Quick Answer

Xero can work well for freelancers and small businesses when you run it as a cashflow control system, not just accounting software. The article recommends a risk-first workflow: standardize quote-to-invoice steps, run weekly reminders and exception handling, reconcile quickly, and separate bookkeeping from filing checks. If delays or cross-border complexity keep growing, add tools only when they close a clear control gap.

Stop Chasing Features and Build a Get-Paid System That Actually Protects Cashflow#

Treat Xero for freelancers as a get-paid system, not a feature checklist. Most freelancers do not struggle because their accounting software lacks features. They struggle when payments arrive late or when the process for delays, disputes, or partial payments is unclear. In a business of one, your job is to make cash collection a repeatable system, not a personality trait.

Late payment is still a live operating problem for small businesses, and it puts immediate pressure on cashflow planning. In a recent U.S. data point from Xero, payments averaged 7.8 days late. That kind of delay can trigger avoidable decisions. You might push your own bills, use reserves too early, or accept weaker terms on the next client just to stabilize income.

| If you chase features | If you run a get-paid system |

|---|---|

| You compare tools by screens and add-ons | You define terms, reminders, escalation, and records before sending invoices |

| You treat invoicing as a one-time task | You run invoicing, controls, and reconciliation as one recurring loop |

| You react to late payers case by case | You follow clear escalation paths and protect cashflow consistently |

Use this as your Xero review lens: cashflow protection first, features second. This is not a product tour. It is a reusable playbook for invoicing and financial management in Xero.

Use these safe defaults:

- Invoicing discipline: set clear terms, payment options, and reminder timing.

- Control points: assign ownership for approvals, follow-up, and escalation.

- Reconciliation habits: close exceptions fast so records match cleared funds.

- Cross-border caveats: spot where market or program rules change your next step.

If a new client asks for open-ended payment timing, you do not improvise. You run the same checklist, lock terms before work starts, and know when to pause delivery.

Where rules vary by country or program, this article flags uncertainty and shows you how to confirm the final requirement with official guidance before you act.

Build the Mental Model Before You Touch Settings#

Build your get-paid model first, then configure Xero so every setting protects cashflow. Before you touch Xero Invoicing, map your operating flow. The goal is to make Xero enforce your process, not become another accounting software setup project.

| Model part | What it means in practice | What you decide before changing settings |

|---|---|---|

| Get paid system | One flow from quote to cleared funds to reconciled records | Who owns each step and what proof closes each step |

| Cashflow protection | Prevent delayed payment and reconciliation blind spots in Xero Dashboard | Your reminder path, dispute response, and exception review cadence |

| Operational control | Repeatable weekly cadence with owner, due date, and escalation rule | What triggers follow up, pause, or escalation |

| Compliance safe workflow | Collect only required data, keep audit-ready records, and separate bookkeeping from filing duties | What you store, how long you keep it, and when to verify with IRS or FinCEN guidance |

Use a simple flow: quote accepted, invoice sent, funds cleared, transactions reconciled. Xero supports this directly by letting you turn a quote into an invoice quickly. It also reinforces control through dashboard visibility and frequent reconciliation. In any Xero review, score the tool on this end-to-end flow, not on feature count.

Run this weekly checklist:

- Confirm each open invoice has a clear owner and next action.

- Review Xero Dashboard deadlines before you start new delivery work.

- Reconcile often so your financial management view reflects cleared reality, not assumptions.

- Record client replies and payment proof in the same workflow so invoicing and reconciliation stay connected.

Imagine a client approves your quote, then asks for open-ended payment timing after work starts. Your model should force a clean decision. Hold scope, restate agreed terms, and escalate using your preset rule instead of improvising under pressure.

Keep the compliance boundary clear. Use Xero to keep clean records, maintain them as long as needed to support what you report on returns, and treat filing obligations as a separate check based on your facts. FBAR (FinCEN Form 114) and Form 8938 are separate requirements when their thresholds apply. If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

What Is the Minimum Weekly Workflow in Xero to Protect Cashflow?#

Run one fixed weekly Xero cycle: check the dashboard, run reminders and payment options, then update overdue dates for your short-term cash flow projection. You already built the model. Now run it the same way each week so Xero becomes a control system, not just a ledger.

