Quick Answer

Document a platform payment win as a scoped decision record with a defensible baseline, clear design tradeoffs, an auditable implementation sequence, and outcomes tied to operations or economics. Build claims from approved artifacts, separate symptoms from causes, compare rejected options, and place compliance, tax, and market qualifiers next to each claim so the story stays credible for buyers and internal reviewers.

Define the Win and the Proof#

Payment case studies are most credible when they read like an operating record, not marketing copy. In payments, a "win" often reflects design tradeoffs across routing, controls, and settlement behavior, not just a faster user flow.

That standard matters because payment infrastructure is fragmented, regulated, and high stakes. In many environments, teams still operate in rail-specific silos with separate processing, compliance logic, and operations, so a polished narrative can hide execution risk. If a change introduced new operational burden or a new failure path, that belongs in the story.

This guide uses a compact format to document one platform payment win so teams can inspect and challenge it. The core test is simple:

- What changed

- Why that decision was made

- What it cost to implement

- What risk it introduced

- Which operational signal improved

Keep the proof operational and explicit. A practical checkpoint in payment stories is routing validation: did the instruction have enough information, and what rules applied at execution time? If that is unclear, you may be documenting a symptom instead of the design choice.

Make downside risk visible too. Poor payment design can show up as outages, failed transactions, or compliance gaps. If smart routing helped because you could reroute when a rail was unavailable or not the best fit, say that plainly. If a faster path was rejected because operational risk was worse, say that too.

Finally, scope your claims by market and program. Rail coverage and controls vary. Real-time systems are not interchangeable across regions. For example, RTP and FedNow in the US are not the same as Faster Payments in the UK or SEPA Instant in Europe. Use qualifiers like "where supported" or "when enabled" so readers do not infer universal coverage from a corridor-specific result.

Define the document scope before you draft#

Set the scope before drafting. Treat this as a scoped decision record, closer to a business-case document than a campaign brief. The goal is to make expected benefits, costs, and risks clear enough for a decision-maker to inspect.

Step 1. Name the document type and audience#

Set the boundary in the first lines. Treat this as one scoped record of what changed, why it was approved, and which business result matters.

Decide the audience up front: buyer-facing B2B asset, internal decision memo, or both. If it serves both, say so, then split the output into a clear external narrative and internal support detail.

Step 2. Lock the use case into one sentence#

Write one sentence that fixes the use case. Keep it narrow and operational, such as a speed improvement, failure-rate reduction, or reconciliation simplification. Set it during project initiation, before planning and before narrative drafting. That sentence should make three points unambiguous:

- What changed

- For whom

- How success will be judged

Step 3. Define the win before you write the story#

Define the win in business terms before you write copy. Use business-case logic: expected benefits, costs, and risks. Set option boundaries too.

Show at least a light comparison of options with pros, cons, and estimated costs instead of presenting one path as automatically correct. If the section will include implementation claims, set approval criteria up front, including timeline, milestones, resources, and key deliverables, so later claims stay auditable.

Related: Accounts Payable Document Management: How Platforms Organize Invoices Contracts and Payment Records.

Gather prerequisites and evidence before writing#

Build the evidence pack before you draft. If a rail, compliance, or tax claim is not tied to a document, treat it as unknown and leave it out.

Step 1. Build a claim-to-artifact sheet#

Create a simple sheet that maps each planned claim to one owner and one record. Use: claim, date range, source artifact, owner, approval status, and publishable yes or no.

This is the control that keeps payment storytelling from turning into unverified "fact." In this evidence pack, ACH, RTP, FedNow, and SEPA Instant outcomes are not established. Mark those outcomes unknown rather than inferring from memory or slides.

Verification point: every numerical or causal sentence should map to one row in the sheet. If you cannot answer "who approved this and what document proves it?", it is still a placeholder.

