Quick Answer

Use payment links when speed and low setup effort matter, then route by context as control needs rise: ACH transfer for U.S. bank-rail flows, wire transfer for large or time-critical payments, and virtual accounts for cross-border bank-transfer behavior. Keep a unified receivable trail across rails, separate confirmation from settlement, and require invoice-linked metadata from the first transaction. This lets teams launch quickly without sacrificing reconciliation quality, dispute readiness, or payout governance.

Payment Links for Platforms: When to Use Them and When to Route to ACH, Wire, or Virtual Accounts

Choosing Between Payment Links, ACH, Wires, and Virtual Accounts#

A payment link is a fast way to start collecting, but it may not be the right rail for every payment. For platform teams, the real decision is when to use links and when to route payments to ACH transfer or wire transfer, based on cost, control, and operational fit.

A payment link is a collection method that does not require your own checkout page. You create a secure payment URL, share it with the customer, and the payer completes payment on a hosted page. Teams commonly send links by email, SMS, WhatsApp, or DM. That is generally safer than asking a customer to read card details out loud, which is a major security risk.

This article is for product, finance, ops, and engineering owners making payment-system decisions, not freelancer marketing decisions. Stripe reports that 74% of freelancers say they are not paid on time, so payment method choices can affect cash flow outcomes, not just checkout completion.

A practical starting point is to use links for fast collection, then apply routing logic as payment size, bank-transfer preference, and control requirements increase. One comparative table describes direct bank or ACH transfers as cost-effective for larger payments, with timing listed as a few business days. The same table describes wire transfers as having higher transaction and currency fees. The point is not that one rail is always better. Your intake logic should match the payment context.

As you implement, treat the payment link as one step in a broader flow that may still need strong reconciliation, dispute handling, and compliance controls. The rest of this article focuses on choosing the right rail by use case and building a click-to-ledger path that still works as volume grows.

Related: A Freelancer's Guide to LinkedIn Marketing.

What a payment link actually is for a platform team#

For a platform team, a payment link is a pre-configured payment request that sends a payer to a provider-hosted checkout page through a URL or QR code. The main question is not what the link does. It is whether a hosted flow gives you enough control for the payments you run.

The basic flow is straightforward:

- Create the link with transaction details, typically including amount and currency.

- Share it through the channel that fits the collection motion, such as email, text, social, website, or invoice.

- The customer clicks or scans and is redirected to a secure hosted checkout page.

- If payment succeeds, your team receives a transaction notification.

Because checkout is provider-hosted, you offload payment-page infrastructure. You still need clear internal handling for payment status and follow-up operations.

Method coverage is a common source of surprises. Some providers support cards, digital wallets like Apple Pay and Google Pay, and local methods, but support varies by provider. Verify the actual method matrix before rollout.

One practical checkpoint is account setup. Some platforms require the payments module to be enabled and the right permissions to be in place before link creation. Reusable links can be useful when you intentionally share the same link with multiple customers, but they are a weaker fit when you need a distinct link per payment.

Where payment links win and where they break down#

Use Payment Link plus Hosted Checkout when speed to collect and low integration effort matter most. Move to deeper invoicing or other rails when reconciliation, settlement visibility, and exception handling become the real bottleneck.

| Collection pattern | Best fit for Payment Link | Red flag that points elsewhere |

|---|---|---|

| One-off service payments | Strong fit when you need fast collection, can define amount and currency clearly, and can share the link through email, SMS, WhatsApp, social, or invoice | Weaker fit when you need stricter approval flow and invoice-level control before payment |

| Milestone billing | Good fit when each milestone is issued as a separate request tied to a clear invoice or project reference | Watch-outs when links are reused and milestone context is not explicit |

| Retainers | Works for occasional or manually reviewed cycles where invoice context stays clear | Weaker fit when you need predictable recurring collection and low-touch reconciliation |

| High-volume recurring collections | Acceptable for small, tightly managed cohorts with active oversight | Poor fit when volume drives spreadsheet reconciliation, delayed exception review, and rising dispute workload |

Links are built for speed, not operational depth. They are a fast way to collect online without a full ecommerce build, but friction comes back when finance needs strict remittance context and repeatable posting to records.

