Quick Answer

Pick the platform path that can prove one payable record end to end, not the one with the longest feature sheet. For accounts payable document management platforms invoices contracts, the deciding test is whether your team can trace invoice, contract or PO support, approval decisions, GL destination, and payout state without manual stitching. Use DMS-first when retrieval is the gap, all-in-one AP when finance control is the gap, and API-first when payout orchestration is the gap. Then pressure-test duplicate handling and retries before scale.

What AP document management should cover#

Choose an accounts payable document management platform for control, not storage alone. You need a traceable path from intake to approval, posting, and payout without pushing teams back into manual handoffs.

At its core, accounts payable document management is how you collect, store, track, and process vendor payment documents. That scope goes beyond invoices to include receipts, purchase orders, payment records, and related communication. For platform teams, the real test is whether those records stay linked when finance, ops, and engineering each touch a different part of the process.

AP automation extends that across the full AP cycle, from invoice capture through approvals, ERP posting, payments, and reconciliation. So this is not just a document retrieval decision. It is also a decision about approval control, accounting handoff, payout visibility, and supplier data support across one or more ERP environments.

Before you evaluate vendors, use this framework:

- Document control

Can you keep invoice, contract, supporting evidence, and payment record data in one place, or at least in one traceable chain of record, so retrieval is fast when someone asks what supported a payment?

- Operational control

Can the system route approvals, reduce manual entry, and give you enough visibility to catch issues early?

- Integration control

Can the AP layer connect cleanly to ERP or accounting software and stay in sync with payout status with minimal manual repair?

Prioritize the control gap creating payment risk today. If your team still stitches records together by hand, fix centralization and retrieval first. If approvals are inconsistent, put approval workflow control first. If payout and finance states drift, move integration quality to the top of the list.

A practical checkpoint is simple: pick one recent payable item and trace it end to end without asking multiple teams for screenshots. You should be able to find the invoice, related contract, supporting PO where relevant, approval decision, accounting destination, and final payment record. If that chain breaks now, it usually gets harder to fix as volume grows.

A common miss is buying capture automation before fixing record linkage and ownership. That may reduce manual entry, but it can still leave contracts, approvals, and payment status split across tools. This guide focuses on the order that helps you avoid that outcome: what to buy first, what to defer, and which controls need to be live before volume grows.

This pairs well with our guide on Accounts Payable Software Comparison for Platforms That Need Operational Proof.

How to choose the right platform path for your team#

Choose for control depth first if you need one traceable trail from purchase order, receipt, and invoice through GL posting and payout status. If you only need searchable storage, versioning, and retrieval, a lightweight DMS may be enough.

Start by separating two very different needs: storing documents well and controlling payments well. Some teams only need better retrieval. Others need a system that can stop bad payments, enforce approvals, and keep accounting and payout states aligned.

- Decide whether you need AP control or only document storage.

A DMS is built for storage, search, version control, and workflow, but it does not inherently provide AP controls like duplicate checks, approval segregation, or payment state sync. Trace one paid item end to end: PO, receiving evidence where relevant, vendor invoice, approval decision, GL destination, and payout status.

- Confirm document coverage before comparing automation claims.

You want a linked payable record set, not loose attachments. For many teams, that includes an invoice plus related authorization or contract details, receiving support, and payment evidence such as canceled checks when available. If billing rules require a contract number or other authorization on the invoice, treat that as a first-class field.

- Prioritize controls that prevent bad payments.

Validation is a core gate because invoices must be validated before payment or accounting entries are created. Check whether duplicate detection evaluates supplier, invoice type, amount, currency, and date, not only invoice number. Review separation of duty in approvals: if one user can submit, approve, and release the same item, the trail is weak.

- Use integration quality as the tiebreaker when payout flows are complex.

If engineering capacity is limited, you may prioritize operational controls first in phase one. If payout complexity is high, evaluate API and event-delivery behavior early. These endpoints are asynchronous, retries happen, and undelivered events can be resent for up to three days. If a vendor cannot explain idempotent retry and duplicate-safe event handling, the risk of status drift between documents and payments is higher.

You might also find this useful: Internal Controls for Accounts Payable on Platforms: How to Prevent Fraud and Ensure Accurate Disbursements.

