Quick Answer

Start with a per-payee decision sequence, not a standalone threshold lookup. For the keyword "1099 filing threshold calculator platform required file contractor," the reliable approach is to confirm the form path first (for example Form 1099-NEC vs Form 1099-K), then test threshold logic, and output file, do not file, or escalate. If records conflict or documentation is incomplete, route to review and preserve evidence rather than forcing an automated result.

How a 1099 filing threshold calculator supports platform contractor decisions#

If you own compliance, legal, finance, or risk for a platform, the question is not, "what is the general 1099 threshold?" It is this: for this payee, with this payment flow and this documentation, are you required to file, not required to file, or unable to decide yet without review?

That is the standard here. The goal is a repeatable per-payee decision that ends in file, do not file, or escalate, with enough evidence attached that someone else can retrace the call later. In practice, that means you do not stop at a dollar amount. You also need the likely form family, the payee's documentation status, and a record of what was missing or disputed if a case moves to escalation.

The scope here is U.S. information return logic for platform operations, especially where teams are sorting between Form 1099-NEC, Form 1099-K, and Form 1099-MISC. Those forms follow different reporting paths, and it is easy to get to the wrong answer if you start with a threshold before you confirm the payment path. A contractor services payment that points toward Nonemployee Compensation is not the same as a goods or services payment reported through an app, marketplace, or card network.

You should also assume threshold summaries can drift faster than internal controls. Secondary sources have described changes tied to the One Big Beautiful Bill Act. Avalara says it became law on July 4, 2025, including a reported return of the Form 1099-K threshold to $20,000 and 200 transactions and a reported $2,000 threshold for Form 1099-NEC and Form 1099-MISC.

Another secondary source says the $2,000 change starts in 2026 and is adjusted for inflation in 2027. Those are useful signals, but they are not a substitute for current IRS primary instructions. If your calculator or rules engine relies on threshold numbers alone, or only on secondary summaries, it can produce confident but wrong output.

That is why this article treats incomplete facts as a first-class outcome, not something to bury. If payee documentation is incomplete or inconsistent, or your payment records conflict with how the platform actually facilitated the transaction, the right answer may be escalate until someone resolves the mismatch.

The through-line is simple: decide per payee, lock the form logic before the threshold logic, and preserve the evidence behind the call. Do that, and you reduce both under-filing risk and unnecessary filing noise.

Define what this calculator must decide#

This calculator should decide information-return filing duty per payee, not estimate self-employment tax. It should return whether filing is required, which form family is likely in scope or unresolved, and whether the facts are strong enough to automate.

| Output | What it shows |

|---|---|

| Required form / unresolved form family | Which form family is likely in scope, or that it is unresolved |

| Filing channel | The filing channel selected by policy |

| Confidence level | Whether the facts are strong enough to automate |

| Escalation reason | Missing, conflicting, or stale facts |

Use Schedule SE (Form 1040) only as a boundary marker. The IRS says Schedule SE is used to figure tax due on net self-employment earnings, and its self-employment-tax references are about Social Security and Medicare taxes. IRS Topic 554 also notes self-employment tax is usually due at $400 or more and generally applies to 92.35% of net earnings. Those Schedule SE concepts are not 1099 filing thresholds.

Define Nonemployee Compensation operationally as contractor-service payments that may be reportable when IRS information-return filing conditions are met. Return those outputs as structured fields, not a single yes/no.

For Form 1099-NEC and Form 1099-MISC logic, anchor rules to current IRS primary instructions, including the Instructions for Forms 1099-MISC and 1099-NEC. If a secondary summary conflicts with IRS primary instructions, return verification required, attach the conflict, and route the payee for review.

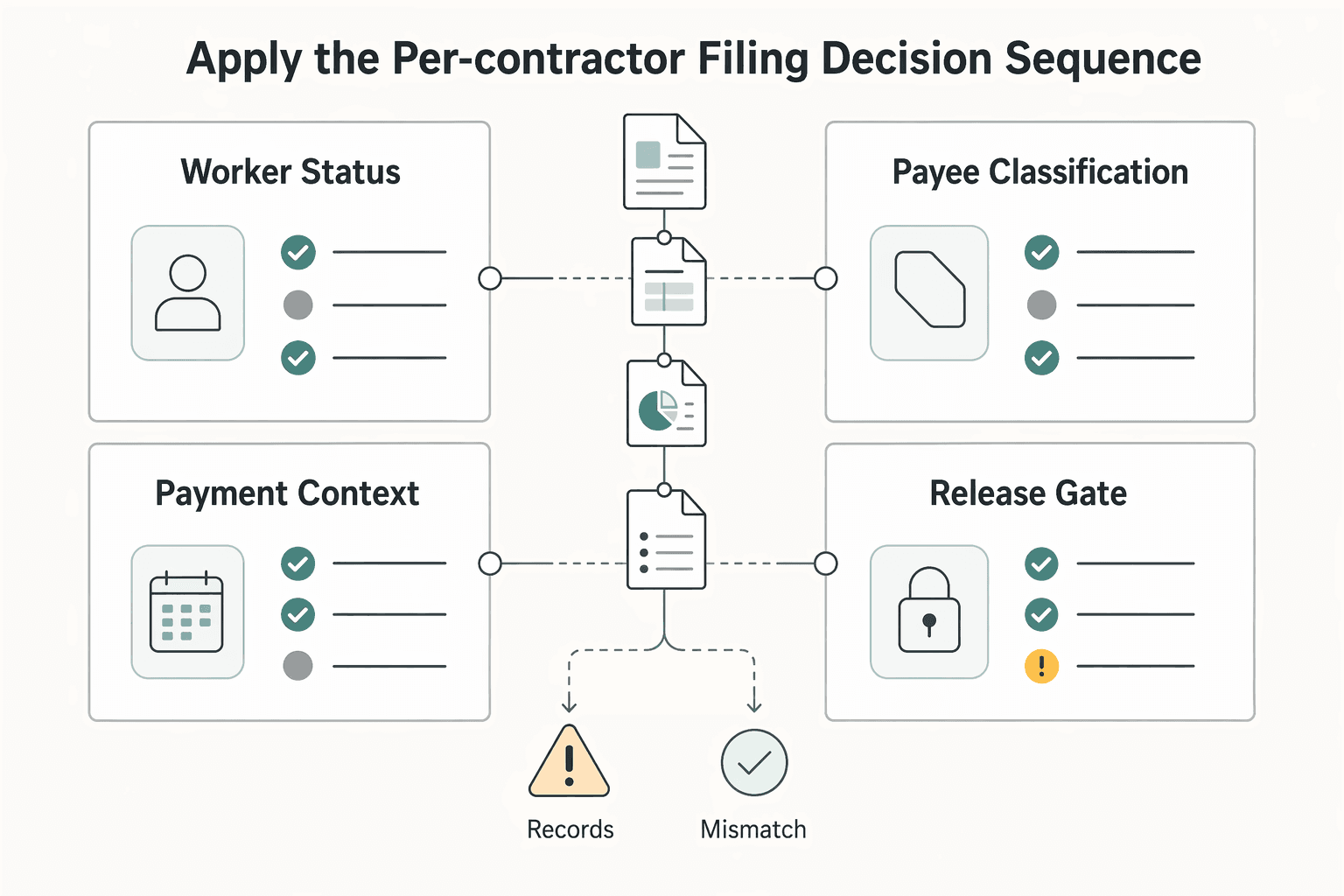

Apply the per-contractor filing decision sequence#

Use a fixed per-contractor sequence, and treat any unclear check as escalate. Do not jump from payment total to a filing answer.

Run four checks in order, with evidence captured for each one:

| Check | What to confirm | Escalate when |

|---|---|---|

| Worker status | The payee is treated as an independent contractor for this payment stream | Status is missing, conflicting, or recently changed |

| Payment context | The payment belongs in the reporting path your team is evaluating | Purpose or scope is unclear |

| Payee classification | Payee profile is consistent across your records, including W-9 data | Entity/tax profile is missing, stale, or contradictory |

| Threshold gate | The threshold logic for the selected form path is applied consistently | Rule input or threshold logic cannot be verified internally |

Keep escalation as a real outcome, not an exception. If one required check is weak, return escalate, log the missing or conflicting fact, and preserve the evidence trail.

Treat W-9 and 1099 handling as a core control, not a checkbox. Knowing when to use each matters, and mishandling can create penalty risk. Record who approved the decision, when they approved it, and which rule/source version the case used so the result is reproducible later.

For a step-by-step walkthrough, see 1099-K Reporting Threshold After the IRS Delay: Control Updates for Platform Operators.

Separate form selection before threshold logic#

Lock the form family before you run any threshold test. If form selection is wrong, the threshold output can still look precise and still be wrong.

In the referenced workflow, the selected form type must be configured before 1099 amounts and statuses are generated. Use the same control in your calculator: do not evaluate thresholds until the form path is set and evidenced.

| Form family | Payment flow to test first | Filer path to test first | Common misclassification risk |

|---|---|---|---|

| Form 1099-NEC | Direct payer settlement path | Direct payer branch | Teams jump to NEC based on worker label without confirming settlement flow |

| Form 1099-K | Settlement through a third party payment organization | Payment network or marketplace branch | Teams keep direct-payer logic even when settlement was handled by a network layer |

| Form 1099-MISC | Specific MISC category path | Category-specific direct payer branch | Teams use MISC as a fallback bucket when NEC/K data is incomplete |

Marketplace facilitation is where this breaks most often. Even if your platform sources the work or sets terms, reporting logic can shift when settlement runs through a third party payment organization; the IRS notes these include many popular payment apps and online marketplaces.

Form-first control also matters because 1099-K thresholds in the cited IRS update follow a different timeline: the new $600 requirement was delayed for tax year 2023, the prior standard remained over $20,000 and over 200 transactions for 2023 and earlier in that announcement, and the IRS said it planned $5,000 for 2024 as a phase-in. Wrong-form testing creates false confidence fast when timelines differ by form family.

Keep adjacent forms as classification context, not threshold outcomes at this step. If your record shows conflicting intake or classification signals across Form W-9, Form W-8, Form W-2, or Form 1042-S, stop the 1099 threshold test and escalate for review.

Store the exact form variant, not just "1099 required." In the referenced workflow, 1099-MISC support is limited to Box 6, which is a practical reminder that broad labels hide decision risk.

For a broader look at platform 1099 rules, thresholds, and deadlines, see 1099 Contractor Payment Guide for Platforms: Rules Thresholds and Filing Deadlines.

Build the evidence pack your auditors will ask for#

Your process is only audit-ready if each payee decision can be reconstructed later without guesswork. Keep one compact per-payee record that shows what you decided, why, and what evidence supported it.

As an internal control baseline, keep these items together for each payee and tax year:

| Record item | What it should show |

|---|---|

| Tax form artifact | The collected Form W-9 or Form W-8 image/status and timing |

| Payment ledger extract | The transaction evidence used for the threshold and form-path decision |

| Classification rationale | A short note on payee type, payment flow, chosen form family, and any escalation |

| Final filing outcome | Filed / did-not-file / escalated decision, with reviewer and date |

Keep your source discipline with the decision record. If your team uses Federal Register material, treat FederalRegister.gov as informational and verify legal research against an official edition; store the corresponding govinfo PDF as the record copy. In your rule snapshot, save the document identifier, effective date, and access date so you can show exactly which rule set was active when the decision was made. A simple example of this pattern is preserving a citation such as TD 9998 with its stated effective date, August 26, 2024.

Run a monthly exception review so issues surface before filing season:

- missing Form W-9 or Form W-8 records

- conflicting payee type across systems

- manual overrides without reviewer signoff

If these exceptions persist, escalate early rather than forcing a filing decision.

Meet the electronic filing requirement without last-minute fire drills#

Treat the electronic filing requirement as a system design input, not a year-end task. If your filing population can span Form 1099-NEC, Form 1042-S, and Form W-2, design for channel readiness, validation, and resubmission controls alongside per-payee threshold decisions.

Do not anchor controls to stale or non-authoritative summaries. A secondary legal commentary says IRS final regulations were published on February 23, 2023, so assumptions should be re-verified against current primary IRS instructions and publications. The IRS also states an Audit Technique Guide is not an official pronouncement of law and says technical accuracy is not guaranteed after the revision date, shown in the cited excerpt as 4/19/2021.

Lock the filing sequence before peak season#

Define the sequence and owners before volume spikes. Without a fixed order, teams improvise under deadline and increase rejection and duplicate-submission risk.

| Stage | Key control |

|---|---|

| Data freeze | Cutoff timestamp and named owner |

| Pre-file validation | Required payee records, form selection, and tax-year totals |

| Transmission | Selected channel |

| Rejection handling | Queue, SLA, and decision owner |

| Correction cycle | Accepted returns later found to be wrong |

| Final reconciliation | Filed output, acknowledgments, and internal ledger |

Work those stages in that order. Keep one strict control: transmitted batches must tie to the approved frozen population count and control total. If either changes after freeze, open a new batch instead of editing the old one.

Control retries so they do not become duplicate filings#

Preventing duplicates should be explicit, not implied. Use an idempotent batch key with tax year, form type, payer, and version, and preserve status history for every retry.

Set ownership boundaries clearly. Tax ops owns readiness, reject-correct decisions, and amendments; engineering owns transport success, message capture, and retry behavior. If manual resubmission and automated retry can run at the same time, the control is incomplete.

Re-check readiness when scope changes mid-cycle#

When scope changes mid-cycle, pause and re-check channel readiness before submitting. Adding a return type, entity, or business line can invalidate assumptions from the original run, including plans involving IRIS.

Use your evidence pack to document the change decision. Update the dated rules snapshot, record the current IRS source used, and capture approver signoff before batch submission. That checkpoint is usually cheaper than unwinding a preventable filing error later.

For an example of how one platform handled this process, see How a Creator Platform Streamlined 1099 Filing with Gruv.

Handle cross-border payees and parallel tax obligations#

Adding non-U.S. payees means your Form 1099-NEC logic is no longer enough on its own. If a payee is documented with Form W-8 instead of Form W-9, or your systems do not agree on residency or tax status, route that record to cross-border review rather than forcing it through domestic auto-filing. That review may include Form 1042-S and separate withholding/reporting analysis.

The operating rule should stay strict: if residency, tax form status, or entity data conflicts across systems, pause auto-filing and escalate to tax/legal review. Resolve the conflict first, then file. Filing from mixed signals creates avoidable over-filing and under-filing risk.

Treat W-8 signals as a routing event, not a cosmetic field#

Your product does not need to auto-decide every cross-border tax question, but it must detect when U.S.-only logic no longer applies. Before year-end filing, reconcile country/residency, tax form type, and payment treatment across onboarding, tax, and payout systems. If those fields do not align, hold the record for review and retain the decision evidence.

| Field or evidence | What to do |

|---|---|

| Country/residency | Reconcile across onboarding, tax, and payout systems |

| Tax form type | Reconcile across onboarding, tax, and payout systems |

| Payment treatment | Reconcile across onboarding, tax, and payout systems |

| Current tax form on file | Retain as decision evidence |

| Residency values by source system | Retain as decision evidence |

| Payment ledger extract | Retain as decision evidence |

| Approval note | Retain for the final filing path |

| Policy gate | Mark as supported or unsupported; unsupported cases route to review |

That evidence should include the current tax form on file, residency values by source system, the payment ledger extract, and the approval note for the final filing path. If your program supports only specific markets, make policy gates explicit as "supported" or "unsupported." Unsupported cases should route to review, not default silently to a 1099 path.

Keep adjacent reporting streams in their lane#

Form 8938, FATCA, FBAR, and FinCEN contexts are related, but they are not substitutes for payee-level 1099 and W-8 controls. IRS materials for Form 8938 state it is used to report specified foreign financial assets when the applicable threshold is exceeded, and the form is attached to an income tax return. That is a different compliance stream from payee filing controls.

Form 8938 thresholds are not one-size-fits-all. IRS materials reference an aggregate value exceeding $50,000 for certain U.S. taxpayers, higher thresholds for joint filers or taxpayers residing abroad, and a $75,000 any-time-in-year threshold in one excerpt for specified domestic entities. IRS also states that if a taxpayer is not required to file an income tax return, Form 8938 is not required even if asset value exceeds the applicable threshold.

For deeper foreign-contractor routing detail, use the dedicated guide: 1099 for Foreign Contractors: When Platforms Must File and When W-8 Forms Apply Instead.

Catch the mistakes competitors gloss over#

The biggest avoidable error is treating tax-calculation math as filing-duty logic. Schedule SE (Form 1040) is for calculating self-employment tax on net earnings, not for deciding whether your platform should file Form 1099-NEC or Form 1099-K. A workflow can be mathematically correct on self-employment tax and still trigger the wrong filing action.

Verify the rule source before you ship it#

Ground your live rules in current IRS instructions, not secondary summaries. The IRS states that self-employment tax refers to Social Security and Medicare taxes only, and Topic 554 says it is usually due at $400 or more in net self-employment earnings, with 92.35% generally subject to that tax. Those points do not, by themselves, define a 1099 filing-duty test.

Use a simple control: store the exact IRS source and retrieval date for each rule. IRS instructions can change, and the Schedule SE page shows a correction to the 2025 instructions dated 20-FEB-2026. If your logic is not tied to a current source, treat it as potentially stale.

Keep an escalation path for ambiguous outcomes#

If your payee classification checks produce conflicting signals, do not force a binary result. Route the record to a named reviewer and retain the supporting records for that hold. The goal is not to automate every edge case; it is to prevent silent misclassification at filing time.

Conclusion#

A strong calculator is a controlled decision process, not a single threshold lookup. The practical standard is simple: lock the form family first, make the call per payee, and keep an evidence pack that shows why you chose file, do not file, or escalate. That is how you cut both over-filing and under-filing risk without pretending the facts are cleaner than they are.

One control matters more than teams expect: source discipline. If someone updates logic from a FederalRegister.gov page or an IRS bulletin index page alone, stop there and verify before you promote the change. FederalRegister.gov says its Web 2.0 display is not an official legal edition, and users relying on it for legal research should verify against an official edition.

The same caution applies when you see an IRS Internal Revenue Bulletin listing such as issue 2025-50 with entries like Notice 2025-69 or Notice 2025-70. A title or listing is not enough by itself to rewrite filing logic. Save the exact citation, source URL, and retrieval date in your rule history.

If you are putting this into practice, start with one contractor cohort that is boring on purpose. Pick a group with clean payment records, consistent tax form status, and a payment path that is unlikely to blur filing treatment. Run your calculator beside a manual review for one cycle and compare outcomes.

The checkpoint is not just whether the final answer matched. It is whether the reviewer had enough evidence to defend the answer later, including tax form status, classification rationale, and who approved any exception.

Document every miss before you scale. The useful exception list is usually short and revealing: missing tax documentation, conflicting payee type across systems, manual overrides without reviewer signoff, or classification references pulled from adjacent labor-law material and treated as if they directly answered IRS reporting.

For example, a Wage and Hour Division rule page dated 01/10/2024 may be relevant background on worker classification, but it is not a substitute for current IRS filing instructions. If those failure modes still show up in your pilot, keep the escalation path human and narrow the automation scope.

Scale across markets only after the exception pattern is stable and your evidence pack is consistent enough to survive audit questions. That slower start usually saves time because you are fixing rule quality and proof quality before volume turns small mistakes into a filing problem.

If you are moving from threshold checks to higher-volume filing, see 1099-NEC Automation for Platforms to File at Scale Without Manual Errors.

Frequently Asked Questions

Is my platform required to file a 1099 for every contractor?

No. A common Form 1099-NEC rule is filing for payees you paid $600 or more in the prior year, but that only matters after you confirm the payment actually belongs on Form 1099-NEC and not another form. If worker status, payee type, or payment flow is unclear, treat the result as escalate, not auto-file.

What is the fastest way to tell whether a payment belongs on Form 1099-NEC or Form 1099-K?

Start with the payment path and the responsible filer, not the dollar threshold. If the payment was processed by a third party payment organization, such as a payment app or online marketplace, that points you toward Form 1099-K. Direct nonemployee compensation paid by a business payer points toward Form 1099-NEC. Lock the form family first, because the wrong form choice makes any threshold check look more certain than it is.

When does the IRS electronic filing requirement apply to platform operators?

A practical trigger to watch is 10 or more combined forms, including 1099s, W-2s, or other federal forms, which QuickBooks summarizes as the point where e-filing is required. Use that as an early design checkpoint, then verify against current IRS instructions before filing. If your counts can rise late in the cycle, re-check before you freeze the batch.

What documents do we need on file before we can make a confident file or do-not-file decision?

This grounding set does not provide a complete document checklist for file/do-not-file decisions. Keep clear payment records, your form-family determination notes, and reviewer decisions, and treat missing documentation as an escalation case. For final filing requirements, verify against current IRS instructions.

How should we handle contractors with Form W-8 instead of Form W-9?

The provided sources do not include W-8 vs W-9 handling procedures. If a payee has Form W-8, route the case for tax review instead of forcing an automatic 1099 decision in the calculator.

What should trigger escalation to tax counsel instead of automatic filing logic?

Escalate when you cannot confidently determine whether the payment belongs on Form 1099-NEC or Form 1099-K, or when records conflict. Escalate too if your rule source is a commercial summary and nobody has checked the current IRS instructions. Those are failure modes that create both over-filing and under-filing risk.

How often should we re-validate threshold and form rules inside the calculator?

Re-check them before every filing cycle and any time the IRS updates the relevant instructions, thresholds, or form guidance. If a live rule depends on a secondary summary, verify it against current IRS primary instructions before you keep using it.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- federalregister.gov/documents/2023/08/29/2023-17565/gross-procee...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- govinfo.gov/content/pkg/FR-2024-06-25/pdf/2024-13331.pdftrusted

- irs.gov/newsroom/irs-announces-2023-form-1099-k-repo...trusted

- irs.gov/forms-pubs/about-schedule-se-form-1040trusted

- ssa.gov/international/CoC_link.htmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Choosing 1099 Filing Ownership for Platform Contractor Payments

At platform scale, 1099 risk is usually an ownership and evidence problem before it is a threshold problem. If you run payouts across multiple programs, entities, or payment rails, the question is not just whether a payment triggers a form. It is who owns the filing, what records support that decision, and how exceptions get handled when the facts are messy.

When Platforms File 1099 for Foreign Contractors and When W-8 Applies

If your platform waits until year end to choose between a Form 1099 path and a W-8 path, you are already late. In cross-border payouts, the real question is not just what each IRS form means, but which document controls the payout decision before money moves, who verifies it, and what you do when the facts do not fit the default path.

1099-NEC vs 1099-K Platform Filing Starts With Settlement Path

Start your filing analysis with the payment flow, not the worker label. The practical question is whether a transaction belongs in the `Form 1099-K` lane, whether another form in the 1099 series, including `Form 1099-NEC`, may apply, whether both might appear across different flows for the same payee, or whether form assignment needs further review.