Fee sensitivity can also change the decision. A cited processor range is 2.6%-3.3% + $0.10-$0.60 per transaction. On $5,000, the gap between 2.6% and 3.3% is $35, and over 50 projects/year that example becomes $1,750. That does not make links the wrong choice by default, but it does mean speed should be weighed against fee impact.

Failure modes teams usually find late#

Weak mapping can be the first issue to surface. At link creation, capture the exact amount, currency, and what is being sold, then connect that record to invoice, project, and client context. If your processor only moves funds and your team reconciles in spreadsheets later, overhead is already rising.

Payer mismatch and reuse ambiguity can come next. Multi-channel sharing is useful, and reused links need explicit payer and invoice context. If you need tighter controls, keep clear invoice or project identifiers attached to each payment record.

Settlement visibility is another break point. A successful checkout event is not the same as fully available funds. Keep a clear internal checkpoint between payment confirmation and settled cash in both ledger and ops views.

Dispute load is the final stress test. As dispute volume rises, missing invoice references and disconnected client records slow response and recovery. Dispute-protection features can help. Payout timing tradeoffs still exist, including cited platform clearing or hold differences like 7-day vs 14-day and 10-day vs 5-day windows.

Channel choice changes control#

The delivery channel changes how much context you keep. Direct link sharing is usually fastest to send, but context control is weaker unless records are tightly mapped. QR Code delivery is useful for printed invoices and other offline handoffs, but attribution can get messy if the destination is too generic. Invoice-embedded links can preserve clearer invoice-to-payment context, which can reduce manual reconciliation.

| Channel | Useful for | Control note |

|---|---|---|

| Direct link sharing | Usually fastest to send | Context control is weaker unless records are tightly mapped |

| QR Code | Printed invoices and other offline handoffs | Attribution can get messy if the destination is too generic |

| Invoice-embedded link | Preserving clearer invoice-to-payment context | Can reduce manual reconciliation |

Use links when speed is the real constraint. Switch to deeper invoicing or bank-rail flows when control, reconciliation, and exception handling become the constraint.

Related reading: What is a Fiduciary Duty? A Guide for Freelancers.

Choose the right collection rail by use case#

Choose the rail based on how your clients actually pay, then validate pricing and market scope in current provider docs.

| Rail | Setup time | Payer friction | Cost predictability | Reconciliation effort | Cross-border fit | When not to use |

|---|---|---|---|---|---|---|

| Payment Link | Depends on provider implementation | Depends on payer preference and checkout flow | For PayPal, fees depend on whether sender and receiver are in the same market (domestic) or different markets (international), and some markets are grouped for rate calculation | Depends on how consistently payment metadata is captured | Can work across markets, but market grouping affects fee treatment | When corridor or account-type pricing is not validated |

| ACH Transfer | Verify with your provider and account setup | Verify with your provider and payer setup | Not covered in the source material here | Not covered in the source material here | Use only where your provider confirms support | When approved pricing artifacts for that corridor are missing |

| Wire Transfer | Verify with your provider and bank setup | Verify with your provider and payer setup | Route and currency matter; Wise says fees vary by currency, and for EUR transfers outside SEPA, additional SWIFT fees may apply | Depends on your reconciliation process | Useful only for routes your provider supports | When fee treatment is unverified for the target route |

| SEPA Transfer | Verify with your provider and account setup | Verify with your provider and payer setup | For EUR transfers, Wise notes additional SWIFT fees may apply if the recipient is outside SEPA | Depends on your reconciliation process | Regional fit depends on route eligibility | When SEPA boundary handling or fee treatment is unverified |

The practical split#

Use a mixed rail strategy, then verify each corridor with current pricing artifacts before rollout.

If your clients are global, do not assume one fee model applies everywhere. As one example of receiving capability shape, Wise says it provides account details to receive funds in 24 currencies.