Use this as your operating baseline before you take new client work:

| Weekly step | What to check | Required output |

|---|---|---|

| Review receivables and payables | Dashboard snapshot of bank position, invoices owed, and bills due | One action owner per open item |

| Align invoice terms | Due terms and payment request language in invoices | Matching terms from agreement to invoice |

| Run reminders and payment options check | Reminder rules for due and overdue invoices, plus invoice payment methods | Active reminder ladder and valid pay-now path |

| Update overdue assumptions and open issues | Expected payment dates for overdue invoices and planned payment dates for overdue bills | Clear next action and owner for each open item |

For reminders, configure a ladder that fits your client mix. Xero supports up to five reminder emails, and you can trigger them around due and overdue states. Keep it tight. You want timely prompts, not noise.

For payment flow, verify that each invoice shows the right way to pay. When you connect payment services, Xero can add a Pay Now button to online invoices, and you can attach multiple payment services. This helps remove friction in how clients pay and supports a cleaner weekly review.

Build one manual exception queue and close every item with evidence:

- Payment confirmation recorded.

- Client reply logged when timing changes.

- Adjusted invoice issued when scope or amount changes.

- Next action and owner updated when status changes.

If a client pays part of an invoice and questions the rest, do not improvise. Put it into the same queue, assign an owner, set the next action, and close it only when records, communication, and balance all agree.

Last step each week: update expected payment dates on overdue invoices and planned payment dates on overdue bills. That one habit improves short-term cash flow projection accuracy and gives you a cleaner signal for decisions.

