams can use it. Keep the stronger join keys first, then use remittance text as supporting context.

For each event, preserve the original provider payload and your internal decisions so you can trace which identifier was paid, which reference arrived, when the system accepted it, and when ERP received it.

Make retries boring with consistent duplicate handling#

Treat duplicate handling as an internal control for inbound events. If retries or replays happen, route them to the same posting outcome so you avoid duplicate credits or duplicate ERP candidates.

When reference data is missing or conflicting, hold the event for review and keep the raw provider payload attached to the case.

Separate operational review from accounting finality in the Ledger#

One workable pattern is to track non-final operational states separately from accounting-final states so operations and finance can work from the same event model without collapsing everything into one status.

A payment can be detected and attributed, but still be in review or waiting for export. Keep finance reporting tied to accounting-final states, and let operations monitor in-flight states.

Capture the audit fields you will actually need#

No source here defines a mandatory schema, so treat this as a practical checklist rather than a hard requirement:

- virtual account identifier used for attribution

- legal entity context

- provider reference, plus remittance or addendum detail received

- status transition, before and after

- review actions taken on the event

Before go-live, replay one inbound event more than once, confirm one posting outcome, and confirm ERP exports still carry attribution even though settlement posts to the linked physical account.

Related: Payment Reconciliation for Freelancers: How to Match Invoices to Bank Deposits.

Build exception handling before you scale volume#

Build the exception layer before volume ramps, or manual clearing becomes the bottleneck once delayed credits, pending confirmations, and other exceptions start to stack up.

A generic support inbox is not enough for payment breaks. Create explicit queues for common break types, for example unmatched deposits, suspected duplicates, short payments, and returns, so each case has a clear owner, risk path, and accounting consequence. That is how you preserve evidence and accountability that still makes sense months later.

Queue by failure type, not by channel#

Sort exceptions by operator decision, not by where the issue arrived, whether email, webhook, or bank report. For each case, require a compact evidence pack before action:

- raw provider payload or bank message as received

- virtual account identifier used for attribution

- amount, currency, rail, and posting timestamp

- provider reference and any remittance detail received

- current posting state and ERP export state

- operator notes for hold, release, reversal, or reallocation

This gives you a defensible record of what happened, when, and why, and helps avoid cases where ERP edits cannot be tied back to the original payment event later.

Tie operator choices to Ledger status and ERP impact#

Base decision trees on status, not intuition. Where your controls allow it, keep unmatched items in a non-final state and delay ERP clearance until attribution is resolved. Handle duplicates by separating likely replayed events from potential second credits, then apply your documented policy, for example reverse, leave unapplied, or reallocate with approval, based on your provider semantics.

| Exception type | Handling note |

|---|---|

| Unmatched items | Keep in a non-final state and delay ERP clearance until attribution is resolved |

| Duplicates | Separate likely replayed events from potential second credits, then apply the documented policy |

| Short payments | Decide up front whether partial ERP application is allowed |

| Returns | Create a traceable reversal path instead of silent overwrites |

Apply the same discipline to short payments and returns. Decide up front whether partial ERP application is allowed, and make sure returns create a traceable reversal path instead of silent overwrites.

A practical check is to sample one case from each queue and trace it from inbound event to final posting state to ERP result. If that replay is unclear, the process is not ready to scale.

Build timing into the review process#

Exception handling breaks down when timing assumptions are vague. ACH clearance can take 1-2 business days, so premature settlement assumptions can create avoidable unmatched items and return work.

Set internal SLA targets by queue, then run a daily shared review between payments ops and accounting. Review queue aging, repeat root causes, time-zone-aware cutoffs, and reference-data quality so screening, reconciliation, and reporting stay aligned.

Use exception volume as a rollout gate#

Define a clear internal expansion gate before rollout: if exceptions stay above manual review capacity across repeated close cycles, pause expansion and fix mapping quality first.

Treat this as your internal control, not a universal benchmark. In practice, these pauses can expose weak reference data, poor identifier assignment, or unclear final-state logic that would otherwise scale into a larger reconciliation and oversight burden.

If you are building reporting around this process, How to Build a Payment Reconciliation Dashboard for Your Subscription Platform covers the dashboard layer.

Add compliance gates without breaking reconciliation throughput#

Compliance gates should freeze movement, not erase attribution. Define where KYC, KYB, and AML checks can stop funds, and make sure every held item still appears in your records with a clear status, owner, and evidence trail.

Payment operations are more reliable when compliance and regulatory requirements sit inside the flow. If a flagged payment is handled outside your reconciliation and accounting view, risk and close-cycle confusion can increase.