Provider examples are only examples#

Use providers as implementation options, not ranking claims. For this section, the grounded examples are Wise and PayPal.

For due diligence, verify the exact pricing artifact for the corridor and account type you are approving. Wise states fees can vary by currency and shows pricing from 0.57%. It notes volume discounts starting at 25,000 USD equivalent and says that discount status resets on the first of the month. PayPal's US consumer fee page defines "domestic" as sender and receiver in the same market and "international" as different markets, with some markets grouped for rate calculation. That page is a recency checkpoint, Last Updated: February 19, 2026, and should be treated as a US consumer pricing reference.

Store the exact fee page export used in approval. Wise also exposes fees in a regulator-standardized format, which helps with auditability.

When marketplace-native rails help, and when they do not#

Marketplace-native rails are outside the source material here, so treat them as a separate evaluation track.

Once you choose the rail mix, the next job is making sure every payment can be followed from click to ledger without manual guesswork.

Design the money flow from click to ledger posting#

When you run more than one payment rail, reliability comes from a defined process across methods. Document your money flow so late payments, unclear terms, and fee-related surprises are less likely to become transaction friction and relationship strain.

Use one explicit process across rails. The exact lifecycle states depend on your systems, but the documented flow should at least account for:

- Invoicing

- Tax compliance

- Cross-border transfer handling

Separate customer events from finance events#

Treat customer actions and finance posting as different checkpoints. Your team should define which payment confirmations are sufficient for accounting and which are only operational signals.

Keep one internal payment record tied to the invoice and use that record across operations and finance. At close, finance should be able to produce consistent payment evidence each time.

Make retries boring#

Write down retry handling rules at the process level so repeated actions are handled consistently. The goal is simple: repeated inputs should resolve predictably unless your exception path classifies them as distinct payments.

That discipline keeps repeated actions from turning into avoidable admin work.

Keep update handling explicit#

Document how payment updates are recorded and reconciled so reprocessing follows the same process definition each time.

If your team cannot quickly reconstruct payment evidence at month end, the flow is still under-specified and needs tighter process definition.

That same discipline should carry into compliance. It is easier to place gates now than to retrofit them after volume arrives.

Put compliance gates in before volume arrives#

Set compliance gates before you scale payment-link volume. Define what must clear before link issuance, before payout eligibility, and when activity must be re-reviewed.

Map checks to real handoffs#

Define where reviews occur in your collection-to-payout flow, and keep that map explicit.

Use explicit checkpoints:

- before an account can create or send payment links

- before collected funds become payout-eligible

For each hold or approval, keep the reviewed entity, linked account or payee ID, decision, and timestamp so you can reconstruct why a payout was released or blocked.

The source material here does not establish specific KYC/KYB/AML trigger requirements by market.

Hosted checkout narrows scope, not responsibility#

A payment link sends the buyer to a provider-hosted checkout page, so you do not maintain that payment page infrastructure yourself. Payment method coverage can still vary by provider.

Hosted checkout narrows checkout-page infrastructure scope, but it does not define your internal approval logic, access controls, monitoring, or payout-release governance on its own.

Add policy triggers for abuse patterns#

Define policy triggers that pause or escalate review before payout. The source material here does not specify required abuse-pattern thresholds, so those settings should be defined in your internal policy.

Put tax records into the same flow#

Include tax-document checkpoints in payout eligibility instead of treating tax handling as year-end cleanup. If you pay independent contractors, you may have to file Form 1099-NEC, and IRS reporting generally applies when four conditions are met. Nonemployee compensation paid to nonresident aliens is reported on Form 1042-S.

| Form | Use in article |

|---|---|

| Form 1099-NEC | If you pay independent contractors, you may have to file it, and IRS reporting generally applies when four conditions are met |

| Form 1042-S | Used for nonemployee compensation paid to nonresident aliens |

| Form 1096 | If you file Form 1099-NEC on paper, submit it; if you file multiple information-return types on paper, use a separate Form 1096 for each type; electronic filing does not require it |

If you file Form 1099-NEC on paper, submit Form 1096. If you file multiple information-return types on paper, use a separate Form 1096 for each type. Electronic filing does not require Form 1096.

