Quick Answer

SEPA transfers work best for freelancers when the client confirms a EUR payment over a verified SEPA route before you invoice. Send one invoice with the exact beneficiary name, IBAN, currency, and a single remittance reference, then match the incoming payment to your records and store the invoice, bank evidence, and delivery or approval proof together.

From Getting Paid to Getting Paid Safely: The Global Professional's SEPA Operations Playbook#

Use SEPA as a cashflow tool, not just a way to move money. Your real goal is simple: the payment arrives on time, in the expected amount, with enough detail to reconcile it quickly.

Before you send any invoice, map the payment path. Cross-border payments can involve multiple institutions, currency conversion, and regulatory requirements, and each step can change timing or cost. If correspondent banks are in the chain, extra intermediaries can add fees and processing time. For client-facing documents, add current SEPA coverage only after you verify it rather than relying on old country counts.

| Risk area | What can go wrong for you | What to check first |

|---|---|---|

| Invoice workflow | Unclear or inconsistent payment instructions trigger delays or correction requests | Use one consistent set of receiving details and reference instructions every time |

| Settlement path | Intermediaries or conversion steps change timing or reduce the amount received | Confirm how the client will send funds and whether the payment stays in EUR on a SEPA path |

| Account setup | Receiving details are not fully verified before invoicing, causing failed or misrouted payments | Verify your account can receive the exact payment type you request before issuing the invoice |

| Recordkeeping | Money arrives, but matching it to the invoice is slow or disputed | Store the invoice, payment confirmation, and bank transaction evidence together |

Run the same three controls before every send: a standardized invoice workflow, a verified provider path, and a complete audit trail. In practice, that means one version of payment instructions, one verified EUR receiving route, and one place for invoice-plus-payment records.

Start with a basic control: ask the client to confirm they will pay in EUR over a SEPA route before you issue the invoice. If that is unclear, stop there and identify where timing, fee, or conversion risk enters. FX markup against the mid-market rate can cut what you receive by several percentage points. So the risk is not just delay. It is also getting paid less than you priced for.

For a step-by-step walkthrough, see A Guide to Index Fund Investing for Freelancers.

SEPA as a Strategic Tool, Not Just a Transfer Method#

Treat this section as an operating template, not a definitive SEPA rulebook. Key details on SEPA scope, timing, fees, and scheme behavior still need provider-level verification before publication.

Keep client-facing wording tied to what you have verified. If you have not rechecked current scheme coverage or timing with the providers involved, describe those details as unverified until the exact scope and settlement timing are confirmed from provider or official source records.

Match the rail to the job#

Decide the route first, then set expectations. If instant handling has not been explicitly confirmed for the exact payer-payee path, describe timelines as unverified and avoid instant commitments.

| Rail | Use it when | Confirm before invoicing | If funds are late, check first |

|---|---|---|---|

| Provider-verified standard EUR route | Timing is not urgent and both providers confirm the route can be used | Provider-confirmed route details for this payer-payee path | Route used and invoice details |

| Provider-verified instant EUR route | Time-sensitive payment and both providers have confirmed instant handling for this payer-payee path | Explicit confirmation from both providers for this exact transfer path | Whether that confirmed path was used |

If confirmation is unclear, set expectations around standard handling until verification is complete.

Lock payment instructions before you invoice#

Run a final pre-send verification pass on the exact invoice file and keep the wording limited to details you can confirm.

| Setup check | Action before sending | Verification note |

|---|---|---|

| Beneficiary identity match | Confirm beneficiary details directly with your receiving provider | Do not publish benefit/outcome claims without evidence |

| IBAN accuracy | Recheck against verified account details | Do not publish benefit/outcome claims without evidence |

| Currency alignment | Confirm invoice currency against the intended payment path | Do not publish benefit/outcome claims without evidence |

| Payer reference format | State the exact reference format the payer should use | Do not publish benefit/outcome claims without evidence |

After sending, if details change, reissue the invoice and keep version history with payment records.

If a transfer is delayed#

When a transfer is late, troubleshoot the actual path and invoice details first. Do not assert a primary delay cause without verified evidence.