Put gates at named points in your flow#

There is no universal checkpoint sequence established across every provider, rail, or market. Document your intervention points and map each one to a posting outcome.

| Example intervention point | What the gate is deciding | What should happen in the ledger |

|---|---|---|

| Account provisioning | Whether the customer or business can be issued an identifier or use the product | Create only after approval, or keep the identifier non-active |

| First inbound credit | Whether incoming funds can be treated as usable value | Record the credit with full attribution, then mark it held pending review |

| Withdrawal | Whether value can move to an external destination | Keep balance and attribution intact, block outbound movement |

| Payout release | Whether a disbursement can be sent onward | Preserve the payable instruction and hold release until cleared |

If you run multiple programs, specify which gate points are active in each one. Then test one flagged case per point and confirm your payment dashboard, reconciliation platform, and accounting interface show the same hold reason and status.

Treat KYCC as evidence, not a label#

Treat KYCC as operational evidence, not a badge. In practice, that means defining what evidence links a payment to the underlying customer relationship and where operators retrieve it during review.

Make the policy explicit: what evidence is captured, where it is stored, who can access it, and how long it is retained under your legal requirements. Because these requirements vary, legal and compliance owners should approve this before launch.

Freeze movement, preserve traceability#

Design a compliance hold to block downstream movement without rewriting event history. Keep the original payment event, identifiers, timestamps, and attribution result in your records, then layer hold status and operator actions on top.

This protects replayability across operations, accounting, and compliance. When that trace breaks, one issue can disrupt cash flow and create significant costs.

Confirm market and program variance before expansion#

Gate logic and evidence expectations vary in practice, and consistent implementation is a known challenge in financial-crime compliance. Treat each new country, entity, or rail as a fresh approval step, not a copy-paste of an existing setup.

Use extra caution for stablecoin or other digital-asset programs. Regulators have highlighted risk-management gaps in digital-asset services, and on January 3, 2023, the FED, OCC, and FDIC issued a joint statement on crypto-asset risks to banking organizations. Before enabling a new market or program, get legal and compliance sign-off on gate points, evidence model, and hold behavior.

Roll out in phases with clear ownership and exit criteria#

Roll out in phases only when each phase has named owners and pre-agreed exit evidence. That keeps you from scaling complexity before you can clearly explain reconciliation differences across sales records, gateway activity, and bank deposits.

A tight first phase is about diagnosability, not caution for its own sake. Since each gateway or rail settles on its own schedule, differences are expected. The checkpoint is whether those differences are explainable, for example timing, fees, refunds, or chargebacks, not forcibly equalized.

| Phase | Example scope | Exit evidence before expansion |

|---|---|---|

| Phase 1 | Narrow initial scope, limited counterparties, strong event observability, regular finance review checkpoints | Inbound events are attributed into the posting system, exceptions are explainable, and ownership is clear for triage and resolution |

| Phase 2 | Add another gateway or rail | Exception patterns remain explainable after adding another independent settlement timeline |

| Phase 3 | Expand to multi-entity scope | Entity-level posting and ERP outputs reconcile with differences documented, owned, and actively resolved through a full close cycle |

Assign a simple RACI across the teams involved, for example product, engineering, treasury, and accounting, for provisioning, exception resolution, and ERP close support. The key test is operational: every exception type should have one owner for triage and one owner for final resolution.

Define exit criteria as evidence, not optimism. At minimum, set and agree phase gates for attribution quality, exception response performance, and tracked system-to-ERP breaks through one full close cycle.

Related reading: When Payment Links Fit and When to Route to ACH, Wire, or Virtual Accounts.