The IRS excerpt here references a threshold condition for 1099-NEC reporting but does not provide the numeric amount.

Even with clean compliance gates, exceptions still need clear triage.

For euro-denominated transfers, see A Guide to SEPA Transfers for European Freelancers.

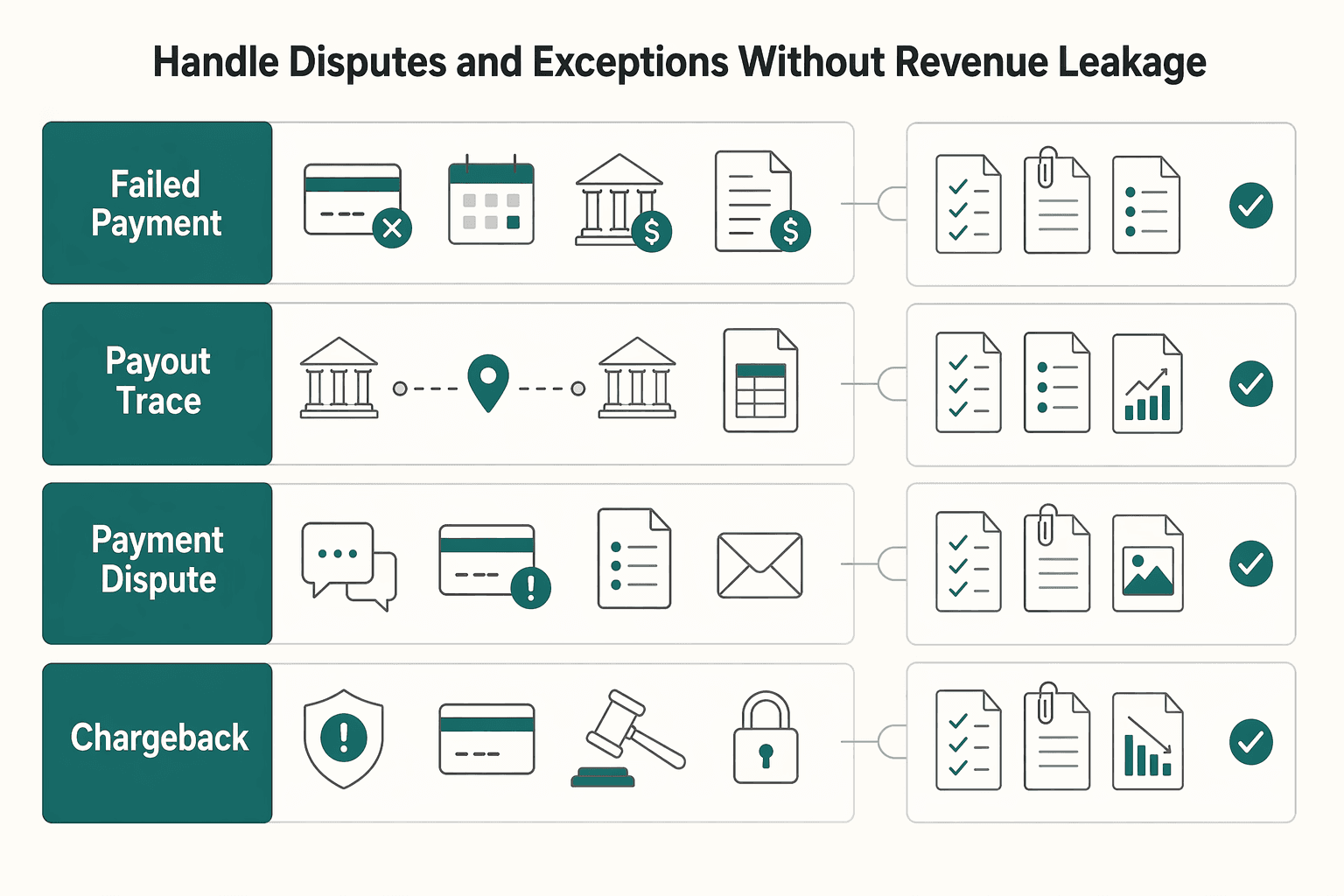

Handle disputes and exceptions without revenue leakage#

Revenue risk rises in the exception queue when different cases are treated as one problem. Run failed payment, partial settlement, Payment Dispute, and Chargeback as separate lanes, and require a complete evidence package before retry, payout, recovery, or write-off decisions.