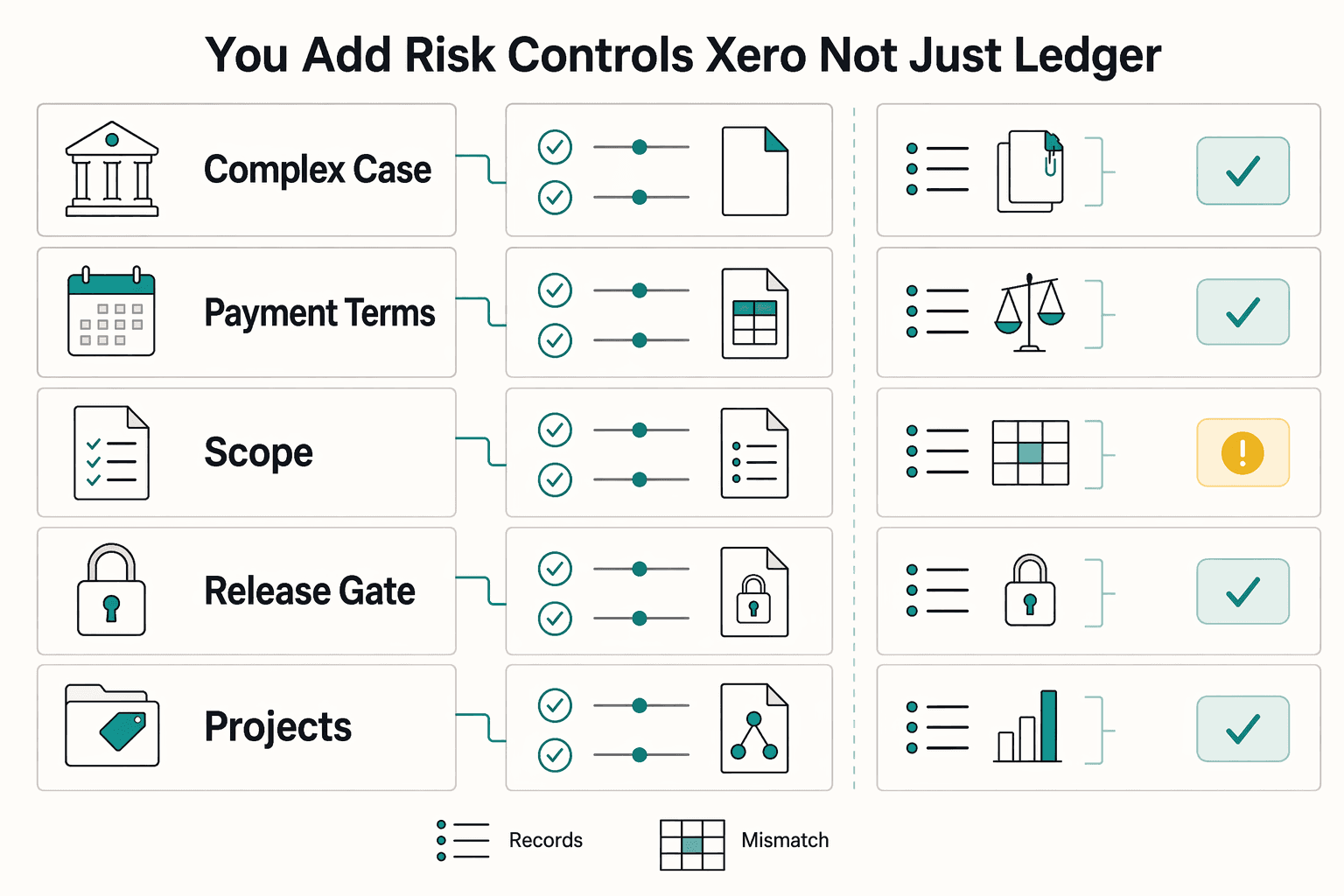

How Do You Add Risk Controls So Xero Is Not Just a Ledger After the Fact?#

Add controls before you send an invoice, then use dispute evidence and app checks so Xero helps earlier, not just after the fact. Your weekly cycle keeps you honest. Controls keep bad inputs from entering the system and give you a playbook when a client pushes back.

| Control point | What to do | Applies to |

|---|---|---|

| Legal client entity name | Confirm the legal client entity name matches the buyer that will pay | Acceptance controls |

| Payment terms | Set agreed payment terms in the quote, then record accepted status before invoicing | Acceptance controls |

| Scope | Tie scope to concrete deliverables so billing lines and work proof match | Acceptance controls |

| Invoice approval | Fix errors before approval; once an invoice is approved, Xero locks financial fields | Acceptance controls |

| Projects | Create invoices only from accepted quotes | If you use Projects |

| Milestones | Break work into smaller milestones | High-risk clients |

| Due windows | Use shorter due windows that match your cash needs | High-risk clients |

| Pause rule | Define a pause rule for missed commitments and log it in your invoicing notes | High-risk clients |

| Escalation owner | Assign one owner for escalation so follow-up does not drift | High-risk clients |

Start with acceptance controls in Xero quote templates and Xero Invoicing:

- Confirm the legal client entity name matches the buyer that will pay.

- Set agreed payment terms in the quote, then record accepted status before invoicing.

- Tie scope to concrete deliverables so billing lines and work proof match.

- Treat approval as a control point. Once an invoice is approved, Xero locks financial fields, so fix errors before approval, not after.

- If you use Projects, create invoices only from accepted quotes so the handoff stays clean.

For high-risk clients, add a payment risk checkpoint before work continues:

- Break work into smaller milestones.

- Use shorter due windows that match your cash needs.

- Define a pause rule for missed commitments and log it in your invoicing notes.

- Assign one owner for escalation so follow-up does not drift.

Build a dispute SOP so you can produce an evidence packet fast. Pull the accepted quote, invoice history, communication notes, and signed delivery proof into one bundle.

Keep notes complete, attach key files, and mark files for online visibility when needed. Respond promptly and state the exact issue you are resolving.

Imagine a client challenges one line item after delivery. You do not debate from memory. Open the packet, confirm what they accepted, show the documented scope, and present the next step in writing.

Treat the Xero App Store as a risk-control decision, not a feature hunt. Xero reviews listed apps, but listing does not guarantee fit or performance for your workflow. In your review process, require each app to reduce one specific failure mode in invoicing or financial management before you adopt it.

When you compare accounting software options like QuickBooks, compare control depth, not brand claims. QuickBooks supports reminder scheduling up to 90 days before or after due date. Use concrete control checks like that to decide whether Xero still meets your risk standard.

Want a quick next step? Try the free invoice generator.

When Do Cross-Border and Tax Rules Change the Setup?#

Cross-border work can change your setup fast, even if your day-to-day invoicing inside Xero looks the same. Keep bookkeeping execution inside Xero, and run filing and reporting checks outside the tool based on your facts.

For daily operations, use Xero US for invoicing, reconciliation, and cashflow tracking. For compliance, run a separate check and confirm with official IRS and FinCEN guidance.

| Decision point | Bookkeeping action in Xero | Filing check outside Xero |

|---|---|---|

| Foreign client payment lands | Record invoice, payment status, and reconcile the transaction | Check whether foreign account reporting rules may now apply |

| Foreign financial accounts grow | Keep account records audit-ready | Check FBAR trigger and filing requirements |

| Foreign financial assets exist | Maintain clear support records | Check FATCA Form 8938 rules and filer-specific thresholds |

FBAR is filed on FinCEN Form 114 when aggregate foreign financial accounts exceed $10,000 at any time during the year. Form 8938 generally starts at $50,000 for certain U.S. taxpayers, but thresholds can be higher in some cases. These are separate obligations, and Form 8938 does not replace FBAR. If you do not have to file an income tax return for the year, you do not file Form 8938 for that year.

Use one consistent records package for every global client so your bookkeeping supports faster review:

- Final invoice and current payment status.

- Reconciliation evidence that ties cleared funds to the invoice.

- Client entity details and payment account context.

- Notes on cross-border facts you still need to confirm with a qualified tax advisor.

Imagine you onboard a client who pays into an overseas account. Keep the same invoicing and reconciliation rhythm inside Xero, then run the IRS and FinCEN check before deadlines instead of cleaning it up under pressure later. If you need payment rail setup details, see How to Connect Wise to Xero.

Is Xero Alone Enough or Should You Pair It With Payment Infrastructure?#

Start with Xero invoicing, add selected apps when control gaps appear, and move to modular payment infrastructure only when risk outgrows both. You already separated bookkeeping from filing obligations. Apply the same discipline here so your setup stays simple until your risk proves you need more.

| Tier | Stack | When it is enough | Trigger to upgrade |

|---|---|---|---|

| Tier 1 | Xero-only baseline | You can run invoicing, reminders, and payment options with a simple operating setup | Repeated late payments, visibility gaps, or manual rework keep growing |

| Tier 2 | Xero plus selected apps from Xero App Store | An app removes one clear failure mode in collections, reconciliation, or reporting | App overlap grows, audit trail breaks, or payout complexity exceeds app fit |

| Tier 3 | Xero plus modular payment infrastructure | You need tighter payout control, better routing, or stronger dispute handling | Continue only if controls improve without adding blind spots |

For Tier 1, Xero gives you a practical baseline: customizable invoices, more ways for clients to pay, and automatic reminders. For Tier 2, treat apps as risk controls, not feature clutter. Xero reviews App Store listings, but it does not guarantee suitability, so test each app against one defined risk.

Use objective upgrade triggers:

- Delays repeat even with reminders and clear terms.

- Payout paths across tools create reconciliation friction.

- Dispute volume rises and evidence prep slows delivery.

- Your current reporting view no longer gives a reliable operating picture.

Keep vendor narratives in perspective when you evaluate Xero. Feature breadth in Xero or QuickBooks does not replace compliance gates, audit trails, or payout-risk controls.

If you consider switching accounting software, treat migration as a high-impact project. Conversion guidance warns that some data types may not transfer, and timelines can vary.

Before you commit, run an unknowns checklist:

- Promo price versus post-promo price.

- Monthly feature caps by plan tier (for example, lower-tier invoice and bill limits).

- Add-on, usage, and payment fees outside base plan pricing.

- Plan fit against your current size, projected growth, and day-to-day needs.

- Migration data gaps and remediation work if you ever move platforms.

Imagine you add more international clients and start tracking payouts across multiple tools. Community discussions in r/Bookkeeping can surface that friction, including bolt-on fatigue. Treat those discussions as early warning signals, then validate with your own workflow tests before you upgrade tiers.

Roll Out a 30-Day Playbook You Can Reuse on Every Client#

Run a repeatable four-week operating cadence in Xero to move clients from approved quotes toward cleared cash and reconciled records with less guesswork. At this point you have a stack rule and a control model. Turn it into a rollout cadence you can reuse.

| Week | Focus | Actions | Exit criteria |

|---|---|---|---|

| 1 | Implementation baseline | Standardize your quote-to-invoice workflow, set invoice terms, and assign an owner for send, reminder, escalation, and reconciliation tasks. Convert quotes to invoices once you deliver the quoted work. Configure automatic reminders for due and overdue states, using up to five reminder slots. | Every new client follows one quote and invoicing path, with one named owner per step. |

| 2 | Controls and exceptions | Build one exception board and feed it from Xero dashboard signals, especially overdue balances from the invoices owed widget. Track disputed and partially paid invoices in the same queue, with next action and due date on each item. | No open exception lacks an owner, next action, or target date. |

| 3 | Reconciliation hardening | Close open reconciliation exceptions in Xero. Treat bank reconciliation as a control step where you confirm each bank transaction appears correctly in your accounting records. Log recurring failure patterns and attach one corrective action for each pattern. | Reconciliation stays current and you can explain repeat failures and fixes quickly. |

| 4 | Fit and extension review | Review whether your current setup still protects cash flow or whether new constraints justify extensions beyond Xero App Store integrations. When you evaluate extensions, require evidence that an app improves control, because you still must assess app quality and suitability yourself. If payment friction keeps growing, plan the next layer deliberately, for example How to Connect Wise to Xero. | You keep, adjust, or extend the stack based on risk, not feature pressure. |

Imagine a client accepts your scope, pays part of the invoice, then goes quiet. Your board should trigger reminders, flag escalation ownership, and force reconciliation follow-through so your records and your cash view stay aligned.

Use this weekly Xero checklist on every active client:

- Send: issue invoices from approved quotes and confirm terms.

- Remind: run the reminder sequence for due and overdue invoices.

- Escalate: move unresolved overdue, disputed, or partial payments to owner-led action.

- Reconcile: clear reconciliation exceptions and record root causes.

- Archive evidence: store payment confirmations, client replies, and adjustment notes.

Run the System With Discipline and Upgrade Only When Risk Justifies It#

Treat Xero as your system for collections and control, then add complexity only when a clear risk gap persists. The point here is not to rank features. It is to build a get-paid system that holds up when clients delay, dispute, or go quiet.

Keep it simple. Protect cashflow through repeatable invoicing, clean bookkeeping, and reliable cash visibility.

Keep your safe default tight#

Run the core loop before you touch new tools:

| Core step | Article guidance |

|---|---|

| Check Xero Dashboard | Review outstanding and overdue invoices and payments so you see what is ahead |

| Act on exceptions fast | So small issues do not become overdue surprises |

| Use invoice reminders in Xero Invoicing | Follow up outstanding invoices and support on-time payment |

| Reconcile bank transactions regularly | Keep dashboard and snapshot views current |

- Start at Xero Dashboard so you can see outstanding and overdue invoices and payments before they surprise you.

- Clear exceptions while they are still small.

- Use invoice reminders in Xero Invoicing to keep follow-up moving.

- Reconcile bank transactions regularly so dashboard and snapshot views stay current.