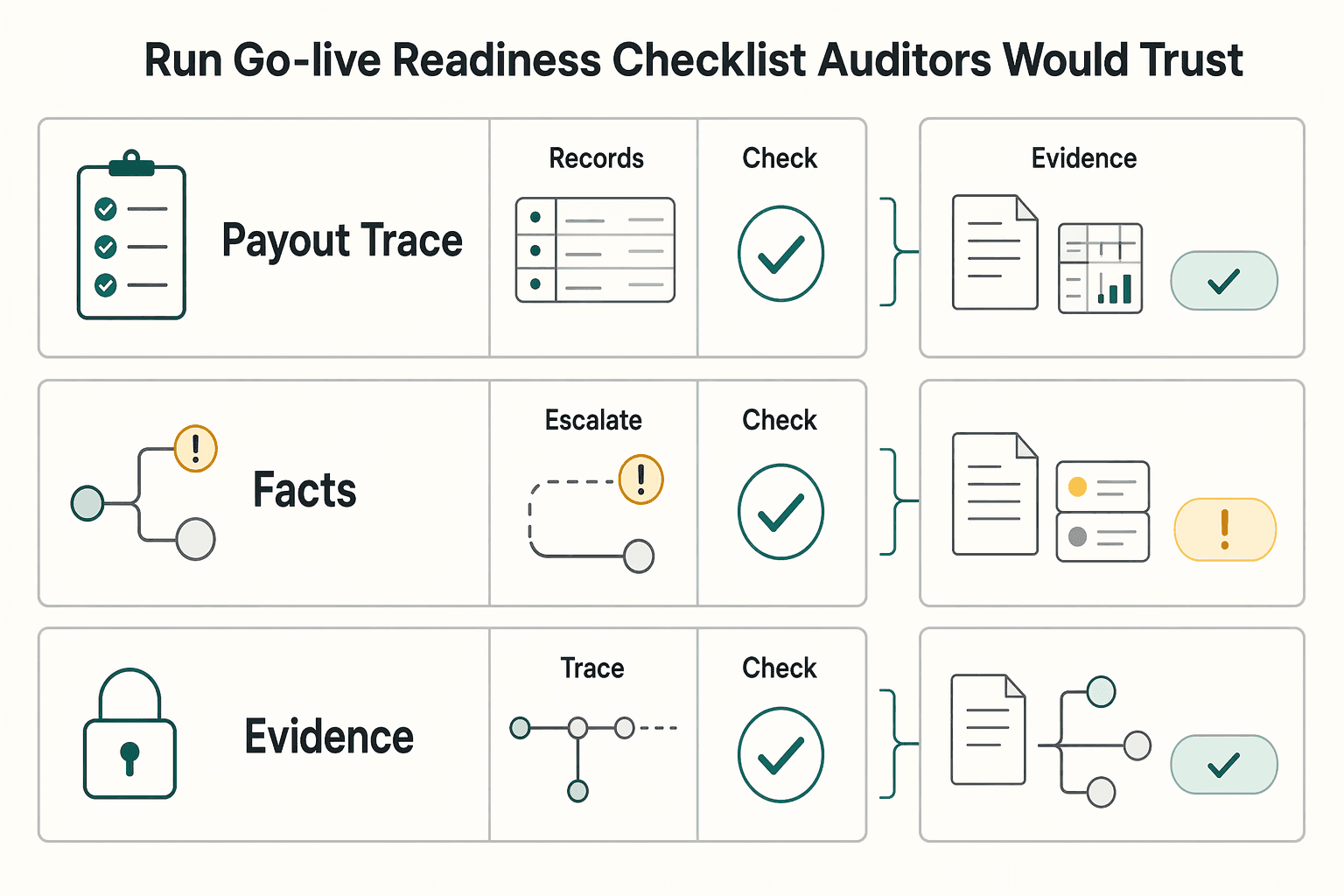

Run a go-live readiness checklist your auditors would trust#

Do not expand beyond the initial cohort until you can show evidence, not just confidence. A credible go-live file should show that records can be compared across systems, exceptions are routed for review, and every action is traceable for audit.

| Evidence item | What it shows |

|---|---|

| End-to-end traces | Straight-through and exception cases |

| Review queue artifacts | Review queues and action history |

| Clear scope record | What was in scope, what was tested, and what remains out of scope |

Start with record integrity in your own model. Verify that the core fields you rely on for reconciliation are complete and consistent across active records, and that operators can trace status and history without relying on ad hoc spreadsheets.

Then test the system-to-ERP trail on both normal and exception paths. Automated reconciliation is useful only when internal and external records can be compared and explained, and manual reconciliation is a known failure mode because it is slow and prone to human error. Before go-live, walk end to end through a clean case and an exception that routes to a review queue, then confirm the actions and outputs are visible in the audit trail.

Controls should be checked as implemented, not as designed in an earlier draft. Validate production behavior for the controls your rollout depends on. Rollouts often fail on execution details like data cleanup, team training, and integration quality.

A lean evidence pack usually includes:

- end-to-end traces for straight-through and exception cases

- artifacts showing review queues and action history

- a clear record of what was in scope, what was tested, and what remains out of scope

Sign-off should name the cohort, known limits, and expansion conditions. That is what makes the rollout controlled instead of just larger.

If you are running this flow on Gruv, compare your checklist against Gruv's Virtual Accounts module.

Track the metrics that reveal hidden cost, not just faster matching#

Match speed alone is not enough. Your scorecard should show where people still intervene, where exceptions sit, and whether the close process is actually improving.

Start with a small set of core measures, and define them once across teams:

- auto-match rate

- manual touch rate

- exception aging

- close-cycle delay impact

Keep a written metric spec with the source field, denominator, and exclusion rules. This helps prevent cross-team KPI drift and reduces the risk that retries or duplicate attempts create false improvement signals.

Break performance out by rail#

Track reconciliation performance separately by rail or system instead of relying on one blended number. Cross-system comparisons get messy, so segmented views help you find where performance is truly weak.

Tie each rail metric to traceable records in your audit trail. If you ingest in batches, validate unique batch numbers and header-trailer consistency before posting so skipped or duplicate batches do not contaminate reporting.