| Exception lane | What to verify first | Minimum case file | Decision path |

|---|---|---|---|

| Failed payment | Payment or link reference and current status, including delay vs final failure | Payment record (value, date, transaction type), invoice terms, communication log | Retry, replace link, or stop collection |

| Partial settlement | Expected amount vs received amount and payment type | Payment record, invoice terms, service-delivery evidence, communication log | Collect balance, adjust receivable, or resolve over or underpayment |

| Payment Dispute | Original transaction context and what was delivered | Payment record, invoice terms, service-delivery evidence, communication log | Submit evidence, recover, or write off |

| Chargeback | Transaction record and invoice terms tied to the contested payment | Payment record, invoice terms, service-delivery evidence, communication log | Represent, recover, or write off |

Keep the response package boring and complete. Store payment value, date, and transaction type with invoice terms, including rate, expiry, and terms. Add delivery proof and communication history where available. This can support both operational follow-up and accounting treatment.

Build this record before the case exists. Cover confirmation delays and other common receiving issues, not just hard failures. Managing multiple payment methods can affect cash flow, so keep exceptions organized by lane.

Link-level metadata may help organize triage, but it does not replace review. If the case file is incomplete, route it to review, complete the record, and then decide recoverable revenue versus controlled loss. For a deeper tactical breakdown, see Payment Disputes and Chargebacks: A Step-by-Step Resolution Guide for Freelancers.

If you collect through multiple payment methods, carry the same evidence discipline through each path.

For a step-by-step walkthrough, see A Guide to Xero for Freelancers and Small Businesses.

Support cross-border collections and payouts cleanly#

Do not force one rail for cross-border payments. Keep Payment Link for hosted checkout, and add Virtual Account receipts for clients that require bank transfer, including SEPA credit transfer where your merchant setup supports it.

This works because each rail fits a different payer behavior. Payment links route clients to hosted checkout, while virtual account numbers let bank-transfer payers push funds and help automate reconciliation. If bank-first clients are part of your mix, this is often the difference between smooth collection and manual exception handling.

Mix checkout with bank receipts, but keep one receivable record#

Use one invoice and one receivable, with multiple settlement paths. If a client pays in checkout, reconcile to that record. If they pay by transfer, route them to the assigned virtual account and require the invoice reference.

At receipt, verify invoice ID, payer name, expected currency, provider payment reference, and the link or virtual-account identifier used. Unlabeled transfers can become a failure mode. Funds arrive, auto-match fails, and teams create manual suspense items or duplicate follow-up.

For Europe, SEPA credit transfer can support euro payments across the SEPA region, 41 countries in the ECB reference. But availability is not uniform, and providers note customer-location support can vary by merchant country. Confirm support for your setup before you promise SEPA as a standard option.

Make currency decisions explicit#

Cross-border leakage can come from unclear FX handling, not just fees. Set decisions at collection, hold, conversion, and payout, and store each decision on the payment record.

| Decision point | What to decide | What to store |

|---|---|---|

| Collect | Invoice or checkout currency or bank-receipt currency | Invoice currency, payer amount, payment rail |

| Hold | Whether to keep funds in received currency before payout | Balance currency, hold rule, settlement status |

| Convert | Who triggers conversion and when | FX timestamp, rate source, converted amount |

| Pay out | Beneficiary currency and destination country | Payout currency, destination, provider reference |

If you collect in one currency and pay out in another, do not rely on stale spreadsheet rates. Record the actual conversion event and timestamp from your provider or treasury process. Also validate corridor reality before promising payout currency options. Payout availability varies by country and context, and some setups require bank accounts in countries where the settlement currency is official. Initial payout timing can also differ, with some providers indicating 7-14 days after first successful live payment.