Quick comparison of the five platform paths#

Use this table to rule out poor fits quickly. Pick the path that is strongest at the failure point you cannot tolerate, whether that is approval control gaps, weak contract linkage, exception handling, GL handoff risk, or payment state drift.

| Platform path | Invoice ingestion | Contract linkage | Approval workflow | Exception queue | GL export depth | Event coverage | Audit retrieval speed | Confidence on pricing, contract depth, validation | Best when | Breaks when |

|---|---|---|---|---|---|---|---|---|---|---|

| All-in-one AP automation software | Usually strong; OCR-based capture is available in AP software, and some products handle review, approval, and payment together. | Often present, but depth varies. Contract-backed invoice creation is a linkage signal, not proof of full contract lifecycle depth. | Usually strong; approval rules can auto-route users or groups. | Usually strong; exceptions can include duplicates, missing receipts, quantity or price mismatches, and tax variances. | Medium to strong; some suites create journal entries and integrate with ERP applications. | Mixed; endpoint coverage and event behavior vary by vendor and need testing. | Can be simpler when invoice, approval, and payment records are in one system. | Medium; third-party review surfaces exist, but pricing transparency and contract-depth clarity are often incomplete. | You want fewer moving parts and a finance-led phase one. | You need product-native payout state handling the suite cannot model cleanly. |

| DMS-first extension | Medium; strong storage and retrieval, lighter capture or extraction unless paired with AP tooling. | Strong for retrieval when required metadata is enforced at save time. | Light to medium; routing exists, but AP-specific controls may need added logic. | Weak to medium; document storage helps retrieval, but reconciliation depth still needs separate validation. | Light to medium; export is often integration dependent. | Light; eventing is usually not the core strength. | Fast when metadata discipline is high and search uses metadata fields, not only file names. | Low to medium; pricing transparency and AP-control evidence vary, and contract-depth proof is often limited. | You already run a strong DMS and prioritize retrieval quality. | You expect storage alone to prevent duplicate payments, enforce role separation, or keep payment status synced. |

| API-first finance stack | Medium to strong when capture plus API ingestion is intentionally designed. | Medium; can be strong with a deliberate data model, rarely turnkey. | Strong when engineering owns rules and state transitions. | Strong when reconciliation states, retries, and failure paths are explicitly built. | Strong when custom ledger mapping and posting logic are stable. | High potential, but only with duplicate-safe processing; some providers explicitly warn the same event may arrive more than once. | Medium unless IDs are normalized across document, contract, and payment systems. | Medium; docs can be detailed, but pricing transparency, contract depth, and independent validation vary across vendors. | AP decisions directly drive product payouts and engineering can own idempotency and replay operations. | Teams expect a configuration-led rollout and no one owns replay testing or failed-event recovery. |

| Compliance-heavy multi-entity stack | Varies; can be strong where invoices are validated against entity, policy, or market requirements. | Strong on required evidence linkage, not necessarily deep contract authoring or lifecycle tooling. | Strong and formal; useful when approval rules differ by entity or program. | Strong for policy-driven exception handling and structured reconciliation. | Strong where entity-level coding and posting references matter. | Mixed; webhook depth and reliability still need endpoint testing. | Medium to fast when evidence packs are standardized; slower when each entity stores records differently. | Medium; some global vendors publish scope and partial pricing, but independent validation beyond vendor claims remains limited. | You operate across entities or regulated flows and need defensible evidence per payment. | Policy overhead slows a small, simple AP motion. |

| Rapid-deploy managed stack | Medium; generally sufficient for baseline intake and archive. | Light to medium; basic linkage is common, deeper contract controls are less certain. | Medium; works for standard routing with fewer configuration levers. | Medium for common exceptions, thinner on edge-case policy logic. | Light to medium; standard exports are common, custom mappings may be limited. | Light to medium; API hooks may exist, but depth should be treated as unproven until tested. | Medium for baseline retrieval. | Low to medium; some vendors publish entry tiers, for example $99/month and $199/month, but many details remain sales-scoped. | You need working controls quickly and can accept narrower customization in phase one. | Exception volume, custom GL needs, or contract rule specificity outgrows the managed setup. |

The deciding columns are usually Exception queue, GL export depth, and Event coverage. That is where document storage turns into payment control and where retry and duplicate behavior expose weak designs.

Use two evaluation checks before you commit:

- Run one payable item end to end with a real pack: invoice, contract, PO or supporting evidence when relevant, approval log, GL destination, and payment record.

- Test failure behavior, not just the happy path. Replay the same event and confirm duplicate-safe handling. Design retries with idempotency in mind, including key retention limits such as 24 hours where applicable.

Do not treat pricing visibility or review visibility as proof of operational depth. Independent review surfaces are useful, but event reliability, contract lifecycle depth, and stalled status handling still need direct testing because status movement can depend on the buyer's internal processes.

For a step-by-step walkthrough, see Accounts Payable Outsourcing for Platforms When and How to Hand Off Your Payables to a Third Party.

All-in-one AP automation suite option#

If your immediate goal is finance-led control, an all-in-one AP suite can be a fast first move. It works best when you need one system to capture invoices, route approvals, run duplicate checks, and sync accounting data without stitching together multiple tools.

- Best fit

Choose this path when you need one place to capture an invoice, route approvals, flag potential duplicates, and sync accounting data to ERP or accounting systems. Gartner describes AP applications as modular, configurable cloud tools that integrate with one or more ERPs, which is why this option can reduce assembly work and ownership gaps.

A practical early use case is centralizing invoice processing with PO and receiving support before adding deeper orchestration. If your current pain is scattered documents, inconsistent approvals, and delayed reconciliation, a unified suite can standardize the core flow quickly.

- Why it works early

The advantage is consistent control, not just a longer feature list. A software-driven AP process can cover invoice processing, matching, approval, payment, and reconciliation, including matching invoices to PO and receiving documents before payment.

Auditability also improves when the system logs status changes and exceptions as they happen. In SAP Concur Invoice, status changes and submitted exceptions are recorded as audit trail rows, which makes it easier to review who changed what and when.

- Tradeoff and red flag

The main risk is whether integration depth will hold up for custom workflows. Even with a one-platform approach, some downstream requirements can still require more integration effort, so "one platform" should not be treated as proof that every edge case is covered.

A published CFO case study shows both sides: the team reported a "50%+ reduction in month-to-end close time (10 days to 5)" and said consolidated books could be pulled in "five minutes," while also noting that some alternatives would have required substantially more integration effort. Treat that outcome as directional, not typical.

- What to verify before you buy

Run one end-to-end payable with a real evidence pack: invoice, PO or supporting evidence where relevant, approval log, accounting sync record, and payment record. Then verify two controls: duplicate logic flags potential repeat invoices before payment, and the audit trail records status changes and exceptions as discrete entries.

Rule of thumb: if near-term success means standardizing AP controls, this path is usually strong. If approved invoices must immediately trigger complex downstream workflows, test integration behavior harder than the demo.

Related: Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

DMS-first extension option#

A DMS-first path fits when record continuity is the priority. You already rely on the document management system for contract, PO, and supporting file retrieval, and now need stronger AP controls without replacing that records layer.

- Best fit

Choose this option when file storage is already disciplined and the gap is payable control. AP automation can be implemented inside a document management system or as standalone software, so extending from DMS is a valid architecture.

This can work well when you already use the DMS as your system of record for contract and purchasing documents. In that setup, AP can inherit existing filing patterns instead of forcing teams to rebuild them in a new tool.

- Why it works well

Its core advantage is document linkage and retrieval. AP systems can link unstructured files, for example images and other document types, to structured AP records, and workflows can include extracting invoice data from email attachments and viewing documents directly in the workspace.

It also supports matching-centric review. Accounts payable matching compares vendor invoice, purchase order, and receiving information, including three-way checks on price and quantity. If those records are already organized in your DMS, reviewers can pull a more complete evidence pack: invoice, contract, PO, delivery proof, and related image or email artifacts where supported.

- Tradeoff and red flag

Strong retrieval does not equal strong AP control. Vendor status and duplicate checks may require explicit rules outside core document storage.

Duplicate logic can be stricter than invoice-number checks alone, for example by combining supplier, invoice type, amount, currency, and date. The failure mode is straightforward: teams can find every file quickly but still increase approval risk when metadata is incomplete or inconsistent.

- What to verify before you buy

Test one real payable end to end before committing. Include the invoice, linked contract, PO and receiving evidence where relevant, related email attachment, and approval record.

Confirm three controls: search retrieves the full pack, matching compares invoice data to PO and receiving data, and duplicate checks evaluate more than invoice number. Choose DMS-first only if you can enforce a required metadata model with required fields, unique record IDs, and consistent values across records.

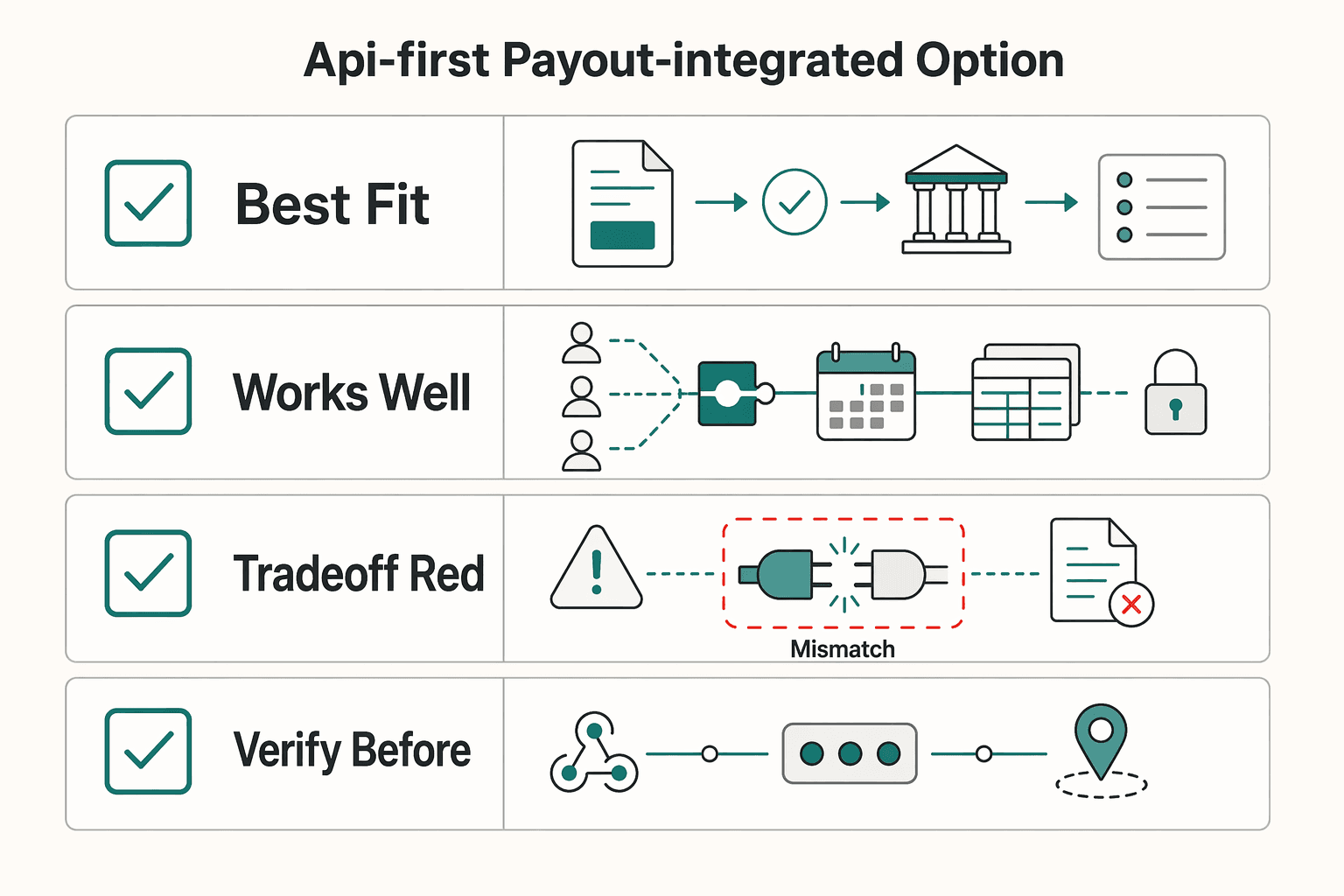

API-first payout-integrated option#

API-first can be a strong fit when invoice approval must directly trigger payout execution and in-product status, not just document workflow.

- Best fit

Consider this for marketplace, contractor, or creator platforms where approval and disbursement are one flow. This model depends on event control across connected accounts: Connect integrations are expected to establish webhook endpoints, and platforms can manage and schedule payouts for connected accounts that do not use a Stripe-hosted Dashboard.

- Why it works well

This path can give you tighter control across invoice ingestion, approval, payout initiation, payout status updates, and reconciliation through API and event orchestration. ServiceNow documents API-based AP invoice ingestion and end-to-end processing through approval, and BILL exposes AP objects and payment actions such as vendors, bills, bill approvals, and payments.

It is also built for retry safety. Stripe supports idempotent requests to avoid double execution, and Adyen supports safe retry after timeout with the same idempotency key.

- Tradeoff and red flag

This route requires engineering ownership for event ordering, retries, replay protection, and document-state orchestration. Finance configuration alone is not enough.

Do not treat event notifications as the only source of truth. Duplicate deliveries can occur, and critical workflows should reconcile event-driven state with read APIs to reduce duplicate payment-record posting risk.

- What to verify before you buy

Run a replay test: approve one invoice, trigger payout, resend the same event, and retry the outbound payment request with the same idempotency key after a simulated timeout. Pass criteria: one payout request, one payment record, and one consistent AP-to-payout-to-GL status trail.

Confirm provider constraints before implementation: Stripe idempotency keys allow up to 255 characters, Adyen caps at 64, and PayPal listeners must both receive and verify messages while returning 2xx on success. PayPal can retry non-2xx deliveries up to 25 times over 3 days, so deduplication must hold under repeated delivery.

Related reading: Designing an End-to-End Accounts Payable Workflow for Platforms.

Compliance-heavy multi-entity option#

Choose this option when payout can be blocked by policy that differs by entity, market, or payee tax status. In that setup, payment is a control decision, not just an approved AP step. You may need contract authorization, receiving or acceptance support, jurisdiction-specific invoice fields, and current payee tax documentation before funds move.

The core requirement is a payment record that answers, for each disbursement: what authorized it, what proved performance, what accounting entry it created, and what held payment when required evidence was missing.

1. Best fit#

This model fits cross-border, regulated, or multi-entity operations where one approval rule does not apply cleanly across all programs. A useful anchor is the "proper invoice" concept: payment depends on valid invoice content and satisfactory contract performance, not only upload plus approval.

FAR 32.905 (page version effective 03/13/2026) is a practical reference point. It ties payment to a proper invoice and satisfactory contract performance, and requires receiving support or other payment-authorizing documentation. It is a defensibility model, not an automatic rulebook for every private platform.

2. Evidence pack#

Use a compact, retrievable evidence pack per payment, then vary requirements by entity and local review.

| Evidence element | What it proves | Verification checkpoint before payment |

|---|---|---|

Contract or equivalent authorization | Commercial authority under the relevant entity or program policy | Confirm vendor linkage and that the invoice references the correct contract number or other authorization |

Approved Invoice | Amount, supplier identity, and invoice approval decision | Validate required invoice fields for the jurisdiction, for example issue date, unique sequential number, and VAT ID where applicable |

Receiving report (or equivalent receiving evidence) | Receipt, acceptance, or fulfillment support for billed goods or services | Verify it matches the invoice line or service period and supports payment authorization |

Final GL posting reference | Accounting entry created from the payment decision | Confirm the posting or journal reference links back to source documents for audit-trail support |

| Vendor tax documentation | Payee tax status and withholding basis | For cross-border payees, confirm current W-8 or W-9 status and withholding statement details are accurate before each payment |

Treat payee tax status as a payment-time control. IRS guidance for payments to nonqualified intermediaries states that withholding statements must be updated for accuracy prior to each payment.

3. Why teams choose it#

The main gain is defensibility during review. You can show one chain from source authorization and invoice support to the final accounting entry, which aligns with maintaining audit trails between source documents and accounting-system entries.

It also improves exception governance. A formal exception queue is an operating choice, not a stated legal requirement in the cited sources, but it gives teams a controlled path for real blockers, such as a missing contract reference, stale W-8 or W-9 data, missing receiving evidence, potential duplicate payment indicators, or missing GL trace.

This model also supports segregation of duties. The person maintaining vendor or tax status should not be the only approver who can release payment exceptions.

4. Tradeoffs and decision rule#

The tradeoff is slower rollout and higher process overhead if the scope is too broad. If every control applies to every payment, exception handling can outgrow capacity.

Define scope first: which entities, markets, and payee classes need hard payment blocks, and which defects can be corrected before posting. A useful control benchmark is timing discipline. FAR 32.905 requires returning a non-compliant invoice within 7 days of receipt. Even where that is not mandatory, a short return SLA helps prevent bad invoices from aging into urgent exceptions.

Keep duplicate controls at payment time, not only intake, because duplicate disbursements are classified as improper payments. Keep retention disciplined as well. IRS Topic 305 references a general 3-year assessment period as a practical floor for preserving supporting records, while your required period may be longer.

If policy can block payout, design contract checks, vendor tax checks, and receiving or acceptance checks before scaling automation volume. If you cannot explain why one entity paid and another blocked, the multi-entity compliance design is not complete.

Rapid-deploy operations option for lean teams#

Choose this path when you need baseline AP control quickly and can run a narrower phase one. It is built for teams that want usable approval and retrieval workflows in weeks, with exceptions still handled by people.

1. Best fit#

This route fits teams dealing with spreadsheet approvals, scattered invoice handling, and slow payment-status answers. Mainstream AP tools support rule-based review where invoices that meet criteria can auto-approve and the rest route to an authorized reviewer, which can provide a workable phase-one control model.

Plan timing as variable, not guaranteed. One published range puts implementation at 2 to 12 weeks depending on complexity, with modern cloud deployments often at 2 to 4 weeks and more complex setups at 8 to 12 weeks or more. Vendor claims of deployment in days exist, but they are scenario dependent. If procurement setup, product setup, or base pricing is not in place, rollout can slip before invoices enter workflow.

2. What you get fast#

The immediate win is three controls working together: approval workflow, invoice archive, and posted payment retrieval. Invoice approval can start when an invoice record is created, and imported invoices can be auto-submitted in a touchless AP process.

For operations, retrieval matters as much as approval. Prioritize archived invoice lookup and access to archived payment transactions after posting. A practical phase-one checkpoint is simple: take one paid invoice, retrieve it from archive, and confirm your team can access the related invoice and payment transaction records.

3. Where phase one usually bends#

Phase-one speed comes from narrower scope, so edge cases are usually where friction appears. If you need deep product-side handoffs or very specific accounting treatment, verify that early rather than assuming it will work later without added integration.

A practical risk is over-automating before rules are stable. Touchless flow works best when matching, policies, and routing are clear. If the line between auto-approve and manual review is unclear, more invoices end up in exception handling and manual follow-up.

4. Concrete use case and upgrade trigger#

A practical phase-one use case is replacing spreadsheet approvals while keeping manual review for exceptions. Clean invoices can move automatically, and exception invoices can route for approval. That gives lean teams better control without waiting for full-process depth.

Monitor the exception queue closely. One documented implementation keeps an audit trail of failed invoice-ingestion emails, but the default view shows only the last 7 days. If misses become recurring and your team repeatedly rekeys data, chases missing items, or spends more time reconciling payment status across tools, it may be time to plan deeper integration.

The minimum document model every platform should enforce#

Lock this model before deeper automation. You need a small, policy-aware record chain that lets you reconstruct what was approved, what was received, and what was paid.

Invoiceas the anchor record

Make every payable invoice traceable to policy-required supporting records. For PO-backed spend, include purchase order linkage. Keep linkage conditional by invoice type so teams do not create fake PO or contract references just to pass validation.

- Receipt evidence for PO-based spend

For goods and other PO-backed purchases, support the three-way match pattern: invoice, PO, and receiving evidence (or equivalent receipt record). This control helps confirm receipt before payment. Gating rules vary by policy, so your model should handle both all-PO receiving requirements and threshold-based rules, including published examples that trigger at $50,000 and above.

- Canonical approval and payment packet

Maintain a chronological approval and status history plus the final payment record for each paid invoice. Without that sequence, you have stored files but not an examinable audit trail. At minimum, the record should show when approvals and status changes happened and which payment closed the invoice.

- Measured exceptions, not ad hoc handling

Capture exception outcomes in a consistent format so failures can be reviewed and improved over time. The goal is a repeatable record, not one-off handling that is hard to analyze later.

Run a recurring verification checkpoint: sample paid invoices and confirm the required chain is complete for that invoice type. For PO-backed invoices, confirm invoice, PO, receiving evidence, approval log, and payment record. For contract-governed spend, confirm any policy-required contract references are present.

We covered this in detail in Accounts Payable Automation ROI for Platforms That Need Defensible Results.

Use this as an implementation checkpoint: map your required invoice-to-supporting-document-to-payment fields and verify your team can enforce them in live workflows using the Gruv docs.

Failure modes that cause payment errors and audit pain#

Once the minimum record chain is in place, many avoidable payment errors come from state and control failures, not just missing files. If you are evaluating platforms in this category, pressure-test the four failure modes below early because each one can create duplicate-payment risk or leave you with an audit trail that is hard to defend.

- Capture-only duplicate checks

A duplicate check at invoice ingestion is not enough when downstream events can be replayed. Event and queue delivery are commonly at-least-once, so the same status or payment event can arrive again, and some providers retry delivery for up to three days. Run a replay checkpoint: resend the same downstream event and confirm no second payment record, no second status transition, and no silent overwrite of invoice state.

- Approval workflow with weak role boundaries

If one person can submit, approve, and override an invoice, the control is weak even if the UI shows approvals. Separation of duties is meant to prevent one person from controlling multiple phases of a payment-related process, and weak segregation weakens accountability. Verify the log is chronological and reconstructable: who approved, who changed status, who released exceptions, and when each action occurred.

- Retries that are not idempotent

Retry logic is a normal part of event-driven systems. Non-idempotent retries create duplicate-operation risk. APIs such as Stripe support idempotency so repeated requests do not perform the same operation twice, and AWS guidance is to design consumers as idempotent because duplicate messages happen. Ask for a replay test, not a promise. If AP says "paid" while the payout layer still says "pending" after event retries, you already have status drift that finance may need to reconcile manually later.

- Approved invoices that fail at payment-time checks

Payment-time mismatches can create exceptions even after approval. In AP platforms, matching discrepancies are checked against tolerances, and holds can block payment release until someone resolves the issue. Focus on the hold evidence pack: invoice, linked contract or PO reference, receiving evidence where required, approver history, and the exact reason code that triggered the stop.

If you want a deeper dive, read AI in Accounts Payable: How Payment Platforms Use Machine Learning to Process Invoices Faster.

90-day implementation sequence that avoids rework#

Use this sequence to avoid rework: lock the record model first, enforce finance controls second, and only then trust API and event automation under replay conditions.

| Phase | Focus | Checkpoint |

|---|---|---|

| Days 1-30 | Freeze invoice, contract, PO, and payment record; define required links and metadata; standardize rejection reasons, queue owners, and SLA targets | On recent items, retrieve the invoice, supporting business documents, and current exception reason without cross-team escalation |

| Days 31-60 | Turn on duplicate checks, vendor status, and approval workflow controls; verify segregation of duties; export approved invoices with known coding to the GL | Confirm entity, account, amount, and status match source records and approval outcomes; validate three-way matching where it applies |

| Days 61-90 | Replay the same event; test duplicate deliveries, stale or partial payloads, out-of-order events, and idempotent retries | Confirm no second payment record, no duplicate status transition, and no silent overwrite of newer invoice state |

| Cutover | Rehearse in a test environment; publish an owner matrix; define rollback criteria; set a post-launch audit sample plan | Sample paid items for linked invoice, contract, PO or receiving evidence where required, approval history, GL posting reference, and final payment record |

- Days 1-30: lock the document taxonomy and the

Exception queue.

Freeze the canonical records your team will use everywhere: invoice, contract, PO, and payment record. Define required links and metadata up front so each invoice can be tied to current vendor status, governing contract, and purchase or receiving evidence where matching applies. Approval controls should compare invoice data to PO or receiving evidence before payment approval.

Make exceptions measurable in this phase: standardize rejection reasons, assign an owner for each queue state, and set team SLA targets for first touch and resolution. If queue aging is unclear, it is harder to spot late-payment risk early. Checkpoint: on recent items, can you retrieve the invoice, supporting business documents, and current exception reason without cross-team escalation?

- Days 31-60: implement core controls and validate

GLoutput against source records.

Turn on duplicate checks, vendor status, and approval workflow controls, then verify that segregation of duties is real. If one person can submit, approve, and override the same invoice, the control is weak even if the UI shows an approval chain. Your audit log should clearly show who acted, what changed, and when.

Then prove accounting outcomes: export approved invoices with known coding to the GL and confirm entity, account, amount, and status match source records and approval outcomes. Validate three-way matching behavior where it applies.

- Days 61-90: test end-to-end flows for duplicates, replay, and out-of-order events.

Do not rely on happy-path tests before cutover. Event consumers should expect duplicate deliveries, and payloads can be stale, partial, or out of order. Replay the same event and confirm no second payment record, no duplicate status transition, and no silent overwrite of newer invoice state.

Run explicit idempotent retry validation. If your payment layer uses idempotency keys, document exact behavior and retention windows. Stripe's published reference points are keys up to 255 characters and possible pruning after 24 hours, so test retries both inside and outside that window.

- Cutover: rehearse, assign owners, and define rollback and first-week audit checks.

Treat cutover as an operations event. It is the final production transition, and cutover windows can be less than 48 hours. Rehearse in a test environment, publish an owner matrix across finance, ops, and engineering, and define rollback criteria before launch.

Set a post-launch audit sample plan for paid items: linked invoice, contract, PO or receiving evidence where required, approval history, GL posting reference, and final payment record. If any link is missing in live transactions, fix the record model before volume ramps.

Conclusion#

Choose the path that can still prove what happened when operations get messy. The right option is the one that keeps the invoice, related contract records where applicable, and final payment record linked under real pressure.

- Choose for proof, not feature count.

End-to-end AP runs from invoice approval through vendor payment, so test whether one transaction can be traced across that full chain without manual stitching. Your baseline check: for paid samples, retrieve the approved invoice, linked contract where applicable, PO and receiving report where three-way match applies, approval log, and final posting or payment reference from one workflow. If finance needs engineering logs or ops has to hunt through email, the setup is not ready to scale.

- Define evidence and control activities before picking architecture.

Start with what your team must prove, then choose DMS-first, AP-automation-first, or API-first based on that requirement. Control activities such as verifications, reconciliations, authorizations, and approvals should be documented in policy and procedure, not implied by a product demo. If payout state and event-driven disbursements matter, require reliable API behavior and idempotency support so retries do not create duplicate operations.

- Scale only when exception handling is predictable.

Invoice exceptions are a known AP bottleneck, and manual invoicing can run as long as 90 days in some organizations. Make sure every exception shows the reason, missing document, owner, next action, and payment block status, with a complete evidence chain: approved invoice, signed contract where relevant, supporting PO or receiving evidence where relevant, approval history, and final payment record. If a paid item cannot be supported by that chain, you are carrying audit and reconciliation risk.

If you use one decision rule, use this: do not buy category labels. Choose the path that can prove an end-to-end audit trail, document its control activities, and keep exceptions verifiable before scale.

If you want a practical fit check for your AP controls, payout flow, and integration constraints, talk with Gruv.

Frequently Asked Questions

What is accounts payable document management for platforms?

Accounts payable document management is the system your team uses to collect, store, track, and process payment-related documents. In practice, that includes records like invoices, purchase orders, and receiving evidence tied to vendor payments. The key distinction is whether the tool is only document-centric, like a DMS, or also runs the full purchase-order-to-payment process through AP automation.

Which documents must be linked before payment approval?

As a control baseline, use an approved invoice plus the documents that prove the order and receipt before payment is released. Where three-way matching applies, that means matching the invoice, purchase order, and receiving report. A practical control check is whether your team can retrieve the full supporting record quickly during review.

Should we choose AP automation software or a Document Management System first?

Choose AP automation first when your main bottleneck is process execution across PO-to-payment, approvals, and payment controls. Choose a DMS first when your primary gap is storing, managing, and retrieving documents, and your process controls are already solid elsewhere. The tradeoff is simple: DMS tools are document-centric, while AP automation tools are process-centric.

How do we prevent duplicate or unauthorized payments at scale?

Start with separation of duties so one person cannot perform consecutive accounting tasks alone. Then enforce idempotent API behavior so retries do not create duplicate payment-side effects. Also design event handling for duplicate delivery, because duplicate events do happen.

What should an audit-ready invoice-to-contract trail include?

An audit-ready trail should be a retrievable chain of transaction evidence and approvals, with supporting documents connected to the payment record. It also needs a chronological audit log showing who acted, what action was taken, and when. That traceability is what makes review and control testing practical.

How should we evaluate pricing and integration depth when vendor details are unclear?

Treat limited vendor transparency as a real procurement risk and test specifics early. Ask for written details on integration mappings, event behavior, duplicate-event handling, retries, and ownership of reconciliation and control evidence. If the service affects your financial reporting controls, request relevant assurance artifacts such as SOC 1.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/32.905trusted

- acquisition.gov/afars/2-10.-separation-dutiestrusted

- comptroller.war.gov/Portals/45/documents/fmr/current/15/15_03.pdftrusted

- congress.gov/116/plaws/publ117/PLAW-116publ117.pdftrusted

- controller.vpfa.fsu.edu/services/accounts-payable/encumbered-payment...trusted

- csrc.nist.gov/glossary/term/audit_trailtrusted

- csrc.nist.gov/glossary/term/Separation_of_Dutytrusted

- ecfr.gov/current/title-36/chapter-XII/subchapter-B/pa...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Payment Platforms Apply AI in Accounts Payable for Faster Invoices

AI in AP is most useful when it speeds up invoice handling without weakening approvals, payment controls, or record matching. The real question is not whether a tool can read an invoice. It is whether your process still holds when documents are messy, approvals are conditional, and payment release has to stay controlled. Three points should frame your decision before you compare tools:

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

Internal Controls for AP Platforms to Prevent Fraudulent Disbursements

Start here: your AP control design should reduce fraudulent disbursements and payment errors without turning every payout into a bureaucratic exercise. In practice, that means clear escalation points at the moments where money can move incorrectly, not extra approvals added just to look controlled.