- Check the route

Confirm how the payer sent the transfer and whether it matched the planned path.

- Check the details

Re-read beneficiary details, currency, and reference on the paid invoice version.

- Check support status

If instant handling was expected, confirm that both providers had explicitly approved that exact transfer path at the time of payment.

For a fuller walkthrough, see A Guide to Invoice Factoring for Freelancers.

How to Create a Bulletproof EU Invoice Corporate Clients Pay Instantly#

Use this four-step pre-send process every time. Fast approval usually comes down to three things: verify the payer entity first, decide tax treatment separately, and send one invoice record with complete SEPA payment instructions.

Step 1: Verify the payer's business identity before you draft tax language#

Start by confirming the exact legal entity that will approve and pay. Under Article 226, your invoice needs the full name and address of both parties and, in relevant cases, the customer VAT identification number.

Check the VAT number in VIES as a point-in-time validation. Treat the result as valid or invalid at check time, and if VIES is inconclusive, pause and ask for billing-entity confirmation. Where needed, follow up through national authorities to confirm whether the VAT number is associated with that name and address.

Save the evidence in the same invoice record before you move on. Keep a dated VIES validation record plus the client's billing-entity confirmation by email or portal record. Use the invoice number as the anchor so the draft invoice and verification evidence stay traceable together. If the contract entity, PO entity, and billing contact do not match, do not send the invoice yet.

Step 2: Decide the VAT treatment separately from the identity check#

Keep tax treatment as its own decision. A validated business identity does not, by itself, determine the VAT outcome for the supply.

Use the same sequence each time. Confirm business versus consumer. Confirm whether the customer VAT ID is relevant for that invoice. Then decide VAT treatment and log the reason in your invoice notes or accounting memo.

If reverse charge is the verified outcome, do not reuse old wording until the jurisdiction review is complete. Confirm the exact invoice wording with the relevant adviser, official guidance, or source records before use. The requirement here is the "Reverse charge" mention where the customer is liable for VAT.

Keep OSS out unless it is actually relevant to cross-border supplies to consumers. For standard B2B corporate invoicing, do not add OSS language by default.

Step 3: Put payment instructions in one block AP can execute without follow-up#

Your payment block should be something AP can copy and use without a clarifying email. For SEPA flows, these fields help reduce avoidable processing delays.

| Field to show on the invoice | What to enter | Failure it helps prevent |

|---|---|---|

| Beneficiary name | Account-holder name exactly as shown by your receiving provider | Name-account mismatch warnings, including where verification-of-payee checks apply |

| IBAN | Verified account IBAN copied from provider details | Keying mistakes and avoidable routing friction after IBAN format or plausibility checks |

| Currency | EUR shown clearly in totals and payment section | Wrong-currency payment attempts and AP query holds |

| Remittance reference | One exact instruction, for example invoice number only, kept short | Unmatched incoming funds and slower reconciliation |

| Optional routing fields | BIC/SWIFT only when payer or route requires it | Back-and-forth on fields that are not always required |

Keep the remittance instruction singular and explicit. SCT supports up to 140 characters, and that field helps you match funds to invoice data. If you expect instant handling, only label it that way after both sides confirm that exact path supports SCT Inst.

Step 4: Run a hard go or no-go check before sending#

Do not send until the record is complete. Your send package should contain the final invoice, business-verification evidence, and the tax-treatment note for that invoice. Use this gate before you send:

- No-go if the payer legal entity is incomplete, inconsistent, or unverified.

- No-go if VAT treatment is undocumented or reverse-charge wording is not jurisdiction-checked.

- No-go if payment instructions are missing beneficiary name, IBAN, EUR, or one remittance reference.

- Go only when the invoice has a unique sequential invoice number and all supporting records are linked in one place.

Electronic and paper invoices are equivalent under EU rules, so the file can be fully digital. What matters is that you can quickly retrieve one complete, traceable invoice record when AP or tax controls ask for proof. Related: How to Create an Automated Email Welcome Sequence.

Before you send your next client invoice, run a quick structure check with the Free Invoice Generator. It can reduce reference and field errors that cause delays.