Tax and reporting still apply#

Digital rails do not remove tax and reporting obligations. For EU VAT, treatment depends on where you buy or sell and whether the transaction is goods or services. One grounded example is that B2B services sold to a business in another EU country usually do not require charging VAT. The EUR 10 000 threshold applies to distance sales to EU customers, so do not apply it as a blanket services rule.

For U.S. persons, FBAR is a separate check. If aggregate foreign financial accounts exceed $10,000 at any time during the year, FinCEN Form 114 filing is generally required. The due date is April 15 with an automatic extension to October 15. For FBAR currency conversion, U.S. Treasury exchange rates are an accepted reference tool.

Final operating caveat: payment-method and payout availability vary by market and program, and provider maps can change without guaranteeing every method. Treat availability as a pre-launch validation item, not a standing assumption.

Implementation checklist for product finance and engineering#

For a broad rollout, use a gated checklist with named owners and explicit go or no-go checkpoints. Payment links can speed up launch with less integration overhead, but that simplicity can hide control gaps unless product, engineering, finance, and compliance decisions are documented and tested.

Product#

Set the Hosted Checkout decision matrix first, then lock it before launch. Define enabled payment methods, allowed currencies, link reuse rules, and link expiry by payer segment, and make the simplicity-versus-control tradeoff explicit for each segment.

Use one checkpoint style across the team. Only tick an item when it is enabled and validated end to end. Confirm the payer sees the intended options and that each completed payment maps to the correct receivable record.

Engineering#

Treat each Payment Link ID as a tracked system record, not just a checkout artifact. Define how your system records payment-status changes so one payment event does not create conflicting internal outcomes.

Launch only after common and failure-path testing is complete. Include failed and disputed-payment scenarios in test cases, then verify records remain consistent.

Finance and ops#

Define your reconciliation and exception-handling workflow before volume scales. Include failed payments and dispute paths, and decide who owns each queue.

If your provider includes dispute-resolution tooling, use it, but keep your own response pack complete. At minimum, ensure teams can quickly retrieve invoice and payment references, status history, and supporting client-service records.

Compliance#

Set compliance launch gates up front and document ownership. Requirements can vary by provider, market, and program, so confirm what applies before broad rollout.

If requirements are unclear, log the unknowns and resolve them before expansion. Do not scale on assumptions.

Related reading: UAE Golden Visa for Freelancers and the Green Visa Decision Guide.

Use this checklist as your launch spec, then map integration details in the Gruv developer docs.

Vendor due diligence before you commit#

Choose the vendor that gives you operational evidence, not the cleanest pricing page. Before comparing headline fees, confirm you can audit, reconcile, and run payment links under failure conditions.

Start with post-launch records. You should be able to tie payouts back to underlying payments, not just confirm a checkout success. Stripe provides a named Payout reconciliation report for matching bank payouts to payment batches. PayPal settlement reporting includes per-currency debit and credit summaries, and PayPal uses five-digit transaction event codes to classify money movement. If you cannot review sample exports early, treat that as a procurement risk.

What to test before fees matter#

Do not treat "supports webhooks" as sufficient. Retry and ordering behavior are product-specific, and that changes your failure-handling design.

| Provider | Webhook or event note |

|---|---|

| Stripe | Undelivered webhook events can be retried for up to three days |

| PayPal REST | Webhook delivery can be retried up to 25 times over 3 days |

| Braintree | Webhook retry behavior differs from PayPal REST |

| Wise | Webhook event order is not guaranteed |

If your receivable state depends on event order, test replay, duplication, delay, and out-of-order delivery in sandbox before procurement.

A minimal verification pack should include:

- one sandbox payment, one refund, and one failed attempt

- webhook logs showing duplicate or delayed delivery handling

- one payout or settlement export mapped to internal invoice IDs

- one dispute or reversal path (where available) with the evidence fields you can retrieve

Coverage and contract terms#

Validate coverage against your real mix of countries, currencies, and methods. Stripe states method availability depends on currency, country, and product integration, so do not assume Apple Pay, Google Pay, ACH Direct Debit, or SEPA Direct Debit will appear everywhere. Check the exact method variant: Stripe ACH documentation is tied to US bank accounts, and Stripe SEPA support is Core scheme, not B2B.

Then review control terms in the contract. Stripe documents reserve balance behavior, and connected-account reserves can last up to 180 days, which can affect payout timing. Payoneer terms include payment-reversal rights and the ability to reject or limit payments for AML reasons. Ask for incident escalation contacts, reserve-notification terms, and settlement-timing language in writing. Then validate behavior with sandbox or controlled test transactions across Stripe, PayPal, Wise, and Payoneer where available instead of relying on marketing pages.

Measure success in the first 90 days#

Use the first 90 days to decide whether payment links should stay in your collection mix, not just whether launch worked. Measure performance by rail and segment, then make a clear keep, expand, or replace decision.

Track outcomes by rail, not in aggregate#

Track four metrics per rail from day one: collection conversion, time to settlement, exception rate, and manual-touch volume. Aggregate performance can hide segment-level tradeoffs between card links and bank-transfer rails.

Time to settlement is an early signal of operational fit. Credit card settlement usually lands in 1 to 3 business days, so repeated delays outside that window should trigger investigation into flow and integration issues before they become close-cycle noise. Use provider analytics that already expose authentication, card acceptance, disputes, and payment-method integration performance.

Manual-touch volume should be explicit, not anecdotal. Count each case where teams must chase payers, fix metadata, remap invoices, or clarify settlement status. Higher conversion with sharply higher manual effort is only acceptable if unit economics still hold.

Add risk KPIs before disputes become a finance problem#

Add risk KPIs immediately: dispute rate, internal chargeback loss ratio, and compliance hold rate from KYC or AML checks. This keeps risk visible while volumes are still manageable.

Treat dispute metrics carefully. Dispute rate and dispute activity serve different purposes, network thresholds are scheme-specific, and prolonged threshold breaches can lead to fines. Avoid a single "acceptable" threshold across providers, schemes, and geographies.

Account for timing lag in early reads. Cardholders can dispute charges up to 120 days after payment, so early-period dispute rates are incomplete by definition. Define your internal chargeback loss ratio formula once and keep it stable across segments for comparable trend tracking.

Track compliance holds with the same discipline. KYC verification is required before connected users can accept payments or receive payouts in documented platform flows, so recurring hold patterns can indicate onboarding, routing, or policy design issues.

Run monthly proof, then decide segment by segment#

Use a monthly reconciliation proof pack as an internal operating rule, then make decisions by segment. At minimum, include:

- Ledger-to-provider matching using provider references and internal receivable or invoice IDs

- Unresolved-item aging so stale exceptions stay visible

- Payout status closure for settled and paid-out payments, with unresolved items tracked separately

Use report formats built for this purpose. Stripe's Payout reconciliation report is designed around settlement batches in payouts, and Adyen's Settlement details report provides transaction-level settled and paid-out detail, including transaction costs.

At day 90, decide by segment. Keep links where conversion and operations are strong. Expand where settlement is predictable and manual effort stays low. Replace or reroute where controls, economics, or compliance outcomes are consistently better.

Conclusion#

Payment links are a strong default when you need to collect quickly with minimal integration, but they are not the right default for every flow.

Make the decision rail by rail. Use payment links when speed and low-friction hosted checkout matter. Route recurring, high-value, or account-based collections to ACH debit, and use wire for large-value, time-critical payments where Fedwire processing is immediate, final, and irrevocable once processed.

As you scale past pilot, keep the channel split explicit: in provider models like Stripe, payment links are broadly shareable, while invoicing is positioned for customer-specific billing. That can improve speed, but it can also require tighter controls on who can create links, how links map to receivables, and when teams should route to invoicing or bank rails.

Before broad launch, validate three things in production-like tests:

- Coverage: confirm support for your exact country, currency, product, and API combination. Even when a provider lists 40+ payment methods, support is still conditional.

- Exception handling: test webhook duplicate-event handling and replay behavior so your processing is idempotent.

- Product limits: verify the exact variant you plan to use. For example, Stripe's "customers choose what to pay" payment link has a default maximum payment amount of 10,000.00 USD.

Treat this as an operating model, not a checkout feature choice. Use links for fast collection where they fit. Keep ACH debit, wire, and invoicing paths active where control and fit matter more.

If you are choosing between payment links, virtual accounts, and payout rails by corridor, talk to Gruv to confirm market coverage and control requirements before rollout.

Frequently Asked Questions

What is a payment link, and how is it different from a hosted invoice page?

A payment link is a reusable, shareable URL that sends a payer to a provider-hosted payment page. In Stripe’s model, you can reuse it across channels, including QR, and the QR code does not expire unless the link is deactivated. A Hosted Invoice Page is invoice-specific: it shows invoice details and status, supports invoice and receipt PDF downloads, and the URL expires, typically 30 days after the due date and never longer than 120 days.

When should a platform use a payment link instead of ACH transfer or wire transfer?

Use a payment link when quick launch and a hosted checkout flow matter more than bank-rail control. Use ACH transfer when you want a U.S. bank rail with business-day processing and settlement cycles, and use wire transfer for large-value, time-critical payments. Fedwire processing is immediate, final, and irrevocable once processed.

Are payment links suitable for milestone billing and recurring retainers?

They can work for milestone billing when each milestone is billed as its own amount. Recurring retainers can work, but you need to confirm the exact payment-link configuration supports recurring charges. Stripe supports recurring and one-off pricing models, while at least one pricing model explicitly does not support recurring payments or recurring donations.

What are the main tradeoffs between speed, cost, control, and dispute risk?

Payment links can improve speed because they route payers to a hosted checkout page with lightweight setup. The tradeoff is control and risk. ACH and wire provide bank-rail options with different timing characteristics, while card-heavy mixes increase dispute exposure. A chargeback can reverse funds and add dispute fees, so dispute-handling readiness should factor into routing decisions.

How do KYC, AML, and tax documents affect payment-link rollout for freelancer payouts?

Payment collection does not remove payout-side compliance work. KYC and AML controls still apply. Covered institutions must maintain AML programs, and covered financial institutions must maintain procedures to identify and verify beneficial owners of legal-entity customers. For tax onboarding, U.S. payees commonly provide Form W-9 and foreign beneficial owners may be asked for Form W-8 BEN.

Can payment links work for cross-border collections and multi-currency payouts?

Yes, but only where provider support exists for your specific country, currency, product, and API combination. Stripe states you can charge in over 135 currencies and, once supported in your country, accept payments from customers worldwide. Payment-method availability is not uniform across markets, so validate your exact collection and payout paths before rollout.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- barbercosmo.ca.gov/forms_pubs/sunsetreview1.pdftrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/cross-borde...trusted

- federalreserve.gov/paymentsystems/fedfunds_about.htmtrusted

- fiscaldata.treasury.gov/currency-exchange-rates-convertertrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

SEPA Transfers for Freelancers: Invoicing EU Clients and Reconciling Payments

Use SEPA as a cashflow tool, not just a way to move money. Your real goal is simple: the payment arrives on time, in the expected amount, with enough detail to reconcile it quickly.

Resolving Payment Disputes and Chargebacks for Freelancer Platforms

This guide is for platform teams managing freelancer revenue risk. The operating rule is simple: by the time a payment dispute or chargeback starts, ownership, first-day actions, and decision criteria should already be defined.

LinkedIn for Freelancers Who Want a Predictable Client Pipeline

Treat LinkedIn as two jobs you run at the same time: a credibility check and a conversation engine. If you only chase attention, you can get noise. If you only send messages, prospects may click through to a thin profile and hesitate.