Watch for operational drag#

Hidden cost usually shows up outside the match engine. Track:

- manual journals in ERP

- repeat exception types

- time to resolution by team

Also watch errors and timeouts as a separate signal. They often point to processor or system issues, and even short error windows can create meaningful operational and reporting impact.

Use each review cycle to make a scope decision#

Use each review cycle to make one clear call: expand coverage, fix an architecture gap first, or narrow rail coverage by market. If manual touches and repeat exceptions stay concentrated in one rail across cycles, do not broaden rollout based only on improving aggregate match metrics.

Conclusion#

Treat this as an operating decision, not a feature request. Virtual accounts work when the identifier model, posting logic, and finance handling launch together, because the identifier alone does not fix attribution.

A virtual account is still a reporting layer inside a physical master account, and funds settle in that parent account. So the real test is end to end: the identifier appears in invoices or payment instructions and supports matching in ERP or treasury tooling. If that chain is not deterministic, you have added labels without removing manual work.

A practical path is phased. Start with one entity and one rail, prove that the same identifier consistently maps to the same owner and posting result, then expand by rail and by entity. A practical checkpoint is simple: include the identifier in payment instructions, confirm settlement in the master account, and verify your ERP or treasury tooling auto-matches by identifier.

Expand only after constraints are clear. Rail behavior, market coverage, and provider programs are not uniform, so Virtual IBAN evaluation in SEPA or eurozone contexts should not be treated as a universal pattern for ACH, SWIFT, domestic wires, or other programs.

A common failure mode is operational drift. Reconciliation can still be hard in transfer-heavy environments, and adoption can stall because of organizational inertia. Missing identifiers, inconsistent entity mapping, or unresolved posting ownership just move exceptions upstream.

A practical recommendation is to prove the model with evidence before broad rollout. Keep a small launch pack showing identifier format, where it appears in payment instructions, how auto-matching works in ERP or treasury tooling, and what happens when attribution fails. If provider or compliance constraints are still unclear for a market or program, pause expansion until they are confirmed.

When you are ready to scope rollout by rail and market, use contact Gruv to confirm fit and implementation path.

Frequently Asked Questions

What are Virtual Accounts for payment reconciliation?

In this context, virtual accounts for payment reconciliation are reporting identifiers inside a physical settlement account, not separate bank accounts. Funds sit in the main physical account, and the virtual identifier helps post each incoming payment to the right customer, entity, or invoice. They support attribution and sub-accounting, but they do not hold balances.

How do Virtual Account Numbers improve client-level matching in practice?

They can improve matching by assigning distinct payment details to each customer, transaction, or invoice. That gives incoming payments a stronger attribution signal than relying only on free-text references. It can also reduce misattribution risk when payer-entered details are wrong or incomplete.

What is the difference between Virtual Accounts and Virtual IBAN?

A virtual account is the broader reporting-layer concept within a physical account. Virtual IBAN is presented as a reconciliation automation approach, but the detailed legal and technical mechanics are not defined in the provided material. Treat implementation details as provider-specific and confirm behavior directly with your provider.

Which rails can support this model, and where do SWIFT, ACH, Domestic Wires, SEPA, and USDC differ most?

From the provided material, ACH and SWIFT are the only rails with concrete detail. ACH is described as a U.S. domestic rail, with typical costs of $0.26-$0.50 per transaction, typical settlement of 1 to 3 business days, and Same-Day ACH cited up to US$1 million. SWIFT is described as a global communications layer for cross-border transfers, often with US$30-US$75 bank fees and 1 to 5 day timing. For Domestic Wires, SEPA, and USDC, the grounded takeaway is to validate rail-specific behavior before rollout rather than assuming they behave like ACH or SWIFT.

Do Virtual Accounts eliminate reconciliation work entirely?

No. Virtual accounts can reduce manual matching, but they do not remove exceptions or all operational follow-up. They also do not remove compliance obligations: KYC and OFAC controls still apply at the legal-entity and physical-account levels.

What should product teams validate before launch to avoid costly rework?

Validate the core model first: each identifier should map cleanly to its owner and the underlying physical account, with traceable posting outcomes. Confirm documentation requirements early, since banks may require addenda to account terms. Then test failure scenarios such as incorrect payer details and confirm the outcome remains traceable for operations.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cms.gov/files/document/mcp-pymt-att-methodologies.pdftrusted

- elibrary.imf.org/view/journals/019/2026/002/article-A001-en.xmltrusted

- federalregister.gov/documents/2026/04/06/2026-06600/medicare-pro...trusted

- govinfo.gov/content/pkg/GPO-CRECB-1970-pt20/pdf/GPO-CREC...trusted

- irs.gov/irm/part3/irm_03-012-279rtrusted

- newcastlede.gov/DocumentCenter/View/27598/E4-Attachment-4-Fu...trusted

- occ.gov/publications-and-resources/publications/comp...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12796320trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: