Quick Answer

Use a forward when payout timing and currency needs are predictable, then set coverage to the committed core instead of the full forecast. Confirm entity authority, corridor compliance, and provider settlement constraints before booking. Tie each trade to a specific payout cycle, enforce approval checkpoints on trade date, and keep execution controlled with idempotency keys, webhook-driven status updates, and ledger journal reconciliation through contract maturity date.

Recurring Contractor Payouts Create FX Cost Uncertainty That Forward Contracts Can Control#

Step 1 Name the exposure#

Recurring cross-border contractor payouts create FX cost uncertainty. You approve a payable, then settle later after exchange rates move. That gap can change the cost of a batch by payout day and introduce margin uncertainty.

Once that pattern repeats, FX risk stops being a finance footnote. It becomes an operating input that affects payout cycles, funding, and margin planning.

Step 2 Use a forward to fix the future rate#

A forward is a practical way to replace that uncertainty with a known future rate. In FX, it is an agreement to lock an exchange rate now for settlement at a future date.

The tradeoff is simple: you get cost certainty, not a guaranteed better outcome than spot every time. You are choosing predictability over the chance to benefit from a favorable market move later.

This guide focuses on execution. It shows how to decide whether a forward fits your payout model. It also shows how to line contract timing up with payout cycles and maintain an audit trail that finance, ops, and engineering can all verify.

Step 3 Verify scope and constraints before you book#

Do not assume every provider supports every corridor, settlement path, or payout feature in the same way. Capabilities vary by market and program, so confirm constraints before you hedge. For example, a provider may support presentment in over 135 currencies while settlement support still differs by country, and another may define 4 payout feature levels with country-level conversion restrictions. Before booking, verify:

- the destination settlement currency your payout account accepts

- whether your provider supports that conversion and payout path for your specific country or program

- any contractual and internal approval requirements that apply before execution

This guide covers operational decisions and implementation checkpoints. It does not provide legal, tax, or accounting advice, and provider terms can vary by market and program. Related reading: How to Calculate Cap Rate for a Rental Property.

Decide whether a forward is the right hedge for your payout model#

Use a forward when payout timing and currency needs are predictable enough that you will actually need the currency by maturity. If both dates and amounts are unstable, consider not hedging the full forecast at once.

Step 1 Test payout predictability#

Start with suitability. A forward works best when the payout is likely to happen and the currency need is real by maturity. That matters more than trying to guess market direction.

Start with operations, not markets. Can your team point to recurring payout windows and committed currency needs with enough confidence to book? If not, start with partial coverage. Hedging part of expected volume, such as 50%, is a practical way to cut overcommitment risk.

Step 2 Choose certainty over upside on purpose#

A forward rate gives you budget certainty for a future payout conversion. If batch timing is fixed and margins are tight, that predictability is often the reason to hedge.

Be explicit about the tradeoff. Once you lock the rate, you do not benefit if spot later moves in your favor. Because business conditions can change after booking, treat the contract as a real obligation, not as a flexible option.

Step 3 Set go/no-go from payout criticality#

If you run large recurring payout batches and adverse FX moves could materially pressure margins, lean toward hedge certainty. If exposure is less predictable, start with lighter coverage and increase it only as forecast reliability improves.

A useful test is simple: would an FX move create a material variance in payout costs or margins? If yes, hedging should move up the priority list.

Step 4 Assign ownership before the first trade date#

Clear ownership matters as much as hedge design. Roles can vary by organization, but control separation should not. Set responsibilities for policy and approvals, execution timing, and system traceability before the first trade.

Apply segregation of duties in practice. One person should not be able to both commit and conceal errors. Define who proposes, who approves, and who verifies the post-trade record trail.

Related: How Blockchain and Smart Contracts Will Change Marketplace Payouts by 2030.

Gather prerequisites before you book anything#

Do not book a forward until you can show three things: documented exposure, clear execution authority, and corridor-level compliance readiness by trade date. The hedge should match a real future currency need and exposure you can reasonably settle.

| Prerequisite | Confirm/include | Why it matters |

|---|---|---|

| Exposure file | Paying entity, payout corridor, expected amount, and expected payout date or period | Baseline for a forward agreed now for settlement on a specific future date |

| Legal and execution authority | Booking entity, provider account enabled for that entity, trading agreement, and authorized executor | Booking may fail at execution if the approved entity or authorized executor is wrong |

| Corridor compliance gates | CIP/KYC, beneficial-owner checks, and AML readiness for the booking entity and each payout corridor | Open compliance items could block settlement or payouts |

| Review pack | Forecast assumptions, approved hedge coverage, linked exposure file, and named rollback owner | Makes the chosen amount, currency, and date window traceable |

Step 1 Build the exposure file#

Build one exposure file by currency and payout date window, then reconcile it to your internal forecasts. For each line, record the paying entity, payout corridor, expected amount, and the date or period when the payout is expected to occur.