Choosing an Operations Partner, Not Just a Bank#

Your provider choice shapes whether incoming EUR payments turn into clean, matchable records or a pile of manual cleanup. Prioritize data quality over headline fees. If payer identity, remittance detail, or exports are weak, the real cost usually shows up later in delays and reconciliation drag.

A correctly sent payment can still create avoidable work if the sender name is missing, remittance text is unusable, or exports are too thin. A low transfer fee is not a real win if month-end means rebuilding who paid what.

Must haves first#

Start with operating basics, not marketing claims. These five checks help you gauge whether a provider will hold up in real use. Also check corridor coverage and legal perimeter for your payer mix, since SEPA-related legal protections are not uniform outside the EU/EEA.

- Stable EUR receiving details: your beneficiary name and IBAN should stay consistent so clients can save them in AP without repeated corrections.

- Payer and remittance visibility: you need sender identity and usable reference data, not just amount and date.

- Export completeness: statement exports must include fields you can match in your books.

- Escalation path for unclear transfers: when data is missing or ambiguous, you need a traceable support route.

- Transparent account review requirements: onboarding, review triggers, and document requests should be clear before volume grows.

Use name consistency as a practical gate. Verification of Payee applies to both standard and instant credit transfers, and the euro-area VoP deadline is 9 October 2025. If beneficiary naming is inconsistent across onboarding, app views, and statements, you may see payer warnings and AP follow-up.

Use remittance visibility as the second hard gate. Basic SCT carries one unstructured remittance field of 140 characters. Extended Remittance Information can support richer structured data and automatic reconciliation. If payer name or a usable reference is not visible in both the dashboard and exports, expect ongoing matching issues.

Use a scorecard, but do not let fees dominate it#

A scorecard helps only if it protects the non-negotiables. Score each provider from 0 to 2 on each line: 0 = weak or unclear, 1 = usable with manual work, 2 = strong and easy to operate.

| Capability | Priority | What you need to verify | Score |

|---|---|---|---|

| Stable EUR receiving details | Must have | Same beneficiary name and IBAN across account details, invoice instructions, and statement records | 0 to 2 |

| Payer name and reference visibility | Must have | Incoming transaction view shows sender identity and usable remittance text | 0 to 2 |

| Export completeness | Must have | Export includes date, amount, currency, payer, and reference fields you can actually match in your books | 0 to 2 |

| Escalation path | Must have | Clear support route for unclear or unmatched incoming credits | 0 to 2 |

| Account review transparency | Must have | Review and document requirements are explained before issues arise | 0 to 2 |

| Accounting integration | Nice to have | Reduces retyping and manual posting | 0 to 2 |

| Alerts or rules for incoming credits | Nice to have | Helps you catch and route exceptions faster | 0 to 2 |

No-go rule: if payer-reference visibility is weak, or export quality is weak, reject the provider even if the total score looks good. Also, do not treat any export as audit-ready until you validate field-level matching in your own books.

Tax and records fit#

Keep the tax check practical. If OSS is relevant, remember it is optional, and OSS returns are additional to your domestic VAT return. That means your provider needs to support reliable evidence retrieval, not just receipt confirmation.

OSS records must be kept for 10 years from the end of the year and made electronically available without delay when requested. Persistent failure can lead to exclusion from the scheme, so weak transaction evidence is an operations risk. For OSS, or any cross-border VAT path, verify the eligibility condition from official guidance, adviser notes, provider records, or source records before relying on it.

Pilot it before rollout#

Before routing all billing through one provider, test the full chain with a live payment. That is the fastest way to see whether your clean invoice instructions turn into usable records.

- Receive one real payment from a trusted client using your exact invoice payment block.

- Verify end-to-end matching by checking beneficiary details, payer identity, remittance visibility, and successful booking in your records.

- Finalize a written playbook for invoicing, reconciliation, and exception handling, including unmatched credits and escalation contacts for incomplete transfer data.

If the first live payment is hard to identify, export, and reconcile, scale will only amplify the problem.

If currency exposure is part of the picture too, see Foreign Exchange Risk for Freelancers Getting Paid Internationally.

