Quick Answer

Build filing reliability upstream: tie payout eligibility to Form W-9/Form W-8 readiness, keep stable payee IDs across ledger and payout records, and classify Form 1099-NEC, Form 1099-K, and Form 1099-MISC with year-specific rules. This creator platform 1099 filing case study shows that weak records create year-end finance drag, while early controls reduce exception volume. The practical checkpoint is simple: one payment should be traceable from event history to final reporting export with consistent legal-name and tax-status fields.

The 1099 Filing Problem#

If your platform waits until filing season to think about tax reporting, you are already late. The practical point here is simple: 1099 quality is shaped upstream, in payout design, identity collection, and transaction records, not in a January cleanup sprint.

That matters because creator platforms can have more than one income path. A single product can combine direct contractor payouts with payments routed through third-party settlement organizations, including online marketplaces. For IRS purposes, many of the people paid through these products are treated as independent contractors, and the forms that usually matter are the Form 1099 series, especially Form 1099-NEC, Form 1099-K, and sometimes Form 1099-MISC. If you are a founder, product lead, or finance operator, the real question is not just which form exists. It is whether your product choices create records that support the right form, for the right payee, with enough context to defend exceptions later.

Form 1099-K is where many teams get sloppy because the threshold story has changed. Congress lowered the federal threshold in 2021 from more than $20,000 and 200 transactions to more than $600 with no minimum transaction count. Then the IRS delayed that lower threshold in 2022 and 2023, and set a $5,000 threshold for 2024 transactions as part of a phased approach. So do not hardcode one permanent rule into your operating assumptions. Just as important, 1099-K tracks money moving through payment apps and online marketplaces, but not every amount reported on the form is necessarily taxable income without context. That is why weak product records turn into finance drag.

The useful lens here is operational, not abstract. You want product decisions that improve control over Form 1099-NEC, Form 1099-K, and the exception queue before filing season shows up. In practice, that means collecting the right tax profile data early, tying payouts to a consistent payee identity, and preserving transaction fields finance can export without rebuilding the story by hand. A good verification checkpoint is whether you can trace one payment end to end, from event to ledger entry to payout record to tax-ready export, with the same legal name and tax status attached throughout.

The failure mode is predictable. If payout routes multiply before those controls exist, finance ends up reconciling mismatched names, incomplete tax records, and gross payment totals that lack the detail needed to explain what belongs on which form. Income can still be taxable whether or not a creator receives a particular form, which raises the stakes for getting platform records right. That is the operating lens here.

Why creator platforms break at year end#

Creator platforms usually break at year end because records are fragmented across systems, not because filing software is weak. Once independent contractor payouts, sponsorships, and affiliate earnings sit in different tools, finance has to rebuild who was paid, for what, and under which tax identity.

A common split looks manageable until filing season:

- campaign or sponsorship data in a creator ops tool

- affiliate earnings in a network dashboard

- payouts in a processor or banking rail

- tax profiles in a separate Form W-9 or Form W-8 flow

That setup can run for months without obvious pain. It breaks when you need clean information-return outputs and find one payee tied to multiple IDs, inconsistent earning labels, or a legal name that changed between intake and payout. A practical checkpoint is to trace one creator payment from earning event to ledger entry to payout record to tax-ready export. If the same legal name, payee ID, and tax status do not survive that trace, filing quality is already at risk.

IRS research shows why late fixes get expensive. After 2016, researchers identified a "1099-K gap," and raw counts were estimated to understate platform work by about 770,000 workers by 2018. The same research found that workers who received an information return reported, on average, $420 more in self-employment profits, and by 2021 at least 5 million individuals were receiving platform gig-work information returns. Even without a form, workers still must report income, which raises the bar for record quality.

Most creator-tax content stops at basic reminders. The operator question is simpler: can you produce an evidence pack with transaction ID, payee ID, earning type, gross amount, and document status for every disputed total? If not, January becomes a manual merge of CSVs, screenshots, and exceptions.

Related: 1099 Filing Threshold Calculator: Is Your Platform Required to File for Each Contractor?.

What to prepare before you touch filing logic#

Do not start with filing logic. If ownership, intake quality, and evidence standards are unclear, you will scale record problems instead of fixing them.

Treat tax intake as onboarding work, not a year-end scramble. Collect Form W-9 data, validate TINs, and maintain accurate records early, especially if you expect to send 10 or more 1099 forms.

Step 1: Assign ownership across teams. Finance should define what a complete tax profile requires and when updates are needed. Product should own collection UX and missing-data prompts. Engineering should own validation, status changes, and audit fields that show who changed what and when.

Step 2: Align payout eligibility with tax-profile readiness. Use one clear rule linking payout access to tax-profile completeness. Split logic between teams is a common failure mode: payouts go live while records are still incomplete.

Step 3: Inventory earning types before classification decisions. List your earning events and standardize labels in business terms so teams do not classify the same payment differently. The checkpoint is consistency from ledger entry through payout export.

Step 4: Define the evidence pack upfront. Set a minimum export for each paid record, including payee ID, legal name, masked TIN or document status, earning type, gross amount, transaction ID, payout ID, update timestamp, and reporting period. If your stack tracks IRS reporting periods, include that field from day one. Use secure, validated collection workflows and mask PII in operational views.

For a step-by-step walkthrough, see Choosing Creator Platform Monetization Models for Real-World Operations.

Step 1 map the money flow to filing obligations#

Map every live payment route end to end before you scale it. If you cannot trace a path from collection to ledger posting to payout and into tax export, treat that route as not ready.

Step 1 trace each payment route before you label it#

Start from actual product flows, then document the event chain in order: payment collected, fees applied (if relevant), ledger posted, payout approved, payout released, refunds/reversals/adjustments, and tax export output.

Tag each route for Form 1099-K review vs separate Form 1099-NEC/Form 1099-MISC review, but keep those NEC/MISC tags as review flags at this stage, not final determinations. Form 1099-K applies to payment card and third-party network transactions, and the IRS used a phased approach after delays in 2022 and 2023, including a $5,000 threshold for 2024 transactions reported in 2025.

Do not use thresholds as a reason to delay mapping. Income from sales of goods or services is still taxable whether or not a Form 1099-K is issued, so capture route tags and records from the first transaction. If a route resembles a crowdfunding platform or freelance marketplace flow, flag it early for 1099-K review.

Step 2 build one source-of-truth matrix#

Use one matrix that links each transaction event to payee identity, tax-document status at that moment, and reconciliation fields finance will need later.

| Transaction event | Tax tag to store now | Fields that must reconcile |

|---|---|---|

| Payment collected | 1099-K candidate or separate NEC/MISC review flag | payee ID, transaction ID, gross amount, event timestamp, reporting period |

| Ledger posted | same tag carried forward from collection | ledger entry ID, payee ID, gross amount, fee treatment if tracked, update timestamp |

| Payout released | same tag plus payee tax profile status at release | payout ID, legal name, masked TIN or document status, payee ID, payout amount |

| Refund, reversal, or adjustment | original tag plus correction indicator | original transaction ID, adjustment ID, amount delta, reason code, timestamp |

Enforce two controls now: keep tax-document status on the event lineage, not only the current profile, and keep stable join keys across systems. If finance must reconcile by display name or email, the matrix is weak.

Step 3 route weak paths into controlled payout flows and force a sign-off#

Move weak routes into controlled payout flows before adding volume. If a route cannot produce audit-ready records, do not scale it until identity and tax status, ledger events, and payout IDs are consistently tied.

Require a joint finance-and-engineering sign-off on one real end-to-end trace: payment event, ledger posting, payout release, and tax export row. Then run one stress case, such as a profile update or payout adjustment, to confirm the lineage still holds when records change.

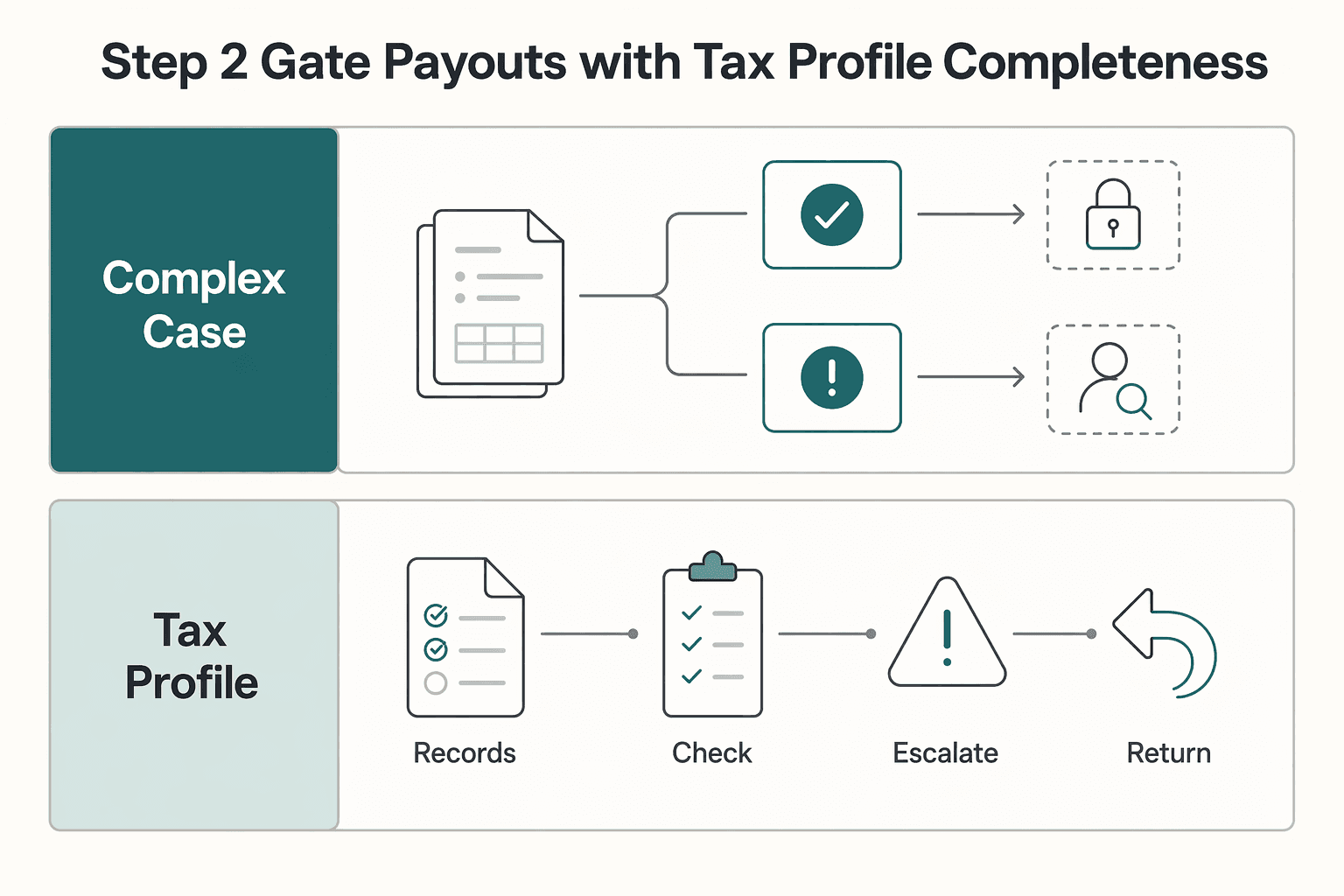

Step 2 gate payouts with tax profile completeness#

After mapping the money flow, set a clear payout gate: only release payouts when the payee tax profile is complete and matches the identity on the payout record. Treat this as an in-product eligibility check, not a year-end cleanup step.

A practical default is simple: creators can onboard and earn, but payout release stays pending until Form W-9 or Form W-8 status is complete. Use direct user messaging (payouts pending: tax details incomplete or under review) and route exceptions to manual review instead of silent bypasses.

Keep the core decision check unified across compliance and payout operations:

| Check | Release outcome |

|---|---|

| Tax profile is complete and identity records match across payout + KYB/KYC status | Release payout |

| Tax profile is incomplete | Hold payout and request missing data |

| Identity and tax records disagree | Hold payout and escalate to manual review |

This keeps payout operations aligned: evaluate compliance, tax management, and liability together with KYB/KYC and payout methods, not as separate tracks.

Keep the audit trail usable. For each release decision, store the payee ID, legal name used for approval, tax-document status at decision time, approval timestamp, and review source so finance can later explain why that payout was eligible at that point in time.

Related reading: Filing Back Taxes as a US Expat: A Guide to the Streamlined Procedures.

Step 3 classify earnings and contractor status consistently#

Classify each earning event with the same inputs every time, or month-end turns into manual tax-form triage. Keep the rule set explicit, versioned by tax year, and tied to stored record fields instead of reviewer judgment.

Separate two decisions on every payable record: what the payment was for, and how it was paid. Independent contractor payouts, affiliate income, and brand sponsorships can look similar in reporting, but they do not always map to the same form path. If your records only carry a broad label like "creator earnings," exceptions will pile up.

Use a controlled input set: earning type, payment method, payee tax-form status, residency indicator, tax year, and paying entity. Then apply a counsel-approved mapping table:

| Form | Use when | Operator caveat |

|---|---|---|

| Form 1099-K | Payment card or third-party network transactions | Threshold handling must be tax-year specific because implementation changed and was phased |

| Form 1099-NEC | Your policy classifies the payment as nonemployee compensation for services | Do not auto-classify from a generic earning label |

| Form 1099-MISC | Your policy classifies it into an approved reportable category outside your 1099-NEC logic | Affiliate and sponsorship flows can be fact-dependent, so route edge cases to review |

Treat 1099-K logic as year-aware, not permanent. Source guidance notes the shift from "$20,000 and over 200 transactions" to "$600 with no minimum transaction requirement," plus IRS delays and a phased approach, including a referenced $5,000 threshold for 2024 transactions in the 2025 filing context. Store both tax year and rule version so old records are reproducible.

For cross-border contributors, keep a separate review branch. If a payee is on Form W-8 status, route it to manual classification checks before U.S. form mapping rather than converting by analogy.

Also separate platform filing operations from user tax obligations. IRS FATCA materials state that certain U.S. taxpayers with specified foreign financial assets may need Form 8938 with their annual return when thresholds are exceeded, and some may also need FBAR (FinCEN Form 114). Keep your product copy precise and avoid implying that W-8 status resolves all U.S. reporting questions.

Verification checkpoint: run a fixed sample across contractor, affiliate, sponsorship, and cross-border records, then run it again with identical inputs. The output should match on form classification, exception flag, and tax-year treatment every time, with saved evidence for rule version, inputs, escalation reviewer (if any), and final reason.

Step 4 run exception operations before filing season#

Run exceptions as a standing operation before filing season, not a last-minute cleanup. Once classification is stable, route any record that cannot cleanly map to Form 1099-NEC, Form 1099-K, or Form 1099-MISC into a tracked queue with an owner, supporting evidence, and a defined next action.

Use fixed queue categories so work stays predictable:

- Missing Form W-9 or Form W-8

- Mismatched legal names

- Duplicate accounts

- Unresolved payout reversals

For each exception, store enough detail to resolve and defend it later: payee ID, tax year, payer legal entity, current tax-form status, affected payout IDs, and what is blocking filing. If someone needs Slack history to understand a case, the record is not ready.

Reconcile throughout the year so your totals stay explainable. Compare ledger totals, payout totals, reversal totals, and draft reportable totals by form type, then investigate deltas while records are still easy to trace. Save a small evidence pack for each review.

This matters for reporting outcomes. IRS research found platform workers who received an information return reported, on average, $420 more in self-employment profits, and the same research describes a post-2016 1099-K coverage gap where many workers under $20,000 did not receive an information return. A clean exception trail helps you explain why a creator did or did not receive a form.

Define your correction loop before filing pressure hits. IRS Information Returns Processing materials include correction-procedure sections, so treat corrections as normal operations: one path for issues found before filing and one for issues raised after filing. Start both with the same packet: original tax document, filed amount, ledger detail, payout/reversal history, and the reason for any corrected form.

Common mistakes that increase filing risk and how to recover#

Most filing risk here comes from operational drift, not surprise rules. The recurring pattern is late tax-form collection, split ownership, weak evidence, and over-automation.

- Collecting tax forms too late: Late W-9 collection often shows up as missing or invalid TIN issues when filing work is already under deadline pressure. Recover by gating payout expansion until the payee tax profile is complete and verified against the account record.

- Treating filing as finance-only: Filing quality drops when product and finance work separately. Recover by assigning shared ownership and running a regular exception review before payout or program changes create filing noise.

- Weak evidence retention: Corrections turn into scrambles when filing history is incomplete. Recover by keeping audit-trail exports tied to each filing batch and each correction, with enough detail to explain what changed.

- Overpromising automation: Not every record fits one automated path. Recover by keeping a manual escalation path for edge cases, especially where coverage varies by market or program.

The takeaway and a checklist you can copy#

The practical move is operational: build tax handling into product and payout controls early, then verify monthly that records still reconcile. If you cannot trace a payment from transaction event to filing artifact, you are not ready to scale payout volume safely.

Keep your reporting paths documented and ready for change. Form 1099-K rules have shifted from more than $20,000 and more than 200 transactions to more than $600 with no minimum transaction count, with IRS delays in 2022 and 2023, a phased approach starting in 2024, and a cited $5,000 threshold for 2024 transactions with forms required in 2025. Treat that as an operating reality: thresholds can change, so your controls need to adapt quickly. Also remember income from sales of goods or services is still taxable whether a Form 1099-K is received or not.

Use this as your minimum operating checklist:

- Tax ownership assigned across product, finance, and engineering

- Form W-9 and Form W-8 intake validated and tied to payout eligibility

- Form 1099-NEC, Form 1099-K, and Form 1099-MISC classification rules documented

- Exception queue active with SLA for identity and document mismatches

- Monthly reconciliation completed with audit-ready exports

- Filing-season dry run completed on sample data with correction path tested

If even one box is still open, treat it as operating risk, not admin cleanup.

Frequently Asked Questions

What is the practical difference between Form 1099-NEC and Form 1099-K for a creator platform?

Treat the 1099-NEC vs 1099-K determination as a tax-policy decision using current IRS guidance and taxpayer-specific advice before you lock platform logic.

What usually triggers an IRS mismatch review or CP2000 notice in platform payout data?

These sources do not define specific CP2000 trigger criteria. The safe operating baseline is keeping records reconciled and keeping correction history clear enough to explain original and revised amounts.

What should a platform track all year so filing is not a year-end cleanup project?

Track a complete record from transaction event to ledger entry to payout outcome, plus batch timing and any corrections. Keep the schema and ownership documented so year-end filing is a controlled process, not reconstruction.

When should payouts be blocked until Form W-9 or Form W-8 is complete?

The provided excerpts do not state a universal legal rule to block payouts based on W-9/W-8 completion. Treat payout gating as a documented compliance policy and apply it consistently.

How do KYC, KYB, and AML checks affect tax-document quality and filing readiness?

Handle identity/compliance controls and tax-document controls as related but separately governed workflows.

What is the minimum viable operating setup for accurate 1099 reporting with Gruv?

At minimum, run a traceable flow: transaction-to-ledger-to-payout mapping, policy gates where required, an exception queue, and reconciliation exports with audit-ready records. Keep those controls stable before adding more automation.

How should teams handle creators with cross-border tax considerations like FATCA or FBAR context?

Do not treat cross-border tax handling as "W-8 collected, done." Under FATCA, certain U.S. taxpayers with foreign financial assets must report to the IRS, generally through Form 8938 when applicable thresholds are exceeded. IRS notes a general reportability level above $50,000 in some cases, with higher thresholds in others; for specified domestic entities, the instructions excerpt includes $50,000 at year-end or $75,000 at any time during the year. Form 8938 is attached to the annual return, and if no income tax return is required for the year, the IRS excerpt says Form 8938 is not required. Some taxpayers may also need FBAR (FinCEN Form 114), and IRS guidance explains when Form 8938, FBAR, or both apply.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/116/plaws/publ136/PLAW-116publ136.htmtrusted

- dced.pa.gov/download/housing-rehabilitation-guidebooktrusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/pub/irs-soi/23rpevolutionofplatformgigwork.pdftrusted

- irs.gov/forms-pubs/about-form-8938trusted

- oversight.house.gov/wp-content/uploads/2024/12/2024.12.04-SSCP-F...trusted

- prhome.war.gov/Portals/52/Documents/MRA_Docs/RI/FY24%20Nati...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Handle Tax on Patreon and Other Crowdfunding Income

Tax season should not feel like a siege. For many creators, it does. The fix is not a bigger spreadsheet or a last-minute scramble. It is a setup you build on purpose, in the right order.

1099 Filing Threshold Calculator for Platform Contractor Decisions

If you own compliance, legal, finance, or risk for a platform, the question is not, "what is the general 1099 threshold?" It is this: for this payee, with this payment flow and this documentation, are you required to file, not required to file, or unable to decide yet without review?

Case Study Framework: How to Document Platform Payment Wins for Marketing

Payment case studies are most credible when they read like an operating record, not marketing copy. In payments, a "win" often reflects design tradeoffs across routing, controls, and settlement behavior, not just a faster user flow.