Step 2. Pull tax documents only when they changed the story#

Include tax artifacts only when they materially affected eligibility, timing, or segment handling.

| FEIE item | Grounded detail | When relevant |

|---|---|---|

| Filed return | Keep the filed return reporting the income | If FEIE appears in the narrative |

| Form 2555 / 2555-EZ | Keep Form 2555 or Form 2555-EZ | If FEIE appears in the narrative |

| Day-count support | Keep day-count support | If qualification relies on physical presence |

| 330-day test | 330 full days in 12 consecutive months | Missing the threshold fails the physical presence test |

| Full day | 24 consecutive hours, midnight to midnight | Used for the physical presence test |

| Tax home | The test is tied to having a tax home in a foreign country | State the qualification basis precisely |

| 2025 maximum | $130,000 per qualifying person | Adjust by qualifying days if qualification covers only part of a year |

| 2026 maximum | $132,900 per person | Adjust by qualifying days if qualification covers only part of a year |

If FEIE appears in your narrative, keep the filed return reporting the income plus Form 2555 or Form 2555-EZ. If qualification relies on physical presence, keep day-count support. You need 330 full days in 12 consecutive months. A full day is 24 consecutive hours, midnight to midnight. The test is tied to having a tax home in a foreign country.

Be precise about limits and edge cases. Missing the 330-day threshold fails the physical presence test. If qualification covers only part of a year, adjust the maximum by qualifying days rather than assuming the full annual amount. The stated maximum is $130,000 per qualifying person (2025) and $132,900 per person (2026).

Verification point: if FEIE is mentioned, show the exact form and qualification basis, not just "working abroad."

Step 3. Separate policy labels from proved impact#

Treat labels like KYC, KYB, and AML as categories, not proof. If you claim they delayed go-live or changed conversion, you need policy records or case-level evidence showing that effect. That proof is not present here, so do not present those impacts as settled fact.

| Reference | How to treat it | Publish rule |

|---|---|---|

| KYC | Treat as a category, not proof | Use policy records or case-level evidence before claiming impact |

| KYB | Treat as a category, not proof | Use policy records or case-level evidence before claiming impact |

| AML | Treat as a category, not proof | Use policy records or case-level evidence before claiming impact |

| W-8 | Note touchpoints only if needed | Do not assign specific operational outcomes without records |

| W-9 | Note touchpoints only if needed | Do not assign specific operational outcomes without records |

| IRS Practice Unit | Use as orientation, not binding authority | Anchor publishable claims to the filed return, Form 2555, and the relevant IRS rules |

Apply the same rule to W-8 and W-9 references: note touchpoints only if needed, but do not assign specific operational outcomes without records.

If you use the IRS Practice Unit during prep, treat it as orientation, not binding authority. For publishable claims, anchor to the filed return, Form 2555, and the relevant IRS rules.

Doing this prep first keeps reviewers aligned on evidence before anyone debates prose. For structure and sourcing, read A Guide to Writing Case Studies for a B2B SaaS Audience.

Step 1 document the business problem and baseline economics#

Treat Step 1 as a publish gate. If you cannot defend the before-state with evidence, do not publish the case study.

Define the problem in operating terms, then support the financial story with records. This step is not about celebrating the win yet. It is about capturing the starting state clearly enough that product, ops, and finance would all agree it is accurate.

Write the transaction path like an operator#

Document the full before-path end to end: trigger, routing decision, rail, reconciliation handoff, and completion signal. If ACH, RTGS, Visa, or Mastercard appear in the path, note where each appears and where manual intervention enters when flows break.

Keep symptom language out of the process map. "Payouts were slow" is a symptom. The useful baseline is the actual sequence of queueing, routing, exception handling, and reconciliation steps. Focus on the workflow, not isolated tasks.

Capture cost pressure without hype. Cost pressure can include repeated manual review, unresolved exceptions, duplicated support work, avoidable retries, higher-cost routing than intended, or finance time spent reconciling mismatches.

Verification point: every path step should map to one approved artifact and one owner in your claim sheet.

Separate the symptom from the cause#

Treat symptoms and causes as separate lines in the draft. Slow payouts, failed charges, or higher support volume describe what people experienced. Routing logic, reconciliation lag, exception handling, or policy-gate friction describe why.