The SEPA-to-Tax-Return Audit Trail: Your Defense Against Anxiety#

Treat each incoming payment as complete only when you can trace it from invoice to booking entry to return-support records. This is an operating standard, not legal advice, and it helps reduce cleanup later when payment detail is unclear.

Keep three linked records for every paid invoice#

One practical setup is one folder per paid invoice with three linked records: the final invoice, bank evidence, and proof of acceptance or delivery. Use that as your minimum working standard, not as a universal legal requirement.

Use a sortable naming pattern so retrieval stays fast, for example:

/Finance/2026/Income/ClientName/INV-2026-014/

You might keep files like:

2026-04-18_ClientName_INV-2026-014_invoice.pdf 2026-04-22_ClientName_INV-2026-014_bank-evidence.pdf 2026-04-20_ClientName_INV-2026-014_approval-email.pdf

For each record, you can keep:

- Invoice file: final sent version, invoice number, issue date, client name, amount, currency, and the payment details you provided.

- Bank evidence file: amount, currency, booking or value date, payer name when available, and remittance or reference text used for matching.

- Work-proof file: approval, acceptance, milestone signoff, portal confirmation, or delivery thread that ties payment to delivered work.

If your current view does not show full remittance text, capture an export or transaction PDF that preserves the full reference.

Post each receipt the same way every time#

Consistency matters more than speed here. Before you mark a payment as posted, check amount, currency, payer identity, and reference against that invoice folder. If anything is unclear, route it to an unmatched-income queue and hold posting until the match is defensible.

Once matched, post with consistent tags: invoice number, client, posting date, income category, and your internal project or tax labels. Keep those tags aligned across your bookkeeping tool and any ERP or AP workflow so the records stay usable later.

Know which setup you are actually running#

This is where people often overestimate how ready they are. Use the table below to call your current setup what it is.

| Maturity level | What you capture | What breaks | Operational effort | Audit/verification readiness |

|---|---|---|---|---|

| Ad hoc | Mixed files, screenshots, inbox search, no naming standard | Hard to prove what a credit covered | High | Weak |

| Partial | Invoices and bank records, but inconsistent proof or tagging | Ambiguous references trigger manual rework | Medium to high | Usable but fragile |

| Disciplined | Three linked records, consistent naming, consistent posting tags, monthly review | Issues are usually isolated early in unmatched-income | Medium upfront, lower ongoing | Strong |

If you are in the middle row, a practical upgrade is consistent naming and same-day bank-evidence capture.

Keep the compliance note jurisdiction-aware#

Build your archive to support your real filing path, but do not guess the rules. Verify the filing trigger, filing window, and record-retention rule from official guidance, adviser notes, provider records, or source records before you put them in the checklist.

This matters because payout compliance depends on your internal finance process, system dependencies including ERP or AP, and country-level tax requirements.

Run a monthly routine and keep a proof packet ready#

Monthly review is where the setup either holds together or falls apart. Run the same short routine every month so missing evidence does not accumulate.

- Confirm each incoming payment has all three linked records.

- Clear or document every item in

unmatched-income. - Reconcile paid invoices, bank activity, and bookkeeping totals.

- Store month-end exports in the same year-folder structure.

Consider keeping a proof-of-income packet ready with items like:

- recent account statements

- year-to-date invoice summary

- reconciled income totals from your books

- supporting folders for larger or unusual items

- a short note for pending, refunded, unmatched, or split payments

If you automate reminders or summaries, make sure the automation feeds this archive rather than replacing it. Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe can help if it improves record quality, not just speed.

If you want a broader cashflow angle, The FIRE Movement for Freelancers Who Need Reliable Cashflow may also help.

