Quick Answer

Divide Net Operating Income by the property’s current market value to calculate cap rate. Build NOI from operating income minus recurring property expenses, and keep mortgage principal and interest, owner income taxes, and major projects like a roof replacement outside that figure. Then test vacancy and expense shocks, and compare your result with local comparable sales and market reports before making a buy-or-walk decision.

How to Calculate Cap Rate for a Rental Property: A Professional's Stress-Test Framework#

To calculate cap rate, divide Net Operating Income (NOI) by the property's current market value. That gives you an unlevered view of the asset's earning power, without mixing in loan terms or owner tax position.

| Item | What it is | Key check |

|---|---|---|

| NOI | Total annual income minus annual operating expenses | Use operating statements and keep loan payments, owner income taxes, and major capital work out of NOI |

| Current market value | The value used as the denominator in cap rate | Use a value that reflects the asset today, not an old assumption |

| Cap rate | NOI divided by current market value | Compare properties only when the inputs were built on the same basis |

| Income and expense history | Review 2 to 3 years before forecasting | One unusually light repair year can skew the result |

- Build the unlevered baseline first.

Your first job is to produce two numbers you can defend: a credible NOI and a current market value. If either input is soft, the output is soft. Checkpoint: before you move on, you should be able to point to the operating statements behind NOI and explain why the value you used reflects the asset today, not an old assumption.

- Classify NOI with a hard include and exclude line.

NOI is total income minus total operating expenses, but most errors show up in classification. Treat recurring property costs as operating expenses. Keep financing, owner taxes, and major capital work out of NOI.

| Line item | Correct treatment | Common mistake |

|---|---|---|

| Real estate taxes, insurance, utilities, repairs and maintenance, management fees, payroll, legal and professional fees | Include in operating expenses | Leaving them out to make NOI look stronger |

| Loan payments | Exclude from NOI | Subtracting principal and interest as if debt service were an operating cost |

| Owner income taxes | Exclude from NOI | Treating the owner's tax bill as a property expense |

| Roof replacement or major kitchen renovation | Exclude from NOI as capital expenditure | Running a major project through operating expenses |

| Ordinary repair vs improvement | Ordinary repair and maintenance can sit in operating expenses; improvements must be capitalized under IRC section 263(a) | Calling an improvement "maintenance" to smooth the numbers |

A common failure mode is mixing repairs with improvements. If the cost is really a property improvement, it belongs in capital, not NOI. That is not just a modeling preference. It is a real tax boundary.

- Run the baseline math, then test input quality.

Once classifications are clean, the math is straightforward: NOI = total annual income - annual operating expenses Cap rate = NOI / current market value

A simple variable example looks like this: if annual income is I, operating expenses are E, and current market value is V, then NOI = I - E and cap rate = (I - E) / V.

That gives you a usable screening number only if the inputs were built on the same basis. If you compare one property on actual NOI and another on projected NOI, the comparison is already distorted. In practice, review 2 to 3 years of income and expense history before you forecast anything. One unusually light repair year can skew the result.

That baseline is only the mechanical start. The next step is to rebuild each input from source records and see whether the number survives contact with reality.

If you want a deeper dive, read How to Calculate Your Billable Rate as a Freelancer. If you want a quick next step for "calculate cap rate," try the free invoice generator.

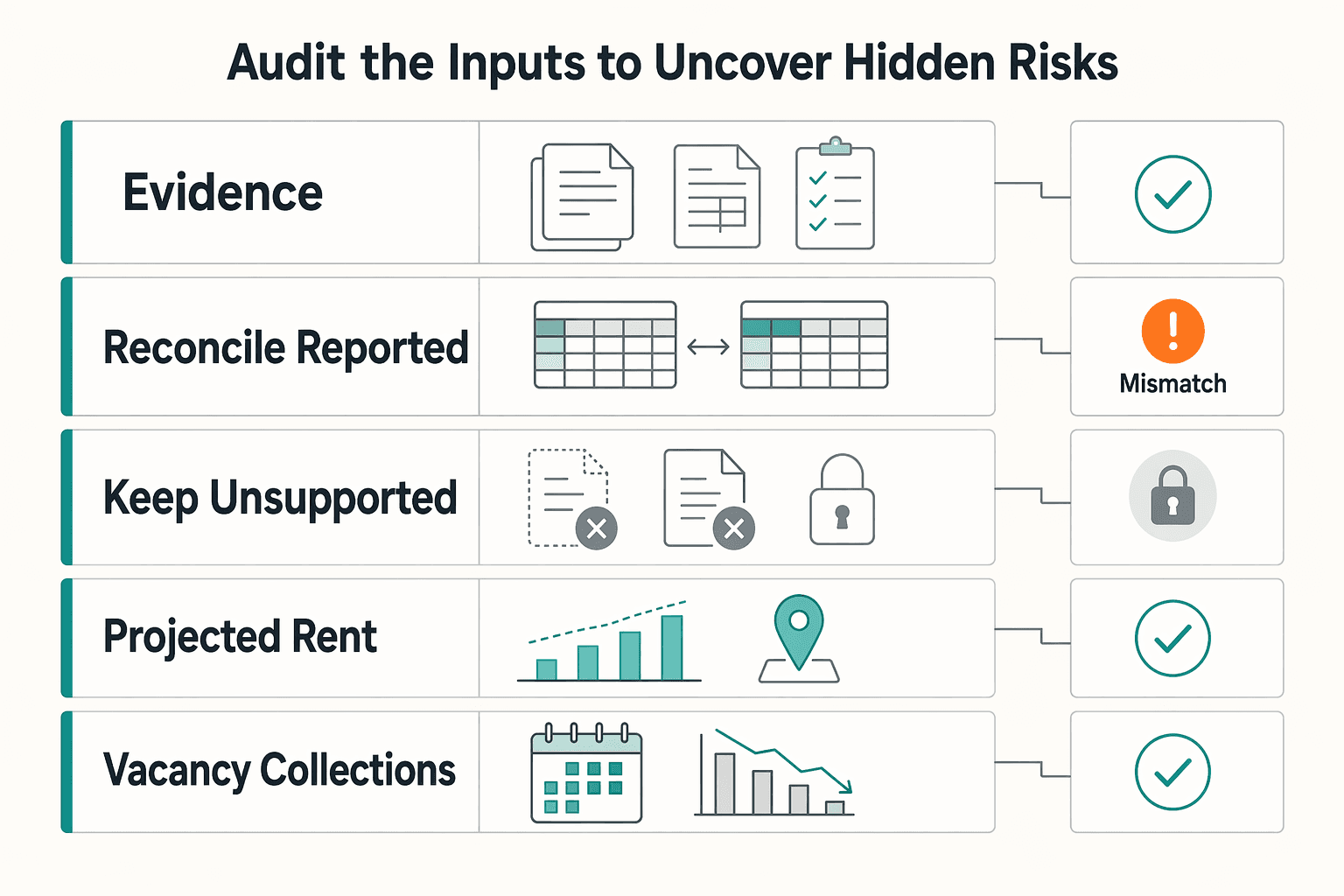

Part 1: Audit the Inputs to Uncover Hidden Risks#

Treat the seller pro forma as a draft, not a decision-ready input. Your goal in this step is to rebuild NOI from verified records and keep an audit trail for every adjustment.

| Audit step | What to do | Output |

|---|---|---|

| Gather core records | Collect operating statements, current rent roll, lease terms, and support for major expense lines | Core records collected in one pass |

| Reconcile reported to verified | Use document support, not verbal assumptions, for each line item | Verified amounts and an adjustment trail |

| Keep unsupported items provisional | Keep unsupported items provisional until they can be traced | Model remains provisional until support is traced |

Start with a simple workflow you can follow in order:

- Gather the core records in one pass: operating statements, current rent roll, lease terms, and support for major expense lines.

- Reconcile each line item from

reportedtoverifiedusing document support, not verbal assumptions. - Keep anything unsupported in a provisional bucket until you can trace it.

For income, separate what is in place now from what is assumed. Keep current leased rent distinct from vacancy/collection loss and other income, so you can see which parts are stable and which are still conditional.

For expenses, use the same structure: reported amount, supporting record, verified amount. If support is incomplete, keep those inputs provisional rather than forcing certainty:

- Current market reserve assumption pending property-market or source-record verification.

- Current management fee range pending provider, contract, property-market, or source-record verification.

| Reported input | Verified input | NOI impact |

|---|---|---|

| Projected rent blended into current revenue | In-place rent supported by current leases, with assumptions separated | Usually lowers or stabilizes current NOI quality |

| Vacancy/collections blended into top-line income | Vacancy and collection loss shown separately from in-place rent | Makes risk visible and often reduces verified NOI |

| Light or missing maintenance/management assumptions | Add reserve and management assumptions only after support is verified | Reduces risk of overstated operating performance |

Do not call this model final until each material adjustment has a traceable reason. Corrections become harder once decisions are already in motion, so finish the audit first, then pressure-test the verified base in Part 2.

For a step-by-step walkthrough, see How to Calculate Depreciation on a Foreign Rental Property.

Part 2: Stress-Test the Model Against Future Shocks#

Do not trust the deal-level cap rate until your verified NOI still holds under stress. Because cap rate is a first-year snapshot, pressure-test the assumptions before you use it for a live decision.

Use the same loop for every scenario: adjust one assumption, recalculate NOI and cap rate (NOI / value), then record a clear pass/fail note with the verification prompt behind the change.

| Scenario | What changes | Primary risk signal | Decision implication |

|---|---|---|---|

| Vacancy shock | Apply a conservative vacancy and collection case after local market check | NOI falls quickly when rent durability weakens | If a market-normalized vacancy case breaks the deal, your pricing or assumptions are too tight |

| Expense shock | Current tax, insurance, and management assumptions pending official, provider, contract, or source-record verification | Returns depend on unusually light reported costs | If it only works with seller-era expenses, underwrite to your ownership cost structure or walk |

| CapEx reality check | Keep NOI method consistent, then test owner cash durability with replacement needs and financing impact | Accounting NOI appears stable, but owner cash becomes fragile | If near-term repairs or debt pressure erase cash durability, the headline cap rate is not decision-ready |

Run the vacancy case with in-place rent unchanged, then document whether your minimum durability threshold still holds. If reported vacancy looks unusually low, test a higher market case after you verify local leasing conditions.

Run the expense case next and challenge taxes, insurance, and management realism directly. Even when a property is currently owner-managed, include a typical management-cost assumption in your stressed view and log what support you used.

Then separate accounting NOI from owner cash durability. Debt service and major CapEx are outside NOI, so use a 2- to 3-year view to track replacement needs, reserve treatment, and financing pressure before calling the deal resilient.

You might also find this useful: Tax Implications for a UK Resident Owning a US LLC.

Part 3: Benchmark Against the Market for Strategic Context#

After your stress tests, your next job is simple: check whether your calculated cap rate is competitive for this asset type, location, and risk profile. There is no universal "good" cap rate, so you need a like-for-like market benchmark before you decide.

| Benchmark step | Source or criteria | What to record or normalize |

|---|---|---|

| Define comp criteria | Same broad asset type, same submarket or competing area, and similar size, condition, and operating profile | Note unusually low expenses or unusually high occupancy before comparing |

| Use market reports | Market reports from a verified period | Record report date, coverage area, asset definition, and verified source-record lookback window |

| Use comparable sales | Recent comparable sales from a verified period | Keep sale date, occupancy context, and obvious condition differences |

| Normalize inputs | Use stabilized NOI with the same cap-rate formula | Reflect a temporary vacancy gap instead of underwriting a full-year income figure as if nothing happened |

| Add macro context | Rate environment and financing conditions | Verify current lender terms and current local market commentary first |

Step 1. Define comp criteria before you look at rates. Set your comparison rules first: same broad asset type, same submarket or competing area, and similar size, condition, and operating profile. If your deal depends on unusually low expenses or unusually high occupancy, note that up front so you do not compare it to stabilized assets without adjustment.

Step 2. Pull two evidence streams. Use both market reports and recent comparable sales from a verified period. Reports help you frame the local cap-rate range and market tone; comps show what buyers paid for similar income streams. Use the report date, coverage area, asset definition, and lookback window only after you verify them from the market report or source record, then keep a comp sheet with sale date, occupancy context, and any obvious condition differences.

Step 3. Normalize to apples-to-apples inputs. For benchmarking, use stabilized NOI (normal occupancy and expense levels), not a single unusually strong or weak year. Keep the formula consistent: cap rate is NOI divided by value or purchase price, and NOI excludes mortgage payments, depreciation, and income taxes. If there was a temporary vacancy gap, reflect it instead of underwriting a full-year income figure as if nothing happened.

Now compare your calculated cap rate to the local range you built from those two sources.

| Observed cap-rate position | Likely risk explanation | Next underwriting action |

|---|---|---|

| Above local range | Market may be pricing in higher perceived risk or weaker income durability | Recheck rent durability, condition risks, and expense assumptions before relying on the upside case |

| In line with local range | Pricing appears broadly consistent with this risk level | Move to final return and financing checks without assuming mispricing |

| Below local range | Price may be rich for the risk, or NOI may be overstated | Rebuild stabilized NOI, challenge price, and proceed only with a verified premium case |

Step 4. Verify macro context before using it. Cap rate is an unlevered comparison tool, but market expectations still shift with rate environment and financing conditions. Use that context only after you verify current lender terms and current local market commentary. If competitiveness depends on outdated conditions, treat that as a warning sign.

Related: How to Invest in Real Estate as a Digital Nomad.

Conclusion: From Calculation to Confident Capital Allocation#

After you clear up the metric questions, keep one rule in front of you: if you can quote a number but cannot defend the source status, you do not have decision-grade evidence yet. Confidence comes from process quality, not from a summary that looked complete on first pass.

-

Verify the source file status. Treat summary pages as a starting point, not a final legal record. For FederalRegister.gov pages, verify against the official edition on govinfo.gov and keep the official PDF you relied on. Your checkpoint is simple: what you cite should reconcile to the official record, not only the prototype view.

-

Pressure-test the failure mode first. Once details reconcile, check what could break your conclusion. A common failure mode is relying on the XML rendition alone, which does not itself carry legal or judicial notice status.

| Decision path | Source authenticity checked | Official edition verified | Notice-status risk |

|---|---|---|---|

| Prototype-only read | No | No | Higher |

| Verification workflow | Yes | Yes (official govinfo PDF) | Lower |

- Choose a decision gate based on evidence quality. Treat the prototype and the official edition as separate checkpoints before final conclusions. Use this closeout checklist:

- Proceed if the FederalRegister.gov content reconciles to the official govinfo edition.

- Recheck if key details are missing, inconsistent, or only visible in one version.

- Pause and escalate if legal reliance is required and official status is not clearly confirmed.

Related reading: Day Rate or Project Rate for Consulting Engagements.

Frequently Asked Questions

Does cap rate include mortgage payments?

No. Cap rate is tied to net operating income and market value, so it ignores financing by design. If the result changes because you changed the loan terms, you are no longer looking at cap rate alone.

What is the difference between cap rate and cash-on-cash return?

Use cap rate to compare properties on an unlevered basis. Use cash-on-cash return to judge what your actual cash investment earns after debt service. If financing is central to your decision, move to How to Calculate Cash-on-Cash Return for Real Estate instead of forcing one metric to do both jobs. | Measure | Best use case | What it includes and excludes | When it can mislead you | | --- | --- | --- | --- | | NOI | Rebuilding the property's operating performance from the ground up | Includes income minus operating expenses; excludes debt service, owner income taxes, and major infrequent capital projects | If you mix actual results with optimistic projections or misclassify repairs vs capital items | | Cap rate | Comparing one property to similar properties in the same market on a one-year yield basis | Uses NOI divided by market value; excludes financing effects | If you compare unlike assets, use mismatched NOI bases, or treat it as a full investment verdict | | Cash-on-cash return | Measuring the annual cash flow on the cash you actually invested | Uses annual cash flow relative to total cash invested and therefore reflects debt service | If attractive financing makes a weak property look stronger than its operations really are |

Is a higher cap rate always better?

No. A higher rate can reflect different risk and property characteristics, including location, condition, and income durability. If a property looks unusually cheap, the next move is not celebration. It is a file review of assumptions, operating history, and property condition.

What should you include and exclude when building NOI?

Use this quick classification check before you underwrite or compare comps: Include in NOI: rent and other operating income, real estate taxes, insurance, utilities, repairs and maintenance, management fees, payroll, and legal or professional service fees tied to operations.. Exclude from NOI: mortgage principal and interest, owner income taxes, and major infrequent capital projects such as a roof replacement or major kitchen renovation. Your verification point is simple: every line item should answer one question. “Is this part of running the property today?” If the answer is no, keep it out of NOI and track it elsewhere.

Can you use projected income instead of actual history?

You can, but only after you separate actual history from your forward view and explain every adjustment. A practical check is to start with 2 to 3 years of income and expense history, then normalize from there. Inconsistent cap-rate methodology can produce aggressive, unsupported valuation outcomes.

How should you stress-test a cap rate?

You do not stress-test the formula itself. You stress-test the NOI underneath it. Rebuild income and expenses using a conservative scenario once the supporting records and market inputs are verified, then recalculate the rate and compare that result to your base case and local comp range.

How does CapEx affect your real return if it is excluded from NOI?

CapEx stays out of NOI because it is not a routine operating expense, but it still affects what you keep. Verify the current reserve assumption from property-market or source records before using it in a separate cash flow view, or a property with a clean reported rate can still disappoint you once the first major project hits.

What is the fastest red flag when you compare your result with market cap rates?

Watch for mismatched inputs. If your property is using pro forma rents or unusually low expenses while the comp set reflects stabilized or actual operations, the comparison is not apples to apples. The quoted rate may overstate value.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/bcbs128b.pdftrusted

- cookcountyassessoril.gov/assessors-cap-rate-policytrusted

- federalregister.gov/documents/2025/01/16/2025-00592/securing-the...trusted

- federalregister.gov/documents/2014/01/07/2013-29627/introduction...trusted

- federalreserve.gov/publications/2025-stress-test-scenarios.htmtrusted

- gao.gov/assets/gao-24-107282.pdftrusted

- govinfo.gov/content/pkg/GPO-UA-2001-12-03/html/GPO-UA-20...trusted

- in.gov/dlgf/files/2025-level-i-and-ii-certification...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Calculate a Freelance Rate You Can Actually Get Paid On

A workable rate is not the neat number a calculator produces. It is the number that still works after you account for real billable capacity, non-client time, scope drift, and the gap between sending an invoice and receiving cleared cash. Start with hourly math even if you do not plan to bill hourly, then turn that number into a quote with clear `payment terms`.

How to Invest in Real Estate as a Digital Nomad

**Run anything with money and moving parts like an operations system (cash, docs, delegation, and controls), not a "passive income" vibe.** Real life stress-tests weak spots. You change time zones, a client pays late, and something breaks at the worst moment. As the CEO of a business-of-one, your job is to build a setup that keeps working when you are not available on demand.

Tax Implications for a UK Resident Owning a US LLC

When people search **uk resident owning us llc tax**, they often start with the wrong question. You do not win by chasing a clever position. You win by running a compliant system that can handle the way the US and UK classify LLC income differently, with records you can defend.