This is your baseline because a forward is agreed now for settlement on a specific future date. Keep committed payouts separate from softer pipeline volume so you do not hedge uncertain demand as if it were firm.

Step 2 Confirm legal and execution authority#

Before requesting pricing, confirm which legal entity will book the trade. Confirm that the provider account is enabled for that entity and what trading agreement is in place, whether a master agreement or provider equivalent. Account onboarding alone does not mean you are ready to book forwards.

Also confirm who is authorized to execute on trade date, with documented authority and signatory coverage. If the approved entity or authorized executor is wrong, booking may fail at execution.

Step 3 Clear corridor compliance gates#

Check CIP/KYC, beneficial-owner (KYB-style) checks, and AML readiness for the booking entity and each payout corridor before booking. Identity verification is risk-based, beneficial-owner verification can apply to legal entities, and AML controls are expected to reflect geographic risk.

Treat this corridor by corridor, not as a single global pass/fail. If open compliance items could block settlement or payouts, limit coverage to exposure you can actually settle.

Step 4 Assemble the review pack#

Assemble the approval pack before execution. Include forecast assumptions, approved hedge coverage, the linked exposure file, and the named rollback owner if volumes change. If you plan formal hedge documentation, set it up at inception rather than after the trade.

Attach the pack to the approval record so the chosen amount, currency, and date window are traceable. Thin records make later reviews and ownership handoffs harder.

Set hedge coverage and tenor with explicit decision rules#

Set coverage and tenor with one principle: hedge what you can defend, and stage the rest as certainty improves. Do not turn weak forecast volume into a firm forward position just to get budget certainty.

| Timing | Coverage | Context |

|---|---|---|

| three- to nine-month period | about 80% of forecast exposure | Use as an example, not a rule |

| 6 months | 80% | common layered example |

| 12 months | 50% | common layered example |

| 18 months | 20% | common layered example |

Step 1 Hedge the committed core first#

Do not treat projected contractor payouts as one blended total. Split them into confidence bands. Hedge the committed core first: the volume you reasonably expect to settle on time and in size, based on the strength of your forecast.

A practical treasury benchmark is about 80% of forecast exposure over a three- to nine-month period in rolling programs. Use that as an example, not a rule. Stable recurring flows can often support higher near-dated coverage. A variable tail should stay unhedged until forecast quality improves.

If you need hedge documentation, specify timing and magnitude clearly enough to identify the hedged transactions when they occur. A percentage-only definition is not specific enough by itself, so tie coverage to clear time buckets, currencies, and amounts.

Step 2 Match tenor to actual payout timing#

Choose tenor from actual payout timing, not from a generic tenor rule. If you use monthly or other time buckets, make sure they match how payouts actually occur. Maturity should line up with when payout cash is really needed. If payouts cluster on specific cycle dates, align maturities to those windows or use a structure that can settle across specified dates.

This reduces mismatch risk. If hedge maturity and expected cash-flow timing do not line up, ineffectiveness can follow.

Use a hard check before approval: every forward should map to a payout cycle in the exposure file, with currency, amount, trade date, and contract maturity date visible.

Step 3 Stagger bookings instead of going all in once#

If forecast certainty improves over time, layer the hedge rather than booking the whole position at once. The goal is not perfect market timing. It is to average decisions over time as exposure becomes more certain. As one treasury lead put it: "It is difficult to time specific events in the market; instead, we aim to average over a period of time."

In practice, split exposure across multiple trade dates. A common layered example is 6-, 12-, and 18-month layers at 80%, 50%, and 20%, with higher coverage nearer maturity. For contractor payouts, use the same logic across your operating horizon by topping up as payout approvals firm up.

Step 4 Set top-up and re-hedge triggers before booking#

Do not rely on ad hoc judgment after the trade is on. Define review triggers before the first trade. You do not need one fixed percentage, but you do need clear events: drift in expected amount or timing, or sudden payout growth above the hedged core.

Keep each top-up decision auditable. Attach the updated exposure file, what changed, which payout windows are affected, and whether added volume is committed or still variable. That keeps re-hedging deliberate and limits accumulated mismatch risk.

Choose contract structure and provider terms without surprises#

Pick the structure your payout operations can actually run, not just the one with the best headline rate. Many failures here are operational: timing shifts, batches split, margin requests arrive faster than expected, or cut-off times miss your release window.

Step 1 Match contract structure to payout variance#

Start with the payout pattern. If payouts usually land on one firm date, a fixed-date forward is easier to run. If timing moves within a known range, use an open date forward so settlement can happen during a predefined timeframe rather than on one specific day.

If your provider allows a Delivery Window and Draw Down, partial settlements can happen before maturity. That matters when one planned batch turns into multiple smaller settlements. If your team expects partial settlements but the contract allows only one full settlement date, you can create immediate mismatch and manual overhead.

Check each proposed structure against your last three payout cycles. If normal delays or split approvals would force manual exceptions, the structure is too rigid. Also confirm that flexible drawdown is explicitly included in the signed terms, because it is not universal.

Step 2 Compare risk terms before you compare rates#

Do not shortlist on quoted forward rate alone. Forward pricing reflects interest-rate differentials between currencies, and then provider spread and terms are layered on top. A sharper headline rate can still come with tighter collateral terms or higher unwind risk. Request the same pack from every provider:

- Sample trade confirmation with trade date, pair, notional, and maturity

- Governing agreement or addendum covering collateral, cancellation, and default

- Clear spread policy, whether all-in rate or separate fees

Treat risk language as operational, not boilerplate. These are derivatives, and terms can require material payments from you. Margin or collateral calls may come on short notice and be substantial. One addendum requires a partial prepayment within two business days.

Do not assume one standard deposit model. One provider describes common levels of 5% (business) and 10% (personal), while another offers possible zero-margin structures based on credit. If finance cannot fund a stress margin call without risking payouts, that provider is a liquidity risk.

Step 3 Test settlement mechanics against your payout stack#

A correct hedge still fails if settlement mechanics do not fit your rails. Validate currency coverage, timing rules, and funding behavior before launch.

Coverage and tenor vary by provider. Examples in market materials include 44 currencies and tenors up to two years, and elsewhere two days to 12 months. Use those as reference points only, and confirm that your exact corridors are supported for trading and settlement through your trading entity.

Time rules matter just as much. For cross-currency payments, Barclays states that cut-off uses the earlier cut-off time of the two currencies. An earlier deadline can push release timing later, including to the next business day.

If you plan API scheduling, confirm hard limits early. Convera's docs include: value date no more than 90 days from commitment, commitment at least 5 days in advance, and funding typically 1-3 days before value date. If your workflow schedules far ahead, that changes what can be automated. Run one realistic dry run before go-live and verify corridor-level value-date windows, funding lead times, and cut-offs.

Step 4 Use a one-meeting decision matrix#

Keep the decision pack tight enough for finance, ops, and engineering to review together.

| Criterion | What to confirm | Pass rule | Red flag |

|---|---|---|---|

| Contract structure | Fixed-date only, or open date with delivery window and draw down | Matches payout timing and partial-settlement pattern | Ops expects split batches but contract settles once |

| Pricing visibility | Forward construction, spread policy, sample confirmation | Treasury can explain all-in economics like-for-like | No specimen docs or unclear pricing basis |

| Collateral and margin terms | Deposit requirements, credit exceptions, top-up timing | Finance can fund stress calls without payout disruption | Short-notice top-up with no liquidity owner |

| Settlement operations | Supported corridors, cut-offs, future-date limits | Fits batch cadence and release window | Early cross-currency cut-off breaks release timing |

| Change and exit terms | Amendment flow, cancellation requests, unwind or breakage economics | Owners and approvals are explicit | Team assumes cancellation is free |

Before signing, close open items: onboarding scope, setup steps, minimums, recurring fees, amendment rules, and cancellation economics. A provider may allow cancellation requests up to maturity, but unwind losses can still apply, and some terms require payment within five business days.

If a provider wins on rate but fails on settlement fit or liquidity resilience, it is the wrong contract for your payout system.

Design booking and approval flow across teams#

Set booking up as a controlled handoff across teams, not as an informal treasury action. A clear sequence, role separation, and confirmation logging reduce booking-error risk and make exceptions easier to manage.

Step 1 Freeze the forecast before booking on the trade date#

Freeze the payout forecast before approval and before sending booking instructions externally. In a forward, the rate is fixed on the trade date, so booking against a moving forecast can lock the wrong exposure.

At minimum, freeze and approve the currency pair, intended notional, payout window, and any internal payout forecast ID used for traceability. Require the approver to confirm the forecast version in the booking request. If it changes, route it back for re-approval.

Step 2 Separate proposing, approving, and settlement instruction duties#

Separate duties across roles: one person proposes, one approves, and another handles settlement instructions and reconciliation controls. This follows established control patterns around dual control and segregation of duties, such as initiator, approver, and reconciler. A practical split for contractor payouts is:

- Finance or treasury proposes hedge size, tenor, and structure

- Authorized approver approves the booking

- Payments ops executes settlement instructions and release coordination

- Accounting or reconciliation owner matches booked terms to confirmations and internal records

If your system supports maker-checker flow, use it so transactions move from unauthorized to authorized through checker action. Keep authorization evidence tied to the contract reference, including who created the transaction and who authorized it.

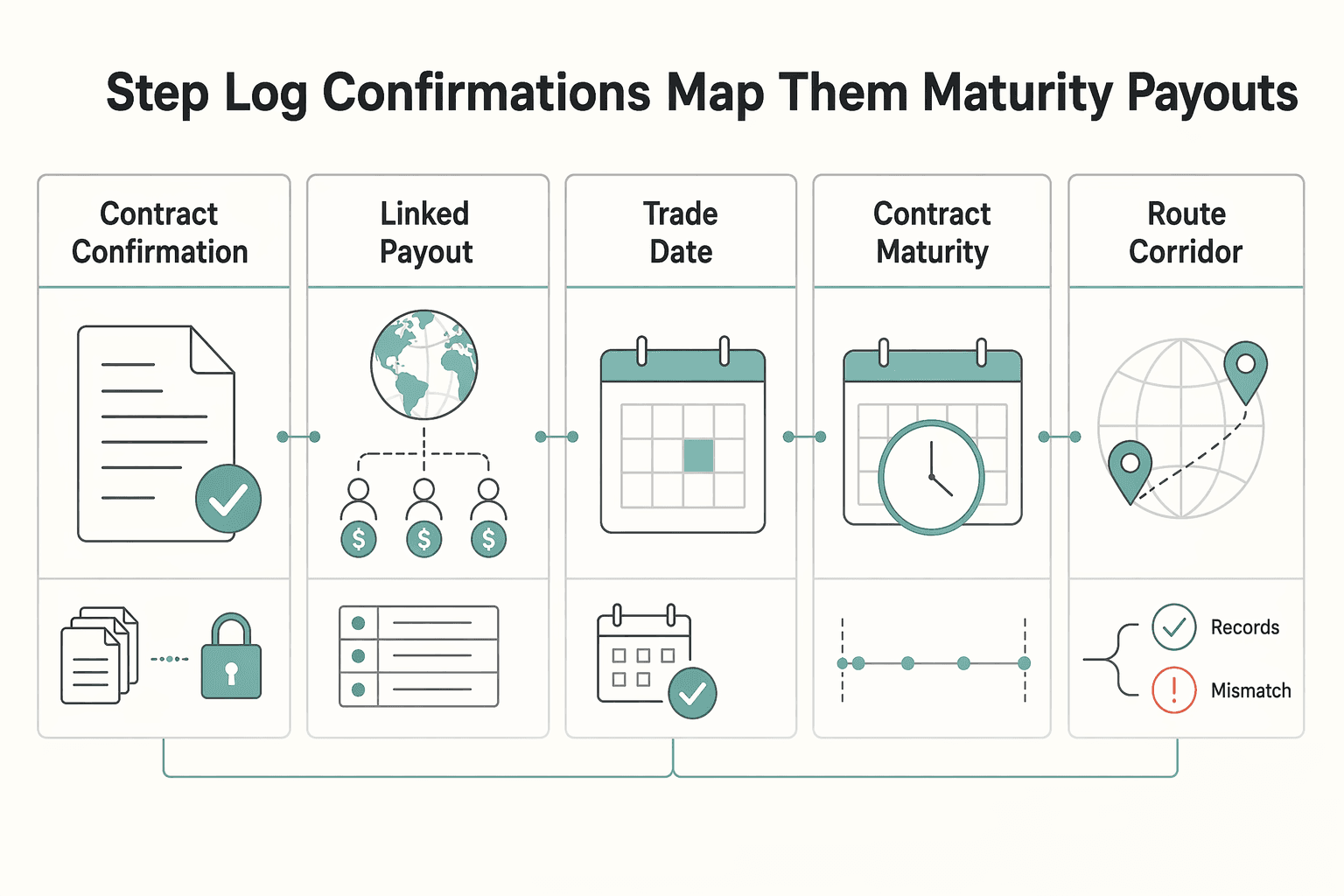

Step 3 Log confirmations and map them to maturity and payouts#

Log and validate the confirmation after booking. Confirmation is a core control because it validates key economic and legal terms, and timely confirmation is part of risk-mitigation frameworks in many jurisdictions. Capture these fields in the booking record:

| Record field | Why it matters |

|---|---|

| Contract confirmation or reference number | Evidence of what was booked with the counterparty |

| Linked payout forecast ID (internal) | Traceability to approved exposure |

| Trade date | Record of when the rate was fixed |

| Contract maturity date | Settlement deadline for the contract |

| Route or corridor | Early check for payout-path fit |

For open forwards, partial drawdowns can happen during the window, but the total amount is still due by maturity date. Validate promptly that confirmation terms match approval on pair, notional, and maturity.

Step 4 Add exception checkpoints before booking proceeds#

Do not let booking continue through unresolved exceptions. Route them through a named escalation path first. At minimum, define exception handling for out-of-policy tenor, unusually large notional, and unsupported currency route. Make the action explicit for each case:

- Unsupported route: stop and return for corridor validation

- Out-of-policy tenor: require additional approval with documented rationale

- Unusually large notional: require documented liquidity-impact review

After authorization, generate system messages or audit log events so finance, ops, and engineering are all working from the same record at settlement time. For a step-by-step walkthrough, see Independent Contractor Status for Cross-Border Freelancer Contracts.

Implement the payout execution path in Gruv systems#

Treat this as an event-driven money path with one control rule: do not release a payout batch until funding, conversion, and ledger journal entries reconcile to the same internal record set.

Step 1 Map the lifecycle from funding intake to batch release#

Use one lifecycle record per funded payout cycle that links funding intake (including Virtual Account rails where enabled), the approved conversion path, and final payout batch release. Treat the Virtual Account as routing and identification for inbound funds, not as proof of a separate stored balance, since virtual-account models can settle into an underlying master account. Keep at least these fields on the execution record:

- internal batch ID

- Virtual Account identifier or funding reference

- currency in, currency out, and target payout amount

- conversion path:

firm quoteor forward settlement reference (when available) - payout batch ID and status

Where forward settlement is enabled, carry the contract reference and settlement date forward from booking. For quoted conversion, store the quote ID and expiry timestamp. Enforce one approved conversion path per funded batch.

Step 2 Enforce idempotent execution on every payout-triggering request#

Require an idempotency key on every payout-triggering request, and treat retries as replays of the same intent. This prevents duplicate conversion or duplicate payout release during timeouts, missing responses, or transient errors.

Persist the idempotency key, a hash of the request body, and the first accepted response or terminal error. If the same key arrives with the same payload, return the stored result. If the payload differs, reject it and raise an operator exception.

Do not hardcode one provider's behavior into Gruv logic. For example, one documented model allows keys up to 64 characters and keeps them valid for at least 7 days. Use that as design input, not as a universal rule. Never generate a fresh key for a retry of the same request.

Step 3 Drive state changes from webhook events, not request submission alone#

Treat request submission as requested, not completed. Advance internal states from webhook events for funding received, conversion completed, payout submitted, payout settled, and payout failed.

That prevents false positives from synchronous API responses. FX settlement failures can still happen for operational, counterparty, or liquidity reasons, so your state machine needs to handle late failures and route exceptions correctly.

Make the webhook consumer idempotent too. Retry patterns differ by provider: Stripe documents automatic resend of undelivered events for up to 3 days, while Adyen documents 3 immediate retries followed by queue-based retries up to 30 days. Design for duplicate delivery, track delivery attempts, and route missing settlement events to a visible exception queue.

Step 4 Post every conversion and payout event to the ledger journal#

Post every money movement to the ledger journal: funding receipt, FX conversion or forward settlement, payout batch release, and failed or returned payout events that affect balances. This is the accounting trace that supports reconciliation.

Tie each journal line to the internal batch ID, external funding reference, quote or forward reference, and payout batch ID. If provider data supports settlement-batch reconciliation, map grouped payouts back to underlying transactions. If not, do not assume that mapping exists in every payout mode. Before releasing the next batch, verify that batch totals match the journaled payout instructions for that batch.

Step 5 Reject stale quotes and route controlled recovery#

Reject expired pricing before it causes an execution error. Check firm quote validity immediately before creating the conversion or transfer, not after failure. Store quote status and expiry, then re-check at execution time.

Some quote products document lock durations of 5 minutes, 1 hour, or 24 hours, with a maximum of 1 day, but the exact window is provider- and product-specific. If a quote has expired, reject execution and route to an approved recovery path only: get a fresh quote, re-approve if economics moved beyond tolerance, or use the prebooked forward route when available.

Do not silently fall back to spot pricing. If you're mapping forward settlement into idempotent payout execution and webhook-driven status handling, start with the implementation surfaces in Gruv Docs.

Reconcile finance records and prove control readiness#

Control readiness means you can reconstruct each hedge and payout from booking through settlement and accounting without gaps. Treat reconciliation as an active-cycle control while forwards are open or settling, not only at month-end.

Step 1 Run reconciliation during active hedges#

During active hedges, run reconciliation on a regular cadence (often daily) across provider confirmations, internal payout state, and the ledger journal when those records exist in your workflow. Use consistent identifiers such as forward reference, trade date, contract maturity date, internal batch ID, and payout batch ID so matching is reliable.

Under EMIR, timely confirmation and portfolio reconciliation are named risk-mitigation techniques for non-centrally cleared OTC derivatives. Federal Reserve FX-settlement guidance also ties risk control to settlement being confirmed and reconciled. Even when those rules do not directly apply to your entity, this operating standard is still useful: treat a hedge as complete only when confirmation, settlement status, and accounting entries agree.

Step 2 Build a month-end pack that supports reconstruction#

At month-end, assemble one evidence pack that can retrace forecast, hedge booking, settlement, and payout outcome end to end. If a settlement or accounting entry is disputed, this pack should let finance and ops reconstruct what happened quickly. A practical pack can include:

| Pack item | Include | Purpose |

|---|---|---|

| Booked forwards | Amendments or cancellations | Hedge booking evidence |

| Provider confirmations | Linked to trade date and contract maturity date | Booking evidence |

| Settlement records | Funding references | Settlement evidence |

| Payout outcomes by batch | Failed or returned payouts | Payout outcome evidence |

| Open exceptions | Current owner and next step, if you track them | Exception status |

| Ledger journal exports | Full accounting trace | Accounting trace |

CFTC swap recordkeeping and reconstruction standards are specific to covered entities, but the reconstruction bar is still a useful control target for platform operations.

Step 3 Close tax and compliance dependencies with reconciliation#

Before period close, verify tax-document and compliance dependencies that affect payout or reporting in your model and jurisdictions. For U.S. reporting contexts, check W-9 completeness where needed for payer information returns. For non-U.S. payees, track [W-8BEN](https://www.irs.gov/forms-pubs/about-form-w-8-ben) when requested by the withholding agent or payer.

Review 1099 mapping against actual payout classification. 1099-NEC Box 1 is for nonemployee compensation, but not every payout maps the same way. Keep VAT dependencies visible in EU VAT contexts where tax treatment or invoicing status affects booking or payout approval.

Step 4 Track adherence metrics and trigger intervention#

Track policy adherence each cycle with stable internal definitions: hedge coverage versus approved forecast, settlement timeliness, exception rate, and forecast-driven rework. You do not need external benchmarks to use these signals, but you do need consistency.

Set explicit intervention rules. If forecast-miss rework keeps rising, reduce coverage scope or shorten tenor on future bookings. If settlement timeliness or exception rates degrade, move from routine flow to manual review until the root cause is identified.

Manage risk when forecasts or markets move against plan#

Once you book forwards, a key risk is mismatch. Payout forecasts can move while the contract obligation stays in place, so the key is to detect drift early and decide what to do before settlement pressure builds.

Step 1 Escalate volume drift before the hedge becomes the problem#

Treat falling payout volume as an immediate finance escalation. A forward is still a commitment to exchange two currencies at a fixed rate on a specified future date. If actual contractor payouts drop below hedged amounts, decide quickly how to manage the mismatch under provider terms.

If you use IFRS 9 hedge accounting, trigger finance early. A reduction in highly probable forecast transactions can require partial termination, and if a forecast transaction is no longer highly probable, discontinuation logic may apply. Do not wait until contract maturity date to surface the mismatch.

Verification point: compare current forecast, hedged notional, and approved payout volume by currency and maturity window. Include trade date, contract maturity date, provider confirmation reference, latest payout forecast, and amendment or offset approver in the escalation pack.

Step 2 Pre-fund the liquidity response to a margin call#

Assume liquidity pressure can happen and assign ownership before launch. Margin-call amount and timing depend on provider terms, and adverse market moves can trigger additional calls where contracts allow them.

Name one funding owner, whether treasury, finance, or a designated cash manager, and define a clear escalation path if cash is tight. This is a governance control, not just a legal review item, because unclear ownership during stress can delay payout response.

Verification point: document the funding source, approver, and transfer timing for emergency liquidity. If your provider can request funds faster than your approval chain can release them, you have a continuity gap.

Step 3 Add scenario rules for growth and route disruption#

Predefined scenario rules let you respond without rebuilding the whole program. If payout volume rises, add hedge layers for incremental exposure where policy allows. A rolling hedge approach supports this by renewing or adding hedges over time.

Set one explicit trigger: when approved payout volume exceeds covered core exposure, finance can book an additional layer after forecast validation. If settlement infrastructure is unavailable or unsuitable for that route, shift to triage: prioritize critical payouts, pause lower-priority batches, and communicate delays early.

BIS has noted that settlement risk remains material in deliverable FX, including an estimate of $2.2 trillion still at risk on a given day in April 2022.

Step 4 Report the risk in the right language#

Call the instrument what it is: a derivative financial instrument. That keeps obligation risk visible to finance, accounting, and leadership approving liquidity decisions.

In your monthly risk note, state four items clearly: hedged amount versus current forecast, contracts at mismatch risk, margin or collateral exposure under provider terms, and routes with elevated settlement risk. Also note the core tradeoff: locking a forward rate protects downside but removes upside if spot later moves in your favor.

Common mistakes and how to recover quickly#

When failures happen, treat them as control problems first: pause new bookings, fix the blocking control, and restart only with cleared volume.

Step 1 Verify compliance readiness before the next hedge cycle#

Do not book a major hedge cycle on assumed readiness. CDD expectations center on identification, beneficial ownership, relationship purpose, and ongoing monitoring, so legal-entity readiness can still fail if records are stale.

Operational recovery: run an internal pre-cycle CDD readiness check for the entity and corridor in scope, including beneficial-owner records and monitoring flags. Attach that status to the booking pack, and hold the hedge if any item is under review. If blocked, reduce coverage to payout flows that are already cleared.

Step 2 Hedge only the committed core when forecast confidence is weak#

If forecast confidence is mixed, do not lock the full forecast. Under IFRS 9 cash-flow hedge logic, forecast transactions must be highly probable, and uncertainty in both timing and magnitude matters.

Operational recovery: hedge committed core volume first, then add staged bookings as approvals firm up. If forecast quality drops after booking, stop adding tenors and recut coverage to the defensible portion.

Step 3 Enforce traceability for every payout state change#

Without traceability, retries can create duplicates and status breaks become hard to resolve. Use an idempotency key on each payout or conversion request so retries do not create a second operation, and capture webhook events for asynchronous state changes.

Operational recovery: maintain your own request-to-result mapping and reconcile webhook states back to it. Do not treat webhooks alone as a complete audit trail.

Step 4 Run daily exception checks against the ledger journal#

Do not wait for month-end-only reconciliation when hedges are active. Run a daily exception check across prior-business-day confirmations, internal payout states, and the ledger journal. FCA CASS 7.15's prior-business-day internal reconciliation model is a practical benchmark.

Operational recovery: assign same-day owners for exceptions and block the next batch until they are resolved, including missing journal entries, unmatched webhook events, or payout states marked sent without matching confirmation.

Conclusion and copy-paste launch checklist#

Use forwards when payout timing and FX exposure are predictable enough that rate certainty matters more than potential spot upside. If forecast quality is still uneven, hedge only the committed core first, because a forward is a binding commitment once booked.

The payoff comes from execution, not from the instrument alone. You only realize hedge value when booking, approvals, settlement instructions, payout processing, and reconciliation all stay aligned to the same exposure and contract maturity date.

- Confirm the exposure map by currency, date window, and owner.

Keep one shared view of notional, timing window, and owner so finance, ops, and engineering are working from the same forecast.

- Verify

master agreementand approval roles beforetrade date.

Confirm that the governing agreement is executed and that approval and instruction roles are documented before booking day.

- Set hedge coverage and tenor rules tied to payout predictability.

Size and duration should follow forecast confidence, and each booked amount should map to a defined payout population.

- Validate provider terms for collateral and settlement mechanics.

Check deposit or collateral requirements, settlement instructions, and amendment or cancellation economics, including possible mark-to-market cost; where applicable, confirm whether variation margin can apply.

- Enforce

idempotency key,webhook, andledger journalcontrols.

Make retries safe, ensure async provider events update internal status, and keep booking-to-payout ledger traceability end to end.

- Run daily reconciliation and exception review until all hedges mature.

Match provider confirmations, payout state, and accounting records daily, and close each exception with a named owner until every hedge is settled, amended, canceled, or unwound.

When your hedge policy is defined and you need controlled batch execution with traceable payout states, review Gruv Payouts.

Frequently Asked Questions

Can you lock FX rates for recurring contractor payouts, or only one-off payments?

You can do both. A standard forward is set for a specific future date at a fixed rate, while a window forward can settle across multiple specified dates, which can fit recurring payout schedules. Before booking, confirm that your provider supports the settlement pattern your payout operations require.

How far in advance should a platform hedge payout exposure with forward contracts?

There is no single universal lead time. Published ranges differ, including 3 days to 1 year in one source and two days to 12 months in a provider example, so your minimum and maximum tenor should be provider-verified. If you are applying hedge-accounting logic, only designate forecast payouts that are highly probable.

What do we give up when we lock a forward rate instead of staying on spot?

You give up upside on the hedged amount if spot moves in your favor before maturity. The tradeoff is straightforward: more rate certainty on the hedged portion, less ability to benefit from favorable FX moves. Set coverage with that tradeoff explicit, not assumed.

What happens if actual payout volume is lower than the amount we hedged?

You can still be obligated to transact at maturity even if actual payout need drops. If the contract is no longer needed, cancellation or unwind can create a cost or a benefit based on prevailing market rates. Treat over-hedges as a position to manage early, not at maturity.

Do forward contracts improve budgeting and margin planning for marketplaces?

They can improve planning for the portion of payout exposure you hedge and settle. The practical benefit is a fixed rate and greater cash-flow certainty for budgeting. For margin planning, treat that certainty as conditional on actual volumes, since positions that are no longer needed may need to be unwound at prevailing market rates.

What operational data should finance, ops, and engineering prepare before booking?

At minimum, align on currency pair, notional amount, and settlement date. Pair that with clear settlement instructions and internal records that let teams match trade confirmations to planned payout settlements.

How should teams evaluate provider differences in fees, collateral, and settlement flexibility?

Do not compare providers on headline forward rate alone. Ask what costs apply to terminations, pre-deliveries, and extensions, whether the line is collateralised or uncollateralised, and whether variation margin can apply. Then verify settlement flexibility, including fixed-date versus window settlement across specified dates, against your actual payout workflow.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- assets.publishing.service.gov.uk/media/6425b1da2fa848000cec1078/HMT_FX_Guidan...trusted

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01trusted

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/0...trusted

- cftc.gov/csl/25-10/downloadtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/capital-markets/derivativestrusted

- fdic.gov/news/financial-institution-letters/2021/fil2...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Pitch Instant Payouts to Gig Contractors Without Overpromising

Instant payouts are not a headline feature first. They are a promise about what your payout operation can actually deliver, explain, and recover when something goes wrong. If that promise is vague, any growth upside can be short-lived, and cleanup can land in support, finance, and contractor trust.

How Blockchain and Smart Contracts Will Change Marketplace Payouts by 2030

2030 blockchain narratives can be useful directional context for marketplace payouts, but they are not proof that payout operations, compliance, or reconciliation are solved. The real production question is not chain mechanics alone. It is whether you can run an end-to-end payment flow that Finance, Compliance, and Treasury can actually operate, with regulated money handling, wallet infrastructure, and clear ownership when something fails.

Push Notification Strategy for Payment Platform Payouts

**Payout alerts fail when your message language gets ahead of a verified payout state.** If you want notifications your contractors can trust, optimize for what you can prove in your payout lifecycle. Do not optimize only for send speed or open rate.