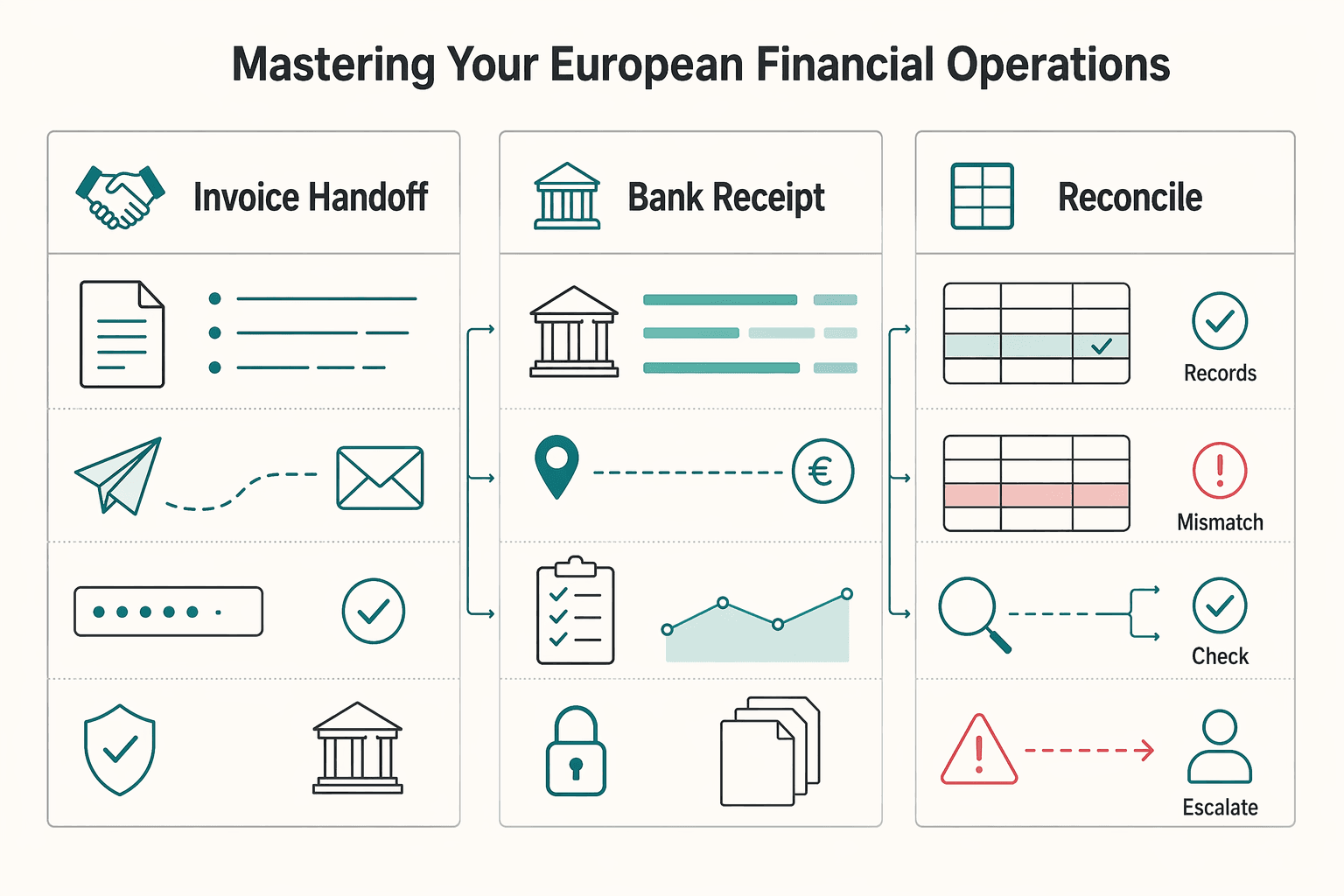

From Transfer to System: Mastering Your European Financial Operations#

The core shift is simple: stop treating each payment as a one-off event. Use one repeatable process to invoice cleanly, choose the right SEPA rail, reconcile accurately, and archive the evidence.

Start with invoice inputs you can reconcile later. Send an electronic invoice with exact payee details: beneficiary name, IBAN, currency, and one copy-ready payment reference. Keep the reference short and unique. SCT supports up to 140 characters of remittance information, and that field helps match incoming funds to invoices. Before sending, confirm the client will pay in EUR from an account in SEPA, since SCT is for euro transfers between accounts located in SEPA.

Choose the rail based on urgency, then set expectations. Use SCT for routine payments and plan around crediting the beneficiary PSP within one Banking Business Day. Use SCT Inst only when urgency is real and both PSPs or channels confirm support. If the payer bank applies Verification of Payee, mismatched beneficiary details can trigger a discrepancy warning before initiation and may delay payment until corrected.

| Workflow point | Where a transaction-only approach fails | System control to apply | Operational result |

|---|---|---|---|

| Invoice handoff | Client edits or improvises payment reference | Require one exact invoice reference | Faster matching, fewer clarification threads |

| Bank receipt capture | Payer or remittance detail is lost in a truncated dashboard view | Export full transaction evidence the same day | Stronger audit trail, less month-end rework |

| Reconciliation decision | Unclear credits are forced into the books | Route unresolved items to an internal unmatched-income queue until verified | Fewer misposts and cleaner return-support records |

From new-client onboarding to first reconciliation, run this sequence every time:

- Confirm billing entity details and that payment will be sent in EUR via SCT.

- Issue the invoice with exact payee details and one required reference.

- If timing is critical, confirm SCT Inst support on both sides. Otherwise default to SCT.

- On receipt, match amount, currency, payer detail, booking or value date, and remittance text before marking the invoice paid.

- If any field does not match, move the payment to an internal

unmatched-incomequeue and hold posting while you keep client communication and bank evidence together. - Archive the three linked records: final invoice, bank evidence, and approval or delivery proof.

Once this process is stable in day-to-day work, Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe is an optional next step. Use it to reduce manual capture without hiding exceptions.

If you want a deeper dive, read Separating Business and Personal Finances: A Important Step for LLCs.

If you want one operational setup for invoicing, payouts, and audit-ready records, review Gruv for Freelancers and confirm fit for your payment corridors.

Frequently Asked Questions

Should you ask your client to use SEPA or SWIFT?

Use the rail that both the payer and your receiving setup can support for that specific invoice. Verify the exact route, expected fees, conversion handling, and payment instructions before sending the invoice. Use exact beneficiary and remittance details, and validate the setup before a first large transfer.

How should you handle U.S. tax issues when European clients pay you this way?

Treat the payment rail as an operations choice, not a tax shortcut. If you are a U.S. taxpayer, review your Form 1040 or 1040-SR obligations separately. Publication 17 is guidance and does not replace the law.

Do you need a company to receive these payments?

Do not assume you do or do not need a company. Confirm with your bank or provider which payee setup your account permits before you invoice. Keep the name and payment details consistent across your contract, invoice, and beneficiary instructions.

Are these transfers always fast and cheap?

Not necessarily. Do not assume timing or total cost from the label alone. Confirm expected fees, conversion handling, and settlement flow with your provider before sending or requesting a large payment. If the invoice is material, run a small live test and log the invoiced amount, received amount, currency, booking date, and any deductions.

Why does the VAT reverse-charge note matter?

Use reverse-charge wording only when your adviser confirms it applies to that transaction in that jurisdiction. Check the client legal name, tax details, and your local registration threshold and filing deadline requirements before the first invoice. Keep VAT treatment separate from rail choice.

What is the best way to store records after payment arrives?

Keep one evidence pack per paid invoice with the final invoice, bank transaction evidence, and approval or delivery proof. Capture the full bank record, match the amount, currency, payer, and remittance, then archive all three records together. If anything does not match, hold posting and keep it in unmatched-income until resolved.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bea.gov/resources/methodologies/nipa-handbook/pdf/al...trusted

- ecb.europa.eu/paym/retail/instant_payments/html/instant_pa...trusted

- ecb.europa.eu/paym/retail/sepa/html/index.en.htmltrusted

- eur-lex.europa.eu/eli/reg/2024/886/oj/engtrusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- federalregister.gov/documents/2021/01/07/2020-29274/independent-...trusted

- govinfo.gov/content/pkg/CFR-2016-title39-vol1/html/CFR-2...trusted

- irs.gov/pub/irs-pdf/p17.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

How to Create an Automated Email Welcome Sequence

Treat your automated email welcome sequence like a first-week system: one trigger, one path, one primary call to action (CTA), and a measurement loop you can run without guesswork. If you're a business-of-one, the job is to turn "marketing" into something you can run and improve without relying on motivation.