Use two checks for each issue:

- What did the customer, merchant, or team experience?

- What in the transaction path produced it?

If the second answer depends on guesswork, remove the causal claim for now. Keep the scope tight to the proved problem instead of expanding into adjacent areas without separate evidence.

Build a before-state table you can defend#

Use one compact table with fixed fields and approved definitions. This is the baseline your later after-state must beat.

| Field | Record in before-state | Evidence check | Common mistake |

|---|---|---|---|

| Volume profile | Covered period, payment/payout type, approved rail or segment split | Same date range across ops, finance, and support | Mixing periods across sources |

| Failure categories | Actual error or exception categories, preferably internal status codes | Labels match source exports | Collapsing distinct failures into one bucket |

| Retry behavior | Whether retries happened, who triggered them, auto vs manual | Retry definitions approved by queue owner | Counting all repeat attempts as retries |

| Support burden | Ticket themes, escalation path, owning team | Support and ops labels align for the period | Using anecdotes as measured burden |

| Margin pressure | Where cost or loss appeared, such as labor, exceptions, or routing | Finance confirms the pressure point is attributable | Claiming later improvement without a baseline source |

If a value is disputed, mark it unresolved instead of smoothing it over in prose.

Apply the publish gate#

Before moving forward, verify all four:

- One shared date range across baseline fields

- One owner and one source artifact per field

- Symptoms and causes written separately

- Unknowns marked unknown, not inferred from memory or slides

If any check fails, stop and fix the evidence first. Every later claim depends on this baseline.

Step 2 capture the payment design decision and its tradeoffs#

Once the baseline is defensible, document the payment design decision as a clear before-and-after architecture record, not a modernization claim.

Separate what stayed stable from what changed#

Write this step in two columns: stable core and changed components. In many cases, the real change is narrower than the narrative: one transaction path changes while the ledger stays fixed, or responsibility shifts while onboarding stays the same.

For each major design element, state whether it changed the core or was added as a complement through an interface. That distinction matters because interface choices shape future platform control and can be harder to revise than core internals.

Attach one architecture artifact your team can defend:

- a network graph of parties and handoffs

- a layer map across application, payments, messaging, and reconciliation

- a design structure matrix when dependency shifts are central

Verification point: each changed element maps to one artifact, one owner, and one explicit before-and-after statement.

Compare rejected options, not only the final choice#

A credible decision record shows what you kept and what you discarded. If you only show the selected path, reviewers cannot evaluate the operating judgment.

| Decision area | Option kept | Option discarded | What to record |

|---|---|---|---|

| Core vs complement boundary | Keep capability in the stable core | Move capability to a complement | The decision rule used in this use case |

| Interface design | Keep or standardize the chosen interface | Alternate interface design | Which teams and dependencies changed |

| Participation openness | Narrower or wider participation path | The alternative openness level considered | Which supplier, customer, or complementary-provider paths changed |

| Representation artifact | Chosen architecture view for review | Other views considered | Why this view best captures the decision and tradeoffs |

Do not add precision you cannot support. You do need the decision rule and why the rejected path lost.

If relevant, state openness effects directly: the design made participation paths narrower or wider for suppliers, customers, or complementary providers.

State tradeoffs in plain language#

Make the tradeoff explicit in body text so readers can see what improved and what got harder. Cover these four comparisons directly:

- User value vs value appropriation

- Openness vs control

- Interface stability vs ease of future change

- Core stability vs complement flexibility

Use a direct pattern: "We chose X to improve Y, knowing it would increase Z."

Build a decision pack a reviewer can audit#

Keep the evidence pack small and exact: selected option, rejected alternatives, one architecture artifact, and a written tradeoff statement approved by product, payments ops, and finance. For each changed element, give a one-line operational before-and-after description.

Close with one sentence that can be audited later: what the team chose, what it rejected, and which risk it accepted knowingly.

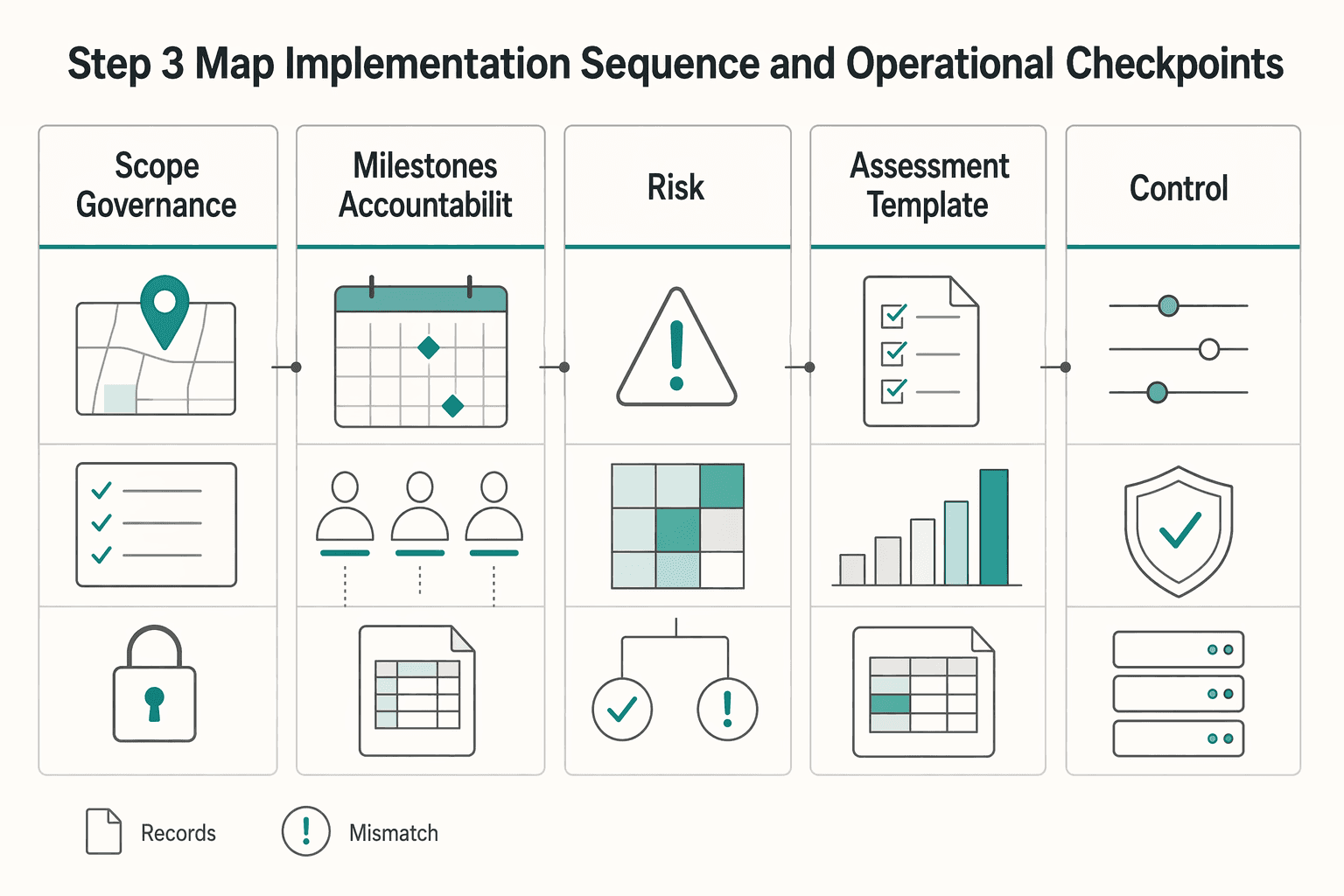

Step 3 map implementation sequence and operational checkpoints#

This section should read like an auditable timeline, not a launch recap. Show the implementation order, the checkpoint owner, the go or no-go rule, and the record kept at each gate.

Start by defining scope, aligning stakeholders, and establishing governance so the sequence does not blur owners or stop conditions.

Use a strict sequence unless you have a documented reason to change it:

| Stage | What to document |

|---|---|

| Scope and governance setup | Scope, exclusions, stakeholder alignment, governance owner, and approval gate |

| Milestones and accountability checkpoints | Milestone, checkpoint owner, go or no-go rule, and retained record |

| Risk tiering | Tier definitions, assessment depth and frequency by tier, and exception-lane owner |

| Assessment template design | How rigor vs usability was balanced, expected response-rate impact, and sign-off |

| Oversight controls | Supervisory tier model (for example Tier 0/1/2, if used), dual-control approvals for sensitive actions, and who can act versus observe |

| Audit trail readiness | Immutable audit records captured at each checkpoint and retrieval ownership |

If a stage has no stop condition, treat that as a gap before rollout.

Name expected failure modes before go-live, especially where manual checkpoints could slow operations or create an inconsistent experience. For each one, record owner, handling path, and immutable audit evidence.

If payment-specific controls or rails are not fully documented, label their status as unknown or out of scope instead of inferring implementation details.

Step 4 connect outcomes to monetization and margin decisions#

Treat this as a finance test, not a storytelling step. A routing change, recovery improvement, or support reduction is only a potential monetization win until you can tie it to pricing headroom, take-rate durability, or retention behavior with auditable evidence. If you cannot make that link, classify it as an ops improvement.

That distinction matters because platform growth and platform scaling are different. You can increase transactions, users, or platform value while costs still rise sharply. A scaling outcome is stricter: revenue grows without costs growing at the same rate.

Step 1. Convert technical outputs into decision metrics#

Start with the payment output you changed: approval quality, recovery effort, payout cost profile, manual exception volume, or payment-related support contacts. Then convert it into a decision metric leadership can act on.

| Output | When it matters | Trace to |

|---|---|---|

| Approval quality | When it can support a pricing decision, protect take rate, or improve retention behavior | A finance system, support log, or pricing file |

| Recovery effort | When it can protect gross margin or reduce human intervention as volume grows | A finance system, support log, or pricing file |

| Payout cost profile | When it can create room to hold price, test hybrid pricing, or reduce cross-subsidization risk | A finance system, support log, or pricing file |

- Better approval quality matters when it can support a pricing decision, protect take rate, or improve retention behavior.

- Lower recovery effort matters when it can protect gross margin or reduce human intervention as volume grows.

- Lower payout cost profile matters when it can create room to hold price, test hybrid pricing, or reduce cross-subsidization risk.

Use one check: can finance trace the commercial claim to a finance system, support log, or pricing file? If not, keep the claim operational.

Step 2. Separate growth signals from margin signals#

Do not treat volume lift as proof of monetization improvement. More payment volume can indicate growth, but if cost to serve or support staffing rises with it, unit economics may not improve.

Label each claimed outcome separately: growth signal, margin signal, and retention signal. Track full costs from day one, including founder time and temporary launch labor, so the economics are not overstated.

Step 3. Build a before-and-after table finance can audit#

Use one compact table with metric definitions and caveats.

| Metric | Before | After | Definition | Caveat for finance review |

|---|---|---|---|---|

| Approval quality | [baseline] | [current] | Share of attempted payments that complete under the approved product or finance definition | Do not attribute all movement to payment changes if onboarding, risk, or traffic mix also changed |

| Recovery effort | [baseline] | [current] | Manual ops or support work needed to resolve failed, delayed, or duplicate events | Include temporary launch labor, exception handling, and founder time when material |

| Payout cost profile | [baseline] | [current] | Cost per successful payout or settled payment under the finance-approved cost view | Separate one-time implementation cost from ongoing cost to serve |

| Support cost impact | [baseline] | [current] | Support contacts or support spend tied to payment issues over a defined volume band | Keep ticket taxonomy stable before and after |

| Pricing or take-rate decision | [old rule] | [new rule] | Monetization decision enabled or protected by the change | If no pricing, margin, or retention effect is documented, classify as ops only |

Keep period definitions and cohort rules consistent between before and after. If you use adjusted or non-GAAP-style internal views, include reconciliation support and do not present them as substitutes for standard financial reporting.

Step 4. Write the monetization judgment with caveats#

Make the judgment short and explicit. For example: this change reduced support cost per payment and recovery effort, but evidence for pricing headroom is still limited. Or: this change helped protect take rate in a churn-risk segment, but margin impact remains provisional because manual exceptions are still high.

This caveat discipline helps avoid soft ROI claims. Around pricing, keep the language narrow: the change created room to test pricing or preserve a margin band, not proof that higher prices are justified in general.

Step 5. Choose pricing implications only when the math scales#

Only connect outcomes to pricing models the economics can support. When cost variability is still high, hybrid pricing, a base fee plus usage or outcome tiers, can be the more defensible choice. Outcome-based pricing can align value, but it can also shift cost variability onto you.

Run a scale check at both 10 customers and 1,000. If results depend on heroic manual handling, heavy exception work, or favorable mix, treat the result as operational progress, not a durable monetization win.

If the story hinges on savings or margin lift, use Measure AP Automation ROI for Payment Platform Finance Teams to tighten the math. Before locking your margin narrative, pressure-test your assumptions against an operational reference in Gruv Payouts.

Step 5 document compliance and tax caveats without killing clarity#

State scope limits in the same sentence as the claim. Keep FEIE caveats to supported eligibility, timing, and limit facts, and avoid legal conclusions.

Step 1. State the control boundary as an observed fact#

Describe only what your records and this grounding set support for FEIE. If a non-FEIE compliance topic appears, mark it as out of scope or unknown unless separately supported.

Keep the claim at the effect level unless you have stronger support. If records only show "pending review," use that wording and stop there.

Step 2. Include tax-document details only when they are supported and material#

Do not add document-specific filing requirements here unless they are directly supported and material to the outcome you are claiming.

For FEIE, keep the caveat narrow and factual:

- It applies only to qualifying individuals with foreign earned income, and that income is still reported on a U.S. return.

- A physical presence route uses 330 full days during any period of 12 consecutive months.

- A full day is 24 consecutive hours, beginning and ending at midnight.

- FEIE is claimed on Form 2555 or 2555-EZ.

- The maximum exclusion is $130,000 for 2025 and $132,900 for 2026, per qualifying person.

Do not soften the 330-day requirement with ordinary reasons like vacation, illness, or employer instruction. If that minimum is missed, the test fails on those grounds. Adverse-condition waivers are a separate exception. Keep timing precise too: FEIE allocation follows when work was performed, even if payment arrived later.

Step 3. Add qualifiers where FEIE eligibility varies#

Use short qualifiers tied to FEIE eligibility, like "if you are a qualifying individual," "if you meet the physical presence test," and "if your tax home is in a foreign country." Place the qualifier at the claim, not in a disclaimer block.

Treat IRS LB&I process-unit text as background, not binding authority. The IRS language states it is not an official pronouncement of law.

Step 6 write the buyer-facing story without losing technical truth#

Turn the evidence into a buyer story people can trust. Keep a clear sequence from starting context to outcomes and limits so the section stays readable without sliding into hype.

Step 1. Anchor the story in the buyer's starting problem#

Start with the real operating problem the buyer can recognize, not a success claim. If readers cannot see the before-state clearly, the rest will read like promotion instead of practical problem-solving.

Keep the scope tight to one decision under one set of conditions. Simply describing completed work is not enough unless the audience can connect it to practical benefits.

Step 2. Describe the decision with concrete nouns#

Name the exact objects and process changes, not slogans. If wording is too abstract for an operator to map to a real artifact, log, or workflow, rewrite it.

Use shorthand frameworks only when they reduce confusion. If they hide the mechanism, remove them.

Step 3. Keep constraints inside the story#

Put limits next to each claim, not in a disclaimer block. Buyers look for proof, and outcomes presented without clear boundaries can read like hype.

Before publishing, attach a short score sheet at the end of the case as a practical check. Use it to confirm each outcome maps to evidence and each qualifier is stated at claim level.

Step 4. Note what stayed difficult#

If something stayed difficult or unchanged, state it plainly as part of the operating reality. This gives readers a clearer view of where the case may or may not transfer.

Step 5. Close with fit and non-fit#

End with who should copy the approach and who should not, based on operating context and constraints. A buyer should be able to compare your conditions and evidence to their own and quickly see whether the result is likely to transfer.

For a step-by-step walkthrough, see How to Make the Case for AP Automation to Your CFO: A Platform Finance Team Playbook.

Choose publish candidates with explicit decision rules#

Publish the case that is easiest to repeat and easiest to defend, not the one with the biggest headline.

Step 1. Score transferability first#

Start by testing whether the change can be repeated beyond one project. Ad-hoc experience from a single project is a weak guide for broader implementation, so one-off hero fixes should usually stay internal.

Use one check: can another team in a similar segment reproduce the decision from the document alone? If success depends on tribal knowledge, founder intervention, or a nonstandard exception path, reject it as a publish candidate.

Step 2. Prefer complete evidence over larger claims#

A smaller win with clear support is stronger than a larger win with fuzzy definitions. Prioritize cases with clear evidence, defined metric definitions, and a stable before-versus-after comparison.

A fixed comparison structure keeps selection defensible. In one cross-case framework, researchers documented 4 main categories, 14 factors, and 74 measures across thirty-two projects. You do not need that exact depth, but you do need a consistent structure so comparisons stay usable.

Do not select on feature checklists or unit-pricing snapshots alone. That can look objective while leaving core decisions ambiguous.

Step 3. Reject unclear attribution and unresolved limits#

Do not publish when you cannot separate the result from other simultaneous changes. If multiple changes shipped together and attribution is unclear, keep the case internal until the mechanism is clear.

Apply the same standard to applicability constraints. Put limits in the body copy, and if those limits are still unresolved, do not publish externally yet.

Avoid common case-study failures and recover fast#

When a publish candidate breaks, fix the evidence before you polish the narrative. Recovery usually comes from records discipline, stable metric definitions, explicit option logic, and clear caveats in the main body.

Step 1. Rebuild the before-state from records, not memory#

A case with no defensible baseline is not ready to publish. Rebuild the before-state from your auditable records and ops logs first, then edit copy.

Use complaint and ticket data as a cross-check to find likely root causes, not as the primary baseline. Keep dated extracts and notes together so another reviewer can retrace the baseline without relying on tribal context.

Step 2. Lock metric definitions before editing outcomes#

Inflation starts when labels stay the same but definitions drift. Create finance-reviewed metric definitions, and remove any claim that cannot be reproduced from source records or separated from concurrent changes.

For each headline metric, include the definition, the source record, and a note on other changes in the same window. If finance cannot reproduce the result from the same extract, the claim is not publishable. Do not assume a failure automatically creates a satisfaction lift; any recovery upside is conditional and less likely after severe failures.

Step 3. Show option logic, not just labels#

Listing options without decision logic weakens trust. Add a compact option table with one clear acceptance reason and one clear rejection reason for each non-selected path.

| Option | Decision logic to include | If rejected, state why |

|---|---|---|

| Option A | Why it fit or did not fit the operating model | Why it lost for this case |

| Option B | Why it fit or did not fit the operating model | Why it lost for this case |

| Option C | Why it fit or did not fit the operating model | Why it lost for this case |

If readers cannot explain in one sentence why the losing option lost, the section is still incomplete. For a deeper instant-vs-batch compare, use Real-Time Payment Use Cases for Gig Platforms: When Instant Actually Matters.

Step 4. Move operational constraints into core sections#

If delivery constraints were part of the execution reality, keep them in the main section, not footnotes. State the practical impact in plain language: who is affected, where the flow pauses, and what operational checks are required.

Use formal checkpoints as governance points, not ceremony. The goal is simple: a buyer, operator, or finance reviewer should understand limits and execution impact without legal translation.

Conclusion#

A strong payment win case study is simple to inspect: one clear decision, one defensible baseline, one transparent path from change to execution, and one outcome story tied to economics. The point is proof, not promotion, because buyers are skeptical of hype and a recap of completed work alone is not enough.

Use this checklist before you publish#

- Define the win and scope in one sentence.

Name the business problem, the decision, and the context. If one sentence tries to carry multiple wins, split it.

- Include baseline and after-state metrics with clear definitions when available.

Keep metric names, time windows, and inclusion rules consistent across both states. If a reader cannot trace each number to records, tighten definitions before rewriting the narrative.

- Document the approach, rejected options, and tradeoffs.

Show what you chose, what you did not choose, and why. A short tradeoff explanation is usually enough.

- Record the implementation sequence and failure handling.

Show the order of operations and at least one failure mode you planned for or encountered.

- Add material caveats only when they changed this case.

Include caveats when they changed timing, process, approval, or cost in your documented path. If they did not materially change outcomes, leave them out.

- Include a plainspoken buyer narrative and one "what didn't improve" note.

A 3-part SCR flow, Situation, Complication, Recommendation, can keep the story focused. The explicit limit note makes the rest of the evidence more credible.

- Run a final evidence read-through before publishing.

Confirm claims match records and caveats, and avoid overstating attribution when multiple changes happened at once.

Final check: tie the result to platform economics, not just activity. Growth and scaling are related but distinct. If the story shows more usage without a clear view of costs and revenue, it is not yet a strong publishable case.

Related reading: Digital Nomad Payment Infrastructure for Platform Teams: How to Build Traceable Cross-Border Payouts.

If your final case points to consolidating compliance and money movement under one operating model, review whether Merchant of Record fits your market and program constraints.

Frequently Asked Questions

What is a case study framework for documenting platform payment wins?

It is a structured way to document one payment problem, the decision made, and the results that followed. For platform payments, it should read like an operating record, not a testimonial. Readers should be able to see what changed and which outcomes are actually supported.

Which sections are mandatory for a credible payment win case study?

There is no single payment-specific mandatory checklist in this article. A credible case still needs the challenge, the solution, the results, and the end-to-end journey between them. If one of those pieces is missing, the story is harder to trust.

How is a case study framework different from a marketing strategy?

Here, the framework is the evidence-focused document that captures challenge, solution, and results. A marketing strategy is the broader plan for how that proof gets used. Keeping them separate helps prevent promotional language from getting ahead of the evidence.

How do I prove a payment win without overstating causality?

Anchor claims to outcomes you can demonstrate, and describe them only at the level your records support. Separate symptoms from causes, and avoid saying the payment change alone caused broader business results when multiple changes happened at once. Clear caveats are more credible than inflated attribution.

What makes buyers trust one payment case study over another?

Buyers trust a payment case study more when it shows the full journey and demonstrates outcomes instead of making broad claims. Plain language, concrete evidence, and explicit limits usually matter more than polish. A candid note about tradeoffs can improve credibility.

When should I include compliance and tax details like KYC, AML, W-8, or 1099?

Include these details when they materially affected onboarding, approval, or ongoing operations in this case. For KYC, show process reality, not just forms, including data collection, verification, risk assessment, decisioning, monitoring, periodic review, and case-management logging where relevant. Include W-8 or 1099 details only when they directly changed execution and you can evidence that impact.

How much technical architecture detail is enough for a B2B marketing audience?

There is no single threshold that fits every B2B audience. Include enough detail for a reader to understand what changed and why the operational outcome changed, then stop before it becomes an implementation manual. Concise control-point detail can be enough when decisions and supporting artifacts are auditable.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- academia.edu/14442843/Case_structure_Step_1_Frame_the_pro...trusted

- cdn.careers.bloch.umkc.edu/wp-content/uploads/sites/130/2021/11/Profess...trusted

- documents.fresno.gov/WebLink/DocView.aspxtrusted

- economics.virginia.edu/sites/economics.as.virginia.edu/files/inline...trusted

- hbs.edu/ris/Publication%20Files/09-034_149607b7-2b95...trusted

- hbs.edu/ris/Publication%20Files/22-050_ec28aaca-2b94...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: