Quick Answer

Map programmatic advertising payouts dsp ssp settlements from bid-linked event records to billing, ledger entries, and final payout status, then automate only after terms and controls are explicit. In practice, teams should lock deduction precedence, enforce idempotent retries, and gate release with approvals, holds, and dispute evidence. The article’s core checkpoint is reproducibility: finance must be able to rebuild one net payable line from contract terms and source records without spreadsheet guesswork.

Programmatic payouts are won or lost after the auction#

In programmatic advertising DSP/SSP settlement flows, the hard part starts after the bid win. Real-Time Bidding (RTB) sets impression pricing in milliseconds, but settlement determines whether finance, ops, and engineering can trust the money movement from buyer to publisher.

Step 1 Anchor the auction roles#

Start with the auction layer, because every later payout decision depends on it. A Demand-Side Platform (DSP) is what advertisers use to buy digital inventory programmatically across publishers, SSP-connected supply, and exchanges. A Supply-Side Platform (SSP) is publisher-side technology used to sell ad space based on impression opportunities. An Ad Exchange is the auction marketplace connecting buyers with publishers, where impressions are bought and sold in real time.

RTB is the decision engine inside that market. Demand evaluates an impression and bids on it within milliseconds. In a unified auction context such as Google Ad Manager bidding, demand sources compete in a single auction and the serving ad source is the highest paying advertiser. That tells you who won the impression. It does not by itself define how money should be recognized, billed, checked, and finally paid out.

Checkpoint: you should be able to describe, for one won impression, which party bought, which party sold, where the auction happened, and what event record proves the win.

Step 2 Separate auction truth from settlement truth#

Auction truth is narrow: who bid, who won, and at what price. Settlement truth is broader: who owes whom, under which terms, against which records, and when a payout is actually releasable.

That distinction runs through the rest of this guide. We are not stopping at DSP, SSP, and exchange definitions. We are tracing the handoffs from DSP bid win to publisher payout, with controls and verification points in between. If your team cannot follow an amount from the auction-side event to the payable-side record, you do not yet have a settlement model you can automate with confidence.

A common failure mode is treating bid or auction logs as if they are the full reconciliation set. Depending on counterparty terms, additional records may still be needed once billing documents, deductions, adjustments, or counterparty statements enter the picture. The practical test is simple: if an amount is disputed or delayed, can you identify the exact source record and the handoff where it diverged?

Step 3 Read this guide as an operator, not a glossary#

Many resources explain what a DSP, SSP, or ad exchange is, then stop there. They may not show an operator-grade settlement model with explicit ownership, verification points, and release controls around payout execution.

This guide is for teams building inside the Programmatic Advertising Network: platform founders deciding architecture, product teams defining records and states, finance teams closing the books, ops teams handling exceptions, and engineering teams wiring the settlement path. If that is your seat, the useful question is not "Who won the auction?" It is "Can we prove, approve, and reproduce the money movement after the auction?"

Related: Integrated Payouts vs. Standalone Payouts: Which Architecture Is Right for Your Platform?. If you want a quick next step, try the free invoice generator.

What to prepare before you automate DSP and SSP settlements#

Before you automate DSP and SSP settlements, lock commercial terms, record ownership, and release controls so you do not hard-code ambiguity into payouts.

| Preparation step | What to document | Grounded note |

|---|---|---|

| Contracts and overrides | Revenue Share, Fee Deduction, clawback triggers, dispute windows, and who owns the billing document or seller statement | Microsoft states exact payment terms are contract-specific, even where invoices may be issued within 5 business days after month-end and are typically net 30. |

| System of record | Choose platform invoice, seller statement, or your internal settlement ledger, then define linkage from source event to settlement line item to payout instruction | Microsoft also notes some invoice amounts can be reconciled in platform UI reports. |

| Release controls | Define policy gating, payout approvals, and exception escalation ownership before launch | AdSense describes issuance between the 21st and 26th only when thresholds and holds are satisfied, and Microsoft reserves the right to withhold seller payment under specified account conditions. |

| Unresolved unknowns | Timing-model differences, deduction order, and dispute liability allocation across the chain | The ISBA/PwC study reports 15% of spend in an unattributable "unknown delta." |

Step 1. Inventory contracts and term overrides. For each DSP, SSP, and Ad Exchange relationship, document what changes net payable: Revenue Share, Fee Deduction, clawback triggers, dispute windows, and who owns the billing document or seller statement. Treat timing as contract-defined, not standard. Microsoft states exact payment terms are contract-specific, even where invoices may be issued within 5 business days after month-end and are typically net 30.

Step 2. Confirm your system of record. Choose one billing truth source before you build automation: platform invoice, seller statement, or your internal settlement ledger. Then define ledger linkage from source event to settlement line item to payout instruction, plus audit-trail exports finance can run without engineering. Microsoft also notes some invoice amounts can be reconciled in platform UI reports.

Step 3. Set release controls before launch. Define policy gating, payout approvals, and exception escalation ownership up front. Holds are real in live payout systems: AdSense describes a monthly cycle with issuance between the 21st and 26th only when thresholds and holds are satisfied, and Microsoft reserves the right to withhold seller payment under specified account conditions (for example, outstanding unpaid invoices).

Step 4. Document unresolved unknowns and block full automation until decided. Write down open decisions on timing-model differences, deduction order, and dispute liability allocation across the chain. Industry work still flags supply-chain transparency gaps, and the ISBA/PwC study reports 15% of spend in an unattributable "unknown delta." If those points are unresolved, keep automation in draft and require an explicit decision.

If you want a deeper dive, read What Is a Demand-Side Platform (DSP)? How Programmatic Ad Platforms Manage Publisher Payouts.

Map money and data from bid win to publisher payout#

Build this map before you automate release: every payout line should trace back to a bid-linked identifier and billing record, or it stays on hold.

Step 1 Build one settlement row for each real handoff#

Use one row per operational event: RTB win, billing trigger, document issue, settlement calculation, payout release, and reconciliation close.

| Event | Primary actor | Required linkage artifact | Common break |

|---|---|---|---|

| RTB win | DSP / Ad Exchange | Bid-win record with request/response identifier and buyer billing ID | Missing or inconsistent event ID, so later billing cannot be attributed cleanly |

| Billing trigger | DSP / SSP | Billable event key linked to win record and accrual/pending ledger entry | Trigger fires without a durable link to the auction record |

| Billing document issue | DSP, SSP, or Publisher (by contract) | Billing reference tied to accrued ledger lines and source event set | Document lines cannot be matched to prior billable events |

| Settlement calc | SSP / Publisher finance layer | Settlement batch ID linking billing reference, deductions, and net payable ledger entry | Gross-to-net logic applied against incomplete or stale source records |

| Payout release | Publisher payout operator or platform | Payout instruction ID linked to settlement batch and billing reference | Duplicate retries without idempotency create double-release risk |

| Reconciliation close | Finance / Ops | Close record tying payout status, billing reference, and source-event totals | Delayed status updates leave ledger and payment state out of sync |

Keep ownership explicit across Advertiser, DSP, Ad Exchange, SSP, and Publisher, and make sure your internal records can reconcile even when partner schemas differ.

Step 2 Force linkage between event IDs, ledger entries, and invoices#

Auction decisions happen fast, while settlement does not, so your identifiers must survive both phases. In Google Authorized Buyers, winning happens in the auction flow and bidder response windows run 80 to 1000 ms; publisher earnings can remain estimated and finalize at month end.

Use one internal rule: every billable event carries a durable linkage key into the ledger. For each row, capture and retain:

- Source event ID

- Ledger entry ID

- Billing reference (when issued)

If the billing document arrives later, append the linkage instead of overwriting prior IDs.

Step 3 Mark expected divergence vs control failures#

Some variance is expected; some is a release blocker. Estimated versus finalized earnings can differ, including invalid-activity deductions, so your map should label these as expected adjustment classes.

Treat the following as exceptions:

- Missing event IDs

- Unmatched billing lines

- Duplicate retries without idempotency

- Delayed payout or return-status updates that leave reconciliation open

Apply one decision rule: if you cannot explain a variance as timing, a known deduction, or a documented adjustment class, hold release and investigate. That discipline matters in a chain where unattributable spend and opaque value flow are still documented risks.

For a step-by-step walkthrough, see How Staffing Agencies Automate Contractor Disbursements with Batch Payouts via CSV.

Define gross-to-net settlement rules before writing code#

Lock the gross-to-net math before you automate anything. If finance cannot reproduce net payable line by line from raw events, partner terms, and adjustment records, freeze automation and resolve the rule ambiguity first.

Step 1 Write one canonical settlement order#

Document one internal Gross-to-Net Settlement order in plain language: gross media amount, platform Fee Deduction, Revenue Share, adjustments, then net payable. Treat this as your product rule, not a universal rule for every DSP, SSP, or ad exchange contract.

Keep each line auditable. Gross-to-net checks and DSP fee checks are validated separately in reconciliation flows, so avoid collapsing fees and shares into one opaque "take rate" field.

If partner assignments use revenue share, keep the exact percentage tied to the assignment that governed that traffic. Finance should be able to trace each net payout back to that percentage term and the underlying records.

Step 2 Fix deduction precedence and keep it deterministic#

Set one contract-backed deduction precedence and apply it consistently. For each DSP, SSP, or exchange fee, define the calculation base, where it sits in the order, and the contract or assignment that authorizes it.

Use one control rule: the same fee should hit the same base each cycle unless terms changed. This is how you prevent double application and quiet base-amount drift that still looks "close enough" at payout time.

Test reproducibility directly. Run the same event set through the same terms twice and confirm the same net result. Investigate bounded variance where the external process allows it, but do not pass unexplained differences into payout logic.

Step 3 Classify adjustments before they become manual exceptions#

Define adjustment classes as structured transaction types, not free-text notes. At minimum, require a traceable reason code, source record, and link to the original settlement line for each adjustment.

| Adjustment class | Typical trigger | Evidence to retain |

|---|---|---|

| Invalid traffic reversal | Revenue refunded to affected advertisers for invalid clicks or impressions | Platform statement, impacted period, original settlement or billing reference |

| Credit | Commercial correction or approved billing adjustment | Approval record, credit reference, linked counterparty line |

| Clawback | Advertiser non-payment or failed collections on fraudulent advertisers | Reason code, source notice, original payable line, reversal amount |

Keep timing status separate from settlement math. Revenue can post by the 2nd of the month and payment can arrive later in the cycle, but those milestones should not change net-calculation logic. If timing, fee order, or adjustment classes are still disputed, the code is not ready.

Related: Cash Pickup Payouts for Unbanked Contractors in Cash-Preferred Markets.

Choose build in-house or modular payout infrastructure#

For DSP/SSP settlements and publisher payouts, the practical default is usually hybrid: keep settlement logic internal, and use modular infrastructure for onboarding, verification, payout execution, and status tracking unless you have a clear reason to own all of it.

After you lock gross-to-net logic, the decision is not an abstract "build vs buy." Decide which layers are truly tied to your DSP/SSP economics and which mostly add compliance and reliability workload.

Step 1 Separate settlement logic from payout plumbing#

Keep commercially specific logic close to your ledger: fee precedence, revenue share, clawbacks, dispute-linked adjustments, and partner-specific exceptions. If those rules vary by counterparty or assignment, direct control over calculations and evidence is usually worth it.

Be more cautious about building onboarding, KYC collection, payout rails, and status tooling from scratch. Provider documentation is explicit that prebuilt onboarding can reduce compliance and operational complexity, and requirements can change over time. A useful boundary is this: if change is driven by your ad economics, keep it internal; if change is driven by verification or payment-regulation shifts, modular infrastructure is often the better owner.

Step 2 Pick the lightest onboarding model that still gives enough control#

You are not limited to fully in-house or fully outsourced.

| Option | Control you keep | What gets easier | Main tradeoff |

|---|---|---|---|

| Build in-house | Full control over UI, verification flow, payout release logic, and custom data capture | Maximum flexibility for unusual partner cases | Highest lift for policy gating, requirement updates, support operations, and payout reliability |

| Modular with API onboarding | You build onboarding UI with provider APIs | Keep UX control while using provider account and payout capabilities | More integration work than hosted flows; you may still own parts of verification operations and communications |

| Modular with hosted onboarding | Provider-hosted onboarding flow | Fastest start; hosted flows can adapt to changing requirements | Less flexibility for unusual onboarding or branded edge cases |

Stripe documents API onboarding as building your own customized onboarding UI via API, while Adyen recommends hosted onboarding as the default start. That choice directly affects how much verification-change work stays with your team.

Step 3 Validate retry safety and audit evidence before committing#

Modular infrastructure can speed launch, but it does not eliminate ownership. You still need internal controls for approvals, exceptions, and release decisions.

Prioritize predictable behavior under retries and partial failures. If the in-house path cannot demonstrate safe retries, or the modular path cannot expose enough payout status detail for reconciliation, the design is not ready. Before finalizing architecture, require one traceable evidence chain for a sample payable line: settlement line ID, approval record, connected-account/beneficiary status, verification state, payout instruction ID, and final payout status.

If economics are highly custom, keep settlement core logic internal and externalize payout rails. If the pressure is delivery speed, compliance drift, and limited staffing, start modular, typically with hosted onboarding first, then move to API-led onboarding only when the added control justifies the added operational surface.

Related: AdTech Platform Payments: How DSPs SSPs and Ad Networks Pay Publishers in a Cookieless World.

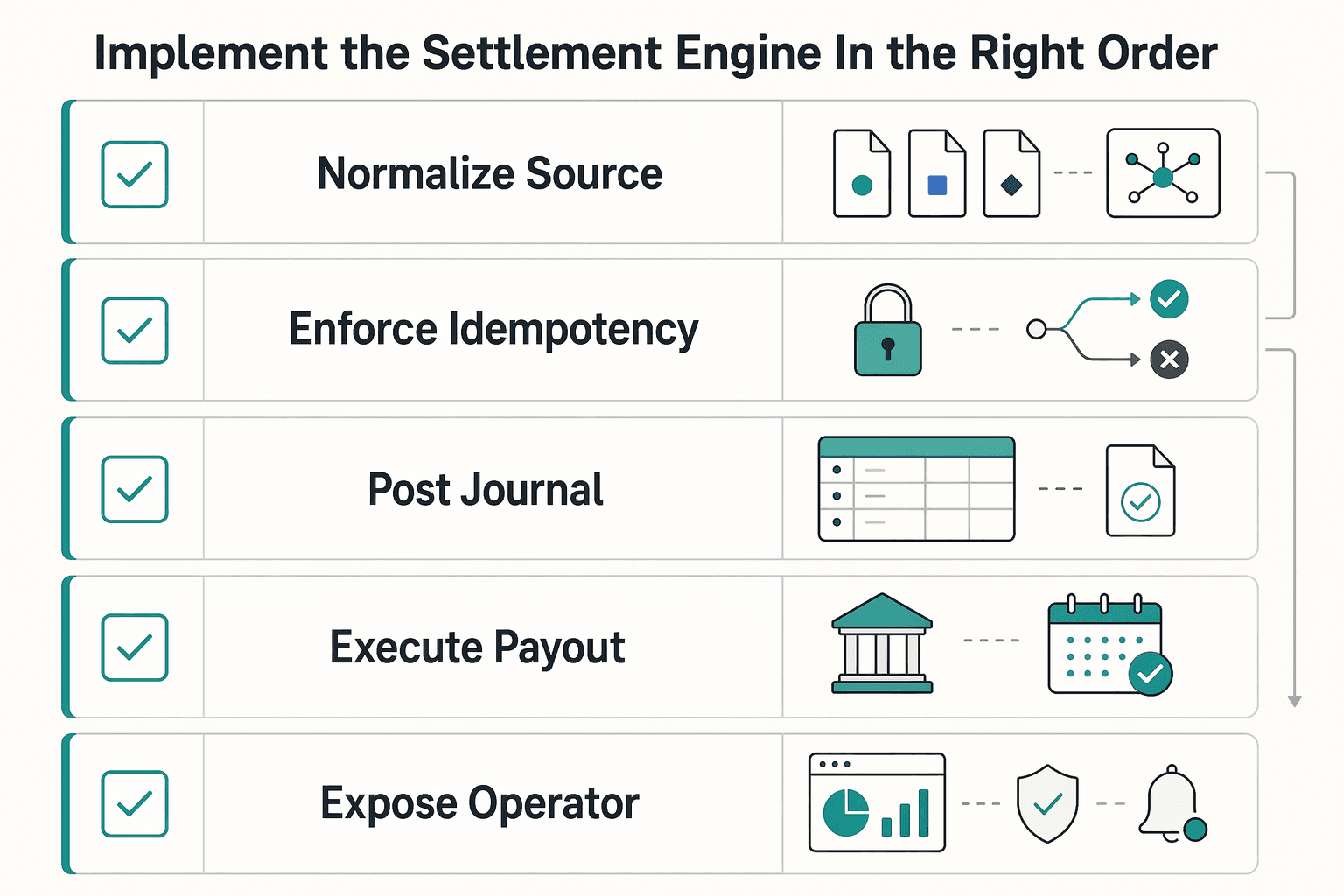

Implement the settlement engine in the right order#

Build the engine in this sequence: lock IDs, make retries safe, link the ledger, then move money. If you reverse that order, you can still send payouts, but you lose auditability and duplicate-payment protection.

| Engine step | Required control | Checkpoint or detail |

|---|---|---|

| Normalize source events | Ingest DSP, SSP, and ad exchange records into one internal settlement event model, preserve stable upstream IDs, and assign an internal settlement event ID | OpenRTB provides a globally unique bid request or auction ID, and bid responses may include bidder-generated IDs for logging and tracking. |

| Enforce idempotency | Require idempotency keys for journal posting, payout instruction creation, payout release, and reversals or clawbacks | Reusing the same key should return the same result, including server-error responses. |

| Post journal entries | Use an immutable ledger engineered with double-entry principles and link each journal entry to the settlement event, invoice or billing line, and payout instruction or payable record | Rule: no orphan entries. |

| Execute payout batches | Treat payout execution as asynchronous and reconcile only after terminal outcomes | One documented lifecycle is pending -> in_transit -> paid/failed/canceled, with failed or canceled outcomes possible within 5 business days. |

| Expose operator checkpoints | Show pending approvals, blocked payouts, failed disbursements, returned or canceled payouts, and reopened disputes in the UI and API | At month end, finance should retrieve pending items, block reasons, payout status, and expected-net versus paid-net deltas without engineering intervention. |

- Step 1 Normalize source events into one settlement event model

Ingest DSP, SSP, and ad exchange records into one internal settlement event model, and preserve stable upstream IDs. OpenRTB provides a globally unique bid request or auction ID, and bid responses may include bidder-generated IDs for logging and tracking. Keep those IDs when present, then assign your own durable internal settlement event ID.

Checkpoint: for one payable line, trace billing line -> settlement event -> upstream auction or bid identifiers without raw-log forensics. If one economic event can enter twice with no stable dedupe path, fix this before automating calculations.

- Step 2 Enforce idempotency on every posting and payout action

Require idempotency keys for every money-state action: journal posting, payout instruction creation, payout release, and reversals or clawbacks. The key should represent the business action, not a single network attempt.

This is the retry control. Reusing the same key should return the same result, including server-error responses, so retries do not create a second object or execute the update twice. If retries generate new keys, the control is broken.

- Step 3 Post journal entries with strict ledger linkage

After normalization and idempotency, post into an immutable ledger engineered with double-entry principles. Link each journal entry to the settlement event, invoice or billing line, and payout instruction or payable record.

Rule: no orphan entries. From any counterparty balance movement, your team should be able to show source event, billing line, and payout instruction quickly.

- Step 4 Execute payout batches through explicit status transitions, then reconcile

Treat payout execution as asynchronous. One documented lifecycle is pending -> in_transit -> paid/failed/canceled, with failed or canceled outcomes possible within 5 business days. Do not assume every provider uses identical status names.

Release only after approvals, then reconcile by counterparty expected net versus paid net. Marking a batch complete at submission is too early; completion should follow terminal outcomes and reconciliation.

- Step 5 Expose operator checkpoints in the UI and API

Expose operational states directly in UI and API: pending approvals, blocked payouts, failed disbursements, returned or canceled payouts, and reopened disputes where applicable. Operators need status views that match the real lifecycle from initiation through approvals and reconciliation.

At month end, finance should be able to retrieve pending items, block reasons, payout status, and expected-net versus paid-net deltas without engineering intervention.

For a full breakdown, read Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Add controls for disputes clawbacks and failed payouts#

Exceptions need first-class controls, not manual cleanup. Treat disputes, clawbacks, returned payouts, and compliance holds as settlement states with explicit records, owners, and posting rules so net position stays accurate.

| Exception area | Required record or control | Specific detail |

|---|---|---|

| Disputes | Start in an unsubmitted state and store settlement event ID, billing line, counterparty, reason, amount in question, evidence checklist, owner, due date, and outcome | One documented path expires after 110 days from transaction clearing if the dispute is not submitted. |

| Clawbacks | Create a distinct transaction with reason code, source reference, linked billing record, and auditable journal entries that can be reversed if needed | This includes invalid-activity adjustments where revenue is refunded to affected advertisers. |

| Failed payouts and holds | Track failed, returned, and canceled states directly, store failure reasons on the payout instruction, and queue compliance and verification holds with blocked payouts | ACH return code R03 ("No Bank Account/Unable to Locate Account") can surface within 2 Banking Days. |

| Re-release checks | Require linked billing record present, prior payout history visible, and updated net position reflecting every posted dispute or clawback | If any check fails, keep the item blocked until records are complete. |

Step 1 Define a dispute workflow that cannot skip evidence. Start each dispute in an unsubmitted state, capture required intake fields, and require a complete evidence pack before submission. Store the settlement event ID, billing line, counterparty, reason, amount in question, evidence checklist, owner, due date, and outcome, then write the outcome back to the linked settlement record and net position. If you rely on provider-backed disputes, timing can decide the result: one documented path expires after 110 days from transaction clearing if the dispute is not submitted, and incomplete packets can lose on quality alone.

Step 2 Post clawbacks as a first-class transaction type. Do not bury clawbacks in notes or unlabeled negative adjustments. Create a distinct transaction with reason code, source reference, linked billing record, and auditable journal entries that can be reversed if needed. This keeps a clean chain from original earning to deduction to any reinstatement, including invalid-activity adjustments where revenue is refunded to affected advertisers.

Step 3 Add explicit recovery paths for failed payouts and holds. Track failed, returned, and canceled states directly, and store failure reasons on the payout instruction. For beneficiary-detail failures, a concrete case is ACH return code R03 ("No Bank Account/Unable to Locate Account"), which can surface within 2 Banking Days. Put compliance and verification holds in the same operational queue so blocked payouts are not retried as if they were ordinary technical failures.

Step 4 Require exception checks before re-release. Before reissuing or releasing an adjusted payout, require three checks: linked billing record present, prior payout history visible, and updated net position reflecting every posted dispute or clawback. If any check fails, keep the item blocked until records are complete.

Related: How to Lock In FX Rates for Contractor Payouts Using Forward Contracts.

Verify close and audit readiness every settlement cycle#

If finance cannot close the period without engineering reconstructing transactions, your settlement process is not done.

Step 1 Run a close checklist that ties cash to records#

Run four checks each cycle: statement-to-ledger tie-out, open exception count, payout completion rate, and unresolved dispute aging. Start with the cash-to-GL check, because it compares GL cash account balances against bank balances and highlights unreconciled journal entries and bank statement lines.

Validate this on a closed payout batch: bank movement, ledger posting, and payout batch total should match. Treat any batch marked paid in ops with unreconciled bank cash activity as a close blocker.

Step 2 Trace every payable line end to end#

Each payable line should have one continuous audit trail from source event to billing document to payout status. In practice, the event ID, linked line item, journal entry, and payout instruction or batch reference should all be queryable without manual stitching.

If a sample still needs ad hoc SQL or spreadsheet matching, you are not audit ready. Transaction-level settlement reporting is built for this, so reconciliation is possible per transaction, not only at aggregate totals.

Step 3 Export a finance evidence pack without engineering#

Finance should be able to export monthly close evidence directly from reporting. A practical pack can include a settlement summary, deduction log, dispute log, and payout register, exported as CSV or equivalent. A payout reconciliation report helps preserve transaction-to-payout linkage for audit review.

Use external benchmarks as context, not policy. eMarketer, citing GroupM, reported global ad revenues at $1.04 trillion in 2024 and $1.1 trillion in 2025; that supports stronger verification discipline, but it should not set your internal settlement thresholds.

Build a settlement system your finance team can close#

You are ready to automate only when finance can reproduce one publisher net payout from contract terms, source records, ledger entries, and payout history. DSP/SSP/ad exchange definitions are table stakes; close-ready settlement, reconciliation, and payout controls are the differentiator.

- Confirm commercial terms before modeling.

Pull signed terms for Revenue Share, Fee Deduction, clawbacks, dispute ownership, billing ownership, and the entity that owes the publisher. Do not assume a universal deduction order across counterparties. Your checkpoint: finance and ops can point to the clause or schedule for each deduction and adjustment class.

- Map bid-to-payout with one paid entity per payment path.

Build a row-level map from bid win to billing trigger, line item, journal entry, payout instruction, and payout status. For each row, record actor, source record, and ledger touchpoint. Keep seller mapping unambiguous: each Seller ID should map to a single entity paid for that inventory.

- Lock gross-to-net rule order and adjustment classes.

Define one canonical rule order before implementation. Include explicit classes for deductions, credits, and clawbacks with reason codes, since earnings may be adjusted. Verify by reproducing net payable from raw events and documented rules without spreadsheet-only logic.

- Enforce idempotency and ledger linkage before payout batches.

Use idempotency keys on posting and payout actions so retries do not create duplicate side effects. Link each settlement event to its billing line, journal entry, and payout instruction before funds move. If a retry cannot be explained through a clean ledger chain, treat that as a control gap.

- Gate release with holds, disputes, and approvals.

Separate payout creation from payout release. Check payment holds before issuing funds, and require approval paths for disputes and exception cases. If you run a monthly cadence, resolve exceptions before the release window rather than after.

- Prove close readiness with repeatable reconciliation and exportable evidence.

Reconcile each payout as a settlement batch, with a reconciliation report (or equivalent download path) and exportable payment history (for example, CSV). Build an evidence pack that includes settlement summary, deduction log, dispute log, payout register, and payment history export. If one payable line cannot be traced end to end from source event to payout status, block launch.

Related reading: How to Build a SaaS Marketplace That Manages Subscriptions and Contractor Payouts.

Frequently Asked Questions

Who pays publishers in programmatic advertising when both a DSP and SSP are in the chain?

There is no universal rule across every contract. The publisher is generally paid by the entity that holds the publisher settlement obligation in the contract, statement, and payout process. If that owner is not explicit on the billing document and payout register, treat it as a setup gap before you automate.

How are DSP, SSP, and ad exchange fees deducted before publisher payout?

There is no fixed industry-wide deduction order, which is why your gross-to-net rules need to be documented before code. In practice, fees and adjustments are applied according to contract terms, then the remaining net amount becomes the publisher payable. A red flag is when finance can explain net payout only with spreadsheet logic that does not match the contract or settlement engine.

What is the practical difference between RTB auction pricing and settlement payout operations?

RTB decides impression pricing at auction time, within milliseconds, using impression-level bidding. Settlement and payout happen later, often on a longer operating cycle, and some publisher payment programs run monthly, with one published example issuing payments between the 21st and 26th of the month. If you mix those layers together, you end up trying to use auction logs as if they were payout records, and the close will break.

What records are required to reconcile programmatic payouts end to end?

At minimum, you need an event identifier from the auction side, the commercial record that created the receivable or payable, the accounting record, and the payment record. A strong evidence chain can include a bid request ID, impression linkage through impid where relevant, billing line, journal entry, payout batch or instruction, and payment history export in CSV or equivalent. Your verification check is simple: pick one payable line and confirm those records connect without manual stitching.

Where does the commonly cited platform take in programmatic supply chains come from, and what remains unknown?

A lot of discussion traces back to the ISBA and PwC programmatic supply chain study summary using Q1 2020 data. That summary reported 15% of spend as an unattributable "unknown delta," which is useful as a transparency warning but not as a fee schedule for your business. What often remains unknown is the exact path of every deducted amount in a specific chain, so do not use that study as a substitute for counterparty-level reconciliation in programmatic advertising payouts dsp ssp settlements.

What is often missing in DSP vs SSP explainers for finance and ops teams building settlement automation?

Definitions alone often do not tell you who posts the liability, when deductions are applied, or which record is the source of truth when numbers disagree. The missing layer is operational: stable IDs, ledger linkage, dispute handling, payout status tracking, and an exportable evidence pack that finance can review without engineering. If you are building settlement automation, that detail matters more than another high-level diagram of the programmatic advertising payouts dsp ssp settlements chain.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- docs.stripe.com/issuing/purchases/disputestrusted

- support.stripe.com/questions/where-is-my-payout-faq-for-late-an...trusted

- admanager.google.com/home/resources/how_authorized_buyers_work_wi...external

- advertising.amazon.com/library/guides/dsp-ssp-dmp-differenceexternal

- advertising.amazon.com/library/guides/demand-side-platformexternal

- developers.google.com/authorized-buyers/rtb/get-started/startexternal

- iabtechlab.com/standards/openrtbexternal

- iabuk.com/news-article/cross-industry-programmatic-tas...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is a Demand-Side Platform (DSP)? How Programmatic Ad Platforms Manage Publisher Payouts

Do not use a DSP as a stand-in for payout infrastructure. If you are expanding a programmatic business, the first decision is not which buying tool looks strongest. It is where buying ends, where settlement begins, and who actually owns publisher payment outcomes.

How DSPs, SSPs, and Ad Networks Pay Publishers in a Cookieless Market

If you are evaluating this market, focus on payment execution before role labels. The hard part is not memorizing definitions. It is knowing who bills whom, when cash is released, and what can break between an auction win and a publisher payout as identity signals get less reliable. We recommend starting there so your team does not confuse market labels with payout accountability.

Integrated Payouts vs Standalone Payouts for Platform Architecture Decisions

**Treat integrated and standalone payouts as an architecture decision, not a product toggle.** The real split is the same one you see in payment processing more broadly: either payments are connected to the core platform experience, or they are not. [Lightspeed](https://www.lightspeedhq.com/blog/payment-processing-integrated-vs-non-integrated) puts that plainly in POS terms: your payment terminal either speaks to your point of sale, or it does not. For platform teams, the equivalent question is whether payment flows run through one connected system or sit in separate lanes you manage independently.