If a client starts paying slower and you see overdue items grow while your reconciliation queue slips, do not jump platforms first. Tighten your reminder sequence, clean up exception handling, and verify that your controls are actually running on schedule.

Add complexity only when evidence demands it#

Use integrations when they close a specific control gap, not because they look efficient in a demo. Xero App Store listings can help you expand workflows, but you still must assess fit and risk yourself. Hold every add-on to the same bar: clearer control, less manual leakage, better visibility.

| Decision step | Article guidance |

|---|---|

| Review your current process | Review it end to end |

| Identify weak controls | Check send, remind, escalate, reconcile, or evidence capture |

| Re-run your playbook | Run it against those weak points |

| Upgrade only if risk still outgrows your current Xero setup | Do this only after re-running the playbook |

If you evaluate QuickBooks or any other accounting software, keep the same comparison lens. Judge operational control depth, not feature volume. Also keep commercial assumptions current, because pricing and promotions can change over time.

Before you change platforms, run one last operator checklist in order:

- Review your current process end to end.

- Identify weak controls in send, remind, escalate, reconcile, or evidence capture.

- Re-run your playbook against those weak points.

- Upgrade only if risk still outgrows your current Xero setup.

Frequently Asked Questions

Is Xero enough to help freelancers get paid on time or does it mostly track bookkeeping after payment events?

Xero can support collections if you run it like an operating loop, not a receipt drawer. Xero Invoicing supports reminders and connected payment services that let clients pay directly from emailed invoices. The leverage comes from your workflow: clear terms, consistent reminders, and fast exception closeout.

What is the minimum weekly workflow in Xero that protects cashflow without creating admin overload?

Block one weekly session and keep the sequence unchanged. Start with overdue invoices and upcoming bills, then clear reconciliation exceptions, then run reminders, then escalate disputed or partially paid items. The "minimum" is not a shorter list. It is a list you actually run every week.

How should freelancers configure reminders, payment options, and bill scheduling in Xero to reduce late payments?

Turn on invoice reminders so Xero sends nudges when due dates approach and after clients miss due dates. Connect an online payment service so invoices include a Pay Now action when you email them. Use repeating bill templates for predictable costs so payables stay on schedule while you focus on collections.

When should a freelancer use Xero alone versus pairing it with additional payment infrastructure for cross-border work?

Use Xero alone when your reminder flow, payment collection, and reconciliation stay stable. Add payment infrastructure when cross-border routes create repeated delays, exceptions, or weak visibility that your current setup cannot control. If you test additional apps, run your own suitability check before rollout.

What key details are still unknown before choosing Xero, including pricing tiers and feature limits?

Start with constraints, not marketing copy. Xero materials show plans from $29 per month, and Xero US pricing notes that Early plan invoice limits apply to both approving and sending invoices. Also verify add-on costs, payment-service fees, and plan-level caps that can change unit economics as you scale.

How should freelancers compare Xero and QuickBooks when payment risk control is the priority?

Use one checklist and score both tools against it. QuickBooks comparison content frames evaluation around features, pricing plans, and add-ons across both products, but feature count alone will not protect cashflow. Compare reminder control, exception handling clarity, and reconciliation reliability for your real client mix.

What tax and reporting areas should US freelancers verify with IRS or FinCEN before assuming their setup is complete?

Treat this as two separate tracks: bookkeeping execution and filing obligations. The IRS states that gig workers generally must file a return when net self-employment earnings reach $400 or more, and IRS FBAR guidance points to a $10,000 aggregate foreign-account threshold for potential FinCEN Form 114 filing. Form 8938 does not replace FBAR, so confirm both tracks directly with IRS and FinCEN rules for your facts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

Connect Wise to Xero Without Reconciliation Surprises

**Short answer:** To connect Wise to Xero without reconciliation surprises, first confirm you mean **Wise** rather than **ConnectWise**, connect the correct **Wise Business** profile to the correct **Xero** organisation, document where each active currency should appear in Xero, and test one real transaction before you turn on more features.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.